Valuation Spotlight: Is that Really Worth That?

|

|

|

- Moris Watts

- 5 years ago

- Views:

Transcription

1 Valuation Spotlight: Is that Really Worth That? Panelist: Panelist: Panelist: HUD/ORCF: Moderator: JP LoMonaco, MAI Valuation & Information Group Colleen Blumenthal, MAI HealthTrust Michael Baldwin, MAI, ASA OHC Advisors Wayne Harris Jenifer Williams Berkadia HMAC ANNUAL CONFERENCE October 25-26, 2018

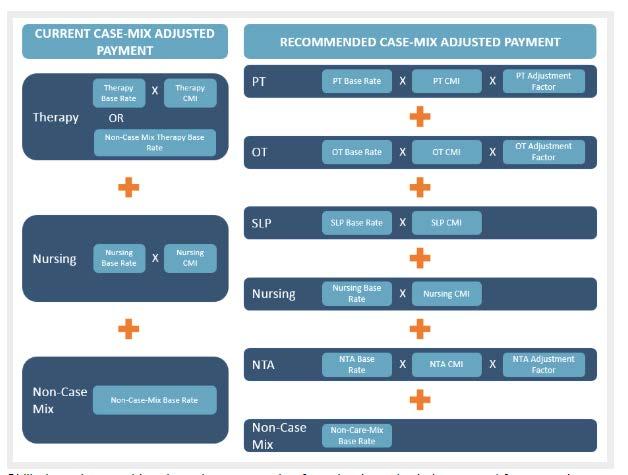

2 Medicare PDPM Implementation RCS1 to be replaced with patient driven payment model or PDPM as of 10/1/2019 Goals - CMS describes three goals for the new reimbursement system: (1) more accurately compensating SNFs; (2) reducing incentives for SNFs to deliver therapy based on financial considerations, rather than resident need; and (3) maintaining simplicity, to the extent possible

3 Medicare PDPM Implementation

4 Medicare PDPM Implementation Structure shift Current System Resource Utilization Groups (RUG-IV) Two components Case-mix A patient s RUG is based on the higher of two case mix components (Nursing and Therapy). More than 90% of patients assigned rehab based RUGs. Non case-mix board and various capital costs Proposed System - Patient Driven Payment Model or PDPM Five Components Physical Therapy Occupational Therapy Speech Therapy Nursing Non-Therapy Ancillary Services NTAS

5 Medicare PDPM Implementation Conclusions 1. Funding neutral 2. Eliminates rehabilitation minutes 3. Allows for concurrent therapy 4. Assessment based on Hospital DRG and changes to assessments are more limited 5. Providers with adequate resources will adapt and are generally in favor of the new system

6 Potential Changes to Appraisal Dates Chapter 5.3B states: The effective date of the value estimate should be the date that the designated appraiser inspected the subject property. The date of valuation may not be a future date. However, often by the time the appraisal is being reviewed, the financials analyzed in the report are over six months old, resulting in many requests to appraisers to update the financials in the report.

7 Potential Changes to Appraisal Dates Pros Cons - Saves time and money - Changes may have occurred at the property - Market conditions could be different with - Allows appraisal and underwriting to be new supply, closing of a primary economic more in sync producer, etc. - Appraiser can customize scope of work to what adds value UPDATING WITHOUT REINSPECTING - Concerns exist already when the date of the report is months removed from the date of value

8 Potential Changes to Appraisal Dates There is no consensus. ORCF will be open to inspection and date of value waiver requests. Appraisers will have to assess the scope of work needed to minimize liability and update the report.

9 Corporate Adjustments The income approach premise that value equals the present worth of future benefits means: Owner-specific income and expenses should not be modeled in cash flow projections, such as owner distributions, interest, etc. Projected cash flow should reflect market-supported assumptions. Historical statements are not to be adjusted to market. Please do not modify the Standardized HUD tables/decision Circuit to show the adjusted history. If for discussion purposes you want to show how the adjusted history would look, do it below the standard tables. The adjustments should not be applied to the NOI used to calculate the Debt Service Coverage. Ultimately, keep adjustments transparent.

10 Corporate Expense Adjustments Transparent, But Inappropriate: SUMMARY OF SUBJECT'S ADJUSTED FINANCIAL STATEMENTS Year TTM August 2018 YE 2017 YE 2016 YE 2015 Total $ $/Unit $/RD % EGI Total $ $/Unit $/RD % EGI Total $ $/Unit $/RD % EGI Total $ $/Unit $/RD % EGI Total Effective Gross Revenue $10,884,080 $120,934 $ % $10,475,990 $116,400 $ % $9,490,925 $105,455 $ % $9,128,065 $101,423 $ % Expenses Real Estate Taxes $39,088 $434 $ % $42,359 $471 $ % $38,038 $423 $ % $68,120 $757 $ % Insurance $300,389 $3,338 $ % $306,966 $3,411 $ % $317,766 $3,531 $ % $314,261 $3,492 $ % Utilities $134,312 $1,492 $ % $131,567 $1,462 $ % $135,831 $1,509 $ % $128,459 $1,427 $ % Maintenance $161,940 $1,799 $ % $143,656 $1,596 $ % $144,602 $1,607 $ % $157,381 $1,749 $ % Administrative/General $1,109,070 $12,323 $ % $1,046,048 $11,623 $ % $812,898 $9,032 $ % $1,029,955 $11,444 $ % Housekeeping/Laundry $335,838 $3,732 $ % $332,984 $3,700 $ % $311,455 $3,461 $ % $308,548 $3,428 $ % Dietary $652,999 $7,256 $ % $647,521 $7,195 $ % $636,995 $7,078 $ % $689,638 $7,663 $ % Nursing/Personal Care $4,145,523 $46,061 $ % $3,993,308 $44,370 $ % $3,932,229 $43,691 $ % $3,901,314 $43,348 $ % Activities/Social $316,869 $3,521 $ % $309,554 $3,439 $ % $248,011 $2,756 $ % $248,311 $2,759 $ % Other Payroll, Payroll Taxes and Benefits $852,108 $9,468 $ % $776,779 $8,631 $ % $917,244 $10,192 $ % $1,044,847 $11,609 $ % Total Operating Expenses $8,048,136 $89,424 $ % $7,730,740 $85,897 $ % $7,495,070 $83,279 $ % $7,890,833 $87,676 $ % Net Operating Income Before Adjustments $2,835,944 $31,510 $ % $2,745,250 $30,503 $ % $1,995,855 $22,176 $ % $1,237,231 $13,747 $ % Plus Excess Insurance $200,000 $0 $ % $200,000 $2,222 $ % $200,000 $2,222 $ % $200,000 $2,222 $ % Plus Actual Management Fee $0 $0 $ % $586,550 $6,517 $ % $477,217 $5,302 $ % $459,416 $5,105 $ % Less Market Management Fee $544,204 $6,047 $ % $523,800 $5,820 $ % $474,546 $5,273 $ % $456,403 $5,071 $ % Less Reserve for Replacement $45,000 $500 $ % $45,000 $500 $ % $45,000 $500 $ % $45,000 $500 $ % Adjusted Net Operating Income (EBITDAR) $2,446,740 $27,186 $ % $2,963,000 $32,922 $ % $2,153,526 $23,928 $ % $1,395,244 $15,503 $ %

11 Corporate Expense Adjustments Transparent and Appropriate: SUMMARY OF SUBJECT'S ADJUSTED FINANCIAL STATEMENTS Note Year TTM August 2018 YE 2017 YE 2016 YE 2015 Total $ $/Unit $/RD % EGI Total $ $/Unit $/RD % EGI Total $ $/Unit $/RD % EGI Total $ $/Unit $/RD % EGI Total Effective Gross Revenue $10,884,080 $120,934 $ % $10,475,990 $116,400 $ % $9,490,925 $105,455 $ % $9,128,065 $101,423 $ % Expenses Real Estate Taxes $39,088 $434 $ % $42,359 $471 $ % $38,038 $423 $ % $68,120 $757 $ % (1) Insurance $300,389 $3,338 $ % $306,966 $3,411 $ % $317,766 $3,531 $ % $314,261 $3,492 $ % Utilities $134,312 $1,492 $ % $131,567 $1,462 $ % $135,831 $1,509 $ % $128,459 $1,427 $ % Maintenance $161,940 $1,799 $ % $143,656 $1,596 $ % $144,602 $1,607 $ % $157,381 $1,749 $ % Administrative/General $1,109,070 $12,323 $ % $1,046,048 $11,623 $ % $812,898 $9,032 $ % $1,029,955 $11,444 $ % Housekeeping/Laundry $335,838 $3,732 $ % $332,984 $3,700 $ % $311,455 $3,461 $ % $308,548 $3,428 $ % Dietary $652,999 $7,256 $ % $647,521 $7,195 $ % $636,995 $7,078 $ % $689,638 $7,663 $ % Nursing/Personal Care $4,145,523 $46,061 $ % $3,993,308 $44,370 $ % $3,932,229 $43,691 $ % $3,901,314 $43,348 $ % Activities/Social $316,869 $3,521 $ % $309,554 $3,439 $ % $248,011 $2,756 $ % $248,311 $2,759 $ % Other Payroll, Payroll Taxes and Benefits $852,108 $9,468 $ % $776,779 $8,631 $ % $917,244 $10,192 $ % $1,044,847 $11,609 $ % Total Operating Expenses $8,048,136 $89,424 $ % $7,730,740 $85,897 $ % $7,495,070 $83,279 $ % $7,890,833 $87,676 $ % Net Operating Income Before Adjustments $2,835,944 $31,510 $ % $2,745,250 $30,503 $ % $1,995,855 $22,176 $ % $1,237,231 $13,747 $ % 2 Plus Actual Management Fee $0 $0 $ % $586,550 $6,517 $ % $477,217 $5,302 $ % $459,416 $5,105 $ % Less Market Management Fee $544,204 $6,047 $ % $523,800 $5,820 $ % $474,546 $5,273 $ % $456,403 $5,071 $ % Less Reserve for Replacement $45,000 $500 $ % $45,000 $500 $ % $45,000 $500 $ % $45,000 $500 $ % Adjusted Net Operating Income (EBITDAR) $2,246,740 $24,964 $ % $2,763,000 $30,700 $ % $1,953,526 $21,706 $ % $1,195,244 $13,280 $ % Note Line Item (1) Insurance Historical Periods reflect above-market insurance expense (2) Plus Actual Management Fee Includes Corporate Overhead Charged plus Owner's Salary

12 Corporate Income Adjustments If a profit center, therapy for example, is handled by a separate entity, and would not show up on the facility's income and expense statement, we have been allowing an adjustment to add the profit from that activity to be included in the appraiser's NOI conclusion. We don't want to see this adjustment applied to small facilities, where due to the economies of scale, the highest and best use would be to contract out those services. Because of the difficulty of disentangling income and expenses at the corporate level, we will also require market evidence of the profits adjustments in addition to that profit center s income and expense reports.

13 As-Is vs. Stabilized Values Most HUD appraisals are of stabilized facilities What if the appraiser determines the property is not stabilized or has upside? Handbook: do not consider significant physical or operational changes However, changes are OK if a buyer could immediately implement them Must account for impact on value associated with reaching stabilization Not-for-profit valuations Recent, short-term declines in occupancy / census Above-market expenses

14 As-Is vs. Stabilized Values Length of time needed to reach the stabilization Risk of achieving stabilization DCF appropriate? Cap rate selection What if it were already stable? Low risk / quick timeframe High risk / long timeframe

15 Cost Approach Concerns Section 232 Handbook, Section II, Production, Chapter 5.3.R.2. ORCF will expect to see a fully developed cost approach in cases where there is little depreciation or in cases where the undepreciated replacement cost new would be expected to be lower than the conclusions of the Sales Comparison or Income Capitalization Approaches. For that reason, base costs of new facilities will need to be carefully discussed in the narrative justification for excluding the approach. ORCF underwriters need to give Loan Committee an explanation when there is a disconnect between the concluded value and the cost to build new. This discussion will need to include a discussion of the market and the likelihood of competition being built.

16 Cost Approach Concerns In cases where you are allowed to exclude the cost approach, it is acceptable to apply a simple test showing the concluded value doesn t exceed the cost to build and reach stabilized occupancy. ORCF doesn t dictate the method of the test. The appraiser sets the scope, which should expand and contract depending on how clear the case is.

17 Cost Approach Concerns The scope may or may not need to include a full land valuation. The scope may or may not need to include an analysis of intangibles Analyzing cost comparables is a good tool to help you decide the scope. Example: The preceding construction budgets from recently built or proposed SNFs range from $175,911 to $279,804 per licensed bed. Our subject value conclusion at $63,000 per licensed bed is significantly below the undepreciated replacement cost new comps, so there is a low possibility that a competitor may be added to the market based on financial feasibility. In this case a fully developed Undepreciated Cost Approach or land value would not be needed.

18

BUSI 330 Suggested Answers to Review and Discussion Questions: Lesson 10

BUSI 330 Suggested Answers to Review and Discussion Questions: Lesson 10 1. The client should give you a copy of their income and expense statements for the last 3 years showing their rental income by

BUSI 330 Suggested Answers to Review and Discussion Questions: Lesson 10 1. The client should give you a copy of their income and expense statements for the last 3 years showing their rental income by

Basics of Commercial Real Estate Transactions Day Two

Basics of Commercial Real Estate Transactions Day Two John Rockwell, Partner Energy October 12, 2016 PG&E refers to the Pacific Gas and Electric Company, a subsidiary of PG&E Corporation. 2010 Pacific

Basics of Commercial Real Estate Transactions Day Two John Rockwell, Partner Energy October 12, 2016 PG&E refers to the Pacific Gas and Electric Company, a subsidiary of PG&E Corporation. 2010 Pacific

2016 MAP Guidelines: Presentation Title Chapter 7 Issues

2016 MAP Guidelines: Presentation Title Chapter 7 Issues Your companyinformation National Council of Housing Market Analysts Baltimore, MD April 19, 2016 Agenda MAP Market Study Guidelines Robert Lefenfeld

2016 MAP Guidelines: Presentation Title Chapter 7 Issues Your companyinformation National Council of Housing Market Analysts Baltimore, MD April 19, 2016 Agenda MAP Market Study Guidelines Robert Lefenfeld

Getting More Value for Your Practice

Getting More Value for Your Practice D A N I E L M. B E R N I C K, E S QUI R E, M B A T H E H E A LT H C A R E GROUP P LY M OUT H M E E T I N G, PA W W W. H E A LT H C A R E G R O U P. C O M Who We Are

Getting More Value for Your Practice D A N I E L M. B E R N I C K, E S QUI R E, M B A T H E H E A LT H C A R E GROUP P LY M OUT H M E E T I N G, PA W W W. H E A LT H C A R E G R O U P. C O M Who We Are

Guide to Appraisal Reports

Guide to Appraisal Reports What is an appraisal? An appraisal is an independent valuation of real property prepared by a qualified Appraiser and fully documented in a report. Based on a series of appraisal

Guide to Appraisal Reports What is an appraisal? An appraisal is an independent valuation of real property prepared by a qualified Appraiser and fully documented in a report. Based on a series of appraisal

Benchmarking Your CCRC

Benchmarking Your CCRC Presented by: Moore Stephens Lovelace, P.A. Objectives Provide information on how ratios can provide insight into financial statements Give information about key ratios and what

Benchmarking Your CCRC Presented by: Moore Stephens Lovelace, P.A. Objectives Provide information on how ratios can provide insight into financial statements Give information about key ratios and what

Atascadero Community Redevelopment Agency Staff Report Executive Director

ITEM NUMBER: RA C - 1 DATE: 12/08/09 Initially brought before the Board on 11/10/09 Atascadero Community Redevelopment Agency Staff Report Executive Director Business Stimulus Program: Loan Program for

ITEM NUMBER: RA C - 1 DATE: 12/08/09 Initially brought before the Board on 11/10/09 Atascadero Community Redevelopment Agency Staff Report Executive Director Business Stimulus Program: Loan Program for

ILLINOIS HOUSING DEVELOPMENT AUTHORITY APPRAISAL SCOPE AND GUIDELINES December 2015

ILLINOIS HOUSING DEVELOPMENT AUTHORITY APPRAISAL SCOPE AND GUIDELINES December 2015 As part of the Common Application for Multifamily Financing, the Illinois Housing Development Authority (IHDA) requires

ILLINOIS HOUSING DEVELOPMENT AUTHORITY APPRAISAL SCOPE AND GUIDELINES December 2015 As part of the Common Application for Multifamily Financing, the Illinois Housing Development Authority (IHDA) requires

Selling Your Ophthalmology Practice. Financial Interest Disclosure 5/2/2016. Mark E. Kropiewnicki, Esquire, LLM* Daniel M. Bernick, Esquire, MBA*

Selling Your Ophthalmology Practice Mark E. Kropiewnicki, Esquire, LLM* Daniel M. Bernick, Esquire, MBA* The Health Care Group Plymouth Meeting, PA www.healthcaregroup.com * Financial Interest Financial

Selling Your Ophthalmology Practice Mark E. Kropiewnicki, Esquire, LLM* Daniel M. Bernick, Esquire, MBA* The Health Care Group Plymouth Meeting, PA www.healthcaregroup.com * Financial Interest Financial

Practice Valuations. Welcome To The Digital Learning Center. Today s Presentation. Course Faculty. Presented by. What s Your Practice Worth?

Welcome To The Digital Learning Center Presented by Your Partner In Building High Performance Practices Today s Presentation Practice Valuations What s Your Practice Worth? Course Faculty R. Thomas (Tom)

Welcome To The Digital Learning Center Presented by Your Partner In Building High Performance Practices Today s Presentation Practice Valuations What s Your Practice Worth? Course Faculty R. Thomas (Tom)

Cap Rate Trends, Methodology and Analysis. Dane R. Anderson MAI, CCIM Appraisal & Litigation Services Director

Cap Rate Trends, Methodology and Analysis Dane R. Anderson MAI, CCIM Appraisal & Litigation Services Director 1 Quickly The Income Approach Basis of the Approach Present worth of future benefits Two Methods:

Cap Rate Trends, Methodology and Analysis Dane R. Anderson MAI, CCIM Appraisal & Litigation Services Director 1 Quickly The Income Approach Basis of the Approach Present worth of future benefits Two Methods:

Broker. Basic Business Appraisal. Chapter 9. Copyright Gold Coast Schools 1

Broker Chapter 9 Basic Business Appraisal 1 Learning Objectives Describe the characteristics of the legal entities a business appraiser may encounter List at least 5 reasons for a business appraisal List

Broker Chapter 9 Basic Business Appraisal 1 Learning Objectives Describe the characteristics of the legal entities a business appraiser may encounter List at least 5 reasons for a business appraisal List

Special Purpose Properties. Special Valuation Considerations

Special Purpose Properties Special Valuation Considerations 2017 Case Study in Ottawa: New Automobile Dealership Many brand-specific specialties Cost: $4,000,000 (including land and a developer fee) Sales

Special Purpose Properties Special Valuation Considerations 2017 Case Study in Ottawa: New Automobile Dealership Many brand-specific specialties Cost: $4,000,000 (including land and a developer fee) Sales

The Uniform Act. Acquisition, Relocation & Demolition. Disaster Recovery CDBG Administration Training. February 14, 2012

The Uniform Act Acquisition, Relocation & Demolition Disaster Recovery CDBG Administration Training February 14, 2012 Uniform Act Overview 49 CFR 24 Protections and assistance to establish minimum standards

The Uniform Act Acquisition, Relocation & Demolition Disaster Recovery CDBG Administration Training February 14, 2012 Uniform Act Overview 49 CFR 24 Protections and assistance to establish minimum standards

VHDA Low Income Housing Tax Credit Manual Version: K. Appraisal Guidelines

VHDA Low Income Housing Tax Credit Manual Version: 2018.1 K. Appraisal Guidelines VHDA LIHTC Program Page 119 Last Modified: 11/30/2017 Appraisal Information Appraisals are required to be submitted with

VHDA Low Income Housing Tax Credit Manual Version: 2018.1 K. Appraisal Guidelines VHDA LIHTC Program Page 119 Last Modified: 11/30/2017 Appraisal Information Appraisals are required to be submitted with

Real Estate Appraisal

Market Value Chapter 17 Real Estate Appraisal This presentation includes materials from Ling and Archer, 4 th edition, Real Estate Principles The highest price a property will bring if: Payment is made

Market Value Chapter 17 Real Estate Appraisal This presentation includes materials from Ling and Archer, 4 th edition, Real Estate Principles The highest price a property will bring if: Payment is made

HUD RAD (Rental Assistance Demonstration) Overview

Overview") HUD RAD (Rental Assistance Demonstration) Overview Who is? Company formed in 1991 Headquartered in Bedford, N.H. with 5 offices nationwide, family owned Approved We have recapitalized to finance Apartment,

HUD RAD (Rental Assistance Demonstration) Overview Who is? Company formed in 1991 Headquartered in Bedford, N.H. with 5 offices nationwide, family owned Approved We have recapitalized to finance Apartment,

How to Read a Real Estate Appraisal Report

How to Read a Real Estate Appraisal Report Much of the private, corporate and public wealth of the world consists of real estate. The magnitude of this fundamental resource creates a need for informed

How to Read a Real Estate Appraisal Report Much of the private, corporate and public wealth of the world consists of real estate. The magnitude of this fundamental resource creates a need for informed

Typical Valuation Approaches and How to Deal With Them

Typical Valuation Approaches and How to Deal With Them January, 2018 Anthony F. DellaPelle, Esq., CRE Shareholder, McKirdy, Riskin, Olson & DellaPelle, P.C. Morristown, New Jersey Christian F. Torgrimson,

Typical Valuation Approaches and How to Deal With Them January, 2018 Anthony F. DellaPelle, Esq., CRE Shareholder, McKirdy, Riskin, Olson & DellaPelle, P.C. Morristown, New Jersey Christian F. Torgrimson,

Valuation Issues. Lindsey Sutton Novogradac & Company LLP. Brad Weinberg Novogradac & Company LLP

Valuation Issues PANELISTS Lindsey Sutton Novogradac & Company LLP Brad Weinberg Novogradac & Company LLP Visit www.crowdmics.online/novocolihtc to send questions to the moderator Valuation Issues How

Valuation Issues PANELISTS Lindsey Sutton Novogradac & Company LLP Brad Weinberg Novogradac & Company LLP Visit www.crowdmics.online/novocolihtc to send questions to the moderator Valuation Issues How

NSP Project Feasibility Analysis Template: Instruction Manual

NSP Project Feasibility Analysis Template: Instruction Manual About this Tool Description: This tool provides tab-by-tab instructions for using the NSP Project Feasibility Analysis Template, a workbook

NSP Project Feasibility Analysis Template: Instruction Manual About this Tool Description: This tool provides tab-by-tab instructions for using the NSP Project Feasibility Analysis Template, a workbook

International Valuation Congress Consulting and Valuation to Hotel and Resort Industry Clients

International Valuation Congress Consulting and Valuation to Hotel and Resort Industry Clients Peggy Berg, ISHC, CPA The Highland Group www.highland-group.net Peggy Berg ISHC CPA President, The Highland

International Valuation Congress Consulting and Valuation to Hotel and Resort Industry Clients Peggy Berg, ISHC, CPA The Highland Group www.highland-group.net Peggy Berg ISHC CPA President, The Highland

Preface Who Should Read This Book 3 Organization and Content 4 Acknowledgments 5 Contacting the Author 5 About the Author 6

Preface.................................................................... 3 Who Should Read This Book 3 Organization and Content 4 Acknowledgments 5 Contacting the Author 5 About the Author 6...........................................................

Preface.................................................................... 3 Who Should Read This Book 3 Organization and Content 4 Acknowledgments 5 Contacting the Author 5 About the Author 6...........................................................

Risk Management Insights

Risk Management Insights Appraisal Review Part II: Income Capitalization Approach George Mann, Managing Director and Chief Appraiser, Collateral Evaluation Services, Inc.and Nikki Griffith, MAI, CCIM,

Risk Management Insights Appraisal Review Part II: Income Capitalization Approach George Mann, Managing Director and Chief Appraiser, Collateral Evaluation Services, Inc.and Nikki Griffith, MAI, CCIM,

FASB s 2013 Proposal on Accounting for Leases

FASB s 2013 Proposal on Accounting for Leases Frequently Asked Questions September 2013 The project on lease accounting is a joint project of the FASB and the International Accounting Standards Board.

FASB s 2013 Proposal on Accounting for Leases Frequently Asked Questions September 2013 The project on lease accounting is a joint project of the FASB and the International Accounting Standards Board.

UNIFIED FUNDING 2017 QUESTIONS AND ANSWERS

UNIFIED FUNDING 2017 QUESTIONS AND ANSWERS Project Financing: Q1: Are HDC bond financed projects eligible for other sources besides HWF if they are not applied for in conjunction with HWF? Is HWF the sole

UNIFIED FUNDING 2017 QUESTIONS AND ANSWERS Project Financing: Q1: Are HDC bond financed projects eligible for other sources besides HWF if they are not applied for in conjunction with HWF? Is HWF the sole

NYS HOME Local Program Small Rental Development Initiative Pro forma Budget Workbook Instructions

NYS HOME Local Program Small Rental Development Initiative Pro forma Budget Workbook Instructions I. Overview This Excel Workbook consists of 6 worksheets: 1) Project Summary 2) HOME Limits 3) Units &

NYS HOME Local Program Small Rental Development Initiative Pro forma Budget Workbook Instructions I. Overview This Excel Workbook consists of 6 worksheets: 1) Project Summary 2) HOME Limits 3) Units &

EXHIBIT E LOW INCOME HOUSING TAX CREDIT APPLICATION REQUIREMENTS

EXHIBIT E LOW INCOME HOUSING TAX CREDIT APPLICATION REQUIREMENTS A. Application for Tax Credit Reservation or Tax-Exempt Bond Conditional Commitment shall Include: 1. Complete application form (current

EXHIBIT E LOW INCOME HOUSING TAX CREDIT APPLICATION REQUIREMENTS A. Application for Tax Credit Reservation or Tax-Exempt Bond Conditional Commitment shall Include: 1. Complete application form (current

Conceptualizing Fair Market Value in Compensation Arrangements

Conceptualizing Fair Market Value in Compensation Arrangements Health Care Compliance Association Physician Practice Compliance Conference San Francisco, California September 9, 2005 Gregory D. Anderson,

Conceptualizing Fair Market Value in Compensation Arrangements Health Care Compliance Association Physician Practice Compliance Conference San Francisco, California September 9, 2005 Gregory D. Anderson,

METHODOLOGY GUIDE VALUING LONG-TERM CARE HOMES IN ONTARIO. Valuation Date: January 1, 2016

METHODOLOGY GUIDE VALUING LONG-TERM CARE HOMES IN ONTARIO Valuation Date: January 1, 2016 AUGUST 2016 August 22, 2016 The Municipal Property Assessment Corporation (MPAC) is responsible for accurately

METHODOLOGY GUIDE VALUING LONG-TERM CARE HOMES IN ONTARIO Valuation Date: January 1, 2016 AUGUST 2016 August 22, 2016 The Municipal Property Assessment Corporation (MPAC) is responsible for accurately

The Uniform Act. CDBG Disaster Recovery Regional Training Acquisition Rehabilitation Demolition Displacement August 2015

The Uniform Act CDBG Disaster Recovery Regional Training Acquisition Rehabilitation Demolition Displacement August 2015 Introductions Minnesota Wisconsin Illinois Indiana Michigan - Ohio Maureen Thurman,

The Uniform Act CDBG Disaster Recovery Regional Training Acquisition Rehabilitation Demolition Displacement August 2015 Introductions Minnesota Wisconsin Illinois Indiana Michigan - Ohio Maureen Thurman,

Ashland Transit Triangle:

Ashland Transit Triangle: Strategic Approach to Implementation Fregonese Associates Inc. 12/19/16 Phase I of the Transit Triangle Study Conducted in the Fall of 2015 Tasks Completed: Market analysis Initial

Ashland Transit Triangle: Strategic Approach to Implementation Fregonese Associates Inc. 12/19/16 Phase I of the Transit Triangle Study Conducted in the Fall of 2015 Tasks Completed: Market analysis Initial

2015 Appraisal Guidelines

2015 Appraisal Guidelines Pursuant to Section 13 VAC 10-180-60 of the QAP, appraisals are required for all acquisition, acquisition/rehab and adaptive reuse developments, where the applicant is seeking

2015 Appraisal Guidelines Pursuant to Section 13 VAC 10-180-60 of the QAP, appraisals are required for all acquisition, acquisition/rehab and adaptive reuse developments, where the applicant is seeking

NEW HAMPSHIRE HOUSING FINANCE AUTHORITY AFFORDABLE HOUSING FUND PROGRAM RULES HFA 113

NEW HAMPSHIRE HOUSING FINANCE AUTHORITY AFFORDABLE HOUSING FUND PROGRAM RULES HFA 113 Table of Contents HFA 113 PART ONE: Overview, Purpose, Applicability HFA 113.01 Overview and Purpose HFA 113.02 Applicability

NEW HAMPSHIRE HOUSING FINANCE AUTHORITY AFFORDABLE HOUSING FUND PROGRAM RULES HFA 113 Table of Contents HFA 113 PART ONE: Overview, Purpose, Applicability HFA 113.01 Overview and Purpose HFA 113.02 Applicability

HOTEL CAPITALIZATION RATES AND THE IMPACT OF CAP EX

JANUARY 2014 PRICE $500 HOTEL CAPITALIZATION RATES AND THE IMPACT OF CAP EX Author Suzanne R. Mellen, MAI, CRE, ISHC, FRICS Senior Managing Director www.hvs.com HVS San Francisco 100 Bush Street, Suite

JANUARY 2014 PRICE $500 HOTEL CAPITALIZATION RATES AND THE IMPACT OF CAP EX Author Suzanne R. Mellen, MAI, CRE, ISHC, FRICS Senior Managing Director www.hvs.com HVS San Francisco 100 Bush Street, Suite

Rental Assistance Demonstration (RAD) 101: Public Housing Conversions. US Department of Housing & Urban Development May 14, 2018

101: Public Housing Conversions. US Department of Housing & Urban Development May 14, 2018") Rental Assistance Demonstration (RAD) 101: Public Housing Conversions US Department of Housing & Urban Development May 14, 2018 BACKGROUND 2 Why RAD for Public Housing? RAD was designed to help address

Rental Assistance Demonstration (RAD) 101: Public Housing Conversions US Department of Housing & Urban Development May 14, 2018 BACKGROUND 2 Why RAD for Public Housing? RAD was designed to help address

Chapter 8. How much would you pay today for... The Income Approach to Appraisal

How much would you pay today for... Chapter 8 One hundred dollars paid with certainty each year for five years, starting one year from now. Why would you pay less than $500 Valuation Using the Income Approach

How much would you pay today for... Chapter 8 One hundred dollars paid with certainty each year for five years, starting one year from now. Why would you pay less than $500 Valuation Using the Income Approach

Always Accurate, Always on Time

Always Accurate, Always on Time U.S. Small Business Administration (SBA) Recent Changes to Standards of Operating Procedures (SOP) Qualified Appraiser and Remaining Economic Life June, 2015 Retail Petroleum

Always Accurate, Always on Time U.S. Small Business Administration (SBA) Recent Changes to Standards of Operating Procedures (SOP) Qualified Appraiser and Remaining Economic Life June, 2015 Retail Petroleum

concepts and techniques

concepts and techniques S a m p l e Timed Outline Topic Area DAY 1 Reference(s) Learning Objective The student will learn Teaching Method Time Segment (Minutes) Chapter 1: Introduction to Sales Comparison

concepts and techniques S a m p l e Timed Outline Topic Area DAY 1 Reference(s) Learning Objective The student will learn Teaching Method Time Segment (Minutes) Chapter 1: Introduction to Sales Comparison

Professional Certification Programs

Professional Certification Programs Participants in NDC training, including staff members of Housing and Economic Development Networks, State and Local Governments, Community Development Banks and Charitable

Professional Certification Programs Participants in NDC training, including staff members of Housing and Economic Development Networks, State and Local Governments, Community Development Banks and Charitable

Accounting and Auditing Update. Tennessee Chapter of hfma Spring Institute 2016 Presented by William C. Matheney FHFMA CPA and Meredith P.

Accounting and Auditing Update Tennessee Chapter of hfma Spring Institute 2016 Presented by William C. Matheney FHFMA CPA and Meredith P. Cate Today s Objectives Present an overview of pertinent recently

Accounting and Auditing Update Tennessee Chapter of hfma Spring Institute 2016 Presented by William C. Matheney FHFMA CPA and Meredith P. Cate Today s Objectives Present an overview of pertinent recently

will not unbalance the ratio of debt to equity.

paragraph 2-12-3. c.) and prime commercial paper. All these restrictions are designed to assure that debt proceeds (including Title VII funds disbursed from escrow), equity contributions and operating

paragraph 2-12-3. c.) and prime commercial paper. All these restrictions are designed to assure that debt proceeds (including Title VII funds disbursed from escrow), equity contributions and operating

Contract-Related Intangible

Income Tax Insights Valuation of Contract-Related Intangible Assets Robert F. Reilly, CPA The valuation of contract-related intangible assets is often an issue in matters related to income tax, gift tax,

Income Tax Insights Valuation of Contract-Related Intangible Assets Robert F. Reilly, CPA The valuation of contract-related intangible assets is often an issue in matters related to income tax, gift tax,

Exit Strategies for a Medical Practice

Exit Strategies for a Medical Practice John D. Colucci, Esq., CPA McLane Middleton, PA Jonathan P. Gorski, CPA, MBA Edelstein & Company LLP June 12, 2018 Introduction John D. Colucci, a director at McLane

Exit Strategies for a Medical Practice John D. Colucci, Esq., CPA McLane Middleton, PA Jonathan P. Gorski, CPA, MBA Edelstein & Company LLP June 12, 2018 Introduction John D. Colucci, a director at McLane

NON-GAAP FINANCIAL MEASURES

NON-GAAP FINANCIAL MEASURES Welltower Inc. (HCN) believes that revenues, net operating income from continuing operations (NOICO), net income and net income attributable to common stockholders (NICS), as

NON-GAAP FINANCIAL MEASURES Welltower Inc. (HCN) believes that revenues, net operating income from continuing operations (NOICO), net income and net income attributable to common stockholders (NICS), as

NEWS FLASH! HUD Memo October 23, Upcoming Training. CHDO Development Process Webinar Part 2 October 25, 2017

CHDO Development Process Webinar Part 2 October 25, 2017 Catalyst Training Schedule Gladys Cook Florida Housing Coalition Technical Advisor cook@flhousing.org Sponsored by the Florida Housing Finance Corporation

CHDO Development Process Webinar Part 2 October 25, 2017 Catalyst Training Schedule Gladys Cook Florida Housing Coalition Technical Advisor cook@flhousing.org Sponsored by the Florida Housing Finance Corporation

Sales Associate Course

Sales Associate Course Chapter Seventeen Real Estate Investments and Business Opportunity Brokerage 1 Investment Analysis Most important consideration: Economic soundness Land use controls Zoning Deed

Sales Associate Course Chapter Seventeen Real Estate Investments and Business Opportunity Brokerage 1 Investment Analysis Most important consideration: Economic soundness Land use controls Zoning Deed

Index of Examples. Chapter 1 Letter of Transmittal Chapter 2 General Assumptions and Limiting Conditions... 19

Index of Examples Chapter 1 Letter of Transmittal... 1 Example 1A Detailed Letter of Transmittal... 2 Example 1B Detailed Letter of Transmittal with Risk Factors and Assumptions... 6 Example 1C Brief Letter

Index of Examples Chapter 1 Letter of Transmittal... 1 Example 1A Detailed Letter of Transmittal... 2 Example 1B Detailed Letter of Transmittal with Risk Factors and Assumptions... 6 Example 1C Brief Letter

HOME Investment Partnership Program Project Development Funds. Application

City of Spartanburg Neighborhood Services 145 West Broad Street Spartanburg, South Carolina 29306 HOME Investment Partnership Program Project Development Funds Application Applicant Name: Project Name:

City of Spartanburg Neighborhood Services 145 West Broad Street Spartanburg, South Carolina 29306 HOME Investment Partnership Program Project Development Funds Application Applicant Name: Project Name:

Real Estate Development 46th Annual Basic Economic Development Course

Real Estate Development 46th Annual Basic Economic Development Course Emil Malizia Research Professor Department of City and Regional Planning University of North Carolina at Chapel Hill August 1, 2018

Real Estate Development 46th Annual Basic Economic Development Course Emil Malizia Research Professor Department of City and Regional Planning University of North Carolina at Chapel Hill August 1, 2018

Appraisal and Market Analysis of Indoor Waterpark Resorts

Appraisal and Market Analysis of Indoor Waterpark Resorts By David J. Sangree, MAI, CPA, ISHC An appraisal of an indoor waterpark resort is similar to other appraisals in that it is a professional appraiser

Appraisal and Market Analysis of Indoor Waterpark Resorts By David J. Sangree, MAI, CPA, ISHC An appraisal of an indoor waterpark resort is similar to other appraisals in that it is a professional appraiser

Business Valuation More Art Than Science

Business Valuation More Art Than Science One of the more difficult aspects of business planning is business valuation. It is also one of the more important aspects. While owners of closely held businesses

Business Valuation More Art Than Science One of the more difficult aspects of business planning is business valuation. It is also one of the more important aspects. While owners of closely held businesses

Understanding the Economics & Financing Structures of Moderately Priced Life Plan Communities

Understanding the Economics & Financing Structures of Moderately Priced Life Plan Communities 2 Today s Presenters Wayne Olson, Executive Vice President, Volunteers of America National Services Steve Kuhns,

Understanding the Economics & Financing Structures of Moderately Priced Life Plan Communities 2 Today s Presenters Wayne Olson, Executive Vice President, Volunteers of America National Services Steve Kuhns,

REAL ESTATE INVESTMENTS

REAL ESTATE INVESTMENTS PROBLEM SET 2 1. PROBLEM The leases for space in an office building provide for limitations or stops on the lessor s liability for real estate taxes and operating expenses. Each

REAL ESTATE INVESTMENTS PROBLEM SET 2 1. PROBLEM The leases for space in an office building provide for limitations or stops on the lessor s liability for real estate taxes and operating expenses. Each

Connecticut Housing Finance Authority

Connecticut Housing Finance Authority Multifamily Rental Housing Program Guideline 2018 This Guideline is Effective Table of Contents I. Preface... 4 II. Background... 4 III. Pre-Application... 4 IV. Application

Connecticut Housing Finance Authority Multifamily Rental Housing Program Guideline 2018 This Guideline is Effective Table of Contents I. Preface... 4 II. Background... 4 III. Pre-Application... 4 IV. Application

PROJECT FINANCE & APPRAISAL Translating the Value of Regenerative Design into Real Estate Speak. Matt Macko Environmental Building Strategies

PROJECT FINANCE & APPRAISAL Translating the Value of Regenerative Design into Real Estate Speak Matt Macko Environmental Building Strategies The Developer Role Understand your client! How a developer thinks

PROJECT FINANCE & APPRAISAL Translating the Value of Regenerative Design into Real Estate Speak Matt Macko Environmental Building Strategies The Developer Role Understand your client! How a developer thinks

Frequently Asked Questions Regarding the FY-2016 Rental Production NOFA

Frequently Asked Questions Regarding the FY-2016 Rental Production NOFA These FAQ s provide answers to common questions regarding MHDC s FY-2016 NOFA application process. The FAQ is divided into three

Frequently Asked Questions Regarding the FY-2016 Rental Production NOFA These FAQ s provide answers to common questions regarding MHDC s FY-2016 NOFA application process. The FAQ is divided into three

IMPAIRMENT TESTING OF LONG-LIVED ASSETS TO BE HELD AND USED

IMPAIRMENT TESTING OF LONG-LIVED ASSETS TO BE HELD AND USED Prepared by: Rick Day, Partner, National Director of Accounting, RSM US LLP rick.day@rsmus.com, +1 563 888 4017 TABLE OF CONTENTS Introduction...

IMPAIRMENT TESTING OF LONG-LIVED ASSETS TO BE HELD AND USED Prepared by: Rick Day, Partner, National Director of Accounting, RSM US LLP rick.day@rsmus.com, +1 563 888 4017 TABLE OF CONTENTS Introduction...

An Interactive Feasibility Tool

INSTRUCTION GUIDE Affordable Assisted Living and Community Based Care: An Interactive Feasibility Tool Developed for: The Coming Home Program In partnership with the Robert Wood Johnson Foundation NCB

INSTRUCTION GUIDE Affordable Assisted Living and Community Based Care: An Interactive Feasibility Tool Developed for: The Coming Home Program In partnership with the Robert Wood Johnson Foundation NCB

Chapter 8. How much would you pay today for... The Income Approach to Appraisal

How much would you pay today for... Chapter 8 One hundred dollars paid with certainty each year for five years, starting one year from now. Why would you pay less than $500 Valuation Using the Income Approach

How much would you pay today for... Chapter 8 One hundred dollars paid with certainty each year for five years, starting one year from now. Why would you pay less than $500 Valuation Using the Income Approach

60-HR FL Real Estate Broker Post-Licensing Learning Objectives by Lesson

Lesson 1: Starting a Real Estate Office SECTION 1: BROKERAGE OFFICE ESSENTIALS Recall the characteristics of business entities that may register as a real estate brokerage and the rules involved to operate

Lesson 1: Starting a Real Estate Office SECTION 1: BROKERAGE OFFICE ESSENTIALS Recall the characteristics of business entities that may register as a real estate brokerage and the rules involved to operate

Budgeting for Industry Sponsored Clinical Research. Sarah Bernardo Senior Financial Analyst, MCA Specialist Partners Clinical Trials Office

Budgeting for Industry Sponsored Clinical Research Sarah Bernardo Senior Financial Analyst, MCA Specialist Partners Clinical Trials Office Elements of Successful Budgeting Analyze research or protocol

Budgeting for Industry Sponsored Clinical Research Sarah Bernardo Senior Financial Analyst, MCA Specialist Partners Clinical Trials Office Elements of Successful Budgeting Analyze research or protocol

Lease & Finance Accountants Conference. September The Westin Charlotte Charlotte, NC

Lease & Finance Accountants Conference September 11-13 The Westin Charlotte Charlotte, NC H A N D O U T S Basic Principles of Lessors under ASC 842 Mamta Shori, Wells Fargo Equipment Finance Joe Sebik,

Lease & Finance Accountants Conference September 11-13 The Westin Charlotte Charlotte, NC H A N D O U T S Basic Principles of Lessors under ASC 842 Mamta Shori, Wells Fargo Equipment Finance Joe Sebik,

Technical Line FASB final guidance

No. 2017-17 29 June 2017 Technical Line FASB final guidance How the new revenue standard affects operating real estate entities In this issue: Overview... 1 Real estate sales... 2 Property management services...

No. 2017-17 29 June 2017 Technical Line FASB final guidance How the new revenue standard affects operating real estate entities In this issue: Overview... 1 Real estate sales... 2 Property management services...

ANALYTICS & MANAGEMENT OF MIXED INCOME PROPERTY

MIXED INCOME PROPERTY CFO FORUM NEIGHBORWORKS AMERICA TRAINING INSTITUTE KANSAS CITY, MISSOURI Presented by Len Tatem (Tatem Consulting LLC) & John Kelley (CNAHS/HRI Cambridge, MA) DEFINING MIXED-INCOME

MIXED INCOME PROPERTY CFO FORUM NEIGHBORWORKS AMERICA TRAINING INSTITUTE KANSAS CITY, MISSOURI Presented by Len Tatem (Tatem Consulting LLC) & John Kelley (CNAHS/HRI Cambridge, MA) DEFINING MIXED-INCOME

BARNSTABLE COUNTY HOME CONSORTIUM UNDERWRITING ANALYSIS OF FUNDING REQUEST

BARNSTABLE COUNTY HOME CONSORTIUM UNDERWRITING ANALYSIS OF FUNDING REQUEST APPLICANT/SPONSOR: Dakota Partners PROJECT NAME/ADDRESS: Village Green- Phase II 770 Independence Drive- Hyannis HOME $ REQUESTED:

BARNSTABLE COUNTY HOME CONSORTIUM UNDERWRITING ANALYSIS OF FUNDING REQUEST APPLICANT/SPONSOR: Dakota Partners PROJECT NAME/ADDRESS: Village Green- Phase II 770 Independence Drive- Hyannis HOME $ REQUESTED:

Chapter 18. Investors have different required yields Different risk assessment Different opportunity cost of equity

Decision Making in Real Estate Centers Around Valuation Chapter 18 Investment Decisions: Ratios We examined the concept of market value in Chapters 7 & 8 As noted, professional RE appraisers are often

Decision Making in Real Estate Centers Around Valuation Chapter 18 Investment Decisions: Ratios We examined the concept of market value in Chapters 7 & 8 As noted, professional RE appraisers are often

C O O K C O U N T Y A S S E S S O R S O F F I C E VALUATION ESTIMATES AND APPRAISAL METHODOLOGY

C O O K C O U N T Y A S S E S S O R S O F F I C E EXEMPT HOSPITALS VALUATION ESTIMATES AND APPRAISAL METHODOLOGY EXEMPT HOSPITALS VALUATION ESTIMATES AND APPRAISAL METHODOLOGY PURPOSE OF THE REPORT In

C O O K C O U N T Y A S S E S S O R S O F F I C E EXEMPT HOSPITALS VALUATION ESTIMATES AND APPRAISAL METHODOLOGY EXEMPT HOSPITALS VALUATION ESTIMATES AND APPRAISAL METHODOLOGY PURPOSE OF THE REPORT In

Shawnee Landing TIF Project. City of Shawnee, Kansas. Need For Assistance Analysis

Shawnee Landing TIF Project City of Shawnee, Kansas Need For Assistance Analysis December 17, 2014 Table of Contents 1 EXECUTIVE SUMMARY... 1 2 PURPOSE... 2 3 THE PROJECT... 3 4 ASSISTANCE REQUEST... 7

Shawnee Landing TIF Project City of Shawnee, Kansas Need For Assistance Analysis December 17, 2014 Table of Contents 1 EXECUTIVE SUMMARY... 1 2 PURPOSE... 2 3 THE PROJECT... 3 4 ASSISTANCE REQUEST... 7

2019 9% Competitive Housing Credit Application

2019 9% Competitive Housing Credit Application Application Checklist This checklist includes all the items from the CFA application and the LIHTC Addendum that are required for the 2019 9% Application

2019 9% Competitive Housing Credit Application Application Checklist This checklist includes all the items from the CFA application and the LIHTC Addendum that are required for the 2019 9% Application

Kitsap County Assessor

Kitsap County Assessor Narrative for Countywide Model Tax Year: 2018 Appraisal Date: 1/1/2017 Property Type: Countywide Retail - Big Box Updated 6/8/2017 by CM20 Area Overview Countywide models are for

Kitsap County Assessor Narrative for Countywide Model Tax Year: 2018 Appraisal Date: 1/1/2017 Property Type: Countywide Retail - Big Box Updated 6/8/2017 by CM20 Area Overview Countywide models are for

UNDERSTANDING THE DEVELOPMENT PRO FORMA

UNDERSTANDING THE DEVELOPMENT PRO FORMA March 16, 2017 ULI Urban Leadership Program Dr. Steven Webber Ryerson University/Urbanformation Consulting Pro forma Financial analysis based on Revenues Costs Return

UNDERSTANDING THE DEVELOPMENT PRO FORMA March 16, 2017 ULI Urban Leadership Program Dr. Steven Webber Ryerson University/Urbanformation Consulting Pro forma Financial analysis based on Revenues Costs Return

7401 PACIFIC BLVD. HUNTINGTON PARK, CA 90255

OFFERING MEMORANDUM $1,295,000 7401 PACIFIC BLVD. HUNTINGTON PARK, CA 90255 90% FINANCING AVAILABLE STRIP CENTER - MTM TENANCY 1 This Memorandum ( Offering Memorandum ) has been prepared by Brookfield

OFFERING MEMORANDUM $1,295,000 7401 PACIFIC BLVD. HUNTINGTON PARK, CA 90255 90% FINANCING AVAILABLE STRIP CENTER - MTM TENANCY 1 This Memorandum ( Offering Memorandum ) has been prepared by Brookfield

GAAP UPDATE DEANA BOWDEN, CPA, MSA WHITE NELSON DIEHL EVANS LLP

GAAP UPDATE DEANA BOWDEN, CPA, MSA WHITE NELSON DIEHL EVANS LLP TOPICS 2016-02 Topic 842 Leases 2016-14 Topic 958 Not for Profits 2016-18 Topic 230 Cash Flows LEASES Current US Generally Accepted Accounting

GAAP UPDATE DEANA BOWDEN, CPA, MSA WHITE NELSON DIEHL EVANS LLP TOPICS 2016-02 Topic 842 Leases 2016-14 Topic 958 Not for Profits 2016-18 Topic 230 Cash Flows LEASES Current US Generally Accepted Accounting

Presentation of Key Findings and Recommendations to the Broward County Commission. Assessment Report and Recommendations: Young At Art Museum

Presentation of Key Findings and Recommendations to the Broward County Commission Assessment Report and Recommendations: Young At Art Museum 1 Broward County contracted the consultant to assess and develop

Presentation of Key Findings and Recommendations to the Broward County Commission Assessment Report and Recommendations: Young At Art Museum 1 Broward County contracted the consultant to assess and develop

2017 Uniform Multifamily Application Templates

2017 Uniform Multifamily Application Templates 221 East 11 th Street Austin, TX 78701 Table of Contents Template Overview... 3 Using the Templates... 4 Public Notification Template... 5 Twice the State

2017 Uniform Multifamily Application Templates 221 East 11 th Street Austin, TX 78701 Table of Contents Template Overview... 3 Using the Templates... 4 Public Notification Template... 5 Twice the State

Land / Site Valuation A Basic Review. Leslie G. Pruitt Certified General Appraiser

Land / Site Valuation A Basic Review Leslie G. Pruitt Certified General Appraiser Whose is the land, it is to the sky and the depth Whose is the land, it is to the sky and the depth This ancient maxim

Land / Site Valuation A Basic Review Leslie G. Pruitt Certified General Appraiser Whose is the land, it is to the sky and the depth Whose is the land, it is to the sky and the depth This ancient maxim

10 Common Mistakes in Valuing ASCs and How to Avoid Them

10 Common Mistakes in Valuing ASCs and How to Avoid Them Presented by: Hunter Outcalt, MTx, CPA Director, HealthCare Appraisers HealthCare Appraisers, Inc. HealthCare Appraisers is the nation s leading

10 Common Mistakes in Valuing ASCs and How to Avoid Them Presented by: Hunter Outcalt, MTx, CPA Director, HealthCare Appraisers HealthCare Appraisers, Inc. HealthCare Appraisers is the nation s leading

Proposed FASB Staff Position No. 142-d, Amortization and Impairment of Acquired Renewable Intangible Assets (FSP 142-d)

") Financial Reporting Advisors, LLC 100 North LaSalle Street, Suite 2215 Chicago, Illinois 60602 312.345.9101 www.finra.com Mr. Lawrence W. Smith Director - Technical Application and Implementation Activities

Financial Reporting Advisors, LLC 100 North LaSalle Street, Suite 2215 Chicago, Illinois 60602 312.345.9101 www.finra.com Mr. Lawrence W. Smith Director - Technical Application and Implementation Activities

Acquisition of Place Properties

September 15, 2005 Acquisition of Place Properties Presentation to Stockholders 1 Table of Contents SECTION 1 Company Overview 3 SECTION 2 Transaction Overview 6 SECTION 3 Financial Summary of Transaction

September 15, 2005 Acquisition of Place Properties Presentation to Stockholders 1 Table of Contents SECTION 1 Company Overview 3 SECTION 2 Transaction Overview 6 SECTION 3 Financial Summary of Transaction

DETERMINING AGENCY VALUE PART 2

DETERMINING AGENCY VALUE PART 2 NORMALIZING THE INCOME STATEMENT By: Chuck Coyne, ASA This month we continue our discussion of how to determine an agency s value. Last month we briefly discussed some of

DETERMINING AGENCY VALUE PART 2 NORMALIZING THE INCOME STATEMENT By: Chuck Coyne, ASA This month we continue our discussion of how to determine an agency s value. Last month we briefly discussed some of

Chapter 8. The Income Approach to Appraisal. Two Approaches to Income Valuation. How Does DCF Differ from Direct Cap? Rationale:

The Income Approach to Appraisal Chapter 8 Valuation Using the Income Approach Rationale: Value of a property is the present value of its anticipated income. Often called income capitalization Capitalize:

The Income Approach to Appraisal Chapter 8 Valuation Using the Income Approach Rationale: Value of a property is the present value of its anticipated income. Often called income capitalization Capitalize:

Before the Minnesota Public Utilities Commission State of Minnesota. Docket No. E002/GR Exhibit (LMC-1) Property Taxes

Property Taxes") Direct Testimony and Schedules Leanna M. Chapman Before the Minnesota Public Utilities Commission State of Minnesota In the Matter of the Application of Northern States Power Company for Authority to Increase

Direct Testimony and Schedules Leanna M. Chapman Before the Minnesota Public Utilities Commission State of Minnesota In the Matter of the Application of Northern States Power Company for Authority to Increase

Hotel / Motel. Market Value Assessment in Saskatchewan Handbook. Hotel / Motel Valuation Guide

Market Value Assessment in Saskatchewan Handbook Hotel / Motel Saskatchewan Assessment Management Agency 2012 This document is a derivative work based upon a handbook entitled the "Market Value and Mass

Market Value Assessment in Saskatchewan Handbook Hotel / Motel Saskatchewan Assessment Management Agency 2012 This document is a derivative work based upon a handbook entitled the "Market Value and Mass

RAINS COUNTY APPRAISAL DISTRICT

RAINS COUNTY APPRAISAL DISTRICT 2017 MASS APPRAISAL SUMMARY REPORT mass appraisal report 2017 uspap_appr_report RAINS COUNTY APPRAISAL DISTRICT 2017 MASS APPRAISAL SUMMARY REPORT Identification of Subject:

RAINS COUNTY APPRAISAL DISTRICT 2017 MASS APPRAISAL SUMMARY REPORT mass appraisal report 2017 uspap_appr_report RAINS COUNTY APPRAISAL DISTRICT 2017 MASS APPRAISAL SUMMARY REPORT Identification of Subject:

Differences, Procurement and

U.S. Department of Housing and Urban Development Developers and Subrecipients: Differences, Procurement and Other Rules July 24, 2012 2:00 PM EDT Community Planning and Development Purpose of Webinar To

U.S. Department of Housing and Urban Development Developers and Subrecipients: Differences, Procurement and Other Rules July 24, 2012 2:00 PM EDT Community Planning and Development Purpose of Webinar To

Fully Stabilized 24-Unit Property at 11% Cap Rate!

Fully Stabilized 24-Unit Property at 11% Cap Rate! To Insert a Picture here, click inside this box with your mouse, then click on "INSERT PIC" button on the right and select the picture 24 Units consisting

Fully Stabilized 24-Unit Property at 11% Cap Rate! To Insert a Picture here, click inside this box with your mouse, then click on "INSERT PIC" button on the right and select the picture 24 Units consisting

MEMORANDUM ADDENDUM. Dan Moye, Economic Development Corporation of Kansas City, Missouri

MEMORANDUM ADDENDUM TO: FROM: Dan Moye, Economic Development Corporation of Kansas City, Missouri Fran Lefor Rood, SB Friedman Development Advisors Direct: (312) 424-4253; Email: frood@sbfriedman.com DATE:

MEMORANDUM ADDENDUM TO: FROM: Dan Moye, Economic Development Corporation of Kansas City, Missouri Fran Lefor Rood, SB Friedman Development Advisors Direct: (312) 424-4253; Email: frood@sbfriedman.com DATE:

Revised Seller/Servicer Guide Chapter 12 Multifamily Appraisals. Martin A. Skolnik, MAI (Marty) Director, Multifamily Appraisals

Director, Multifamily Appraisals") Revised Seller/Servicer Guide Chapter 12 Multifamily Appraisals Martin A. Skolnik, MAI (Marty) Director, Multifamily Appraisals June 26, 2014 Multifamily Real Estate Valuation at Freddie Mac Freddie Mac

Revised Seller/Servicer Guide Chapter 12 Multifamily Appraisals Martin A. Skolnik, MAI (Marty) Director, Multifamily Appraisals June 26, 2014 Multifamily Real Estate Valuation at Freddie Mac Freddie Mac

Capital Assets, Supplies, Equipment, and Intangible Property

Capital Assets, Supplies, Equipment, and Intangible Property 1 Uniform Guidance vs. OMB Circulars Prior to the Uniform Guidance, requirements governing cost Designed for DOL-ETA direct principles, administrative

Capital Assets, Supplies, Equipment, and Intangible Property 1 Uniform Guidance vs. OMB Circulars Prior to the Uniform Guidance, requirements governing cost Designed for DOL-ETA direct principles, administrative

Rental Assistance Demonstration

Rental Assistance Demonstration NERC NAHRO Newport, Rhode Island 1 24 12 Gregory A. Byrne Gregory.A.Byrne@hud.gov HISTORY February 2010: FY11 Budget requests $350m for Transforming Rental Assistance (TRA)

Rental Assistance Demonstration NERC NAHRO Newport, Rhode Island 1 24 12 Gregory A. Byrne Gregory.A.Byrne@hud.gov HISTORY February 2010: FY11 Budget requests $350m for Transforming Rental Assistance (TRA)

APPRAISER & ASSESSOR Real Estate Tax Valuation Overview and Issues

APPRAISER & ASSESSOR Real Estate Tax Valuation Overview and Issues James R. Johnston, MAI, SRA J. Michael Tarello, MAI, ASA, MRA May 20, 2015 BOSTON Property Advisors Vision Government Solutions AGENDA

APPRAISER & ASSESSOR Real Estate Tax Valuation Overview and Issues James R. Johnston, MAI, SRA J. Michael Tarello, MAI, ASA, MRA May 20, 2015 BOSTON Property Advisors Vision Government Solutions AGENDA

REPORT. DATE ISSUED: December 19, 2014 REPORT NO: HCR Chair and Members of the San Diego Housing Commission For the Agenda of January 16, 2015

REPORT DATE ISSUED: December 19, 2014 REPORT NO: HCR15-008 ATTENTION: SUBJECT: Chair and Members of the San Diego Housing Commission For the Agenda of January 16, 2015 COUNCIL DISTRICT: 9 REQUESTED ACTION

REPORT DATE ISSUED: December 19, 2014 REPORT NO: HCR15-008 ATTENTION: SUBJECT: Chair and Members of the San Diego Housing Commission For the Agenda of January 16, 2015 COUNCIL DISTRICT: 9 REQUESTED ACTION

Sales Associate Course

Sales Associate Course Chapter Sixteen Appraisal 1 2 Appraiser Specific amount Impartial (non biased) Defendable Estimate (Opinion) of value Fee based on time and difficulty Must follow Uniform Standards

Sales Associate Course Chapter Sixteen Appraisal 1 2 Appraiser Specific amount Impartial (non biased) Defendable Estimate (Opinion) of value Fee based on time and difficulty Must follow Uniform Standards

SELF-STORAGE INVESTMENT OFFERING

SELF-STORAGE INVESTMENT OFFERING A-Economy Storage 104 S. Division Street ±481 Storage Units + ±12,000 SF of Commercial / Retail Space ±113,915 SF Gross Building Area Offered at $3,700,000 ($32/SF gross

SELF-STORAGE INVESTMENT OFFERING A-Economy Storage 104 S. Division Street ±481 Storage Units + ±12,000 SF of Commercial / Retail Space ±113,915 SF Gross Building Area Offered at $3,700,000 ($32/SF gross

Kitsap County Assessor

Documentation for Countywide Model Tax Year: 2019 Appraisal Date: 1/1/2018 Property Type: Land Leases for Cell Sites, Espresso Sites, ATM Sites, and Billboard Sites Updated 2/6/2018 by CM20 Area Overview

Documentation for Countywide Model Tax Year: 2019 Appraisal Date: 1/1/2018 Property Type: Land Leases for Cell Sites, Espresso Sites, ATM Sites, and Billboard Sites Updated 2/6/2018 by CM20 Area Overview

Modeling your Appraisal Report to Meet your Client's Needs in the Commercial Marketplace

Modeling your Appraisal Report to Meet your Client's Needs in the Commercial Marketplace Myth #1 The Final Estimate of Value is the Only Area of the Report Anyone Reads Financial Institutions -Interagency

Modeling your Appraisal Report to Meet your Client's Needs in the Commercial Marketplace Myth #1 The Final Estimate of Value is the Only Area of the Report Anyone Reads Financial Institutions -Interagency

REPORT. DATE ISSUED: February 3, 2006 ITEM 103. Loan to San Diego Youth and Community Services for Transitional Housing (Council District 3)

") 1625 Newton Avenue San Diego, California 92113-1038 619/231 9400 FAX: 619/544 9193 www.sdhc.net REPORT DATE ISSUED: February 3, 2006 ITEM 103 REPORT NO.: HCR06-11 For the Agenda of February 10, 2006 SUBJECT:

1625 Newton Avenue San Diego, California 92113-1038 619/231 9400 FAX: 619/544 9193 www.sdhc.net REPORT DATE ISSUED: February 3, 2006 ITEM 103 REPORT NO.: HCR06-11 For the Agenda of February 10, 2006 SUBJECT:

MANUFACTURED HOME PARK LOAN PROGRAM TERM SHEET

MANUFACTURED HOME PARK LOAN PROGRAM TERM SHEET Description: The Manufactured Home Park Loan Program provides permanent financing for the acquisition of mobile home parks (MHPs) by organizations interested

MANUFACTURED HOME PARK LOAN PROGRAM TERM SHEET Description: The Manufactured Home Park Loan Program provides permanent financing for the acquisition of mobile home parks (MHPs) by organizations interested

NSP Rental Basics: A Primer on Using Rental Projects to Meet NSP Obligation and 25% Set-Aside Requirement. About this Tool

NSP Rental Basics: A Primer on Using Rental Projects to Meet NSP Obligation and 25% Set-Aside Requirement About this Tool Description: This tool is intended for NSP grantees and their partners seeking

NSP Rental Basics: A Primer on Using Rental Projects to Meet NSP Obligation and 25% Set-Aside Requirement About this Tool Description: This tool is intended for NSP grantees and their partners seeking