CITY COUNCIL WORK SESSION MEETING AGENDA May 21, :30 6:30pm

|

|

|

- Rhoda Hopkins

- 5 years ago

- Views:

Transcription

MSAS 101 / Special Assessment Policy 3) Gene Lehner Park 4) Adjourn")

1 CITY COUNCIL WORK SESSION MEETING AGENDA May 21, :30 6:30pm 1) Call to Order 2) MSAS 101 / Special Assessment Policy 3) Gene Lehner Park 4) Adjourn

2 WS Item 2 STATE AID SYSTEM 101 City of Minnetrista May 21, 2018

3 State Aid What is State Aid? Who Oversees State Aid? How is State Aid Funded? Who Is Eligible? How is Money Distributed? How is Money Received?

4 What is State Aid? State Aid for Local Transportation (SALT) Established to administer CSAH and MSAS portions of the Highway User Tax Distribution Fund Serves as liaison between MnDOT and City and County engineers

5 How is State Aid Funded? Fund designated City and County Roads Since 1955 Fuel Tax Revenue License Fees Motor Vehicle Sales Tax Other Interest and Sources

6 MN Hwy Users Tax Distribution Fund TO TAL TO TAL M ONDO -FRESH G a so lin e GASOLINE AND SPECIAL FUEL TAXES $921,300,000 MOTOR VEHICLE LICENSE FEES $787,300,000 MOTOR VEHICLE SALES TAX $470,820,000 Total Highway Users Fund $2,273,775,000 OTHER (INTEREST ) $94,355,000 (2018)

7 Minnesota Highway Users Tax Distribution Fund Collection Costs and Refunds to DNR, Public Safety, Revenue, Administration, etc. $35,765,000 Total Highway Users Fund $ 2,273,775,000 Special 5% Distribution $111,300,500 Town Bridge Account 16% Town Road Account 30.5% Flexible Highway Account 53.5% Trunk Highway Fund 62% Regular Distribution $2,114,709,500 County State Aid Highway Fund Municipal State Aid Street Fund 29% 9% (2018 )

8 Gas Tax Distribution Formula MnDOT - $1,311,119,890 County State Aid Highways - $ 613,265,755 Municipal State Aid Streets - $ 190,323,855

9 Who is Eligible? CSAH - All 87 counties MSAS - Only cities > 5,000 pop MSAS Cities

10 How is Money Distributed? CSAH MSAS Both have their own formulas and systems

11 CSAH Funds Distributed to all 87 Counties by the following formula: 50% - Construction Needs 30% - Lane miles of CSAH roads 10% - Motor Vehicle registrations 10% - Equalization factor For 2018, approximately $613 million is designated for Counties.

12 MSAS Funds Distributed to cities over 5,000 population by the following formula: 50% - Population 50% - Construction Needs For 2018, approximately $190 million is designated for MSA cities.

13 Population Apportionment Based on Annual Census (every 10 years), and Annual estimates by Met Council or State Demographer. Population estimates cannot result in a decrease in population from the census.

14 Needs Definition Needs are the estimated construction costs to build out the CSAH or MSAS system.

15 Certification of Mileage - MSAS Required annually Certifying total mileage within City Due January 15 th

16 Limitations on Mileage CSAH - None MSAS - Maximum 20% of the total City street mileage Note: Turnback mileage is above and beyond the 20% MSAS limit

17 Designating Routes CSAH and MSAS Subject to the approval of the Commissioner of MnDOT Integrated network required: - Must connect up with another State Aid route (CSAH or MSAS) or a trunk highway.

18 Designating Routes (cont d) Selection criteria - Should be designated as a collector or arterial road or carry a higher ADT - Should connect towns, communities, schools, industrial/commercial areas, parks, points of major interest, recreational areas or state institutions. - Meets integrated network test.

19 MSAS System

20 MSAS System Revisions Allowed annually additions or deletions Requests to State Aid by March 1 st City Council resolution by May 1 st Approved by Commissioners Order Additions must stay within the 20% limit Routes can be revoked at any time. Payback may be required if State Aid money was spent on them within past 25 years.

21 Needs Criteria Based on a 25 year service life City or County Engineer must report their needs annually by March 1 st The screening board, along with MnDOT set the unit prices for each item in the needs on an annual basis.

22 Needs Calculation Current System Reinstatement Needs (2012) Minimal Needs for 20 years (after construction) Full needs after reinstated Based on existing vs. proposed conditions Proposed System Continual Needs (2013 Present) Full needs regardless of when constructed Based on existing ADT

23 Apportionment Date (2018) $1,000 in needs = $12.68 in MSA funding 1 person = $24.54 in MSA funding

24 State Aid Funding Examples City Pop. Apport. Needs Apport. Total Apport. Mpls $10,306,361 $ 7,213,277 $17,519,638 Lakeville $1,496,188 $ 1,618,486 $ 3,114,674 Monticello $ 329,080 $ 292,417 $ 621,497 Minnetrista $ 177,633 $ 264,440 $ 442,073 Rosemount $ 578,179 $ 620,073 $ 1,198,252 St. Anthony $ 226,619 $ 162,481 $ 389,100 Duluth $2,131,673 $ 3,505,816 $ 5,637,489

25 State Aid Balance Penalty for not utilizing funds Penalty sets in when balance is $1.5M or 3 times the current allotment, whichever is greater Penalty increases (multiplies) each year the balance is not drawn down Minnetrista current balance = $937,253

26 How is Money Received? Cities receive funds via two accounts Maintenance Fund Construction Fund

27 Maintenance Funds Cities must choose from one of the following options: $1500 per MSAS mile (minimum) or up to 35% of total annual amount (maximum) Most cities set maintenance at 25% Remainder of annual amount is available for construction projects.

28 Maintenance Funds (cont d) Get sent to the City directly twice/year City is supposed to put towards maintenance of the State Aid system. Most cities put it in their General Fund budget under Public Works to offset maintenance activities of all streets patching, seal coating, etc. No reporting requirements on how the money is spent (if 25% or less requested)

29 Construction Funds Cities don t receive any money until requested. Request must be accompanied by an estimate. City account is maintained by MnDOT and keeps growing annually until a project is awarded. Once project is awarded, City can receive 95% of the bid amount right away. The remaining 5% is paid upon close out of the project. Only eligible bid items included in funding.

30 Const. Plans for State Aid Projects Must meet CSAH or MSAS design standards. There is flexibility in the rules regarding the type of road you are proposing (2 lane vs. 4 lane, urban vs. rural, parking, etc), but standards are set for each type. MnDOT State Aid office must approve and sign plans prior to opening bids

31 Special Assessment Policy Discussion City Council Work Session May 21, 2018

32 Assessment Methods Unit Method: The project cost for the local improvement shall be divided by the total number of abutting and/or benefiting properties to arrive at the project assessment rate per unit. For all street/road projects, the City s policy will be to assess sub-dividable properties on the following basis: ZONING Agriculture Rural Residential R2 - Low (single family) R3 - Low-medium (Townhouse & multi-family) R4 & R5 - Medium (Multi-family) # OF UNITS 1 unit for every 40 acres 1 unit for every 10 acres 2 units per acre 6 units per acre 9 units per acre In all cases, all but one unit may be deferred with interest until such time as the property is developed or at the end of the life of the improvement, whichever occurs first. If the development occurs at less than the number of units deferred, no reduction will be given.

33 Assessment Methods Area Method: This category includes both the Net Acre method and the Square Foot method. Assessable area shall be expressed in the terms of the number of acres or the number of square feet subject to assessment. Net Acre - When using this method, the assessable area of a parcel is multiplied by the per net acre rate to arrive at the assessment amount for that parcel. Square Foot - When using this method, the assessable area of a parcel is multiplied by the per square foot rate to arrive at the assessment amount for that parcel. When determining the assessable area, the following considerations will be given: Lakes, ponds and swamps will be considered part of the assessable area of the parcel. However, the property owner has the option of giving a storm water ponding easement for the land under the lake, pond, or swamp to the City. If such ponding easement is given, a ponding credit equal to the area of the lake, pond, or swamp is to be subtracted from the gross acreage of the parcel before determining other credits.

34 Assessment Methods Front Foot Method: When using this method, the front footage of each parcel to be assessed is calculated. When calculating front footage for unusually shaped lots, the following will apply. Rectangular Lots Cul - De - Sac Lots Lots with Curved Frontage Trapezoidal and Triangular Measure the lot width at the front line Measure the lot width at the front building set back Measure the lot width at the front building setback Measure the lot width at the front and back lot lines, Corner Lots When assessing for streets/utilities, corner lots to be assessed at the front foot method plus 20% of the side street frontage. Each parcel along a project road shall be assigned its current number of development units as permitted under the existing zoning and density standards. This assignment of development units would be exclusive of Agricultural Preserve Status. A parcel currently being used for agricultural purposes may have the special assessment on all but one assessment unit/per 40 acres, postponed until the land is subdivided, developed or ceased being used for agricultural purposes. A parcel that is currently unbuildable (for example no septic available) shall have its assessment(s) postponed until the parcel is buildable. At such time as the property that is the subject of a postponed assessment is developed or becomes buildable, it shall be assessed by the City Council with notice and public hearing pursuant to Minn. Stat All parcels that are subject to a postponed special assessment shall be so identified on the original Special Assessment Roll that is filed with the Count; that additionally, the City Clerk shall make notation of the postponed units within the City.

35 Recent Assessment Parcel Map Parcel size variations:

36 Assessable Improvements NEW STREET/ROAD CONSTRUCTION Street/road construction is defined as the initial installation of a permanent street/road into an area, consisting of the necessary grading, base, hard surfacing (bituminous or concrete), and curb and gutter. Policy. It is the intention of the City to install all utilities and utility service lines concurrently with construction of new streets/roads that lie within the MUSA. However, each road needs to be examined on a case by case basis. No street/road construction shall be approved for less than both sides of a street/road except as necessary to complete the improvement of a block that has previous partial completion. A street/road improvement may occur wholly or partially outside of the MUSA, as determined by the City Council. Method of Assessment. The assessable costs for street/road construction shall be distributed among benefited properties on a per unit basis. Assessable Cost. The assessable cost equals 100 percent (100%) of the entire project cost for the street/road construction including intersections, alley openings, and street/road openings. Street/road improvements shall be assessed consistent with the street/road improvement method.

37 Assessable Improvements

38 Assessable Improvements Method of Assessment. The assessable costs for street/road construction shall be distributed among benefited properties on a per unit basis. For rural street/road improvements, properties that do not directly abut the improvement but benefit from it shall be eligible for whole or partial unit special assessment consideration. Assessable Cost. The assessable cost equals 50 percent (50%) of reconstructing a rural and/or urban street/road and 100 percent (100%) of overlaying a rural/gravel street/road and 100 percent (100%) of milling and overlaying an urban street. Street/road improvements shall be assessed consistent with the street/road improvement method.

39 Assessable Improvements MAINTENANCE Maintenance is a cost-effective measure to extend the useful street life of a particular roadway and to delay street reconstruction needs. Street/road maintenance may occur wholly or partially outside of the MUSA, as determined by the City Council. Maintenance projects shall include but are not limited to the following: Crack Sealing - Placement of petroleum-based material in the cracks of a bituminous surfaced street for the purpose of eliminating the flow of water from the surface to the aggregate base material below. Bituminous Seal Coating - Placement of petroleum-based material and aggregate on an existing bituminous surfaced street for the purpose of filling cracks and covering mild wear. Bituminous Surfacing Patching - Repair or replacement of existing bituminous surfacing or portions of surfacing which has deteriorated. Gravel Roads - Adding moderate amount of gravel, maintenance grading repairs. The City will not special assess for maintenance costs.

40 Assessable Improvements APPURTENANCES Appurtenances are items such as sidewalks, street lighting, or trees that are often encountered during street improvement projects. Policy. Appurtenances to new street construction, street/road reconstruction or resurfacing projects shall be included in the cost of the street/road improvement project and assessed according to those methods and policies. Appurtenances constructed or provided separate from new street/road construction; street/road reconstruction or resurfacing projects shall be assessed consistent with the percentage for the type of improvement on a per unit basis. Special requests shall be assessed 100% of the cost of the improvement.

41 Financing Improvements A. TERMS OF ASSESSMENT The City shall collect payment of special assessments in equal annual installments of principal for the period of years indicated, and as recommended by the City Engineer, from the year of adoption of the assessment roll by the following types of improvements: Sanitary Sewer System Improvements years Water System Improvements years Street System Improvements (street, alley, curb and gutter) years Appurtenances years Other 5-10 years In some cases, improvements that are undertaken could warrant longer or shorter terms. In any event, the assessment term should never exceed the potential life of the improvement.

42 Financing Improvements A. INTEREST RATE The City most often finds itself required to issue debt in order to finance improvements. Such debt requires that the City pay an interest cost to the holders of the debt with such interest cost varying on the timing, bond rating, size and type of bond issue. In addition, the City experiences problems with delinquencies in the payment of assessment by property owners or the inability to invest prepayments of assessments at an interest rate sufficient to meet the interest cost of the debt. These situations create immediate cash flow problems in the timing and ability to make scheduled bond payments. Therefore, for all projects financed by debt issuance, the interest rate charged on assessments shall be 2% greater than the new interest on the bonds issued, or 2% greater than the current investment rate if the project is funded internally.

43 Discussion/Questions?

44 SPECIAL ASSESSMENT POLICY 1

45 SECTION 1: GENERAL POLICY STATEMENT The purpose of this assessment policy is to set forth a guide of policies and procedures to be followed by the City of Minnetrista in making improvements for the general safety, health and welfare of the City, and charging special assessments to finance such improvements. Minnesota State Statutes, Chapter 429, provides that a municipality shall have the power to make public improvements such as sanitary sewer systems, storm sewers, water supply, storage and distribution facilities, street improvements including grading, curb & gutter, surfacing, sidewalks and street lighting. The various procedures that a municipality must follow in regards to financing public improvements are well defined within the law. The special assessment is a device used to finance these public improvements desired by a particular neighborhood or area. The beginnings of use of the special assessment dates back over three hundred years. It has now grown to be an essential and reliable source of municipal revenue. CHARACTERISTICS AND APPLICATIONS Special assessments are defined by three distinct characteristics: 1. They are compulsory charges used to finance particular public improvement projects. 2. The special assessments are charged only against those particular parcels of property deemed to receive some special benefit from the project. 3. The amount of the assessment bears some relationship to the value of the benefits received: (a) (b) the assessment must be confined to property specially benefited; and the amount of the assessments must not exceed the special benefits. In theory, special assessments are frequently regarded as more equitable than property taxes because a more direct benefit is received from the improvements undertaken. Also, special assessments are only imposed on real estate, and they are never levied upon personal and/or movable property. 2

46 Special Assessments have three important applications: 1. Financing New Improvements. The assessments are frequently used to finance the construction of new street/road improvements, sanitary sewer system improvements, water system improvements, storm water system improvements and other appropriate improvements in developing and/or developed areas of the City. 2. Financing Redevelopment. When commercial and residential neighborhoods are confronted with deterioration, special assessments can be utilized in a variety of ways to redevelop and revitalize an area. 3. Financing Major Infrastructure Maintenance Programs. Rehabilitation and reconstruction improvements on streets, sidewalks, sewer systems, water systems and similar facilities can and often should be financed with special assessments. SECTION 2: INTENT The policies contained in this document establish and delineate a procedure for undertaking public improvements and levying special assessments pursuant to Minnesota State Statutes. This policy should be viewed as a starting point for conducting assessments for public improvement projects. When an improvement conveys special benefit to properties in a definable area, the City intends to levy special assessments on those benefited properties to finance such improvements. It shall be the policy of the City of Minnetrista that the amount of the assessment for public improvements should not exceed the special benefit to the property. The City will use the assessment policy to insure that assessments have a reasonable relationship to benefits. Public improvements include the construction and reconstruction of streets, sidewalks, storm sewer, sanitary sewer, water works, street lighting, or any other public improvements allowed by State law. When applying this assessment policy the City Council reserves the right to adjust the policy so as to achieve a more equitable distribution. This may occur in the event that the literal application of the provisions outlined herein would result in an inequitable distribution of special assessments. The City maintains the right to apply this policy differently for the purposes of fairness and equity. It should also be noted that any errors or omissions in this policy are not to be held against the City of Minnetrista. 3

47 SECTION 3: GENERAL ASSESSMENT POLICY TYPES OF IMPROVEMENTS This policy shall relate only to those public improvements allowable under Minnesota State Statutes, Chapter 429. Those public improvements include, but are not limited to, the following: Street improvements; including curb, gutter, grading, graveling, and surfacing Sanitary sewer system improvements Water utility system improvements Storm sewer and drainage systems Appropriate, related landscaping such as planting, trimming, care and removal of trees Sidewalks and Trails Street lighting systems Service charges that are unpaid for the cost of rubbish removal from sidewalks, weed elimination, and the elimination of public health or safety hazards, upon passage of appropriate ordinances. INITIATION OF IMPROVEMENTS The initiation of public improvement projects may occur in one of three ways: Petition of not less than 35% of property owners. An improvement project can begin with a signed petition by the owners of not less than 35% of the frontage of the real property abutting the proposed improvements. This improvement can only be ordered after a public hearing. Petition of 100% of property owners. An improvement project can begin with a signed petition by the owners of 100% of the frontage of the real property abutting the proposed improvements. This improvement does not require a public hearing, and may be ordered by the City Council by a simple majority vote if the petitioning property owners agree to pay 100% of the costs of the improvements. City Council Initiation. No petition is needed. This improvement can only be ordered after a public hearing. The resolution ordering the improvement must be adopted by four-fifths (4/5) vote of the City Council. 4

48 GENERAL DEFINITIONS Project Cost. The project cost of an improvement shall be deemed to include the costs of all necessary construction work required to accomplish the improvement, including expenses incurred or to be incurred in making the improvement that includes engineering, consulting, legal, administration, financing, easements, right-of-way acquisition, and other contingent costs. City Cost. Where the project cost of an improvement is entirely attributable to the need for service to the areas served by said improvement, or whereas unusual conditions beyond the control of the property owners in the area served by the improvement would result in inequitable distribution of special assessments, the City, through the use of other funds, may negotiate such city costs which, in the opinion of the City Council, represents those costs not directly attributable to the area served. Assessable Cost. The assessable cost of an improvement shall be defined as those costs which, in the opinion of the City Council, are attributable to the need for service in the areas served by the improvement and are not in excess of the special benefit conveyed to the property by the improvements. Use of Other Funds. If financial assistance is received from the federal government, from the State of Minnesota, or from any other source to defray a portion of the cost of a given improvement, such aid will first be used to reduce the city cost of the improvement. Project Cost - (City Cost + Use of Other Funds) = Assessable Cost Improvement. An improvement shall be considered a new project or an upgrade of existing systems that the Council determines is necessary for the Community and meets the statutory guidelines for special assessment. Residential Unit (Unit). A unit shall be defined as a platted, buildable, residential parcel occupied or unoccupied, in accordance with Minnetrista zoning and subdivision regulations. City Property. City-owned property, including municipal building sites, parks, nature areas, but not including public streets and alleys (Public Rights of Way), shall be regarded as being assessable on the same basis as if such property was privately owned. Application of Policy. In the event the literal application of the provisions outlined herein would result in an inequitable distribution of special assessments in the opinion of the City Council, the Council reserves the right to adjust the policy so as to achieve a more equitable distribution. 5

49 SECTION 4: METHOD OF ASSESSMENT METHODS OF ASSESSMENT Different methods of assessing property are available to the Council when considering special assessments. However, in general, the Council will use the per unit method unless it is demonstrated that an alternative method (area method, front foot method or some other method that is deemed appropriate and equitable by the City Council) which allows for a fair distribution of the cost. To utilize an alternative method, it is suggested that at least 4/5 of the Council must agree to do so based on demonstrated unusual circumstances of the situation. 1. PER UNIT METHOD The project cost for the local improvement shall be divided by the total number of abutting and/or benefiting properties to arrive at the project assessment rate per unit. For all street/road projects, the City=s policy will be to assess sub-dividable properties on the following basis: ZONING Agriculture Rural Residential R2 - Low (single family) R3 - Low-medium (Townhouse & multi-family) R4 & R5 - Medium (Multi-family) # OF UNITS 1 unit for every 40 acres 1 unit for every 10 acres 2 units per acre 6 units per acre 9 units per acre In all cases, all but one unit may be deferred with interest until such time as the property is developed or at the end of the life of the improvement, whichever occurs first. If the development occurs at less than the number of units deferred, no reduction will be given. 2. AREA METHOD This category includes both the Net Acre method and the Square Foot method. Assessable area shall be expressed in the terms of the number of acres or the number of square feet subject to assessment. 6

50 Net Acre - When using this method, the assessable area of a parcel is multiplied by the per net acre rate to arrive at the assessment amount for that parcel. Square Foot - When using this method, the assessable area of a parcel is multiplied by the per square foot rate to arrive at the assessment amount for that parcel. When determining the assessable area, the following considerations will be given: Lakes, ponds and swamps will be considered part of the assessable area of the parcel. However, the property owner has the option of giving a storm water ponding easement for the land under the lake, pond, or swamp to the City. If such ponding easement is given, a ponding credit equal to the area of the lake, pond, or swamp is to be subtracted from the gross acreage of the parcel before determining other credits. 3. FRONT FOOT METHOD When using this method, the front footage of each parcel to be assessed is calculated. When calculating front footage for unusually shaped lots, the following will apply. Rectangular Lots Cul - De - Sac Lots Lots with Curved Frontage Trapezoidal and Triangular Measure the lot width at the front line Measure the lot width at the front building set back Measure the lot width at the front building setback Measure the lot width at the front and back lot lines, Corner Lots When assessing for streets/utilities, corner lots to be assessed at the front foot method plus 20% of the side street frontage. Each parcel along a project road shall be assigned its current number of development units as permitted under the existing zoning and density standards. This assignment of development units would be exclusive of Agricultural Preserve Status. A parcel currently being used for agricultural purposes may have the special assessment on all but one assessment unit/per 40 acres, postponed until the land is subdivided, developed or ceased being used for agricultural purposes. A parcel that is currently unbuildable (for example no septic available) shall have its assessment(s) postponed until the parcel is buildable. At such time as the property that is the subject of a postponed assessment is developed or becomes buildable, it shall be assessed by the City Council with notice and public hearing pursuant to Minn. Stat All parcels that are subject to a postponed special assessment shall be so identified on the original Special Assessment Roll that is filed with the Count; that 7

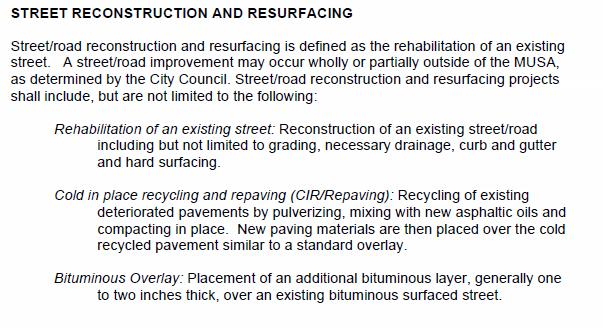

51 additionally, the City Clerk shall make notation of the postponed units within the City. SECTION 5: STREET/ROAD IMPROVEMENTS NEW STREET/ROAD CONSTRUCTION Street/road construction is defined as the initial installation of a permanent street/road into an area, consisting of the necessary grading, base, hard surfacing (bituminous or concrete), and curb and gutter. Policy. It is the intention of the City to install all utilities and utility service lines concurrently with construction of new streets/roads that lie within the MUSA. However, each road needs to be examined on a case by case basis. No street/road construction shall be approved for less than both sides of a street/road except as necessary to complete the improvement of a block that has previous partial completion. A street/road improvement may occur wholly or partially outside of the MUSA, as determined by the City Council. Method of Assessment. The assessable costs for street/road construction shall be distributed among benefited properties on a per unit basis. Assessable Cost. The assessable cost equals 100 percent (100%) of the entire project cost for the street/road construction including intersections, alley openings, and street/road openings. Street/road improvements shall be assessed consistent with the street/road improvement method. STREET RECONSTRUCTION AND RESURFACING Street/road reconstruction and resurfacing is defined as the rehabilitation of an existing street. A street/road improvement may occur wholly or partially outside of the MUSA, as determined by the City Council. Street/road reconstruction and resurfacing projects shall include, but are not limited to the following: Rehabilitation of an existing street: Reconstruction of an existing street/road including but not limited to grading, necessary drainage, curb and gutter and hard surfacing. Cold in place recycling and repaving (CIR/Repaving): Recycling of existing deteriorated pavements by pulverizing, mixing with new asphaltic oils and compacting in place. New paving materials are then placed over the cold recycled pavement similar to a standard overlay. Bituminous Overlay: Placement of an additional bituminous layer, generally one to two inches thick, over an existing bituminous surfaced street. 8

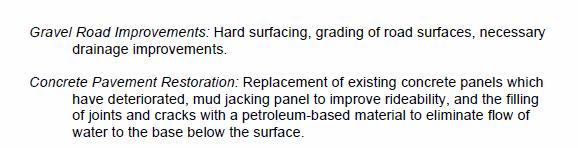

52 Gravel Road Improvements: Hard surfacing, grading of road surfaces, necessary drainage improvements. Concrete Pavement Restoration: Replacement of existing concrete panels which have deteriorated, mud jacking panel to improve rideability, and the filling of joints and cracks with a petroleum-based material to eliminate flow of water to the base below the surface. Method of Assessment. The assessable costs for street/road construction shall be distributed among benefited properties on a per unit basis. For rural street/road improvements, properties that do not directly abut the improvement but benefit from it shall be eligible for whole or partial unit special assessment consideration. Assessable Cost. The assessable cost equals 50 percent (50%) of reconstructing a rural and/or urban street/road and 100 percent (100%) of overlaying a rural/gravel street/road and 100 percent (100%) of milling and overlaying an urban street. Street/road improvements shall be assessed consistent with the street/road improvement method. MAINTENANCE Maintenance is a cost-effective measure to extend the useful street life of a particular roadway and to delay street reconstruction needs. Street/road maintenance may occur wholly or partially outside of the MUSA, as determined by the City Council. Maintenance projects shall include but are not limited to the following: Crack Sealing - Placement of petroleum-based material in the cracks of a bituminous surfaced street for the purpose of eliminating the flow of water from the surface to the aggregate base material below. Bituminous Seal Coating - Placement of petroleum-based material and aggregate on an existing bituminous surfaced street for the purpose of filling cracks and covering mild wear. Bituminous Surfacing Patching - Repair or replacement of existing bituminous surfacing or portions of surfacing which has deteriorated. Gravel Roads - Adding moderate amount of gravel, maintenance grading repairs. The City will not special assess for maintenance costs. 9

53 APPURTENANCES Appurtenances are items such as sidewalks, street lighting, or trees that are often encountered during street improvement projects. Policy. Appurtenances to new street construction, street/road reconstruction or resurfacing projects shall be included in the cost of the street/road improvement project and assessed according to those methods and policies. Appurtenances constructed or provided separate from new street/road construction; street/road reconstruction or resurfacing projects shall be assessed consistent with the percentage for the type of improvement on a per unit basis. Special requests shall be assessed 100% of the cost of the improvement. SECTION 6: SANITARY SEWER AND WATER IMPROVEMENTS SANITARY SEWER AND WATER - SYSTEM, MAINS AND TRUNKS Assessable Costs. New sanitary sewer system, main and trunk improvements and water system, main and trunk improvements are 100% assessed to benefiting properties, within the current staged MUSA, on a per unit basis. Replacement sanitary sewer main and trunk improvements and water main and trunk improvements are 25% assessable costs to benefiting properties, within the current staged MUSA, on a per unit basis. Repair and/or replacement of sanitary sewer and/or water mains and trunks are usually done in conjunction with a street improvement project, when needed. SANITARY SEWER AND WATER - INDIVIDUAL SERVICES For individual services, the City shall maintain and improve, if necessary, all service lines between the individual property line and the city main in the public right-of-way. All service lines from buildings to the property line are the responsibility of the benefited property. Assessable Cost. Individual sanitary and water services are 100% assessable costs for new and 25% for replacement, on a per unit basis. SECTION 7: STORM SEWER SYSTEM IMPROVEMENTS Storm drainage and ponding/basin systems are usually constructed to serve a specific drainage or watershed area. The cost of storm system and drainage improvements shall be 50% for new storm water improvements and 50% for replacement projects, on a per unit basis to benefiting properties. 10

54 The City does collect revenues from the storm water utility and are intended to fund the general operating costs of the storm and drainage system, along with appropriate capital improvements associated with this overall system. SECTION 8: SUPPLEMENTAL ASSESSMENT GUIDELINES A. SUPPLEMENTAL ASSESSMENT AND REASSESSMENT The City Council may, subject to legal notice and hearing requirements, make supplemental assessments to correct omissions, errors, or mistakes in the relating to the total cost of the improvement or any other particular item. If an assessment is set aside by a court for any reason or if the Council finds that the assessment or any part of it is excessive or determines on the advice of the City Attorney that it is or may be invalid for any reason, the Council may upon notice and hearing as required for the original assessment, make a reassessment or a new assessment as to such parcel or parcels. B. TAX-EXEMPT PROPERTY Other than land under city ownership, there are three categories of tax exempt property. Said properties are to be assessed as follows: 1. Tax-exempt property shall be assessed in the same manner as if it were privately owned, subject to the limitations set forth in Minnesota State Statutes, Section , subd.1, as long as the assessments do not exceed the special benefits conferred. 2. State land is subject to assessment based upon procedures set forth in Minnesota State Statutes, Section , subd County land and land owned by all other local taxing jurisdictions is subject to assessment and shall be assessed in the same manner as if it were privately owned, subject to the limitations set forth in Minnesota State Statutes, Section , subd.1, as long as the assessments do not exceed the special benefits conferred. The number of residential equivalent units applied to tax exempt property to determine the special assessment amount shall be calculated at the time of the special assessment. The residential equivalent units shall be based on the type of use and impact of the property on infrastructure relative to residential use and impact. In no case shall the residential equivalent unit be less than one (1). C. COMMERCIAL PROPERTY 11

55 All aspects of this policy apply to commercial property. The number of residential equivalent units applied to commercial property to determine the special assessment amount shall be calculated at the time of the special assessment. The residential equivalent units shall be based on the type of use and impact of the property on infrastructure relative to residential use and impact. In no case shall the residential equivalent unit be less than one (1). D. MULTIPLE DWELLING UNITS Multiple dwelling units are defined for the purposes of this policy as those that consist of two or more dwelling units. All aspects of this policy apply to multiple dwelling units. Each unit in a multiple dwelling unit shall be considered one residential unit. E. TOWNHOUSES AND CONDOMINIUMS All aspects of this policy apply to townhouses and condominiums. Each townhouse and condominium unit shall be considered one residential unit. F. TAX FORFEITURE ASSESSMENTS When a parcel of tax forfeited land is returned to private ownership, and the parcel is benefited by an improvement for which special assessments were canceled because of the forfeiture, the City may, upon notice and hearing as provided for the original assessment, make a reassessment or a new assessment as to the parcel in an amount equal to the remaining unpaid on the original assessment. G. NEW DEVELOPMENTS AND SUBDIVISIONS Policy. It is the policy of the City that new development will not be the sole cause of a special assessment project. The improvement costs of new subdivisions shall be the sole responsibility of the property developer. In addition, it is the policy of the City that all city infrastructure improvements needed due to development will be borne by the developer to reflect the impact of that development on the community. H. ASSESSMENT OF NON-CITY ROADS It is the policy of the City that, in general, non-city street/road projects will not be special assessed. However, the City reserves the right to assess its share of non-city street/road projects. 12

56 SECTION 9: LOCAL IMPROVEMENT PROCESS INITIATION OF PROCEEDINGS Improvement project proceedings may be initiated in any one of the three (3) following ways: Petition by not less than thirty five percent (35%) of the affected property owners determined by front footage. Petition by 100% of the affected property owners. By order of the City Council. PROCEDURAL STEPS FOR PROJECTS WHICH ARE NOT 100% PETITIONED An improvement project that is initiated by action of the City Council or by a 35% petition may be ordered only after a public hearing. The following are the procedural steps that must be followed by the City Council prior to the ordering of an improvement if it is not initiated by a 100% petition. Feasibility Report. Prior to adopting a resolution calling a public hearing on an improvement, the City Council must secure from the City Engineer a report advising it in a preliminary way: a.) b.) as to whether the proposed improvement is feasible; as to whether it should be made as proposed or in connection with some other improvement; and the estimated cost of the improvement. At the discretion of the City Council, an abbreviated, preliminary, feasibility report may be requested prior to the required, full feasibility report for the purpose of assisting in the determination of interest to continue with the project. Resolution Calling Public Hearing. The City Council must adopt a resolution calling a public hearing on the improvement project. Mailed and published notice of the hearing must be given as described in the next paragraph below. The notice of public hearing must include the following information: the time and place of the public hearing; the general nature of the improvements; the estimated costs; and the area proposed to be assessed Mailed Notice of Hearing to Property Owners Proposed to be Assessed. Not less than ten (10) days before the hearing, the notice of hearing must be mailed to the owner of each parcel in the area proposed to be assessed. For purposes of determining who is to receive notice, the owners of the property are those shown on the records of the 13

57 county auditor, or in any county where the City Treasurer mails tax statements. The owners of property that is tax exempt or subject to taxation on a gross earnings basis shall be as certified by any practicable means. Published Notice of Hearing. The notice of public hearing must be published in the city s legal newspaper at least twice, each publication being at least one week apart, with the last publication occurring at least three days prior to the hearing. Resolution Ordering the Improvement. The resolution ordering the improvement must be adopted within six months of the date of the public hearing by a four-fifths vote of the City Council, unless the improvement was initiated by a thirty-five percent (35%) petition, in which event it may be adopted by a majority vote. The resolution may reduce, but not increase, the extent of the improvement as stated in the notice. PROCEDURAL STEPS FOR 100% PETITIONED PROJECTS Improvement projects, which are initiated by a 100% petition, may be ordered by the City Council without a public hearing if the petitioning property owners agree to pay 100% of the costs of the improvements. If any portion of the cost of the improvements including issuance costs of the bonds, such as discount, capitalized interest and legal fees, are not included in the amount assessed, but are to be repaid by an ad valorem property tax levy, a public hearing must be held. The following are the procedural steps for a 100% petitioned project: ISSUANCE OF BONDS Petition. The City Council must receive a petition which is both signed by all of the owners of the real property abutting any street named as the location of the improvement, and states that they agree to pay 100% of the cost of the improvements. Resolution Determining Sufficiency of Petition and Ordering Improvement. Upon receipt of the 100% petition, the City Council must determine that it has been signed by 100% of the owners of the affected property, and that they have agreed to pay 100% of the costs of the improvements. After making this determination, the project may be ordered without a public hearing. At any time after the City Council has ordered the improvements, the City Council may issue its general obligation bonds to finance the cost of the improvements. In the event of any omission, error or mistake in any of the proceedings precedent to the ordering of the improvements, state law provides that the validity of the bonds will not be affected by such deficiencies. However, deficiencies in these proceedings may result in property 14

58 owners successfully appealing the special assessments levied against their property. The resolution authorizing the issuance of the bonds will contain covenants by the City Council that at least 20% of the cost of each improvement project will be specially assessed against the benefited property, and the City Council will take all further actions and proceedings necessary in order for the final and valid levy of special assessments. These two covenants are necessary in order for the bonds to be issued without an election. LETTING CONTRACTS Ordering Plans and Specifications. After the ordering of an improvement project, the City Council must order the preparation of plans and specifications. This may be included as part of the resolution ordering the improvement. Advertisement for Bids. If the estimated cost of the improvement exceeds $25,000, bids must be advertised for in the legal newspaper and such other papers and for such length of time as the City Council deems desirable. If the estimated cost of the improvement exceeds $100,000, the advertisement must be in a paper published in a first class city or in a trade paper not less than three (3) weeks before the last date of the submission of the bids. The notice must contain the following information: the work to be done; the time when the bids will be publicly opened, which must not be less than ten (10) days after the first publication of the advertisement when the estimated cost is less than $100,000, and not less than three (3) weeks after publication in all other cases; and a statement that no bids will be considered unless they are sealed and accompanied by cash, a cashier s check, bid bond, or certified check for such percentage of the bid as specified by the City Council. Award of Contracts. The City Council must either award the contract to the lowest responsible bidder or reject all bids. The contract must be awarded no later than one year after the adoption of the resolution ordering the improvement, unless the resolution ordering improvement specifies a different time limit. If : the initial cost of the entire work does not exceed $25,000; 15

59 if no bid is submitted after advertisement; or if the only bids are higher than the engineer s estimate; the City Council may purchase the materials and order the work done by day labor or in any manner it deems proper. If the estimated cost exceeds $10,000, the work must be supervised by the City Engineer or some other qualified person. SPECIAL ASSESSMENT PROCEDURES The cost of any improvement undertaken in accordance with the procedures set forth in Chapter 429 may be specially assessed, in whole or in part, upon property benefited by the improvement, whether or not the property abuts on the improvement. The area to be assessed may be less than, but not more than, the area proposed to be assessed as stated in the notice of public hearing on the improvement. Resolution Determining Amount to be Specially Assessed. After the expense incurred or to be incurred in the completion of an improvement has been calculated, the City Council must determine the amount it will pay and the amount to be specially assessed. The City Clerk, with the assistance of the engineer or other qualified person, must calculate the amount to be specially assessed against every parcel of land. The assessment roll must be filed with the City Clerk and available for public inspection. Resolution Calling Public Hearing on Assessments. A public hearing on the special assessments must be held following published and mailed notice thereof as described below. The notice of public hearing must include the following information: date, time, and place of the meeting; the general nature of the improvement; the area proposed to be assessed; the total amount of the proposed assessment; that the assessment roll is on file with the City Clerk; that written or oral objections will be considered; that no appeal may be taken as to the amount of the assessments unless a written objection signed by the affected property owner is filed with the City Clerk prior to the hearing or presented to the presiding officer at the hearing; that the owner may appeal the assessment to the district court by serving notice on the Mayor or City Clerk within three (3) working days after the adoption of the assessment and filing notice with the court within ten (10) days after such appeal to the Mayor or City Clerk; and 16

60 any deferment procedures established by the City Council for senior citizens. Published Notice. The notice of the assessment hearing must be published in the legal newspaper at least once, not less than two weeks prior to the hearing. Mailed Notice. The City Clerk must mail notice of the assessment hearing to the owner of each parcel described in the assessment roll at least two weeks prior to the hearing. For purposes of giving mailed notice, the owners shall be those shown on the records of the county auditor, or in any city where tax records are mailed by the City Treasurer. The mailed notice must also include, in addition to the information required to be in the published notice, the following information: the amount to be specially assessed against that particular lot, piece, or parcel of land; adoption by the City Council of the proposed assessment may be taken at the hearing; the right of the property owner to prepay the entire assessment and the person to whom the prepayment must be made; whether partial prepayment of the assessment has been authorized by ordinance; the time within which prepayment may be made without the assessment of interest; and the rate of interest to accrue if the assessment is not prepaid within the required time period. Adoption of Assessments. At the hearing or any adjournment thereof, the City Council may adopt the assessments as proposed or adopt the assessments with amendments. If the adopted assessment differs from the proposed assessment, the City Clerk must mail the owner a notice stating the amount of the adopted assessment. Owners must also be notified by mail of any changes in interest rates or prepayment provisions from those contained in the notice of the proposed assessment. Overview of Assessment Adoption Procedure. 1. The City will present its case first by calling witnesses who may testify by narrative or by examination, and by the introduction of exhibits. After all of the City's witnesses have testified, the contesting party or parties will be allowed to ask questions. This procedure will be repeated with each witness until neither side has further questions. Then the Council may ask questions. 17

61 2. After the City has presented all its evidence, any objector may call witnesses or present such testimony as the objector desires. The same procedure for questioning of the City's witnesses will be followed with the objectors' witnesses. 3. The objectors may be represented by counsel. 4. Minnesota rules of evidence will not be strictly applied; however, they may be considered and argued to the Council as to the weight of items of evidence or testimony presented to the Council. 5. The entire proceedings will be video-taped. 6. At the close of presentation of evidence, the objectors may make a final presentation to the Council based on the evidence and the law. No new evidence may be presented at this point. 7. The Council will either adopt the proposed special assessment at the hearing, reduce the assessment or continue the hearing. Transmittal of Assessments to the County Auditor. After the adoption of the assessment, the City Clerk must transmit a certified duplicate copy of the assessment roll to the county auditor. In the alternative, the City Council may direct the City Clerk to file the assessment roll in the Clerk=s office and to certify annually to the county auditor, on or before October 10th in each year, the total installments of principal and interest thereon to become due in the following year. With the certification of the assessments to the county auditor, the procedures under Minnesota State Statutes, Chapter 429 are complete. SECTION 10: SPECIAL ASSESSMENTS FOR CURRENT SERVICES The City Council may provide for the collection of certain service charges as a special assessment against the property benefiting from the service. Special charges that may be assessed include, but are not limited to, those as defined by State Statutes. SECTION 11: CONDITIONS OF PAYMENT OF ASSESSMENTS Minnesota State Statutes, Chapter 429, provide the City with considerable discretion in establishing the terms and conditions of payment of special assessment by property owners. Chapter 429 does establish two precise requirements regarding payment. First, the property owner has thirty (30) days from the date of adoption of the assessment roll to pay the assessment in full without interest charge ( , subd. 3). 18

62 Second, all assessments shall be payable in equal annual installments extending over a period not exceeding thirty (30) years from the date of adoption of the assessment roll ( , subd. 2). The conditions of payment established in this section follow the requirements of Chapter 429 and seek to balance the burden of payment of the property owner with the financing requirements imposed by debt issuance. A. TERMS OF ASSESSMENT The City shall collect payment of special assessments in equal annual installments of principal for the period of years indicated, and as recommended by the City Engineer, from the year of adoption of the assessment roll by the following types of improvements: Sanitary Sewer System Improvements years Water System Improvements years Street System Improvements (street, alley, curb and gutter) years Appurtenances years Other 5-10 years In some cases, improvements that are undertaken could warrant longer or shorter terms. In any event, the assessment term should never exceed the potential life of the improvement. B. INTEREST RATE The City most often finds itself required to issue debt in order to finance improvements. Such debt requires that the City pay an interest cost to the holders of the debt with such interest cost varying on the timing, bond rating, size and type of bond issue. In addition, the City experiences problems with delinquencies in the payment of assessment by property owners or the inability to invest prepayments of assessments at an interest rate sufficient to meet the interest cost of the debt. These situations create immediate cash flow problems in the timing and ability to make scheduled bond payments. Therefore, for all projects financed by debt issuance, the interest rate charged on assessments shall be 2% greater than the new interest on the bonds issued, or 2% greater than the current investment rate if the project is funded internally. PREPAYMENT AND ASSESSMENT CERTIFICATION Partial Prepayment. After the adoption by the City Council of the assessment roll in any local improvement proceeding, the owner of any property specially assessed in the proceeding may, prior, to the certification of the assessment of the first installment to the County Auditor, pay to the City any portion of the assessment. The remaining unpaid balance shall be spread over the period of time established by the Council for installment 19

63 payment of the assessment. Certification of Assessments. After the adoption of any special assessment by the City Council, the City Clerk shall transmit a certified duplicate of the assessment roll with each installment, including interest, set forth separately to the County Auditor on an annual basis to be extended on the proper tax lists to the County. SECTION 12: HARDSHIP DEFERRALS Minnesota Statutes, sections , et seq. allow the City, at its discretion, to defer the payment of any special assessment for any homestead property owned by a person 65 years of age or older or retired by virtue of a permanent and total disability for whom it would be a hardship to make the payments or owned by a person who is a member of the Minnesota National Guard or other military reserves who is ordered into active military service, as defined in Minnesota Statutes, section , subd. 5b or 5c, as stated in the person s military orders, for whom it would be a hardship to make the payments. Any such person is hereinafter referred to as a Qualified Person. POLICY In determining whether a Qualified Person is eligible for deferral of special assessment installment payments, the following criteria are established: Effective Date. Special assessment hardship deferral for the above reasons applies to special assessments levied after the date of this Policy. Application. Special assessment hardship deferral applies to qualifying special assessments against all properties classified as homestead pursuant to Minnesota State Statutes, Chapter 273, where one or more owner of such property is a Qualified Person and for whom it would be a hardship to pay the special assessment installments as they become due. Hardship Defined. No person shall be deemed to have a hardship unless his or her income, as determined by the applicant s most recent federal or state income tax return, is no more than 60 percent of the median income for the Minneapolis-St. Paul metropolitan area, as determined by the United States Department of Housing and Urban Development, adjusted for family size, and the average annual assessment installment exceeds 3 percent (3%) of the previous year s total adjusted gross incomes, for Federal Income Tax purposes, for all owners of the property. In no event shall total adjusted gross income include Social Security benefits, railroad retirement benefits, retirement benefits attributable to employee contributions, disability benefits, personal injury awards or workmen s compensation payments; and all owners of the property verify, under oath, that they meet the criteria for establishing a hardship by completing an application provided by the City. 20

64 Existence of a Disability. The existence of a disability shall be determined under the criteria of the United States Social Security Administration. Exceptional Cases. In cases where exceptional and unusual circumstances exist, the City Council may determine that a hardship exists despite the fact that the minimum income requirements as defined in this section do not exist. Such cases shall be decided by the City Council on a case-by-case basis. INTEREST Interest will be charged on any assessment deferred pursuant to this policy at a rate equal to the rate charged on other assessments for the particular public improvement project that the assessment is financing. If the assessment is not associated with a public improvement project, the rate of interest shall be determined by the City Council at its discretion. Interest, compounded annually, will accrue from the date of adoption of the assessment. TERMINATION OF DEFERMENT The option to defer the payment of special assessments pursuant to this Policy shall terminate and all installment amounts previously deferred, plus applicable interest, shall become due upon the occurrence of any of the following events: a) Request of a Qualifying Person; b) Death of a Qualifying Person, providing the surviving spouse is otherwise not eligible for the deferral; c) Sale, transfer, or subdivision of the property or any part thereof; d) The property, for any reason, loses its homestead status; or e) The City, for any reason, determines that there would be no hardship to require immediate or partial payment. SECTION 13: FINANCING AUTHORITY At any time after one or more improvements are ordered, the City Council may issue obligations in such amount as it deems necessary to defray in whole or in part the costs incurred and estimated to be incurred in making the improvements. 21

65 TYPES OF OBLIGATIONS Obligations used to finance public improvement projects are called improvement bonds. The proceeds from the sale of the improvement bonds are used to fund project costs. The improvement bonds are then paid off as the funds become available through collection of special assessments and any taxes levied for that purpose. Improvement bonds carry the City s general obligation pledge. METHOD OF ISSUANCE All improvement bonds shall be issued in accordance with the provisions of Minnesota State Statutes, Chapter 475. If twenty percent (20%) or more of the cost of the improvement or improvements is to be assessed against benefited properties, no election is required prior to issuing the improvement bonds and the improvement bonds do not count against the City s statutory debt limit. CONSOLIDATING PROJECT FINANCING If several public improvements are being carried out at the same time, the City Council reserves the right to consolidate all necessary financings into one improvement project for the purpose of issuing improvement bonds. This election will be made at the time of the public hearing on the improvements. 22

66 WS Item 3 CITY OF MINNETRISTA WORK SESSION DISCUSSION ITEM Subject: Prepared By: Through: Gene Lehner Playground Equipment Replacement and ADA Compliance Improvements Nickolas Olson, City Planner David Abel, Community Development Director Meeting Date: May 21, 2018 Overview: The playground equipment at Gene Lehner Park is proposed to be replaced as part of the 2018 Parks Capital Improvement Plan. The proposed improvements, however, trigger the requirement to bring the park into compliance with ADA requirements which will add additional costs to the project not accounted for in the budget. Discussion: Installing a new playground into the park means that the playground needs to meet current safety and accessibility guidelines, otherwise the City could face liability issues. In order for any amenity to be fully compliant it has to have proper access to it. The options include: Option #1: Install the new playground and then provide a document that states the following: 1. Identify the barriers / non-compliant features (parking, trail, etc.) 2. Identify the proposed solution for making it compliant (new trail route, parking stall) 3. Identify the party responsible for making it compliant (City) 4. Identify potential dates or timeframe for removal of barriers / becoming compliant Option #2: Create an overall site plan that includes brings the site into compliance. Due to the grade differences at the site, we would recommend looking at a means to identify a HC stall in the parking bay and creating an accessible route up to the playground, as well as the tennis court, so this park has fully accessible amenities. By just installing the new playground as shown it could be concerning that it could prohibit a creative solution to getting that trail up the hill. Maybe a different shaped container with trails that wind through it would provide a more creative approach. It may require broader site modifications, but could be interesting when complete. In the 2018 Parks Capital Improvement Plan, $125,000 was budgeted for the playground replacement. That included $60,000 for the equipment and $65,000 for site work, Mission Statement: The City of Minnetrista will deliver quality services in a cost effective and innovative manner and provide opportunities for a high quality of life while protecting natural resources and maintaining a rural character.

67 removals, etc. but did not included any ADA compliance items. A preliminary scope of work for ADA compliance anticipates between $7,500 and $11,000 for project design. Without having a design and plan in place, it is difficult to establish a cost for project implementation, but a range of between $75,000 and $150,000 is likely to be expected. Staff has begun the process of receiving quotes for the replacement of the playground equipment and associated site work at Gene Lehner Park. To date, staff has received one quote for $70,000 for installing the playground equipment and $54,155 for site work, removals, etc. If the Council determines they wish to postpone the improvements to Gene Lehner Park, the next city park that Staff would recommend looking into would be Friendship Park in the Painters Creek neighborhood. The cost of improvements to the park should be similar to the amount budgeted for Conclusion: The City Council has a few options with regards to the direction it could take with the proposed improvements to Gene Lehner Park as included in the 2018 Parks Capital Improvement Plan. Those options are as follows: 1. Proceed with installing new playground equipment and develop a document that outlines a timeframe for compliance; 2. Proceed with installing new playground equipment and making the park ADA compliant at the same time; or 3. Proceed to install new playground equipment in a different city park, specifically Friendship Park. Recommended Action: Staff is seeking direction from the City Council on how to proceed with the planned improvements to Gene Lehner Park given the additional, unforeseen costs associated with making the park ADA compliant. Mission Statement: The City of Minnetrista will deliver quality services in a cost effective and innovative manner and provide opportunities for a high quality of life while protecting natural resources and maintaining a rural character.

68 Hennepin County Natural Resources Map Date: 5/17/2018 Legend 2 Foot Elevation Contours Index Intermediate PID: Address: 4180 TRILLIUM LA E, MINNETRISTA Owner Name: CITY OF MINNETRISTA Acres: 1.73 Comments: Gene Lehner Park 1 inch = 100 feet This data (i) is furnished 'AS IS' with no representation as to completeness or accuracy; (ii) is furnished with no warranty of any kind; and (iii) is notsuitable for legal, engineering or surveying purposes. Hennepin County shall not be liable for any damage, injury or loss resulting from this data. COPYRIGHT HENNEPIN COUNTY 2018

69

70

71

72

73

74

75

76 Hennepin County Natural Resources Map Date: 5/17/2018 Legend 2 Foot Elevation Contours Index Intermediate PID: Address: 5676 KRAMER RD, MINNETRISTA Owner Name: CITY OF MINNETRISTA Acres: 0.58 Comments: Friendship Park 1 inch = 50 feet This data (i) is furnished 'AS IS' with no representation as to completeness or accuracy; (ii) is furnished with no warranty of any kind; and (iii) is notsuitable for legal, engineering or surveying purposes. Hennepin County shall not be liable for any damage, injury or loss resulting from this data. COPYRIGHT HENNEPIN COUNTY 2018

77

78

79

80

81

CITY OF CIRCLE PINES SPECIAL ASSESSMENT POLICY

CITY OF CIRCLE PINES SPECIAL ASSESSMENT POLICY Policy 53 Revised 02/10/2015 SECTION 1: GENERAL POLICY STATEMENT The purpose of this assessment policy is to set forth a guide of policies and procedures

CITY OF CIRCLE PINES SPECIAL ASSESSMENT POLICY Policy 53 Revised 02/10/2015 SECTION 1: GENERAL POLICY STATEMENT The purpose of this assessment policy is to set forth a guide of policies and procedures

CITY OF MARSHALL SPECIAL ASSESSMENT POLICY (Originally Adopted: October 18, 2004) (First Revision: August 1, 2005)

(First Revision: August 1, 2005)") RESOLUTION NUMBER 2946, SECOND SERIES RESOLUTION AMENDING RESOLUTION NUMBER 2757, SECOND SERIES RESOLUTION AMENDING RESOLUTION NUMBER 2673, SECOND SERIES ESTABLISHING AND PROVIDING FOR THE CITY OF MARSHALL

RESOLUTION NUMBER 2946, SECOND SERIES RESOLUTION AMENDING RESOLUTION NUMBER 2757, SECOND SERIES RESOLUTION AMENDING RESOLUTION NUMBER 2673, SECOND SERIES ESTABLISHING AND PROVIDING FOR THE CITY OF MARSHALL

CITY OF EAU CLAIRE, WISCONSIN. SPECIAL ASSESSMENT POLICY (Dated: November 8, 2016)

") CITY OF EAU CLAIRE, WISCONSIN SPECIAL ASSESSMENT POLICY (Dated: November 8, 2016) (Adopted by reference by Ordinance No. 7207 adopted November 8, 2016) PURPOSE The purpose of this Policy is to assure fair

CITY OF EAU CLAIRE, WISCONSIN SPECIAL ASSESSMENT POLICY (Dated: November 8, 2016) (Adopted by reference by Ordinance No. 7207 adopted November 8, 2016) PURPOSE The purpose of this Policy is to assure fair

ORDINANCE NO AN ORDINANCE AMENDING THE CODE OF ORDINANCES OF THE CITY OF PORT ARANSAS, TEXAS, BY ADOPTING A NEW CHAPTER

ORDINANCE NO. 2008-09 AN ORDINANCE AMENDING THE CODE OF ORDINANCES OF THE CITY OF PORT ARANSAS, TEXAS, BY ADOPTING A NEW CHAPTER TWENTY-SIX CONCERNING IMPACT FEES FOR ROADWAY FACILITIES; INCORPORATING

ORDINANCE NO. 2008-09 AN ORDINANCE AMENDING THE CODE OF ORDINANCES OF THE CITY OF PORT ARANSAS, TEXAS, BY ADOPTING A NEW CHAPTER TWENTY-SIX CONCERNING IMPACT FEES FOR ROADWAY FACILITIES; INCORPORATING

Chapter 3 FINANCE, TAXATION, AND PUBLIC RECORDS

Chapter 3 FINANCE, TAXATION, AND PUBLIC RECORDS 3.01 Preparation of Tax Roll and Receipts 3.02 Fiscal Year 3.03 Allowance of Claims 3.04 Budget 3.05 Village Borrowing 3.06 Monthly Reports of Receipts 3.07

Chapter 3 FINANCE, TAXATION, AND PUBLIC RECORDS 3.01 Preparation of Tax Roll and Receipts 3.02 Fiscal Year 3.03 Allowance of Claims 3.04 Budget 3.05 Village Borrowing 3.06 Monthly Reports of Receipts 3.07

City of Edwardsville, Kansas Special Benefit District Policy

City of Edwardsville, Kansas Special Benefit District Policy Date Adopted: September 12, 2011 Section 1. Objective The objective is to establish a policy to finance public streets, sanitary sewers, water

City of Edwardsville, Kansas Special Benefit District Policy Date Adopted: September 12, 2011 Section 1. Objective The objective is to establish a policy to finance public streets, sanitary sewers, water

NC General Statutes - Chapter 153A Article 9 1

Article 9. Special Assessments. 153A-185. Authority to make special assessments. A county may make special assessments against benefited property within the county for all or part of the costs of: (1)

Article 9. Special Assessments. 153A-185. Authority to make special assessments. A county may make special assessments against benefited property within the county for all or part of the costs of: (1)

Guide to Special Assessments

South Dakota Municipal League Guide to Special Assessments Special Assessments are a financing mechanism that allow payment for improvements by those who benefit, or for specific items, rather than general

South Dakota Municipal League Guide to Special Assessments Special Assessments are a financing mechanism that allow payment for improvements by those who benefit, or for specific items, rather than general

LETTER OF TRANSMITTAL

Victoria Simonsen, City Manager 221 East Clark Street Albert Lea, Minnesota 56007 Honorable Mayor & City Council City of Albert Lea Freeborn County, Minnesota ASSESSMENT POLICY April, 2006 Submitted to

Victoria Simonsen, City Manager 221 East Clark Street Albert Lea, Minnesota 56007 Honorable Mayor & City Council City of Albert Lea Freeborn County, Minnesota ASSESSMENT POLICY April, 2006 Submitted to

ST. JOSEPH TOWNSHIP RESOLUTION CITY OF ST. JOSEPH RESOLUTION 2018-

ST. JOSEPH TOWNSHIP RESOLUTION 2018- CITY OF ST. JOSEPH RESOLUTION 2018- JOINT RESOLUTION FOR DESIGNATION OF AN AREA FOR ORDERLY ANNEXATON AND FOR DESIGNATION OF AN AREA FOR IMMEDIATE ANNEXATION PURSUANT

ST. JOSEPH TOWNSHIP RESOLUTION 2018- CITY OF ST. JOSEPH RESOLUTION 2018- JOINT RESOLUTION FOR DESIGNATION OF AN AREA FOR ORDERLY ANNEXATON AND FOR DESIGNATION OF AN AREA FOR IMMEDIATE ANNEXATION PURSUANT

SERVICE AND ASSESSMENT PLAN CITY OF HASLET PUBLIC IMPROVEMENT DISTRICT NO. 2 SERVICE AND ASSESSMENT PLAN August 3, \ v

SERVICE AND ASSESSMENT PLAN CITY OF HASLET PUBLIC IMPROVEMENT DISTRICT NO. 2 SERVICE AND ASSESSMENT PLAN August 3, 2015 CITY OF HASLET PUBLIC IMPROVEMENT DISTRICT NO. 2 SERVICE AND ASSESSMENT PLAN Table

SERVICE AND ASSESSMENT PLAN CITY OF HASLET PUBLIC IMPROVEMENT DISTRICT NO. 2 SERVICE AND ASSESSMENT PLAN August 3, 2015 CITY OF HASLET PUBLIC IMPROVEMENT DISTRICT NO. 2 SERVICE AND ASSESSMENT PLAN Table

Okaloosa County BCC. Okaloosa County BCC. MSBU / MSTU Policy. Municipal Service Benefit Units Municipal Service Taxing Units.

Okaloosa County BCC Okaloosa County BCC MSBU / MSTU Policy Municipal Service Benefit Units Municipal Service Taxing Units Revised 5/6/2014 Table of Contents INTRODUCTION... 1 MSBU CALENDAR YEAR SCHEDULE...

Okaloosa County BCC Okaloosa County BCC MSBU / MSTU Policy Municipal Service Benefit Units Municipal Service Taxing Units Revised 5/6/2014 Table of Contents INTRODUCTION... 1 MSBU CALENDAR YEAR SCHEDULE...

S U B D I V I S I O N AGREEMENT

S U B D I V I S I O N AGREEMENT THIS AGREEMENT made this 17th day of January, 2006, by and between Peachtree Properties, L.L.C., (hereinafter referred to as "Developer"); SANITARY AND IMPROVEMENT DISTRICT

S U B D I V I S I O N AGREEMENT THIS AGREEMENT made this 17th day of January, 2006, by and between Peachtree Properties, L.L.C., (hereinafter referred to as "Developer"); SANITARY AND IMPROVEMENT DISTRICT

CHAPTER 14: DRIVEWAYS, TOWN HIGHWAYS, AND PRIVATE ROADS

CHAPTER 14: DRIVEWAYS, TOWN HIGHWAYS, AND PRIVATE ROADS TABLE OF CONTENTS CHAPTER 14: PRIVATE DRIVEWAYS, TOWN HIGHWAYS AND PRIVATE ROADS 14-1 14.0100 AUTHORITY... 14-1 14.0200 TITLE... 14-1 14.0300 REGULATION

CHAPTER 14: DRIVEWAYS, TOWN HIGHWAYS, AND PRIVATE ROADS TABLE OF CONTENTS CHAPTER 14: PRIVATE DRIVEWAYS, TOWN HIGHWAYS AND PRIVATE ROADS 14-1 14.0100 AUTHORITY... 14-1 14.0200 TITLE... 14-1 14.0300 REGULATION

HOUSE BILL lr1125 A BILL ENTITLED. St. Mary s County Metropolitan Commission Fee Schedule

L HOUSE BILL lr By: St. Mary s County Delegation Introduced and read first time: February, 0 Assigned to: Environmental Matters A BILL ENTITLED AN ACT concerning St. Mary s County Metropolitan Commission

L HOUSE BILL lr By: St. Mary s County Delegation Introduced and read first time: February, 0 Assigned to: Environmental Matters A BILL ENTITLED AN ACT concerning St. Mary s County Metropolitan Commission

ESCAMBIA COUNTY MUNICIPAL SERVICES BENEFITS UNITS GUIDELINES AND PROCEDURES

ESCAMBIA COUNTY MUNICIPAL SERVICES BENEFITS UNITS GUIDELINES AND PROCEDURES Adopted by the Escambia County Board of County Commissioners July 28, 1998 INTRODUCTION The Escambia County Board of County Commissioner's

ESCAMBIA COUNTY MUNICIPAL SERVICES BENEFITS UNITS GUIDELINES AND PROCEDURES Adopted by the Escambia County Board of County Commissioners July 28, 1998 INTRODUCTION The Escambia County Board of County Commissioner's

BY-LAW NO OF THE COUNTY OF GRANDE PRAIRIE NO. 1

BY-LAW NO. 2702 OF THE COUNTY OF GRANDE PRAIRIE NO. 1 A By-law of the County of Grande Prairie, in the Province of Alberta to impose and collect off-site levies for new or expanded roads required for or

BY-LAW NO. 2702 OF THE COUNTY OF GRANDE PRAIRIE NO. 1 A By-law of the County of Grande Prairie, in the Province of Alberta to impose and collect off-site levies for new or expanded roads required for or

SUBDIVISION DESIGN PRINCIPLES AND STANDARDS

SECTION 15-200 SUBDIVISION DESIGN PRINCIPLES AND STANDARDS 15-201 STREET DESIGN PRINCIPLES 15-201.01 Streets shall generally conform to the collector and major street plan adopted by the Planning Commission

SECTION 15-200 SUBDIVISION DESIGN PRINCIPLES AND STANDARDS 15-201 STREET DESIGN PRINCIPLES 15-201.01 Streets shall generally conform to the collector and major street plan adopted by the Planning Commission

ORDINANCE NO

ORDINANCE NO. 2014-160 AN ORDINANCE OF THE CITY COUNCIL OF THE CITY OF MENIFEE, CALIFORNIA, REPEALING SECTION 10.35 OF RIVERSIDE COUNTY LAND USE ORDINANCE NO. 460.152 AS ADOPTED BY THE CITY OF MENIFEE

ORDINANCE NO. 2014-160 AN ORDINANCE OF THE CITY COUNCIL OF THE CITY OF MENIFEE, CALIFORNIA, REPEALING SECTION 10.35 OF RIVERSIDE COUNTY LAND USE ORDINANCE NO. 460.152 AS ADOPTED BY THE CITY OF MENIFEE

CHARTER OF THE TOWN OF HANOVER, N.H.

CHARTER OF THE TOWN OF HANOVER, N.H. 1963 N.H. Laws Ch. 374, as amended Section 1. Definitions. The following terms, wherever used or referred to in this chapter, shall have the following respective meanings,

CHARTER OF THE TOWN OF HANOVER, N.H. 1963 N.H. Laws Ch. 374, as amended Section 1. Definitions. The following terms, wherever used or referred to in this chapter, shall have the following respective meanings,

CITY OF MADISON, WISCONSIN

CITY OF MADISON, WISCONSIN A SUBSTITUTE ORDINANCE Amending Secs. 4.09(13), 16.23(8)(f), 16.23(9)(e), 20.04(18)(a), 20.06, and 20.09 relating to the imposition and collection of subdivision service costs

CITY OF MADISON, WISCONSIN A SUBSTITUTE ORDINANCE Amending Secs. 4.09(13), 16.23(8)(f), 16.23(9)(e), 20.04(18)(a), 20.06, and 20.09 relating to the imposition and collection of subdivision service costs

ARTICLE SINGLE FAMILY SITE CONDOMINIUM DEVELOPMENT STANDARDS

ARTICLE 28.00 SINGLE FAMILY SITE CONDOMINIUM DEVELOPMENT STANDARDS Section 28.01 PURPOSE The purpose of this Article is to recognize that conventional single family developments, traditionally developed

ARTICLE 28.00 SINGLE FAMILY SITE CONDOMINIUM DEVELOPMENT STANDARDS Section 28.01 PURPOSE The purpose of this Article is to recognize that conventional single family developments, traditionally developed

CHAPTER Senate Bill No. 2222

CHAPTER 98-167 Senate Bill No. 2222 An act relating to taxation; amending s. 197.122, F.S.; specifying the time within which property appraisers may correct a material mistake of fact in an appraisal;

CHAPTER 98-167 Senate Bill No. 2222 An act relating to taxation; amending s. 197.122, F.S.; specifying the time within which property appraisers may correct a material mistake of fact in an appraisal;

ORDINANCE NUMBER 1154

ORDINANCE NUMBER 1154 AN ORDINANCE OF THE CITY COUNCIL OF THE CITY OF PERRIS ACTING AS THE LEGISLATIVE BODY OF COMMUNITY FACILITIES DISTRICT NO. 2005-1 (PERRIS VALLEY VISTAS) OF THE CITY OF PERRIS AUTHORIZING

ORDINANCE NUMBER 1154 AN ORDINANCE OF THE CITY COUNCIL OF THE CITY OF PERRIS ACTING AS THE LEGISLATIVE BODY OF COMMUNITY FACILITIES DISTRICT NO. 2005-1 (PERRIS VALLEY VISTAS) OF THE CITY OF PERRIS AUTHORIZING

FOCUS ENGINEERING, inc.

FEASIBILITY REPORT for OLD VILLAGE PHASE 3 STREET, DRAINAGE AND UTILITY IMPROVEMENTS RESOULTION RECEIVING REPORT AND CALLING FOR PUBLIC HEARING OLD VILLAGE CIP PHASING PLAN Phase 3 2017. Amount: $ 2,557,000.

FEASIBILITY REPORT for OLD VILLAGE PHASE 3 STREET, DRAINAGE AND UTILITY IMPROVEMENTS RESOULTION RECEIVING REPORT AND CALLING FOR PUBLIC HEARING OLD VILLAGE CIP PHASING PLAN Phase 3 2017. Amount: $ 2,557,000.

SECTION WATER SYSTEM EXTENSION

SECTION 10.00 WATER SYSTEM EXTENSION 10.01 General Statement: The Board shall make or cause to be made such extension, or replacements, to the water transmission and distribution system of the Board as

SECTION 10.00 WATER SYSTEM EXTENSION 10.01 General Statement: The Board shall make or cause to be made such extension, or replacements, to the water transmission and distribution system of the Board as

DISTRICT OF SICAMOUS BYLAW NO A bylaw of the District of Sicamous to establish a Revitalization Tax Exemption Program

DISTRICT OF SICAMOUS BYLAW NO. 917 A bylaw of the District of Sicamous to establish a Revitalization Tax Exemption Program WHEREAS under the provisions of Section 226 of the Community Charter, the Council

DISTRICT OF SICAMOUS BYLAW NO. 917 A bylaw of the District of Sicamous to establish a Revitalization Tax Exemption Program WHEREAS under the provisions of Section 226 of the Community Charter, the Council

SUBDIVISION REGULATIONS

CHAPTER 14 SUBDIVISION REGULATIONS 14-100 Provisions 14-200 Preliminary Plat 14-300 Final Plat 14-400 Replat 14-500 Minor Subdivision 14-600 Administrative Replat 14-700 Vacation of Roadways, Public Easements,

CHAPTER 14 SUBDIVISION REGULATIONS 14-100 Provisions 14-200 Preliminary Plat 14-300 Final Plat 14-400 Replat 14-500 Minor Subdivision 14-600 Administrative Replat 14-700 Vacation of Roadways, Public Easements,

AVENIR COMMUNITY DEVELOPMENT DISTRICT