Typical Valuation Approaches and How to Deal With Them

|

|

|

- Gilbert Carroll

- 5 years ago

- Views:

Transcription

1 Typical Valuation Approaches and How to Deal With Them January, 2018 Anthony F. DellaPelle, Esq., CRE Shareholder, McKirdy, Riskin, Olson & DellaPelle, P.C. Morristown, New Jersey Christian F. Torgrimson, Esq. Managing Partner, Pursley Friese Torgrimson Atlanta, Georgia

2 Just & Adequate Compensation For the taking and damaging of property rights and interests Intended to make the owner whole Measured by Fair Market Value: the price a willing buyer and willing seller come to when neither is being compelled to act

3 Elements of Just and Adequate Compensation YES Land Buildings Improvements Trade Fixtures FF&E Leasehold/Fee Easements & Rights NO Temporary damage Contract Rights Supplier Claims Loss of income/sales Loss of customers Traffic patterns Medians Sentimental value

4 Sales Comparison or Market Data Approach The Three Approaches to Value Cost Approach Income Approach 4

5 Highest and Best Use drives the approach: Applying Approaches to Value Is if physically possible? Is it legally permissible? Is it financially feasible? Is it max productive?

6 Sales Comparison Approach 6

7 Sales Comparison Approach Elements of Comparison Real property rights conveyed Financing terms Conditions of sale Physical characteristics and condition of property Market conditions at time of sale Location Use/zoning/approvals highest and best use of the sale vs. subject

8 Sales Comparison Approach: Apples to Apples

9 Sales Comparison Data Sheets

10 The Not So Easy Comparable

11 Sales Comparison Approach: Adjusting the Comps Quantitative vs. Qualitative Adjustments? What is the basis for the adjustments? Are they net opinions? Does the size of each adjustment matter? How is FMV derived from the range of adjusted sales? Do adjustments reflect true nature of the subject property?

12 Sales Comparison Approach

13 Cost Approach The cost approach is based on the understanding that market participants relate value to cost. Value of a property is derived by adding the estimated value of the land to the current cost of constructing a reproduction or replacement for the improvements, and then subtracting the amount of depreciation in the structures from all causes. Entrepreneurial profit and/or incentive may be included in the value indication. Land value is derived through a comparable sales/market approach Source(s) of current cost cost estimators, cost manuals, builders and contractors. Not replacement value Depreciation physical deterioration, functional obsolescence and external obsolescence measured through market research and the application of specific procedures. Cost approach is particularly useful in valuing new or nearly new improvements and special purpose properties that are not frequently exchanged in the market. Can also be employed to derive information needed in the sales comparison and income capitalization approaches to value, such as an adjustment for the cost to cure items of deferred maintenance. 13

14 Cost Approach Replacement costs Less depreciation Plus value of land as vacant

15 Income Capitalization Approach Based on conversion of income and capitalization into property value Often summarized as the present value of future benefits Example: An asset produces $5,000 of net income per year What is the value of that asset? If the rate of return is known to be 5%, then the value is $100,000 S5,000 income/ 5% = $100,000 If the rate of return is known to be 10%, then the value is $50,000 $5,000 income/10% = $50,000 15

16 Income Capitalization Approach Properties that generate positive cash flow/income can be appraised using a present value or time value of money concept. The income approach estimates the present value of (a) future income generated by a property and (b) its eventual resale value. The term capitalization refers to the mechanism by which future income can be converted into a present value. Direct capitalization: A capitalization rate or income multiplier is derived by considering the relationship between one year s income and value. Yield capitalization: Uses yield rate to reflect determine present value by considering the relationship between several years stabilized income and a reversionary value at the end of a designated period. Sometimes referred to as a discounted cash flow or DCF analysis. Courts prefer direct capitalization over yield or DCF methods as the latter is deemed speculative 16

17 Income Capitalization Approach Rental income key factors Contract rent vs. market rent Gross, modified gross, net, triple net Which are common for the type of real estate being appraised? Are there comps and what types of leases are they? Can you utilize both gross and net leases as comps? How do you handle comps with rent escalations? Options? Rent abatements/tenant improvements and impact upon effective rent How to handle excess rent or percentage rents 17

18 Income Capitalization Approach Potential Gross Income = total income based upon full occupancy before expenses Effective Gross Income = total income adjusted for vacancy and collection losses How do you handle a property which is 100% occupied? 100% vacant? Net Operating Income ( NOI ) = anticipated net income after expenses This is the income which is then capitalized to derive FMV Expenses those necessary to maintain the property and continue income production Actual or economic? Fixed expenses Variable expenses Reserves and replacement allowance 18

19 Income Capitalization Approach Capitalization rates key factors Risk Prospective rate of return basis therefor Financing available Economic issues/impacts Direct Capitalization Value (V) = Income (I)/Capitalization Rate (R) Employs cap rates extracted from sales preferred method Use of market reports/investor surveys Use of band of investment to identify equity capitalization rate vs. mortgage component Only first year of income is considered When market date scarce or unavailable, mortgage equity techniques should only be used to TEST capitalization rates, not to develop them. Appraisal of Real Estate, CITE 19

20 Income Capitalization Approach Direct Capitalization: technique is often referred to as Direct Cap or using a Cap Rate. Direct capitalization requires data concerning comparable sales and their income generation. Consider the following chart: Each of the three sales sold for 10 times their annual income. Therefore the market recognizes 10 times annual income for properties of this type. The Cap Rate is the inverse of an income multiplier. If an income multiplier is 10x, which is the same thing as 10/1, then the cap rate is 10% (1 divided by 10). Cap Rate = income/sale price(value) Are the comparables truly comparable? How do you account for differences? What if there are insufficient comparables to derive a market rate? 20

21 Income Capitalization Approach Consider the differences between multipliers and cap rates as follows for the same income stream: 21

22 Income Capitalization Approach Yield Capitalization Mortgage Equity Formula Direct capitalization requires comparable sales AND only takes into account the investor s equity return based upon the first year s income No consideration given to future variability of income stream or potential change in value over time Mortgage Equity Formula market yield rate should reflect net income over time to market value Called Elwood or Akerson formulavalue (V) = Income (I)/Capitalization Rate (R) Includes following variables cap rate, yield rate, LTV ratio, percentage of loan paid off, sinking fund factor, mortgage constant, change in total property value, total ratio of change income, J factor accounts for change in income during holding period HOW GOOD ARE ALL OF YOU AT MATH? 22

23 Income Capitalization Approach Elwood Formula 23

24 Income Capitalization Approach Yield Capitalization/DCF Converts future benefits to present value by applying yield rate Reflects investment s income pattern, change in value and yield rate over time Discounting is the process which converts periodic incomes, cash flows and reversions into present value on the basis that the benefits in the future are worth less than benefits received now Considered speculative by many courts Too many variables Reversion reflects anticipated return of capital sum at end of investment s life cycle 24

25 Reconciliation of Value Indications If two or more approaches to value are used, the value indications must be reconciled Are they averaged or weighted? Do they indicate that more research is required? What if the indications are disparate? Will this test the reliability of each approach? Quality and quantity of data used Is a range an acceptable conclusion? 25

26 Final Thoughts What are the factors that should be considered in deciding which approach(es) to value to employ? Role of the attorney/appraiser/client Verify the data! Test the conclusions Have confidence in the conclusions! 26

27 Q&A? Thank you! Anthony F. DellaPelle, Esq., CRE Christian F. Torgrimson, Esq. 27

How to Read a Real Estate Appraisal Report

How to Read a Real Estate Appraisal Report Much of the private, corporate and public wealth of the world consists of real estate. The magnitude of this fundamental resource creates a need for informed

How to Read a Real Estate Appraisal Report Much of the private, corporate and public wealth of the world consists of real estate. The magnitude of this fundamental resource creates a need for informed

concepts and techniques

concepts and techniques S a m p l e Timed Outline Topic Area DAY 1 Reference(s) Learning Objective The student will learn Teaching Method Time Segment (Minutes) Chapter 1: Introduction to Sales Comparison

concepts and techniques S a m p l e Timed Outline Topic Area DAY 1 Reference(s) Learning Objective The student will learn Teaching Method Time Segment (Minutes) Chapter 1: Introduction to Sales Comparison

Sales Associate Course

Sales Associate Course Chapter Sixteen Appraisal 1 2 Appraiser Specific amount Impartial (non biased) Defendable Estimate (Opinion) of value Fee based on time and difficulty Must follow Uniform Standards

Sales Associate Course Chapter Sixteen Appraisal 1 2 Appraiser Specific amount Impartial (non biased) Defendable Estimate (Opinion) of value Fee based on time and difficulty Must follow Uniform Standards

The Three Approaches to Value

Chapter 6 The Three Approaches to Value The appraiser considers three approaches to develop indications of value. These are: Cost approach; Sales comparison (market) approach; and Income approach. All

Chapter 6 The Three Approaches to Value The appraiser considers three approaches to develop indications of value. These are: Cost approach; Sales comparison (market) approach; and Income approach. All

THE APPRAISAL OF REAL ESTATE 3 RD CANADIAN EDITION BUSI 330

THE APPRAISAL OF REAL ESTATE 3 RD CANADIAN EDITION BUSI 330 REVIEW NOTES by CHUCK DUNN CHAPTER 16 Copyright 2010 by the Real Estate Division and Chuck Dunn. All rights reserved CHAPTER 16 - LAND AND SITE

THE APPRAISAL OF REAL ESTATE 3 RD CANADIAN EDITION BUSI 330 REVIEW NOTES by CHUCK DUNN CHAPTER 16 Copyright 2010 by the Real Estate Division and Chuck Dunn. All rights reserved CHAPTER 16 - LAND AND SITE

Real Estate Appraisal

Market Value Chapter 17 Real Estate Appraisal This presentation includes materials from Ling and Archer, 4 th edition, Real Estate Principles The highest price a property will bring if: Payment is made

Market Value Chapter 17 Real Estate Appraisal This presentation includes materials from Ling and Archer, 4 th edition, Real Estate Principles The highest price a property will bring if: Payment is made

GENERAL ASSESSMENT DEFINITIONS

21st Century Appraisals, Inc. GENERAL ASSESSMENT DEFINITIONS Ad Valorem tax. A tax levied in proportion to the value of the thing(s) being taxed. Exclusive of exemptions, use-value assessment laws, and

21st Century Appraisals, Inc. GENERAL ASSESSMENT DEFINITIONS Ad Valorem tax. A tax levied in proportion to the value of the thing(s) being taxed. Exclusive of exemptions, use-value assessment laws, and

THE APPRAISAL OF REAL ESTATE 3 RD CANADIAN EDITION BUSI 330

THE APPRAISAL OF REAL ESTATE 3 RD CANADIAN EDITION BUSI 330 REVIEW NOTES by CHUCK DUNN CHAPTER 20 Copyright 2010 by the Real Estate Division and Chuck Dunn. All rights reserved CHAPTER 20 - THE INCOME

THE APPRAISAL OF REAL ESTATE 3 RD CANADIAN EDITION BUSI 330 REVIEW NOTES by CHUCK DUNN CHAPTER 20 Copyright 2010 by the Real Estate Division and Chuck Dunn. All rights reserved CHAPTER 20 - THE INCOME

California Real Estate License Exam Prep: Unlocking the DRE Salesperson and Broker Exam 4th Edition

California Real Estate License Exam Prep: Unlocking the DRE Salesperson and Broker Exam 4th Edition ANSWER SHEET INSTRUCTIONS: The exam consists of multiple choice questions. Multiple choice questions

California Real Estate License Exam Prep: Unlocking the DRE Salesperson and Broker Exam 4th Edition ANSWER SHEET INSTRUCTIONS: The exam consists of multiple choice questions. Multiple choice questions

BUSI 330 Suggested Answers to Review and Discussion Questions: Lesson 10

BUSI 330 Suggested Answers to Review and Discussion Questions: Lesson 10 1. The client should give you a copy of their income and expense statements for the last 3 years showing their rental income by

BUSI 330 Suggested Answers to Review and Discussion Questions: Lesson 10 1. The client should give you a copy of their income and expense statements for the last 3 years showing their rental income by

Broker. Sales Comparison, Cost Depreciation and Income Approaches. Chapter 7. Copyright Gold Coast Schools 1

Broker Chapter 7 Sales Comparison, Cost Depreciation and Income Approaches 1 Learning Objectives Describe the assumptions underlying the sales comparison approach Calculate the various adjustments necessary

Broker Chapter 7 Sales Comparison, Cost Depreciation and Income Approaches 1 Learning Objectives Describe the assumptions underlying the sales comparison approach Calculate the various adjustments necessary

THE APPRAISAL OF REAL ESTATE 3 RD CANADIAN EDITION BUSI 330

THE APPRAISAL OF REAL ESTATE 3 RD CANADIAN EDITION BUSI 330 REVIEW NOTES by CHUCK DUNN CHAPTER 17 Copyright 2010 by the Real Estate Division and Chuck Dunn. All rights reserved CHAPTER 17- THE COST APPROACH

THE APPRAISAL OF REAL ESTATE 3 RD CANADIAN EDITION BUSI 330 REVIEW NOTES by CHUCK DUNN CHAPTER 17 Copyright 2010 by the Real Estate Division and Chuck Dunn. All rights reserved CHAPTER 17- THE COST APPROACH

Cornerstone 2 Basic Valuation of Machinery and Equipment

INSTITUTE FOR PROFESSIONALS IN TAXATION PERSONAL PROPERTY TAX SCHOOL Cornerstone 2 Basic Valuation of Machinery and Equipment Learning Objectives At the end of this section, the learner will be able to:

INSTITUTE FOR PROFESSIONALS IN TAXATION PERSONAL PROPERTY TAX SCHOOL Cornerstone 2 Basic Valuation of Machinery and Equipment Learning Objectives At the end of this section, the learner will be able to:

absorption rate ad valorem appraisal broker price opinion capital gain

absorption rate The estimated time required to sell or lease property within a designated area at its fair market value. ad valorem Real estate taxes imposed on property based on its assessed value. appraisal

absorption rate The estimated time required to sell or lease property within a designated area at its fair market value. ad valorem Real estate taxes imposed on property based on its assessed value. appraisal

Part 1. Estimating Land Value Using a Land Residual Technique Based on Discounted Cash Flow Analysis

Table of Contents Overview... v Seminar Schedule... ix SECTION 1 Part 1. Estimating Land Value Using a Land Residual Technique Based on Discounted Cash Flow Analysis Preview Part 1... 1 Land Residual Technique...

Table of Contents Overview... v Seminar Schedule... ix SECTION 1 Part 1. Estimating Land Value Using a Land Residual Technique Based on Discounted Cash Flow Analysis Preview Part 1... 1 Land Residual Technique...

Following is an example of an income and expense benchmark worksheet:

After analyzing income and expense information and establishing typical rents and expenses, apply benchmarks and base standards to the reappraisal area. Following is an example of an income and expense

After analyzing income and expense information and establishing typical rents and expenses, apply benchmarks and base standards to the reappraisal area. Following is an example of an income and expense

Risk Management Insights

Risk Management Insights Appraisal Review Part II: Income Capitalization Approach George Mann, Managing Director and Chief Appraiser, Collateral Evaluation Services, Inc.and Nikki Griffith, MAI, CCIM,

Risk Management Insights Appraisal Review Part II: Income Capitalization Approach George Mann, Managing Director and Chief Appraiser, Collateral Evaluation Services, Inc.and Nikki Griffith, MAI, CCIM,

Cap Rate Trends, Methodology and Analysis. Dane R. Anderson MAI, CCIM Appraisal & Litigation Services Director

Cap Rate Trends, Methodology and Analysis Dane R. Anderson MAI, CCIM Appraisal & Litigation Services Director 1 Quickly The Income Approach Basis of the Approach Present worth of future benefits Two Methods:

Cap Rate Trends, Methodology and Analysis Dane R. Anderson MAI, CCIM Appraisal & Litigation Services Director 1 Quickly The Income Approach Basis of the Approach Present worth of future benefits Two Methods:

Basic Appraisal Procedures

Hondros Learning Basic Appraisal Procedures Timed Outline Topic Area Reference(s) Learning Objectives The student will be able to identify and/or apply: Teaching Method Time Segment (Minutes) Day 1 Chapter

Hondros Learning Basic Appraisal Procedures Timed Outline Topic Area Reference(s) Learning Objectives The student will be able to identify and/or apply: Teaching Method Time Segment (Minutes) Day 1 Chapter

Chapter 8. How much would you pay today for... The Income Approach to Appraisal

How much would you pay today for... Chapter 8 One hundred dollars paid with certainty each year for five years, starting one year from now. Why would you pay less than $500 Valuation Using the Income Approach

How much would you pay today for... Chapter 8 One hundred dollars paid with certainty each year for five years, starting one year from now. Why would you pay less than $500 Valuation Using the Income Approach

A Demonstration Appraisal Report. Of a. Located at. Date of Appraisal. Prepared for. Prepared by

A Demonstration Appraisal Report Of a Located at Date of Appraisal Prepared for Prepared by International Association of Assessing Officers Professional Designation Subcommittee 314 West 10 th Street Kansas

A Demonstration Appraisal Report Of a Located at Date of Appraisal Prepared for Prepared by International Association of Assessing Officers Professional Designation Subcommittee 314 West 10 th Street Kansas

Basics of Commercial Real Estate Transactions Day Two

Basics of Commercial Real Estate Transactions Day Two John Rockwell, Partner Energy October 12, 2016 PG&E refers to the Pacific Gas and Electric Company, a subsidiary of PG&E Corporation. 2010 Pacific

Basics of Commercial Real Estate Transactions Day Two John Rockwell, Partner Energy October 12, 2016 PG&E refers to the Pacific Gas and Electric Company, a subsidiary of PG&E Corporation. 2010 Pacific

PROBLEM SOLVING IN RESIDENTIAL REAL ESTATE APPRAISING

PROBLEM SOLVING IN RESIDENTIAL REAL ESTATE APPRAISING Copyright 2000 by LEE & GRANT COMPANY, Atlanta, Georgia. All rights reserved, including the right to reproduce this book or portions of this book in

PROBLEM SOLVING IN RESIDENTIAL REAL ESTATE APPRAISING Copyright 2000 by LEE & GRANT COMPANY, Atlanta, Georgia. All rights reserved, including the right to reproduce this book or portions of this book in

WYOMING DEPARTMENT OF REVENUE CHAPTER 7 PROPERTY TAX VALUATION METHODOLOGY AND ASSESSMENT (DEPARTMENT ASSESSMENTS)

") CHAPTER 7 PROPERTY TAX VALUATION METHODOLOGY AND ASSESSMENT (DEPARTMENT ASSESSMENTS) Section 1. Authority. These Rules are promulgated under the authority of W.S. 39-11-102(b). Section 2. Purpose of Rules.

CHAPTER 7 PROPERTY TAX VALUATION METHODOLOGY AND ASSESSMENT (DEPARTMENT ASSESSMENTS) Section 1. Authority. These Rules are promulgated under the authority of W.S. 39-11-102(b). Section 2. Purpose of Rules.

I R V. where I = Annual Net Income, R= Capitalization Rate and V= Value

Income Approach to Valuation Capitalization (Cap Rates) the short version! Capitalization is the process of converting net income into a meaningful value that correlates net income to the value of the

Income Approach to Valuation Capitalization (Cap Rates) the short version! Capitalization is the process of converting net income into a meaningful value that correlates net income to the value of the

Land / Site Valuation A Basic Review. Leslie G. Pruitt Certified General Appraiser

Land / Site Valuation A Basic Review Leslie G. Pruitt Certified General Appraiser Whose is the land, it is to the sky and the depth Whose is the land, it is to the sky and the depth This ancient maxim

Land / Site Valuation A Basic Review Leslie G. Pruitt Certified General Appraiser Whose is the land, it is to the sky and the depth Whose is the land, it is to the sky and the depth This ancient maxim

60-HR FL Real Estate Broker Post-Licensing Learning Objectives by Lesson

Lesson 1: Starting a Real Estate Office SECTION 1: BROKERAGE OFFICE ESSENTIALS Recall the characteristics of business entities that may register as a real estate brokerage and the rules involved to operate

Lesson 1: Starting a Real Estate Office SECTION 1: BROKERAGE OFFICE ESSENTIALS Recall the characteristics of business entities that may register as a real estate brokerage and the rules involved to operate

Chapter 8. How much would you pay today for... The Income Approach to Appraisal

How much would you pay today for... Chapter 8 One hundred dollars paid with certainty each year for five years, starting one year from now. Why would you pay less than $500 Valuation Using the Income Approach

How much would you pay today for... Chapter 8 One hundred dollars paid with certainty each year for five years, starting one year from now. Why would you pay less than $500 Valuation Using the Income Approach

Industrial and Commercial Real Estate Appraisal Procedures

Property Valuation Thought Leadership Industrial and Commercial Real Estate Appraisal Procedures John C. Ramirez The application of the asset-based approach to business valuation often involves the appraisal

Property Valuation Thought Leadership Industrial and Commercial Real Estate Appraisal Procedures John C. Ramirez The application of the asset-based approach to business valuation often involves the appraisal

Rockwall CAD. Basics of. Appraising Property. For. Property Taxation

Rockwall CAD Basics of Appraising Property For Property Taxation ROCKWALL CENTRAL APPRAISAL DISTRICT 841 Justin Rd. Rockwall, Texas 75087 972-771-2034 Fax 972-771-6871 Introduction Rockwall Central Appraisal

Rockwall CAD Basics of Appraising Property For Property Taxation ROCKWALL CENTRAL APPRAISAL DISTRICT 841 Justin Rd. Rockwall, Texas 75087 972-771-2034 Fax 972-771-6871 Introduction Rockwall Central Appraisal

Course Income Approach To Value. Course Description

Course 102 - Income Approach To Value Course Description The Income Approach to Valuation is designed to provide the students with an understanding and working knowledge of the procedures and techniques

Course 102 - Income Approach To Value Course Description The Income Approach to Valuation is designed to provide the students with an understanding and working knowledge of the procedures and techniques

Chapter 3 Business Valuation Report

CHAPTER 3: BUSINESS VALUATION REPORT Chapter 3 Business Valuation Report A1. Pre-IPO Valuation Need Company Restructuring and Financing It is not unusual that companies undergo series of restructuring

CHAPTER 3: BUSINESS VALUATION REPORT Chapter 3 Business Valuation Report A1. Pre-IPO Valuation Need Company Restructuring and Financing It is not unusual that companies undergo series of restructuring

VALUATION CONSIDERATIONS AND METHODS FOR A PATENT VALUATION ANALYSIS

Insights Autumn 2009 54 Intellectual Property Valuation Insights VALUATION CONSIDERATIONS AND METHODS FOR A PATENT VALUATION ANALYSIS C. Ryan Stewart In recent years, the value of patents and other intellectual

Insights Autumn 2009 54 Intellectual Property Valuation Insights VALUATION CONSIDERATIONS AND METHODS FOR A PATENT VALUATION ANALYSIS C. Ryan Stewart In recent years, the value of patents and other intellectual

2. The, and Act, also known as FIRREA, requires that states set standards for all appraisers.

CHAPTER 4 SHORT-ANSWER QUESTIONS 1. An appraisal is an or of value. 2. The, and Act, also known as FIRREA, requires that states set standards for all appraisers. 3. Value in real estate is the "present

CHAPTER 4 SHORT-ANSWER QUESTIONS 1. An appraisal is an or of value. 2. The, and Act, also known as FIRREA, requires that states set standards for all appraisers. 3. Value in real estate is the "present

procedures Basic Appraisal F i n a l Examination #2 2 nd edition

F i n a l Examination #2 A n s w e r Key Page 82 1. When determining effective gross income from potential gross income, an appraiser considers a. debt service. b. depreciation. c. fixed expenses. d. vacancy

F i n a l Examination #2 A n s w e r Key Page 82 1. When determining effective gross income from potential gross income, an appraiser considers a. debt service. b. depreciation. c. fixed expenses. d. vacancy

Table of Contents. Chapter 1: Introduction (Mobile Technology Evolution) 1

1") Chapter 1: Introduction (Mobile Technology Evolution) 1 I. WHY APPRAISAL IS IMPORTANT (p. 3) II. DEFINITION OF APPRAISAL (p. 4) A. Opinion (p. 4) B. Value (p. 5) C. Appraisal Art or Science? (p. 5) D.

Chapter 1: Introduction (Mobile Technology Evolution) 1 I. WHY APPRAISAL IS IMPORTANT (p. 3) II. DEFINITION OF APPRAISAL (p. 4) A. Opinion (p. 4) B. Value (p. 5) C. Appraisal Art or Science? (p. 5) D.

Registration Course Description Classroom Rules & Procedures

Course Schedule SECTION 1. (Day 1 Morning) Introduction Part 1. Introduction and Overview Registration Course Description Classroom Rules & Procedures Part 2. Components of Discounted Cash Flow Analysis

Course Schedule SECTION 1. (Day 1 Morning) Introduction Part 1. Introduction and Overview Registration Course Description Classroom Rules & Procedures Part 2. Components of Discounted Cash Flow Analysis

Chapter 8. The Income Approach to Appraisal. Two Approaches to Income Valuation. How Does DCF Differ from Direct Cap? Rationale:

The Income Approach to Appraisal Chapter 8 Valuation Using the Income Approach Rationale: Value of a property is the present value of its anticipated income. Often called income capitalization Capitalize:

The Income Approach to Appraisal Chapter 8 Valuation Using the Income Approach Rationale: Value of a property is the present value of its anticipated income. Often called income capitalization Capitalize:

Business Valuation More Art Than Science

Business Valuation More Art Than Science One of the more difficult aspects of business planning is business valuation. It is also one of the more important aspects. While owners of closely held businesses

Business Valuation More Art Than Science One of the more difficult aspects of business planning is business valuation. It is also one of the more important aspects. While owners of closely held businesses

Examples of Quantitative Support Methods from Real World Appraisals

Examples of Quantitative Support Methods from Real World Appraisals Jeffrey A. Johnson, MAI Integra Realty Resources Minneapolis / St. Paul Tony Lesicka, MAI Central Bank 1 Overview of Presentation EXAMPLES

Examples of Quantitative Support Methods from Real World Appraisals Jeffrey A. Johnson, MAI Integra Realty Resources Minneapolis / St. Paul Tony Lesicka, MAI Central Bank 1 Overview of Presentation EXAMPLES

Residential Site Valuation and Cost Approach 2 nd Edition Hondros Learning Chapter Quiz and Work Problem Answer Key:

Residential Site Valuation and Cost Approach 2 nd Edition Hondros Learning Chapter Quiz and Work Problem Answer Key: Chapter 1 Quiz 1. A parcel of land with on-site improvements (e.g., utilities) is best

Residential Site Valuation and Cost Approach 2 nd Edition Hondros Learning Chapter Quiz and Work Problem Answer Key: Chapter 1 Quiz 1. A parcel of land with on-site improvements (e.g., utilities) is best

Requirements for International Standards in Valuation & Surveying

Requirements for International Standards in Valuation & Surveying Jonathan Harris CBE DLitt(Hon), FRICS, FInstCPD, CRE President of RICS 2000-2001 Member of REM Glossary of Terms for International Valuation

Requirements for International Standards in Valuation & Surveying Jonathan Harris CBE DLitt(Hon), FRICS, FInstCPD, CRE President of RICS 2000-2001 Member of REM Glossary of Terms for International Valuation

Mass Appraisal of Income-Producing Properties

Chapter 10 Mass Appraisal of Income-Producing Properties Whether valuing income-producing property or residential property, you can use similar information and methods for collecting and analyzing data

Chapter 10 Mass Appraisal of Income-Producing Properties Whether valuing income-producing property or residential property, you can use similar information and methods for collecting and analyzing data

APPRAISER & ASSESSOR Real Estate Tax Valuation Overview and Issues

APPRAISER & ASSESSOR Real Estate Tax Valuation Overview and Issues James R. Johnston, MAI, SRA J. Michael Tarello, MAI, ASA, MRA February 11, 2015 BOSTON Property Advisors Vision Government Solutions AGENDA

APPRAISER & ASSESSOR Real Estate Tax Valuation Overview and Issues James R. Johnston, MAI, SRA J. Michael Tarello, MAI, ASA, MRA February 11, 2015 BOSTON Property Advisors Vision Government Solutions AGENDA

Special Purpose Properties. Special Valuation Considerations

Special Purpose Properties Special Valuation Considerations 2017 Case Study in Ottawa: New Automobile Dealership Many brand-specific specialties Cost: $4,000,000 (including land and a developer fee) Sales

Special Purpose Properties Special Valuation Considerations 2017 Case Study in Ottawa: New Automobile Dealership Many brand-specific specialties Cost: $4,000,000 (including land and a developer fee) Sales

PREPARING FOR THE MINNESOTA INCOME PROPERTY CASE STUDY EXAM WORKSHOP

PREPARING FOR THE MINNESOTA INCOME PROPERTY CASE STUDY EXAM WORKSHOP Date: September 18, 2018 Location: Country Inn & Suites Chanhassen, MN Instructor: Bob Wilson, CAE, ASA Revised October, 2017 PREPARING

PREPARING FOR THE MINNESOTA INCOME PROPERTY CASE STUDY EXAM WORKSHOP Date: September 18, 2018 Location: Country Inn & Suites Chanhassen, MN Instructor: Bob Wilson, CAE, ASA Revised October, 2017 PREPARING

Chapter 37. The Appraiser's Cost Approach INTRODUCTION

Chapter 37 The Appraiser's Cost Approach INTRODUCTION The cost approach for estimating current market value starts with the recognition that a parcel of real estate contains two components - the land and

Chapter 37 The Appraiser's Cost Approach INTRODUCTION The cost approach for estimating current market value starts with the recognition that a parcel of real estate contains two components - the land and

APPRAISER & ASSESSOR Real Estate Tax Valuation Overview and Issues

APPRAISER & ASSESSOR Real Estate Tax Valuation Overview and Issues James R. Johnston, MAI, SRA J. Michael Tarello, MAI, ASA, MRA May 20, 2015 BOSTON Property Advisors Vision Government Solutions AGENDA

APPRAISER & ASSESSOR Real Estate Tax Valuation Overview and Issues James R. Johnston, MAI, SRA J. Michael Tarello, MAI, ASA, MRA May 20, 2015 BOSTON Property Advisors Vision Government Solutions AGENDA

Classify and describe basic forms of real estate investments.

LOS 43.a 2017 CFA Exam SS 15 Classify and describe basic forms of real estate investments. Card 1 of 52 LOS 43.a There are four basic forms of real estate investment; private equity (direct ownership),

LOS 43.a 2017 CFA Exam SS 15 Classify and describe basic forms of real estate investments. Card 1 of 52 LOS 43.a There are four basic forms of real estate investment; private equity (direct ownership),

Fundamentals of Real Estate APPRAISAL. 10th Edition. William L. Ventolo, Jr. Martha R. Williams, JD

A Fundamentals of Real Estate APPRAISAL 10th Edition William L. Ventolo, Jr. Martha R. Williams, JD Dennis S. Tosh, PhD William B. Rayburn, PhD, MAI, CFA Consulting Editors Dearb rri Real Estate Education

A Fundamentals of Real Estate APPRAISAL 10th Edition William L. Ventolo, Jr. Martha R. Williams, JD Dennis S. Tosh, PhD William B. Rayburn, PhD, MAI, CFA Consulting Editors Dearb rri Real Estate Education

RESIDUAL ANALYSIS PRINCIPLES AND PROCEEDURES

RESIDUAL ANALYSIS PRINCIPLES AND PROCEEDURES OVERVIEW 1. Residual analysis or extractions, are a form of land valuation study. 2. This analysis relies on the improved sales (typically the largest group

RESIDUAL ANALYSIS PRINCIPLES AND PROCEEDURES OVERVIEW 1. Residual analysis or extractions, are a form of land valuation study. 2. This analysis relies on the improved sales (typically the largest group

Strip Commercial. Market Value Assessment in Saskatchewan Handbook. Strip Commercial Properties Valuation Guide

Market Value Assessment in Saskatchewan Handbook Strip Commercial Saskatchewan Assessment Management Agency 2012 This document is a derivative work based upon a handbook entitled the "Market Value and

Market Value Assessment in Saskatchewan Handbook Strip Commercial Saskatchewan Assessment Management Agency 2012 This document is a derivative work based upon a handbook entitled the "Market Value and

Proving Depreciation

Institute for Professionals in Taxation 40 th Annual Property Tax Symposium Tucson, Arizona Proving Depreciation Presentation Concepts and Content: Kathy G. Spletter, ASA Stancil & Co. Irving, Texas kathy.spletter@stancilco.com

Institute for Professionals in Taxation 40 th Annual Property Tax Symposium Tucson, Arizona Proving Depreciation Presentation Concepts and Content: Kathy G. Spletter, ASA Stancil & Co. Irving, Texas kathy.spletter@stancilco.com

Residential Property Value Procedures: How to calculate a value

2500 Handley Ederville Road Fort Worth, TX 76118 (817) 284 3925 res@tad.org Residential Property Value Procedures: How to calculate a value Mass Appraisal: The Residential Department is responsible for

2500 Handley Ederville Road Fort Worth, TX 76118 (817) 284 3925 res@tad.org Residential Property Value Procedures: How to calculate a value Mass Appraisal: The Residential Department is responsible for

Index of Examples. Chapter 1 Letter of Transmittal Chapter 2 General Assumptions and Limiting Conditions... 19

Index of Examples Chapter 1 Letter of Transmittal... 1 Example 1A Detailed Letter of Transmittal... 2 Example 1B Detailed Letter of Transmittal with Risk Factors and Assumptions... 6 Example 1C Brief Letter

Index of Examples Chapter 1 Letter of Transmittal... 1 Example 1A Detailed Letter of Transmittal... 2 Example 1B Detailed Letter of Transmittal with Risk Factors and Assumptions... 6 Example 1C Brief Letter

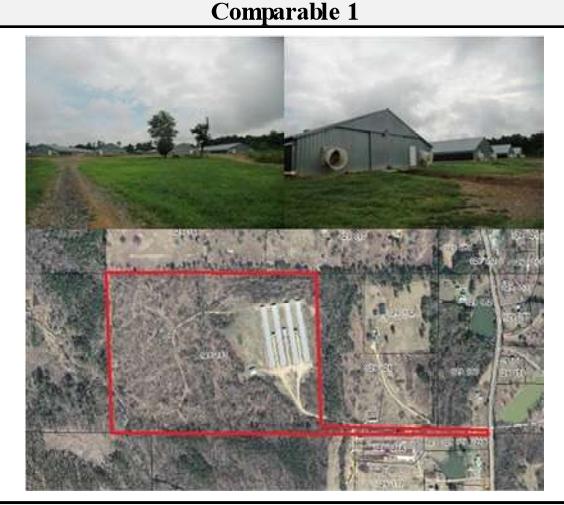

Distressed Properties, Vacancy Shortfall, and Entrepreneurial Incentive

Property Tax Valuation Insights Distressed Properties, Vacancy Shortfall, and Entrepreneurial Incentive Michelle DeLappe, Esq., and Andrew T. Robinson, MAI A commercial property that suffers from below-market

Property Tax Valuation Insights Distressed Properties, Vacancy Shortfall, and Entrepreneurial Incentive Michelle DeLappe, Esq., and Andrew T. Robinson, MAI A commercial property that suffers from below-market

INSTITUTE FOR PROFESSIONALS IN TAXATION REAL PROPERTY TAX SCHOOL REVIEW AND INTRODUCTION

INSTITUTE FOR PROFESSIONALS IN TAXATION REAL PROPERTY TAX SCHOOL REVIEW AND INTRODUCTION This section is an overview of the major topics covered by IPT s Property Tax School which are directly relevant

INSTITUTE FOR PROFESSIONALS IN TAXATION REAL PROPERTY TAX SCHOOL REVIEW AND INTRODUCTION This section is an overview of the major topics covered by IPT s Property Tax School which are directly relevant

This chapter explores the principles of value, the forces that impact the value of property, and the appraisal process.

Principles of Real Estate Chapter 13-Valuation and Economics This chapter explores the principles of value, the forces that impact the value of property, and the appraisal process. Overview Objectives

Principles of Real Estate Chapter 13-Valuation and Economics This chapter explores the principles of value, the forces that impact the value of property, and the appraisal process. Overview Objectives

In-Depth Capitalization Rate Review

In-Depth Capitalization Rate Review Leonard J. Patcella, Jr., CMI, MAI President Equity Appraisal Co., Inc. Springhouse, PA jack.equityappraisal@comcast.net David A. Schneider, Esq. Partner Archer & Greiner,

In-Depth Capitalization Rate Review Leonard J. Patcella, Jr., CMI, MAI President Equity Appraisal Co., Inc. Springhouse, PA jack.equityappraisal@comcast.net David A. Schneider, Esq. Partner Archer & Greiner,

REPORTING GUIDELINES FOR REAL ESTATE APPRAISAL REPORTS

Property Tax Valuation Reporting REPORTING GUIDELINES FOR REAL ESTATE APPRAISAL REPORTS Robert F. Reilly and Robert P. Schweihs 43 INTRODUCTION Appraisal reports become important documents in property

Property Tax Valuation Reporting REPORTING GUIDELINES FOR REAL ESTATE APPRAISAL REPORTS Robert F. Reilly and Robert P. Schweihs 43 INTRODUCTION Appraisal reports become important documents in property

Course Mass Appraisal Practices and Procedures

Course 331 - Mass Appraisal Practices and Procedures Course Description This course is designed to build on the subject matter covered in Course 300 Fundamentals of Mass Appraisal and prepare the student

Course 331 - Mass Appraisal Practices and Procedures Course Description This course is designed to build on the subject matter covered in Course 300 Fundamentals of Mass Appraisal and prepare the student

Published in Spring 1986 Issue The Real Estate Appraiser & Analyst Society of Real Estate Appraisers 1

(1) Published in Spring 1986 Issue The Real Estate Appraiser & Analyst Society of Real Estate Appraisers 1 Alternative Valuation Methods for Leasehold Properties By Tony Sevelka, AACI, SREA, MAI, CRE Introduction

(1) Published in Spring 1986 Issue The Real Estate Appraiser & Analyst Society of Real Estate Appraisers 1 Alternative Valuation Methods for Leasehold Properties By Tony Sevelka, AACI, SREA, MAI, CRE Introduction

AI General Demonstration Grading Sheet

AI General Demonstration Grading Sheet Traditional Report - Fundamental Market Analysis Option Account # Candidate Subject Property Address Grader Date Mailed to Grader Original Submission If original

AI General Demonstration Grading Sheet Traditional Report - Fundamental Market Analysis Option Account # Candidate Subject Property Address Grader Date Mailed to Grader Original Submission If original

A Demonstration Appraisal Report. Of a. Located at. Date of Appraisal. Prepared for. Prepared by

A Demonstration Appraisal Report Of a Located at Date of Appraisal Prepared for Prepared by International Association of Assessing Officers Professional Designation Subcommittee 314 W. 10 th Street Kansas

A Demonstration Appraisal Report Of a Located at Date of Appraisal Prepared for Prepared by International Association of Assessing Officers Professional Designation Subcommittee 314 W. 10 th Street Kansas

MODULE 7-A: APPRAISALS, BPOS AND USPAP

MODULE 7-A: APPRAISALS, BPOS AND USPAP LEARNING OBJECTIVES One of the most challenging aspects of the real estate business is the development of prices or values of the rights to real estate. Buyers and

MODULE 7-A: APPRAISALS, BPOS AND USPAP LEARNING OBJECTIVES One of the most challenging aspects of the real estate business is the development of prices or values of the rights to real estate. Buyers and

C O O K C O U N T Y A S S E S S O R S O F F I C E VALUATION ESTIMATES AND APPRAISAL METHODOLOGY

C O O K C O U N T Y A S S E S S O R S O F F I C E EXEMPT HOSPITALS VALUATION ESTIMATES AND APPRAISAL METHODOLOGY EXEMPT HOSPITALS VALUATION ESTIMATES AND APPRAISAL METHODOLOGY PURPOSE OF THE REPORT In

C O O K C O U N T Y A S S E S S O R S O F F I C E EXEMPT HOSPITALS VALUATION ESTIMATES AND APPRAISAL METHODOLOGY EXEMPT HOSPITALS VALUATION ESTIMATES AND APPRAISAL METHODOLOGY PURPOSE OF THE REPORT In

Purchase Price Allocations ASC 805 Business Combinations

Purchase Price Allocations Introduction Mergers, acquisitions, and other business transactions have numerous accounting and tax implications. Buyers generally identify and report the fair values of the

Purchase Price Allocations Introduction Mergers, acquisitions, and other business transactions have numerous accounting and tax implications. Buyers generally identify and report the fair values of the

Introducing. Property. Valuation. Second edition. Michael Blackledge. Routledge R Taylor & Francis Croup LONDON AND NEW YORK

Introducing Property Valuation Second edition Michael Blackledge Routledge R Taylor & Francis Croup LONDON AND NEW YORK I Contents List of illustrations List ofcases Acknowledgements Disclaimers x xiii

Introducing Property Valuation Second edition Michael Blackledge Routledge R Taylor & Francis Croup LONDON AND NEW YORK I Contents List of illustrations List ofcases Acknowledgements Disclaimers x xiii

Cost Segregation Instructor Teaching Schedule (3-Hour)

") Time Topic Pages Student Objectives 8:30-8:35 Course introduction Page 2 What is cost segregation? Objective of cost segregation: to increase cash flow Benefit of cost segregation Learning objectives Page

Time Topic Pages Student Objectives 8:30-8:35 Course introduction Page 2 What is cost segregation? Objective of cost segregation: to increase cash flow Benefit of cost segregation Learning objectives Page

Appraisal Review: Analyzing the 1004

Appraisal Review: Analyzing the 1004 1 LIVE ONLINE PARTICIPANT GUIDE Version: 8.12 Table of Contents The Purpose of the Appraisal... 3 Define Market Value... 3 Scenario 1 (John Johnson report) - 1004 Uniform

Appraisal Review: Analyzing the 1004 1 LIVE ONLINE PARTICIPANT GUIDE Version: 8.12 Table of Contents The Purpose of the Appraisal... 3 Define Market Value... 3 Scenario 1 (John Johnson report) - 1004 Uniform

Chapter 1 Economics of Net Leases and Sale-Leasebacks

Chapter 1 Economics of Net Leases and Sale-Leasebacks 1:1 What Is a Net Lease? 1:2 Types of Net Leases 1:2.1 Bond Lease 1:2.2 Absolute Net Lease 1:2.3 Triple Net Lease 1:2.4 Double Net Lease 1:2.5 The

Chapter 1 Economics of Net Leases and Sale-Leasebacks 1:1 What Is a Net Lease? 1:2 Types of Net Leases 1:2.1 Bond Lease 1:2.2 Absolute Net Lease 1:2.3 Triple Net Lease 1:2.4 Double Net Lease 1:2.5 The

Fully Stabilized 24-Unit Property at 11% Cap Rate!

Fully Stabilized 24-Unit Property at 11% Cap Rate! To Insert a Picture here, click inside this box with your mouse, then click on "INSERT PIC" button on the right and select the picture 24 Units consisting

Fully Stabilized 24-Unit Property at 11% Cap Rate! To Insert a Picture here, click inside this box with your mouse, then click on "INSERT PIC" button on the right and select the picture 24 Units consisting

Table of Contents 2013 Commercial Revaluation Report

Table of Contents Commercial Revaluation Report 1. Commercial & Industrial Valuation Summary Introduction Uniform Standards Approaches to Value Land Valuation Land to Building Ratios Parking to Building

Table of Contents Commercial Revaluation Report 1. Commercial & Industrial Valuation Summary Introduction Uniform Standards Approaches to Value Land Valuation Land to Building Ratios Parking to Building

Introducing Property Valuation

Introducing Property Valuation Michael Blackledge Routledge Taylor & Francis Group LONDON AND NEW YORK Illustrations Cases Acknowledgements Disclaimers x xii xiv xv 1: Background 1 Economic context 3 1.1

Introducing Property Valuation Michael Blackledge Routledge Taylor & Francis Group LONDON AND NEW YORK Illustrations Cases Acknowledgements Disclaimers x xii xiv xv 1: Background 1 Economic context 3 1.1

CHAPTER 4 - VALUATION

CHAPTER 4 - VALUATION Notes: READ THIS CAREFULLY: It is important for the student to remember that the license exam will not test you about "mechanical" aspects of appraisal (i.e., "what does an appraiser

CHAPTER 4 - VALUATION Notes: READ THIS CAREFULLY: It is important for the student to remember that the license exam will not test you about "mechanical" aspects of appraisal (i.e., "what does an appraiser

Licensing Education STUDY GUIDE. The Manitoba Real Estate Association

Licensing Education STUDY GUIDE The Manitoba Real Estate Association NOTE: This Study Guide replaces the Assignment Booklet referred to in the Appraisal workbook. It does not have to be returned to the

Licensing Education STUDY GUIDE The Manitoba Real Estate Association NOTE: This Study Guide replaces the Assignment Booklet referred to in the Appraisal workbook. It does not have to be returned to the

ASSESSMENT METHODOLOGY

2018 ASSESSMENT METHODOLOGY MULTI-RESIDENTIAL MANUFACTURED HOME PARK A summary of the methods used by the City of Edmonton in determining the value of multi-residential manufactured home park land properties

2018 ASSESSMENT METHODOLOGY MULTI-RESIDENTIAL MANUFACTURED HOME PARK A summary of the methods used by the City of Edmonton in determining the value of multi-residential manufactured home park land properties

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence OVERVIEW OF RESIDENTIAL APPRAISAL PROCESS And Cost Valuation Report Introduction The

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence OVERVIEW OF RESIDENTIAL APPRAISAL PROCESS And Cost Valuation Report Introduction The

Appraiser Qualifications Board

Appraiser Qualifications Board Course Analysis Course Name Provider Date of Approval Course Expiration Date This detailed breakdown of the subject content of this course is provided by the AQB as part

Appraiser Qualifications Board Course Analysis Course Name Provider Date of Approval Course Expiration Date This detailed breakdown of the subject content of this course is provided by the AQB as part

Edmonton Composite Assessment Review Board

Edmonton Composite Assessment Review Board Citation: CVG v The City of Edmonton, 2013 ECARB 01878 Assessment Roll Number: 10002533 Municipal Address: 10904 102 A venue NW Assessment Year: 2013 Assessment

Edmonton Composite Assessment Review Board Citation: CVG v The City of Edmonton, 2013 ECARB 01878 Assessment Roll Number: 10002533 Municipal Address: 10904 102 A venue NW Assessment Year: 2013 Assessment

Revised Seller/Servicer Guide Chapter 12 Multifamily Appraisals. Martin A. Skolnik, MAI (Marty) Director, Multifamily Appraisals

Director, Multifamily Appraisals") Revised Seller/Servicer Guide Chapter 12 Multifamily Appraisals Martin A. Skolnik, MAI (Marty) Director, Multifamily Appraisals June 26, 2014 Multifamily Real Estate Valuation at Freddie Mac Freddie Mac

Revised Seller/Servicer Guide Chapter 12 Multifamily Appraisals Martin A. Skolnik, MAI (Marty) Director, Multifamily Appraisals June 26, 2014 Multifamily Real Estate Valuation at Freddie Mac Freddie Mac

Intangible assets have continually grown in their importance as a driver of value in businesses, in particular over the past thirty years.

Intangible assets have continually grown in their importance as a driver of value in businesses, in particular over the past thirty years. In the 1980s large, publicly-traded company values were generally

Intangible assets have continually grown in their importance as a driver of value in businesses, in particular over the past thirty years. In the 1980s large, publicly-traded company values were generally

Math Relating to Real Property Appraisals

1. Sales Comparison Approach Math Relating to Real Property Appraisals A. If the comparable property is superior in a feature, you subtract value from the comparable. Example: Comp #l has a 1-car garage

1. Sales Comparison Approach Math Relating to Real Property Appraisals A. If the comparable property is superior in a feature, you subtract value from the comparable. Example: Comp #l has a 1-car garage

2016 Level I Tutorials. Income Approach to Value

2016 Level I Tutorials Income Approach to Value 1 The income approach is based on the principal that the value of an investment property reflects the quality and quantity of the income it is expected to

2016 Level I Tutorials Income Approach to Value 1 The income approach is based on the principal that the value of an investment property reflects the quality and quantity of the income it is expected to

Assessment and Taxation Department Service de l évaluation et des taxes VALUATION OF HOTELS General Assessment

Assessment and Taxation Department Service de l évaluation et des taxes VALUATION OF HOTELS 2012 General Assessment City of Winnipeg Assessment and Taxation Department May 4, 2011 TABLE OF CONTENTS INTRODUCTION...

Assessment and Taxation Department Service de l évaluation et des taxes VALUATION OF HOTELS 2012 General Assessment City of Winnipeg Assessment and Taxation Department May 4, 2011 TABLE OF CONTENTS INTRODUCTION...

THE APPRAISAL OF REAL ESTATE 3 RD CANADIAN EDITION BUSI 330

THE APPRAISAL OF REAL ESTATE 3 RD CANADIAN EDITION BUSI 330 REVIEW NOTES by CHUCK DUNN CHAPTER 19 Copyright 2010 by the Real Estate Division and Chuck Dunn. All rights reserved CHAPTER 19 - DEPRECIATION

THE APPRAISAL OF REAL ESTATE 3 RD CANADIAN EDITION BUSI 330 REVIEW NOTES by CHUCK DUNN CHAPTER 19 Copyright 2010 by the Real Estate Division and Chuck Dunn. All rights reserved CHAPTER 19 - DEPRECIATION

BUSI 330 Suggested Answers to Review and Discussion Questions: Lesson 9

BUSI 330 Suggested Answers to Review and Discussion Questions: Lesson 9 1. Students should give a brief definition of each of the following terms and provide one example which illustrates how they are

BUSI 330 Suggested Answers to Review and Discussion Questions: Lesson 9 1. Students should give a brief definition of each of the following terms and provide one example which illustrates how they are

Office Building. Market Value Assessment in Saskatchewan Handbook. Office Building Valuation Guide

Market Value Assessment in Saskatchewan Handbook Office Building Saskatchewan Assessment Management Agency 2012 This document is a derivative work based upon a handbook entitled the "Market Value and Mass

Market Value Assessment in Saskatchewan Handbook Office Building Saskatchewan Assessment Management Agency 2012 This document is a derivative work based upon a handbook entitled the "Market Value and Mass

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence OVERVIEW OF RESIDENTIAL APPRAISAL PROCESS And Cost Valuation Report Introduction The

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence OVERVIEW OF RESIDENTIAL APPRAISAL PROCESS And Cost Valuation Report Introduction The

Edmonton Composite Assessment Review Board

Edmonton Composite Assessment Review Board Citation: CVG v The City of Edmonton, 2013 ECARB 01877 Assessment Roll Number: 9942678 Municipal Address: 10020 103 A venue NW Assessment Year: 2013 Assessment

Edmonton Composite Assessment Review Board Citation: CVG v The City of Edmonton, 2013 ECARB 01877 Assessment Roll Number: 9942678 Municipal Address: 10020 103 A venue NW Assessment Year: 2013 Assessment

Four (4) Factors in Investment Definition: Investment

Factors in Investment Definition: Investment") Introductions Your name Where you work Your job responsibilities How long you have been in the industry What you hope to get from this class Chapter 1: Investments Agenda 2 Investments Adding Value to

Introductions Your name Where you work Your job responsibilities How long you have been in the industry What you hope to get from this class Chapter 1: Investments Agenda 2 Investments Adding Value to

Schedule. SECTION 1. Cost Approach Principles and Cost Estimation (Morning Day 1) Overview 8:00 8:30 Registration Classroom Rules and Procedures

Overview 8:00 8:30 Registration Classroom Rules and Procedures") Schedule SECTION 1. Cost Approach Principles and Cost Estimation (Morning Day 1) Overview 8:00 8:30 Registration Classroom Rules and Procedures Introduction Cost Approach Pretest Part 1. Introduction to

Schedule SECTION 1. Cost Approach Principles and Cost Estimation (Morning Day 1) Overview 8:00 8:30 Registration Classroom Rules and Procedures Introduction Cost Approach Pretest Part 1. Introduction to

Before the Minnesota Public Utilities Commission State of Minnesota. Docket No. E002/GR Exhibit (LMC-1) Property Taxes

Property Taxes") Direct Testimony and Schedules Leanna M. Chapman Before the Minnesota Public Utilities Commission State of Minnesota In the Matter of the Application of Northern States Power Company for Authority to Increase

Direct Testimony and Schedules Leanna M. Chapman Before the Minnesota Public Utilities Commission State of Minnesota In the Matter of the Application of Northern States Power Company for Authority to Increase

State of Mexicali Ad Valorem Taxation of Property Statutes, Rules and Regulations

STATUTES CODE OF MEXICALI OF 2000, TITLE 50 REVENUE AND TAXATION, CHAPTER 7 AD VALOREM TAXATION OF PROPERTY Sec. 50-7-1. Legislative intent The intent and purpose of the tax laws of this state are to have

STATUTES CODE OF MEXICALI OF 2000, TITLE 50 REVENUE AND TAXATION, CHAPTER 7 AD VALOREM TAXATION OF PROPERTY Sec. 50-7-1. Legislative intent The intent and purpose of the tax laws of this state are to have

WALLER COUNTY APPRAISAL DISTRICT MASS APPRAISAL REPORT APPRAISAL YEAR 2018

WALLER COUNTY APPRAISAL DISTRICT MASS APPRAISAL REPORT APPRAISAL YEAR 2018 ADDENDUM TO WCAD REAPPRAISAL PLAN FOR 2017 AND 2018 WALLER COUNTY APPRAISAL DISTRICT Uniform Standards of Professional Appraisal

WALLER COUNTY APPRAISAL DISTRICT MASS APPRAISAL REPORT APPRAISAL YEAR 2018 ADDENDUM TO WCAD REAPPRAISAL PLAN FOR 2017 AND 2018 WALLER COUNTY APPRAISAL DISTRICT Uniform Standards of Professional Appraisal

Definitions ad valorem tax Adaptive Estimation Procedure (AEP) - additive model - adjustments - algorithm - amenities appraisal appraisal schedules

- additive model - adjustments - algorithm - amenities appraisal appraisal schedules") Definitions ad valorem tax - in reference to property, a tax based upon the value of the property. Adaptive Estimation Procedure (AEP) - A computerized, iterative, self-referential procedure using properties

Definitions ad valorem tax - in reference to property, a tax based upon the value of the property. Adaptive Estimation Procedure (AEP) - A computerized, iterative, self-referential procedure using properties

San Patricio County Appraisal District. Reappraisal Plan For. Tax Years 2013 & 2014

San Patricio County Appraisal District Reappraisal Plan For Tax Years 2013 & 2014 (adopted by SPCAD Board of Directors on September 11 th, 2012) 1 TABLE OF CONTENTS ITEM PAGE Executive Summary 4 Revaluation

San Patricio County Appraisal District Reappraisal Plan For Tax Years 2013 & 2014 (adopted by SPCAD Board of Directors on September 11 th, 2012) 1 TABLE OF CONTENTS ITEM PAGE Executive Summary 4 Revaluation

HOTEL CAPITALIZATION RATES AND THE IMPACT OF CAP EX

JANUARY 2014 PRICE $500 HOTEL CAPITALIZATION RATES AND THE IMPACT OF CAP EX Author Suzanne R. Mellen, MAI, CRE, ISHC, FRICS Senior Managing Director www.hvs.com HVS San Francisco 100 Bush Street, Suite

JANUARY 2014 PRICE $500 HOTEL CAPITALIZATION RATES AND THE IMPACT OF CAP EX Author Suzanne R. Mellen, MAI, CRE, ISHC, FRICS Senior Managing Director www.hvs.com HVS San Francisco 100 Bush Street, Suite

Discussing Green Building & Property Valuation U.S. Green Building Council Washington, D.C. -- September 16, 2014

Discussing Green Building & Property Valuation U.S. Green Building Council Washington, D.C. -- September 16, 2014 M. Lance Coyle, MAI, SRA, CCIM 2015 President of the Appraisal Institute About the Appraisal

Discussing Green Building & Property Valuation U.S. Green Building Council Washington, D.C. -- September 16, 2014 M. Lance Coyle, MAI, SRA, CCIM 2015 President of the Appraisal Institute About the Appraisal

$450,000 $63,425 $39, % PURCHASE PRICE NET OPERATING INCOME ANNUAL CASH FLOW CAP RATE

Executive Summary Key Property Metrics $450,000 $63,425 $39,143 14.1% PURCHASE PRICE NET OPERATING INCOME ANNUAL CASH FLOW CAP RATE $70,000 $60,000 $50,000 $40,000 $30,000 Annual Cash Flow Repairs, 8%

Executive Summary Key Property Metrics $450,000 $63,425 $39,143 14.1% PURCHASE PRICE NET OPERATING INCOME ANNUAL CASH FLOW CAP RATE $70,000 $60,000 $50,000 $40,000 $30,000 Annual Cash Flow Repairs, 8%