2018 Mackinac County Equalization Report

|

|

|

- Alexina Anthony

- 5 years ago

- Views:

Transcription

1 218 Mackinac County Equalization Report Approved by the Mackinac County Board of Commissioners April 12, 218 Taxable Values are tentative until June 5th

2 Cut River Bridge is a cantilevered steel deck bridge over the Cut River in the Upper Peninsula of the U.S. state of Michigan. It is located along U.S. Highway 2 (US 2) in Hendricks Township, Mackinac County, between Epoufette and Brevort, about 25 miles northwest of St. Ignace and the Straits of Mackinac. There is a long but not often traversed wooden staircase to the valley below that was constructed sometime after the construction of the bridge itself. The bridge was built in 1947 and is one of only two cantilevered deck truss bridges in Michigan, it is 641 feet (195 m) long and contains 888 short tons (793 long tons; 86 t) of structural steel. The bridge carries traffic on US 2 above and spans the Cut River Valley, 147 feet (45 m) below. The State Highway Department designed this structure, and W.J. Meager and Sons, Contractors, built it. Actual construction began in Due to the demand for steel during World War II, construction on the bridge was halted until after the war. Legislation passed in 214 by the Michigan Legislature named the bridge after Heath Michael Robinson, a fallen member of the Navy SEALs who was killed on August 6, 211 in Wardak, Afghanistan when their Chinook helicopter came under fire. *photo credit unknown, online photo*

3

4 CONTENTS Letter of Transmittal Mackinac County Board of Commissioners 218 L-424, dated April 12, 218 Section 1: Preparation of the County Tax Base 218 Parcel Count per unit & Mackinac County total Brief Overview: establishing the tax base Equalization Department Staff Supervisors and Assessors by unit State Tax Commission Property Tax and Equalization Calendar Section 2: Ad Valorem Totals and Analysis 218: What s in the bag. 218 Mackinac County Real and Personal - County Assessed, Tentative Equalized and Tentative Taxable Values 218 Mackinac County Real and Personal - Units Assessed, Tentative Equalized and Tentative Taxable Values Assessing Units ranked by Assessed Value change in Equalized Value by unit Difference between CEV/SEV Taxable Values Ten Year History of Assessed, Equalized and Taxable Values 218 Distribution of Real Property: Assessed, Equalized and Tentative Taxable Values Distribution of Personal Property: Equalized Values Section 3: By Governmental Unit as Reported by Assessors L-422 Report of Assessment Roll Changes and Classification L-423 Summary Analysis for Equalized Valuation

5

6

7

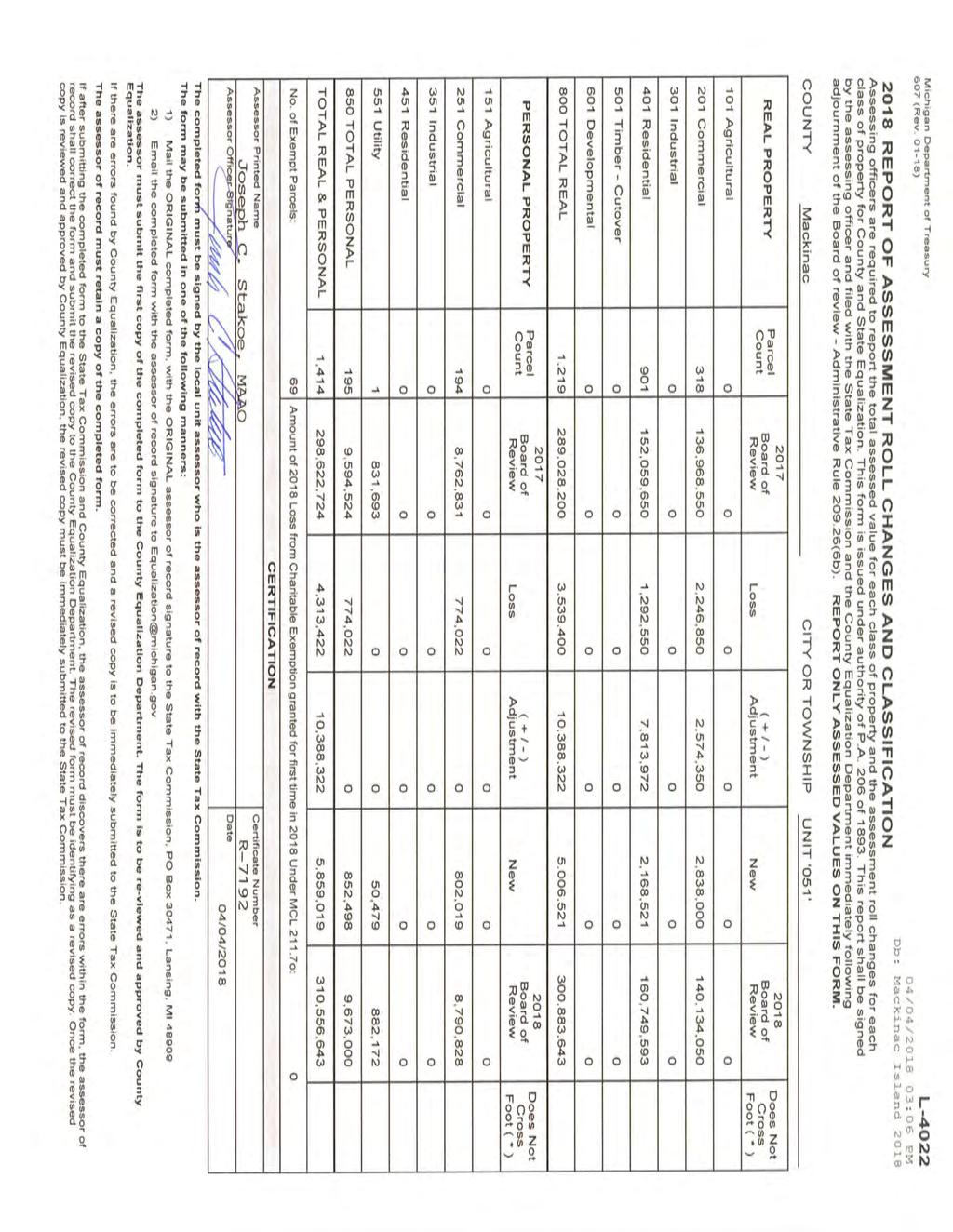

8 Mackinac County Facts Mackinac County is Comprised of 11 Townships and 2 Cities 691, total Acres (1,8 Square Miles) 135, Acres of Federal Land 199,7 Acres of State Land 84 Miles in Length Approximately 23 Miles of Shoreline 37 Islands 88 Inland lakes covering 25, Acres PARCEL COUNT REPORT As reported on the assessors 218 L422's Real/PERS Unit GOVERNMENTAL UNIT REAL PERS Total EXEMPT TOTAL BOIS BLANC BB BREVORT BR CLARK CL GARFIELD GR HENDRICKS HE HUDSON HU MARQUETTE MA MORAN MO TON NE PORTAGE PO ST IGNACE TWP ST CITY OF MACKINAC ISLAND MI CITY OF ST IGNACE SC Mackinac County Totals

9 Brief overview: establishing the tax base The Equalization Department is the second level in the preparation of assessment rolls for property taxation. The first level begins the process with local unit assessors creating an assessment roll which is reviewed by the March Board of Review. After review and acceptance by the March Board of Review, the assessment rolls are submitted to the county equalization departments. The Equalization Department works on behalf of the County Board of Commissioners. The equalization department assists the Board of Commissioners to establish uniform and fair assessments in the county as the second step to establishing the tax base. The county equalized assessments are reviewed and accepted by the County Board of Commissioners. Finally, the county assessment data is submitted to the State Tax Commission for state wide equalization and review. Article 9, Section 3 of the Michigan Constitution of 1963, as amended, established five requirements regarding assessments and taxes: The uniform general ad valorem taxation of real and personal property The determination of true cash value of real and personal property The uniform assessment of real and personal property is not to exceed 5% of true cash value The establishment of a system to equalize assessments The determination of taxable value of each property parcel. Property Classifications: The classification of real and personal property is completed strictly for the equalization process. Although classification reflects property use, classification does not impact the use of the property. There are six real and five personal property classifications: Real Property Personal Property 11 Agricultural 15 Agricultural 21 Commercial 25 Commercial 31 Industrial 35 Industrial 41 Residential 45 Residential 51 Timber cutover 55 Utility 61 Developmental Adjusting assessed values: Properties physically change and values change. Annual adjustments are required to true cash value and assessed values to reflect changes in physical characteristics and in market conditions. Three types of adjustment are used by the assessor for assessed values; two are required due to the legislation created by the Headlee Amendment in New: adjusts for value that is coming on to the assessment roll for the first time Loss: adjusts for value that is removed from the assessment roll. Adjustments: reflect positive or negative changes in value required to maintain the assessed value at 5% according to state law. The categories of Headlee additions and Headlee losses are not used in the equalization process. Mackinac County Equalization Department April 12, 218

10 218 MACKINAC COUNTY EQUALIZATION DEPARTMENT Pamela Chipman, Director, MAAO, PPE David Sullivan, Appraiser, MCAO Jolene Larsen, Equalization Clerk, MCAT We would also like to recognize the contributions of: Sherry Dewitt- MCAT, Equalization Clerk /Legal Description Specialist Emily Reid, Equalization & Mapping Clerk I

11 MACKINAC COUNTY TWP & CITY OFFICIALS SUPERVISOR ASSESSOR SUPERVISOR ASSESSOR BB : BOIS BLANC TOWNSHIP PO -49-1: PORTAGE TOWNSHIP STEPHEN SICINSKI, SUPERVISOR PAULA FILLMAN, ASSR BRENT P SHARPE, SUPERVISOR JOAN SCHROKA, ASSR PO BOX 7 PO BOX 7 P. O. BOX 898 P. O. BOX 898 CURTIS, MI 4982 CURTIS, MI 4982 POINTE AUX PINS, MI PTE AUX PINS, MI ext 3 OFFICE # fax: bbishoroka@yahool.com portageassessor@att.net HC ADDRESSES USE ZIP CODE ST : ST.IGNACE TOWNSHIP BR : BREVORT TOWNSHIP STEVEN CAMPBELL, SUPERVISOR DAWN NELSON, ASSR 324 GORMAN RD 3119 Ingalsbe Rd. ED SERWACH, SUPERVISOR SHERRY BURD, ASSR ST.IGNACE, MI P. O. BOX S LAKESIDE RD dawnnelson@charter.net MORAN, MI CEDARVILLE, MI TEL: CL : CLARK TOWNSHIP sherryburd@aol.com MI : CITY OF MACKINAC ISLAND GARY REID, SUPERVISOR SHERRY BURD, ASSR CITY OFFICE JOSEPH STAKOE, ASSR. P. O. BOX 367 P. O. BOX MARKET STREET 325 E LAKE ST STE #29 CEDARVILLE, MI N. BLINDLINE RD. PO BOX 187 PETOSKEY, MI 4977 office CEDARVILLE, MI MACKINAC ISLAND, MI (PETOSKEY) fax OFFICE: FAX FAX: MARGRET M DOUD, MAYOR CELL assessor@clarktwp.org jstakoe@nappraisal.net GR : GARFIELD TOWNSHIP SC : CITY OF ST.IGNACE DONALD BUTKOVITCH, SUPERVISOR JANET MAKI, ASSR PO BOX CO RD 457 CITY OFFICE Vacant- ASSR. ENGADINE, MI BERRY, MI N STATE ST 396 N. STATE STREET (HOME) ST IGNACE, MI ST.IGNACE, MI jmakipenttwp@gmail.com OFFICE OFFICE FAX FAX HE : HENDRICKS TOWNSHIP CONNIE LITZNER, MAYOR siassessor@lighthouse.net HOWARD HOOD, SUPERVISOR ELIZABETH ZABIK, ASSR N 85 H POND ST Naubinway, MI MACKINAW CITY, MI bettyjo68@gmail.com HU : HUDSON TOWNSHIP EQUALIZATION DEPARTMENT ALLYN GARAVAGLIA, SUPERVISOR SUZANNE NELSON, ASSR DIRECTOR W783 Hiawatha trl 7961 Hurd Rd. PO BOX 136 PAMELA CHIPMAN, MAAO PPE 1 S. NAUBINWAY, MI Naubinway, MI Marley, Rm FAX ST.IGNACE, MI APPRAISER HOME hudsontwpassessor@gmail.com OFFICE DAVID SULLIVAN, MCAO CELL 119 B ST. MA : MARQUETTE TOWNSHIP FAX Cheboygan, MI equalize@mackinaccounty.net OFFICE JOHN KRONEMEYER, SUPERVISOR KATIE VANEENENAAM-CARPENTER davids@mackinaccounty.net E 7177 James St S PARK AVE CLERK PICKFORD, MI CEDARVILLE, MI JOLENE LARSEN, MCAT HOME PO BOX TWP marquettetownshipassessor@gmail.com ST. IGNACE, MI FAX OFFICE MO : MORAN TOWNSHIP equalclerk@mackinaccounty.net PATRICK J. DURM, SUPERVISOR EDWARD VANDERVRIES MORAN TWP. HALL STREET ADDRESS 716 VENICE DR P. O. BOX 364 W1362 US #2 PORTAGE, MI 4924 ST. IGNACE, MI OFFICE OFFICE HRS: 1st & 3rd Friday monthly FAX cell NE : TON TOWNSHIP evandervries@hotmail.com FRED BURTON, SUPERVISOR THOMAS W. KITZMAN N661 H S. County Rd. 442 GOULD CITY, MI Cooks, MI , ext cell home assessortrk@centurylink.net

12 512 (Rev. 4-15) RICK SNYDER GOVERNOR STATE OF MICHIGAN DEPARTMENT OF TREASURY LANSING NICK A. KHOURI STATE TREASURER TO: FROM: Equalization Directors and Assessors The State Tax Commission Bulletin No. 17 of 217 Annual Calendar October 3, 217 SUBJECT: Property Tax and Equalization Calendar for 218 STATE TAX COMMISSION 218 PROPERTY TAX, COLLECTIONS AND EQUALIZATION CALENDAR By the 1 st day of each month By the 15 th day of each month December 1, 217 County Treasurer must account for and deliver to the State the State Education Tax collections on hand on or before the fifteenth day of the immediately preceding month. MCL (1) County Treasurer must account for and deliver to the State the State Education Tax collections on hand on the last day of the preceding month. MCL (1) Results of equalization studies should be reported to assessors of each Township and City. December 31, 217 Tax Day for 218 assessments and 218 property taxes. MCL January 2, 218 December 31, 217 is a Sunday, January 1, 218 is a State Holiday January 1, 218 Deadline for an owner that had claimed a conditional rescission of a Principal Residence Exemption to verify with the assessor that the property still meets the requirements for the conditional rescission through a second and third year annual verification of a Conditional Rescission of Principal Residence Exemption (PRE) (form 464) (on or before December 31). MCL 211.7cc(5) Deadline for counties to file 217 equalization studies for 218 starting bases with State Tax Commission (STC) for all classifications in all units on STC form L-418. [R 29.41(5)] Except as otherwise provided in section 9m, 9n, or 9o, Assessors and/or Supervisors are required to annually send a personal property statement to any taxpayer they believe has personal property in their possession in their local unit. Form Personal Property Statements must be sent or delivered no later than January 1 each year. P.O. BOX 3471 LANSING, MICHIGAN

13 Page 2 January 24, 218 February 1, 218 Local units with an SEV of $15,, or Less: 217 taxes collected by January 1 must be distributed within 1 business days of January 1. MCL (5) All other local units: Must distribute 217 taxes collected within 1 business days after the 1st and 15th of each month except in March. MCL (3)(a) Deadline for a qualified business to submit STC form L-4143 for qualified personal property with the assessor (not later than February 1). MCL 211.8a(2) Notice by certified mail to all properties that are delinquent on their 216 property taxes (not later than February 1). MCL f(1) February 1, 218 February 14, 218 February 15, 218 Property Services Division staff reports to the State Tax Commission on the progress and quality of equalization studies for each county on preliminary Form L-43. Deadline to file the affidavit to claim the exemption for Eligible Personal Property Form 576. See the Assessor Guide to Small Business Taxpayer Exemption for more information. MCL 211.9o(2) Last day to pay property taxes without the imposition of a late penalty charge equal to 3% percent of the tax in addition to the property tax administration fee, if any. MCL (3) The governing body may waive the penalty for the homestead property of a senior citizen, paraplegic, quadriplegic, hemiplegic, eligible service person, eligible veteran, eligible widow or widower, totally and permanently disabled or blind persons, if that person has filed a claim for a homestead property tax credit with the State Treasurer before February 15. Also applies to a person whose property is subject to a farmland/development rights agreement if they present a copy of the development rights agreement or verification that the property is subject to the development rights agreement before February 15. If statements are not mailed by December 31, the local unit may not impose the 3% late penalty charge. A local unit of government that collects a summer property tax shall defer the collection until this date for property which qualifies. MCL (3) STC reports assessed valuations for DNR lands to assessors. MCL (2)

14 Page 3 February 16, 218 Feb. 17 is a Saturday Feb. 18 is a Sunday Feb. 19 is a State Holiday February 2, 218 Deadline for county equalization director to publish in a newspaper, the tentative equalization ratios and estimated SEV multipliers for 218, and to provide a copy to each assessor and board of review in the county. All notices of meetings of the boards of review must give the tentative ratios and estimated multipliers pertaining to their jurisdiction. MCL a(1) (on or before the third Monday in February). Deadline for taxpayer filing of personal property statement with assessor. Form 5278 must be filed not later than February 2 for each personal property parcel for which the Eligible Manufacturing Personal Property exemption is being claimed. Deadline for taxpayer to file form 3711 if a claim of exemption is being made for heavy earth moving equipment. STC Bulletin 4 of 21; MCL (2) Deadline for payments to municipalities from the Local Community Stabilization Authority: Local Community Stabilization Share revenue for county extravoted millage, township millage, and other millages levied 1% in December. MCL (5)(b) February 28, 218 Last day for local treasurers to collect 217 property taxes. MCL a March 1, 218 The STC shall publish the inflation rate multiplier before March 1. (MCL d(15). Properties with delinquent 216 taxes, forfeit to the County Treasurer. MCL g(1). County Treasurer adds $175 fee per MCL g(1), as well as all recording fees and all fees for service of process or notice. MCL g(3)(d) 216 tax-delinquent redemptions require additional interest at noncompounded rate of ½% per month from March 1 forfeiture. MCL g(3)(b) County Treasurer commences settlement with local unit treasurers. MCL County Property Tax Administration Fee of 4% added to unpaid 217 taxes and interest at 1% per month. MCL a(3) Local units to turn over 217 delinquent taxes to the County Treasurer. MCL a(2). On March 1 in each year, taxes levied in the immediately preceding year that remain unpaid shall be returned as delinquent for collection. However, if the last day in a year that taxes are

15 Page 4 March 1, 218 Cont. March 5, 218 March 6, 218 due and payable before being returned as delinquent is on a Saturday, Sunday, or legal holiday, the last day taxes are due and payable before being returned as delinquent is on the next business day and taxes levied in the immediately preceding year that remain unpaid shall be returned as delinquent on the immediately succeeding business day The 218 assessment roll shall be completed and certified by the assessor. MCL (on or before the first Monday in March). The assessor/supervisor shall submit the 218 certified assessment roll to the Board of Review (BOR). MCL (1) (Tuesday after first Monday in March) Organizational meeting of Township Board of Review. MCL City BOR may vary according to Charter provisions. March 12, 218 March 14, 218 March 3, 218 March 31 is a Saturday April 1 is a Sunday The BOR must meet on the second Monday in March. This meeting must start not earlier than 9 a.m. and not later than 3 p.m. The BOR must meet one additional day during this week and shall hold at least 3 hours of its required sessions during the week of the second Monday in March after 6 p.m. MCL Note: The governing body of a city or township may authorize an alternative starting date for the second meeting of the March Board of Review, which can be either the Tuesday or the Wednesday following the second Monday in March. MCL211.3(2) Within ten business days after the last day of February, at least 9% of the total tax collections on hand, must be delivered by the local unit treasurer to the county and school district treasurers. MCL (3)(b) District or ISD must reach agreement for summer tax collection with township or city, or county if there is a summer school levy. MCL (2) Not later than April 1, local unit treasurers make final adjustment and delivery of the total amount of tax collections on hand. MCL (3)(c) Last day to pay all forfeited 215 delinquent property taxes, interest, penalties and fees, unless an extension has been granted by the circuit court. If unpaid, title to properties foreclosed for 215 real property taxes vests solely in the foreclosing governmental unit. MCL k Assessors are required to annually provide a copy of Form 5278 and Form 5277 (rescission affidavit) and other parcel information required by the Department of Treasury in a form and manner required by the Department of Treasury no later than April 1 of each year. (MCL 211.9m and 9n)

16 Page 5 March 3, 218 Cont. April 1, 218 April 2, 218 April 4, 218 No later than April 1, assessors shall transmit to the Department of Treasury the information contained in Form 5278, Eligible Manufacturing Personal Property Tax Exemption Claim, Personal Property Statement and Report of Fair Market Value of Qualified New and Previously Existing Personal Property (Combined Document), in a form and manner as directed by the Department. MCL 211.9m and MCL 211.9n Separate tax limitations voted after April 1 of any year are not effective until the subsequent year. MCL i(2) On or before the first Monday in April, the BOR must complete their review of protests of assessed value, taxable value, property classification or denial by assessor of continuation of qualified agricultural property exemption. MCL 211.3a The township supervisor or assessor shall deliver the completed assessment roll, with BOR certification, to the county equalization director not later than the tenth day after adjournment of the BOR or the Wednesday following the first Monday in April, whichever date occurs first. MCL 211.3(7) An assessor shall file STC form L-421 with the County Equalization Department, and STC form L-422 (signed by the assessor) with the County Equalization Department and the STC, immediately following adjournment of the board of review. (STC Administrative Rule: R 29.26(6a), (6b)). The form L-422 must be signed by the assessor of record. Form 4626 Assessing Officers Report of Taxable Values as of State Equalization due to the County. April 1, 218 County Board of Commissioners meets in equalization session. MCL 29.5(1) and (1) The equalization director files a tabular statement of the county equalization adopted by the County Board of Commissioners on Form L- 424 prescribed and furnished by the STC, immediately after adoption. County equalization shall be completed and official report (Form L- 424) filed with STC prior to May 7, 218. (first Monday in May) MCL 29.5(2) The Property Services Division staff makes a final report to the State Tax Commission on Form L-43 after the adoption of the 218 equalization

17 Page 6 report by the County Board of Commissioners and prior to Preliminary State Equalization. April 16, 218 Equalization director files separate Form L-423 for each unit in the county with the STC no later than the third Monday in April. STC Rule 29.41(6); MCL (4) Allocation Board meets and receives budgets. MCL Equalization Director submits separate Form 4626 for each unit in the county with the STC no later than the third Monday in April. May 1, 218 Final day for completion of delinquent tax rolls. MCL (1) Deadline for filing a Principal Residence Exemption (PRE) Active Duty Military Affidavit to allow military personnel to retain a PRE for up to three years if they rent or lease their principal residence while away on active duty. MCL 211.7dd Last day of deferral period for winter (December 1) property tax levies, if the deferral for qualified taxpayers was authorized by the County Board of Commissioners. MCL (3) Deadline for filing the Farmland Exemption Affidavit (Form 2599) with the local assessor if the property is NOT classified agricultural or if the assessor asks an owner to file it to determine whether the property includes structures that are not exempt. Deadline for Department of Treasury to post the millage rate comparison reports on the PPT Reimbursement website. MCL (5) May 7, 218 Deadline for filing official County Board of Commissioners report of county equalization (L-424) with STC. MCL 29.5(2) (first Monday in May) Appeal from county equalization to Michigan Tax Tribunal must be filed within 35 days after the adoption of the county equalization report by the County Board of Commissioners. MCL (3) Deadline for assessor to file tabulation of Taxable Valuations for each classification of property with the county equalization director on STC form L-425 to be used in Headlee calculations. MCL d(2). (first Monday in May)

18 Page 7 May 14, 218 May 15, 218 May 29, 218 May 28 is a State Holiday After May 3 and Before June 6, 218 Preliminary state equalization valuation recommendations presented by the Property Services Division staff to the State Tax Commission. MCL 29.2(1) (second Monday in May) Not later than this date, the State must have prepared an annual assessment roll for the state-assessed properties. MCL 27.9(1) State Equalization Proceeding - Final State Equalization order is issued by State Tax Commission. MCL 29.4 (fourth Monday in May) Last day for Allocation Board Hearing (not less than 8 days or more than 12 days after issuance of preliminary order). MCL May 31, 218 (MTT) Appeals of property classified as commercial real, industrial real, developmental real, commercial personal, industrial personal or utility personal must be made by filing a written petition with the Michigan Tax Tribunal on or before May 31 of the tax year involved. MCL a(6) June 1, 218 If as a result of State Equalization, the taxable value of property changes, the Equalization Director shall revise the millage reduction fractions by the Friday following the fourth Monday in May. MCL d(2) Deadline for filing Principal Residence Exemption Affidavits (form 2368) for exemption from the 18-mill school operating tax to qualify for a PRE for the summer tax levy. MCL 211.7cc(2) Deadline for filing the initial request (first year) of a Conditional Rescission of Principal Residence Exemption (PRE) (form 464) for the summer tax levy. MCL 211.7cc(5) Deadline for filing for Foreclosure Entity Conditional Rescission of a PRE (Form 4983) to qualify for the summer tax levy. MCL 211.7cc(5) Assessment Roll due to County Treasurer if local unit is not collecting summer taxes. MCL b(6)(a) Last day to send the first notice to all properties that are delinquent on 217 taxes. MCL b No later than June 1, the county treasurer delivers to the state treasurer a statement listing the total amount of state education tax (SET) not returned delinquent, collected by the county treasurer, and collected and remitted to the county treasurer by each city or township treasurer, also a statement for the county and for each city or township of the number of parcels from which the SET was collected, the number of parcels for which SET was billed, and the total amount retained by the county treasurer and by the city or township treasurer MCL b(12) Requests are due from a Brownfield Redevelopment Authority, Tax

19 Page 8 Increment Finance Authority, Local Development Financing Authority or Downtown Development Authority for state reimbursements of tax increment revenue decreases as a result of the MBT reduction in personal property taxes (not later than June 1). Form 465; P.A of 28. June 4, 218 Deadline for notifying protesting taxpayers in writing of Board of Review Action (by the first Monday in June). MCL 211.3(4) County Equalization Director calculates current year millage reduction fractions including those for inter-county taxing jurisdictions. The completed, verified STC form L-428 is filed with the County Treasurer and the STC on or before the first Monday in June. MCL d(3) June 5, 218 Deadline for Assessors to report the current year taxable value of commercial personal property and industrial personal property to the County Equalization Director (each June 5). MCL (3) Deadline for Assessors to file the Personal Property 218 Taxable Value for Expired Tax Exemptions Form 543 with the County Equalization Director and Department of Treasury (each June 5). MCL (6) Deadline for Assessors to file the Personal Property 218 Taxable Value for Expired/Expiring Renaissance Zone Tax Exemptions Form 5429 with the County Equalization Director and Department of Treasury (each June 5). MCL (6) June 11, 218 June 15, 218 Allocation Board must issue final order not later than the second Monday in June. MCL Deadline for submission of Water Pollution Control PA 451 of 1994 Part 37 and Air Pollution Control PA 451 of 1994 Part 59 tax exemption applications to the State Tax Commission. Note: Applications for the above exemption programs received on or after June 16 shall be considered by the Commission contingent upon staff availability. Deadline for the assessor s report to the STC on the status of each Neighborhood homestead exemption granted under the Neighborhood Enterprise Zone Act. MCL (2) Deadline for foreclosing governmental units to file petition for tax foreclosure with the circuit court clerk for the March 1, 218 forfeitures. MCL h(1) Deadline for Tax Increment Finance (TIF) Authorities to file the 218 TIF loss reimbursement claims Form 5176, Form 5176BR, or Form 5176ICV. MCL a(3)

20 Page 9 June 2, 218 Deadline for County Equalization Directors to file the Personal Property Summary Report (PPSR) and the Personal Property Inter-County Summary Report (PPSR-IC) to the Department of Treasury. MCL (3) June 25, 218 June 29, 218 June 3 is a Saturday Deadline for equalization directors to file tabulation of final Taxable Valuations with the State Tax Commission on STC form L-446. MCL d (fourth Monday in June) Summer Tax Levy for School Millage Detail and Tax Roll. MCL (4)(c). Before June 3 the county treasurer or the treasurer of the school district or intermediate school district shall spread the taxes being collected. County Treasurer to spread summer SET and County Allocated and Prepare Tax Roll MCL b(6)(b). Not later than June 3, the county treasurer or the state treasurer shall spread the millage levied against the assessment roll and prepare the tax roll. Deadline for classification appeals to STC. MCL c(6). A classification appeal must be filed with the STC in writing on Form 2167 (June 3). Deadline for County Equalization Director to file Interim Status Report of the ongoing study for the current year. [R 29.41(4)] Township supervisor shall prepare and furnish the summer tax roll before June 3 to the township treasurer with supervisor s collection warrant attached if summer school taxes are to be collected. MCL (1) July 2, 218 July 1 is a Sunday July 3, 218 July 17, 218 Taxes due and payable in those jurisdictions authorized to levy a summer tax. (Charter units may have a different due date). MCL a(3) and (4) Deadline for governmental agencies to exercise the right of refusal for 217 tax foreclosure parcels. MCL m(1) The July BOR may be convened to correct a qualified error (Tuesday after the third Monday in July). MCL b. The governing body of the city or township may authorize, by adoption of an ordinance or resolution, 1 or more of the following alternative meeting dates for the purposes of this section. An alternative meeting date during the week of the third Monday in July. MCL b(9)(b) An owner who owned and occupied a principal residence on May 1 for taxes levied before January 1, 213, for which the exemption was not on the tax roll may file an appeal with the July Board of Review in the year

21 Page 1 for which the exemption was claimed or the immediately succeeding 3 years. For taxes levied after December 31, 212, an owner who owned and occupied a principal residence on June 1 or November 1 for which the exemption was not on the tax roll may file an appeal with the July Board of Review in the year for which the exemption was claimed or the immediately succeeding 3 years. MCL 211.7cc(19) July 17, 218 Cont. An owner of property that is Qualified Agricultural Property on May 1 may appeal to the July Board of Review for the current year and the immediately preceding year if the exemption was not on the tax roll. MCL 211.7ee(6) July BOR may hear appeals for current year only for poverty exemptions, but not poverty exemptions denied by the March Board of Review. MCL 211.7u, STC Bulletin No. 6 of 217. July 31, 218 Industrial Facilities Exemption Treasurer s Report (Form 17) must be filed with the Property Services Division on or before July 31 of the tax year involved. Appeals of property classified as residential real, agricultural real, timber-cutover real or agricultural personal must be made by filing a written petition with the Michigan Tax Tribunal on or before July 31 of the tax year involved. MCL a(6) August 15, 218 A protest of assessed valuation or taxable valuation or the percentage of Qualified Agricultural Property exemption subsequent to BOR action, must be filed with the Michigan Tax Tribunal, in writing on or before July 31. Deadline for Local School Districts and Intermediate School Districts to file the Personal Property Exemption Loss 218 Debt Millage Reimbursement Claim for School Districts & Intermediate School Districts (ISDs) Form MCL (4) Deadline for electronically paying and filing the essential services assessment with the Department of Treasury without interest and penalty. MCL August 2, 218 Deadline for taxpayer to file appeal directly with the Michigan Tax Tribunal if final equalization multiplier exceeds tentative multiplier and a taxpayer s assessment, as equalized, is in excess of 5 percent of true cash value (by the third Monday in August). MCL (7)

22 Page 11 September 1, 218 September 14, 218 Last day to send second notice by first class mail to all properties that are delinquent on 217 taxes. MCL c Summer Taxes Due: Summer taxes due, unless property is located in a city with a separate charter due date (Sept 14). MCL b(1), MCL (4)(e). MCL Interest of 1% per month will accrue if the payment is late for the State Education Tax and County Taxes that are part of the summer tax collection. MCL b(9) and a(6). Note: date may be different depending on the city charter. Last day of deferral period for summer property tax levies, if the deferral for qualified taxpayers. MCL (7). September 2, 218 September 28, 218 September 29 is a Saturday September 3 is a Sunday October October 1, 218 October 15, 218 Deadline for payments to counties from the Local Community Stabilization Authority: Local Community Stabilization Share revenue for county allocated millage. MCL (5)(a) Clerk of township or city delivers to supervisor and county clerk a certified copy of all statements, certificates, and records of vote directing monies to be raised by taxation of property. MCL (1). Financial officer of each unit of local government computes tax rates in accordance with MCL d and MCL and governing body certifies that rates comply with Section 31, Article 9, of 1963 Constitution and MCL e, Truth in Taxation, on STC form L-429 on or before September 3. County prosecutor is obligated by statute to furnish legal advice promptly regarding the apportionment report. A County Board of Commissioners shall not authorize the levy of a tax unless the governing body of the taxing jurisdiction has certified that the requested millage has been reduced, if necessary, in compliance with Section 31 of Article 9 of the State Constitution of 1963 and MCL d, and (1). The County Board also receives certifications that Truth in Taxation hearings have been held if required. MCL e County Treasurer adds $15 for each parcel of property for which the 215 real property taxes remain unpaid. MCL d The assessor reports the status of real and personal Industrial Facility Tax property to STC. MCL (2) Governmental units report to the STC on the status of each exemption granted under the Commercial Redevelopment Act. MCL

23 Page 12 October 15, 218 Cont. Qualified local governmental units report to the STC on the status of each exemption granted under the Commercial Rehabilitation Act. MCL The assessor s annual report of the determination made under MCL (1) to each taxing unit that levies taxes upon property in the local governmental unit in which a new facility or rehabilitated facility is located and to each holder of the Neighborhood Enterprise Zone certificate. MCL (2) Qualified local governmental units report to the STC on the status of each exemption granted under the Obsolete Property Rehabilitation Act. MCL October 22, 218 October 2 is a Saturday October 31, 218 Deadline for payments to municipalities from the Local Community Stabilization Authority: Local Community Stabilization Share revenue for other millages not levied 1% in December. MCL (5)(c) October apportionment session of the County Board of Commissioners to examine certificates, direct spread of taxes in terms of millage rates to be spread on Taxable Valuations. MCL Deadline for submission of New Personal Property PA 328 of 1998, Obsolete Property PA 146 of 2, Commercial Rehabilitation PA 21 of 25, Neighborhood Enterprise Zone PA 147 of 1992, Commercial Facilities PA 255 of 1978 and Industrial Facilities PA 198 of 1974 tax exemption applications to the State Tax Commission. Note: Applications for the above exemption programs received after October 31 shall be considered by the Commission contingent upon staff availability. November 1, 218 Deadline for filing Principal Residence Exemption Affidavits (form 2368) for exemption from the 18-mill school operating tax to qualify for a PRE for the winter tax levy. MCL 211.7cc(2) Deadline for filing the initial request (first year) of a Conditional Rescission of Principal Residence Exemption (PRE) (form 464) for the winter tax levy. MCL 211.7cc(5) Deadline for filing for Foreclosure Entity Conditional Rescission of a PRE to qualify for the winter tax levy. MCL 211.7cc (5)

24 Page 13 November 5, 218 November 15, 218 November 28, 218 November 3, 218 December 1 is a Saturday On or before November 5, Township Supervisor shall notify township treasurer of the amount of county, state and school taxes apportioned in township to enable treasurer to obtain necessary bond for collection of taxes. MCL (1) Form 6/L-416, Supplemental Special Assessment Report due to the STC. On or before November 28, Township Treasurer gives County Treasurer a bond running to the county in the actual amount of county, state and school taxes. MCL (2) County Equalization Director submits apportionment millage report to the STC. MCL On or before December 1, County Treasurer delivers to township supervisor a signed statement of approval of the bond and the township supervisor delivers the tax roll to the township treasurer. On or before December 1, Deadline for foreclosing governmental units to transfer list of unsold 218 tax foreclosure parcels to the clerk of the city, township, or village in which the parcels are located. MCL m(6) December 1, taxes due and payable to local unit treasurer are a lien on real property. Charter cities or villages may provide for a different day. MCL Results of equalization studies should be reported to assessors of each Township and City. MTT Note: December 11, 218 Appeal to Michigan Tax Tribunal of a contested tax bill must be filed within 6 days after the mailing of the tax bill that the taxpayer seeks to contest. MCL (Limited to arithmetic errors) Special Board of Review meeting may be convened by assessing officer to correct qualified errors (Tuesday after the second Monday in Dec.). MCL b. The governing body of the city or township may authorize, by adoption of an ordinance or resolution, one or more of the following alternative meeting dates for the purposes of this section: An alternative meeting date during the week of the second Monday in December. MCL b(7) An owner who owned and occupied a principal residence on May 1 for taxes levied before January 1, 212, for which the exemption was not on the tax roll may file an appeal with the December Board of Review in the year for which the exemption was claimed or the immediately succeeding 3 years. For taxes levied after December 31, 211, an owner

25 Page 14 who owned and occupied a principal residence on June 1 or November 1 for which the exemption was not on the tax roll may file an appeal with the December Board of Review in the year for which the exemption was claimed or the immediately succeeding 3 years. MCL 211.7cc(19) December 11, 218 Cont. An owner of property that is Qualified Agricultural Property on May 1 may appeal to the December Board of Review for the current year and the immediately preceding year if the exemption was not on the tax roll. MCL 211.7ee(6) December Board of Review to hear appeals for current year poverty exemptions only, but not poverty exemptions denied by the March Board of Review. MCL 211.7u, STC Bulletin No. 6 of 217 December 31, 218 Tax Day for 219 property taxes. MCL 211.2(2) All taxes due and liens are canceled for otherwise unsold 218 tax foreclosure parcels purchased by the state or transferred to the local unit or the Michigan Land Bank Fast Track Authority. MCL m(12) and (13) An eligible claimant may appeal an assessment levied, a penalty or rescission under the Essential Service Assessment Act to the Michigan Tax Tribunal by filing a petition no later than December 31 in that same tax year. The Department of Treasury may appeal the 218 classification of any assessable property to the Small Claims Division of the Michigan Tax Tribunal. MCL c(7) Deadline for an owner that had claimed a conditional rescission of a Principal Residence Exemption to verify to the assessor that the property still meets the requirements for the conditional rescission through a second and third year annual verification of a Conditional Rescission of Principal Residence Exemption (PRE) (form 464). MCL 211.7cc(5) Deadline for a land contract vendor, bank, credit union or other lending institution that had claimed a foreclosure entity conditional rescission of a Principal Residence Exemption to verify to the assessor that the property still meets the requirements for the conditional rescission through the filing of an annual verification of a foreclosure entity. (MCL 211.7cc (5) A rescission affidavit (form 5277) shall be filed with the assessor of the Township or City in which the personal property is located, no later than December 31 of the year in which the exempted property is no longer eligible for the Eligible Manufacturing Personal Property exemption.

26 Page 15 January 2, 219 December 31 is a State holiday January 1 is a State Holiday Deadline for counties to file equalization studies for 219 starting bases with State Tax Commission for all classifications in all units on STC form L-418. [R 29.41(5)].

27 218 Analysis: What s in the bag.. Potential Revenue: One 1 mill applied to the tentative taxable value will yield a revenue of $1,21,569. A millage rate of.5 mills applied to the tentative taxable value will yield $51,785. Potential revenue based on the county allocation of 4.5 mills is $4,597,6. Taxable Value continues to increase, still lagging behind the Equalized Value The 218 inflation rate multiplier is 1.21 or 2.1%. This is used in the formula to calculate 218 taxable value. The current difference between equalized and taxable value is 23.99%. In 27, the gap separating total Mackinac County State Equalized Value and Taxable Value peaked at 56.19%. Between 28 and 212, State Equalized Values slid 14.34% while Taxable Values continued to increase until 29. After a slight 21 decline, taxable values resumed a steady increase. The average annual increase between 211 and 218 is 2.8%. The total tentative taxable value for real property has increased 2.32%. For comparison, the 218 Cost of Living Adjustment (COLA) is 2%. Comparing 217 and 218 equalized values, Brevort Township exhibits the greatest growth in value (6.25%) and Hendricks the least (.18%). Three units have declining equalized values. Garfield Township has the smallest decrease (-1.86%) and Newton Township the greater decline in equalized value (- 4.1%). Real residential property (41) values comprise the largest percentage of total equalized value (77.32%); Real commercial property (21) is second (19.38%). There is little shifting of value between classes. Parcel counts by class are showing minimal variation between 217 and 218. Clark Township reports an increase in agricultural value (11 class) over 12 parcels. Garfield Township has the largest agricultural class at 182 parcels and reports a slight decrease in value (-1.45%). The city of Mackinac Island has the largest commercial class (21) with 318 parcels and an increase in commercial equalized value of 2.31%. The largest industrial class (31) is in Clark Township (55 parcels) with a value increase of 2.51%. Clark Township has the greater number of residential classed parcels ( 3,149) and 218 values are 4.% higher than in 217. Brevort Township had the most growth in residential value at 7.24%. There are only 111 parcels in the 51 timber cutover class county wide. The total 51 class in Mackinac County has decreased -6.64% - which most likely does not reflect falling land prices but a correction in assessing/valuation methods. Due to the nature of personal property valuation, decreases in overall value would generally indicate that accrued depreciation exceeded new personal property acquisition. Commercial and industrial personal property investment is most likely masked by the more recently granted Small Business and Eligible Manufacturing Exemptions. Mackinac County Equalization Department 218 Equalization Report Mackinac County Board of Commissioners April 12, 218.

28 Mackinac County 218 Assessed, County Equalized and Tentative Taxable Values Tentative Mackinac County Assessed Equalized Taxable Agricultural 11 14,295,211 14,295,211 9,99,313 Commercial ,269,99 216,269,99 169,24,177 Industrial 31 18,84,26 18,84,26 16,14,874 Residential ,892, ,892, ,12,447 Timber/Cutover 51 3,731,96 3,731,96 2,24,841 Total Real 1,115,992,764 1,115,992, ,615,652 Agricultural 151 Commercial ,151,37 17,151,37 17,125,27 Industrial 351 8,2,25 8,2,25 8,2,25 Residential 451 Utility ,327, ,327, ,627,883 Total Personal 15,678,938 15,678, ,953,358 Grand Total 1,266,671,72 1,266,671,72 1,21,569,1 Mackinac County Equalization Department 218 Equalization Report Mackinac County Board of Commissioners April 12, 218

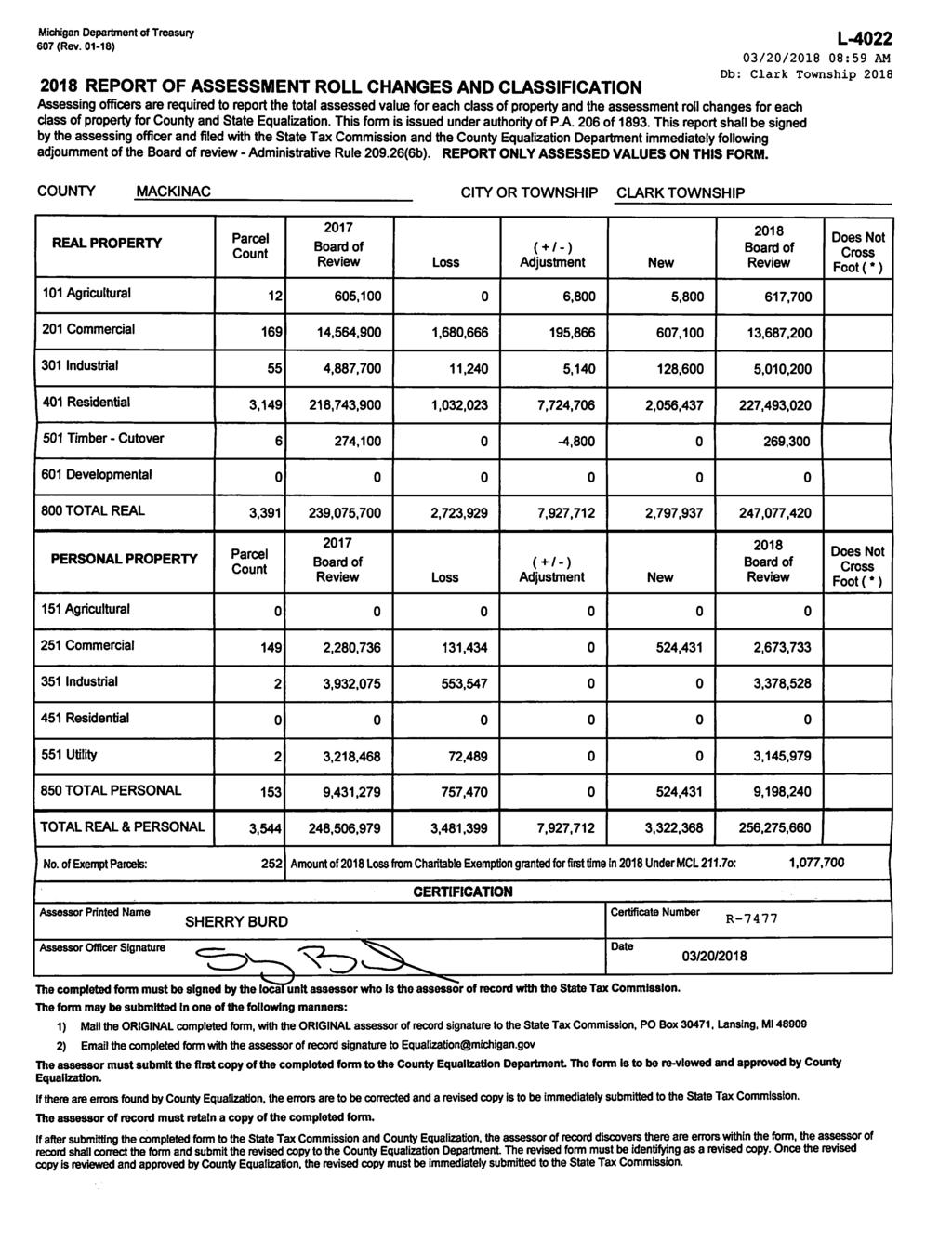

29 Mackinac County 218 Assessed, County Equalized and Tentative Taxable Values Tentative Equalization Tentative Equalization Bois Blanc Township Assessed Equalized Taxable Factor Brevort Township Assessed Equalized Taxable Factor Agricultural 11 Agricultural 11 13, 13, 75,42 1. Commercial ,85 662,85 589,14 1. Commercial ,3 432,3 399, Industrial 31 Industrial ,8 156,8 99, Residential 41 41,449,35 41,449,35 32,532, Residential 41 39,341,4 39,341,4 27,299,85 1. Timber/Cutover 51 Timber/Cutover 51 Total Real 42,112,2 42,112,2 33,121,448 Total Real 4,33,5 4,33,5 27,874,78 Agricultural 151 Agricultural 151 Commercial Commercial 251 1, 1, 1, 1. Industrial 351 Industrial 351 Residential 451 Residential 451 Utility ,8 267,8 267,8 1. Utility 551 1,698,821 1,698,821 1,668, Total Personal 268,1 268,1 268,1 Total Personal 1,78,821 1,78,821 1,678,539 Grand Total 42,38,3 42,38,3 33,389,548 Grand Total 41,742,321 41,742,321 29,552, Tentative Equalization Tentative Equalization Clark Township Assessed Equalized Taxable Factor Garfield Township Assessed Equalized Taxable Factor Agricultural ,7 617,7 411, Agricultural 11 8,162,988 8,162,988 6,8,45 1. Commercial 21 13,687,2 13,687,2 11,849, Commercial 21 3,69,67 3,69,67 3,7, Industrial 31 5,1,2 5,1,2 4,425, Industrial ,68 529,68 473,88 1. Residential ,493,2 227,493,2 17,198, Residential 41 68,163,625 68,163,625 6,437, Timber/Cutover ,3 269,3 148,28 Timber/Cutover 51 Total Real 247,77,42 247,77,42 187,34,272 Total Real 8,465,9 8,465,9 69,998,813 Agricultural 151 Agricultural 151 Commercial 251 2,673,733 2,673,733 2,673, Commercial , , , Industrial 351 3,378,528 3,378,528 3,378, Industrial 351 2,63,767 2,63,767 2,63, Residential 451 Residential 451 Utility 551 3,145,979 3,145,979 3,145, Utility ,745,848 12,745,848 12,632, Total Personal 9,198,24 9,198,24 9,198,24 Total Personal 15,33,957 15,33,957 14,92,63 Grand Total 256,275,66 256,275,66 196,232,512 Grand Total 95,499,857 95,499,857 84,919,416 Mackinac County Equalization Department 218 Equalization Report Mackinac County Board of Commissioners April 12, 218

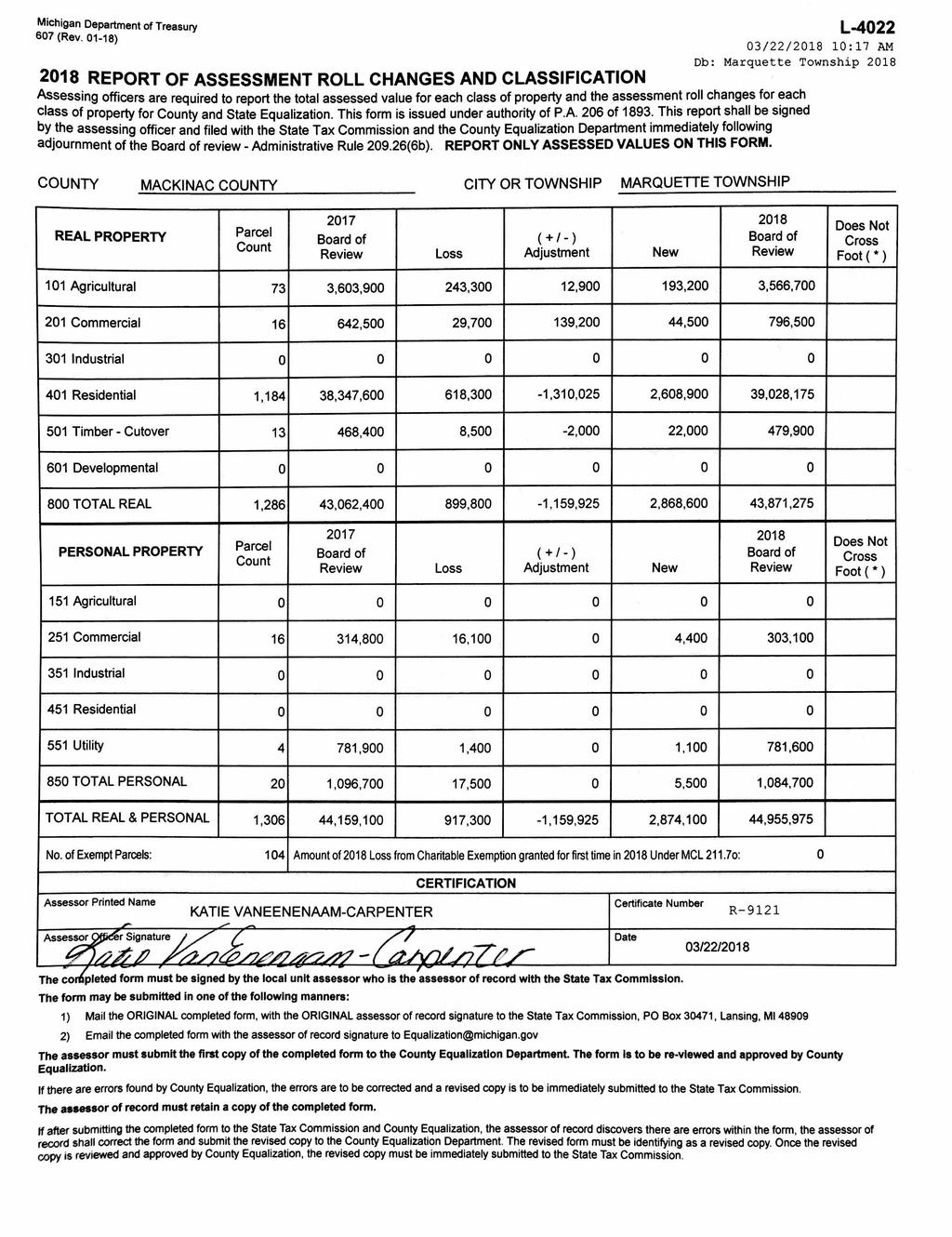

30 Mackinac County 218 Assessed, County Equalized and Tentative Taxable Values Tentative Equalization Tentative Equalization Hendricks Township Assessed Equalized Taxable Factor Hudson Township Assessed Equalized Taxable Factor Agricultural 11 Agricultural 11 Commercial , ,213 57, Commercial ,42 242,42 241, Industrial 31 68,231 68,231 4, Industrial 31 37,823 37,823 36, Residential 41 8,624,272 8,624,272 6,64, Residential 41 11,3,163 11,3,163 9,597, Timber/Cutover 51 Timber/Cutover , ,496 59,52 1. Total Real 9,328,716 9,328,716 7,215,4 1. Total Real 12,485,92 12,485,92 1,78,954 Agricultural 151 Agricultural 151 Commercial , , , Commercial 251 4,39 4,39 4,39 1. Industrial 351 Industrial Residential 451 Residential 451 Utility 551 3,453,161 3,453,161 3,453, Utility 551 4,329,532 4,329,532 3,92, Total Personal 3,642,855 3,642,855 3,642,855 Total Personal 4,334,151 4,334,151 3,96,877 Grand Total 12,971,571 12,971,571 1,857,859 Grand Total 16,82,53 16,82,53 14,615, Tentative Equalization Tentative Equalization Marquette Township Assessed Equalized Taxable Factor Moran Township Assessed Equalized Taxable Factor Agricultural 11 3,566,7 3,566,7 2,316,58 1. Agricultural 11 Commercial ,5 796,5 588, Commercial 21 12,95,7 12,95,7 1,76, Industrial 31 Industrial 31 8,85,7 8,85,7 7,719,67 1. Residential 41 39,28,175 39,28,175 27,914, Residential 41 68,942,2 68,942,2 52,724, Timber/Cutover ,9 479,9 262, Timber/Cutover 51 Total Real 43,871,275 43,871,275 31,82,477 Total Real 89,123,6 89,123,6 71,149,995 Agricultural 151 Agricultural 151 Commercial ,1 33,1 33,1 1. Commercial 251 1,56,9 1,56,9 1,56,9 1. Industrial 351 Industrial 351 1,629,9 1,629,9 1,629,9 1. Residential 451 Residential 451 Utility ,6 781,6 781,6 1. Utility 551 7,347,4 7,347,4 69,24,25 1. Total Personal 1,84,7 1,84,7 1,84,7 Total Personal 73,34,2 73,34,2 71,927,5 Grand Total 44,955,975 44,955,975 32,167,177 Grand Total 162,157,8 162,157,8 143,77,45 Mackinac County Equalization Department 218 Equalization Report Mackinac County Board of Commissioners April 12, 218

31 Mackinac County 218 Assessed, County Equalized and Tentative Taxable Values Tentative Equalization Tentative Equalization Newton Township Assessed Equalized Taxable Factor Portage Township Assessed Equalized Taxable Factor Agricultural 11 1,15,8 1,15,8 579,87 1. Agricultural 11 64,3 64,3 425, Commercial 21 1,43,1 1,43,1 1,288, Commercial 21 6,113,6 6,113,6 4,998, Industrial 31 3,994,7 3,994,7 2,461, Industrial 31 Residential 41 27,549,3 27,549,3 24,33, Residential 41 84,633,9 84,633,9 69,575,44 1. Timber/Cutover 51 2,112,4 2,112,4 1,32, Timber/Cutover 51 Total Real 36,21,3 36,21,3 29,953,75 Total Real 91,387,8 91,387,8 74,998, Agricultural 151 Agricultural 151 Commercial , , , Commercial ,15 18,15 18,15 1. Industrial 351 1,127,43 1,127,43 1,127,43 1. Industrial 351 Residential 451 Residential 451 Utility 551 1,931,639 1,931,639 1,931, Utility 551 1,19,6 1,19,6 1,19,6 1. Total Personal 12,19,483 12,19,483 12,19,483 Total Personal 1,127,75 1,127,75 1,127,75 Grand Total 48,4,783 48,4,783 42,144,188 Grand Total 92,515,55 92,515,55 76,126, Tentative Equalization St. Ignace Township Assessed Equalized Taxable Factor Agricultural 11 53,723 53,723 19, Commercial 21 2,274,6 2,274,6 1,743, Industrial 31 19,32 19,32 58,39 1. Residential 41 32,15,411 32,15,411 25,561,81 1. Timber/Cutover 51 Total Real 34,542,496 34,542,496 27,382,21 Agricultural 151 Commercial ,29 55,29 55,29 1. Industrial 351 Residential 451 Utility ,873,981 13,873,981 13,873, Total Personal 14,379,271 14,379,271 14,379,271 Grand Total 48,921,767 48,921,767 41,761,472 Mackinac County Equalization Department 218 Equalization Report Mackinac County Board of Commissioners April 12, 218

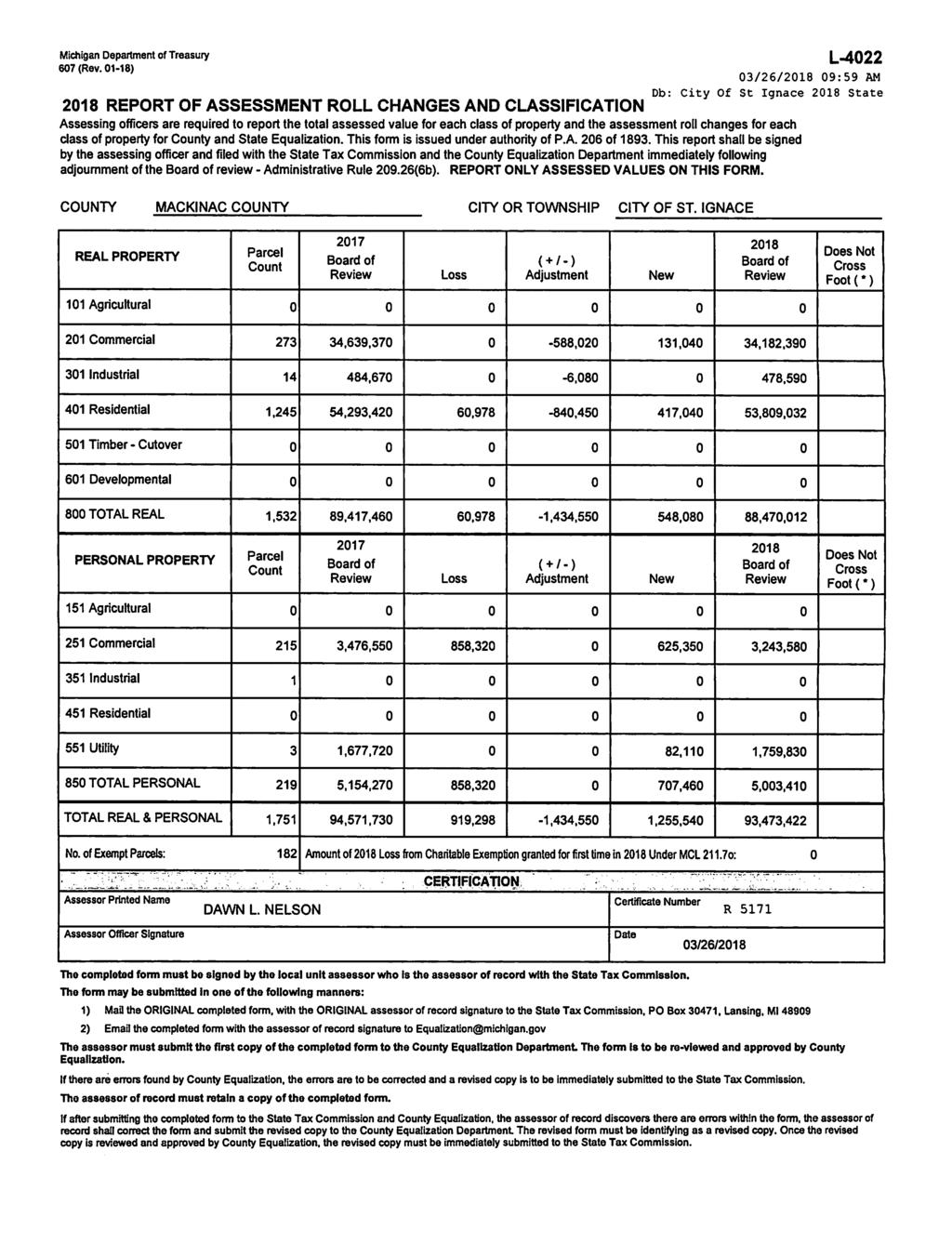

32 Mackinac County 218 Assessed, County Equalized and Tentative Taxable Values Tentative Equalization Tentative Equalization City of Mackinac Island Assessed Equalized Taxable Factor City of St. Ignace Assessed Equalized 1 Taxable Factor Agricultural 11 Agricultural 11 Commercial 21 14,134,5 14,134,5 14,756, Commercial 21 34,182,39 34,182,39 28,5, Industrial 31 Industrial ,59 478,59 467, Residential 41 16,749,593 16,749, ,32,56 1. Residential 41 53,89,32 53,89,32 46,339, Timber/Cutover 51 Timber/Cutover 51 Total Real 3,883,643 3,883, ,788,338 Total Real 88,47,12 88,47,12 75,37,518 Agricultural 151 Agricultural 151 Commercial 251 8,79,828 8,79,828 8,79, Commercial 251 3,243,58 3,243,58 3,217,48 1. Industrial 351 Industrial 351 Residential 451 Residential 451 Utility , , , Utility 551 1,759,83 1,759,83 1,738,41 1. Total Personal 9,673, 9,673, 9,673, Total Personal 5,3,41 5,3,41 4,955,89 Grand Total 31,556,643 31,556, ,461,338 Grand Total 93,473,422 93,473,422 8,263,48 1 The State Tax Commission at their 2/13/18 meeting directed Mackinac County to complete a line 7 adjustment to allow the 218 assessment roll to be equalized as assessed. Mackinac County Equalization Department 218 Equalization Report Mackinac County Board of Commissioners April 12, 218

33 Mackinac County Assessed, CEV & Tentative Taxable By Governmental Unit 35,, 3,, 25,, 2,, 15,, 1,, 5,, 218 Assessed County Equalized Tentative TV Mackinac Island 31,556,643 31,556, ,461,338 Clark Twp 256,275,66 256,275,66 196,232,512 Moran Twp 162,157,8 162,157,8 143,77,45 Garfield Twp 95,499,857 95,499,857 84,919,416 Portage Twp 92,515,55 92,515,55 76,126,599 St Ignace City 93,473,422 93,473,422 8,263,48 Newton Twp 48,4,783 48,4,783 42,144,188 St Ignace Twp 48,921,767 48,921,767 41,761,472 Marquette Twp 44,955,975 44,955,975 32,167,177 Bois Blanc Twp 42,38,3 42,38,3 33,389,548 Brevort Twp 41,742,321 41,742,321 29,552,617 Hudson Twp 16,82,53 16,82,53 14,615,831 Hendricks Twp 12,971,571 12,971,571 1,857,859 Mackinac County Equalization Department 218 Equalization Report Mackinac County Board of Commissioners April 12, 218

34 Difference Between CEV/SEV & Taxable Value 1,6,, 1,4,, 1,2,, 1,,, 8,, 6,, CEV/SEV Taxable 4,, 2,, Mackinac County Equalization Department CEV/SEV Taxable Difference ,863, ,863,841.% ,143,51 455,98, % ,11, ,698, % ,515,723 49,355, % ,529,87 511,681, % ,576, ,76, % 2 742,424,236 57,369, % ,382,946 69,248, % ,584, ,17, % ,148, ,371, % 24 1,111,58, ,672, % 25 1,167,97, ,621, % 26 1,233,53,991 81,24, % 27 1,327,136, ,671, % 28 1,344,439,5 887,734, % 29 1,286,13,331 97,38, % 21 1,266,671,72 1,21,569, % 211 1,168,476, ,859,41 3.% 212 1,151,657,564 94,23, % 213 1,176,568, ,182, % 214 1,196,934,43 951,6, % 215 1,24,493, ,42, % 216 1,23,34, ,64, % 217 1,238,92,851 1,5,239, % 218 1,266,671,72 1,21,569, % 218 Equalization Report Mackinac County Board of Commissioners April 12, 218

35 Mackinac County Change in County Equalized Value Change in Equalized Value Township/City Brevort Twp St Ignace City Hudson Twp Mackinac Island Clark Twp Marquette Twp Portage Twp Moran Twp St Ignace Twp Hendricks Twp Garfield Twp Bois Blanc Twp Newton Twp -6.% -4.% -2.%.% 2.% 4.% 6.% 8.% Percent Change Township/City % Change 217 CEV 218 CEV Newton Twp -4.1% 5,342,96 48,4,783 Bois Blanc Twp -1.91% 43,189,9 42,38,3 Garfield Twp -1.86% 97,277,686 95,499,857 Hendricks Twp.18% 12,948,319 12,971,571 St Ignace Twp.25% 48,798,725 48,921,767 Moran Twp 1.44% 159,819,1 162,157,8 Portage Twp 1.63% 91,9,725 92,515,55 Marquette Twp 1.77% 44,159,1 44,955,975 Clark Twp 3.3% 248,56, ,275,66 Mackinac Island 3.84% 298,622,724 31,556,643 Hudson Twp 4.28% 16,99,571 16,82,53 St Ignace City 4.77% 89,11,371 93,473,422 Brevort Twp 6.25% 39,134,745 41,742,321 Mackinac County Equalization Department 218 Equalization Report Mackinac County Board of Commissioners April 12, 218

36 Mackinac County 218 Real Property Assessed, County Equalized and Taxable Values Real Property - County Equalized Value 218 % of Tentative Unit Equalized Total Value Mackinac County Assessed Equalized Taxable Agricultural 14,295, % Agricultural 11 14,295,211 14,295,211 9,99,313 Commercial 216,269, % Commercial ,269,99 216,269,99 169,24,177 Industrial 18,84, % Industrial 31 18,84,26 18,84,26 16,14,874 Residential 862,892, % Residential ,892, ,892, ,12,447 Utility 3,731,96.33% Timber/Cutover 51 3,731,96 3,731,96 2,24,841 Total: 1,115,992,764 1.% Total Real 1,115,992,764 1,115,992, ,615,652 Real Property - Assessed Value 218 % of Class Assessed Total Value Agricultural 14,295, % Commerical 216,269, % Industrial 18,84, % Residential 862,892, % Real Property - Tentative Taxable Value Timber Cutover 3,731,96.33% 218 Tentative % of Total: 1,115,992,764 1.% Class Taxable Value Total Value Agricultural 9,99, % Real Property Distribution of Assessed Value Agricultural Commerical Industrial Commerical 169,24, % Industrial 16,14, % Residential 675,12, % Timber Cutover 2,24,841.26% Total: 872,615,652 1.% Real Property Distribution of County Equalized Value Real Property Distribution of Tentative Taxable Value Agricultural Commercial Industrial Residential Utility Agricultural Commerical Industrial Residential Timber Cutover Residential Timber Cutover Mackinac County Equalization Department 218 Equalization Report Mackinac County Board of Commissioners April 12, 218

37 Mackinac County Personal Property County/State Equalized Values by Class Personal Property Personal Property Personal Property Distribution of County Equalized Value Unit 218 % of 217 % of Equalized Total Value Unit Equalized Total Value Agricultural.% Agricultural.% Commercial 17,151, % Agricultural Commercial 17,151, % Industrial 8,2, % Industrial 8,2, % Residential.% Commercial Residential.% Utility 125,327, % Utility 125,327, % Total: 15,678,938 1.% Industrial Total: 15,678,938 1.% Residential Utility Personal Property Distribution of County Equalized Value Agricultural Commercial Industrial Residential Utility Personal Property Personal Property Personal Property 216 % of Distribution of State Equalized Value 215 % of Unit Equalized Total Value Unit Equalized Total Value Agricultural.% Agricultural.% Commercial 2,49, % Agricultural Commercial 18,466, % Industrial 8,625, % Industrial 13,998, % Residential.% Commercial Residential.% Utility 128,729, % Utility 124,766, % Total: 157,44,62 1.% Industrial Total: 157,231,97 1.% Residential Utility Personal Property Distribution of State Equalized Value Agricultural Commercial Industrial Residential Utility Mackinac County Equalization Department 218 Equalization Report Mackinac County Board of Commissioners April 12, 218

38 Mackinac County Analysis by Class Value change between 217 and 218 Mackinac County 217 to 218 CEV Change 2.92% Property County 218 County change from Units % Property Classification Parcel Count Equalized Equalized previous year of Total CEV Classification Real Real Agricultural ,536,236 14,295, % 1.28% 241,25 Agricultural Commercial ,568,99 216,269, % 19.38% 4,71, Commercial Industrial ,818,115 18,84,26.7% 1.68% 14,89 Industrial Residential 18, ,441,79 862,892, % 77.32% 27,451,362 Residential Timber cutover 111 3,996,57 3,731, %.33% 265,411 Timber cutover Unit Totals ,84,36,927 1,115,992, % 1.% 31,631,837 Mackinac County 217 to 218 CEV Change 2.51% T TV Change 2.29% Property County 218 County change from change from Property Classification Parcel Count Equalized Equalized previous year Tent Taxable Tent Taxable previous year Classification Personal Personal Commercial 97 16,888,34 17,151, % 16,776,841 17,125,27 2.3% Commercial Industrial 9 1,339,432 8,2, % 1,339,432 8,2, % Industrial Utility ,332, ,327, % 125,252,88 123,627, % Timber cutover Unit Totals ,559,924 15,678, % 152,369, ,953, % 11 Agricultural CEV Change 1.66% County 218 County change from Units % Parcel Count Equalized Equalized previous year of Total CEV Townships Townships Brevort 6 152,6 13, 32.5%.72% 49,6 Brevort Clark 12 65,1 617,7 2.8% 4.32% 12,6 Clark Garfield 182 8,283,13 8,162, % 57.1% 12,142 Garfield Marquette 76 3,63,9 3,566,7 1.3% 24.95% 37,2 Marquette Newton 61 1,153,3 1,15,8.22% 8.5% 2,5 Newton Portage ,9 64,3 6.38% 4.48% 43,6 Portage St. Ignace 2 54,36 53, %.38% 583 St. Ignace Unit Totals ,536,236 14,295, % 1.% 241,25 Mackinac County Equalization Department 218 Equalizaton Report Mackinac County Board of Commissioners April 12, 218

39 Mackinac County Analysis by Class Value change between 217 and Commercial CEV Change 2.22% County 218 County change from Units % Parcel Count Equalized Equalized previous year of Total CEV Township Township Bois Blanc ,9 662, %.31% 17,95 Bois Blanc Brevort , 432,3 4.57%.2% 2,7 Brevort Clark ,564,9 13,687,2 6.3% 6.33% 877,7 Clark Garfield 67 3,499,831 3,69, % 1.67% 19,776 Garfield Hendricks ,86 636, %.29% 26,593 Hendricks Hudson 7 235, , %.11% 6,556 Hudson Marquette ,5 796, %.37% 154, Marquette Moran ,826,2 12,95,7 2.28% 5.59% 269,5 Moran Newton 27 1,492,5 1,43,1 5.99%.65% 89,4 Newton Portage 75 6,113,7 6,113,6.% 2.83% 1 Portage St. Ignace 42 2,487,329 2,274,6 8.57% 1.5% 213,269 St. Ignace city city Mackinac Island ,968,55 14,134,5 2.31% 64.8% 3,165,5 Mackinac Island St Ignace ,976,91 34,182,39 6.9% 15.81% 2,25,48 St Ignace Unit Totals ,568,99 216,269, % 1.% 4,71, 31 Industrial CEV Change.7% County 218 County change from Units % Parcel Count Equalized Equalized previous year of Total CEV Township Township Brevort 4 161,3 156,8 2.79%.83% 4,5 Brevort Clark 55 4,887,7 5,1,2 2.51% 26.64% 122,5 Clark Garfield 7 478, , % 2.82% 5,711 Garfield Hendricks 3 68,231 68,231.%.36% Hendricks Hudson 6 359,839 37, % 1.97% 1,984 Hudson Moran 34 8,27,3 8,85,7 1.48% 43.% 121,6 Moran Newton 32 4,97,9 3,994,7 2.52% 21.24% 13,2 Newton St. Ignace 3 69,416 19, %.58% 39,886 St. Ignace city city St Ignace ,46 478, % 2.55% 8,87 St Ignace Unit Totals ,818,115 18,84,26.7% 1.% 14,89 Mackinac County Equalization Department 218 Equalizaton Report Mackinac County Board of Commissioners April 12, 218

40 Mackinac County Analysis by Class Value change between 217 and Residential CEV Change 3.29% County 218 County change from Units % Parcel Count Equalized Equalized previous year of Total CEV Township Township Bois Blanc ,281,5 41,449, % 4.8% 832,15 Bois Blanc Brevort ,685,1 39,341,4 7.24% 4.56% 2,656,3 Brevort Clark ,743,9 227,493,2 4.% 26.36% 8,749,12 Clark Garfield 286 7,663,358 68,163, % 7.9% 2,499,733 Garfield Hendricks 337 8,776,64 8,624, % 1.% 152,332 Hendricks Hudson 44 1,451,694 11,3, % 1.28% 551,469 Hudson Marquette ,347,6 39,28, % 4.52% 68,575 Marquette Moran ,51,2 68,942,2 6.87% 7.99% 4,432, Moran Newton 19 27,295,961 27,549,3.93% 3.19% 253,339 Newton Portage ,6,825 84,633,9 1.89% 9.81% 1,573,75 Portage St. Ignace ,171,956 32,15, % 3.72% 933,455 St. Ignace city city Mackinac Island ,59,65 16,749, % 18.63% 8,689,943 Mackinac Island St Ignace ,392,731 53,89,32 4.7% 6.24% 2,416,31 St Ignace Unit Totals ,441,79 862,892, % 1.% 27,451, Timber Cutover % County 218 County change from Units % Parcel Count Equalized Equalized previous year of Total CEV Township Township Clark 6 274,1 269,3 1.75% 7.22% 4,8 Clark Hudson 24 93,7 869, % 23.3% 33,511 Hudson Marquette ,4 479,9 2.46% 12.86% 11,5 Marquette Newton 68 2,351, 2,112,4 1.15% 56.62% 238,6 Newton Unit Totals 111 3,996,57 3,731, % 1.% 265,411 Mackinac County Equalization Department 218 Equalizaton Report Mackinac County Board of Commissioners April 12, 218

41

42 L-423 ANALYSIS FOR EQUALIZED VALUATION COUNTY: 49 - Mackinac 1 - Bois Blanc Tax Year: REAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 11 Agricultural. 12 LOSS TOTAL Agricultural. 19 Computed 5% TCV Agricultural Recommended CEV Agricultural 2 REAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 21 Commercial , ,295,24 22 LOSS , ,295, ,85 17, ,295,24 34, TOTAL Commercial , ,329, Computed 5% TCV Commercial 664,668 Recommended CEV Commercial 662,85 3 REAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 31 Industrial. 32 LOSS TOTAL Industrial. 39 Computed 5% TCV Industrial Recommended CEV Industrial 4 REAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 41 Residential 1,653 42,281, ,758, LOSS 399, , ,881,65-918, ,966, ,963,2 486, ,966, , TOTAL Residential 1,682 41,449, ,951, Computed 5% TCV Residential 41,975,763 Recommended CEV Residential 41,449,35 5 REAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 51 Timber-Cutover. 52 LOSS TOTAL Timber-Cutover. 59 Computed 5% TCV Timber-Cutover Recommended CEV Timber-Cutover 6 REAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 61 Developmental. 62 LOSS TOTAL Developmental. 69 Computed 5% TCV Developmental Recommended CEV Developmental 8 TOTAL REAL 1,711 42,112, ,28,86 89 Computed 5% TCV REAL 42,64,43 Recommended CEV REAL 42,112,2

43 L-423 ANALYSIS FOR EQUALIZED VALUATION COUNTY: 49 - Mackinac 1 - Bois Blanc Tax Year: PERSONAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 151 Ag. Personal. 152 LOSS TOTAL Ag. Personal. 25 PERSONAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 251 Com. Personal LOSS TOTAL Com. Personal PERSONAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 351 Ind. Personal. 352 LOSS TOTAL Ind. Personal. 45 PERSONAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 451 Res. Personal. 452 LOSS TOTAL Res. Personal. 55 PERSONAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 551 Util. Personal 1 263, ,4 552 LOSS , , ,2 4, ,4 9, TOTAL Util. Personal 1 267, ,6 85 TOTAL PERSONAL 2 268, ,2 859 Computed 5% TCV PERSONAL 268,1 Recommended CEV PERSONAL 268,1 9 Total Real and Personal 1,731 42,38,3 85,817,6

44

45 L-423 ANALYSIS FOR EQUALIZED VALUATION COUNTY: 49 - Mackinac 2 - Brevort Tax Year: REAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 11 Agricultural 6 152, , LOSS 5, , , , , , TOTAL Agricultural 2 13, , Computed 5% TCV Agricultural 13,787 Recommended CEV Agricultural 13, 2 REAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 21 Commercial , , LOSS 22, , , 1, , , , TOTAL Commercial , , Computed 5% TCV Commercial 432,818 Recommended CEV Commercial 432,3 3 REAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 31 Industrial 4 161, ,45 32 LOSS ,246-4, , , , TOTAL Industrial 4 156, , Computed 5% TCV Industrial 158,172 Recommended CEV Industrial 156,8 4 REAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 41 Residential ,685, ,182, LOSS 82, , ,63,5 2,365, ,5, ,968,4 373, ,5,72 756, TOTAL Residential ,341, ,761, Computed 5% TCV Residential 39,88,679 Recommended CEV Residential 39,341,4 5 REAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 51 Timber-Cutover. 52 LOSS TOTAL Timber-Cutover. 59 Computed 5% TCV Timber-Cutover Recommended CEV Timber-Cutover 6 REAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 61 Developmental. 62 LOSS TOTAL Developmental. 69 Computed 5% TCV Developmental Recommended CEV Developmental 8 TOTAL REAL 914 4,33, ,15,91 89 Computed 5% TCV REAL 4,575,455 Recommended CEV REAL 4,33,5

46 L-423 ANALYSIS FOR EQUALIZED VALUATION COUNTY: 49 - Mackinac 2 - Brevort Tax Year: PERSONAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 151 Ag. Personal. 152 LOSS TOTAL Ag. Personal. 25 PERSONAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 251 Com. Personal 12 3, , LOSS , , ,135 6, ,27 13, TOTAL Com. Personal 14 1, 5. 2, 35 PERSONAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 351 Ind. Personal. 352 LOSS TOTAL Ind. Personal. 45 PERSONAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 451 Res. Personal. 452 LOSS TOTAL Res. Personal. 55 PERSONAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 551 Util. Personal 5 1,679, ,359, LOSS 14, , ,665, ,33, ,665,53 33, ,33,16 67, TOTAL Util. Personal 5 1,698, ,397, TOTAL PERSONAL 19 1,78, ,417, Computed 5% TCV PERSONAL 1,78,821 Recommended CEV PERSONAL 1,78,821 9 Total Real and Personal ,742,321 84,568,552

47

48 L-423 ANALYSIS FOR EQUALIZED VALUATION COUNTY: 49 - Mackinac 3 - Clark Tax Year: REAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 11 Agricultural 12 65, ,24, LOSS ,1 6, ,24, ,9 5, ,24,976 11, TOTAL Agricultural , ,252, Computed 5% TCV Agricultural 626,369 Recommended CEV Agricultural 617,7 2 REAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 21 Commercial ,564, ,63, LOSS 1,68, ,415, ,884, , ,187, ,8,1 67, ,187,467 1,215, TOTAL Commercial ,687, ,42, Computed 5% TCV Commercial 13,71,441 Recommended CEV Commercial 13,687,2 3 REAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 31 Industrial 55 4,887, ,92, LOSS 11, , ,876,46 5, ,897, ,881,6 128, ,897,422 26, TOTAL Industrial 55 5,1, ,158, Computed 5% TCV Industrial 5,79,84 Recommended CEV Industrial 5,1,2 4 REAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 41 Residential 3, ,743, ,222,87 42 LOSS 1,32, ,171, ,711,877 7,724, ,51, ,436,583 2,56, ,51,498 4,178, TOTAL Residential 3, ,493, ,229,55 49 Computed 5% TCV Residential 231,114,775 Recommended CEV Residential 227,493,2 5 REAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 51 Timber-Cutover 6 274, , LOSS ,1-4, , , , TOTAL Timber-Cutover 6 269, , Computed 5% TCV Timber-Cutover 271,979 Recommended CEV Timber-Cutover 269,3 6 REAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 61 Developmental. 62 LOSS TOTAL Developmental. 69 Computed 5% TCV Developmental Recommended CEV Developmental 8 TOTAL REAL 3, ,77, ,587, Computed 5% TCV REAL 25,793,648 Recommended CEV REAL 247,77,42

49 L-423 ANALYSIS FOR EQUALIZED VALUATION COUNTY: 49 - Mackinac 3 - Clark Tax Year: PERSONAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 151 Ag. Personal. 152 LOSS TOTAL Ag. Personal. 25 PERSONAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 251 Com. Personal 129 2,28, ,561, LOSS 131, , ,149, ,298, ,149,32 524, ,298,64 1,48, TOTAL Com. Personal 149 2,673, ,347, PERSONAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 351 Ind. Personal 2 3,932, ,864, LOSS 553, ,17, ,378, ,757, ,378, ,757, TOTAL Ind. Personal 2 3,378, ,757,56 45 PERSONAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 451 Res. Personal. 452 LOSS TOTAL Res. Personal. 55 PERSONAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 551 Util. Personal 2 3,218, ,436, LOSS 72, , ,145, ,291, ,145, ,291, TOTAL Util. Personal 2 3,145, ,291, TOTAL PERSONAL 153 9,198, ,396, Computed 5% TCV PERSONAL 9,198,24 Recommended CEV PERSONAL 9,198,24 9 Total Real and Personal 3, ,275,66 519,983,775

50

51 L-423 ANALYSIS FOR EQUALIZED VALUATION COUNTY: 49 - Mackinac 4 - Garfield Tax Year: REAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 11 Agricultural 182 8,283, ,543,1 12 LOSS 1, , ,272,93-175, ,522, ,97,572 65, ,522, , TOTAL Agricultural 184 8,162, ,656,24 19 Computed 5% TCV Agricultural 8,328,12 Recommended CEV Agricultural 8,162,988 2 REAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 21 Commercial 68 3,499, ,238, LOSS 18, , ,481,153 18, ,199, ,589,63 2, ,199,93 4, TOTAL Commercial 67 3,69, ,24,23 29 Computed 5% TCV Commercial 3,62,12 Recommended CEV Commercial 3,69,67 3 REAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 31 Industrial 7 478, ,61,31 32 LOSS ,969 5, ,61, , ,61, TOTAL Industrial 7 529, ,61,31 39 Computed 5% TCV Industrial 53,655 Recommended CEV Industrial 529,68 4 REAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 41 Residential 2,87 7,663, ,96,48 42 LOSS 344, , ,318,938-2,783, ,288, ,535,1 628, ,288,47 1,277, TOTAL Residential 2,86 68,163, ,565, Computed 5% TCV Residential 69,282,999 Recommended CEV Residential 68,163,625 5 REAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 51 Timber-Cutover. 52 LOSS TOTAL Timber-Cutover. 59 Computed 5% TCV Timber-Cutover Recommended CEV Timber-Cutover 6 REAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 61 Developmental. 62 LOSS TOTAL Developmental. 69 Computed 5% TCV Developmental Recommended CEV Developmental 8 TOTAL REAL 3,64 8,465, ,523, Computed 5% TCV REAL 81,761,768 Recommended CEV REAL 8,465,9

52 L-423 ANALYSIS FOR EQUALIZED VALUATION COUNTY: 49 - Mackinac 4 - Garfield Tax Year: PERSONAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 151 Ag. Personal. 152 LOSS TOTAL Ag. Personal. 25 PERSONAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 251 Com. Personal , , LOSS 125, , , , ,311 7, ,622 14, TOTAL Com. Personal , , PERSONAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 351 Ind. Personal 1 1,893,1 5. 3,786,2 352 LOSS ,893,1 5. 3,786, ,893,1 17, ,786,2 341, TOTAL Ind. Personal 1 2,63, ,127, PERSONAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 451 Res. Personal. 452 LOSS TOTAL Res. Personal. 55 PERSONAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 551 Util. Personal 6 12,116, ,232, LOSS 474, , ,642, ,284, ,642,159 1,13, ,284,318 2,27, TOTAL Util. Personal 6 12,745, ,491, TOTAL PERSONAL 51 15,33, ,67, Computed 5% TCV PERSONAL 15,33,957 Recommended CEV PERSONAL 15,33,957 9 Total Real and Personal 3,115 95,499, ,591,449

53

54 L-423 ANALYSIS FOR EQUALIZED VALUATION COUNTY: 49 - Mackinac 5 - Hendricks Tax Year: REAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 11 Agricultural. 12 LOSS TOTAL Agricultural. 19 Computed 5% TCV Agricultural Recommended CEV Agricultural 2 REAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 21 Commercial , ,271, LOSS ,86-28, ,271, ,689 1, ,271,692 3, TOTAL Commercial , ,274, Computed 5% TCV Commercial 637,373 Recommended CEV Commercial 636,213 3 REAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 31 Industrial 3 68, , LOSS , , , , TOTAL Industrial 3 68, , Computed 5% TCV Industrial 69,313 Recommended CEV Industrial 68,231 4 REAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 41 Residential 338 8,776, ,286, LOSS 8, , ,696, , ,128, ,55,26 119, ,128,78 24, TOTAL Residential 337 8,624, ,368, Computed 5% TCV Residential 8,684,441 Recommended CEV Residential 8,624,272 5 REAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 51 Timber-Cutover. 52 LOSS TOTAL Timber-Cutover. 59 Computed 5% TCV Timber-Cutover Recommended CEV Timber-Cutover 6 REAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 61 Developmental. 62 LOSS TOTAL Developmental. 69 Computed 5% TCV Developmental Recommended CEV Developmental 8 TOTAL REAL 355 9,328, ,782, Computed 5% TCV REAL 9,391,126 Recommended CEV REAL 9,328,716

55 L-423 ANALYSIS FOR EQUALIZED VALUATION COUNTY: 49 - Mackinac 5 - Hendricks Tax Year: PERSONAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 151 Ag. Personal. 152 LOSS TOTAL Ag. Personal. 25 PERSONAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 251 Com. Personal , , LOSS 16, , , , ,854 76, ,78 153, TOTAL Com. Personal , , PERSONAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 351 Ind. Personal. 352 LOSS TOTAL Ind. Personal. 45 PERSONAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 451 Res. Personal. 452 LOSS TOTAL Res. Personal. 55 PERSONAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 551 Util. Personal 4 3,221, ,442, LOSS 4, , ,216, ,433, ,216, , ,433, , TOTAL Util. Personal 4 3,453, ,96, TOTAL PERSONAL 22 3,642, ,285, Computed 5% TCV PERSONAL 3,642,855 Recommended CEV PERSONAL 3,642,855 9 Total Real and Personal ,971,571 26,67,961

56

57 L-423 ANALYSIS FOR EQUALIZED VALUATION COUNTY: 49 - Mackinac 6 - Hudson Tax Year: REAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 11 Agricultural. 12 LOSS TOTAL Agricultural. 19 Computed 5% TCV Agricultural Recommended CEV Agricultural 2 REAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 21 Commercial 7 235, , LOSS ,864-8, , ,127 15, ,217 3, TOTAL Commercial 7 242, , Computed 5% TCV Commercial 243,469 Recommended CEV Commercial 242,42 3 REAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 31 Industrial 5 359, , LOSS ,839 1, , ,63 9, ,568 19, TOTAL Industrial 6 37, ,1 39 Computed 5% TCV Industrial 371,5 Recommended CEV Industrial 37,823 4 REAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 41 Residential 44 1,451, ,54,64 42 LOSS 147, , ,33, , ,742, ,86,95 142, ,742, , TOTAL Residential 44 11,3, ,27, Computed 5% TCV Residential 11,13,671 Recommended CEV Residential 11,3,163 5 REAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 51 Timber-Cutover 25 93, ,841, LOSS 49, , ,33 16, ,74, , ,74, TOTAL Timber-Cutover , ,74,14 59 Computed 5% TCV Timber-Cutover 87,7 Recommended CEV Timber-Cutover 869,496 6 REAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 61 Developmental. 62 LOSS TOTAL Developmental. 69 Computed 5% TCV Developmental Recommended CEV Developmental 8 TOTAL REAL ,485, ,996, Computed 5% TCV REAL 12,498,197 Recommended CEV REAL 12,485,92

58 L-423 ANALYSIS FOR EQUALIZED VALUATION COUNTY: 49 - Mackinac 6 - Hudson Tax Year: PERSONAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 151 Ag. Personal. 152 LOSS TOTAL Ag. Personal. 25 PERSONAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 251 Com. Personal 11 2, , LOSS , , ,274 1, ,548 3, TOTAL Com. Personal 11 4, ,78 35 PERSONAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 351 Ind. Personal , LOSS , , TOTAL Ind. Personal ,16 45 PERSONAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 451 Res. Personal. 452 LOSS TOTAL Res. Personal. 55 PERSONAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 551 Util. Personal 5 4,146, ,292, LOSS 3, , ,115, ,231, ,115, , ,231,66 427, TOTAL Util. Personal 5 4,329, ,659,64 85 TOTAL PERSONAL 17 4,334, ,668, Computed 5% TCV PERSONAL 4,334,151 Recommended CEV PERSONAL 4,334,151 9 Total Real and Personal ,82,53 33,664,696

59

60 L-423 ANALYSIS FOR EQUALIZED VALUATION COUNTY: 49 - Mackinac 7 - Marquette Tax Year: REAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 11 Agricultural 76 3,63, ,251,38 12 LOSS 243, , ,36,6 12, ,761, ,373,5 193, ,761, , TOTAL Agricultural 73 3,566, ,149,23 19 Computed 5% TCV Agricultural 3,574,512 Recommended CEV Agricultural 3,566,7 2 REAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 21 Commercial , ,583, LOSS 29, , ,8 139, ,51, , 44, ,51,476 89, TOTAL Commercial , ,599, Computed 5% TCV Commercial 799,926 Recommended CEV Commercial 796,5 3 REAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 31 Industrial. 32 LOSS TOTAL Industrial. 39 Computed 5% TCV Industrial Recommended CEV Industrial 4 REAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 41 Residential 1,181 38,347, ,32, LOSS 618, ,198, ,729,3-1,31, ,14, ,419,275 2,68, ,14,631 5,236, TOTAL Residential 1,184 39,28, ,341, Computed 5% TCV Residential 39,17,642 Recommended CEV Residential 39,28,175 5 REAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 51 Timber-Cutover , ,51 52 LOSS 8, , ,9-2, , ,9 22, ,65 44, TOTAL Timber-Cutover , , Computed 5% TCV Timber-Cutover 481,612 Recommended CEV Timber-Cutover 479,9 6 REAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 61 Developmental. 62 LOSS TOTAL Developmental. 69 Computed 5% TCV Developmental Recommended CEV Developmental 8 TOTAL REAL 1,286 43,871, ,53, Computed 5% TCV REAL 44,26,691 Recommended CEV REAL 43,871,275

61 L-423 ANALYSIS FOR EQUALIZED VALUATION COUNTY: 49 - Mackinac 7 - Marquette Tax Year: PERSONAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 151 Ag. Personal. 152 LOSS TOTAL Ag. Personal. 25 PERSONAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 251 Com. Personal 1 314, ,6 252 LOSS 16, , , , ,7 4, ,4 8, TOTAL Com. Personal 16 33, ,2 35 PERSONAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 351 Ind. Personal. 352 LOSS TOTAL Ind. Personal. 45 PERSONAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 451 Res. Personal. 452 LOSS TOTAL Res. Personal. 55 PERSONAL PROPERTY # Pcls. Assessed Value % Ratio True Cash Value Remarks 551 Util. Personal 5 781,9 5. 1,563,8 552 LOSS 1,4 5. 2, ,5 5. 1,561, ,5 1, ,561, 2, TOTAL Util. Personal 4 781,6 5. 1,563,2 85 TOTAL PERSONAL 2 1,84,7 5. 2,169,4 859 Computed 5% TCV PERSONAL 1,84,7 Recommended CEV PERSONAL 1,84,7 9 Total Real and Personal 1,36 44,955,975 9,222,781