HOUSING OBSERVER Digest

|

|

|

- Brian Jennings

- 6 years ago

- Views:

Transcription

1 HOUSING OBSERVER 2015 Digest

2 CMHC provides funding for housing content on the Census of Canada and on Statistics Canada surveys. Statistics Canada information is used with the permission of Statistics Canada. Users are forbidden to copy and redisseminate data for commercial purposes, either in an original or modified form, without the express permission of and, where applicable, Statistics Canada. More information on Statistics Canada data can be obtained from its Regional Offices, its World Wide Web site at and its toll-free access number The information, analysis and opinions contained in this publication are based on data compiled from various sources. CMHC makes best efforts to ensure that the contents of this publication are reliable, but cannot guarantee that the information is accurate or complete. You should not rely solely on this publication for the purpose of making financial decisions. CMHC strongly advises that you do additional research and obtain financial advice specific to your individual situation in order to form your own judgments. You may not hold CMHC liable for the consequences of any decision or action that you take in reliance upon this publication All rights reserved. No portion of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means, mechanical, electronic, photocopying, recording or otherwise without the prior written permission of. Without limiting the generality of the foregoing, no portion of this book may be translated from English into any other language without the prior written permission of Canada Mortgage and Housing Corporation. Produced by CMHC 2

3 Table of Contents 1 Condominiums Detailed Examination of Municipal Accessory Apartment Regulations D Printing and the Construction Industry Flexible Housing First Annual Estimate of Urban Households in Core Housing Need Based on Statistics Canada s New Canadian Income Survey Industrialized Housing HPPA now called the Housing Market Assessment (HMA) Report Housing Data Find What You Need Mortgage Arrears Record Covered Bond Issuance of $27.6 Billion in Other Articles: CMHC s Survey of Condominium Owners in Toronto and Vancouver The Housing Market Information Portal 2015 Mortgage Consumer Survey Interactive Chart: Average annual house prices Newcomers Homeownership Rates of Immigrants Rise Over Time House Price Analysis and Assessment April Update Save on property management costs recruit your tenants as volunteers An alternative water ready home what s the plan? Housing Markets Outlook Canada edition 2015 Rental Market Survey Housing Market Indicator Tables updated to include 2014 data Statistics Canada s Evolution of housing in Canada, 1957 to 2014 CMHC s 2015 First-Time Homebuyers Survey 3

4 Condominiums 4

5 1 What is a condominium? A condominium refers to a form of legal ownership. Buyers purchase private dwellings in condominium buildings called units, and each unit is registered in the buyer s name. The buyers of individual units share ownership of the common elements and assets of the building and community. Property owned under condominium tenure can be of any structure type. Condominiums can be: low-rise or high-rise residential buildings; townhouses or rowhouses; duplexes or triplexes; single-detached houses; or vacant land upon which owners may build. There are mixed-use condominiums that are partly residential and partly commercial buildings. Owning a condominium differs from owning a conventional home in a number of ways. Condominium owners have specific rights and responsibilities and are subject to rules that vary from project to project. To inform consumers and help them decide whether condominium ownership is right for them, we publish a range of information, including the Condominium Buyer s Guide. It includes information on: How condominium ownership differs from other forms of homeownership; How condominium corporations are run and rules that govern day-to-day condominium living; The pros and cons of condominium ownership; What to look for whether you re buying a new or a resale condominium as well as the costs you need to factor into your budget; Checklists, tips and FAQs; A glossary; and Provincial/Territorial fact sheets which provide information specific to each province and territory. 5

6 2 Condominiums by structure type In 2011, 90% of condominiums in Canada were low-rise or high-rise apartments, or row houses. Single-detached houses accounted for 4% of condominiums and other dwelling types for the remaining 6%. FIGURE 1 Condominiums come in various structure types Condominiums by structure type (%), Canada, Single-detached house High-rise apartment Low-rise apartment Row house Other dwelling Includes both owner-occupied and rented condominiums. Low-rise apartments are in buildings with fewer than five storeys. High-rise apartments are in buildings with five or more storeys. Other dwellings comprise duplexes, single-attached houses (a single dwelling attached to another building), semi-detached houses, and movable dwellings. Source: CMHC, adapted from Statistics Canada (National Household Survey) The distribution of structure types varied considerably across the country. In Quebec, low-rise apartments accounted for more than 60% of condominiums in every Census Metropolitan Area (CMA). In contrast, high-rise apartments made up more than two-thirds of condominiums in Toronto, the only CMA in which high-rises accounted for the majority of condominiums. Half of all high-rise condominiums in Canada were in Toronto. Row houses accounted for more than half the condominium stock in a number of Ontario CMAs. Single-detached condominiums were found in every CMA. 6

7 FIGURE 2 Distribution of structure types varies across the country Condominiums by structure type, CMAs, 2011 Victoria Vancouver Abbotsford-Mission Kelowna Edmonton Calgary Saskatoon Regina Winnipeg Thunder Bay Greater Sudbury/Grand Sudbury Barrie Windsor London Guelph Brantford Kitchener-Cambridge-Waterloo St. Catharines-Niagara Hamilton Toronto Oshawa Peterborough Kingston Ottawa Gatineau Montréal Trois-Rivières Sherbrooke Québec Saguenay Saint John Moncton Halifax St. John s Distribution of condominiums by structure type (%) Low-rise apartments High-rise apartments Row houses Single-detached houses Other dwellings Includes both owner-occupied and rented condominiums. Quebec and Ontario portions of Ottawa-Gatineau are shown separately. Low-rise apartments are in buildings with fewer than five storeys. High-rise apartments are in buildings with five or more storeys. Other dwellings comprise duplexes, single-attached houses (a single dwelling attached to another building), semi-detached houses, and movable dwellings. Source: CMHC, adapted from Statistics Canada (National Household Survey) 3 Condominium structure type by age In 2011, 68% of senior (aged 65 or older) households who owned and occupied condominiums lived in apartments, perhaps the easiest type of housing for occupants to maintain. Living space is usually confined to a single floor, and owners are typically not physically responsible for upkeep of any grounds. For people who have problems with eyesight, frailty, or balance, buildings with elevators have the added attraction of reducing the risk of falls on stairs. 7

8 Of all condominium owner-occupants, households with maintainers aged 75 or older are the age segment most likely to live in high-rise apartments, units in buildings of five floors or more that would typically have elevators. In 2011, high-rise units made up 40% of the condominiums in Canada owned and occupied by those 75 or older. Together, high-rise and low-rise apartments accounted for nearly three-quarters (72%) of the condominiums owned and occupied by this group. Per cent FIGURE 3 Senior households are the age group most likely to live in high-rise apartments Structure type choices of condominium owners by age group, Canada, Age of primary household maintainer High-rise apartments Low-rise apartments Row houses Single-detached houses Other dwellings Low-rise apartments are in buildings with fewer than five storeys. High-rise apartments are in buildings with five or more storeys. Other dwellings comprise duplexes, single-attached houses (a single dwelling attached to another building), semi-detached houses, and movable dwellings. Source: CMHC, adapted from Statistics Canada (National Household Survey) 4 Increasing number of condominiums From 1981 to 2011, the number of owner-occupied condominiums in Canada increased nearly seven-fold, and the total number of condominiums, both owneroccupied and rented, reached 1.6 million units. Growth in total stock The condominium stock comprises owner-occupied units and rented units. Many condominiums are purchased by investors who rented them out. In 2011, there were 461,000 such rentals in Canada, 29% of all occupied condominiums. The total number of occupied condominiums in Canada owned plus rented stood at 1,615,000. All told, nearly one out of eight occupied Canadian homes (12%) was a condominium. 8

9 Stock by geographical area Condominiums are found principally in large urban areas, where land costs tend to be high and multiple-unit buildings relatively common. CMAs are home to 68% of all households in Canada, but accounted for 90% of owner-occupied condominiums in Condominiums were underrepresented elsewhere: 7% in medium-sized centres (CAs) and 3% in small towns and rural areas, whereas these were home respectively to 14% and 18% of households in Canada. From 1996 to 2011, the number of owner-occupied condominiums grew by over 600,000 units nationally 28% of the total growth in owner-occupied dwellings. In many CMAs, including Vancouver (58%), Montréal (40%) and Saskatoon (40%), growth in the condominium stock represented upwards of 30% of the total increase in owner-occupied dwellings. FIGURE 4 Increase in condominium ownership highest in Vancouver, Montreal and Saskatoon Condominium share of growth in homeownership, Canada and CMAs, Canada All CMAs Vancouver Montréal Saskatoon Victoria Hamilton Regina Toronto Abbotsford-Mission Calgary Edmonton Québec Winnipeg Kelowna London Guelph St. Catharines-Niagara Ottawa Kitchener-Cambridge-Waterloo Windsor Gatineau Thunder Bay Halifax Brantford Trois-Rivières Saguenay Sherbrooke Kingston Oshawa St. John s Moncton Peterborough Barrie Saint John Greater Sudbury/Grand Sudbury Change in owner-occupied condominiums as a % of change in owner households Data from the 2011 National Household Survey may not be comparable to those from earlier censuses. Quebec and Ontario portions of Ottawa-Gatineau are shown separately. Source: CMHC, adapted from Statistics Canada (Census of Canada, National Household Survey) 9

10 Stock by usage Owner-occupied Condominiums are an increasingly popular housing choice in Canada, and have accounted for a large share of the growth of homeownership over the last three decades. From 1981 to 2011, the number of owner-occupied condominiums in Canada increased from about 171,000 to 1,154,000, more than nine times faster than other owner-occupied homes. Condominiums nearly quadrupled their share of the homeownership market from one in 30 (3%) owner-occupied dwellings in 1981 to one in eight (13%) in Rented In 2011, 11% of all rented homes in Canada were condominiums. If the strong expansion of the owneroccupied condominium stock in previous decades is any indication, the number of condominium rentals likely increased substantially as well. In many communities, condominiums are an important source of rental supply, albeit at the upper end of the market. In 2011, rented condominiums accounted for nearly a quarter of all rented homes in Calgary (25%) and Vancouver (24%). Condominium shares of the rental market were also higher than average in most CMAs in Western Canada, and in Toronto. Condominium rentals are relatively expensive, and condominium renters tend to be comparatively well-off. The median monthly shelter cost (rent plus any utilities paid separately) for condominium rentals in 2011 was $1,022, compared to $765 for other renters. Not surprisingly, households renting condominiums had considerably higher incomes than other renters a median of $42,795 versus $34,888. Thousands of units 1,800 1,600 1,400 1,200 1, FIGURE 5 Condominiums more likely to be owned than rented Occupied condominiums by tenure, Canada, ,615 All occupied condominiums 1 1 Includes 700 units of band housing. 1,154 Owner-occupied condominiums 461 Rented condominiums Source: CMHC, adapted from Statistics Canada (National Household Survey) 10

11 5 Owner-occupied by age Canadians of all ages are more likely today than in the past to live in condominiums. Condominium ownership rates rose in every age group between 1996 and 2001, between 2001 and 2006, and again between 2006 and The increased popularity of condominiums with all age groups accounted for more than three-quarters of condominium growth, the growth and aging of the population for less than one-quarter. Condominium owners as a % of all households FIGURE 6 Popularity of condominiums increased in all age groups Condominium ownership rates by age of primary household maintainer, 1 Canada, 1996, 2001, 2006, Age of primary household maintainer 1 A household maintainer is the person or one of the people in the household responsible for major household payments such as the rent or mortgage. Where more than one person in a household claims responsibility for such payments, the primary maintainer is the first person listed on the census form as a maintainer. Data from the 2011 National Household Survey may not be comparable to those from earlier censuses. Source: CMHC, adapted from Statistics Canada (Census of Canada, National Household Survey) Condominiums can offer features ease of maintenance, security, on-site amenities, and the potential for living close to public transit or within walking distance of work and centrally located attractions and services that appeal to a range of buyers, especially the young and the old. Seniors and young adults account for a disproportionate share of condominium owners. In 2011, 19% of condominium owners in Canada were under the age of 35, and 29% were seniors 65 or older, compared to 11% and 23%, respectively, of other homeowners. People aged 55 or older are much more likely than younger individuals to cite the desire for a smaller dwelling as a reason for moving. They are also more interested in living close to facilities and services. 11

12 6 Owner-occupied by household type The overrepresentation of young adults and seniors in the ranks of condominium owners is echoed in relatively small household sizes an average in 2011 of 1.9 persons for households in condominiums, compared to 2.8 for other owner-occupied dwellings. About 42% of households in owner-occupied condominiums were people who lived alone, compared to only 17% of households in other owner-occupied homes. Of the couples without children who owned and lived in condominiums, 62% were households with maintainers aged 55 or older. Nearly two-thirds (65%) of condominium owners who lived alone were women, who chose them for a variety of reasons such as low maintenance demands, safety and security features, and locations within walking distance of amenities. FIGURE 7 One-person households and couples without children own 71% of condominiums Distributions of condominium owners and other homeowners by household type (%), Canada, Inner ring: Condominium owners Outer ring: Other homeowners Couples without children Couples with children Lone-parent households One-person households Other households Other households comprise multi-family households and non-family households of two or more persons. Family households include at least one census family (a couple with or without children or a lone parent) and may include additional members who are not part of the census family. Source: CMHC, adapted from Statistics Canada (National Household Survey) From 1996 to 2011, one-person households and couples without children people less likely than families with children to need or want the large floor areas and backyards often associated with traditional suburban homes accounted for almost three-quarters (73%) of the growth in owner-occupied condominiums. During these years, as well as in previous decades, people living alone and couples without children were among the fastest-growing household types in Canada, their growth boosted by the aging of Canada s population. 12

13 7 Prices Given the strong growth in condominiums over the past quarter century and their popularity with young buyers, it would be surprising if affordability was not part of their appeal. For first-time buyers with limited savings, affordability is apt to be a deciding factor in housing choices. In 2011, condominium owners in Canada estimated that their homes would sell for a median price of $260,000, compared to $289,000 for other owner-occupied dwellings. In every CMA, the estimated selling price of condominiums was less than that of other owner-occupied units, with the difference in median prices exceeding $300,000 in Vancouver, $200,000 in Victoria and Abbotsford-Mission, and $100,000 in Ottawa (excluding Gatineau), Oshawa, Toronto, Barrie, Calgary, Edmonton, and Kelowna. FIGURE 8 Across Canada, condominiums are more affordable than non-condominiums Median estimated dwelling values 1 for condominiums and other owner-occupied dwellings, selected CMAs, 2011 Victoria Vancouver Abbotsford-Mission Kelowna Edmonton Calgary Saskatoon Regina Winnipeg Barrie Hamilton Toronto Oshawa Ottawa Gatineau Montréal Québec Halifax Thousands of dollars Non-condominium Condominium 1 Values estimated by homeowners if their dwellings were to be sold. Excludes farm households. Quebec and Ontario portions of Ottawa-Gatineau are shown separately. Source: Statistics Canada (National Household Survey) 13

14 8 Shelter costs Consistent with the comparatively low prices of condominiums, condominium buyers generally paid lower monthly shelter costs in 2011 than other home buyers. In a number of CMAs, households financing recent condominium purchases had median monthly shelter costs that were hundreds of dollars less than the costs faced by borrowers financing the recent purchases of other homes. Differences were generally larger in the West, especially in CMAs in British Columbia, where they amounted to $450 or more per month. These figures likely underestimate the cost advantage of condominiums since a portion of repair and maintenance spending, in the form of condominium fees, is included in shelter cost data collected for condominium owners, but not in the cost data for other homeowners. All things considered, shelter cost estimates confirm that condominiums represent a relatively less expensive homeownership option. FIGURE 9 Shelter costs are generally lower for condominiums than for other home types Median shelter costs 1 for condominium owners with mortgages and other owners 2 with mortgages, recently constructed units, 3 selected CMAs, 2011 Victoria Vancouver Abbotsford-Mission Kelowna Edmonton Calgary Saskatoon Regina Winnipeg Barrie Hamilton Toronto Oshawa Ottawa Gatineau Montréal Québec Halifax ,000 1,500 2,000 2,500 Median monthly shelter costs ($) Non-Condominium Condominium 1 Shelter costs include mortgage payments (principal and interest), property taxes, and condominium fees, along with payments for electricity, fuel, water and other municipal services. 2 Excludes farm households. 3 Recent construction refers to units built from January 1, 2006 to May 10, 2011 (Census Day). Quebec and Ontario portions of Ottawa-Gatineau are shown separately. Source: Statistics Canada (National Household Survey) 14

15 9 Mobility and condominium market growth The oldest baby boomers the large generation born in the two decades following World War II have turned 65. Further aging of baby boomers will likely contribute to continued growth in the numbers of one-person households and couples without children, the household types that account for the bulk of condominium residents. Earlier generations achieved their highest rates of condominium ownership during their senior years. If baby boomers follow the same pattern, many will buy condominiums as they age. FIGURE 10 Seniors less likely to move than other age groups Mobility by Age Group, Canada, % of population moving in previous 5 years Mobility data from the 2011 National Household Survey (NHS) and earlier Censuses are not strictly comparable. Census data include people living in non-institutional collective dwellings, such as rooming houses, motels, student residences, and residences for senior citizens, whereas NHS data include only the population living in private households. Source: CMHC, adapted from Statistics Canada (Census of Canada and National Household Survey) One factor that may ultimately restrain the growth of condominiums, however, is the desire of many aging households to remain in their current homes. Despite the increasing availability and popularity of condominiums, the rates at which different age groups move appear, if anything, to have dropped over the past two decades. In 2011, 18% of seniors had moved in the previous five years, compared to 22% in The fact that more than 80% of seniors do not move in any given five-year period suggests that many remain strongly attached to their homes. If baby boomers exhibit similar tendencies, the turnover of the housing stock as they age will be gradual. 15

16 10 Physical condition Reduced maintenance responsibilities are one potential attraction of condominiums; maintenance and repairs to common property elements are handled collectively, often through a property management company, and are typically paid for out of monthly fees or accumulated reserve funds. Comprehensive and up-to-date expert assessments of the state of repair of housing in Canada, including condominiums, are not available. The evidence that does exist is survey data based on the opinions of occupants, not formal inspections. In 2011, condominium owners (5%) were somewhat less likely than other homeowners (7%) to state that their homes (for condominium owners, this relates to their own units, not to the common property elements) were in need of major repairs. The lower perceived rate of disrepair for condominiums reflected their comparatively recent construction. When homes of similar age are compared, condominiums show slightly higher perceived rates of disrepair than other owner-occupied dwellings. In general, however, the perceived rate of disrepair for condominiums in 2011 was low and broadly comparable to that of other homes of similar age. FIGURE 11 Physical condition of condominiums similar to other owner-occupied homes Need for Major Repairs, Condominiumsand Other Owner-Occupied Dwellings, Canada, 2011 % of dwellings rated by occupants as needing major repairs Condominiums Other dwellings All occupied dwellings 1945 or before 1946 to to to to 2011 Source: CMHC, adapted from Statistics Canada (National Household Survey) Period of construction 16

17 Alternative text and data for figures Figure 1: Condominiums come in various structure types Condominiums by structure type (%), Canada, 2011 Structure type Per cent Single-detached house 4 Low-rise apartment 36 High-rise apartment 31 Row house 23 Other dwelling 6 Includes both owner-occupied and rented condominiums. Low-rise apartments are in buildings with fewer than five storeys. High-rise apartments are in buildings with five or more storeys. Other dwellings comprise duplexes, single-attached houses (a single dwelling attached to another building), semi-detached houses, and movable dwellings. Source: CMHC, adapted from Statistics Canada (National Household Survey) 17

18 Figure 2: Distribution of structure types varies across the country Condominiums by structure type, CMAs, 2011 Distribution of condominiums by structure type Geography Low-rise apartments (%) High-rise apartments (%) Row houses (%) Single-detached houses (%) Other dwellings (%) Victoria Vancouver Abbotsford-Mission Kelowna Edmonton Calgary Saskatoon Regina Winnipeg Thunder Bay Greater Sudbury/Grand Sudbury Barrie Windsor London Guelph Brantford Kitchener-Cambridge-Waterloo St. Catharines-Niagara Hamilton Toronto Oshawa Peterborough Kingston Ottawa Gatineau Montréal Trois-Rivières Sherbrooke Québec Saguenay Saint John Moncton Halifax St. John s Includes both owner-occupied and rented condominiums. Quebec and Ontario portions of Ottawa-Gatineau are shown separately. Low-rise apartments are in buildings with fewer than five storeys. High-rise apartments are in buildings with five or more storeys. Other dwellings comprise duplexes, single-attached houses (a single dwelling attached to another building), semi-detached houses, and movable dwellings. Source: CMHC, adapted from Statistics Canada (National Household Survey) 18

19 Figure 3: Senior households are the age group most likely to live in high-rise apartments Structure type choices of condominium owners by age group, Canada, 2011 Age group of primary household maintainer High-rise apartments (%) Low-rise apartments (%) Row houses (%) Single-detached houses (%) Other dwellings (%) Low-rise apartments are in buildings with fewer than five storeys. High-rise apartments are in buildings with five or more storeys. Other dwellings comprise duplexes, single-attached houses (a single dwelling attached to another building), semi-detached houses, and movable dwellings. Source: CMHC, adapted from Statistics Canada (National Household Survey) Figure 4: Increase in condominium ownership highest in Vancouver, Montreal and Saskatoon Condominium share of growth in homeownership, Canada and CMAs, Change in owner-occupied Geography condominiums as a % of change in owner households Canada 27.7 All-CMAs 31.6 Vancouver 58.2 Montréal 39.8 Saskatoon 39.6 Victoria 37.2 Hamilton 35.1 Regina 34.6 Toronto 33.8 Abbotsford-Mission 32.6 Calgary 31.2 Edmonton 30.3 Québec 30.0 Winnipeg 25.1 Kelowna 24.9 London 24.2 Guelph 21.3 St. Catharines-Niagara 19.0 Change in owner-occupied Geography condominiums as a % of change in owner households Ottawa 18.8 Kitchener-Cambridge-Waterloo 17.9 Windsor 16.1 Gatineau 14.6 Thunder Bay 13.6 Halifax 12.6 Brantford 12.6 Trois-Rivières 12.3 Saguenay 12.1 Sherbrooke 11.2 Kingston 10.2 Oshawa 9.0 St. John s 8.9 Moncton 8.5 Peterborough 8.0 Barrie 7.7 Saint John 6.3 Greater Sudbury/Grand Sudbury 1.9 Data from the 2011 National Household Survey may not be comparable to those from earlier censuses. Quebec and Ontario portions of Ottawa-Gatineau are shown separately. Source: CMHC, adapted from Statistics Canada (Census of Canada, National Household Survey) 19

20 Figure 5: Condominiums more likely to be owned than rented Occupied condominiums by tenure, Canada, 2011 Tenure 2011 (units) All occupied condominiums 1 1,615,485 Owner-occupied condominiums 1,153,585 Rented condominiums 461,215 1 Includes 700 units of band housing. Source: CMHC, adapted from Statistics Canada (National Household Survey) Figure 6: Popularity of condominiums increased in all age groups Condominium ownership rates by age of primary household maintainer, 1 Canada, 1996, 2001, 2006, 2011 Age group Condominium owners as a % of all households 1996 (%) 2001 (%) 2006 (%) 2011(%) A household maintainer is the person or one of the people in the household responsible for major household payments such as the rent or mortgage. Where more than one person in a household claims responsibility for such payments, the primary maintainer is the first person listed on the census form as a maintainer. Data from the 2011 National Household Survey may not be comparable to those from earlier censuses. Source: CMHC, adapted from Statistics Canada (Census of Canada, National Household Survey) 20

21 Figure 7: One-person households and couples without children own 71% of condominiums Distributions of condominium owners and other homeowners by household type (%), Canada, 2011 Household type Condominium owners (%) Other homeowners (%) Couples without children Couples with children Lone-parent households 9 8 One-person households Other households 5 5 Other households comprise multi-family households and non-family households of two or more persons. Family households include at least one census family (a couple with or without children or a lone parent) and may include additional members who are not part of the census family. Source: CMHC, adapted from Statistics Canada (National Household Survey) Figure 8: Across Canada, condominiums are more affordable than non-condominiums Median estimated dwelling values 1 for condominiums and other owner-occupied dwellings, selected CMAs, 2011 Geography Condominium ($) Non-Condominium ($) Victoria 348, ,928 Vancouver 375, ,781 Abbotsford-Mission 210, ,651 Kelowna 289, ,227 Edmonton 250, ,098 Calgary 286, ,199 Saskatoon 250, ,761 Regina 259, ,642 Winnipeg 190, ,165 Barrie 174, ,709 Hamilton 240, ,332 Toronto 295, ,427 Oshawa 180, ,263 Ottawa 229, ,357 Gatineau 165, ,602 Montréal 229, ,700 Québec 200, ,721 Halifax 200, ,864 1 Values estimated by homeowners if their dwellings were to be sold. Excludes farm households. Quebec and Ontario portions of Ottawa-Gatineau are shown separately. Source: Statistics Canada (National Household Survey) 21

22 Figure 9: Shelter costs are generally lower for condominiums than for other home types Median shelter costs 1 for condominium owners with mortgages and other owners 2 with mortgages, recently constructed units, 3 selected CMAs, 2011 Geography Condominium ($) Non-Condominium ($) Victoria 1,538 2,289 Vancouver 1,759 2,423 Abbotsford-Mission 1,243 2,202 Kelowna 1,603 2,100 Edmonton 1,554 2,058 Calgary 1,642 2,087 Saskatoon 1,498 1,902 Regina 1,446 1,967 Winnipeg 1,438 1,754 Barrie 1,537 1,898 Hamilton 1,504 1,967 Toronto 1,709 2,054 Oshawa 1,458 1,893 Ottawa 1,567 1,862 Gatineau 1,205 1,492 Montréal 1,228 1,593 Québec 1,131 1,417 Halifax 1,620 1,713 1 Shelter costs include mortgage payments (principal and interest), property taxes, and condominium fees, along with payments for electricity, fuel, water and other municipal services. 2 Excludes farm households. 3 Recent construction refers to units built from January 1, 2006 to May 10, 2011 (Census Day). Quebec and Ontario portions of Ottawa-Gatineau are shown separately. Source: Statistics Canada (National Household Survey) 22

23 Detailed Examination of Municipal Accessory Apartment Regulations Article 2 November

24 1 Introduction The purpose of this study was to 1) examine the characteristics and attributes of the municipal regulations of the 498 municipalities in Canada that allow accessory apartments and 2) to assess how likely these regulations are to enable or dissuade the creation of accessory apartments. In addition, this study collected data on the number of building permits issued for accessory apartments between 2011 and 2013, to assess the feasibility of using building permit data to determine the number of accessory apartments created in a three-year time frame. The focus was only on those units that were created legally through a development and/or building permit process. An accessory apartment is a self-contained dwelling that is accessory to the principal dwelling, and is located either within the primary dwelling or in an accessory building on the same lot as the primary dwelling. Accessory apartments have over 50 different names in the regulations examined, such as garden suite, coach house, basement suite, secondary suite or granny suite in English, and in French, pavilion jardin, logement supplémentaire, logement au sous-sol, or logement intergénérationnel. 2 Methodology Part 1 Analysis of Accessory Apartment Regulations The 2014 study Municipal Accessory Apartment Regulations in the 33 Census Metropolitan Areas and 114 Census Agglomerations in Canada collected information on 650 municipalities, of which 498 permit accessory apartments. Since the objective of this study was to further analyze the regulations that permitted accessory apartments, only the 498 municipalities where accessory apartments are permitted were considered. General provisions for accessory apartments were documented from each municipal by-law which indicated under what circumstances such suites were permitted. While each by-law is unique, the majority had at least a few of the following provisions: Requirement for a specific occupant Limit on the number of occupants Owner occupancy requirement for one of the units Time limitations/temporary use (particularly regarding garden suites) Discretionary or conditional use provisions 24

25 Requirements for special permits or agreements or specific Council approval Restriction by type of building, specific zone, or both Minimum parking requirements Architectural integration requirements Minimum or maximum size requirements. The following were used to categorize each of the identified provisions: (L) Likely to hinder the creation of accessory apartments (SWL) Somewhat likely to hinder the creation of accessory apartments (NL) (CC) Not likely to hinder the creation of accessory apartments; and Case-by-case assessment depends on the nature of the requirement and municipal context. Once each provision was categorized an overall classification of (1) enabling, (2) somewhat restrictive or (3) restrictive was made for the municipal by-law, based on a combination of the number of regulations and likelihood that the regulations would hinder the creation of accessory apartments. The three overall classifications are defined as follows: Enabling (E) Those by-laws that have either no restrictions or very few conditions that are not likely to pose a hindrance to accessory apartment creation. Somewhat Restrictive (SR) A combination of conditions that would be somewhat likely to be a hindrance to accessory apartment creation. Restrictive (R) Regulations with a combination of conditions that are likely to hinder the creation of accessory apartments. Part 2 Tracking the Number of Accessory Apartments Created To determine how many accessory apartments were created in each of the municipalities over a three-year period, information on the number of legal accessory apartments was collected by obtaining building permit records from municipal building departments. In some cases, the building permit information was available on municipal websites; however, it often did not include a separate category for accessory apartments and the municipality had to be contacted for clarification. 25

26 3 Findings The total number of municipalities studied in each province and territory and the percentage of those municipalities where the accessory apartment by-law was classified as restrictive, somewhat restrictive or enabling is shown in Figure 1. Of the 498 municipalities in Canada that permit accessory apartments, the study found the following results: 42% have enabling by-laws with no restrictions or few conditions that are likely to pose a hindrance to accessory apartment creation; 10% have somewhat restrictive regulations that included a combination of conditions that would be somewhat likely to be a hindrance to accessory apartment creation; and 46% to have restrictive regulations with a combination of conditions that are likely to hinder the creation of accessory apartments. FIGURE 1 Proportion of municipalities permitting accessory apartments with enabling, somewhat restrictive and restrictive regulations, by Province and Territory, 2014 CANADA Newfoundland and Labrador Prince Edward Island Nova Scotia New Brunswick Quebec Ontario Manitoba Saskatchewan Alberta British Columbia Northwest Territories Yukon Per cent Enabling regulations Somewhat restrictive regulations Restrictive regulations Uncategorized (Not enough information) 26

27 The majority of by-laws permitting accessory apartments are for units within the primary dwelling. However, a number of municipalities also permit accessory apartments in an accessory building such as a garden suite. In most cases where a municipality permits more than one type of accessory apartment, both types of accessory dwellings have similar provisions, and the municipality was given a single classification of restrictive, somewhat restrictive or enabling based on the regulation for a secondary suite in the primary dwelling. 4 Regional Analysis Among the provinces, British Columbia and Newfoundland and Labrador have the highest proportion of enabling regulations in Canada at 66% and 65% respectively. The majority (55%) of Québec municipal regulations were categorized as restrictive. This is mostly influenced by the fact that many of the regulations required that the accessory apartment be occupied by a specific occupant, usually someone related to the registered owner of the primary dwelling. While Ontario had a relatively high proportion of enabling regulations (49%), it also had 21% somewhat restrictive regulations and 29% restrictive. In all of Canada, Alberta had the lowest rate of enabling municipalities. This is because most municipalities in Alberta that permit accessory apartments allowed them on a conditional or discretionary basis, which may involve special approvals as well as additional time and costs without a guarantee that an accessory suite may be permitted. 5 Core Cities Analysis Core municipalities are usually urban areas with larger and denser populations and possibly higher demand for accessory apartments than rural areas or smaller municipalities. Canada has 147 such core municipalities of which 120 or 82% permit accessory apartments (95 in CAs and 25 in CMAs) according to the 2014 study. Out of the 25 CMA core municipalities, 7 were categorized as restrictive, 7 as somewhat restrictive, and 11 as enabling. Out of the 95 CA core municipalities, 44 were categorized as restrictive, 8 as somewhat restrictive, and 43 as enabling. 27

28 6 Number of Legal Accessory Apartments To determine how many legal accessory apartments may have been created in 2011, 2012 and 2013 in the 498 municipalities that permit them, municipalities were contacted to obtain the number of building permits issued for each year for such suites in their jurisdiction. Efforts were also made to collect information on permits obtained for suites in the primary dwelling or in an accessory building, as well as the number of those suites that were new construction or additions or modifications to an existing dwelling. A 70% response rate was obtained from all municipalities, although a number of municipalities who did respond stated they did not collect the specific details on the type of suite when issuing residential building permits. Some municipalities collect the total number of permits issued for accessory apartments but may not track whether the unit is in the primary or accessory building or whether they are additions to an existing dwelling or new construction. Where data were unavailable, a few officials provided estimates. Over the three year period , 15,421 accessory apartments were created based on the building permit information available. This includes units in new construction, units created as part of an existing home renovation and, in some cases legalization of a pre-existing illegal or non-conforming suite. It is very likely a much larger number of accessory apartments were created than accounted for; however, at this time, there is no easy way of tracking them through the building permit process. So although the data can be used to estimate the number and to some extent the types of dwellings in each municipality and province, when factoring in the response rate, the total should be viewed as an incomplete estimate. Figure 2 illustrates the types of units for which building permits were obtained for municipalities where this information was tracked. The majority (86%) of accessory apartments created were suites within the primary dwelling while the rest were units in an accessory building such as a garden suite. In addition, of the 11,243 accessory apartments for which data were available, about 58% of the units were in new home construction and 42% were renovations to existing homes. 28

29 FIGURE 2 Percentage of accessory apartments that are within or outside the primary residence and are new build or renovations, Canada, % 42% 86% 58% In primary residence Out of primary residence New Build Renovations 7 Implications for the Housing Industry and Policy Makers Changes in demographics, economics and community goals are leading to innovative ways of increasing the housing supply. A consistently low volume of construction of new purpose-built rental housing over the past two decades is resulting in low vacancy rates and rising rents in some jurisdictions across Canada. Alternative rental housing or the secondary rental market, which includes accessory apartments, is an important component of the rental housing sector. In particular, accessory apartments offer an affordable housing option. Regulations help to ensure personal safety and community integration, but the findings of this research show, that while there is great interest in increasing the availability of accessory apartments across the country, there are also significant concerns over community and neighbourhood impacts in many jurisdictions. As demand for affordable housing options such as accessory apartments continues to grow, regulatory approaches may need to be examined to ensure that they are not creating unintended or unnecessary barriers. Better data on the creation of accessory apartments could contribute to a better understanding of the volume and type of suites being created, which in turn may help to guide local dialogues on accessory apartments. 29

30 The Housing Observer Online offers a variety of information on different topics: Housing Markets Housing Finance Housing Data Housing Needs Housing Demographic Affordable Housing Seniors Housing Housing Policy Visit to get the latest information CMHC Project Managers: Janet Kreda, Senior Researcher; Kathleen Ireton, Researcher Housing Needs Research Consultant: Muniscope 30

31 Alternative text and data for figures Figure 1: Proportion of municipalities permitting accessory apartments with enabling, somewhat restrictive and restrictive regulations, by Province and Territory, 2014 Jurisdiction Enabling Regulations (%) Somewhat Restrictive Regulations (%) Restrictive Regulations (%) Uncategorized (not enough information) (%) CANADA Newfoundland and Labrador Prince Edward Island Nova Scotia New Brunswick Quebec Ontario Manitoba Saskatchewan Alberta British Columbia Northwest Territories Yukon Figure 2: Percentage of accessory apartments that are within or outside the primary residence and are new build or renovations, Canada, Accessory Apartment Percentage (%) In primary residence 86 Out of primary residence 14 New build 58 Renovations 42 31

32 Credit: Olivier Middendorp via Hollandse Hoogte 3D Printing and the Construction Industry 32

33 1 What is 3D Printing? 3D printing, also referred to as additive printing or additive manufacturing, is a revolutionary production technique capable of creating solid objects from a digital file uploaded to a 3D printer. The printer reads the file and lays down successive layers of materials, such as plastics, resins, concrete, sand or metals, until the entire object is created. 2 3D Printing in the Construction Industry In the construction industry, 3D printers are used to create 3D models, prototypes or small, non-structural building components such as landscaping bricks or decorative elements. 1 Researchers are experimenting with different types of 3D printers and a range of raw materials and fabrication techniques to advance the technology and expand the range of potential applications to include structural building components and even whole buildings. Current research includes experimentation with: a variety of raw materials including recycled plastic, bioplastics, concrete and a synthetic stone-like material created from a combination of sand and chemicals; advanced 3D printers capable of extruding multiple materials; 2 a variety of fabrication methods (e.g., printing wall components in sections which can be snapped together on site; printing structural scaffolding which can be filled in with construction materials on site to create full-sized walls 3 ); fabrication of reinforced concrete beams; 4 and direct printing on-site or in factories

project currently being printed in Amsterdam.")

34 3 3D Printed Residential Buildings Research projects are underway to create residential buildings from 3D printed modular components. One example is Canal House (DUS Architects) project currently being printed in Amsterdam. Building blocks 3D Print Canal House, credit: DUS architects The 3D Canal House is a 3-year research and development project to create a 13 room demonstration house. The project team built a 3D printer, called a KamerMaker or room maker, which was installed inside a large, upended shipping container. The printer creates wall components from a bioplastic mix of plastic fibres and 80% plant oil. Wall components are then interlocked together and filled with bio-concrete to provide structural strength. See more at: 34

3D printer, called the Big Delta was unveiled in Italy by the World s Advanced Saving Project (WASP).")

35 Architects, engineers and researchers are also exploring the potential of creating complete buildings from 3D printers. In September 2015, a 12 meter (40 foot) 3D printer, called the Big Delta was unveiled in Italy by the World s Advanced Saving Project (WASP). 5 The printer is designed to produce a complete shelter using local materials, such as mud, clay and natural fibres and could potentially be used to create housing in disaster areas or areas where a large supply of emergency housing is needed. 6 Berok Khoshnevis, from the University of Southern California, has developed a 3D fabrication process called contour crafting which he believes offers the potential to automate the construction of a complete house including electrical, plumbing, drywall and insulation (see He envisions widespread use of light-weight contour crafting 3D printers to print houses by 2020 and high rises by Credit: Berok Khoshnevis, University of Southern California

36 4 Potential Implications of 3D Printing for the Home Building Industry Although still in its early days, 3D printing could offer the following benefits: Onsite or factory applications. Printed products only use as much material as needed to form them. This means fewer resources are required and less waste is generated. Reduced transportation costs if products are printed on-site (although the cost of transporting the printer can be expensive due to the size of printers currently needed for construction). Potential to create more efficient and interesting designs as 3D printing can achieve shapes that conventional techniques cannot. Lower labour costs. Reduced cost of customized design (with 3D printing, it costs the same to create one item as to produce thousands.) Reduced health and safety risks if 3D printing can be used to produce assemblies that would otherwise need special equipment and precautions to be taken. Current challenges to be overcome include: More expensive than conventional construction due to high cost of 3D printer and lack of familiarity in the industry with 3D printing technologies and applications. Currently, a limited number of materials have been used, although experimentation is underway with printers capable of using multiple materials to produce more complex assemblies. 3D printers can be large and, therefore, difficult and costly to place on site. 3D printing incurs more up-front costs to create the digital model that will result in safe, cost-effective products. Printers are currently slow compared to conventional construction, although they can be operated 24 hours a day, seven days a week. The potential of a disruptive impact on the type of skills and labour needed to design and build homes. 36

37 5 The Future of 3D Printing in Residential Construction There is a wide range of views about where the technology could be headed. Although 3D printing is still in its early days in all industries, the potential benefits seem to be driving the technology forward. Some suggest 3D printers will be used mainly to print building components and panels either in factories or on site, while others envision 3D printing as a transformative technology that could revolutionize the construction industry. 37

38 Flexible Housing 38

39 1 What is Flexible Housing? The concept of flexible housing has its roots in the innovative Grow Home developed in 1990 by Avi Friedman and Witold Rybczynski at Montreal s McGill University School of Architecture. Designed to be affordable, the Grow Home incorporated flexible and adaptable living spaces within a small footprint. Building on this concept, in 1995 (CMHC) created FlexHousing as part of the universal/inclusive design movement. The objectives of universal housing are the following: Allow people to occupy their homes for longer periods of time; Create housing that meets a wide range of needs; and Improve the convenience of a home for its occupants. 2 How the Flexible Design Concept Works Flexible housing is achieved through planning, design, and construction or renovation. Forethought and careful consideration of possible future needs are required at the design stage to permit maximum flexibility, at the least cost, in the living spaces over time. 3 Everyone Benefits from a Flexible Home A flexible home is an ideal choice for everyone as needs change over time in response to personal circumstances such as aging, changing health conditions, and household composition and income changes. In addition to being well-suited to meet the needs of an aging population and people with disabilities and other special needs, flexible housing is also a good choice for multi-generational living or for households which will need a future home office, or an independent suite for a family member, caregiver, or tenant. Additionally, as well-designed flexible housing is better prepared to adapt to a broad range of needs, it can appeal to a wider range of buyers on eventual resale. 39

40 4 Flexible Housing is an Affordable Option Although flexible housing may initially cost slightly more than a conventional house, it can offer significant savings compared to the costs of demolition and renovation at a future date. The incremental costs of flexible housing features can be less than the cost of relocating when all related expenses, such as packing, moving, new furnishings and appliances, commissions and various fees are factored in. For more information read, Sustainable Housing and Communities Flexible Housing 40

41 First Annual Estimate of Urban Households in Core Housing Need Based on Statistics Canada s New Canadian Income Survey 41

42 First Annual Estimate of Urban Households in Core Housing Need Based on Statistics Canada s New Canadian Income Survey In the 2012 base year, Statistics Canada replaced the Survey of Labour and Income Dynamics (SLID) with the Canadian Income Survey. According to estimates of urban core housing need based on data from the Canadian Income Survey, 1.4 million urban households, or 13.5% of all Canadian households living in urban areas, were in core housing need in This proportion is virtually the same as in 2012, considering the statistical accuracy of the estimate based on this survey. In 2012 and 2013, Ontario remained the province with the highest proportion of urban households in core housing need. In 2013, about half of urban households in core housing need, that is, 739,197 households, were living in Ontario. Ontario and British Columbia were the only two provinces whose proportion of urban households in core housing need was higher than the national average in New Brunswick and Alberta, for their part, were the provinces with the smallest percentage of urban households in core housing need in

43 In 2013, 13.5% of Canadian Households Living in Urban Areas Were in Core Housing Need Source: CMHC (housing indicators and data based on the 2012 and 2013 Canadian Income Survey and the 2011 National Household Survey) Canada 12.8% 13.2% 13.5% Ontario 14.0% 16.6% 16.6% British Columbia 15.7% 16.2% 16.1% Prince Edward Island 9.0% 9.9% 12.9% Nova Scotia 12.8% 14.1% 12.5% Manitoba 10.0% 10.4% 11.8% Saskatchewan 12.0% 12.5% 11.6% Newfoundland and Labrador 12.0% 12.5% 10.3% Québec 11.3% 8.9% 9.8% Alberta 10.4% 7.8% 8.9% New Brunswick 9.8% 8.7% 8.4% 43

44 Industrialized Housing 44

45 Industrialized Housing The modern era of factory-built housing began during the Second World War. Homes were built in a way that would take as little material away from the war effort as possible. These days, the most common forms of factory-built housing are referred to as manufactured and modular homes. Manufactured homes These complete factory-built houses are delivered to their final destinations and placed onto wood or concrete-block piers (to create a crawl-space) or on full-depth basement foundations. Cabinets, flooring, appliances and electrical and plumbing systems are installed and ready to be connected to municipal utilities networks. Homes are built in compliance with a series of standards and are certified before leaving the factory. 45

46 Annual Factory-built, single-detached starts Share of all single-detached starts , % , % , % , % , % , % , % , % , % , % , % Modular homes Factory-built modules are transported and assembled onsite and typically placed on full-depth basement foundations. Modular houses are subject to the same codes as site-built homes as it involves on-site construction processes. Prefabrication In other housing processes, prefabricated panels are often used for walls, floors, and roof assemblies. Manufacturers have developed approaches to interlock the panels together so that the joints are air tight. With panelized construction, the outer walls can go up in as little as one day leaving a weather tight home for the trades to work in focussing on interior completion. Engineered wood products perform better than traditional cut lumber. They are less susceptible to warping, shrinking, and twisting, and they reduce the impact of residential construction on our forests. Other housing components that are commonly prefabricated include window assemblies, door assemblies, cabinets kitchen and bathroom pods 46

47 Distribution Producers of manufactured homes sell through retailers or dealers whereas modular housing producers increasingly sell through on-site builders, often with the producer and the builder sharing the credits in the promotion of the project. Strengths Shorter on-site construction time Precision construction and quality control Potential for improved energy efficiency Reduced waste generation and improved reuse-recycling possibilities Easy to disassemble and reconfigure Labour cost advantages and bulk buying power In-house design and development Challenges Larger capital/high fixed costs vs. site-built houses Transportation freight costs and restrictions For a more in-depth discussion see Sustainable Housing and Communities Industrialized Housing from the 2013 Canadian Housing Observer. 47

.")

48 HPAA Now Called the Housing Market Assessment (HMA) Report This quarterly release of the Housing Market Assessment (HMA) provides updated results regarding evidence of problematic housing market conditions in 15 Census Metropolitan Areas (CMAs). 48

49 Overvaluation Most Commonly Detected Problematic Condition This quarterly release of the Housing Market Assessment (HMA) provides updated results regarding evidence of problematic housing market conditions in 15 Census Metropolitan Areas (CMAs). The HMA points to strong overall evidence of problematic conditions in Toronto, Winnipeg, Saskatoon and Regina. In Toronto, it reflects a combination of price acceleration and overvaluation, while in Winnipeg, Saskatoon, and Regina it reflects detection of overvaluation and overbuilding. The most prevalent issue detected in 11 of the 15 centres covered by the HMA is overvaluation. The evidence of overvaluation has increased since the previous assessment in Toronto, Vancouver, Montréal, Edmonton, and Saskatoon as price levels are not fully supported by economic and demographic factors. Problematic overvaluation conditions in local housing markets could be resolved by moderation in house prices and/or improving economic conditions. See the full report: Housing Market Assessment: Canada Edition 49

50 Housing Data Find What You Need You may have noticed that the Observer format has changed and that the online data can now be found under Housing Market Information. Whether you are an occasional or heavy user, data is useful to validate your housing strategies and decisions with numeric evidence. 50

51 Consider Some Possible Uses of Housing Data Do you require demographic information to complete your municipal or housing development strategy? You may need average incomes, average sales or rents, or number of households in core housing need? Are you completing a needs and demand analysis for a funding proposal? Need information at your fingertips? You may wish to include average incomes, average rents, gender-based data, and the number of households in core housing need. When you meet with your board or association you can have data to back up your ideas. It can help you to understand your community composition. How many are seniors? How much do they spend on housing? How much do they earn; and, how many are in core housing need? You can tailor your outreach to vulnerable groups specific to your area. Perhaps lone-parent women in your location are more likely to be in core housing need. Data can assist you with forecasting and preparing for possible change. Will the population find a large number of seniors in the upcoming years requiring a certain type of housing or related services in your area? Data gives those reviewing funding proposals a clearer picture as to why you are requesting financial assistance. Examples of possible proposal topics could be as follows: the creation of a new affordable housing project, an upgrade to existing housing that may be in need of renovations or accessibility modifications, a conversion to housing from a non-residential use, the housing needs of victims of family violence, or rent subsidies for individuals and families in need. 51

52 To Access Housing Data, Visit: Data Tables Excel spreadsheets with timeline information, Housing in Canada Online (HiCO) an application that allows you to manipulate data for your own research purposes, Housing Market Information Portal a tool for custom research, Interactive Local Data Tables A range of housing information for over 160 municipalities to assist you with making informed decisions. If your town is not listed in the local data tables, you can make a request. Learn More about How to Use Our Data Tools with these Quick Start Videos: Housing in Canada Online (HiCO) (Video) The Housing Market Information Portal (Video) 52

53 Mortgage Arrears 53

54 Mortgage Arrears Nudged Downward Again in 2014 Mortgage arrears in Canada, defined as the percentage of residential mortgages that are delinquent for three months or more, fell slightly again on an annual average basis in 2014, to 0.29%, from 0.31% in However, this may be poised to change, as there was a marginal increase in the arrears rate in 2015 Q1. Regionally, arrears rates were much higher in the Atlantic provinces (0.59%) and Saskatchewan (0.40%); while the lowest arrears rate was observed in Ontario (0.17%) in 2015 Q1. 1 In comparison, the average arrears rate for prime fixed-rate mortgages in the United States (the most comparable mortgages to the overall Canadian mortgage market), was 1.01% in 2015 Q1. 2 While mortgage arrears in the U.S. have recovered significantly from their peak during the financial crisis, they have not yet reached pre-crisis levels, when they were similar to mortgage arrears rates in Canada. While the Canadian arrears rate is useful for observing overall trends, it has limitations, since it is an average of all residential mortgages from 10 financial institutions. 3 From a public policy perspective, it would be useful to have more detailed data from all lenders, to better understand differences in arrears rates between types of mortgage lenders (e.g. big vs. small) and types of mortgages (e.g. insured vs. uninsured; prime vs. non-prime). For example, data from the United States indicates differences in arrears by loan types: 8.53% for sub-prime loans, compared to 1.12% for prime-fixed rate loans in For more on Canadian and U.S. mortgage arrears, see the data table Canadian and U.S. Residential Mortgage Arrears 1 Canadian Bankers Association. 2 U.S. Mortgage Bankers Association. 3 These 10 financial institutions are estimated to currently account for approximately three-quarters of outstanding mortgage credit in Canada. 54

55 Canada: all residential mortgages (%) Canada: average (%) U.S.: prime fixed-rate mortgages (%) U.S.: average since (%) Q Sources: Canadian Bankers Association and U.S. Mortgage Bankers Association 55

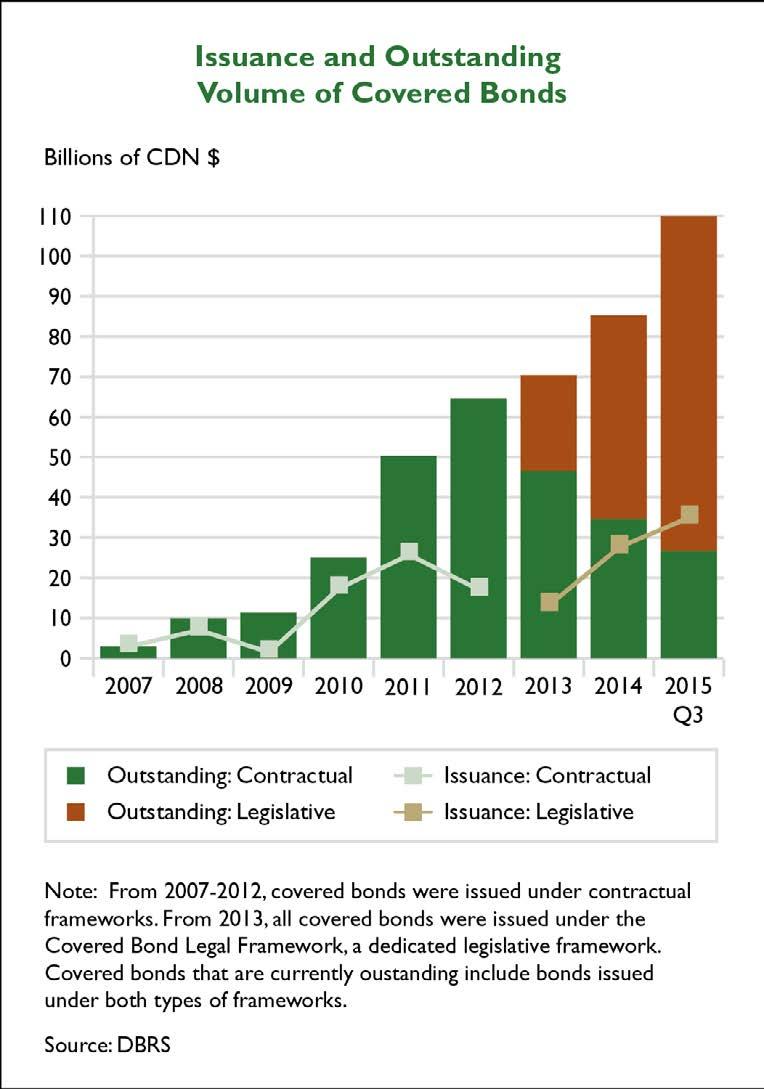

56 Record Covered Bond Issuance of $27.6 Billion in

57 Record Covered Bond Issuance of $27.6 Billion in 2014 Covered bonds are debt obligations generally issued by large, regulated financial institutions and secured by a segregated pool of assets, with residential mortgages the most common asset type. After their introduction in Canada in 2007, there was rapid growth in the issuance of covered bonds. Issuance peaked at $25.7 billion in 2011, under the contractual framework that governed covered bonds from 2007 to 2012 (see grey line (Issuance: Contractual) in chart). Effective 2013, the Government of Canada established a dedicated legal framework for the future issuance of covered bonds. The Covered Bond Legal Framework has made the Canadian covered bonds market more robust, by improving investor certainty in regards to their asset, and by diversifying the investor pool, as some international investors who invest in covered bonds can only purchase those that are issued under a legislative framework. With the switch to the legislative framework there was an adjustment period for issuers. Issuance of covered bonds under the legislative framework began in mid-2013 (see light brown line (Issuance: Legislative) in chart), and surged to $27.6 billion in Issuance reached record high in 2015, with $35.0 billion issued since January. As of 2015 Q3, the total value of covered bonds outstanding stood at $109.6 billion, 76% of which is now under the legislative framework. (see brown bar (Outstanding: Legislative) in chart). Covered bonds provide a diversified funding source for lenders. Covered bonds issued under the legislative framework represent a private source of mortgage funding, as taxpayer-backed insured mortgages are prohibited as collateral assets in cover pools. The term lengths of covered bonds are mostly five-year, but have included seven-year and three-year terms. In the last two years, issuance of covered bonds has been predominately in Euros and U.S. Dollars, with a few issues also in Australian Dollars and British Pounds. Issuing bonds denominated in foreign currencies allows issuers to appeal to more foreign investors and hence achieve greater market depth in foreign markets. 57

58 58

59 Year Issuance and Outstanding Volume of Covered Bonds Issuance Contractual Billions of CDN ($) Issuance Legislative Outstanding Contractual Outstanding Legislative Total Q Note: From , covered bonds were issued under contractual frameworks. From 2013, all covered bonds were issued under the Covered Bond Legal Framework, a dedicated legislative framework. Covered bonds that are currently outstanding include bonds issued under both types of frameworks. Source: DBRS For more on mortgage funding sources in Canada, see the Housing Finance chapter of the 2014 Canadian Housing Observer More data on the covered bond market can be found in the data table Covered Bonds (xls) 59

60 LIST OF TABLES 1 Housing Market Indicators, Canada, Residential Building Permits, Canada, Provinces and Metropolitan Areas, (units) Residential Building Permits, Canada, Provinces and Metropolitan Areas, ($) (thousands) Total Housing Starts, Canada, Provinces and Metropolitan Areas, Total Residential Sales, Canada, Provinces and Metropolitan Areas, (units) Average Residential Price, Canada, Provinces and Metropolitan Areas, (dollars) Teranet - National Bank Composite House Price Index TM (2005 = 100) Occupied Housing Stock by Structure Type and Tenure, Canada, 2001, 2006 and 2011 (dwelling units) Dwelling Condition by Tenure and Period of Construction, Canada, Ownership Rate, Canada, Provinces, Territories and Metropolitan Ares, (per cent) Rental Vacancy Rate, Canada, Provinces and Metropolitan Areas, (per cent) Average Rent for Two-Bedroom Apartments, Canada, Provinces and Metropolitan Areas, (dollars) Seniors Rental Housing, Canada, Provinces and Metropolitan Areas, Secondary Rental Market, Selected Metropolitan Areas, Households by Age of Maintainer and Tenure, Canada, Households by Type and Tenure, Canada,

61 LIST OF TABLES 17 Housing Profile of One-person and Lone-parent Households by Gender, Canada, Household Growth Summary, Canada, Provinces, Territories and Census Metropolitan Areas, 2006 and Households in Core Housing Need, Canada, Provinces, Territories and Metropolitan Areas, Characteristics of Households in Core Housing Need, Canada, Real Median After-Tax Household Income, Canada, Provinces and Selected Metropolitan Areas, (2013 constant dollars) Home Equity and Net Worth by Tenure and Age Group, Canada, 1999, 2005 and 2012 (2012 constant dollars) Home Equity and Net Worth by Tenure, Canada and Provinces, 2012 (2012 constant dollars) Residential Mortgage Credit Outstanding, by Financial Institution Type, 2014 Q Q CMHC Mortgage Loan Insurance Highlights, 2014 Q Q Private Mortgage Securitization, 2014 Q Q Covered Bond Market, 2014 Q Q CMHC National Housing Act Mortgage-Backed Securities (NHA MBS) Program, 2014 Q Q CMHC Canada Mortgage Bonds (CMB) Program, 2014 Q Q Canada Mortgage Bonds (CMB) 5-Year Constant Maturity Spread over the Government of Canada Curve, (basis points) Canadian and U.S. Annual Residential Mortgage Arrears and Foreclosure Rates, 2014 Q Q

62 Table 1 Housing Market Indicators, Canada, Construction Starts, total 225, , , , , , , , , ,329 Single-detached 120, , ,917 93,202 75,659 92,554 82,392 83,657 76,893 75,515 Multiple 105, , , ,854 73,422 97, , , , ,814 Semi-detached 13,477 14,358 14,432 12,651 11,114 13,006 12,570 14,285 12,544 13,407 Row 22,134 20,963 23,281 20,868 13,908 19,857 19,447 20,976 19,993 21,448 Apartment 69,407 70,761 71,713 84,335 48,400 64,513 79,541 95,909 78,493 78,959 Starts by intended market 1, total 193, , , , , , , , , ,843 Homeownership - freehold 114, , ,730 94,871 78,617 97,085 91,250 93,521 82,778 82,985 Rental 17,210 18,518 18,605 18,265 16,237 19,735 20,721 21,990 24,267 25,308 Homeownership - condominium 60,251 61,817 61,595 73,574 34,382 48,506 61,605 77,693 62,794 62,869 Other (co-op and unknown) 2, , Completions, total 211, , , , , , , , , ,428 Residential Building Permits 4 238, , , , , , , , , ,448 Residential Building Permits($) (thousands) 4 34,526 36,613 40,735 35,568 29,253 37,720 38,530 42,229 41,936 44,413 Available Supply Newly completed and unabsorbed homes 2 10,115 12,230 11,632 15,340 13,791 15,048 15,600 17,388 17,636 16,991 Single- and semi-detached 5,029 5,786 6,292 8,566 5,515 5,810 6,121 6,657 7,080 6,797 Row and apartment 5,086 6,444 5,340 6,774 8,276 9,238 9,479 10,731 10,556 10,194 Rental vacancy rate (%) Rental availability rate (%) Vacancy Rate (Standard Spaces) in Seniors Rental 7 NA NA NA NA Housing Costs New Housing Price Index (% change) Teranet - National Bank House Price Index (% change) Consumer Price Index (% change) Construction Materials Cost Index (% change) Construction Wage Rate Index (% change) Owned accommodation costs (% change) Rental accommodation costs (% change) Average rent ($) 3 Bachelor One-bedroom Two-bedroom bedroom Demand Influences Population on July 1 (thousands) 4 32,242 32,571 32,888 33,246 33,629 34,005 34,343 34,751 35,155 35,544 Labour force participation rate (%) Employment (% change) Unemployment rate (%) Real disposable income (% change) NA 1-year mortgage rate (%) year mortgage rate (%) year mortgage rate (%) Net migration 5 203, , , , , , , , , ,097 Housing in GDP ($ millions) 4 Rent imputed to owners 103, , , , , , , , , ,079 Rent paid by tenants 36,203 37,943 40,115 42,287 44,239 46,048 47,964 50,170 52,495 54,854 Total housing-related spending in GDP 5 238, , , , , , , , , ,250 Total consumption-related spending (including repairs) 148, , , , , , , , , ,594 Total residential investment 89,359 98, , ,247 99, , , , , ,656 New construction (including acquisition costs) 43,322 47,082 51,101 50,970 39,782 48,428 49,862 57,289 56,459 57,129 Alterations and improvements 30,271 33,692 37,567 39,182 41,034 42,821 43,847 45,822 47,058 50,494 Transfer costs 15,766 17,386 20,201 17,095 18,850 19,991 22,331 22,612 23,486 26,033 1 Housing units in centres 10, Homeowner and Condominium housing units in centres 50,000+ for which construction has been completed but which have not been sold. 3 In privately initiated apartment structures with at least 3 units 4 Statistics Canada (CANSIM) 5 CMHC, adapted from Statistics Canada (CANSIM) 6 Teranet National Bank House Price Index TM 7 CMHC Seniors Housing Survey. Standard space: A space where the resident does not receive high-level care (that is, the resident receivesless than 1.5 hours of care per day) or is not required to pay an extra amount to receive high-level care. Regional terms for this type of space may vary across the country. Source: CMHC (Starts and Completions Survey, Market Absorption Survey, Rental Market Survey, Seniors Housing Survey); Bank of Canada (mortgage rates); Statistics Canada (CANSIM and custom tabulation of construction materials cost index); Teranet National Bank House Price Index TM For additional data, please refer to the CMHC website: 62

63 Table 2 Residential Building Permits, Canada, Provinces and Metropolitan Areas, (units) Canada 233, , , , , , , , , ,759 Provinces Newfoundland and Labrador 2,065 2,525 3,200 3,013 3,165 3,355 3,473 2,907 2,393 1,774 Prince Edward Island , Nova Scotia 5,854 5,150 4,216 4,370 5,054 5,070 5,197 3,954 3,739 4,128 New Brunswick 4,089 4,182 4,375 3,939 3,997 3,527 3,771 3,150 2,752 1,961 Quebec 49,109 51,786 52,469 45,340 53,579 53,890 51,262 42,493 41,300 38,485 Ontario 72,418 73,271 70,031 57,653 68,703 65,374 69,884 70,133 68,800 73,438 Manitoba 5,636 6,058 5,912 4,504 6,064 6,084 7,340 7,306 7,350 5,809 Saskatchewan 3,341 5,332 5,890 4,401 5,958 6,701 8,643 8,732 7,452 5,491 Alberta 50,514 47,277 27,779 22,235 26,292 28,590 33,807 39,892 41,737 38,831 British Columbia 38,835 40,932 30,110 18,607 28,984 25,745 27,214 28,046 28,709 36,798 Metropolitan Areas St. John s 1,419 1,731 2,019 1,973 1,895 2,034 1,979 1,749 1, Halifax 3,316 2,841 1,923 2,199 2,803 3,054 3,001 2,048 2,161 2,723 Moncton 1,437 1,493 1,274 1,060 1,384 1,322 1,368 1, Saint John Saguenay , ,013 1, Québec 4,864 6,114 5,877 6,595 7,324 5,950 6,958 4,910 5,357 5,472 Sherbrooke 1,669 1,333 1,729 1,762 1,709 1,762 1,748 1,677 1,361 1,476 Trois-Rivières 1,034 1,248 1,115 1,120 1,768 1,161 1, , Montréal 24,392 24,695 24,452 19,278 22,905 26,003 22,722 19,411 19,565 18,391 Gatineau 3,330 3,374 2,980 2,585 3,162 3,092 2,958 1,959 2,153 1,767 Ottawa 5,222 6,956 7,102 6,732 7,094 6,488 6,628 5,468 7,281 4,679 Kingston Peterborough Oshawa 2,924 2,235 2,059 1,104 1,949 2,160 1,692 1,736 1,829 2,729 Toronto 34,438 35,627 33,318 28,269 32,982 32,709 38,002 39,481 34,252 38,945 Hamilton 3,300 3,283 3,595 2,100 3,456 3,137 3,205 2,561 2,647 3,232 St. Catharines - Niagara 1,451 1,183 1, ,252 1,250 1,362 1,492 1,599 1,875 Kitchener-Cambridge-Waterloo 2,994 2,837 2,743 2,790 3,952 3,396 2,280 2,431 3,728 3,578 Brantford Guelph 922 1, , ,176 1,124 1,479 London 4,073 2,901 3,133 1,981 2,322 1,615 2,243 2,317 2,442 1,863 Windsor 1, ,159 Barrie 1,309 1,262 1, , Greater Sudbury/Grand Sudbury , Thunder Bay Winnipeg 3,729 3,849 3,457 2,370 3,898 3,909 4,616 4,470 5,428 4,197 Regina 1,104 1,185 1,459 1,190 1,121 1,926 2,865 3,085 2,218 1,598 Saskatoon 1,502 2,624 2,181 1,856 3,079 3,181 3,760 3,713 3,529 2,772 Calgary 18,784 15,225 8,365 7,529 8,682 11,605 12,819 17,159 16,014 15,414 Edmonton 14,550 15,016 7,299 7,789 10,166 10,410 12,783 14,211 16,684 17,109 Kelowna 2,238 2,951 1, , ,094 1,196 Abbotsford-Mission 1,210 1,107 1, ,145 Vancouver 21,095 22,803 14,781 10,028 17,814 17,384 18,645 19,982 18,830 25,267 Victoria 2,624 2,947 2,141 1,599 1,973 1,660 2,076 1,539 1,781 2,672 Source: Statistic Canada (CANSIM) For additional data, please refer to the CMHC website: 63

64 Table 3 Residential Building Permits, Canada, Provinces and Metropolitan Areas, ($) (thousands) Canada 36,613 40,735 35,568 29,253 37,720 38,530 42,229 41,936 44,413 46,323 Provinces Newfoundland and Labrador Prince Edward Island Nova Scotia New Brunswick Quebec 6,423 7,015 7,259 6,503 8,022 8,275 8,126 6,920 6,573 6,202 Ontario 12,802 14,003 12,823 10,801 13,641 14,040 15,334 15,153 16,794 18,697 Manitoba ,221 1,274 1,311 1,080 Saskatchewan ,000 1,279 1,677 1,639 1,429 1,034 Alberta 7,714 8,557 5,689 4,990 6,193 6,525 7,753 9,228 10,111 9,155 British Columbia 6,931 7,823 6,034 3,754 5,859 5,371 5,955 5,961 6,585 8,640 Metropolitan Areas St. John s Halifax Moncton Saint John Saguenay Québec Sherbrooke Trois-Rivières Montréal 3,454 3,577 3,635 3,060 3,809 4,224 3,934 3,403 3,226 3,100 Gatineau Ottawa 782 1,047 1, , ,114 1,626 1,125 Kingston Peterborough Oshawa Toronto 6,523 7,449 6,426 5,553 6,921 7,601 8,893 8,375 8,756 10,477 Hamilton St. Catharines - Niagara Kitchener-Cambridge-Waterloo Brantford Guelph London Windsor Barrie Greater Sudbury/Grand Sudbury Thunder Bay Winnipeg Regina Saskatoon Calgary 2,797 2,978 1,777 1,679 2,005 2,501 3,040 4,021 4,239 4,087 Edmonton 2,353 2,646 1,601 1,987 2,630 2,524 2,970 3,370 3,917 3,628 Kelowna Abbotsford-Mission Vancouver 3,903 4,352 2,938 2,056 3,605 3,608 4,190 4,273 4,385 6,064 Victoria Source: Statistic Canada (CANSIM) For additional data, please refer to the CMHC website: 64

65 Table 4 Total Housing Starts, Canada, Provinces and Metropolitan Areas, (units) Canada 227, , , , , , , , , ,535 Provinces Newfoundland and Labrador 2,234 2,649 3,261 3,057 3,606 3,488 3,885 2,862 2,119 1,697 Prince Edward Island Nova Scotia 4,896 4,750 3,982 3,438 4,309 4,644 4,522 3,919 3,056 3,825 New Brunswick 4,085 4,242 4,274 3,521 4,101 3,452 3,299 2,843 2,276 1,995 Quebec 47,877 48,553 47,901 43,403 51,363 48,387 47,367 37,758 38,810 37,926 Ontario 73,417 68,123 75,076 50,370 60,433 67,821 76,742 61,085 59,134 70,156 Manitoba 5,028 5,738 5,537 4,174 5,888 6,083 7,242 7,465 6,220 5,501 Saskatchewan 3,715 6,007 6,828 3,866 5,907 7,031 9,968 8,290 8,257 5,149 Alberta 48,962 48,336 29,164 20,298 27,088 25,704 33,396 36,011 40,590 37,282 British Columbia 36,443 39,195 34,321 16,077 26,479 26,400 27,465 27,054 28,356 31,446 Metropolitan Areas St. John s 1,275 1,480 1,863 1,703 1,816 1,923 2,153 1,734 1, Halifax 2,511 2,489 2,096 1,733 2,390 2,954 2,754 2,439 1,757 2,599 Moncton 1,416 1,425 1, ,400 1,194 1, Saint John Saguenay , Québec 5,176 5,284 5,457 5,513 6,652 5,445 6,416 4,680 4,449 5,442 Sherbrooke 1,305 1,318 1,627 1,580 1,656 1,575 1,741 1,496 1,128 1,367 Trois-Rivières 1,017 1,197 1,148 1,027 1,691 1,114 1, Montréal 22,813 23,233 21,927 19,251 22,001 22,719 20,591 15,632 18,672 18,744 Gatineau 2,933 2,788 3,304 3,116 2,687 2,420 2,759 1,924 1,903 1,584 Ottawa 5,875 6,506 6,998 5,814 6,446 5,794 6,026 6,560 5,762 4,972 Kingston Peterborough Oshawa 2,995 2,389 1, ,888 1,859 1,803 1,384 1,671 2,587 Toronto 37,080 33,293 42,212 25,949 29,195 39,745 48,105 33,547 28,929 42,287 Hamilton 3,043 3,004 3,529 1,860 3,562 2,462 2,969 2,709 2,832 2,054 St. Catharines - Niagara 1,294 1,149 1, ,086 1,110 1,137 1,223 1,479 1,737 Kitchener-Cambridge-Waterloo 2,599 2,740 2,634 2,298 2,815 2,954 2,900 1,840 4,450 3,212 Brantford Guelph , , ,064 1,141 London 3,674 3,141 2,385 2,168 2,079 1,748 2,240 2,163 1,983 2,104 Windsor 1, ,010 Barrie 1, , ,148 1,016 Greater Sudbury/Grand Sudbury Thunder Bay Winnipeg 2,777 3,371 3,009 2,033 3,244 3,331 4,065 4,705 4,248 4,400 Regina 986 1,398 1, ,347 1,694 3,093 3,122 2,223 1,597 Saskatoon 1,496 2,380 2,319 1,428 2,381 2,994 3,753 2,980 3,531 2,293 Calgary 17,046 13,505 11,438 6,318 9,262 9,292 12,841 12,584 17,131 13,033 Edmonton 14,970 14,888 6,615 6,317 9,959 9,332 12,837 14,689 13,872 17,050 Kelowna 2,692 2,805 2, ,013 1,311 1,280 Abbotsford-Mission 1,207 1,088 1, Vancouver 18,705 20,736 19,591 8,339 15,217 17,867 19,027 18,696 19,212 20,863 Victoria 2,739 2,579 1,905 1,034 2,118 1,642 1,700 1,685 1,315 2,008 Source: CMHC (Starts and Completions Survey) For additional data, please refer to the CMHC website: 65