BEST PRACTICE PINZ. Valuation and Property Standards Board

|

|

|

- Catherine Blair

- 6 years ago

- Views:

Transcription

1 BEST PRACTICE PINZ Valuation and Property Standards Board

2 Introduction Standards as a very useful tool for supporting best practice A best practice paradigm Typically, for example, Guidance Notes say Guidance notes are intended to embody good practice and therefore may (although this should not be assumed) provide some professional support if properly applied. While they are not mandatory, it is likely that they will serve as a comparative measure of the level of performance of a member. They are an integral part of The Valuation and Property Standards Manual Standards are mandatory, and therefore need to be conformed with, but they too can be seen as embodying best practice. The valuation and property standards are Your guide to being a member of an industry leading professional, property institute

3 Agenda Overview of the new standards Conceptual view of standards Case studies Where are we going wrong? What is the Standards Board working on? Proposed IVSC Standards Summary / close 10 mins 5 mins 40 mins 10 mins 5 mins 5 mins 5 mins Handouts Standards flow chart Ton Remmerswaal s paper

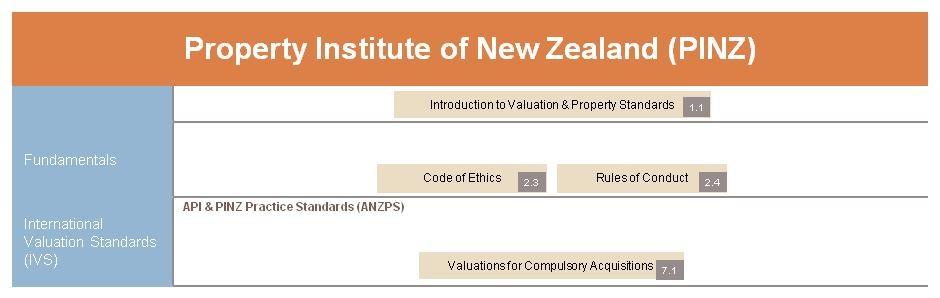

4 The new standards Effective date October 2009 Contain specific NZ content reflecting NZ only requirements Incorporate previous Standards, Applications and Guidance Notes Many of these have been extensively revised together with a number of new Guidance Notes both International and NZ / Australia specific

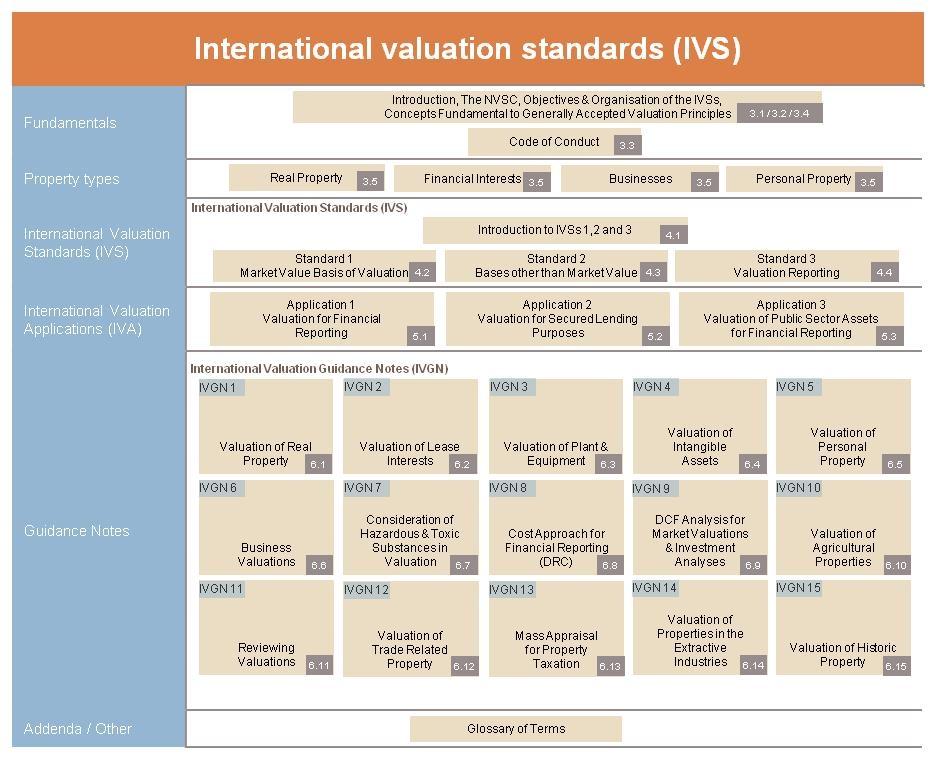

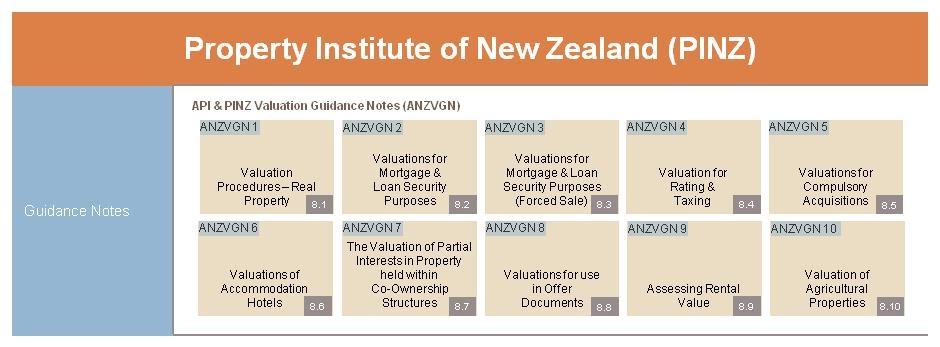

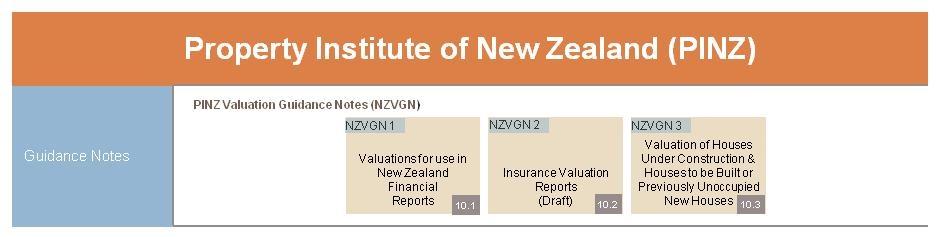

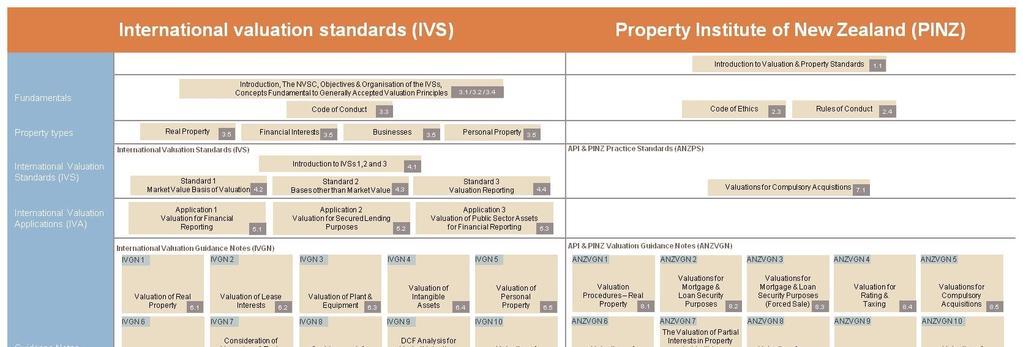

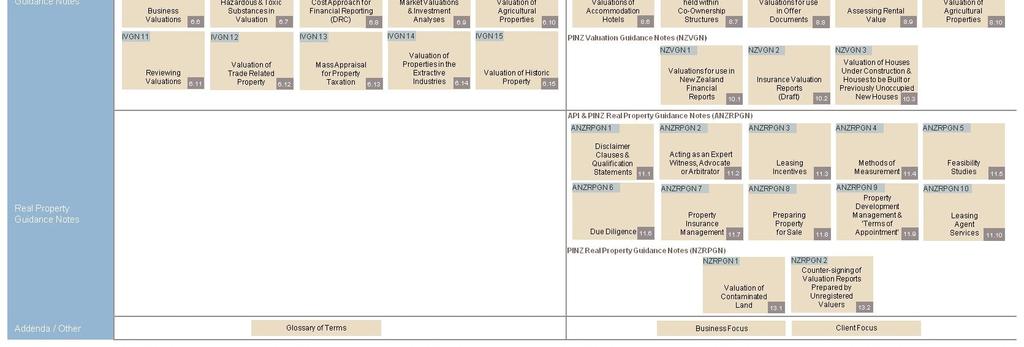

5 Structure of Standards Commence with Fundamentals Generally Accepted Valuation Principles (GAVP) Code of Conduct International & Local Property Types Real Property, Personal, Business and Financial Interests International Standards International Applications International Guidance Notes PINZ / API Standards PINZ / API Guidance Notes PINZ / API Business Focus

6 A conceptual view

7 Case Study 1 You are a Registered Valuer required to value a residential dwelling under construction for finance purposes. An unregistered valuer in your team is to work with you on the valuation. You will also be required to provide progress payment valuations during construction. Q1. What Standards, Applications & Guidance Notes apply? Q2. What are the potential risks when undertaking these types of valuations

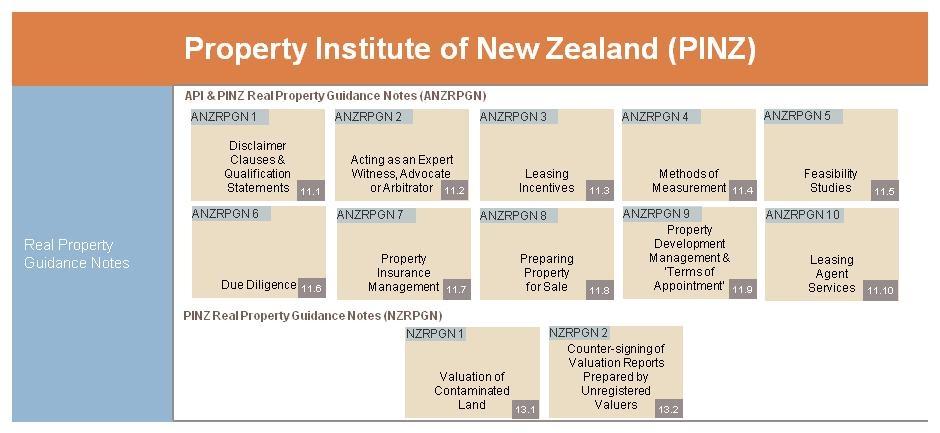

8 Case Study 1 - Answer IVS 1 Market Value Basis of Valuation IVS 3 Valuation Reporting IVA 2 Valuation for Secured Lending Purposes IVGN 1 Real Property Valuation ANZVGN 1 Valuation Procedures real property ANZVGN 2 Valuation for Mortgage and Loan Security Purposes NZVGN 3 Valuation of Houses under Construction and Houses to be Built or Previously Unoccupied New Houses ANZRPGN 1 Disclaimer and Qualification Statement ANZRPGN 4 Methods of measurement NZRPGN 2 Countersigning of Valuation Reports Prepared by Unregistered Valuers

9 Case Study 2 You have been asked to value a commercial office building, recently developed on an ex service station site. This is a multi tenant property and incentives are common in the market. The valuation is required for Financial Reporting Purposes. What standards, applications and guidance notes would you need to refer to and/or consider?

10 Case Study 2 - Answer IVS 1 Market Value Basis of Valuation IVS 3 Valuation Reporting IVA 1 Valuation for Financial Reporting IVGN 1 Real Property Valuation IVGN 7 Consideration of Hazardous and Toxic Substances in Valuation IVGN 9 DCF Analysis for Market Valuations and Investment Analysis NZVGN 1 Valuations for use in New Zealand Financial Reports ANZVGN 1 Valuation Procedures real property ANZRPGN 1 Disclaimer and Qualification Statement ANZRPGN 3 Leasing Incentives ANZRPGN 4 Methods of measurement ANZRPGN 9 Assessing rental value NZRPGN 1 Valuation of Contaminated Land

11 Case Study 3 Your client requires a valuation of a rural property which is to be included in an investment portfolio that will be publicly offered. What standards, applications and guidance notes would you need to refer to and/or consider?

12 Case Study 3 - answer IVS 1 Market Value Basis of Valuation IVS 3 Valuation Reporting IVGN 1 Real Property Valuation IVGN 10 Valuation of Agricultural Properties ANZVGN 1 Valuation Procedures real property ANZVGN 8 Valuations for use in Offer Documents ANZVGN 10 Valuation of Agricultural Properties ANZRPGN 1 Disclaimer and Qualification Statement ANZRPGN 1 Methods of Measurement

13 Case Study 4 You are instructed to value the freehold going concern of an accommodation hotel (in one line) with restaurant, bar and conference facilities, to assist the owner with establishing appropriate market price parameters. What Standards, Applications & Guidance Notes apply?

14 Case Study 4 - answer IVS 1 Market Value Basis of Valuation IVS 3 Valuation Reporting IVGN 1 Real Property Valuation IVGN 4 Valuation of intangible assets (of interest) IVGN 6 Business valuations IVGN 9 DCF for Market Valuations and Investment Analysis IVGN 12 Valuation of Trade Related Property ANZVGN 6 Valuation of Accommodation Hotels ANZVGN 1 Valuation Procedures real property ANZRPGN 1 Disclaimer and Qualification Statement IVGN 3 [possibly] Valuation of Plant and Equipment

15 How does the membership shape up? Ton Remmerswaal (NZIV Councillor Membership Advancements) reviews reports put forward in support of progression to ANZIV So these are reports from experienced valuers How do we shape up on compliance with standards?

16 How does the membership shape up? Some reports still refer to NZIV Practice Standards 1, 2 and 3 (superseded in 2004). Should refer to IVSs and IVAs which for most common reports require reference to: IVS3 (all reports) and IVA2 (all mortgage valuation reports).

17 How does the membership shape up? Common omissions in applicants reports in relation to IVS 3 and IVA 2 (See handout for detail): Identify the client, date of inspection versus date of valuation; State intended use of the valuation; Specify basis of valuation, and define market or rental value; Specify the basis of valuation (i.e. methodology; e.g. comparable sales or rentals, income capitalisation approach), as required by IVS 3 (5.1.3) Contain a mortgage recommendation; NZ 6.16 (contained within IVA 2) requires that the valuer make a mortgage recommendation. i.e. the maximum amount or percentage prudent to lend if the bank requests you not to provide this you must say so in the report or undertake a risk assessment

18 How does the membership shape up? Common omissions in relation to Guidance Notes, which embody best practice include: Details of instructing party and/or client, and who can rely on the report (ANZVGN 1) Disclosures in relation to progress reports (NZVGN 4) Where two or more valuers are involved in a valuation, specifying the involvement of each (ANZVGN 1) Disclosures in relation to compulsory acquisitions, covering instructions (in writing), requirement in interview the owner, zoning detail, effective date etc (ANZVGN 5) Disclosures in relation to forced sale valuations, including defining current forced sale value and marketing conditions, and appropriate statements (ANZVGN 3)

19 How does the membership shape up? FYI, the most common Guidance Notes are: ANZVGN 1 (Valuation procedures real property) as a guide to report content IVGN 1 (Real Property Valuation) as a guide to report format NZVGN 4 (Valuation of houses under construction) for valuations as if complete (Under review, to incorporate commercial property) ANZVGN 9 (Assessing Rental Value) ANZVGN 3 (Valuations for Mortgage and Loan Security Purposes Forced Sale) ANZVGN (5) (Valuations for Compulsory Acquisitions)

20 What is your Valuation Standards Board working on? Insurance Valuation Guidance Note NZVGN 3 - Valuation of Houses under Construction and Houses to be Built or Previously Unoccupied New Houses Review of all NZ Guidance Notes Consideration of standards relating to emerging issues associated with valuing water rights and carbon credits Consideration of IVSC Exposure Draft Proposed New International Valuation Standards released June 2010 The proposed IVSC Standards are a complete change from the current appearance, layout and structure Designed to give users of valuations sufficient understanding of recognised norms. They are not a training manual.

21 Proposed IVSC Standards Transparency of Process Defining the Hypothesis Promoting common terminology Significantly reduced in content Have eliminated repetition Eliminated methodology Eliminated Code of Ethics Reduced Glossary Reduced perscription

22 100 Series General Standards IVS 101 General Concepts & Principles IVS 102 Valuation Approaches IVS 103 Bases of Valuation IVS 104 Scope of Work IVS 105 Valuation Reporting

23 200 Series Application Standards Fair Value under IFRS Valuations for Depreciation Valuations for Lease Accounting Valuations for Impairment Testing Valuations for Property, Plant & Equipment in the Public Sector Valuations of Property Interests for Secured Lending

24 300 Series Asset Standards Valuations of Businesses Valuations of Intangible Assets Valuations of Plant & Equipment Valuations of Property Interests Valuations of Historic Property Valuations of Investment Property under Construction Valuations of Trade Related Property Valuations of Financial Instruments

25 Summary Standards are there for our benefit, to maintain minimum standards of our profession, and offer best practice guidance. Use them as a risk management tool, to guide you and meet minimum expectations / requirements. Think of standards not so much as a book of rules, but as supporting a best practice paradigm

TECHNICAL INFORMATION PAPER VALUATION OF SELF STORAGE FACILITIES

TECHNICAL INFORMATION PAPER VALUATION OF SELF STORAGE FACILITIES Reference ANZVTIP 5 Valuation of Self Storage Facilities Effective 23 November 2016 Owner National Manager Professional Standards Australian

TECHNICAL INFORMATION PAPER VALUATION OF SELF STORAGE FACILITIES Reference ANZVTIP 5 Valuation of Self Storage Facilities Effective 23 November 2016 Owner National Manager Professional Standards Australian

TECHNICAL INFORMATION PAPER VALUATION OF SELF STORAGE FACILITIES

TECHNICAL INFORMATION PAPER VALUATION OF SELF STORAGE FACILITIES Reference ANZVTIP 5 Valuation of Self Storage Facilities Effective 23 November 2016 Review Owner National Manager Professional Standards

TECHNICAL INFORMATION PAPER VALUATION OF SELF STORAGE FACILITIES Reference ANZVTIP 5 Valuation of Self Storage Facilities Effective 23 November 2016 Review Owner National Manager Professional Standards

ANZVGN 9 ASSESSING RENTAL VALUE

8.9 ANZ VALUATION GUIDANCE NOTE 9 ANZVGN 9 ASSESSING RENTAL VALUE 1.0 Introduction 1.1 Purpose The purpose of this Guidance Note is to provide information, commentary and advice to Members assessing rental

8.9 ANZ VALUATION GUIDANCE NOTE 9 ANZVGN 9 ASSESSING RENTAL VALUE 1.0 Introduction 1.1 Purpose The purpose of this Guidance Note is to provide information, commentary and advice to Members assessing rental

TECHNICAL INFORMATION PAPER - VALUATIONS OF REAL PROPERTY, PLANT & EQUIPMENT FOR USE IN AUSTRALIAN FINANCIAL REPORTS

TECHNICAL INFORMATION PAPER - VALUATIONS OF REAL PROPERTY, PLANT & EQUIPMENT FOR USE IN AUSTRALIAN FINANCIAL REPORTS Reference ANZVTIP 8 Valuations of Real Property, Plant & Equipment for Use in Australian

TECHNICAL INFORMATION PAPER - VALUATIONS OF REAL PROPERTY, PLANT & EQUIPMENT FOR USE IN AUSTRALIAN FINANCIAL REPORTS Reference ANZVTIP 8 Valuations of Real Property, Plant & Equipment for Use in Australian

International Valuation Standards 2017 Queenstown 29 June Presenter Chris Stanley

International Valuation Standards 2017 Queenstown 29 June 2017 Presenter Chris Stanley Why Have Standards? To ensure concepts such as Market Value & Fair Value are consistently applied Provides financial

International Valuation Standards 2017 Queenstown 29 June 2017 Presenter Chris Stanley Why Have Standards? To ensure concepts such as Market Value & Fair Value are consistently applied Provides financial

International Valuation Standards & International Financial Reporting Standards - An Update

International Valuation Standards & International Financial Reporting Standards - An Update Trevor R. Ellis, FAusIMM, CPG, CMA, CGA Mineral Property Valuator Ellis International Services, Inc. Denver,

International Valuation Standards & International Financial Reporting Standards - An Update Trevor R. Ellis, FAusIMM, CPG, CMA, CGA Mineral Property Valuator Ellis International Services, Inc. Denver,

On 1 February 2013 the IVSC announced the release of an Exposure Draft dealing with amendments to IVS 2011.

29 April 2013 IVSC Standards Board International Valuation Standards Council 41 Moorgate LONDON EC2R 6PP Dear Sirs, Exposure Draft Amendments to the International Valuation Standards On 1 February 2013

29 April 2013 IVSC Standards Board International Valuation Standards Council 41 Moorgate LONDON EC2R 6PP Dear Sirs, Exposure Draft Amendments to the International Valuation Standards On 1 February 2013

TECHNICAL INFORMATION PAPER - MARKET VALUE OF PROPERTY, PLANT & EQUIPMENT IN A BUSINESS

TECHNICAL INFORMATION PAPER - MARKET VALUE OF PROPERTY, PLANT & EQUIPMENT IN A BUSINESS Please view the video for this Technical Information Paper Reference ANZVTIP 2 Effective 1 st July 2015 Owner National

TECHNICAL INFORMATION PAPER - MARKET VALUE OF PROPERTY, PLANT & EQUIPMENT IN A BUSINESS Please view the video for this Technical Information Paper Reference ANZVTIP 2 Effective 1 st July 2015 Owner National

APES 225 Valuation Services

APES 225 Valuation Services [Supersedes APES 225 Valuation Services issued in July 2008 and revised in May 2012] Prepared and issued by Accounting Professional & Ethical Standards Board Limited REVISED:

APES 225 Valuation Services [Supersedes APES 225 Valuation Services issued in July 2008 and revised in May 2012] Prepared and issued by Accounting Professional & Ethical Standards Board Limited REVISED:

VALUATION REPORTING REVISED Introduction. 3.0 Definitions. 2.0 Scope INTERNATIONAL VALUATION STANDARDS 3

4.4 INTERNATIONAL VALUATION STANDARDS 3 REVISED 2007 1.0 Introduction 1.1 The critical importance of a Valuation Report, the final step in the valuation process, lies in communicating the value conclusion

4.4 INTERNATIONAL VALUATION STANDARDS 3 REVISED 2007 1.0 Introduction 1.1 The critical importance of a Valuation Report, the final step in the valuation process, lies in communicating the value conclusion

Requirements for International Standards in Valuation & Surveying

Requirements for International Standards in Valuation & Surveying Jonathan Harris CBE DLitt(Hon), FRICS, FInstCPD, CRE President of RICS 2000-2001 Member of REM Glossary of Terms for International Valuation

Requirements for International Standards in Valuation & Surveying Jonathan Harris CBE DLitt(Hon), FRICS, FInstCPD, CRE President of RICS 2000-2001 Member of REM Glossary of Terms for International Valuation

International Valuation Standards Update

International Valuation Standards Update Adam Smith Interim Technical Director of Business Valuation Standards OIV International Business Valuation Conference January 16, 2017 INTERNATIONAL VALUATION STANDARDS

International Valuation Standards Update Adam Smith Interim Technical Director of Business Valuation Standards OIV International Business Valuation Conference January 16, 2017 INTERNATIONAL VALUATION STANDARDS

Comment Letter 16 from the National Association of Romanian Valuers, ANEVAR

Comment Letter 16 from the National Association of Romanian Valuers, ANEVAR Comments on the Exposure Draft Proposed New International Valuation Standards, published June 2010 Email: CommentLetters@ivsc.org

Comment Letter 16 from the National Association of Romanian Valuers, ANEVAR Comments on the Exposure Draft Proposed New International Valuation Standards, published June 2010 Email: CommentLetters@ivsc.org

The actual universe of valuation standards

XLI Incontro di Studio del Ce.S.E.T.: 403-410 Ion Anghel Bucharest University of Economics E-mail: ion.anghel@ase.ro Key words: appraisal, valuation standard, globalization, professional services The actual

XLI Incontro di Studio del Ce.S.E.T.: 403-410 Ion Anghel Bucharest University of Economics E-mail: ion.anghel@ase.ro Key words: appraisal, valuation standard, globalization, professional services The actual

What are the accounting requirements for typical real estate lease, property, and investment property activities?

Course introduction This two-day course examines international financial reporting issues and their effect on real estate entities. Our specialist instructors discuss the critical issues that go beyond

Course introduction This two-day course examines international financial reporting issues and their effect on real estate entities. Our specialist instructors discuss the critical issues that go beyond

An International Perspective on U.S. Minerals Appraisal Standards Development

An International Perspective on U.S. Minerals Appraisal Standards Development Trevor R. Ellis, CPG, CMA, CGA, FAusIMM Mineral Property Appraiser Ellis International Services, Inc. Denver, Colorado www.minevaluation.com

An International Perspective on U.S. Minerals Appraisal Standards Development Trevor R. Ellis, CPG, CMA, CGA, FAusIMM Mineral Property Appraiser Ellis International Services, Inc. Denver, Colorado www.minevaluation.com

MARKET VALUE BASIS OF VALUATION

4.2 INTERNATIONAL VALUATION STANDARDS 1 MARKET VALUE BASIS OF VALUATION This Standard should be read in the context of the background material and implementation guidance contained in General Valuation

4.2 INTERNATIONAL VALUATION STANDARDS 1 MARKET VALUE BASIS OF VALUATION This Standard should be read in the context of the background material and implementation guidance contained in General Valuation

Going global. Trouble ahead. Ongoing major projects. Where next?

Where now for IFRS? Gavin Aspden FCA ICAEW Director, Qualifications Going global Trouble ahead Ongoing major projects Where next? 1 Going global Trouble ahead Ongoing major projects Where next? IFRS jurisdictions

Where now for IFRS? Gavin Aspden FCA ICAEW Director, Qualifications Going global Trouble ahead Ongoing major projects Where next? 1 Going global Trouble ahead Ongoing major projects Where next? IFRS jurisdictions

Minimum Educational Requirements

Minimum Educational Requirements (MER) For all persons elected to practice in each Member Association With effect from 1 January 2011 1 Introduction 1.1 The European Group of Valuers Associations (TEGoVA)

Minimum Educational Requirements (MER) For all persons elected to practice in each Member Association With effect from 1 January 2011 1 Introduction 1.1 The European Group of Valuers Associations (TEGoVA)

Securing Investments through Appropriate Financial Reporting Application of IVSC and IASB Standards

Securing Investments through Appropriate Financial Reporting Application of IVSC and IASB Standards Trevor R. Ellis, CPG, CMA, CGA, FAusIMM Leader, Extractive Industries Task Force International Valuation

Securing Investments through Appropriate Financial Reporting Application of IVSC and IASB Standards Trevor R. Ellis, CPG, CMA, CGA, FAusIMM Leader, Extractive Industries Task Force International Valuation

ANZVGN 7 THE VALUATION OF PARTIAL INTERESTS IN PROPERTY HELD WITHIN CO-OWNERSHIP STRUCTURES

8.7 ANZ VALUATION GUIDANCE NOTE 7 ANZVGN 7 THE VALUATION OF PARTIAL INTERESTS IN PROPERTY HELD WITHIN CO-OWNERSHIP STRUCTURES 1.0 Introduction 1.1 Purpose The purpose of this Guidance Note is to provide

8.7 ANZ VALUATION GUIDANCE NOTE 7 ANZVGN 7 THE VALUATION OF PARTIAL INTERESTS IN PROPERTY HELD WITHIN CO-OWNERSHIP STRUCTURES 1.0 Introduction 1.1 Purpose The purpose of this Guidance Note is to provide

The International Valuation and Financial Reporting Standards Their Content and Effect on Us Trevor R. Ellis, CPG, CMA, CGA, FAusIMM

The International Valuation and Financial Reporting Standards Their Content and Effect on Us Trevor R. Ellis, CPG, CMA, CGA, FAusIMM Chairman, Extractive Industries Task Force International Valuation Standards

The International Valuation and Financial Reporting Standards Their Content and Effect on Us Trevor R. Ellis, CPG, CMA, CGA, FAusIMM Chairman, Extractive Industries Task Force International Valuation Standards

International Financial Reporting Standards (IFRS)

") FACT SHEET February 2011 IAS 40 Investment Property (This fact sheet is based on the standard as at 1 January 2011.) Important note: This fact sheet is based on the requirements of the International Financial

FACT SHEET February 2011 IAS 40 Investment Property (This fact sheet is based on the standard as at 1 January 2011.) Important note: This fact sheet is based on the requirements of the International Financial

In December 2003 the Board issued a revised IAS 40 as part of its initial agenda of technical projects.

IAS 40 Investment Property In April 2001 the International Accounting Standards Board (the Board) adopted IAS 40 Investment Property, which had originally been issued by the International Accounting Standards

IAS 40 Investment Property In April 2001 the International Accounting Standards Board (the Board) adopted IAS 40 Investment Property, which had originally been issued by the International Accounting Standards

Public Works Act 1981 Overview on Acquisition and Compensation for Public Works. Workshop : N Pointon, A Roberts and J Haynes

Public Works Act 1981 Overview on Acquisition and Compensation for Public Works Workshop : N Pointon, A Roberts and J Haynes Presentation Content To consider the PINZ Professional Standards. To note the

Public Works Act 1981 Overview on Acquisition and Compensation for Public Works Workshop : N Pointon, A Roberts and J Haynes Presentation Content To consider the PINZ Professional Standards. To note the

EVS Wolfgang Kaelberer, Hon REV. Global Valuation Opportunities and Challenges: European Valuation Standards

Global Valuation Opportunities and Challenges: European Valuation Standards EVS 2016 Wolfgang Kaelberer, Hon REV Member of the Board of TEGoVA Member of the EVS Standards Board 1 Resolved to: remain clearly

Global Valuation Opportunities and Challenges: European Valuation Standards EVS 2016 Wolfgang Kaelberer, Hon REV Member of the Board of TEGoVA Member of the EVS Standards Board 1 Resolved to: remain clearly

I ROC 2017 Financial Administrators Section Conference

I ROC 2017 Financial Administrators Section Conference September 9, 2017 kpmg.ca Presenters Chris Cornell KPMG Partner, Financial Services Steven Sharma KPMG Partner, Financial Services 2 IIROC 2017 Financial

I ROC 2017 Financial Administrators Section Conference September 9, 2017 kpmg.ca Presenters Chris Cornell KPMG Partner, Financial Services Steven Sharma KPMG Partner, Financial Services 2 IIROC 2017 Financial

27 September Hans Hoogervorst IFRS Foundation 30 Cannon Street, London EC4M 6XH. Dear Hans IASB ED/2013/6: LEASES

27 September 2013 Hans Hoogervorst IFRS Foundation 30 Cannon Street, London EC4M 6XH Dear Hans IASB ED/2013/6: LEASES IMA represents the asset management industry operating in the UK. Our members include

27 September 2013 Hans Hoogervorst IFRS Foundation 30 Cannon Street, London EC4M 6XH Dear Hans IASB ED/2013/6: LEASES IMA represents the asset management industry operating in the UK. Our members include

In December 2003 the Board issued a revised IAS 40 as part of its initial agenda of technical projects.

IAS Standard 40 Investment Property In April 2001 the International Accounting Standards Board (the Board) adopted IAS 40 Investment Property, which had originally been issued by the International Accounting

IAS Standard 40 Investment Property In April 2001 the International Accounting Standards Board (the Board) adopted IAS 40 Investment Property, which had originally been issued by the International Accounting

In December 2003 the IASB issued a revised IAS 40 as part of its initial agenda of technical projects.

International Accounting Standard 40 Investment Property In April 2001 the International Accounting Standards Board (IASB) adopted IAS 40 Investment Property, which had originally been issued by the International

International Accounting Standard 40 Investment Property In April 2001 the International Accounting Standards Board (IASB) adopted IAS 40 Investment Property, which had originally been issued by the International

Mineral Property Valuation Standards A US Perspective

Mineral Property Valuation Standards A US Perspective Trevor R. Ellis, FAusIMM, CPG, CMA, CGA Mineral Property Valuer Ellis International Services, Inc. Denver, Colorado, USA www.minevaluation.com Leader

Mineral Property Valuation Standards A US Perspective Trevor R. Ellis, FAusIMM, CPG, CMA, CGA Mineral Property Valuer Ellis International Services, Inc. Denver, Colorado, USA www.minevaluation.com Leader

Standard for the acquisition of land under the Public Works Act 1981 LINZS15005

Standard for the acquisition of land under the Public Works Act 1981 LINZS15005 Version date: 20 February 2014 Table of contents Terms and definitions... 5 Foreword... 6 Introduction... 6 Purpose... 6

Standard for the acquisition of land under the Public Works Act 1981 LINZS15005 Version date: 20 February 2014 Table of contents Terms and definitions... 5 Foreword... 6 Introduction... 6 Purpose... 6

International Accounting Standard 40. Investment Property

International Accounting Standard 40 Investment Property Basis for Conclusions on IAS 40 Investment Property This Basis for Conclusions accompanies, but is not part of, IAS 40. Introduction BC1 BC2 BC3

International Accounting Standard 40 Investment Property Basis for Conclusions on IAS 40 Investment Property This Basis for Conclusions accompanies, but is not part of, IAS 40. Introduction BC1 BC2 BC3

Fair value implications for the real estate sector and example disclosures for real estate entities. Applying IFRS in Real Estate

Applying IFRS in Real Estate IFRS 13 Fair Value Measurement Fair value implications for the real estate sector and example disclosures for real estate entities January 2013 Contents Introduction... 2 Section

Applying IFRS in Real Estate IFRS 13 Fair Value Measurement Fair value implications for the real estate sector and example disclosures for real estate entities January 2013 Contents Introduction... 2 Section

EN Official Journal of the European Union L 320/373

29.11.2008 EN Official Journal of the European Union L 320/373 INTERNATIONAL FINANCIAL REPORTING STANDARD 3 Business combinations OBJECTIVE 1 The objective of this IFRS is to specify the financial reporting

29.11.2008 EN Official Journal of the European Union L 320/373 INTERNATIONAL FINANCIAL REPORTING STANDARD 3 Business combinations OBJECTIVE 1 The objective of this IFRS is to specify the financial reporting

Restoring the Past U.E.P.C. Building the Future

Brussels, 14.12.2010 Dear Sirs, Madam, Re: Exposure Draft Leases On behalf of the European Union of Developers and House Builders (Union Europeénne des Promoteurs-Constructeurs - UEPC), I am writing to

Brussels, 14.12.2010 Dear Sirs, Madam, Re: Exposure Draft Leases On behalf of the European Union of Developers and House Builders (Union Europeénne des Promoteurs-Constructeurs - UEPC), I am writing to

US Views on Valuation Methodology

US Views on Valuation Methodology Trevor R. Ellis, FAusIMM, CPG, CMA, CGA Mineral Property Valuer Ellis International Services, Inc. Denver, Colorado USA President American Institute of Minerals Appraisers

US Views on Valuation Methodology Trevor R. Ellis, FAusIMM, CPG, CMA, CGA Mineral Property Valuer Ellis International Services, Inc. Denver, Colorado USA President American Institute of Minerals Appraisers

CHAPTER 7 Property Companies. This chapter defines and sets out the Listing Rules for Property Companies.

CHAPTER 7 Property Companies This chapter defines and sets out the Listing Rules for Property Companies. General 7.1 Where an Applicant or an Issuer is a Property Company it shall comply with the Listing

CHAPTER 7 Property Companies This chapter defines and sets out the Listing Rules for Property Companies. General 7.1 Where an Applicant or an Issuer is a Property Company it shall comply with the Listing

Professional Valuation and Massey qualifications. An overview for Quantity Surveyors and Valuers

Professional Valuation and Massey qualifications An overview for Quantity Surveyors and Valuers Agenda 1. Massey University qualifications in Valuation and Property Management. 2. Massey University qualifications

Professional Valuation and Massey qualifications An overview for Quantity Surveyors and Valuers Agenda 1. Massey University qualifications in Valuation and Property Management. 2. Massey University qualifications

Headline Verdana Bold The evolutions of leases accounting under IFRS 16 Mariano Bruno, Carlo Laganà, Giuseppe Ambrosio, Deloitte & Touche S.p.A.

SHIPPING AND THE LAW 7^ Edition 25-26 October 2016 NAPLES Headline Verdana Bold The evolutions of leases accounting under IFRS 16 Mariano Bruno, Carlo Laganà, Giuseppe Ambrosio, Deloitte & Touche S.p.A.

SHIPPING AND THE LAW 7^ Edition 25-26 October 2016 NAPLES Headline Verdana Bold The evolutions of leases accounting under IFRS 16 Mariano Bruno, Carlo Laganà, Giuseppe Ambrosio, Deloitte & Touche S.p.A.

International Business Valuation Standards

Standards of Value: Theory and Applications, Second Edition By Jay E. Fishman, Shann on P. Pratt, William J. Morrison Copyright 2013 by John Wiley & Sons, Inc. Appendix A International Business Valuation

Standards of Value: Theory and Applications, Second Edition By Jay E. Fishman, Shann on P. Pratt, William J. Morrison Copyright 2013 by John Wiley & Sons, Inc. Appendix A International Business Valuation

Summary Letter PDS/IPO

20170418-MS16 CBRE Valuations Pty Limited ABN 15 008 912 641 Level 34 8 Exhibition Street Melbourne VIC 3000 T 61 3 8621 3333 F 61 3 8621 3330 25 October 2017 tom.burchell@cbre.com.au www.cbre.com.au Mr

20170418-MS16 CBRE Valuations Pty Limited ABN 15 008 912 641 Level 34 8 Exhibition Street Melbourne VIC 3000 T 61 3 8621 3333 F 61 3 8621 3330 25 October 2017 tom.burchell@cbre.com.au www.cbre.com.au Mr

PRINCIPLES OF VALUATION

PRINCIPLES OF VALUATION AMCHAM 20 th November 2018 Who am I and why am I giving this talk? Chartered Surveyor Real Estate degree 2 years working experience APC examination Qualified member of Royal Institution

PRINCIPLES OF VALUATION AMCHAM 20 th November 2018 Who am I and why am I giving this talk? Chartered Surveyor Real Estate degree 2 years working experience APC examination Qualified member of Royal Institution

IPSAS 17: GUIDANCE NOTE 3 OPENING BALANCES & FAIR VALUE MEASUREMENT of PPE FOR 1 ST TIME ADOPTERS of IPSAS

IPSAS 17: GUIDANCE NOTE 3 OPENING BALANCES & FAIR VALUE MEASUREMENT of PPE FOR 1 ST TIME ADOPTERS of IPSAS Executive Summary At its June 2007 meeting, the Task Force on Accounting Standards (Task Force)

IPSAS 17: GUIDANCE NOTE 3 OPENING BALANCES & FAIR VALUE MEASUREMENT of PPE FOR 1 ST TIME ADOPTERS of IPSAS Executive Summary At its June 2007 meeting, the Task Force on Accounting Standards (Task Force)

Valuation Update 2017

Valuation Update 2017 Valuing Sustainability & Valuing In Uncertain Times Since the BREXIT yes vote, the Trump USA presidency and problems in the Eurozone, property markets are more volatile. Nick French

Valuation Update 2017 Valuing Sustainability & Valuing In Uncertain Times Since the BREXIT yes vote, the Trump USA presidency and problems in the Eurozone, property markets are more volatile. Nick French

Repsol is very pleased to provide comments on the Exposure Draft Leases (ED2013/6), issued by the IASB on 16 May 2013.

, issued by the IASB on 16 May 2013.") Madrid, 13 September, 2013 International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Dear Sir/Madam, Re: Leases Repsol is very pleased to provide comments on the Exposure

Madrid, 13 September, 2013 International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Dear Sir/Madam, Re: Leases Repsol is very pleased to provide comments on the Exposure

TECHNICAL INFORMATION PAPER - VALUATION OF ACCOMMODATION HOTELS

TECHNICAL INFORMATION PAPER - VALUATION OF ACCOMMODATION HOTELS Reference ANZVTIP 7 Valuation of Accommodation Hotels Effective 30 November 2016 Owner National Manager Professional Standards Australian

TECHNICAL INFORMATION PAPER - VALUATION OF ACCOMMODATION HOTELS Reference ANZVTIP 7 Valuation of Accommodation Hotels Effective 30 November 2016 Owner National Manager Professional Standards Australian

BAHRAIN DOMICILED REAL ESTATE INVESTMENT TRUSTS (B-REITs) MODULE

MODULE") : BAHRAIN DOMICILED REAL ESTATE INVESTMENT TRUSTS (B-REITs) MODULE MODULE: BRT (Bahrain Domiciled Real Estate Investment Trusts) Table of Contents BRT-A BRT-B BRT-1 BRT-2 BRT-3 BRT-4 Date Last Changed

: BAHRAIN DOMICILED REAL ESTATE INVESTMENT TRUSTS (B-REITs) MODULE MODULE: BRT (Bahrain Domiciled Real Estate Investment Trusts) Table of Contents BRT-A BRT-B BRT-1 BRT-2 BRT-3 BRT-4 Date Last Changed

CENTRAL GOVERNMENT ACCOUNTING STANDARDS

CENTRAL GOVERNMENT ACCOUNTING STANDARDS NOVEMBER 2016 STANDARD 4 Requirements STANDARD 5 INTANGIBLE ASSETS INTRODUCTION... 75 I. CENTRAL GOVERNMENT S SPECIALISED ASSETS... 75 I.1. The collection of sovereign

CENTRAL GOVERNMENT ACCOUNTING STANDARDS NOVEMBER 2016 STANDARD 4 Requirements STANDARD 5 INTANGIBLE ASSETS INTRODUCTION... 75 I. CENTRAL GOVERNMENT S SPECIALISED ASSETS... 75 I.1. The collection of sovereign

INSTITUTION OF VALUERS

INSTITUTION OF VALUERS Plot No. 3, Parwana Road, Pitampura, New Delhi - 110 034 VALUATION OF REAL ESTATE SIX MONTHS COURSE GENERAL INFORMATION Name of the course : Six Month Course on Valuation of Real

INSTITUTION OF VALUERS Plot No. 3, Parwana Road, Pitampura, New Delhi - 110 034 VALUATION OF REAL ESTATE SIX MONTHS COURSE GENERAL INFORMATION Name of the course : Six Month Course on Valuation of Real

New Zealand Equivalent to International Accounting Standard 40 Investment Property (NZ IAS 40)

") New Zealand Equivalent to International Accounting Standard 40 Investment Property (NZ IAS 40) Issued November 2004 and incorporates amendments up to and inlcuding 28 February 2014 This Standard was issued

New Zealand Equivalent to International Accounting Standard 40 Investment Property (NZ IAS 40) Issued November 2004 and incorporates amendments up to and inlcuding 28 February 2014 This Standard was issued

Financial Accounting. Intangible Assets

Financial Accounting Intangible Assets Disclaimer The online video lectures and related study material (consisting of Powerpoint slides, summary modules, integrated question banks and other academic material)

Financial Accounting Intangible Assets Disclaimer The online video lectures and related study material (consisting of Powerpoint slides, summary modules, integrated question banks and other academic material)

International Accounting Standard 17. Leases

International Accounting Standard 17 Leases Basis for Conclusions on IAS 17 Leases This Basis for Conclusions accompanies, but is not part of, IAS 17. Introduction BC1 BC2 BC3 This Basis for Conclusions

International Accounting Standard 17 Leases Basis for Conclusions on IAS 17 Leases This Basis for Conclusions accompanies, but is not part of, IAS 17. Introduction BC1 BC2 BC3 This Basis for Conclusions

In December 2003 the IASB issued a revised IAS 17 as part of its initial agenda of technical projects.

IFRS Standard 16 Leases In April 2001 the International Accounting Standards Board (IASB) adopted IAS 17 Leases, which had originally been issued by the International Accounting Standards Committee (IASC)

IFRS Standard 16 Leases In April 2001 the International Accounting Standards Board (IASB) adopted IAS 17 Leases, which had originally been issued by the International Accounting Standards Committee (IASC)

New Zealand Equivalent to International Financial Reporting Standard 16 Leases (NZ IFRS 16)

") New Zealand Equivalent to International Financial Reporting Standard 16 Leases (NZ IFRS 16) Issued February 2016 This Standard was issued on 11 February 2016 by the New Zealand Accounting Standards Board

New Zealand Equivalent to International Financial Reporting Standard 16 Leases (NZ IFRS 16) Issued February 2016 This Standard was issued on 11 February 2016 by the New Zealand Accounting Standards Board

TERMS OF ENGAGEMENT Name of the firm. Previous involvement with the property or parties to the case:

The headings contained in this framework for terms of engagement are based directly upon the list of mandatory required content set out in VPS 1 para 3.1, page 39 and the commentary which follows on pages

The headings contained in this framework for terms of engagement are based directly upon the list of mandatory required content set out in VPS 1 para 3.1, page 39 and the commentary which follows on pages

Valuation Presentation for the Residents of the Central Hill Estate

Valuation Presentation for the Residents of the Central Hill Estate Introduction Jeremy Perceval FRICS RPR Founder and Managing Director of SFP Property Jeremy is a fellow of the Royal Institution of Chartered

Valuation Presentation for the Residents of the Central Hill Estate Introduction Jeremy Perceval FRICS RPR Founder and Managing Director of SFP Property Jeremy is a fellow of the Royal Institution of Chartered

How to Read a Real Estate Appraisal Report

How to Read a Real Estate Appraisal Report Much of the private, corporate and public wealth of the world consists of real estate. The magnitude of this fundamental resource creates a need for informed

How to Read a Real Estate Appraisal Report Much of the private, corporate and public wealth of the world consists of real estate. The magnitude of this fundamental resource creates a need for informed

The Influence of EU Regulation and European Valuation Standards on Real Estate Valuation

The Influence of EU Regulation and European Valuation Standards on Real Estate Valuation Thessaloniki 9 th October 2015 Krzysztof Grzesik REV Chairman TEGoVA The European Group of Valuers Associations

The Influence of EU Regulation and European Valuation Standards on Real Estate Valuation Thessaloniki 9 th October 2015 Krzysztof Grzesik REV Chairman TEGoVA The European Group of Valuers Associations

Depreciation A QUICK REFERENCE GUIDE FOR ELECTED OFFICIALS AND STAFF

Depreciation A QUICK REFERENCE GUIDE FOR ELECTED OFFICIALS AND STAFF This booklet is a quick reference guide to help you to: understand the purpose and function of accounting for and reporting on the depreciation

Depreciation A QUICK REFERENCE GUIDE FOR ELECTED OFFICIALS AND STAFF This booklet is a quick reference guide to help you to: understand the purpose and function of accounting for and reporting on the depreciation

The State of Valuers: South Pacific Perspective

The State of Valuers: South Pacific Perspective Matt Myers Sr. Lecturer Property & Valuation School of Property, Construction and Project Management Melbourne, Australia Valuation Issues particular to

The State of Valuers: South Pacific Perspective Matt Myers Sr. Lecturer Property & Valuation School of Property, Construction and Project Management Melbourne, Australia Valuation Issues particular to

ISBA Network News. March 2010

ISBA Network News March 2010 In This Issue ListServe Uncover Tax Advantages Of Running A Home Based Business EBIDA Pros & Cons Health Care Legislation Part 2: Partners In The World Of Valuation ISBA Connect

ISBA Network News March 2010 In This Issue ListServe Uncover Tax Advantages Of Running A Home Based Business EBIDA Pros & Cons Health Care Legislation Part 2: Partners In The World Of Valuation ISBA Connect

Exposure Draft (ED) 64 Summary Leases

64 Summary Leases") AT A GLANCE January 2018 Exposure Draft (ED) 64 Summary Leases This summary provides an overview of Exposure Draft 64, Leases. Project objective: Development of ED 64: This ED proposes new requirements

AT A GLANCE January 2018 Exposure Draft (ED) 64 Summary Leases This summary provides an overview of Exposure Draft 64, Leases. Project objective: Development of ED 64: This ED proposes new requirements

IFRS : Where do we stand? Planned changes 2012 and beyond

International Financial Reporting Standards IFRS : Where do we stand? Planned changes 2012 and beyond Philippe DANJOU Board Member Warsaw, December 6, 2012 The views expressed in this presentation are

International Financial Reporting Standards IFRS : Where do we stand? Planned changes 2012 and beyond Philippe DANJOU Board Member Warsaw, December 6, 2012 The views expressed in this presentation are

IAS 40 Investment Property

IAS 40 Investment Property Scope Applies in the: recognition, measurement and disclosure of investment property measurement in a lessee s financial statements of investment property interests held under

IAS 40 Investment Property Scope Applies in the: recognition, measurement and disclosure of investment property measurement in a lessee s financial statements of investment property interests held under

NETHERLANDS COUNCIL FOR REAL ESTATE ASSESSMENT

IVSC Standards Board 1 King Street LONDON EC2V8AU United Kingdom our ref. att. date 16.1971 BB 1 7 July 2016 About: Consultation IVS Dear mr. Sherman, With great pleasure we have read the exposure draft

IVSC Standards Board 1 King Street LONDON EC2V8AU United Kingdom our ref. att. date 16.1971 BB 1 7 July 2016 About: Consultation IVS Dear mr. Sherman, With great pleasure we have read the exposure draft

Anthony Banfield, FRICS Banfield Real Estate Solutions Ltd

Anthony Banfield, FRICS Banfield Real Estate Solutions Ltd } RICS Practice Statement GN13/2010 Contamination, the environment and sustainability What is it and why should we care? What does it cover? Implications

Anthony Banfield, FRICS Banfield Real Estate Solutions Ltd } RICS Practice Statement GN13/2010 Contamination, the environment and sustainability What is it and why should we care? What does it cover? Implications

The IASB s Exposure Draft on Leases

The Chair Date: 9 September 2013 ESMA/2013/1245 Francoise Flores EFRAG Square de Meeus 35 1000 Brussels Belgium The IASB s Exposure Draft on Leases Dear Ms Flores, The European Securities and Markets Authority

The Chair Date: 9 September 2013 ESMA/2013/1245 Francoise Flores EFRAG Square de Meeus 35 1000 Brussels Belgium The IASB s Exposure Draft on Leases Dear Ms Flores, The European Securities and Markets Authority

Rating Valuations Rules 2008

Rating Valuations Rules 2008 LINZS30300 Version date: 1 October 2010 www.linz.govt.nz Under section 5 of the Rating Valuations Act 1998 I hereby make the Rating Valuations Rules 2008. Unless otherwise

Rating Valuations Rules 2008 LINZS30300 Version date: 1 October 2010 www.linz.govt.nz Under section 5 of the Rating Valuations Act 1998 I hereby make the Rating Valuations Rules 2008. Unless otherwise

Exposure Draft 64 January 2018 Comments due: June 30, Proposed International Public Sector Accounting Standard. Leases

Exposure Draft 64 January 2018 Comments due: June 30, 2018 Proposed International Public Sector Accounting Standard Leases This document was developed and approved by the International Public Sector Accounting

Exposure Draft 64 January 2018 Comments due: June 30, 2018 Proposed International Public Sector Accounting Standard Leases This document was developed and approved by the International Public Sector Accounting

CONTACT(S) Raghava Tirumala +44 (0) Woung Hee Lee +44 (0)

Raghava Tirumala +44 (0) Woung Hee Lee +44 (0)") IASB Agenda ref 18A STAFF PAPER IASB Meeting Project Paper topic Goodwill and Impairment research project Summary of discussions to date CONTACT(S) Raghava Tirumala rtirumala@ifrs.org +44 (0)20 7246 6953

IASB Agenda ref 18A STAFF PAPER IASB Meeting Project Paper topic Goodwill and Impairment research project Summary of discussions to date CONTACT(S) Raghava Tirumala rtirumala@ifrs.org +44 (0)20 7246 6953

Fulfilment of the contract depends on the use of an identified asset; and

ANNEXE ANSWERS TO SPECIFIC QUESTIONS Question 1: identifying a lease This revised Exposure Draft defines a lease as a contract that conveys the right to use an asset (the underlying asset) for a period

ANNEXE ANSWERS TO SPECIFIC QUESTIONS Question 1: identifying a lease This revised Exposure Draft defines a lease as a contract that conveys the right to use an asset (the underlying asset) for a period

31 July 2014 Japan s Modified International Standards (JMIS): Accounting Standards Comprising IFRSs and the ASBJ Modifications

: Accounting Standards Comprising IFRSs and the ASBJ Modifications") 31 July 2014 Japan s Modified International Standards (JMIS): Accounting Standards Comprising IFRSs and the ASBJ Modifications ASBJ Modification Accounting Standard Exposure Draft No. 1 Accounting for

31 July 2014 Japan s Modified International Standards (JMIS): Accounting Standards Comprising IFRSs and the ASBJ Modifications ASBJ Modification Accounting Standard Exposure Draft No. 1 Accounting for

EN Official Journal of the European Union L 320/323

29.11.2008 EN Official Journal of the European Union L 320/323 INTERNATIONAL ACCOUNTING STANDARD 40 Investment property OBJECTIVE 1 The objective of this standard is to prescribe the accounting treatment

29.11.2008 EN Official Journal of the European Union L 320/323 INTERNATIONAL ACCOUNTING STANDARD 40 Investment property OBJECTIVE 1 The objective of this standard is to prescribe the accounting treatment

Residential Valuation Standing Instructions

Residential Valuation Standing Instructions These instructions are designed to outline requirements for Residential Valuation reports prepared for Mortgage Security purposes. Version 1.2 Released 1 November

Residential Valuation Standing Instructions These instructions are designed to outline requirements for Residential Valuation reports prepared for Mortgage Security purposes. Version 1.2 Released 1 November

Implementing GASB s Lease Guidance

The effective date of the Governmental Accounting Standards Board s (GASB) new lease guidance is drawing nearer. Private sector companies also have recently adopted significantly revised lease guidance;

The effective date of the Governmental Accounting Standards Board s (GASB) new lease guidance is drawing nearer. Private sector companies also have recently adopted significantly revised lease guidance;

Submission on Exposure Draft 64: Leases

30 June 2018 Mr John Stanford Technical Director International Public Sector Accounting Standards Board International Federation of Accountants 277 Wellington Street West Toronto Ontario M5V 3H2 CANADA

30 June 2018 Mr John Stanford Technical Director International Public Sector Accounting Standards Board International Federation of Accountants 277 Wellington Street West Toronto Ontario M5V 3H2 CANADA

EVALUATION OF THE REAL ESTATE PROPERTIES - NOVELTIES WITHIN THE COST APPROACH

EVALUATION OF THE REAL ESTATE PROPERTIES - NOVELTIES WITHIN THE COST APPROACH METHOD OF ASSETS Lect. Raluca Florentina Creţu Ph. D The Bucharest University of Economic Studies Faculty Accounting and Management

EVALUATION OF THE REAL ESTATE PROPERTIES - NOVELTIES WITHIN THE COST APPROACH METHOD OF ASSETS Lect. Raluca Florentina Creţu Ph. D The Bucharest University of Economic Studies Faculty Accounting and Management

FASB/IASB Update Part II

American Accounting Association FASB/IASB Update Part II Tom Linsmeier FASB Member August 3, 2014 The views expressed in this presentation are those of the presenters. Official positions of the FASB/IASB

American Accounting Association FASB/IASB Update Part II Tom Linsmeier FASB Member August 3, 2014 The views expressed in this presentation are those of the presenters. Official positions of the FASB/IASB

Board Meeting Handout ACCOUNTING FOR CONTINGENCIES September 6, 2007

PURPOSE Board Meeting Handout ACCOUNTING FOR CONTINGENCIES September 6, 2007 At today s meeting, the Board will discuss whether to add to its technical agenda a project considering whether to revise the

PURPOSE Board Meeting Handout ACCOUNTING FOR CONTINGENCIES September 6, 2007 At today s meeting, the Board will discuss whether to add to its technical agenda a project considering whether to revise the

.01 The objective of this Standard is to prescribe the accounting treatment for investment property and related disclosure requirements.

COMPARISON OF GRAP 16 WITH IAS 40 GRAP 16 IAS 40 DIFFERENCES Objective.01 The objective of this Standard is to prescribe the accounting treatment for investment property and related disclosure requirements.

COMPARISON OF GRAP 16 WITH IAS 40 GRAP 16 IAS 40 DIFFERENCES Objective.01 The objective of this Standard is to prescribe the accounting treatment for investment property and related disclosure requirements.

Introducing. Property. Valuation. Second edition. Michael Blackledge. Routledge R Taylor & Francis Croup LONDON AND NEW YORK

Introducing Property Valuation Second edition Michael Blackledge Routledge R Taylor & Francis Croup LONDON AND NEW YORK I Contents List of illustrations List ofcases Acknowledgements Disclaimers x xiii

Introducing Property Valuation Second edition Michael Blackledge Routledge R Taylor & Francis Croup LONDON AND NEW YORK I Contents List of illustrations List ofcases Acknowledgements Disclaimers x xiii

BUSI 352 Learning Objectives

BUSI 352 Learning Objectives Purpose and Scope of the Course The Case Studies in Residential Appraisal course (BUSI 352) explores the depth and breadth of knowledge around the valuation of residential

BUSI 352 Learning Objectives Purpose and Scope of the Course The Case Studies in Residential Appraisal course (BUSI 352) explores the depth and breadth of knowledge around the valuation of residential

New Zealand Equivalent to International Accounting Standard 40 Investment Property (NZ IAS 40)

") New Zealand Equivalent to International Accounting Standard 40 Investment Property (NZ IAS 40) Issued November 2004 and incorporates amendments up to and including 31 October 2010 This Standard was issued

New Zealand Equivalent to International Accounting Standard 40 Investment Property (NZ IAS 40) Issued November 2004 and incorporates amendments up to and including 31 October 2010 This Standard was issued

NAREIT/REALpac Impact of Revenue Recognition Proposal on Accounting for Real Estate Sales

RR Memo 130B ES April 28, 2010 BM May 5, 2010 NAREIT/REALpac Impact of Revenue Recognition Proposal on Accounting for Real Estate Sales Financial Accounting Standards Board April 28, 2010 Agenda 1. REESA

RR Memo 130B ES April 28, 2010 BM May 5, 2010 NAREIT/REALpac Impact of Revenue Recognition Proposal on Accounting for Real Estate Sales Financial Accounting Standards Board April 28, 2010 Agenda 1. REESA

Edison Electric Institute and American Gas Association New Lease Standard

Edison Electric Institute and American Gas Association New Lease Standard May 16, 2016 Disclaimer The information contained herein is of a general nature and is not intended to address the circumstances

Edison Electric Institute and American Gas Association New Lease Standard May 16, 2016 Disclaimer The information contained herein is of a general nature and is not intended to address the circumstances

Name, title, address of national authority

Name, title, address of national authority Dear TEGoVA Guidance to EU Member States and Candidate Member States on Development of Reliable Valuation Standards in Accordance with Art. 19 of Directive 2014/17/EU

Name, title, address of national authority Dear TEGoVA Guidance to EU Member States and Candidate Member States on Development of Reliable Valuation Standards in Accordance with Art. 19 of Directive 2014/17/EU

IASB Exposure Draft ED/2013/6 - Leases

ACAG AUSTRALASIAN COUNCIL OF AUDITORS GENERAL 13 September 2013 Mr Hans Hoogervorst Chairman International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Dear Mr Hoogervorst

ACAG AUSTRALASIAN COUNCIL OF AUDITORS GENERAL 13 September 2013 Mr Hans Hoogervorst Chairman International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Dear Mr Hoogervorst

Applying IFRS. Presentation and disclosure requirements of IFRS 16 Leases. November 2018

Applying IFRS Presentation and disclosure requirements of IFRS 16 Leases November 2018 Contents 1. Overview 2 2. What is changing from current IFRS? 4 2.1 Presentation 4 2.2 Lessee disclosures 5 3. Presentation

Applying IFRS Presentation and disclosure requirements of IFRS 16 Leases November 2018 Contents 1. Overview 2 2. What is changing from current IFRS? 4 2.1 Presentation 4 2.2 Lessee disclosures 5 3. Presentation

THE VALUATION OF LAND UNDER ROADS

A Coalface Discussion Paper Introduction We are aware of 5 different suggested methodologies for the valuation of land under roads 1, and in this paper we have sought to summarise each method, and to compare

A Coalface Discussion Paper Introduction We are aware of 5 different suggested methodologies for the valuation of land under roads 1, and in this paper we have sought to summarise each method, and to compare

RICS property measurement 2nd edition: Basis for conclusions. Purpose

RICS property measurement 2nd edition: Basis for conclusions Purpose This document has been prepared to accompany publication of the RICS property measurement 2nd edition in order to explain the rationale

RICS property measurement 2nd edition: Basis for conclusions Purpose This document has been prepared to accompany publication of the RICS property measurement 2nd edition in order to explain the rationale

These FAQs reflect current views and understanding of the IASB project.

FAQ 14 SEPTEMBER 2010 IASB PROJECT ON LEASE ACCOUNTING These FAQs reflect current views and understanding of the IASB project. In August 2010, the International Accounting Standards Board (IASB) and the

FAQ 14 SEPTEMBER 2010 IASB PROJECT ON LEASE ACCOUNTING These FAQs reflect current views and understanding of the IASB project. In August 2010, the International Accounting Standards Board (IASB) and the

Country-Specific Legislation and Practice. Greece

Country-Specific Legislation and Practice Country Chapter Greece Introduction One of the guiding principles of TEGoVA is to promote consistency of standard definitions of value and approaches to valuation

Country-Specific Legislation and Practice Country Chapter Greece Introduction One of the guiding principles of TEGoVA is to promote consistency of standard definitions of value and approaches to valuation

Agenda Item 11: Revenue and Non-Exchange Expenses

Agenda Item 11: Revenue and Non-Exchange Expenses David Bean, Anthony Heffernan, and Amy Shreck IPSASB Meeting June 21-24, 2016 Toronto, Canada Page 1 Proprietary and Copyrighted Information Agenda Item

Agenda Item 11: Revenue and Non-Exchange Expenses David Bean, Anthony Heffernan, and Amy Shreck IPSASB Meeting June 21-24, 2016 Toronto, Canada Page 1 Proprietary and Copyrighted Information Agenda Item

1. Introduction - 2 -

PRE-ACTION PROTOCOL FOR CLAIMS FOR DAMAGES IN RELATION TO THE PHYSICAL STATE OF COMMERCIAL PROPERTY AT THE TERMINATION OF A TENANCY (THE DILAPIDATIONS PROTOCOL) - 1 - PRE-ACTION PROTOCOL FOR CLAIMS FOR

PRE-ACTION PROTOCOL FOR CLAIMS FOR DAMAGES IN RELATION TO THE PHYSICAL STATE OF COMMERCIAL PROPERTY AT THE TERMINATION OF A TENANCY (THE DILAPIDATIONS PROTOCOL) - 1 - PRE-ACTION PROTOCOL FOR CLAIMS FOR

International Valuation Standards Board 15 Feb Moorgate London EC2R 6PP United Kingdom

International Valuation Standards Board 15 Feb 2013 41 Moorgate London EC2R 6PP United Kingdom Email: commentletters@ivsc.org The Finnish Association for Real Estate Valuation appreciates the opportunity

International Valuation Standards Board 15 Feb 2013 41 Moorgate London EC2R 6PP United Kingdom Email: commentletters@ivsc.org The Finnish Association for Real Estate Valuation appreciates the opportunity

THE APPRAISAL STANDARDS BOARD & USPAP

THE APPRAISAL STANDARDS BOARD & USPAP INFORMATION FOR APPRAISERS AND THEIR CLIENTS A PPRAISAL S TANDARDS B OARD A MESSAGE FROM THE ASB This brochure is intended to help appraisers and users of appraisal

THE APPRAISAL STANDARDS BOARD & USPAP INFORMATION FOR APPRAISERS AND THEIR CLIENTS A PPRAISAL S TANDARDS B OARD A MESSAGE FROM THE ASB This brochure is intended to help appraisers and users of appraisal

EXPLANATORY NOTES. ASSOCIATE MEMBERSHIP including with or without a Certification (excluding Plant & Machinery) Australian Property Institute

Australian Property Institute") Australian Property Institute ASSOCIATE MEMBERSHIP including with or without a Certification (excluding Plant & Machinery) EXPLANATORY NOTES Effective as at 1 August 2013 Australian Property Institute

Australian Property Institute ASSOCIATE MEMBERSHIP including with or without a Certification (excluding Plant & Machinery) EXPLANATORY NOTES Effective as at 1 August 2013 Australian Property Institute

International Conference A comprehensive approach to NPL resolution international experiences Collateral valuation an appraisers perspective

International Conference A comprehensive approach to NPL resolution international experiences Collateral valuation an appraisers perspective Krzysztof Grzesik FRICS REV Chairman TEGoVA Vienna 16 th May

International Conference A comprehensive approach to NPL resolution international experiences Collateral valuation an appraisers perspective Krzysztof Grzesik FRICS REV Chairman TEGoVA Vienna 16 th May

PURPOSE This paper is to update the Audit and Risk Committee on a number of accounting issues that will impact the finalisation of the Annual Report

6.3 ANNUAL REPORT 2018 Author: Authoriser: Lorraine Walmsley, Manager Finance Systems Kaiwhakahaere Pūnaha Pūtea Roy Baker, General Manager Corporate Services and Chief Financial Officer Kaiārahi Pūtea

6.3 ANNUAL REPORT 2018 Author: Authoriser: Lorraine Walmsley, Manager Finance Systems Kaiwhakahaere Pūnaha Pūtea Roy Baker, General Manager Corporate Services and Chief Financial Officer Kaiārahi Pūtea