Maximizing Credits in Year 1

|

|

|

- Virginia Freeman

- 6 years ago

- Views:

Transcription

1 Maximizing Credits in Year 1 George F. Littlejohn, CPA, HCCP Novogradac & Company LLP george.littlejohn@novoco.com

2 Let s go over Basic Concepts Multiple Building Election Minimum Set-Aside PIS Date (When can you claim credits)

3 Multiple Building Election Each building is considered a separate PROJECT under IRC 42(g)(3)(D) unless each building that is (or will be) part of the multiple-building project is identified by checking yes on Form 8609, line 8b.

4 Multiple Building Election You can combine or not combine any subset of buildings to create more than one project, based on PIS date, credit period, or what works best for your particular situation.

5 Minimum Set-Aside At least 20% of the available units are rented to households with incomes not exceeding 50% of (AMGI) adjusted for family size. At least 40% of the available units are rented to households with incomes not exceeding 60% of (AMGI) adjusted for family size.

6 Minimum Set-Aside The Minimum Set-Aside Test is determined on a Project Basis Single Building Project Multiple Building Project

7 Placed-in-Service Date Placed-in-Service Date When the building is ready and available for its intended use. Temporary Certificate of Occupancy Certificate of Occupancy. Architect s Certificate of Substantial Completion.

8 Placed-in-Service Date Acquisition / Rehab Acquisition different depending on whether the existing building is occupied at time of purchase. Rehabilitation date chosen by the Taxpayer when the minimum expenditure test is met.

9 How are Credits Delivered First year rule - 42(f)(2)(A) Credit are eligible for each full month that the building is in service. Unit must be occupied by tenant by the last day of the month.

10 Credit Delivery Strategy Managing Construction PIS Date Can create more available months. Managing Lease-up Tenants in units Can create more credits in each month.

11 Construction / Lease-up The End of the Year is CRITICAL! Manage your construction and leaseup. Not only do you need to meet your minimum set-aside, you have to lease ALL of your low-income units by 12/31 to avoid 15-year or 2/3 credits.

12 Acq/Rehab 120 Day Rule Household certified within 120 days of acquisition, the effective date is the acquisition date. Household certified more than 120 days after the acquisition, the household is treated as a new move-in.

13 Acquisition / Rehab Credit Period for Acquisition not to begin before credit period for Rehab ( 42(f)(5). Rev. Proc

14 Acquisition / Rehab Under 42(e)(4)(B) - The applicable fraction for Rehab is the applicable fraction for the underlying building.

15 LI Units for Acq/Rehab Existing tenants, under Rev. Proc New Move-ins Initial Income Certification. Transfers - income-qualified households that moved from other units within the project. ( Swap Status )

16 Acquisition / Rehab

17 Acq/Rehab Credit Strategy Understanding the Swap Status Rule Using the Multiple Building Election Move-ins vs. Transfers Vacant Unit Rule New Tenant Certification

18 Using Excess Eligible Basis Depends on State Agency and whether they adjust the credit percentage or eligible basis Line 2 and Line 3Aof the 8609

19 Using Excess Eligible Basis

20 Taxpayer 8609, Part II Taxpayer uses their actual eligible basis, NOT the amount from Part I

21 Taxpayer 8609-A Cannot create more credits per year than allocation, BUT can increase credits in first year.

22 Using Excess Eligible Basis Cannot create more credits per year than allocation, BUT can increase credits in first year.

23 Using Excess Eligible Basis Another Advantage May mitigate 15-year or 2/3rds Credit

24 Conclusion Communication Developer/Investor/Contractor/ Property Manager/Leasing Agent Strategy for Lease-Up Strategy for Construction / Rehab Plan your First Year Credit Delivery BEFORE the First Year

25 ?? QUESTIONS?? George F. Littlejohn, CPA, HCCP Novogradac & Company LLP (512)

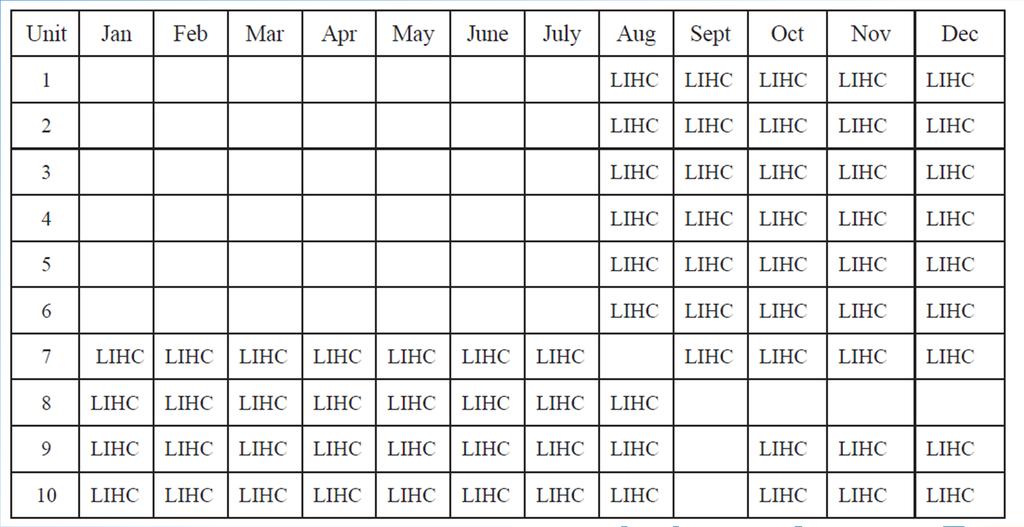

While a project is typically acquired on a specific date

A Presentation of the National Association of Home Builders While a project is typically acquired on a specific date Building rehab (if there are multiple buildings) is typically completed building by

A Presentation of the National Association of Home Builders While a project is typically acquired on a specific date Building rehab (if there are multiple buildings) is typically completed building by

Acq/Rehab Compliance. Jen Brewerton. Charles A. Rhuda III. Emily Bias. Stephanie Naquin. Matthew Rooney. Pillsbury Winthrop Shaw Pittman LLP

Acq/Rehab Compliance MODERATOR Charles A. Rhuda III Novogradac & Company LLP PANELISTS Emily Bias Pillsbury Winthrop Shaw Pittman LLP Stephanie Naquin Novogradac & Company LLP Jen Brewerton Dominium Matthew

Acq/Rehab Compliance MODERATOR Charles A. Rhuda III Novogradac & Company LLP PANELISTS Emily Bias Pillsbury Winthrop Shaw Pittman LLP Stephanie Naquin Novogradac & Company LLP Jen Brewerton Dominium Matthew

Chapter 11 Category 11g Gross Rent(s) Exceed Tax Credit Limits

Exceed Tax Credit Limits") Chapter 11 Category 11g Gross Rent(s) Exceed Tax Credit Limits Definition Determination on a Tax Year Basis This category is used to report noncompliance with the rent restrictions outlined in IRC 42(g)(2).

Chapter 11 Category 11g Gross Rent(s) Exceed Tax Credit Limits Definition Determination on a Tax Year Basis This category is used to report noncompliance with the rent restrictions outlined in IRC 42(g)(2).

HAWAII HOUSING FINANCE AND DEVELOPMENT CORPORATION. Low Income Housing Tax Credit Compliance Manual

HAWAII HOUSING FINANCE AND DEVELOPMENT CORPORATION Low Income Housing Tax Credit Compliance Manual Effective January, 2018 HAWAII COMPLIANCE MANUAL TABLE OF CONTENTS 1. Introduction to Manual 1-1. The

HAWAII HOUSING FINANCE AND DEVELOPMENT CORPORATION Low Income Housing Tax Credit Compliance Manual Effective January, 2018 HAWAII COMPLIANCE MANUAL TABLE OF CONTENTS 1. Introduction to Manual 1-1. The

Presented by: 2013 Zeffert & Associates All Rights Reserved

Presented by: & 2013 Zeffert & Associates All Rights Reserved The Goal of this Training The purpose of this training is to provide information for all interested personnel to successfully provide housing

Presented by: & 2013 Zeffert & Associates All Rights Reserved The Goal of this Training The purpose of this training is to provide information for all interested personnel to successfully provide housing

Louisiana Bankers Association CFO Conference. Baton Rouge Renaissance Hotel. Benny Jeansonne, CPA Partner Silas Simmons, LLP.

Louisiana Bankers Association CFO Conference May 21,2015 Baton Rouge Renaissance Hotel Benny Jeansonne, CPA Partner Silas Simmons, LLP Agenda Depreciation I. Current Law II. Cost Segregation III. Code

Louisiana Bankers Association CFO Conference May 21,2015 Baton Rouge Renaissance Hotel Benny Jeansonne, CPA Partner Silas Simmons, LLP Agenda Depreciation I. Current Law II. Cost Segregation III. Code

HISTORIC REHABILITATION

HISTORIC REHABILITATION TAX CREDIT The Tax Basics Herbert F. Stevens NIXON PEABODY LLP 401 9th Street, N.W. Washington, D.C. 20004-2128 Direct Dial: 202.585.8811 Fax: 202.585.8080 E-Mail Address: hstevens

HISTORIC REHABILITATION TAX CREDIT The Tax Basics Herbert F. Stevens NIXON PEABODY LLP 401 9th Street, N.W. Washington, D.C. 20004-2128 Direct Dial: 202.585.8811 Fax: 202.585.8080 E-Mail Address: hstevens

Treasury Regulations 1.42

Treasury Regulations 1.42 1.42-1 [Reserved] 1.42-1T Limitation on low-income housing credit allowed with respect to qualified lowincome buildings receiving housing credit allocations from a State or local

Treasury Regulations 1.42 1.42-1 [Reserved] 1.42-1T Limitation on low-income housing credit allowed with respect to qualified lowincome buildings receiving housing credit allocations from a State or local

Final Repair Regulations and the Impact on Owners of Investment Real Estate

Tom Scarpello Managing Partner 877.410.5040 Final Repair Regulations and the Impact on Owners of Investment Real Estate On September 13, 2013, the IRS released final regulations providing comprehensive

Tom Scarpello Managing Partner 877.410.5040 Final Repair Regulations and the Impact on Owners of Investment Real Estate On September 13, 2013, the IRS released final regulations providing comprehensive

(a)-(g) [Reserved]. For further guidance, see T(a) through (g).

![(a)-(g) [Reserved]. For further guidance, see T(a) through (g).](/thumbs/93/111110189.jpg "(a)-(g) [Reserved]. For further guidance, see T(a) through (g).") 1.42-1 Limitation on low-income housing credit allowed with respect to qualified lowincome buildings receiving housing credit allocations from a State or local housing credit agency. (a)-(g) [Reserved].

1.42-1 Limitation on low-income housing credit allowed with respect to qualified lowincome buildings receiving housing credit allocations from a State or local housing credit agency. (a)-(g) [Reserved].

Section 42 Glossary. Annual Report by Taxpayer to the State Agency: See Certification to State Agency.

Section 42 Glossary Accelerated Portion of the Credit: The excess of the aggregate allowable credit during the 10-year credit period under IRC 42 over the aggregate credit that would have been allowable

Section 42 Glossary Accelerated Portion of the Credit: The excess of the aggregate allowable credit during the 10-year credit period under IRC 42 over the aggregate credit that would have been allowable

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2014

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2014 Presented By: Karen Kent, CPA, Partner, Kevin P. Martin & Associates, P.C. Kenneth Lund,

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2014 Presented By: Karen Kent, CPA, Partner, Kevin P. Martin & Associates, P.C. Kenneth Lund,

Presented by: Anita Moseman

Verification of Information Presented by: Anita Moseman Verification Procedures Verification is a very important step 2 Verification Procedures Need to verify all information that determines income, assets,

Verification of Information Presented by: Anita Moseman Verification Procedures Verification is a very important step 2 Verification Procedures Need to verify all information that determines income, assets,

In the context of a Major Disaster, this revenue procedure provides temporary

CASE MIS No.: RP-141793-11 Administrative, Procedural, and Miscellaneous 26 CFR 601.105: Examination of returns and claims for refund, credit, or abatement; determination of correct tax liability. (Also:

CASE MIS No.: RP-141793-11 Administrative, Procedural, and Miscellaneous 26 CFR 601.105: Examination of returns and claims for refund, credit, or abatement; determination of correct tax liability. (Also:

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2016

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2016 Presented By: Karen Kent, CPA, Partner, Kevin P. Martin & Associates, P.C. Kenneth Lund,

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2016 Presented By: Karen Kent, CPA, Partner, Kevin P. Martin & Associates, P.C. Kenneth Lund,

Developer Non Managing Member- Historic Tax Credit Investor. Managing Member- Developer. Developer Fee Capital Contribution Tax Capital Contributions

Developer Managing Member- Developer Non Managing Member- Historic Tax Credit Investor Developer Fee Capital Contribution Tax Credits Capital Contributions Building Owner LLC/ Master Landlord Managing

Developer Managing Member- Developer Non Managing Member- Historic Tax Credit Investor Developer Fee Capital Contribution Tax Credits Capital Contributions Building Owner LLC/ Master Landlord Managing

INTRODUCTION TO FEDERAL LOW INCOME HOUSING TAX CREDITS. 1. Applicable Percentage

INTRODUCTION TO FEDERAL LOW INCOME HOUSING TAX CREDITS I. THE TAX CREDIT GENERALLY a. Established under the Tax Reform Act of 1986. Essentially an effort to partially privatize the affordable housing industry.

INTRODUCTION TO FEDERAL LOW INCOME HOUSING TAX CREDITS I. THE TAX CREDIT GENERALLY a. Established under the Tax Reform Act of 1986. Essentially an effort to partially privatize the affordable housing industry.

OVERVIEW OF HOUSING TAX CREDITS

OVERVIEW OF HOUSING TAX CREDITS Under the provisions of the Tax Reform Act of 1986, a federal Housing Tax Credit (HTC) was created to encourage the development of rental housing for limited income households.

OVERVIEW OF HOUSING TAX CREDITS Under the provisions of the Tax Reform Act of 1986, a federal Housing Tax Credit (HTC) was created to encourage the development of rental housing for limited income households.

Audit & Compliance Department Barbosa Ave. 606 Juan C. Cordero Dávila Bldg. Rio Piedras, PR Phone Fax

COMPLIANCE MONITORING PLAN LOW INCOME HOUSING TAX CREDIT PROGRAM Audit & Compliance Department Barbosa Ave. 606 Juan C. Cordero Dávila Bldg. Rio Piedras, PR 00919 Phone 787-765-7577 Fax 787-300-3171 JULY

COMPLIANCE MONITORING PLAN LOW INCOME HOUSING TAX CREDIT PROGRAM Audit & Compliance Department Barbosa Ave. 606 Juan C. Cordero Dávila Bldg. Rio Piedras, PR 00919 Phone 787-765-7577 Fax 787-300-3171 JULY

Historic Tax Credits: Leveraging History to Rebuild Legacy Cities. Jason Yots, Esq. ~ November 14, 2016

Historic Tax Credits: Leveraging History to Rebuild Legacy Cities Jason Yots, Esq. ~ November 14, 2016 Today s Discussion Why do legacy cities need tax credits? The historic tax credit program The Mattress

Historic Tax Credits: Leveraging History to Rebuild Legacy Cities Jason Yots, Esq. ~ November 14, 2016 Today s Discussion Why do legacy cities need tax credits? The historic tax credit program The Mattress

Novogradac LIHTC 101: The Basics Webinar Copyright 2016 Novogradac & Company LLP

Wayne Michael, CPA, NPCC, HCCP Director of Eternal Education Novogradac & Company LLP wayne.michael@novoco.com Tom Schneider, CPA Manager Novogradac & Company LLP tom.schneider@novoco.com 10-minute break

Wayne Michael, CPA, NPCC, HCCP Director of Eternal Education Novogradac & Company LLP wayne.michael@novoco.com Tom Schneider, CPA Manager Novogradac & Company LLP tom.schneider@novoco.com 10-minute break

DIFFERENCES BETWEEN THE HISTORIC REHABILITATION TAX CREDIT AND THE LOW-INCOME HOUSING TAX CREDIT

DIFFERENCES BETWEEN THE HISTORIC REHABILITATION TAX CREDIT AND THE LOW-INCOME HOUSING TAX CREDIT Andrew S. Potts NIXON PEABODY LLP 401 Ninth Street NW Washington, D.C. 20004 apotts@nixonpeabody.com. 202-585-8337

DIFFERENCES BETWEEN THE HISTORIC REHABILITATION TAX CREDIT AND THE LOW-INCOME HOUSING TAX CREDIT Andrew S. Potts NIXON PEABODY LLP 401 Ninth Street NW Washington, D.C. 20004 apotts@nixonpeabody.com. 202-585-8337

Using NSP to Preserve Affordability. March 22, 2011

Using NSP to Preserve Affordability March 22, 2011 1 Using NSP to Preserve Affordability March 22, 2011 10 a.m. Pacific/ 1 p.m. Eastern Presenters Ron Whitman, Pima County Community Land Trust Staci Horwitz,

Using NSP to Preserve Affordability March 22, 2011 1 Using NSP to Preserve Affordability March 22, 2011 10 a.m. Pacific/ 1 p.m. Eastern Presenters Ron Whitman, Pima County Community Land Trust Staci Horwitz,

THE LIKE KIND EXCHANGE: A CURRENT REVIEW TABLE OF CONTENTS I. OVERVIEW... 1

THE LIKE KIND EXCHANGE: A CURRENT REVIEW TABLE OF CONTENTS Page I. OVERVIEW... 1 II. BASICS OF LIKE KIND EXCHANGES... 1 A. General Rules... 1 B. Exchanges... 17 C. Designations of Replacement Property

THE LIKE KIND EXCHANGE: A CURRENT REVIEW TABLE OF CONTENTS Page I. OVERVIEW... 1 II. BASICS OF LIKE KIND EXCHANGES... 1 A. General Rules... 1 B. Exchanges... 17 C. Designations of Replacement Property

Adventures in Section 1031

NYSBA Real Estate Section Advanced Real Estate Topics Adventures in Section 1031 Lana Kalickstein Roberts & Holland LLP December 12, 2016 1 Acquisition of Property for $150 A (an individual) LLC 1 $100

NYSBA Real Estate Section Advanced Real Estate Topics Adventures in Section 1031 Lana Kalickstein Roberts & Holland LLP December 12, 2016 1 Acquisition of Property for $150 A (an individual) LLC 1 $100

Tax Reform Update: Proposed Regulations on Bonus Depreciation

Tax Reform Update: Proposed Regulations on Bonus Depreciation Thursday, September 27, 2018 2:00-3:00 pm ET We will be starting soon Please disable pop-up blocking software before viewing this webcast Speakers

Tax Reform Update: Proposed Regulations on Bonus Depreciation Thursday, September 27, 2018 2:00-3:00 pm ET We will be starting soon Please disable pop-up blocking software before viewing this webcast Speakers

The Legal and Financial Facets of Historic Tax Credits

California Preservation Foundation From Dollars & Cents to Success: Financial Incentive Programs for Historic Preservation February 10, 2016 The Legal and Financial Facets of Historic Tax Credits Roy Chou,

California Preservation Foundation From Dollars & Cents to Success: Financial Incentive Programs for Historic Preservation February 10, 2016 The Legal and Financial Facets of Historic Tax Credits Roy Chou,

CHAPTER Committee Substitute for Committee Substitute for House Bill No. 437

CHAPTER 2013-83 Committee Substitute for Committee Substitute for House Bill No. 437 An act relating to community development; amending s. 159.603, F.S.; revising the definition of qualifying housing development

CHAPTER 2013-83 Committee Substitute for Committee Substitute for House Bill No. 437 An act relating to community development; amending s. 159.603, F.S.; revising the definition of qualifying housing development

TABLE OF CONTENTS I. OVERVIEW... 1

TABLE OF CONTENTS I. OVERVIEW... 1 II. BASICS OF LIKE KIND EXCHANGES... 1 A. General Rules... 1 B. Exchanges... 21 C. Designations of Replacement Property -- Generally... 24 III. EXCHANGES WITH BOOT...

TABLE OF CONTENTS I. OVERVIEW... 1 II. BASICS OF LIKE KIND EXCHANGES... 1 A. General Rules... 1 B. Exchanges... 21 C. Designations of Replacement Property -- Generally... 24 III. EXCHANGES WITH BOOT...

Internal Revenue Code Section 25D Residential energy efficient property.

Internal Revenue Code Section 25D Residential energy efficient property. CLICK HERE to return to the home page Note: IRC Section 25D(a), following, is effective for periods before Jan. 1, 2017. For IRC

Internal Revenue Code Section 25D Residential energy efficient property. CLICK HERE to return to the home page Note: IRC Section 25D(a), following, is effective for periods before Jan. 1, 2017. For IRC

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2011

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2011 Presented By: Marianne Heard, CPA, MST, Tax Director, Kevin P. Martin & Associates, P.C.

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2011 Presented By: Marianne Heard, CPA, MST, Tax Director, Kevin P. Martin & Associates, P.C.

B-11-MN April 1, 2014 thru June 30, 2014 Performance Report. Community Development Systems Disaster Recovery Grant Reporting System (DRGR)

") Grantee: Grant: Southfield, MI B-11-MN-26-0011 April 1, 2014 thru June 30, 2014 Performance Report 1 Grant Number: B-11-MN-26-0011 Grantee Name: Southfield, MI Grant Award Amount: $1,084,254.00 LOCCS Authorized

Grantee: Grant: Southfield, MI B-11-MN-26-0011 April 1, 2014 thru June 30, 2014 Performance Report 1 Grant Number: B-11-MN-26-0011 Grantee Name: Southfield, MI Grant Award Amount: $1,084,254.00 LOCCS Authorized

DATE: TO OWNER: Washington State Housing Finance Commission Low-Income Housing Tax Credit Program 1000 Second Avenue Suite 2700 Seattle WA

INDEPENDENT CERTIFIED PUBLIC ACCOUNTANT'S REPORT on CARRYOVER ALLOCATION BASIS PURSUANT TO IRS SECTION 42 (h)(1)(e)(ii) and AMERICAN RECOVERY AND REINVESTMENT ACT (ARRA) EXCHANGE PROGRAM 30% TEST PURSUANT

INDEPENDENT CERTIFIED PUBLIC ACCOUNTANT'S REPORT on CARRYOVER ALLOCATION BASIS PURSUANT TO IRS SECTION 42 (h)(1)(e)(ii) and AMERICAN RECOVERY AND REINVESTMENT ACT (ARRA) EXCHANGE PROGRAM 30% TEST PURSUANT

Capital Cost Recovery Changes

College of William & Mary Law School William & Mary Law School Scholarship Repository William & Mary Annual Tax Conference Conferences, Events, and Lectures 1986 Capital Cost Recovery Changes B. Cary Tolley

College of William & Mary Law School William & Mary Law School Scholarship Repository William & Mary Annual Tax Conference Conferences, Events, and Lectures 1986 Capital Cost Recovery Changes B. Cary Tolley

Tax Credit Management Abilities

Web-Based, ASP Hosted, Enterprise Class Property Management Software Tax Credit Management Abilities Dear Property Manager, Property management software is becoming more and more complicated and loaded

Web-Based, ASP Hosted, Enterprise Class Property Management Software Tax Credit Management Abilities Dear Property Manager, Property management software is becoming more and more complicated and loaded

NSP Closeout for Grantees

U.S. Department of Housing and Urban Development Community Planning and Development NSP Problem Solving Clinic 2013 NSP Closeout for Grantees When can grantees close out? To close out, grantees must: Draw

U.S. Department of Housing and Urban Development Community Planning and Development NSP Problem Solving Clinic 2013 NSP Closeout for Grantees When can grantees close out? To close out, grantees must: Draw

CHAPTER 1 LIHTC PROPERTY MANAGEMENT

Contents CHAPTER 1 LIHTC PROPERTY MANAGEMENT 19 1.01 Overview 19 1.02 Importance of a Good Property Manager 20 1.03 Minimum Set-Asides 20 1.04 Documentation 23 1.05 Proper Tenant File Retention Techniques

Contents CHAPTER 1 LIHTC PROPERTY MANAGEMENT 19 1.01 Overview 19 1.02 Importance of a Good Property Manager 20 1.03 Minimum Set-Asides 20 1.04 Documentation 23 1.05 Proper Tenant File Retention Techniques

Section 14. Changes in Median Gross Income

Section 14 Changes in Median Gross Income REVENUE RULE 94-57 1994-2 C.B. 5, 1994-37 I.R.B. 4. Internal Revenue Service Revenue Ruling LOW-INCOME HOUSING CREDIT; CHANGES IN AREA MEDIAN GROSS INCOME; TENANT

Section 14 Changes in Median Gross Income REVENUE RULE 94-57 1994-2 C.B. 5, 1994-37 I.R.B. 4. Internal Revenue Service Revenue Ruling LOW-INCOME HOUSING CREDIT; CHANGES IN AREA MEDIAN GROSS INCOME; TENANT

Management of Low-Income Housing Tax Credit Projects - Intermediate Requirements:

Management of Low-Income Housing Tax Credit Projects - Basic Requirements: This training is designed primarily for new site manager and supervisory property managers, and is especially beneficial to those

Management of Low-Income Housing Tax Credit Projects - Basic Requirements: This training is designed primarily for new site manager and supervisory property managers, and is especially beneficial to those

Valuation Issues. Lindsey Sutton Novogradac & Company LLP. Brad Weinberg Novogradac & Company LLP

Valuation Issues PANELISTS Lindsey Sutton Novogradac & Company LLP Brad Weinberg Novogradac & Company LLP Visit www.crowdmics.online/novocolihtc to send questions to the moderator Valuation Issues How

Valuation Issues PANELISTS Lindsey Sutton Novogradac & Company LLP Brad Weinberg Novogradac & Company LLP Visit www.crowdmics.online/novocolihtc to send questions to the moderator Valuation Issues How

Town of Watertown. Affordable Housing Development Requirements: Complying with Section 5.07

Town of Watertown Affordable Housing Development Requirements: Complying with Section 5.07 Be Informed If you are considering the development of a project that will trigger the Town s Inclusionary Zoning

Town of Watertown Affordable Housing Development Requirements: Complying with Section 5.07 Be Informed If you are considering the development of a project that will trigger the Town s Inclusionary Zoning

Rental Process. Proportionate Lease-Up Requirement New Construction Properties. Counting Vacant Units to Meet Set-Aside Requirements

z Rental Process Rental Process & Reporting Procedures Residents of set-aside units must be income-qualified at move-in, and the income verifications must be dated prior to and within 120 days of the date

z Rental Process Rental Process & Reporting Procedures Residents of set-aside units must be income-qualified at move-in, and the income verifications must be dated prior to and within 120 days of the date

Opening Doors to Affordable Mixed-Use Development

Opening Doors to Affordable Mixed-Use Development 1 Housing Colorado October 5, 2016 2 Session Objectives Learn: The Basics of Low-Income and Historic Tax Credits, including recent Colorado LIHTC program

Opening Doors to Affordable Mixed-Use Development 1 Housing Colorado October 5, 2016 2 Session Objectives Learn: The Basics of Low-Income and Historic Tax Credits, including recent Colorado LIHTC program

Federal Requirements. Summary To qualify for tax credits, a property must meet either the 20/50 or

Federal Requirements Summary To qualify for tax credits, a property must meet either the 20/50 or 40/60 test (see Chapter 1, Introduction, for explanation of the 20/50-40/60 test). All affordable unit

Federal Requirements Summary To qualify for tax credits, a property must meet either the 20/50 or 40/60 test (see Chapter 1, Introduction, for explanation of the 20/50-40/60 test). All affordable unit

Chapter 8 Category 11e Changes in Eligible Basis

Chapter 8 Category 11e Changes in Eligible Basis Definition This category is used to report violations associated with the Eligible Basis of a building or any occurrence that result in a decrease in the

Chapter 8 Category 11e Changes in Eligible Basis Definition This category is used to report violations associated with the Eligible Basis of a building or any occurrence that result in a decrease in the

Important Notice Exhibit A Owner s Certificate of Continuing Program Compliance Line by Line Instructions

Important Notice Exhibit A Owner s Certificate of Continuing Program Compliance Line by Line Instructions The Missouri Housing Development Commission (MHDC) is offering line by line instruction for Exhibit

Important Notice Exhibit A Owner s Certificate of Continuing Program Compliance Line by Line Instructions The Missouri Housing Development Commission (MHDC) is offering line by line instruction for Exhibit

2017 SECTION 42 HOUSING TAX CREDIT PROGRAM COMPLIANCE MANUAL for

MINNEAPOLIS COMMUNITY PLANNING ECONOMIC DEVELOPMENT AGENCY 2017 SECTION 42 HOUSING TAX CREDIT PROGRAM COMPLIANCE MANUAL for MINNEAPOLIS - SAINT PAUL HOUSING FINANCE BOARD Minneapolis CPED Contact: Mr.

MINNEAPOLIS COMMUNITY PLANNING ECONOMIC DEVELOPMENT AGENCY 2017 SECTION 42 HOUSING TAX CREDIT PROGRAM COMPLIANCE MANUAL for MINNEAPOLIS - SAINT PAUL HOUSING FINANCE BOARD Minneapolis CPED Contact: Mr.

Managing a Section 8, Section 236, PRAC/LIHTC Project

Managing a Section 8, Section 236, PRAC/LIHTC Project www.lizbramletconsulting.com www.lbctrainingcenter.com www.lizbramlet.wordpress.com HUD-Assisted Projects and LIHTC Across the country, owners are

Managing a Section 8, Section 236, PRAC/LIHTC Project www.lizbramletconsulting.com www.lbctrainingcenter.com www.lizbramlet.wordpress.com HUD-Assisted Projects and LIHTC Across the country, owners are

2012 Low Income Housing Tax Credit Qualified Allocation Plan And On-Line Application Mandatory Developer Training Guide

2012 Low Income Housing Tax Credit Qualified Allocation Plan And On-Line Application Mandatory Developer Training Guide December 12, 2011 December 14, 2011 December 14, 2011 December 15, 2011 1:00 p.m.

2012 Low Income Housing Tax Credit Qualified Allocation Plan And On-Line Application Mandatory Developer Training Guide December 12, 2011 December 14, 2011 December 14, 2011 December 15, 2011 1:00 p.m.

Reinvesting With 1031 Exchange

Reinvesting With 1031 Exchange SEMINAR OUTLINE: Introduction and Learning Objectives... 2 1031 Exchange Rules: Myth or Fact?... 2 Non-Qualifying Replacement Property... 3 Exchanges with Special Challenges...

Reinvesting With 1031 Exchange SEMINAR OUTLINE: Introduction and Learning Objectives... 2 1031 Exchange Rules: Myth or Fact?... 2 Non-Qualifying Replacement Property... 3 Exchanges with Special Challenges...

Q&A September 23, 2011, 9 a.m. NSP III Multi Family Workshop City of Miami, City Hall, Commission Chambers

Q&A September 23, 2011, 9 a.m. NSP III Multi Family Workshop City of Miami, City Hall, Commission Chambers Question 1: Is this NSP for a property that is in foreclosure currently or a property that had

Q&A September 23, 2011, 9 a.m. NSP III Multi Family Workshop City of Miami, City Hall, Commission Chambers Question 1: Is this NSP for a property that is in foreclosure currently or a property that had

Overview. Five Eligible NSP Uses. Meeting the 25% Set-Aside for Low-Income Persons

U.S. Department of Housing and Urban Development Meeting the 25% Set-Aside for Low-Income Persons Neighborhood Stabilization Program Neighborhood Stabilization Program Eligible uses Program activities

U.S. Department of Housing and Urban Development Meeting the 25% Set-Aside for Low-Income Persons Neighborhood Stabilization Program Neighborhood Stabilization Program Eligible uses Program activities

This document is available via in a Microsoft Word format upon request. LOW INCOME HOUSING TAX CREDIT PROGRAM APPLICATION

This document is available via e-mail in a Microsoft Word format upon request. Development Name: LOW INCOME HOUSING TAX CREDIT PROGRAM APPLICATION DELAWARE STATE HOUSING AUTHORITY STATE OF DELAWARE Part

This document is available via e-mail in a Microsoft Word format upon request. Development Name: LOW INCOME HOUSING TAX CREDIT PROGRAM APPLICATION DELAWARE STATE HOUSING AUTHORITY STATE OF DELAWARE Part

WYOMING COMMUNITY DEVELOPMENT AUTHORITY. Affordable Rental Housing Compliance Manual For Tax Credit, Bond and HOME Projects

WYOMING COMMUNITY DEVELOPMENT AUTHORITY Affordable Rental Housing Compliance Manual For Tax Credit, Bond and HOME Projects Effective January 1, 2013 TABLE OF CONTENTS 1. Introduction A. The Purpose of

WYOMING COMMUNITY DEVELOPMENT AUTHORITY Affordable Rental Housing Compliance Manual For Tax Credit, Bond and HOME Projects Effective January 1, 2013 TABLE OF CONTENTS 1. Introduction A. The Purpose of

Contents TABLE OF CONTENTS

Contents CHAPTER 1 Low-Income Housing Tax Credits and Year 15 17 1.01 Introduction 17 1.02 Overview of the LIHTC Program 18 [1] Land Use Restriction Agreement (LURA) 20 [2] Extended-Use Period 21 1.03

Contents CHAPTER 1 Low-Income Housing Tax Credits and Year 15 17 1.01 Introduction 17 1.02 Overview of the LIHTC Program 18 [1] Land Use Restriction Agreement (LURA) 20 [2] Extended-Use Period 21 1.03

Managing Compliance. Presented by Grace Robertson Internal Revenue Service November 17, 2009

Managing Compliance Presented by Grace Robertson Internal Revenue Service November 17, 2009 Introduction Objectives Guide for Completing Form 8823: Summary of Revisions Prioritize for Day-to-Day Operations

Managing Compliance Presented by Grace Robertson Internal Revenue Service November 17, 2009 Introduction Objectives Guide for Completing Form 8823: Summary of Revisions Prioritize for Day-to-Day Operations

Washington State Housing Finance Commission LIHTC Owner s Annual Certification. Federal Requirements

Washington State Housing Finance Commission LIHTC Owner s Annual Certification The Owner hereby certifies that: Federal Requirements 1. The project met the requirements of: the 20-50 test under section

Washington State Housing Finance Commission LIHTC Owner s Annual Certification The Owner hereby certifies that: Federal Requirements 1. The project met the requirements of: the 20-50 test under section

Historic Tax Credit Presentation Date: March 22, 2016

Historic Tax Credit Presentation Date: March 22, 2016 Today s Presenter(s): Lynn Wickham Hartman (319) 896-4083 lhartman@simmonsperrine.com Matthew J. Hektoen (319) 896-4030 mhektoen@simmonsperrine.com

Historic Tax Credit Presentation Date: March 22, 2016 Today s Presenter(s): Lynn Wickham Hartman (319) 896-4083 lhartman@simmonsperrine.com Matthew J. Hektoen (319) 896-4030 mhektoen@simmonsperrine.com

January 1, 2016 thru March 31, 2016 Performance Report

Grantee: Grant: Clark County, NV B-08-UN-32-0001 January 1, 2016 thru March 31, 2016 Performance Report 1 Grant Number: B-08-UN-32-0001 Grantee Name: Clark County, NV Grant Award Amount: $29,666,798.00

Grantee: Grant: Clark County, NV B-08-UN-32-0001 January 1, 2016 thru March 31, 2016 Performance Report 1 Grant Number: B-08-UN-32-0001 Grantee Name: Clark County, NV Grant Award Amount: $29,666,798.00

Differences, Procurement and

U.S. Department of Housing and Urban Development Developers and Subrecipients: Differences, Procurement and Other Rules July 24, 2012 2:00 PM EDT Community Planning and Development Purpose of Webinar To

U.S. Department of Housing and Urban Development Developers and Subrecipients: Differences, Procurement and Other Rules July 24, 2012 2:00 PM EDT Community Planning and Development Purpose of Webinar To

R E N O & C A V A N A U G H PLLC

Transactional Pitfalls and Challenges in Affordable Housing Development Outline Megan Glasheen, Julie McGovern & Dwayne Barrett Reno & Cavanaugh, PLLC Presentation will focus on the most active development

Transactional Pitfalls and Challenges in Affordable Housing Development Outline Megan Glasheen, Julie McGovern & Dwayne Barrett Reno & Cavanaugh, PLLC Presentation will focus on the most active development

HISTORIC TAX CREDIT IMPROVEMENT ACT OF 2017 (H.R. 425, S. 1158) SECTION-BY-SECTION SUMMARY

SECTION-BY-SECTION SUMMARY") SEC. 6 MODIFICATIONS REGARDING CERTAIN TAX-EXEMPT USE PROPERTY. This provision would modify the disqualified lease rules to limit the definition of a disqualified lease to those leases that are part of

SEC. 6 MODIFICATIONS REGARDING CERTAIN TAX-EXEMPT USE PROPERTY. This provision would modify the disqualified lease rules to limit the definition of a disqualified lease to those leases that are part of

Neighborhood Stabilization Program

Neighborhood Stabilization Program Neighborhood Stabilization Program What is the Neighborhood Stabilization Program? NSP was funded in 3 rounds to provide assistance to state and local governments to

Neighborhood Stabilization Program Neighborhood Stabilization Program What is the Neighborhood Stabilization Program? NSP was funded in 3 rounds to provide assistance to state and local governments to

EXHIBIT E LOW INCOME HOUSING TAX CREDIT APPLICATION REQUIREMENTS

EXHIBIT E LOW INCOME HOUSING TAX CREDIT APPLICATION REQUIREMENTS A. Application for Tax Credit Reservation or Tax-Exempt Bond Conditional Commitment shall Include: 1. Complete application form (current

EXHIBIT E LOW INCOME HOUSING TAX CREDIT APPLICATION REQUIREMENTS A. Application for Tax Credit Reservation or Tax-Exempt Bond Conditional Commitment shall Include: 1. Complete application form (current

Housing Tax Credit Carryover, 10 Percent Test, Evidence of Construction Start and Final Allocation Application Training Workshop. September 20, 2018

Housing Tax Credit Carryover, 10 Percent Test, Evidence of Construction Start and Final Allocation Application Training Workshop September 20, 2018 Table of Contents Topic Page Carryover Allocation Application

Housing Tax Credit Carryover, 10 Percent Test, Evidence of Construction Start and Final Allocation Application Training Workshop September 20, 2018 Table of Contents Topic Page Carryover Allocation Application

January 1, 2015 thru March 31, 2015 Performance Report

Grantee: Grant: West Palm Beach, FL B-08-MN-12-0030 January 1, 2015 thru March 31, 2015 Performance Report 1 Grant Number: B-08-MN-12-0030 Grantee Name: West Palm Beach, FL Grant Award Amount: $4,349,546.00

Grantee: Grant: West Palm Beach, FL B-08-MN-12-0030 January 1, 2015 thru March 31, 2015 Performance Report 1 Grant Number: B-08-MN-12-0030 Grantee Name: West Palm Beach, FL Grant Award Amount: $4,349,546.00

Maximizing Economic Development and Job Creation with the 2011 Universal Cycle

Maximizing Economic Development and Job Creation with the 2011 Universal Cycle In preparing our response to the Draft White Paper posted on the FHFC website regarding Jobs Created by New Construction and

Maximizing Economic Development and Job Creation with the 2011 Universal Cycle In preparing our response to the Draft White Paper posted on the FHFC website regarding Jobs Created by New Construction and

July 1, 2015 thru September 30, 2015 Performance Report

Grantee: Grant: Brevard County, FL B-08-UN-12-0001 July 1, 2015 thru September 30, 2015 Performance Report 1 Grant Number: B-08-UN-12-0001 Grantee Name: Brevard County, FL Grant Award Amount: $5,269,667.00

Grantee: Grant: Brevard County, FL B-08-UN-12-0001 July 1, 2015 thru September 30, 2015 Performance Report 1 Grant Number: B-08-UN-12-0001 Grantee Name: Brevard County, FL Grant Award Amount: $5,269,667.00

October 1, 2016 thru December 31, 2016 Performance

Grantee: Grant:, MN B-08-UN-27-0003 October 1, 2016 thru December 31, 2016 Performance 1 Grant Number: B-08-UN-27-0003 Grantee Name:, MN Grant Award Amount: $3,885,729.00 LOCCS Authorized Amount: $3,885,729.00

Grantee: Grant:, MN B-08-UN-27-0003 October 1, 2016 thru December 31, 2016 Performance 1 Grant Number: B-08-UN-27-0003 Grantee Name:, MN Grant Award Amount: $3,885,729.00 LOCCS Authorized Amount: $3,885,729.00

2019 9% Competitive Housing Credit Application

2019 9% Competitive Housing Credit Application Application Checklist This checklist includes all the items from the CFA application and the LIHTC Addendum that are required for the 2019 9% Application

2019 9% Competitive Housing Credit Application Application Checklist This checklist includes all the items from the CFA application and the LIHTC Addendum that are required for the 2019 9% Application

Putting Real Estate To Good Use: Current Issues with Obtaining

Putting Real Estate To Good Use: Current Issues with Obtaining Conservation Easement Deductions and Rehabilitation Tax Credits Panelists: Robert Honigman, Arent Fox LLP Lee Sheller, DLA Piper ABA Tax Section

Putting Real Estate To Good Use: Current Issues with Obtaining Conservation Easement Deductions and Rehabilitation Tax Credits Panelists: Robert Honigman, Arent Fox LLP Lee Sheller, DLA Piper ABA Tax Section

The Tax Cuts and Jobs Act (P.L ) as signed by President Trump on December 22, Numerous provisions discussed below affect depreciation.

as signed by President Trump on December 22, Numerous provisions discussed below affect depreciation.") The Tax Cuts and Jobs Act (P.L. 115-97) as signed by President Trump on December 22, 2017. Numerous provisions discussed below affect depreciation. Code Sec. 179 Effective for tax years beginning after

The Tax Cuts and Jobs Act (P.L. 115-97) as signed by President Trump on December 22, 2017. Numerous provisions discussed below affect depreciation. Code Sec. 179 Effective for tax years beginning after

Cover Sheet. City of Lakewood, Division of Community Development. Address Detroit Avenue, Lakewood, OH Phone

Cover Sheet Organization Organization Type City of Lakewood, Division of Community Development Municipal Government Address 12650 Detroit Avenue, Lakewood, OH 44107 Contact Person & Title Mary Leigh, Programs

Cover Sheet Organization Organization Type City of Lakewood, Division of Community Development Municipal Government Address 12650 Detroit Avenue, Lakewood, OH 44107 Contact Person & Title Mary Leigh, Programs

ATTACHMENT A 2018 RESERVATION FEDERAL LOW INCOME RENTAL HOUSING TAX CREDIT PROGRAM CARRYOVER ALLOCATION REQUIREMENTS

ATTACHMENT A 2018 RESERVATION FEDERAL LOW INCOME RENTAL HOUSING TAX CREDIT PROGRAM CARRYOVER ALLOCATION REQUIREMENTS PART I The following requirements must be received in hard copy by the Agency by November

ATTACHMENT A 2018 RESERVATION FEDERAL LOW INCOME RENTAL HOUSING TAX CREDIT PROGRAM CARRYOVER ALLOCATION REQUIREMENTS PART I The following requirements must be received in hard copy by the Agency by November

April 1, 2012 thru June 30, 2012 Performance Report

Grantee: Elyria, OH Grant: B-08-MN-39-0007 April 1, 2012 thru June 30, 2012 Performance Report 1 Grant Number: B-08-MN-39-0007 Grantee Name: Elyria, OH Grant Amount: $2,468,215.00 Estimated PI/RL Funds:

Grantee: Elyria, OH Grant: B-08-MN-39-0007 April 1, 2012 thru June 30, 2012 Performance Report 1 Grant Number: B-08-MN-39-0007 Grantee Name: Elyria, OH Grant Amount: $2,468,215.00 Estimated PI/RL Funds:

HC FINAL COST CERTIFICATION FORM AND INSTRUCTIONS

HC FINAL COST CERTIFICATION FORM AND INSTRUCTIONS The Final Cost Certification Application (FCCA) must be completed by the Applicant and returned to Florida Housing along with an unqualified audit report

HC FINAL COST CERTIFICATION FORM AND INSTRUCTIONS The Final Cost Certification Application (FCCA) must be completed by the Applicant and returned to Florida Housing along with an unqualified audit report

U.S. Department of Housing and Urban Development. Meeting the 25% Set-Aside for Low-Income Persons

U.S. Department of Housing and Urban Development Meeting the 25% Set-Aside for Low-Income Persons Neighborhood Stabilization Program Neighborhood Stabilization Program Overview Eligible uses Program activities

U.S. Department of Housing and Urban Development Meeting the 25% Set-Aside for Low-Income Persons Neighborhood Stabilization Program Neighborhood Stabilization Program Overview Eligible uses Program activities

Managing Capitalization and Expense Depreciation

Managing Capitalization and Expense Depreciation PRESENTED BY: TRACY MONROE, CPA, MT, PARTNER LISA LOYCHIK, CPA, PARTNER JON WILLIAMSON, CPA, MT, MANAGER July 10, 2018 Welcome & Introductions Tracy Monroe,

Managing Capitalization and Expense Depreciation PRESENTED BY: TRACY MONROE, CPA, MT, PARTNER LISA LOYCHIK, CPA, PARTNER JON WILLIAMSON, CPA, MT, MANAGER July 10, 2018 Welcome & Introductions Tracy Monroe,

VALUATION OF GOODWILL FOR TAX PURPOSES

1 VALUATION OF GOODWILL FOR TAX PURPOSES James P. Catty President, Corporate Valuation Services Limited Chair, International Association of Consultants, Valuators and Analysts 2 All businesses have these

1 VALUATION OF GOODWILL FOR TAX PURPOSES James P. Catty President, Corporate Valuation Services Limited Chair, International Association of Consultants, Valuators and Analysts 2 All businesses have these

VHFA FEDERAL HOUSING CREDIT APPLICATION & VERMONT STATE AFFORDABLE HOUSING TAX CREDIT APPLICATION SUPPLEMENT

VHFA FEDERAL HOUSING CREDIT APPLICATION & VERMONT STATE AFFORDABLE HOUSING TAX CREDIT APPLICATION SUPPLEMENT Syndication Information Provide information below concerning syndication and estimated proceeds

VHFA FEDERAL HOUSING CREDIT APPLICATION & VERMONT STATE AFFORDABLE HOUSING TAX CREDIT APPLICATION SUPPLEMENT Syndication Information Provide information below concerning syndication and estimated proceeds

B-08-UN April 1, 2015 thru June 30, 2015 Performance Report. Community Development Systems Disaster Recovery Grant Reporting System (DRGR)

") Grantee: Grant: Lee County, FL B-08-UN-12-0009 April 1, 2015 thru June 30, 2015 Performance Report 1 Grant Number: B-08-UN-12-0009 Grantee Name: Lee County, FL Grant Award Amount: $18,243,867.00 LOCCS

Grantee: Grant: Lee County, FL B-08-UN-12-0009 April 1, 2015 thru June 30, 2015 Performance Report 1 Grant Number: B-08-UN-12-0009 Grantee Name: Lee County, FL Grant Award Amount: $18,243,867.00 LOCCS

2. Our community wants to demolish some blighted properties. How can we meet a CDBG national objective with this activity?

ENTITLEMENT CDBG PROGRAM FAQs ON MEETING A NATIONAL OBJECTIVE WITH ACQUISITION, DEMOLITION, AND DISPOSITION 1. What are the basic principles to meet eligibility and national objective requirements? As

ENTITLEMENT CDBG PROGRAM FAQs ON MEETING A NATIONAL OBJECTIVE WITH ACQUISITION, DEMOLITION, AND DISPOSITION 1. What are the basic principles to meet eligibility and national objective requirements? As

REALTORS CONTINUING EDUCATION SEMINAR

REALTORS CONTINUING EDUCATION SEMINAR THE ABANDONED BUILDING REVITALIZATION AND RETAIL REVITALIZATION ACTS May 2015 Burnet R. Maybank, III bmaybank@nexsenpruet.com Tushar V. Chikhliker tushar@nexsenpruet.com

REALTORS CONTINUING EDUCATION SEMINAR THE ABANDONED BUILDING REVITALIZATION AND RETAIL REVITALIZATION ACTS May 2015 Burnet R. Maybank, III bmaybank@nexsenpruet.com Tushar V. Chikhliker tushar@nexsenpruet.com

FACT SHEET. Depreciation of Farm Drainage Tile. Agriculture and Natural Resources OAM-1-12

FACT SHEET Agriculture and Natural Resources OAM-1-12 Depreciation of Farm Drainage Tile Wm. Bruce Clevenger OSU Extension Educator and Assistant Professor Introduction Agriculture is one of Ohio s largest

FACT SHEET Agriculture and Natural Resources OAM-1-12 Depreciation of Farm Drainage Tile Wm. Bruce Clevenger OSU Extension Educator and Assistant Professor Introduction Agriculture is one of Ohio s largest

Atypical Owner- Occupant Situations. Robert N Merryman O R Colan Associates

Atypical Owner- Occupant Situations Robert N Merryman O R Colan Associates RMerryman@orcolan.com Refresh the General Rules Displaced 90-day residential owner-occupants of a dwelling are eligible for a

Atypical Owner- Occupant Situations Robert N Merryman O R Colan Associates RMerryman@orcolan.com Refresh the General Rules Displaced 90-day residential owner-occupants of a dwelling are eligible for a

KPMG report: Proposed bonus depreciation regulations and 2018 filing season: Opportunities and pitfalls

KPMG report: Proposed bonus depreciation regulations and 2018 filing season: Opportunities and pitfalls August 9, 2018 The U.S. Treasury Department and IRS on August 3, 2018, released for publication in

KPMG report: Proposed bonus depreciation regulations and 2018 filing season: Opportunities and pitfalls August 9, 2018 The U.S. Treasury Department and IRS on August 3, 2018, released for publication in

HOME Investment Partnerships Program FAQs

HOME Investment Partnerships Program FAQs Last Updated: December 30, 2015 Description: This document contains the HOME Investment Partnerships Program FAQs posted on the HUD Exchange website (https://www.hudexchange.info/home/).

HOME Investment Partnerships Program FAQs Last Updated: December 30, 2015 Description: This document contains the HOME Investment Partnerships Program FAQs posted on the HUD Exchange website (https://www.hudexchange.info/home/).

Undivided Fractional Interest In Rental Real Property

April 28, 2002 About Exchanges Services Knowledge Base Contact Us About the Firm Featured Properties Undivided Fractional Interest In Rental Real Property Part III Administrative, Procedural, and Miscellaneous

April 28, 2002 About Exchanges Services Knowledge Base Contact Us About the Firm Featured Properties Undivided Fractional Interest In Rental Real Property Part III Administrative, Procedural, and Miscellaneous

April 1, 2014 thru June 30, 2014 Performance Report

Grantee: Grant: Prince Georges County, MD B-11-UN-24-0002 April 1, 2014 thru June 30, 2014 Performance Report 1 Grant Number: B-11-UN-24-0002 Grantee Name: Prince Georges County, MD Grant Award Amount:

Grantee: Grant: Prince Georges County, MD B-11-UN-24-0002 April 1, 2014 thru June 30, 2014 Performance Report 1 Grant Number: B-11-UN-24-0002 Grantee Name: Prince Georges County, MD Grant Award Amount:

5. The cost of buildings includes all necessary costs related to the purchase or construction

CHAPTER REVIEW Plant Assets 1. (S.O. 1) Plant assets are tangible resources that are used in the operations of a business and are not intended for sale to customers. Plant assets are subdivided into four

CHAPTER REVIEW Plant Assets 1. (S.O. 1) Plant assets are tangible resources that are used in the operations of a business and are not intended for sale to customers. Plant assets are subdivided into four

EXHIBIT E FORM OF CERTIFICATE OF CDLAC PROGRAM COMPLIANCE. T. Bailey Manor Apartments

EXHIBIT E FORM OF CERTIFICATE OF CDLAC PROGRAM COMPLIANCE Project Name: Name of Bond Issuer: T. Bailey Manor Apartments City of Los Angeles CDLAC Application No.: 15-331 Pursuant to Section 13 of Resolution

EXHIBIT E FORM OF CERTIFICATE OF CDLAC PROGRAM COMPLIANCE Project Name: Name of Bond Issuer: T. Bailey Manor Apartments City of Los Angeles CDLAC Application No.: 15-331 Pursuant to Section 13 of Resolution

U.S. Department of Housing and Urban Development Community Planning and Development

U.S. Department of Housing and Urban Development Community Planning and Development Special Attention of: Notice: CPD 98-2 All Secretary's Representatives All State/Area Coordinators Issued: March 18,

U.S. Department of Housing and Urban Development Community Planning and Development Special Attention of: Notice: CPD 98-2 All Secretary's Representatives All State/Area Coordinators Issued: March 18,

January 1, 2012 thru March 31, 2012 Performance Report

Grantee: Elyria, OH Grant: B-08-MN-39-0007 January 1, 2012 thru March 31, 2012 Performance Report 1 Grant Number: B-08-MN-39-0007 Grantee Name: Elyria, OH Grant Amount: $2,468,215.00 Estimated PI/RL Funds:

Grantee: Elyria, OH Grant: B-08-MN-39-0007 January 1, 2012 thru March 31, 2012 Performance Report 1 Grant Number: B-08-MN-39-0007 Grantee Name: Elyria, OH Grant Amount: $2,468,215.00 Estimated PI/RL Funds:

July 1, 2011 thru September 30, 2011 Performance Report

Grantee: Pinellas County, FL Grant: B-08-UN-12-0015 July 1, 2011 thru September 30, 2011 Performance Report 1 Grant Number: B-08-UN-12-0015 Grantee Name: Pinellas County, FL Grant Amount: $8,063,759.00

Grantee: Pinellas County, FL Grant: B-08-UN-12-0015 July 1, 2011 thru September 30, 2011 Performance Report 1 Grant Number: B-08-UN-12-0015 Grantee Name: Pinellas County, FL Grant Amount: $8,063,759.00

April 1, 2017 thru June 30, 2017 Performance Report

Grantee: Grant: Orange County, FL B-08-UN-12-0012 April 1, 2017 thru June 30, 2017 Performance Report 1 Grant Number: B-08-UN-12-0012 Grantee Name: Orange County, FL Grant Award Amount: $27,901,773.00

Grantee: Grant: Orange County, FL B-08-UN-12-0012 April 1, 2017 thru June 30, 2017 Performance Report 1 Grant Number: B-08-UN-12-0012 Grantee Name: Orange County, FL Grant Award Amount: $27,901,773.00

NYS HOME Local Program

NYS HOME Local Program Homebuyer Development Projects Technical Assistance Webinar October 10, 2018 Welcome and Introductions Ann M. Petersen, LEED AP Director NYS HOME Program (Albany Regional Office)

NYS HOME Local Program Homebuyer Development Projects Technical Assistance Webinar October 10, 2018 Welcome and Introductions Ann M. Petersen, LEED AP Director NYS HOME Program (Albany Regional Office)

April 1, 2013 thru June 30, 2013 Performance Report

Grantee: Prince William County, VA Grant: B-08-UN-51-0002 April 1, 2013 thru June 30, 2013 Performance Report 1 Grant Number: B-08-UN-51-0002 Grantee Name: Prince William County, VA Grant Amount: Estimated

Grantee: Prince William County, VA Grant: B-08-UN-51-0002 April 1, 2013 thru June 30, 2013 Performance Report 1 Grant Number: B-08-UN-51-0002 Grantee Name: Prince William County, VA Grant Amount: Estimated

April 1, 2013 thru June 30, 2013 Performance Report

Grantee: Pinellas County, FL Grant: B-08-UN-12-0015 April 1, 2013 thru June 30, 2013 Performance Report 1 Grant Number: B-08-UN-12-0015 Grantee Name: Pinellas County, FL Grant Amount: $8,063,759.00 Estimated

Grantee: Pinellas County, FL Grant: B-08-UN-12-0015 April 1, 2013 thru June 30, 2013 Performance Report 1 Grant Number: B-08-UN-12-0015 Grantee Name: Pinellas County, FL Grant Amount: $8,063,759.00 Estimated

Glossary of Terms Low-Income Housing Tax Credit Program

Glossary of Terms 2017 Low-Income Housing Tax Credit Program AMGI: Area Median Gross Income as defined by HUD. AMI: Area Median Income as defined by HUD. BIN: The state credit agency assigns a Building

Glossary of Terms 2017 Low-Income Housing Tax Credit Program AMGI: Area Median Gross Income as defined by HUD. AMI: Area Median Income as defined by HUD. BIN: The state credit agency assigns a Building

New York State and Federal Historic

1 New York State and Federal Historic Rehabilitation Tax Credits Co Sponsor: Preservation League of New York State www.preservenys.org 2 New York State and Federal Historic Rehabilitation Tax Credits New

1 New York State and Federal Historic Rehabilitation Tax Credits Co Sponsor: Preservation League of New York State www.preservenys.org 2 New York State and Federal Historic Rehabilitation Tax Credits New