Final Report on Strategic Alternatives for the Village & Town of Seneca Falls, NY Considerations for a New Governance Model

|

|

|

- Alexia Lamb

- 5 years ago

- Views:

Transcription

1 Final Report on Strategic Alternatives for the Village & Town of Seneca Falls, NY Considerations for a New Governance Model November, 2008

2 Final Report on Strategic Alternatives for the Village & Town of Seneca Falls, NY Considerations for a New Governance Model December, 2008 This report was prepared with funds provided by the New York State Department of State under the Shared Municipal Services Incentive Grant Program Prepared for: Village & Town of Seneca Falls, NY Charles Zettek, Jr. Project Director 1 South Washington Street Suite 400 Rochester, NY State Street Suite 330 Albany, NY Copyright CGR Inc All Rights Reserved

3 i Final Report on Strategic Alternatives for the Village & Town of Seneca Falls, NY Considerations for a New Governance Model December, 2008 EXECUTIVE SUMMARY The Village and Town of Seneca Falls are rich with history as the birthplace of the women s rights movement. They are located in prime territory, nestled between two Finger Lakes in central New York State s fertile wine country. However, as with many local economies in New York State (NYS), high property taxes are putting a financial strain on their individuals, families and businesses. Thus, in 2006, the Village and Town boards affirmed the need to work together to address economic and service delivery issues and to form a comprehensive plan to reduce tax burdens and revitalize the area. As a result of this collaboration, the Village and Town hired the firm of Camoin Associates to conduct an economic development study. Camoin presented a report in 2007 called the Economic Development & Commercial Revitalization Plan. This plan offered a number of ideas for igniting the local economy, and the Village and Town boards adopted several of the initiatives very quickly. The first initiative adopted was the hiring of a jointly funded Economic Development Specialist to work full time on economic development initiatives in the community. Simultaneously, efforts were begun to rebrand the community and make it more visible both as a destination in the Finger Lakes area and also as a tourist site in order to take advantage of its rich history. Another prominent recommendation of the 2007 study was that the Town & Village should explore obvious areas for consolidation of services and act upon those issues immediately. In the long-term, local officials should continue to work together to consolidate the Town & Village into one efficient unit of local government to lower the tax burden on residents and businesses. This particular recommendation spurred the Village and Town boards to write a grant to receive funds from New York State s Shared Municipal

4 ii Services Incentive Grant Program 1 to engage a consultant and study consolidation/dissolution issues between the Village and Town. The Center for Governmental Research, Inc. (CGR) was selected to conduct this study in February The goal of the study, as described in the program work plan approved by the state, was to evaluate the optimal level of consolidation for maximum efficiency and cost savings. 2 CGR initiated the project at a public hearing on February 27, Over the course of the next seven months, CGR participated in several public meeting discussions with the Town and Village boards regarding progress and findings of the study. Further, CGR worked very closely with an eight-person study committee (two representatives from each board and three citizen representatives) to review our findings and develop alternatives. Thus, our findings have been reviewed by the study committee, the Village and Town boards and the broader community. The primary work product for this study culminated in a Power Point presentation that was delivered to the public on September 30, This presentation consisted of CGR findings with regard to shared service options, as well as possible tax and revenue impacts for the Village and Town should the Village dissolve. Each of the options forms the framework for a new governance model once the community decides whether to maintain two governments or consolidate into one. This presentation has been included as Appendix 1. The sections that form the written component of this report address the specific project components identified in the Town and Village Program Work Plan, the foundation of the SMSI grant. The appendix also includes primary information about the Village and Town that was developed and presented to the study committee, working papers developed by CGR addressing several of the key issues affected by consolidation of the Village and Town, and additional reference material from other sources that will provide useful information if the community pursues dissolution. Key Findings CGR conducted the study within the framework of two options: shared service alternatives between the Village and Town and full consolidation through dissolution of the Village. In a shared services approach, costs can be saved by leveraging economies of scale (combined capital and other tangible assets or combined volumes for purchasing goods and services) and/or economies of skill (sharing talent and individual 1 As of the NYS Budget, SMSI became known as the Local Government Efficiency Grant Program (LGEG). 2 From the Project Description, Appendix D Program Work Plan of Contract No. C between the State and the Village for the SMSI project.

5 iii expertise), while still retaining both local governments. Full consolidation can yield these type of cost savings as well as additional savings and efficiencies that result from eliminating one layer of government. Either approach can yield operational efficiencies. Thus, CGR analyzed each alternative in light of both cost savings and efficiency considerations. CGR s review of the current operations in the Village and Town and potential options resulted in the following key findings: 1. If current service levels are maintained: a. There are several opportunities to improve efficiencies through either shared services or full consolidation. b. There are limited opportunities to achieve significant cost reductions. 2. The two highest cost drivers for the Village are the Police Department and the Department of Public Works. a. Police Dispatch services could be eliminated, saving the Village roughly $150,000. Service would largely remain the same, as County 911 would become responsible. b. Maximum cost savings in the DPW would come from elimination of one Superintendent position in the event of full consolidation. Cost shifts between the Village and Town are possible under shared services agreements. 3. The Town has a large non-property tax revenue stream, which can be used in a number of ways to benefit the Village taxpayers. 4. Full consolidation yields large tax savings for former Village taxpayers but potentially shifts the tax burden to town taxpayers, affecting former Town Outside Village (TOV) taxpayers the most. However, the impact of tax shifts would be mitigated by various options the town would choose for applying future non-property tax revenue. 5. The Historic Preservation District and Visitor Center in the Village can be maintained by the Town in the event of Village dissolution. 6. Facility options are driven by: a. What services are delivered b. Who delivers those services c. Potential to increase the tax base. Under either shared services or full consolidation, the Village and Town should be able to consolidate facilities and put municipal properties back on the tax rolls.

6 iv 7. Current Village general fund debt would likely remain with the former Village taxpayers if the Village dissolves; however, the details of handling existing Village debt would be developed as a part of a formal Dissolution Plan. 8. Full Consolidation would yield a minimum of $495,000 of new, annually renewable money to the Town of Seneca Falls due to the New York State revenue sharing incentive program, an outgrowth of the Aid and Incentives to Muncipalities (AIM) funding. These findings, taken together, indicate that the change that would produce the highest level of efficiencies and cost savings would be for the Village to dissolve and consolidate with the Town. Dissolution would result in the highest level of direct cost reductions, and, under current State law, would bring an additional amount of at least $495,000 into the community in new State aid revenues. This combination of highest cost reductions and new revenues would result in the largest property tax reductions for Village property owners. There are many possible ways to share the cost savings and net new revenue among Village and TOV property owners. The amount of tax shifting between Village and TOV property owners ultimately has to be decided during development of a Dissolution Plan; however, CGR presented one reasonable plan that would result in Village taxpayers receiving a net property tax reduction of $978/year and TOV taxpayers having a net property tax increase of $373/year. 3 Next Steps The Village and the Town have two clear options to pursue. The Village could continue to exist as a separate government and pursue shared service agreements with the Town. Or, the Village could dissolve, in effect achieving full consolidation with the Town. Either course can produce cost savings and efficiency gains; however, full consolidation will clearly result in the largest net fiscal impact to the community of the two options. The Village and Town boards can pursue shared services options directly through intermunicipal cooperation agreements. However, voters of the Village would have to approve dissolution of the Village by majority vote at a public referendum. The Village Board could choose to pursue a dissolution vote, or citizens can initiate a dissolution vote. 4 In either case, once the dissolution process is initiated, state law 5 prescribes a process 3 For a property assessed at $100, By submitting a valid petition signed by one-third of eligible voters through a process defined by state law. 5 Village Law Article 19

7 v that must be followed. Two key elements of the process are that a Dissolution committee must be formed, and the Dissolution committee must develop and present to the public a Dissolution Plan, which details exactly what will happen to village assets, services, employees, etc. if the village dissolves and the town is left to provide services in what was formerly the village. Thus, as a result of the community discussion generated by the findings of this report, community leaders and citizens interested in improving their community will need to determine which option to pursue. This report provides the framework for a new governance model once the community decides whether to maintain two governments or consolidate into one.

8 vi Acknowledgements CGR would like to thank Village and Town staff and elected leaders for their time, investment and perspective throughout the course of this study. In particular, CGR would like to thank Village Administrator Connie Sowards for her professional support and administrative expertise in providing information and also in coordinating meetings and scheduling public hearings. Special thanks is also extended to Mayor Diana Smith and Supervisor Peter Same for their leadership and help in assuring open access to all data, personnel and information to make this study as comprehensive as possible. Staff Team Charles Zettek, Jr., Vice President and Director of Government Management Services, directed the study. Scott Sittig, Senior Research Associate, served as the project manager, and Katherine Corley, Research Assistant, contributed significant research and data analysis to this study.

9 vii TABLE OF CONTENTS Executive Summary...i Key Findings... ii Next Steps... iv Table of Contents...vii Work Plan Components...1 Work Plan Framework...1 Revenue Considerations...2 Cost Considerations...5 Municipal Facilities Considerations...7 Shared Services and Dissolution Considerations...9 Next Steps...10 Conclusion...10 Appendix Power Point Presentation to Community Town Report on Joint Facility Municipal Budgets Historical Designations and Alternatives in Dissolution of the Village Landfill Revenue Sharing Alternatives List of People Interviewed during Study General Dissolution Information...

10 1 WORK PLAN COMPONENTS CGR started this research project in March of The study involved data collection and analysis of budget information from the Village and Town, as well as personnel and asset inventory analysis. CGR interviewed all key department heads in the Village and Town and met extensively with key administrative personnel 6 from both in order to gain first-hand perspective on issues facing the entities. In addition to key appointed and civil service staff, CGR also interviewed Mayor Diana Smith and Supervisor Peter Same and received other feedback from elected officials through the study committee. 7 CGR was able to interview representatives of two local businesses as well as to speak with Village and Town community representatives who served on the study committee. During the course of the study, CGR participated in four committee meetings to review options and two public hearings. CGR developed its work plan and completed the work of the project in accordance with CGR s Proposal, made in response to the Request for Proposals solicited by the Village of Seneca Falls, and the subsequent contract between the Village and CGR. What follows in this section is a review of key background information that was incorporated into the September 30 Power Point presentation (Appendix 1). CGR s work in total incorporates specific Project Components listed under Section 2 a) - Objectives, contained in Appendix D of Contract C between the Village of Seneca Falls and the State. The work plan was not specifically designed to address each of those objectives in the order listed, but clearly does address them as part of an integrated approach designed to achieve the overall goal of the study. Work Plan Framework CGR engaged in a comprehensive analysis of revenues and expenses and a side by side comparison of line items in each municipality s budget (see Appendix 3). Assuming that the level of assessment is near 100% and updated on a regular revaluation cycle 8, high tax rates can only be addressed by reducing the costs that make up the tax levy or increasing the non-property tax revenue to offset those costs. Each alternative was 6 Listed in Appendix 6 7 Listed in Appendix 6 8 The Town of Seneca Falls and the Town of Fayette operate as one coordinated assessment program (CAP), are on a regular three-year revaluation schedule and each Town maintains a current and equitable Level of Assessment.

11 2 analyzed in the context of shared services or full consolidation 9 and took into account personnel and asset inventory analysis as well as debt and equity positions for each municipality. Revenue Considerations The Town of Seneca Falls has a contract with a private company, Seneca Meadows that allows the latter to operate a landfill within the Town borders. Compensation for this arrangement yields non-property tax revenue to the Town in excess of $3.5 million dollars annually for over a decade, renewable for a second term. This revenue stream has allowed the Town to essentially operate without a Townwide tax 10 for several years in a row while simultaneously funding the operation of a community recreation center accessible to all residents of the Town. According to the contract, this revenue stream will grow. Under current Town policy, a significant portion of this revenue is being set aside in a Tax Stabilization Reserve Account to offset future tax increases for all Town residents. At the request of the study committee, CGR was able to identify strategies that would allow the Town to use this special non-property tax revenue (what is referred to as Excess Revenue in the 9/30 Power Point) to cover Village specific costs. Several of these options did not require full consolidation and would be possible with intermunicipal shared services agreements between the Village and Town. Service levels would remain the same as a result of these agreements, but control of the operation and budgeting would likely transition from the Village to the Town. The primary services identified as being prime opportunities for shared services that might benefit from creative sharing of the town excess revenue included street maintenance, snow removal, refuse collection and the Historic Visitor s Center. Under intermunicipal shared services agreements, the Village could cease operation of its street maintenance function and turn the entire operation over to the Town Highway Department. This would include all aspects of street maintenance and would also involve the transfer of existing employees and assets related to this function to the Town. Refuse collection could also then be transferred to the Town Highway Department since it has historically been overseen by the DPW in the Village. The Town Highway Department would then be responsible for all street maintenance, repair, snow plowing and refuse collection associated with the Village. If this were implemented, the Village budget (and thus Village taxes) would be substantially lower and 9 Full Consolidation = Dissolution of the Village of Seneca Falls and the folding of remaining assets, debts and services into the operational budget of the Town of Seneca Falls. 10 The Town did have a town wide highway tax of $.46/1000 in 2008.

12 3 the Town could apply some of the revenue currently being allocated to the Tax Stabilization Reserve to offset the increase in costs yielding potentially no tax increase to Town residents. If the Village were to transfer the street maintenance, snow plowing and refuse collection services to the Town Highway Department under a shared services agreement, the Village would likely retain its Superintendent of Public Works. The Superintendent would be focused on maintaining water and sewer services within the Village and would continue to supervise the current staff associated with these operations. The Town could not use its excess revenue to supplement these services as long as the Village retained operational responsibility for some of its public works infrastructure. Thus, there would still need to be a position of Superintendent of Public Works, with the result being that there would be no personnel reductions and thus little direct savings. The operation of the Visitor Center could be transferred to the Town and absorbed by the Town budget. This operation is roughly $66,000 per year. The Visitor Center did receive a NYS grant several years ago that obligated the Village to operate the facility as a Visitor Center through the year However, the stipulation does not preclude the Town from operating it (as opposed to the Village) as long as the Visitor Center itself remains in operation through the specified year. Town non-property tax revenue could offset this transfer of operation, thus generating no tax increase for TOV residents. The intermunicipal shared services options identified above represent cost shifts as opposed to true cost savings between the two communities. A cost shift means that costs for a particular service transfer from one municipality to another while the aggregate total cost remains the same. One advantage of shifting costs is that it allows the Town to legally use its non-property tax revenue to fund services that largely benefit the Village. CGR heard repeatedly that this has been a difficult point of discussion between the Village and Town boards for several years. The Village is the core business district for the Town and comprises a substantial majority of the economic development and commercial activity within the Town. Keeping village streets paved and keeping sewer and water lines operational clearly benefits the entire population in the Town, at least indirectly. Another advantage of cost shifting is that it allows those same costs to be spread over a larger taxable assessed valuation and thus reduces the potential tax impact to village residents. The obvious downside is the increased tax burden it puts on current Town Outside of Village residents, who currently enjoy almost no town tax. Cost shifting is one option for allowing the Town to use its revenue for purposes that largely benefit needs within the Village. This is not to be confused with the options that exist for the Town to share its revenue

13 4 with the Village. CGR researched several different methods for this to happen and has summarized those options in Appendix 5. Should the Village and Town consolidate, new revenue to the community would be available in the form of Aid and Incentive to Municipalities (AIM). 11 NYS put these incentives into the budget to encourage local municipalities to consolidate their operations and legal structures, and the incentives, as defined in current law, continue in future years (with no end date prescribed.) The most lucrative incentive available to the Village and Town of Seneca Falls would increase the Village s and Town s current combined AIM revenue by an amount equal to 15% of the combined tax levy of the two municipalities in the previous fiscal year. CGR estimated that this would yield a minimum of $495,000 in new revenue to the newly merged entity. This increase would be offset by a loss in revenue associated with the Gross Utilities Receipts Tax of $85,000, which towns are not eligible to receive. Thus, the net increase in revenue to the merged entity could be $410,000, or slightly more than 3% of the combined budgets of both municipalities (including water and sewer). CGR conducted additional revenue analysis on the impact of putting tax exempt properties back on the tax roll in the future. The sites used for the analysis included the current Town Hall (rendered uninhabitable due to fire), the current Village Hall and the current Village Department of Public Works (DPW) facility. The Village and Town Halls were selected due to the likelihood that each would be sold after the new joint municipal facility has been built. The DPW facility was analyzed when the study identified the option of eliminating the Village DPW in a dissolution and combining the operation with the Town Highway Department. In this scenario, the most efficient course of action is to eventually combine the operation at the current Town Highway Department location. Using assessed valuation figures for 2008 and using the tax rate for the Village, CGR estimated that putting the three municipal facilities back on the tax roll would yield another $20,000 in additional revenue to the community. These steps could be taken regardless of whether the municipalities completed a formal consolidation. Selling the current DPW facility would demand that a larger shared facility could be built on the current Town Highway Department location. This would obviously take time and planning and is likely a longer term option for the community to consider. 11 CGR and the study committee recognize the current fiscal crisis facing NYS. As of the writing of this report, no indication had been received of any reduction in AIM funding that might impact our calculations. As with any funding that is appropriated in the annual NYS budget, no guarantees can be given as to future availability.

14 5 Cost Considerations CGR obtained budget data from each municipality and analyzed the data for possible service overlap and cost savings options. CGR identified $393,000 of true cost saving opportunities, which represents slightly less than 3% of the combined Town, Village and special districts budgets (including water and sewer). General and Administrative savings would equal approximately $150,000 in a full consolidation model due to consolidation of personnel and a reduction of administrative overhead. $93,000 of savings could accrue from eliminating the Superintendent of DPW should the Village eliminate its DPW function and all public works operations be consolidated with the Town Highway Department. Another $150,000 would accrue from eliminating the dispatch function and allowing the County 911 operation to fully cover the Village. General and administrative services could be reduced through a combination of staff reductions (through attrition where possible) and elimination of certain duties and overhead costs. In a shared services model, both offices would benefit from being located in one facility, making it easier for residents to have one location to deal with both Village and Town matters. Clerk functions could be redefined to allow for streamlining of activities. Office equipment could be shared and office supplies could be ordered and managed for one office instead of two. Were the Village to dissolve, its budgeting processes would be eliminated and some of the responsibility associated with the Village Administrator would cease. Through some reallocation of duties, CGR estimates that the Administrator position could be eliminated with duties absorbed by the remaining staff in a combined office. Under a dissolution scenario, CGR projects savings to be closer to $150,000. However, in a shared services model, savings is likely to be much less than $150,000 since fewer positions could be eliminated. If the Village were to dissolve, the Village DPW would no longer exist. Water and sewer services would become the responsibility of the Town and would likely be absorbed operationally within the Town Highway Department. Since these services are financially self-sustaining (they are billed with user fees), the financial burden would not change. All remaining staff, assets and services (i.e. street maintenance, snow plowing, refuse collection, etc.) of the Village DPW would be absorbed by the Town Highway Department. This would likely mean that the position of Superintendent of the Village DPW could be eliminated, saving the community $93,000 in salary and benefits. Other DPW service areas that were reviewed included street lighting and sidewalks. Both could transfer to the Town Highway Department to maintain efficiencies with operations. Since each relate solely to Village property, the most likely scenario would be to create special districts for

15 6 each and to levy ad valorem taxes on those within each district. Thus, village residents would see no tax savings, but operational efficiencies would occur by keeping management of these districts coordinated under one department. One service area in which the Village and Town are already taking steps to consolidate is the planning, zoning and code enforcement function. This particular option will likely increase costs minimally, as current plans are to create a full-time position operated under the Town budget to replace the current part-time positions in each. The consolidation of this operation is intended to produce efficiencies and streamline the permit and enforcement process in the Town so that all residents can access the process more effectively. One municipal facility will enhance this service consolidation option by creating one location for the community to pick up permits, ask questions and take care of payments. County 911 currently offers dispatch services for the entire county. The Seneca Falls Village Police Dispatch service is thus inherently redundant in its service and could be eliminated with existing personnel transferred up to the County or reassigned within the Village. It is recognized that this would result in the loss of some secretarial support as a result of the dispatchers not being available on a daily basis to the police officers. In addition, CGR understands that the current dispatch offers a personal touch in the community that provides some residents with extra assurance of police access and thus public safety. However, the current village dispatch operation currently costs the Village approximately $150,000 in personnel salaries and benefits. This is in addition to the overlapping 911 service provided by the county and paid for by Village taxpayers as part of their county tax bill. CGR analyzed the police department from an operational and budgetary perspective to determine the impact that police have on the community. Police officers provide a sense of security in the Village by spending nearly 50% of their time in proactive community policing strategies. CGR calculated that a police car likely travels all village streets an average of 2 times per day. Of course, local police are also the first to arrive at a scene and have jurisdiction to handle all criminal activity within the borders of the village. CGR heard many conflicting comments regarding the Village police throughout the course of the study, ranging from a desire to keep the police to a desire to see them disband in favor of coverage by the Sheriff and/or State Police. It was beyond the scope of this study to perform a full analysis of the merits of these options. However, our study did assess the financial impact of moving the operation of the police department from the Village to the Town.

16 7 If the Village dissolved, presumably the Dissolution Plan would include the transfer of police function to the Town. Or, if the community chose to pursue this transfer prior to (or instead of) a dissolution, a formal public referendum would have to be taken by Village residents to dissolve the Village Police Department. In either case, the Town board would then have to consider whether to add the police department to the Town budget or operate without a police department in favor of coverage by the County Sheriff and/or State Police. If the Town took on the current Village police operations, the Town could expect costs to increase somewhat due to the gas and maintenance costs related to coverage of an expanded service area. Increased costs from adding more patrol officers would be a function of the size of the force needed to provide coverage based upon the final service area identified by the Town. CGR estimates that shifting current Village police department costs to all town taxpayers would increase town tax bills by $3 - $4/$1000 assessed valuation, although current Village taxpayers would see a net decrease because the current Village police operations cost approximately $6-$7/$1000 assessed valuation in the current Village tax bill. Present NYS legislation does not allow for police districts to be created; however, the community could pursue special state legislation to allow for Town police to provide coverage solely within the current Village boundaries. Under this scenario, the cost of the current Village department could be assigned to current Village properties. In that case, Town police services would only be provided to former Village properties. This strategy would permit the Town to retain a police department, but would assign the services and costs to former Village properties. The effect would be a hold harmless situation current Village properties could keep their police services (and associated costs) and TOV taxpayers would see no shift of police costs to their own tax bills. If, at some future time, TOV property owners determined that they would be better served by Town police than by the county sheriff, the Town police department could be expanded to cover the whole Town (with, of course, the attendant increase in costs and taxes.) Municipal Facilities Considerations CGR was initially asked to select and evaluate alternative sites for a new municipal facility as well as to perform cost and financing projections for the potential facility. However, prior to finalizing our contract, the Village and Town board had already done significant research on multiple sites within the community. As a result, CGR conducted a preliminary assessment of the following facilities and sites: Existing Town Hall facility at 10 Falls Street Existing Village Hall

17 8 Academy Building St. Patrick's/St John Bosco School Wescott Rule Seneca Factory Ovid Street These sites had previously been discussed at length by the Village and Town boards, and the Town had tentatively decided to move forward with the Ovid Street location prior to any analysis by CGR. CGR understood that the Town desired to build the facility on the Ovid Street site because it was largely vacant and already owned by the Town. The Town would then invite the Village to join them in a shared facility. CGR had some concerns after preliminary observations revealed that this location was not in the Village center and in fact was ¾ of a mile away from the main village business corridor. In addition, it did not appear that the Village Board fully supported this plan. During the course of our preliminary assessment work, the Town proposed a new option to the Village: a joint facility to be built on South Street along the canal. The Village and Town mutually agreed that this was a good location and invited the Town s engineers to begin to draw mockups and do some site analysis and building cost projections. At this point, members of the study committee asked CGR to readjust the focus of our contract with the Village and spend no more time on site analysis or cost projections related to a new facility. It was decided by the Village, Town and CGR together that CGR s focus would shift to other priorities, including how Town non-property tax revenue could be used to support the Village budget and what the impact would be on the Village historic designations in the event of dissolution. Both boards agreed to use the findings of CGR s study to inform the ultimate size and needs of the new joint facility. CGR has included as Appendix 2 the work that the Town and their engineers have done regarding site identification and cost projections for building and financing the new structure. The Space Planning figures shown in Appendix 2 were based on an assumption that the Village and Town governments would share the same facility. However, if the Village dissolves and if the Village dispatch operation is transferred to the County, a minimum of 1,600 square feet could be reduced from the building

18 9 plans. 12 At a construction cost range of $175-$200 per square foot, this would reduce building costs by $280,000 to $320,000. The study committee concluded that the final sizing of the joint municipal facility and options for funding construction of the new facility will be affected by the outcome of the broader community decision about whether or not to dissolve the Village. Shared Services and Dissolution Considerations There are many different resources that the Village and Town can utilize in determining what steps to follow and what lessons to remember in pursuing both shared services and the dissolution options. Any and all agreements to share services, to whatever degree, between the Village and Town should be set forth in writing. A good general reference with many different examples of shared services agreements can be found at Two reports with examples of shared services agreements that apply specifically to the highways and public works are: Developing Intermunicipal Agreements for Highway Services: A Guide for Local Government Officials at ents.pdf Promoting Intermunicipal Cooperation for Shared Highway Services at: It is clear from reviewing shared service agreements among municipalities across the state that municipalities have the freedom to be creative in terms of how they define what services will be shared, how the costs of those services will be shared, and how delivery of those services will be managed and measured. The shared services options identified in this report could clearly be carried out under intermunicipal service agreements, if the agreements were perceived as fair and equitable and provided the services desired. 12 For example, under the personnel plan projected if the Village dissolves, the new facility would not need separate dedicated space for a Village Administrator s office, a Mayor s office, a Trustees office, a workroom/conference room, etc.

19 10 As noted previously, should the Village choose to initiate a dissolution process, the elements of dissolution are clearly delineated in Article 19 of the Village Law. In particular, Section 1903 of the NYS Village Law articulates the elements that are required in a formal dissolution plan. A plan is only required after a formal petition to dissolve the Village has been submitted to the Village board with 1/3 of eligible voters signatures, or if the Village board adopts a resolution calling for a dissolution vote to occur. As neither of these actions has occurred, CGR s work does not constitute an official dissolution plan. However, our work was organized to address, in general terms, the major cost, service and implementation concerns that a formal dissolution plan would specifically cover. CGR s Power Point presentation addresses each of the primary questions raised during a dissolution process: 1) What services would be retained; 2) What services would be changed or eliminated; 3) What would be the budget implications; and 4) What would be the tax implications. More specific requirements for the dissolution process are provided in references identified in Appendix 7. Next Steps To conclude our presentation, CGR developed a list of possible next steps for the Village and Town to consider. During the course of the public meetings, there appeared to be a wide range of opinions in the community about the best way to proceed. In order to gain a better perspective on this, the Village and Town could conduct a scientifically valid survey to determine the will of the people in relation to dissolution or shared services prior to engaging in the preparation of a full dissolution plan. Alternatively, Village leaders and/or citizens could initiate steps to develop a dissolution plan to be put before the voters (see previous section or Appendix 7 for details on the process). Or, short of moving in a direction towards dissolution, the Village and Town Boards could conduct joint hearings to discuss implementation of shared service options that have been outlined in the context of this report. Conclusion Compared to many other communities, Seneca Falls has the following competitive advantages: It is a full service community with a vibrant village core. It has a large and predictable revenue stream. It has plans to provide public water to the entire town at low cost. It is located in the prime Finger Lakes Region.

20 11 It has a world class marketing brand as the home of the Women s Rights movement. These competitive advantages are all part of the context in which the Village and Town boards have taken a comprehensive look at costs, tax rates and the economic vitality of the community. Seneca Falls is uniquely positioned to restructure itself and achieve lower taxes without significantly changing the level of services that residents have come to expect.

21 12 APPENDIX 1. Power Point Presentation to Community 2. Town Report on Joint Facility 3. Municipal Budgets CGR has included a crosswalk of Village and Town budgets for the Town Fiscal Year 2008 and Village Fiscal Year The Village numbers on this crosswalk were part of the original budget. Subsequent to our analysis, the Village amended their budget and we included the amended budget as a separate attachment in this appendix. 4. Historical Designations and Alternatives in Dissolution of the Village 5. Landfill Revenue Sharing Alternatives 6. List of People Interviewed during Study 7. General Dissolution Information

22 APPENDIX 1. Power Point Presentation to Community

23 Preliminary Findings toward a Strategic Plan for a new Governance Model Seneca Falls, NY Charles Zettek, Jr., M.S. VP & Director, Government Management Services Scott Sittig, M.P.P. Senior Research Associate September 30,

24 Key Definitions Town = All residents within the Town border. Village (V) = Residents inside the Village border Town Outside of Village (TOV) = Residents in Town but outside of Village border 2

25 Key Definitions (2) Shared Services = Consolidation of services while keeping Village and Town government Dissolution = Assumes Village dissolves and Town remains Efficiency = Eliminate duplication or overlap Cost Savings = Reduce expenses (All numbers presented are for 2008 in the Town and in the Village) Cost Shift = Costs remain but who pays changes 3

26 Tax Savings Benchmark Tax Impact of Budget Changes Input Tax Levy Change ==> $10,000 Township Tax Levy Change Tax Rate Change Town-wide $10,000 TOV $10,000 Village $10,000 $0.027 $0.061 $

27 CGR s Task Develop a strategic plan that outlines a future governance model consistent with the goals identified in the 2007 Economic Development & Commercial Revitalization Plan 5

28 First Goal in the Economic & Commercial Revitalization Plan Strategic Plan 1.1 Consolidation of Town & Village The Town & Village should explore obvious areas for consolidation of services and act upon those issues immediately. In the long-term, local officials should continue to work together to consolidate the Town & Village into one efficient unit of local government to lower the tax burden on residents and businesses. 6 (Seneca Falls Strategic Plan for Economic Development & Commercial Revitalization Plan, Page 3, May, 2007)

29 How to Reduce the Tax Burden 5 Factors to Consider Identify Cost Savings Shared services options Dissolution options Identify Additional Revenues Putting municipal buildings on tax roll NYS AIM incentives Town sharing excess revenue 7

30 Tax Reduction Strategies Shared Services Approach Village services shared with and/or transferred to Town Some direct cost savings No NYS AIM incentive Town has options for sharing its excess revenue 8

31 Tax Reduction Strategies (2) Village Dissolution Higher direct cost savings Eligible for NYS AIM incentive Town has more options for sharing its excess revenue 9

32 Comparing the Strategies Shared Services There are a number of strategies that could be pursued The cost and tax impacts vary depending on what options are pursued Dissolution Dissolution and complete transfer of village assets and services to the Town results in the largest cost savings and property tax reduction to village tax payers 10

33 Key Questions To Ask When Thinking About Shared Services or Dissolution What Government Services do you want? Who should provide those services? What is most efficient and cost effective (i.e. least tax impact)? Who controls the interests of the community? 11

34 Community Choices will Drive Facility Decisions Facility Impact 12

35 Tax Impact of Facility Options using Village Tax Rate Village Hall Assessed Valuation = $540,000 Town Hall Assessed Valuation = $200,000 Village DPW Assessed Valuation = $525,000 *Current market conditions will affect final sales and taxable assessed valuation 13

36 Probable Tax Revenue Increase with 3 Properties Back on the Tax Roll Village Hall = $9000 per year Town Hall = $3000 per year DPW Garage = $8000 per year Sum Total = $20,000 per year to reduce the Village Tax Levy in shared services model. Under Dissolution, Town tax benefit would depend on new Town tax rate. 14

37 Potential for Reducing Costs Key Cost Drivers & What Can Be Changed 15

38 Services Budgeted by the Town and Village in 2008 Includes Special Districts such as Water/Sewer and Lighting Districts 16 Service Town Village General & Administrative X X Zoning & Code Enforcement X X Court X Police X Dispatch X Fire X X Economic Development X X Transportation X X Refuse Collection X X Water X X Sewer X X Recreation X

39 Existing Village Cost Components General Fund General Fund Budget ( ) = $4.1 Million Village Expenses (General Fund) Transportation 28% Fire 3% Dispatch 4% Refuse Collection 4% Other 8% Debt Service 8% 17 Police 34% General & Administrative 11%

40 How We Identify Opportunities Using G & A As An Example Key Cost Elements Village 1 FT Administrator 1 FT and 2 PT Clerks Village Hall costs for Maintenance and Utilities No existing debt on current Village Hall Town 1 FT Elected Clerk 1 FT and 2 PT Other Positions (1 PT position is filled by current Elected Town Clerk) 2 PT Tax Collectors (1 Elected) Currently Operating in Old Library No debt on existing Town facilities 18

41 Shared Services Approach General and Administrative Two small offices limit options for eliminating duplication Combining Offices under a shared services agreement would create a staff of 4 FT and 4 PT (6 FTE) Existing work might be reallocated to save 1 PTE position Maintenance & Utility costs would be reduced by combining into 1 facility Potential to put Village Hall back on tax roll Increase Revenues Estimated Potential Cost Savings = $33,000 Potential new tax revenue = $9,000 19

42 Street Maintenance Current Village Operations = $1.1 Million Personnel: 1 Superintendent, 1 Deputy Superintendent, 7 FTE MEO s and 1 PT Custodian Services Included in $1.1 Million Cost Street Administration, Street Maintenance Operations, Snow Removal, Street Lighting, CHIPS, Sidewalks, Allocated Benefits 20

43 Shared Services Approach Street Maintenance Village could stop providing street maintenance services and arrange for the Town to provide those services to the Village Could move all operations for highway maintenance, snow removal, sidewalks, street lighting, and refuse collection Would include all staff associated with those operations Results in significant cost shifts, but potentially no cost savings Likely retain both facilities could combine into a new facility Town may inherit union in the transition process 21

44 Police Department Current Operation = $1.35 Million 1 Chief, 5 Sergeants (1 Investigator), 6 Patrol, 1 Secretarial Support Primary Activities Community Service Policing = 54% Criminal/Penal Law Activity = 36% Other Activities = 10% Based on miles driven, every street is patrolled 2 times per day on average. 22

45 Shared Services Approach Police Village Could Dissolve the Police Department Police could become a Town Department Requires separate vote to dissolve the Department Assumes all costs of current operation shift to Town Village and/or Town could pursue options to have Sheriff provide police services 23

46 Homeowner Tax Impact Example - Police Assume Police become a Town service under a Shared Services Agreement: Cost Savings Projection = $0 Tax Shift Projection: Village tax bill goes down = $6.57/$1000 If NO Excess Revenue is used: Town tax bill goes up = $3.65/$1000 If $750,000 Excess Revenue is used: Town tax bill goes up = $1.62/$

47 Village Dispatch 25 Current Operation = $150,000 for 3 dispatch personnel not including OT for Sergeants and Patrol Officers 24x7 coverage includes overtime for sergeants or officers that cover shifts currently not maintained by dispatch personnel Dispatch personnel provide additional clerical support Creates double taxation because of County 911

48 Shared Services Approach Village Dispatch 26 Village discontinue Dispatch services Discontinuing dispatch makes County 911 responsible Village personnel might shift to County 911 Village could re-assign some dispatch personnel within other Village operations Could result in $150,000 in savings to Village residents Discontinuation of Village Dispatch is also a viable option for dissolution consideration

49 Refuse Collection Village Refuse Collection = $139,000 Town Refuse District = $34,000 Combined Operation under Town Highway Department could range from $173,000 - $200,000 to pick up all residents Current Village Customers = 2250 Additional Potential Town Customers =

50 Shared Services Approach Refuse Collection 28 Current Town Refuse District may be eliminated in favor of creating a town-wide refuse collection service under the direction of the Highway Dept. Town would buy garbage truck from Village and hire Village staff to operate townwide collection service. Town could contract with Village to provide townwide refuse collection service Represents a potential cost shift likely no cost savings but potential operational efficiencies

51 Water & Sewer - A Water Budget = $1.6 Million Sewer Budget = $1.5 Million Customers Inside Village = 2619 Customers Outside Village = 913 Personnel: 1 Superintendent, 1 Deputy Superintendent 5 Plant Operators, 2 Maintenance Mechanics, 4 Maintainers, 2 PT Laborers 29

52 Water & Sewer - B Many examples around the state where Towns run Water and Sewer operations Current districts could be maintained and operated at the Town level Could equalize the rates to offset some cost shifts incurred in the process If operation is transferred to Town Highway Supervisor, could save $93,000 in personnel cost 30

53 Visitor Center Transfer Operation to Town = $66,000 Visitor Center must be maintained through 2013 Town could operate and assume cost with a legally binding Inter-municipal Agreement or extension of Heritage Area Borders 31

54 Historic Preservation District Issues (A) Three Historic Designations 1. Historic Preservation District (HPD) & National Park are listed on the National Register of Historic Places 2. A portion of the Village is a State designated Heritage Area 3. HPD also qualifies as a Certified Local Government 32

55 Historic Preservation District Issues (B) National Register can be updated through administrative notification and name change Heritage Area and Visitor Center would involve working with the State to update Management Plan and transfer operation to Town CLG status can be transferred, but may not be necessary 33

56 Summary of Major Shared Services Approaches A combined municipal facility could save 1 PT staff person in General and Administrative services Current Village Hall and Current Town Hall could be sold to generate future tax revenue Street maintenance services could be transferred to the Town and provided to the village 34

57 Summary of Major Shared Services Approaches (2) 35 Police services could be transferred to the Town (Pending a referendum to dissolve the police department) Dispatch services could be transferred to County 911 Historic Preservation District can be managed by the Town Water and Sewer could be transferred to the Town

58 Village Dissolution Considerations A Closer Look at Functional Services 36

59 Dissolution Considerations: General and Administration (A) 37 Current Village Operation = $450,000 Cost Savings = $150,000 What Goes Away? 1 FT Administrator, Village Board, Mayor, Engineer Contract, Grant Writing Contract, Auditors, Village Hall Maintenance & Utilities, Miscellaneous Other Administration Transfers to Town = $300,000 What Transfers? 1 FT and 2 PT staff plus benefits, Maintenance & Utilities on Central Garage, Insurance Costs and Miscellaneous Other costs. Assumes a contingency for legal and other staff costs.

60 Dissolution Considerations: General and Administration (B) Personnel Savings One FTE position No need for a Village Administrator Would also save on the cost of the Village Mayor & Board, Engineers, Grant Writing, Auditors, Other Items including Maintenance & Utility Costs Estimated Potential Cost Savings = $150,000 Potential new tax revenue = $9,000 38

61 Dissolution Considerations: General and Administration (C) Dissolution Combined Tax Levy Impact = $159,000 Savings G&A that Transfers to Town = $300,000 Hypothetical Town Taxpayer would see an increase in annual Town tax of $81 for a house assessed at $100,000 Hypothetical Former Village Taxpayer would see a reduction of $217 for a house assessed at $100,000 because they would no longer pay a Village tax. 39

62 Dissolution Considerations: Police Department Option Create a Town-wide Department Maintain local control by Town Government Distribute costs to the whole Town Coverage would be for whole Town Assume coverage in whole Town would remain the same At the size of the current Village Police Department: Village taxpayer reduction = $6.57/$1000 Town-wide taxpayer Increase = $3.65/$1000 Pursue Options with Sheriff 40

63 Dissolution Considerations: Street Maintenance All village transportation services can be absorbed into the Town budget and operated by the Town Highway Department by transferring existing Village personnel to the Town. Would not need to transfer 1 FTE Supervisory Role Savings = $93,000 Town may inherit Union in the transition process Street Lighting and Sidewalks could become special taxing districts for former Village residents CHIP s funding would remain the same 41

64 Dissolution Considerations: Fire Department Fire Department = $108,000 All staff minimally paid by stipend 7 Command Staff 19 Firefighters plus 4 vacancies Village Department could separately incorporate and Town could contract with new entity for Fire Protection Services of the same portion of the Town currently being serviced by the Village. 42

65 Dissolution Considerations: Zoning & Code Enforcement Combine Zoning and Code Enforcement Function at the Town Level Plans Already Underway Combined Planning and Zoning Board of Appeals Maintain Historic Preservation Commission 43

66 Dissolution Considerations: Other Services 44 All other services could be maintained by the Town with the potential for some operational efficiencies. Storm Sewers = $13,000 Economic Development = $30,000 Cemetery Maintenance = $34,000 Culture & Recreation = $66,000 Public Health = $4,000 Retiree Health Insurance = $40,000

67 Dissolution Considerations: Debt Current Village General Fund Debt = $2 Million Current Village General Fund Balance approximately = $1.65 Million Combination of selling buildings and liquidating General Fund Balance could mitigate debt that remains after dissolution. Who is responsible for Village General Fund Debt would be decided as part of dissolution plan 45

68 Dissolution Considerations Village Assets Current Village Facilities Ownership would transfer to the Town and some could be sold Village Equipment Ownership would transfer to the Town and some could be sold Village Owned Property All ownership would transfer to the Town Any assets sold prior to dissolution could pay down current general fund debt 46

69 Revenue Considerations Revenue Considerations Relating to Dissolution 47

70 Revenue Impact 48 All State sources of Village non-property tax revenue would transfer to the Town except: Utilities Gross Receipts Tax = $85,000 Telephone Commissions = $0 in the Village Largest Impact from AIM Incentive $495,000 in NEW Money to the Community Would only lose grant opportunities if Certified Local Government Status was abandoned (Note: All revenue considerations are CGR s best current estimate but are not guaranteed)

71 Aid & Incentives for Municipalities (AIM) Considerations NYS added dissolution incentives to the FY 2008 budget to encourage municipal consolidation. In FY 2009 NYS increased the AIM incentive further by adding new, more lucrative formulas. The most lucrative formula bases the incentive on tax levies in both the Town and Village. This best case for Seneca Falls is new AIM funding that generates $495,000 to $506,000 in new revenue to the community. 49

72 Aid & Incentives for Municipalities (AIM) Impact Estimated total AIM received by new consolidated Town in Year 1 = $655, Town AIM = $100, Village AIM = $60,543 Additional AIM = $495,000 Year 1 becomes the baseline for all future AIM payments & increases Increases can range from 3-9% annually 50

73 New Model Town Model After Village Dissolution 51

74 Current Budgets Current 2008 Town Budget = $5.6 Million Town Special Districts Budgets = $646,000 Current Village General Fund Budget = $4.1 Million Current Water Budget = $1.6 Million Current Sewer Budget = $1.5 Million Combined Current Budgets = $13.5 Million 52

75 Potential Savings Potential Savings from dissolution of the Village = $393,000 G & A Savings = $150,000 Police = $0 (assumes Townwide department at current operational capacity) Dispatch = $150,000 DPW = $93,000 53

76 Potential Revenue Changes $495,000 in new AIM funding Additional annual aid equal to 15 percent of the combined property tax levy, capped at $1 million annually. New AIM funds projected to increase annually. Facilities Tax Revenue (if sold) = $20,000 Loss of Utilities Gross Receipts = ($85,000) Net Potential Revenue Changes = $430,000 54

77 Tax Levy Impact - Baseline Current Town Tax Levy = $75,478 TOV Tax Rate = $.46/$1000 Current Village Tax Levy = $3,299,091 Village Tax Rate = $16.048/$1000 Combined 2008 Village & Town Tax Levy = $3,374,519 55

78 Tax Impact New Tax Levy 56 Proposed New Townwide Tax Levy = $2,623,417 New Townwide Tax Rate = $7.09/$1000 Components of Levy Changes Move general fund debt service to special district for former Village residents Create lighting and sidewalk special districts for former Village residents Eliminate some G & A and dispatch Accounts for shifts in salaries and benefits between funds Eliminate one-time expenses Remove Utilities Gross Receipts Tax Revenue

79 Tax Impact: Additional Revenue Tax Levy reduced with additional AIM New Tax Levy with AIM = $2,128,417 New Townwide Tax Rate = $5.75/$1000 Tax Levy reduced further if future Excess Revenue (ER) is applied to levy: New Tax Levy with $750,000 ER = $1,378,417 New Townwide Tax Rate = $3.73/$

80 Tax Impact Estimates Tax savings estimates have a wide range Estimates depend on various public policy decisions that need to be made by the boards: How much of the Village and Town Fund Balances to use How much of the town Excess Revenue to use 58

81 Homeowner Tax Impact With Dissolution IF consolidated Town applies $750,000 ER to resulting Town tax levy and keeps service levels the same For a House Assessed at $100,000 Current Village property tax bill is reduced by $1600 per year Tax bill increase for Village residents due to special districts and current debt level = $249 Townwide taxpayer bill would increase $373 per year Net Savings to Village taxpayer = $978 59

82 Summary of Dissolution of the Village Village taxpayer savings are projected to be $978 annually on a typical house with a taxable assessed value of $100,000 Consolidated Town Taxes are projected to be $373 on a typical house with a taxable assessed value of $100,000 Impact on Former Village and TOV taxpayers could be reduced further depending on use of fund balances 60

83 Conclusion 61 Compared to many other communities, Seneca Falls has the following competitive advantages: It is a full service community with a vibrant village core. It has a large and predictable revenue stream It has plans to provide public water to the entire town at low cost It is located in the prime Finger Lakes Region It has a world class marketing brand as the home of the Women s Rights movement

84 Next Step Options Town and Village could conduct a scientifically valid survey to determine the will of the people in relation to Dissolution or Shared Services Town and Village Boards could conduct joint hearings to implement shared service options Village leaders and/or citizens could initiate steps to develop a dissolution plan to be put before the voters 62

85 2. Town Report on Joint Facility

86

87

88 Seneca Falls, New York Proposed New Town Hall, Village Hall, Police and Court Facility Barton & Loguidice Engineers PC Space Planning - April 28, 2008 TOWN OFFICE'S Town Clerk's Office Zoning Office Safe Storage Town Board Office Supervisor's Office Payroll Office Workroom/Conference Assessor's Office Reception/Waiting Open Office Open Office Meeting/Conference Active File Storage Subtotal AREA (SF) ,027 Notations 2 people adjacent to town clerk's office 2 safes - 80 to 100 sf requested make 12 x 12' make 12 x 12' space for supervisor and payroll meetings possibly just a row of chairs possible future employee requested for private discussions with public VILLAGE OFFICE'S Village Administrator Village Deputy Clerk Mayor's Office Councilmen's/Trustee's Office Codes Enforcement/Zoning Economic Developer Water Program Workroom/Conference Mailroom/Fax/Copier Safe Storage Active File Storage Subtotal AREA (SF) ,442 added space not a village function, space still req'd separate storage for village files only COMMON VILLAGE & TOWN SPACES Employee Toilets (men) Employee Toilets (women) Office Supplies/Cleaning Public Toilet (men) Public Toilet (women) Kitchen/Breakroom Fax/Copier/Mailroom Main Entrance/Reception Building Utilities Subtotal AREA (SF) ,395 COMMON VILLAGE, TOWN & COURT SPACES AREA (SF) Fire Rated/Climate Controlled Record Storage Town 800 Village 500 Court 400 Subtotal 1,700 climate controlled, secure from other files climate controlled, secure from other files climate controlled, secure from other files

89 VILLAGE POLICE Police Public Entrance Waiting Secretary Supply Room Public Toilet (men) Public Toilet (women) Chief's Office Chief's Storage Sargent's Office Main Records Command Center J. D. Room Evidence Tech Room Evidence Storage Patrol Office Interview Room #1 Interview Room #2 Investigator's Office Storage Men's Shower/Toilet Men's Lockers Women's Shower/Toilet Women's Lockers Garage/Salleyport Dispatch Dispatch Waiting Dispatch Kitchenette Booking Cell #1 Cell #2 Cell #3 Subtotal AREA (SF) , ,876 separate police entrance requested conference table, soundproof files, armor, safe, weapons 12' x 12', added space training out of main flow, interview/holding/safe haven tech room requested, added space high ceilings, 12' shelving 3-4 workstations soundproof, i.d. window, no finishes soundproof, i.d. window, no finishes ivestigator to be able to talk w/2 people 2 showers requested 11 people 1 shower requested 4 people 2 cars, entry into booking area, near dispatch generator power req'd COURT FACILITIES Courtroom Judge's Office Judge's Entrance Chief Clerk's Office Open Office/Conference (16-18 yr. Olds) Employee Toilet (men) Employee Toilet (women) Drug Court Drug Testing Toilet Jury Room Attorney/Client Attorney/Client Public Toilets (men) Public Toilets (women) Main Courtroom Entrance/Lobby Subtotal AREA (SF) 1, ,306 design for 150 people, 1600 sf min. near courtroom 2 peoplenormally, safe, copier next to courtroom & judge's/conference need dedicated toilet for testing 2 people, next to & dedicated for drug court holds 7-8 jurors, added space added space

90 COMMON POLICE & COURT SPACES Kitchen/Break Room Holding Area Holding Area (16-18 yr. olds) Building Utilities Subtotal AREA (SF) , people separate area for yr. Olds Town Office's 2,027 Village Office's 2,442 Common Town & Village Spaces 2,395 Common Town, Village & Court Spaces 1,700 Village Police 6,876 Court Facilities Common Police & Court Spaces Subtotal Public Circulation Space Subtotal Wall Construction Total Proposed Building Area 4,306 1,270 21,015 15% 3,152 24,167 7% 1,692 25,859

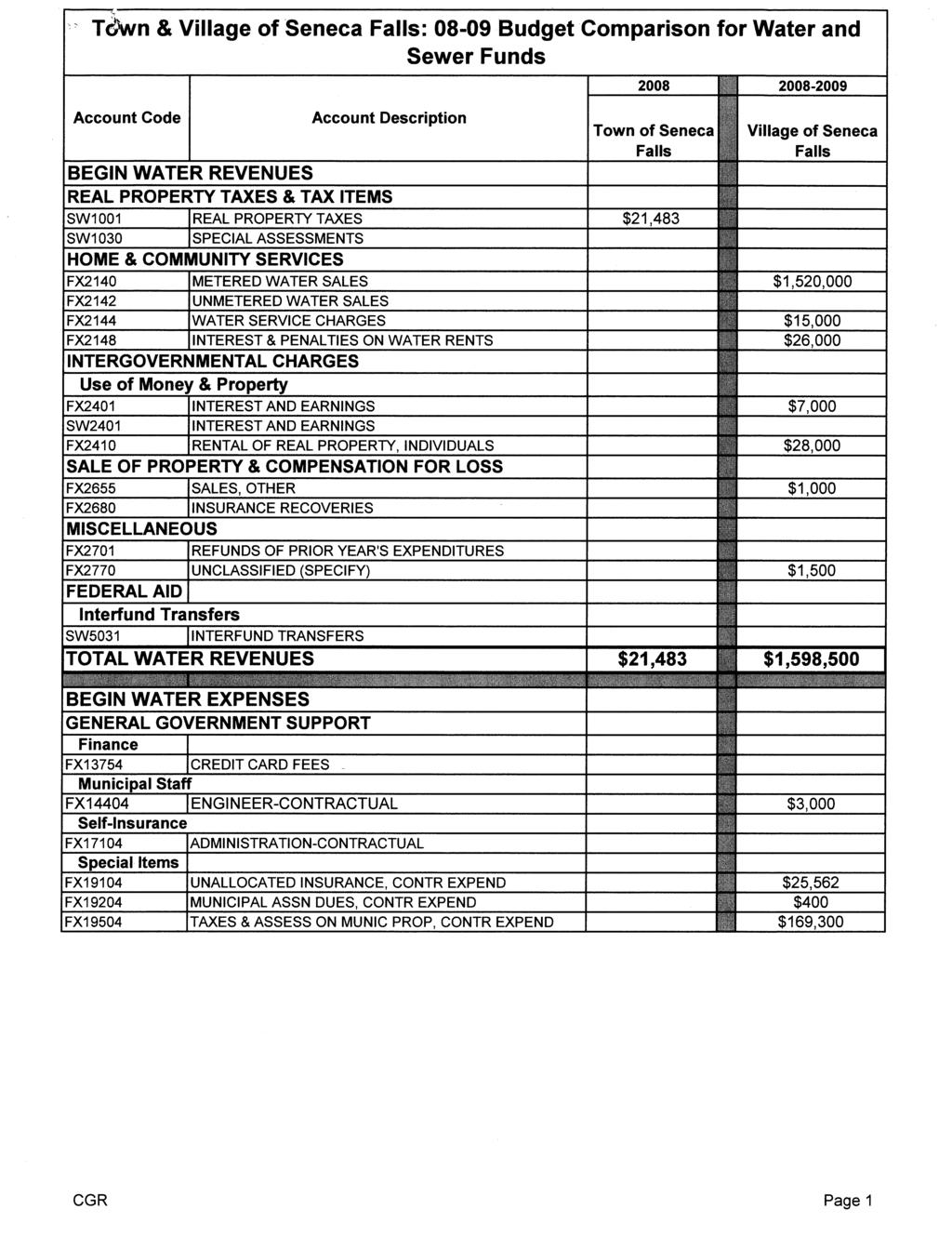

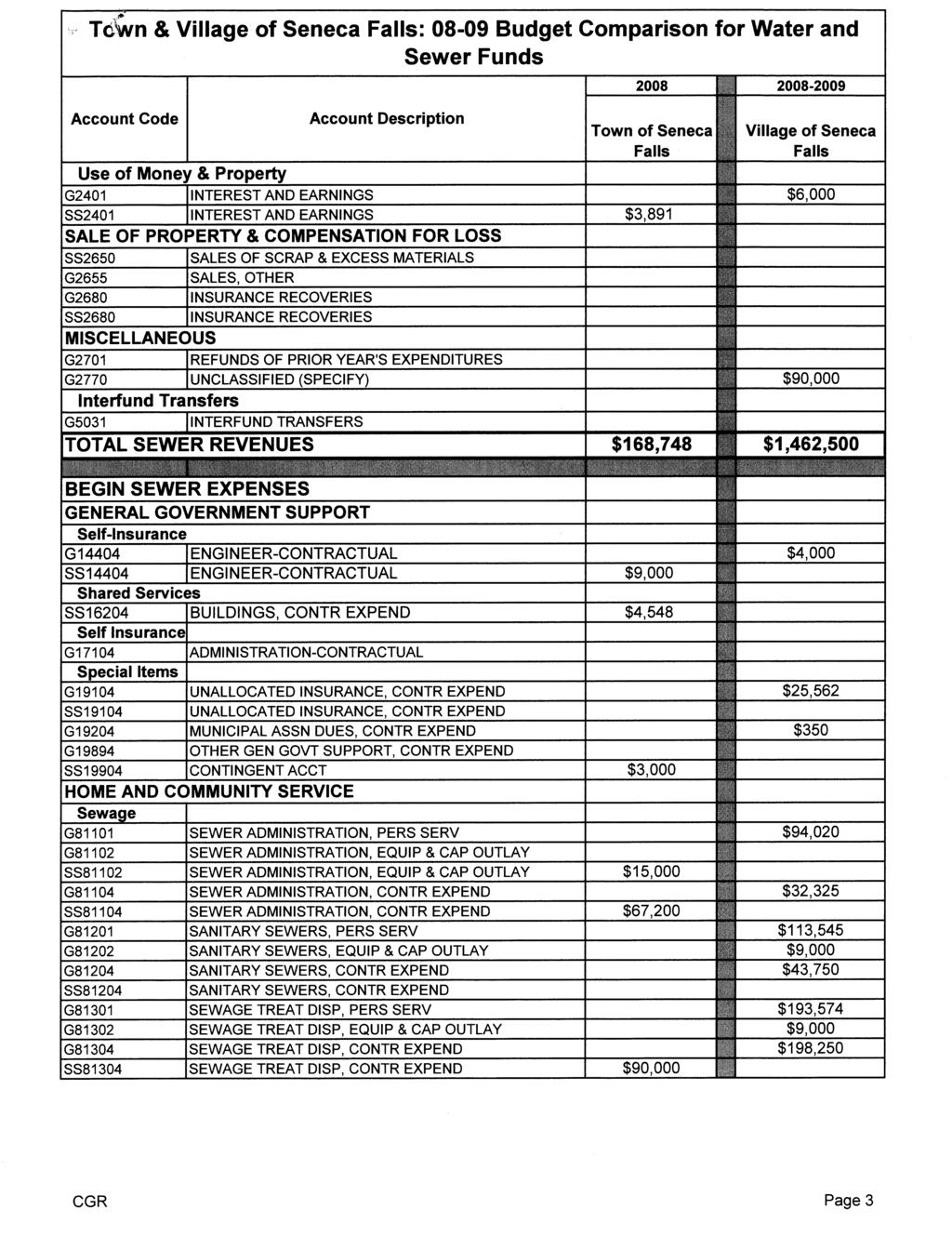

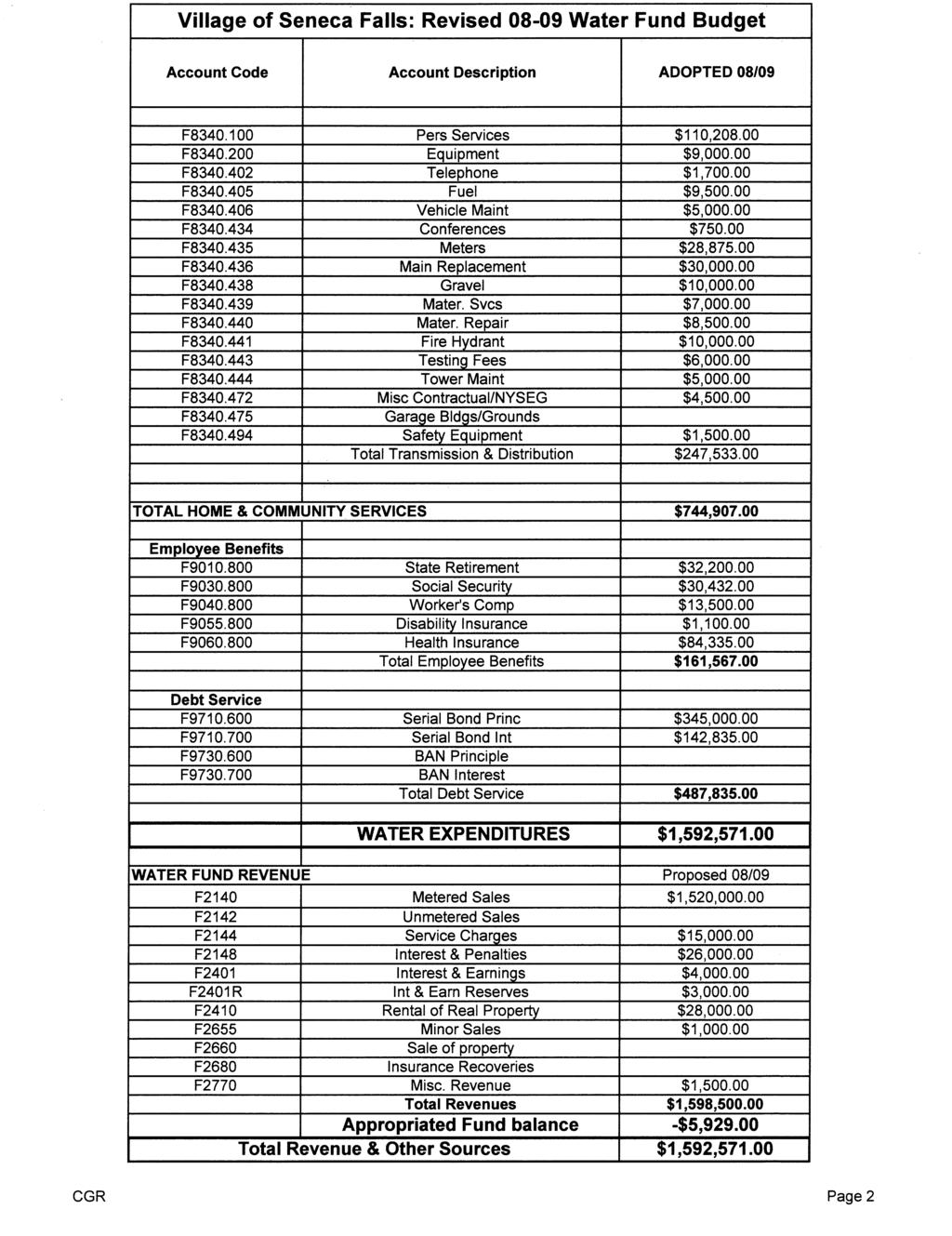

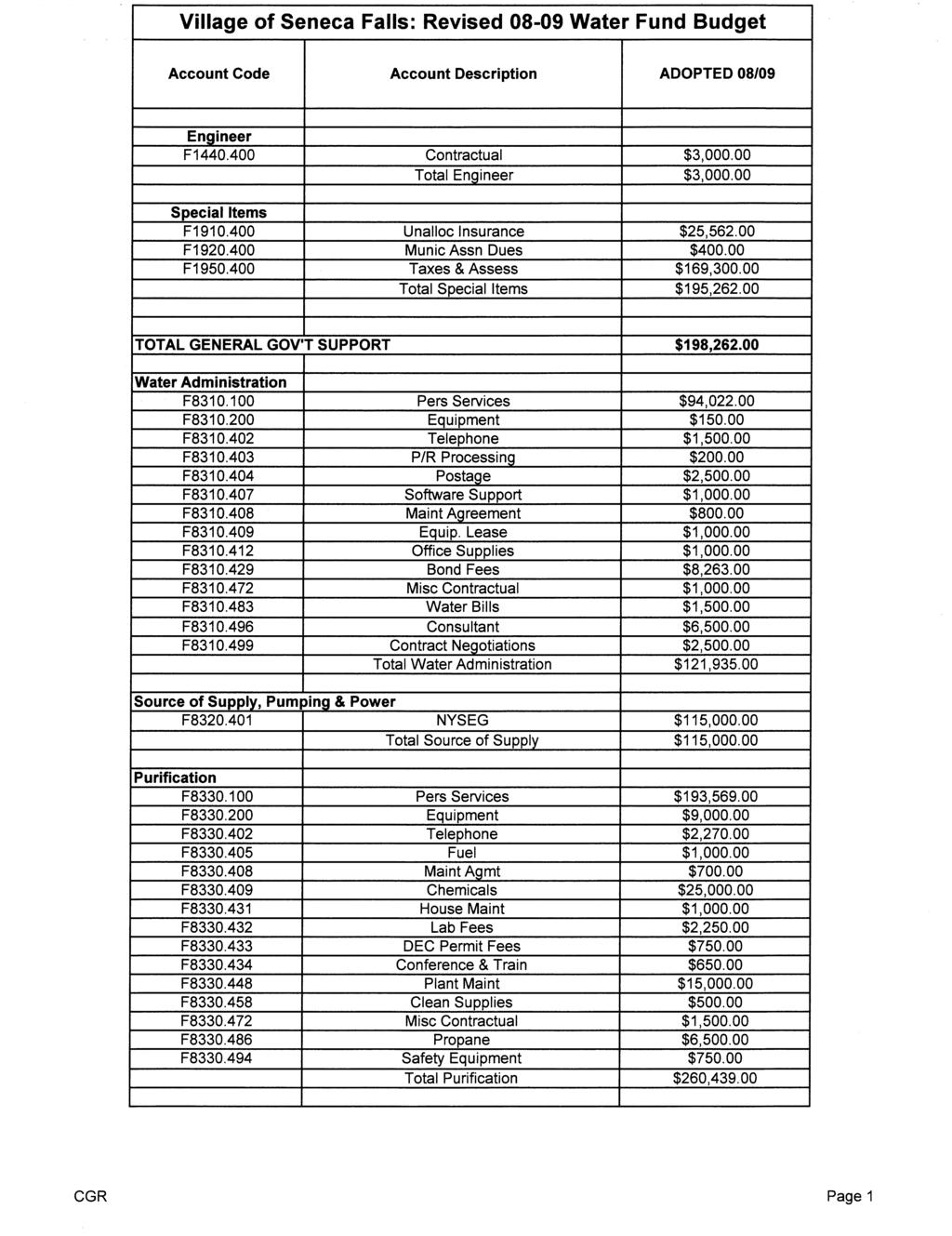

91 3. Municipal Budgets CGR has included a crosswalk of Village and Town budgets for the Town Fiscal Year 2008 and Village Fiscal Year The Village numbers on this crosswalk were part of the original budget. Subsequent to our analysis, the Village amended their budget and we included the amended budget as a separate attachment in this appendix.

92 Town & Village of Seneca Falls: Budget Comparison for General, Highway, Fire, Lighting, Parks, and Refuse Funds Account Code Account Description 2008 Town of Seneca Falls Village of Seneca Falls BEGIN A, B, DA, DB, SF, SL, SP, SR FUND REVENUES REAL PROPERTY TAXES & TAX ITEMS A1001 REAL PROPERTY TAXES $3,299,041 B1001 REAL PROPERTY TAXES DB1001 REAL PROPERTY TAXES $75,478 SF1001 REAL PROPERTY TAXES $271,473 SL1001 REAL PROPERTY TAXES $2,750 SR1001 REAL PROPERTY TAXES $33,188 TOTAL $382,889 $3,299,041 A1081 OTHER PAYMENTS IN LIEU OF TAXES $3,500 $54,500 DB1081 OTHER PAYMENTS IN LIEU OF TAXES TOTAL $3,500 $54,500 A1090 INTEREST & PENALTIES ON REAL PROP TAXES $5,000 $31,000 TOTAL $5,000 $31,000 Subtotal REAL PROPERTY TAXES & TAX ITEMS $391,389 $3,384,541 NON-PROPERTY TAXES A1130 UTILITIES GROSS RECEIPTS TAX $750 $85,000 TOTAL $750 $85,000 A1170 FRANCHISES $51,000 TOTAL $51,000 Subtotal NON-PROPERTY TAXES $750 $136,000 DEPARTMENTAL INCOME General Government A1230 TREASURER FEES $700 TOTAL $700 A1235 CHARGES FOR TAX REDEMPTION TOTAL A1255 CLERK FEES $2,000 $100 TOTAL $2,000 $100 Subtotal General Government $2,000 $800 Public Safety A1550 PUBLIC POUND CHARGES, DOG CONTROL FEES $1,000 TOTAL $1,000 Health A1601 PUBLIC HEALTH FEES TOTAL A1603 VITAL STATISTICS FEES $2,000 B1603 VITAL STATISTICS FEES $500 TOTAL $500 $2,000 Subtotal Health $500 $2,000 Transportation A1710 PUBLIC WORKS CHARGES $1,000 TOTAL $1,000 Subtotal DEPARTMENTAL INCOME $3,500 $3,800 CGR Page 1

93 Town & Village of Seneca Falls: Budget Comparison for General, Highway, Fire, Lighting, Parks, and Refuse Funds 2008 Account Code Account Description Town of Seneca Falls CULTURE & RECREATION A2001 PARK AND RECREATIONAL CHARGES SP2001 PARK AND RECREATIONAL CHARGES TOTAL A2012 RECREATIONAL CONCESSIONS SP2012 RECREATIONAL CONCESSIONS $1,000 TOTAL $1,000 SP2025 SPECIAL RECREATIONAL FACILITY CHARGES $6,000 TOTAL $6,000 SP2089 OTHER CULTURE & RECREATION INCOME $4,000 TOTAL $4, Village of Seneca Falls Subtotal CULTURE & RECREATION $11,000 HOME & COMMUNITY SERVICES A2110 ZONING FEES $100 B2110 ZONING FEES $1,500 TOTAL $1,500 $100 A2122 SEWER CHARGES $11,338 TOTAL $11,338 A2130 REFUSE & GARBAGE CHARGES $2,600,000 B2130 REFUSE & GARBAGE CHARGES $35,000 TOTAL $2,635,000 A2189 OTHER HOME & COMMUNITY SERVICES INCOME $2,500 TOTAL $2,500 A2190 SALE OF CEMETERY LOTS TOTAL A2192 CHARGES FOR CEMETERY SERVICES $10,000 TOTAL $10,000 Subtotal HOME & COMMUNITY SERVICES $2,650,338 $10,100 INTERGOVERNMENTAL CHARGES General A2210 GENERAL SERVICES, INTER GOVERNMENT $10,000 TOTAL $10,000 Public Safety A2262 FIRE PROTECTION SERVICES OTHER GOVTS $35,000 TOTAL $35,000 Transportation DA2300 TRANSPORTATION SERVICES, OTHER GOVTS $12,000 DA2302 SNOW REMOVAL SERVICES-OTHER GOVTS TOTAL $12,000 CGR Page 2

94 Town & Village of Seneca Falls: Budget Comparison for General, Highway, Fire, Lighting, Parks, and Refuse Funds Account Code Account Description 2008 Town of Seneca Falls Village of Seneca Falls Use of Money & Property A2401 INTEREST AND EARNINGS $95,000 $86,000 B2401 INTEREST AND EARNINGS $2,000 DA2401 INTEREST AND EARNINGS $5,500 DB2401 INTEREST AND EARNINGS $5,000 SL2401 INTEREST AND EARNINGS $100 SP2401 INTEREST AND EARNINGS $4,000 SR2401 INTEREST AND EARNINGS $532 TOTAL $112,132 $86,000 A2410 RENTAL OF REAL PROPERTY SP2410 RENTAL OF REAL PROPERTY, INDIVIDUALS $8,500 TOTAL $8,500 A2450 COMMISSIONS $50 TOTAL $50 Subtotal Use of Money & Property $120,632 $86,050 Subtotal INTERGOVERNMENTAL CHARGES $142,632 $121,050 LICENSES & PERMITS A2530 GAMES OF CHANCE $200 TOTAL $200 A2544 DOG LICENSES $3,000 TOTAL $3,000 B2545 LICENSES, OTHER $100 TOTAL $100 B2555 BUILDING AND ALTERATION PERMITS $3,000 TOTAL $3,000 A2590 PERMITS, OTHER $1,800 B2590 PERMITS, OTHER $370 SP2590 PERMITS, OTHER $1,500 TOTAL $1,870 $1,800 Subtotal LICENSES & PERMITS $7,970 $2,000 FINES & FORFEITURES A2610 FINES AND FORFEITED BAIL $80,000 $8,000 TOTAL $80,000 $8,000 Subtotal FINES & FORFEITURES $80,000 $8,000 SALE OF PROPERTY & COMPENSATION FOR LOSS A2655 SALES, OTHER $1,000 DA2655 SALES, OTHER TOTAL $1,000 Subtotal SALE OF PROPERTY & COMPENSATION FOR LOSS $1,000 MISCELLANEOUS A2770 UNCLASSIFIED (SPECIFY) $250 $3,000 B2770 UNCLASSIFIED (SPECIFY) $100 DA2770 UNCLASSIFIED (SPECIFY) SF2770 UNCLASSIFIED (SPECIFY) SP2770 UNCLASSIFIED (SPECIFY) TOTAL $350 $3,000 Subtotal MISCELLANEOUS $350 $3,000 CGR Page 3

95 Town & Village of Seneca Falls: Budget Comparison for General, Highway, Fire, Lighting, Parks, and Refuse Funds Account Code Account Description 2008 Town of Seneca Falls Village of Seneca Falls STATE AID General Government A3001 ST AID, REVENUE SHARING $73,032 $60,543 TOTAL $73,032 $60,543 A3005 ST AID, MORTGAGE TAX $50,000 $25,000 TOTAL $50,000 $25,000 A3089 ST AID - OTHER (SPECIFY) $160,000 B3089 ST AID, OTHER AID (SPECIFY) $478 TOTAL $160,478 Subtotal General Government $283,510 $85,543 Transportation A3501 ST AID, CONSOLIDATED HIGHWAY AID $123,000 DB3501 ST AID, CONSOLIDATED HIGHWAY AID $25,000 TOTAL $25,000 $123,000 Culture & Recreation A3820 ST AID, YOUTH PROGRAMS $2,700 TOTAL $2,700 A3845 ST AID, MUSEUMS TOTAL Subtotal Culture & Recreation $2,700 Subtotal STATE AID $308,510 $211,243 FEDERAL AID Interfund Transfers A5031 INTERFUND TRANSFERS DA5031 INTERFUND TRANSFERS $88,550 DB5031 INTERFUND TRANSFERS $90,000 SP5031 INTERFUND TRANSFERS $75,000 TOTAL $253,550 Subtotal FEDERAL AID $253,550 TOTAL A, B, DA, DB, SF, SL, SP, SR FUND REVENUES $3,849,989 $3,880,734 BEGIN A, B, DA, DB, SF, SL, SP, SR FUND EXPENSES GENERAL GOVERNMENT SUPPORT Legislative A10101 LEGISLATIVE BOARD, PERS SERV $62,785 $19,600 A10102 LEGISLATIVE BOARD, EQUIP & CAP OUTLAY $5,500 A10104 LEGISLATIVE BOARD, CONTR EXPEND $70,065 $6,000 Subtotal Legislative $138,350 $25,600 Judicial A11101 MUNICIPAL COURT, PERS SERV $94,772 A11102 MUNICIPAL COURT, EQUIP & CAP OUTLAY $5,000 A11104 MUNICIPAL COURT, CONTR EXPEND $30,770 A11111 DRUG COURT, PERS SERV $15,440 A11114 DRUG COURT, CONTR EXPEND $3,500 Subtotal Judicial $149,482 CGR Page 4

96 Town & Village of Seneca Falls: Budget Comparison for General, Highway, Fire, Lighting, Parks, and Refuse Funds Account Code Account Description 2008 Town of Seneca Falls Village of Seneca Falls Executive A12101 MAYOR, PERS SERV $6,157 A12104 MAYOR, CONTR EXPEND $5,000 A12201 SUPERVISOR,PERS SERV $8,050 A12202 SUPERVISOR,EQUIP & CAP OUTLAY $2,000 A12204 SUPERVISOR,CONTR EXPEND $7,050 Subtotal Executive $17,100 $11,157 Finance A13204 AUDITOR, CONTR EXPEND $17,000 A13251 TREASURER, PERS SERV $84,770 A13252 TREASURER, EQUIP & CAP OUTLAY $1,000 A13254 TREASURER, CONTR EXPEND $68,075 A13301 TAX COLLECTION,PERS SERV $6,150 A13302 TAX COLLECTION,EQUIP & CAP OUTLAY $1,000 A13304 TAX COLLECTION,CONTR EXPEND $6,550 A13554 ASSESSMENT, CONTR EXPEND $78,121 A13624 TAX ADVERTISING, CONTR EXPEND $1,650 Subtotal Finance $108,821 $155,495 Municipal Staff A14101 CLERK,PERS SERV $79,692 A14102 CLERK,EQUIP & CAP OUTLAY $2,000 A14104 CLERK,CONTR EXPEND $5,700 A14204 LAW, CONTR EXPEND $30,000 $57,400 B14204 LAW, CONTR EXPEND $15,000 A14404 ENGINEER, CONTR EXPEND $77,000 $15,000 B14404 ENGINEER, CONTR EXPEND $12,500 A14504 ELECTIONS, CONTR EXPEND $18,000 $500 A14601 RECORDS MGMT, PERS. SERV. $300 Subtotal Municipal Staff $240,192 $72,900 Shared Services A16201 BUILDINGS, PERS SERV $30,333 A16202 BUILDINGS, EQUIP & CAP OUTLAY $500 A16204 BUILDINGS, CONTR EXPEND $98,300 $17,200 A16402 CENTRAL GARAGE, EQUIP & CAP OUTLAY $2,000 A16404 CENTRAL GARAGE, CONTR EXPEND $19,500 A16802 CENTRAL DATA PROCESS & CAP OUTLAY $4,000 A16804 CENTRAL DATA PROCESS, CONTR EXPEND $17,500 Subtotal Shared Services $150,633 $38,700 Special Items A19104 UNALLOCATED INSURANCE, CONTR EXPEND $75,000 $99,238 A19204 MUNICIPAL ASSN DUES, CONTR EXPEND $3,800 A19904 CONTINGENT ACCT $100,000 $5,000 B19904 CONTINGENT ACCT $10,470 SP19904 CONTINGENT ACCT $15,000 Subtotal Special Items $200,470 $108,038 Subtotal GENERAL GOVERNMENT SUPPORT $1,005,048 $411,890 PUBLIC SAFETY Law Enforcement A31201 POLICE, PERS SERV $950,945 A31202 POLICE, EQUIP & CAP OUTLAY $4,500 A31204 POLICE, CONTR EXPEND $80,000 A31891 OTHER TRAFFIC, PERS SERV $5,762 A31894 OTHER TRAFFIC, CONTR EXPEND $500 CGR Page 5

97 Town & Village of Seneca Falls: Budget Comparison for General, Highway, Fire, Lighting, Parks, and Refuse Funds Account Code Account Description Town of Seneca Falls Village of Seneca Falls Subtotal Law Enforcement $1,041,707 CGR Page 6

98 Town & Village of Seneca Falls: Budget Comparison for General, Highway, Fire, Lighting, Parks, and Refuse Funds Account Code Account Description 2008 Town of Seneca Falls Village of Seneca Falls Traffic Control A33104 TRAFFIC CONTROL, CONTR EXPEN $12,000 Subtotal Traffic Control $12,000 Fire Protection and Control A34101 FIRE, PERS SERV $32,379 A34102 FIRE, EQUIP & CAP OUTLAY $22,500 A34104 FIRE, CONTR EXPEND $42,140 B34104 REFLECTIVE NUMBERING, CONTR EXPEND $15,000 SF34104 FIRE PROTECTION, CONTR EXPEND $271,473 Subtotal Fire Protection and Control $286,473 $97,019 Animal Control A35101 CONTROL OF ANIMALS, PERS SERV $12,610 A35102 CONTROL OF ANIMALS, EQUIP & CAP OUTLAY $150 A35104 CONTROL OF ANIMALS, CONTR EXPEND $8,525 $4,000 A35204 OTHER ANIMAL CONTROL, CONTR EXPEND $2,500 Subtotal Animal Control $23,785 $4,000 Subtotal PUBLIC SAFETY $310,258 $1,154,726 HEALTH Public Health Programs A40201 REGISTRAR OF VITAL STATISTICS, PERS SERV $4,100 A40204 REGISTRAR OF VITAL STAT CONTR EXPEND $100 Subtotal Public Health Programs $4,200 Subtotal HEALTH $4,200 TRANSPORTATION Highway A50101 STREET ADMIN, PERS SERV $48,800 $20,630 A50102 STREET ADMIN, EQUIP & CAP OUTLAY $300 $500 A50104 STREET ADMIN, CONTR EXPEND $3,000 $490 A51101 MAINT OF STREETS, PERS SERV $391,081 DB51101 MAINT OF STREETS, PERS SERV $79,735 A51102 MAINT OF STREETS, EQUIP & CAP OUTLAY $18,000 A51104 MAINT OF STREETS, CONTR EXPEND $172,100 DB51104 MAINT OF STREETS, CONTR EXPEND $110,200 DA51302 MACHINERY, EQUIP & CAP OUTLAY $164,500 DA51304 MACHINERY, CONTR EXPEND $36,850 A51124 CHIPS $123,000 A51324 GARAGE, CONTR EXPEND $12,050 DA51421 SNOW REMOVAL, PERS SERV $16,000 A51422 SNOW REMOVAL, EQUIP & CAP OUTLAY $10,000 A51424 SNOW REMOVAL, CONTR EXPEND $40,200 DA51424 SNOW REMOVAL, CONTR EXPEND $10,000 A51822 STREET LIGHTING, EQUIP & CAP OUTLAY $1,000 A51824 STREET LIGHTING, CONTR EXPEND $14,000 $179,000 SL51824 STREET LIGHTING, CONTR EXPEND $2,850 A54104 SIDEWALKS, CONTR EXPEND $13,000 Subtotal Highway $498,285 $969,001 Subtotal TRANSPORTATION $498,285 $969,001 ECONOMIC OPPORTUNITY AND DEVELOPMENT Economic Opportunity and Development A69894 OTHER ECO & DEV, CONTR EXPEND $72,000 $30,000 Subtotal ECONOMIC OPPORTUNITY AND DEVELOPMENT $72,000 $30,000 CGR Page 7

99 Town & Village of Seneca Falls: Budget Comparison for General, Highway, Fire, Lighting, Parks, and Refuse Funds Account Code Account Description 2008 Town of Seneca Falls Village of Seneca Falls CULTURE AND RECREATION Recreation A71101 PARKS, PERS SERV $25,600 SP71101 PARKS, PERS SERV $28,000 A71102 PARKS, EQUIP & CAP OUTLAY $3,500 SP71102 PARKS, EQUIP & CAP OUTLAY $2,800 A71104 PARKS, CONTR EXPEND $37,350 SP71104 PARKS, CONTR EXPEND $42,550 SP71801 SPECIAL REC FACILITY, PERS SERV $25,000 SP71802 SPECIAL REC FACILITY, EQUIP & CAP OUTLAY $2,000 A71804 SPECIAL REC FACILITY, CONTR EXPEND $566,000 SP71804 SPECIAL REC FACILITY, CONTR EXPEND $7,450 A72704 BAND CONCERTS, CONTR EXPEND $1,750 Subtotal Recreation $675,550 $66,450 Culture A74104 LIBRARY, CONTR EXPEND $62,500 A74501 MUSEUM - ART GALLERY, PERS SERV $49,450 A74504 MUSEUM - ART GALLERY, CONTR EXPEND $16,550 A75101 HISTORIAN, PERS SERV $500 A75104 HISTORIAN, CONTR EXPEND $50 $500 A75204 HISTORICAL PROPERTY, CONTR EXPEND $7,000 A75504 CELEBRATIONS, CONTR EXPEND $17,500 Subtotal Culture $87,550 $66,500 Subtotal CULTURE AND RECREATION $763,100 $132,950 HOME AND COMMUNITY SERVICE General Environment A80101 ZONING, PERS SERV $8,656 B80101 ZONING, PERS SERV $9,250 A80104 ZONING, CONTR EXPEND $800 B80104 ZONING, CONTR EXPEND $5,300 B80201 PLANNING, PERS SERV $450 B80204 PLANNING, CONTR EXPEND $950 A80904 ENVIRONMENTAL CONTROL, CONTR EXPEND $20,000 Subtotal General Environment $35,950 $9,456 Sewage A81104 SEWER ADMINISTRATION, CONTR EXPEND $100,000 A81402 STORM SEWERS, EQUIP & CAP OUTLAY $1,000 A81404 STORM SEWERS, CONTR EXPEND $12,250 Subtotal Sewage $100,000 $13,250 Sanitation A81601 REFUSE & GARBAGE, PERS SERV $47,374 A81602 REFUSE & GARBAGE, EQUIP & CAP OUTLAY $39,900 A81604 REFUSE & GARBAGE, CONTR EXPEND $186,000 SR81604 REFUSE & GARBAGE, CONTR EXPEND $33,720 Subtotal Sanitation $33,720 $273,274 Water A83101 WATER ADMINISTRATION, PERS SERV $37,500 A83104 WATER ADMINISTRATION, CONTR EXPEND $227,000 Subtotal Water $264,500 Community Environment A85604 SHADE TREE, CONTR EXPEND $12,000 Subtotal Community Environment $12,000 CGR Page 8

100 Town & Village of Seneca Falls: Budget Comparison for General, Highway, Fire, Lighting, Parks, and Refuse Funds Account Code Account Description 2008 Town of Seneca Falls Village of Seneca Falls Special Services A88101 CEMETERY, PERS SERV $21,120 A88102 CEMETERY, EQUIP & CAP OUTLAY $1,000 $5,000 A88104 CEMETERY, CONTR EXPEND $1,000 $8,200 A89894 MISC HOME & COMM SERV, CONTR EXPEND $80,800 Subtotal Special Services $82,800 $34,320 Subtotal HOME AND COMMUNITY SERVICE $516,970 $342,300 UNDISTRIBUTED Employee Benefits A90108 STATE RETIREMENT SYSTEM $36,850 $72,500 B90108 STATE RETIREMENT, EMPL BNFTS $1,100 DB90108 STATE RETIREMENT, EMPL BNFTS $11,000 A90158 POLICE & FIREMEN RETIREMENT, EMPL BNFTS $130,000 A90308 SOCIAL SECURITY, EMPLOYER CONT $25,000 $127,573 B90308 SOCIAL SECURITY, EMPL BNFTS $750 DA90308 SOCIAL SECURITY, EMPL BNFTS $842 DB90308 SOCIAL SECURITY, EMPL BNFTS $6,800 SP90308 SOCIAL SECURITY, EMPL BNFTS $3,910 A90408 WORKER'S COMPENSATION, EMPL BNFTS $17,380 $52,515 B90408 WORKER'S COMPENSATION, EMPL BNFTS $300 DB90408 WORKER'S COMPENSATION, EMPL BNFTS $4,740 SP90408 WORKER'S COMPENSATION, EMPL BNFTS $350 A90508 UNEMPLOYMENT INSURANCE, EMPL BNFTS $5,000 DB90508 UNEMPLOYMENT INSURANCE, EMPL BNFTS $100 SP90508 UNEMPLOYMENT INSURANCE, EMPL BNFTS $1,000 A90558 DISABILITY INSURANCE, EMPL BNFTS $900 $2,600 DB90558 DISABILITY INSURANCE, EMPL BNFTS $200 A90608 HOSPITAL & MEDICAL (DENTAL) INS, EMPL BNFT $124,200 $322,071 DB90608 HOSPITAL & MEDICAL (DENTAL) INS, EMPL BNFT $41,300 Subtotal Employee Benefits $276,722 $712,259 Debt Service A97106 DEBT PRINCIPAL, SERIAL BONDS $110,000 A97107 DEBT INTEREST, SERIAL BONDS $96,444 A97856 INSTALL PUR DEBT, PRINCIPAL $107,118 A97857 INSTALL PUR DEBT, INTEREST $5,085 Subtotal Debt Service $318,647 Interfund Transfers A99019 TRANSFERS, OTHER FUNDS $768,550 B99019 TRANSFERS, OTHER FUNDS $90,000 A99509 TRANSFERS, CAPITAL PROJECTS FUND $750,000 Subtotal Interfund Transfers $1,608,550 Subtotal UNDISTRIBUTED $1,885,272 $1,030,906 TOTAL A, B, DA, DB, SF, SL, SP, SR EXPENSES $5,050,933 $4,075,973 CGR Page 9

101

102

103

104

105

106

107

108

109

110

111

112

113

114

115

116

117

118

119

120

121

122

123

124 4. Historical Designations and Alternatives in Dissolution of the Village