Appraisal Underwriting. Review of The Sales Comparison Approach October 2015

|

|

|

- Godwin Cobb

- 5 years ago

- Views:

Transcription

1 Appraisal Underwriting Review of October 2015 Genworth Mortgage Insurance Corporation 2015 Genworth Financial, Inc. All rights reserved.

2 Session Overview Participants will learn about analyzing the Uniform Residential Appraisal Report Sales Comparison Approach Review of the Sales Comparison Grid Reconciliation Common Errors, Red Flags and Best Practices Resources 2

3 Appraisal Basics The appraisal report provides: Detailed description of the property Condition and marketability information Market value Appraiser s opinion Supporting detail on how the appraiser arrived at the opinion Additional property issues/information Sales Comparison Grid providing sales of property similar in market appeal to the subject 3

4 Appraisal Basics Seller/Lender Responsibilities Selecting Appraiser Providing Appraiser With Sales Contract Other Available Information Underwriting the Appraisal Disclosing Required Information Ensuring the appraiser has requisite knowledge Page 5 4

5 Appraisal Basics Appraiser Responsibilities An accurate, adequately supported opinion of market value. An objective analysis of quantifiable data to support housing trends. All relevant information that supports the conclusions about market conditions, including: Sales/financing concessions. Down payment assistance. Days on market, list-to-sales price ratios, and availability of financing. Provide minimum of three comparable sales that are: Verified closed sales Similar to the subject or a market alternative Adjusted for based on market reaction Page 8 5

6 AGENCY UPDATES Fannie Mae & Freddie Mac 6

7 Freddie Mac Bulletin

8 Freddie Mac Bulletin

9 Freddie Mac (04/01/14) requirements General property eligibility : 44.2 We expect the Seller to place as much emphasis on the adequacy of the property as collateral as it does on underwriting the Borrower's creditworthiness. The conclusion that a Mortgage is acceptable to Freddie Mac must be based on the determination that the Borrower is creditworthy (acceptable credit reputation and capacity) and the Mortgaged Premises is adequate collateral for the Mortgage transaction. The Seller is responsible for determining the eligibility of the property and the acceptability of the appraisal report. 9

10 Freddie Mac (04/01/14) requirements General property eligibility : 44.2 a)residential ) requirements Freddie Mac will purchase eligible Mortgages secured by residential properties in urban, suburban and rural market areas as long as the Mortgaged Premises is adequate collateral for the Mortgage transaction based on the value, condition and marketability of the property. Freddie Mac does not purchase Mortgages secured by vacant or undeveloped land, land development properties or properties used primarily for agriculture, farming or commercial enterprise. The Mortgaged Premises must be residential based on the property characteristics, zoning and land use. The Mortgaged Premises must: Be safe, sound, habitable and undamaged by fire or windstorms or other perils Be complete unless the requirements of Section 44.2 (b) are met Meet all conditions of the appraisal if an appraisal was performed and made subject to conditions, unless the requirements of Section 44.2(b) are met Represent the highest and best use of the property as improved (or as proposed per plans and specifications) in accordance with Section 44.15(d) 10

11 Freddie Mac : 44.2 General property eligibility requirements (04/01/14) Have a legal or legal non-conforming use in accordance with Section 44.15(d) Have legal access (ingress and egress) Have year round access Have utilities that meet community standards Have mechanical systems that meet community standards Have property insurance coverage that meets Freddie Mac's requirements and coverage for hazards specific to the location of the property Not be subject to a pending legal proceeding for condemnation in whole or in part See Section for requirements on reviewing the appraisal report and underwriting the property. 11

12 Fannie Mae LL

13 SEL

14 B Fannie Mae Selling Guide 14

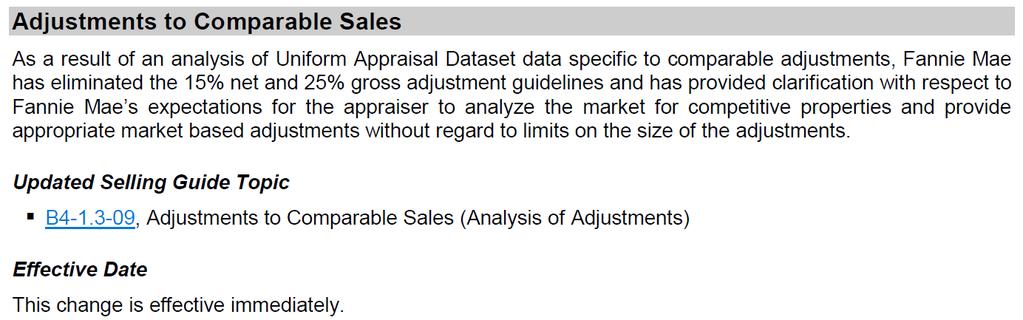

15 LL Appraisal Tools, Processes & Policies Collateral Underwriter (CU) Selling Guide Updates Adjustments to Comparable Sales 15

16 Sales Comparison Sales Grid, Adjustments, Reconciliation Page 32 16

17 Sales Comparison This Section Covers Analyzing Comparable Sales Selection Reading the Sales Comparison Grid Non-Value Adjustment Fields Value Adjustment Fields Reconciliation Sales/Transfer History Page 32 17

18 Analyzing Comparable Properties At Least Three Closed Sales More can be provided. Pending sales or listings: Can be used when appropriate. These might provide additional supporting data. Comparable s Closing Date (Age) Check applicable guidelines. Should have closed within the previous year. Must make sense for market. Recent sales offer measure of current market. Over twelve months: Effort made to find newer comparable. Why newer comparables not available. Is there a market issue? Basis for any market condition adjustment. Page 32 18

19 Analyzing Comparable Properties Shortage of Comparable Properties Possible Reasons: Nature of property improvements. Relatively low number of sale transactions in the neighborhood. Comparables may have to be: Older than a year. From a nearby, competing neighborhood. Appraiser Explanation and Market Data. Page 33 19

20 Analyzing Comparable Properties When there is a shortage of comps, the appraiser should explain: Effort made to find better comps? Why the shortage of recent sales? What does the shortage indicate? Stable market? Marketability issue? Shared unique characteristics? Why a potential comp was not selected? i.e. Foreclosure sale or non-arms length transaction. Page 33 20

21 Analyzing Comparable Properties Unacceptable Comparison Selection Practices Misrepresentation Inappropriate Comps Unacceptable Locationally Not Physically Similar Uninspected Properties No Appraiser Drive-By Page 34 21

22 Analyzing Comparable Properties Requirements Include: Same or Competing Market/Neighborhood Similar Factors Impacting Value Marketability issues. (Adjacent to dump) Functional obsolescence. (Only bathroom located through kitchen) Location issues. (Busy street) Unique features. (Swimming pool) Page 34 22

23 Analyzing Comparable Properties Review Appraisal Map Review Carefully Does the map support the Appraiser s Conclusions? Distances make sense? Natural boundaries honored? i.e. Waterways, Highways, Large Parks. Compare with other maps. Google Maps, MapQuest, etc. School maps. Municipality maps. Page 34 23

24 Analyzing Comparable Properties 24

25 Analyzing Comparable Properties How far (distance) can the appraiser go to find comparables? NO set distance rules. Distances must make sense. Urban location: Highly densely populated, should be close, within one mile. Suburban location: No set distance rule. Case by case. Sometimes more than a mile is appropriate. Rural location: Not a lot of homes to select from. Might be miles to find similar market alternative. Appraiser explanation is key. Page 35 25

26 Analyzing Comparable Properties Subject located in a subdivision, condominium or PUD project. Established (Resale Market) All comparables should be from within the project. Institutional or investor sellers/buyers may require outside comparables as well. New (Builder/Developer still selling) At least one comp from within the project. At least one comp from a nearby competing project. Appraiser should note the nearby project is unrelated to subject s builder/developer. Page 35 26

27 Analyzing Comparable Properties Accounting for Foreclosure/Short Sale Activity in Choosing Comps Suppose the following situation: Two similar houses, one green, one red. Each is on the market for an non-negotiable $200,000. There is no negotiation on the price. Which property are you more likely to purchase? Page 36 27

28 Analyzing Comparable Properties Most would purchase the non-foreclosure if all other things are equal. May indicate a bifurcated market. REO properties. Non-REO properties.but let s keep looking. Page 36 28

29 Analyzing Comparable Properties Suppose there is another house nine blocks away: a blue house. Page 36 29

30 Analyzing Comparable Properties This may point towards three price points: Foreclosed properties. (Green) Properties amongst foreclosure/short sale activity. (Red) Properties away from the foreclosure activity. (Blue) Appraisers must explain: Is there foreclosure/short sale activity in the subject s market? How does this impact the subject? Do the selected comparables reflect this impact? Lenders/Underwriter concerns: A Lender must not require the appraiser include or exclude REO sales or short sales as comps. Analysis: Has the appraiser explained the impact of foreclosure/short sale on the subject? Does this explanation make sense? Do outside resources agree with the appraiser s explanation? Appraisers can include additional documentation as support. Page 37 30

31 Analyzing Comparable Sales When foreclosures are the market Foreclosures /short sales are the only sales. These would typically be used as comps. Marketability issues due to foreclosures/short sales in market Appraiser should address why the subject is marketable despite the activity. Foreclosure/short sale activity needs to be taken into account in the appraisal. Page 38 31

32 Analyzing Comparable Sales Bracketing At least one comparable superior and one inferior to the subject. As many bracketed items as possible: Unadjusted Sale Price Gross Living Area (GLA) Lot Size Adjusted Sale Price Other Major Physical Characteristics Bracketing is a best practice. Accurate Picture of Value Tighter Range/Spread of Values Because there are both upward and downward adjustments in each field. Conformity to Neighborhood Bracketing size and actual range supports the subject s conformity to the neighborhood. Page 39 32

Square Footage and Bedroom Count Page 39")

33 Analyzing Comparable Sales Gross Living Area (GLA) Square Footage and Bedroom Count Page 39 33

34 Analyzing Comparable Properties Gross Living Area (GLA) Square Footage Subject and comps should be similar size. Differences < 100 square feet are not usually adjusted. Common exception: small homes (<1,500 sq ft). Bedroom Count Similar bedroom count is best. Two bedroom subjects must have at least one two-bedroom comps. Appraisers can go up or down one bedroom in choosing comps. Ex: Three and four bedroom homes can usually be compared. Page 39 34

35 Analyzing Comparable Properties Declining Markets Check applicable guidelines carefully. Typical guideline requirements: At least two comparables closed within the past three months. A minimum of one, preferably two, listing(s) and/or pending sales. Downward time adjustments may be warranted. If older comparables used. If market conditions have changed since the comparable went under contract Page 40 35

36 Analyzing Comparable Properties Do the subject and comparables appear to be similar? 36

37 Analyzing Comparable Properties Resources Recent home sales and listings. Distressed home information. Street level pictures. Local real estate tax records, local school district sites, free online AVMs (use with caution). Pay sites, such as Core Logic, Platinum Data s Collateral Expert, FNC Collateral DNA and RealtyTrac. Page 40 37

38 Analyzing Sales Comparison Grid Start: Comp s Actual Sales Price Compare: To make the comp more like the subject, one must add/remove a. Consider: Does bring value to property? If not, no adjustment warranted. If yes, how much? Example: To make this comp more like the subject, add the finished basement rooms. (+) The appraiser s research indicates the rooms bring $3,000 in value, so there is a + $3,000 adjustment. Value: Indicated Value for Subject is established by adding/subtracting the column. Page 42 38

39 Analyzing Sales Comparison Grid Value Adjustment Basics Adjustment based on value feature contributes to property. Not based on building cost. Differ by market area. Must be supported, justified and explained. Should make sense. Page 42 39

40 Analyzing Sales Comparison Grid Field Types Non-Value Adjustment Fields Value Adjustment Fields Basic Information Guidelines and Best Practices 40

41 Analyzing Sales Comparison Grid Non-Value Adjustment Lines Address Proximity to Subject Sales Price Sales Price/Gross Living Area Data Source Verification Source Page 43 41

42 Analyzing Sales Comparison Grid Address Verify at Proximity Distance In miles, to two decimal points. As the crow flies. Direction From the subject, to the comp. Sales Price Actual sales price, Page 43 42

43 Analyzing Sales Comparison Grid Sale Price/Gross Living Area AKA Price per Square Foot: Sales Price divided by Gross Living Area square footage. Can indicate whether the subject and comparables are similar Page 43 43

44 Analyzing Sales Comparison Grid Data and Verification Sources Specific Data Source used for each comparable shown. Specific MLS and MLS#, when applicable. Other sources explained in the Comments section. Days on Market (DOM), to four digits, must be included. Verification Source required. Data Source can be party related to transaction. So long as Verification Source public, published, and verifiable Page 44 44

45 Analyzing Sales Comparison Grid Across the Board Adjustments Subject feature No similarly featured comparable Adjustments to each comp in the same direction for any single item of comparison. Common Examples: Swimming Pool, Shed, Barn, Greenhouse or Workshop Questionable market acceptance Unsupported value additions/subtractions Additional comparables Older, distant or otherwise not usually acceptable Market acceptance Value Page 45 45

46 Analyzing Sales Comparison Grid Sale or Financing Concessions First Line Type of sale. Second Line Financing type. Concession Amount. See Fannie Mae and Freddie Mac Uniform Appraisal Dataset Specification, Field-Specific Standardization Requirements (Appendix D) for abbreviations. Page 45 46

47 Analyzing Sales Comparison Grid Financing Concessions Within allowable limit? Adjustment required? Narrative included? Is sales price inflated by concession s inclusion? Excessive financing concessions deducted from sales price? LTV recalculated, if necessary? Sales Concessions Non-real property items in contract? Non-real property items deducted from sales price? LTV recalculated, if necessary? Page 46 47

48 Analyzing Sales Comparison Grid Date of Sale/Time Sale date and contract date. Market condition adjustments: Sometimes warranted for significant market changes. Explanation required. Measured from date of contract, not sale. Page 47 48

49 Analyzing Sales Comparison Grid Location Look for similar ratings and factors. Impact on value rating. Neutral (N) Beneficial (B) Adverse (A) Factor(s). One or Two Explain what impacts the value rating. Value adjustment may be warranted: Otherwise similar properties. Appraiser explanation. Page 47 49

50 Analyzing Sales Comparison Grid Site Lot size. Not description. (i.e. Average) Entire site. Less than one acre: Whole numbers, square footage. One acre or more: Acreage to two decimal points. Similarly sized lots. Adjustments Consistent with lot value in cost approach. Supported with market data. Page 48 50

51 Analyzing Sales Comparison Grid View Look for similar ratings and factors. Impact on value rating: Neutral. (N) Beneficial. (B) Adverse. (A) Factor(s): One or Two. Explain what impacts the value rating. Value adjustment may be warranted: Otherwise similar properties. Appraiser explanation. Page 48 51

52 Analyzing Sales Comparison Grid Design Architectural design/style Narrative i.e. Mid-Century Modern, Colonial, Craftsman, Ranch Non-Architectural descriptions unacceptable Average Brick Any adjustments require explanation. Page 48 52

53 Analyzing Sales Comparison Grid Quality of Construction UAD Quality Rankings: Q1-Q6 See Appendix D for specific ratings definitions. Q1: Unique Q2: Custom Design Q3: Higher Quality Q4: Meet or Exceed Applicable Codes Q5: Economy Construction Q6: Basic, Lower Cost Similar rankings. Otherwise, possible adjustment. Appraiser explanation Actual Age Page 49 53

54 Analyzing Sales Comparison Grid Condition UAD Condition Rankings: C1-C6 See Appendix D for specific ratings definitions. C1: New C2: No deferred maintenance C3: Well maintained C4: Minor deferred maintenance C5: In need of significant repairs C6: Substantial damage Subject s condition rating must be the same as rating indicated in Improvements Section. Appraisal subject to completion/repair. Sales comparison based on anticipated condition upon completion. Similar rankings. Otherwise, possible adjustment. Appraiser explanation. Page 50 54

55 Analyzing Sales Comparison Grid Bedrooms Appraiser explanations for adjustments. Particular markets. Bathrooms Full and half baths reported. Square Footage Similar adjustments. Page 50 55

56 Analyzing Sales Comparison Grid Basement First Line Square footage. Finished square footage Basement access: Walk-out (wo), walk-up (wu) or interior only (in). Second Line Number of rooms. Type of finished rooms: Rec room (rr), bedroom (br), bath (ba) or other (o). Baths reported in full.half format. Basement value and adjustments must make sense. Page 51 56

57 Analyzing Sales Comparison Grid Functional Utility If adjusted, explained in comments., Heating/Cooling Energy Efficient Items, Garage/Carport, Porch/Patio/Deck, Fireplace. Adjustments need to make sense. Other Outbuildings (see next slide) In blank spaces. Need to make sense. Page 52 57

58 Analyzing Sales Comparison Grid When there are outbuildings: Minimal outbuildings Typical in the subject area. Comparables with similar outbuildings. Significant outbuildings. Residential vs. Agricultural Avoiding across-the-board adjustments Finding additional comparables Expanded search dates/criteria Extent of search Fannie Mae Single Family 2015 Selling Guide Section B

59 Fannie Mae Selling Guide 59

60 Freddie Mac Selling Guide Neighborhood section Properties with outbuildings, such as a barn or stable, must be considered in the underwriting process to determine whether the property is residential or nonresidential. A property with a small barn or stable may be acceptable if the contributory value of the outbuilding(s) is minimal and the appraiser demonstrates through the use of comparable sales with similar characteristics that it is typical for residential properties in the market area. However, if the property has a large outbuilding, such as a large barn or multiple outbuildings, it may indicate that the property is agricultural or non-residential and ineligible as security for a Freddie Mac Mortgage. Properties in rural locations often have relatively large sites as compared to other locations. In addition, there may be a lack of comparable sales due to the relatively low number of recent sales transactions in the market area. In such cases, appraisers may have to use comparable sales that are located a considerable distance from the subject property or comparable sales that are not very similar to the subject property. This is acceptable as long as the appraiser can justify and support the use of the comparable sales and analysis in the appraisal report. 60

61 Analyzing Sales Comparison Grid Previous Sale or Transfer History Page 53 61

62 Analyzing Sales Comparison Grid True or False? Given the Adjusted Sales Price of the Comparables shown here, the indicated value for the subject is $158,200. ( $153,000 + $157,800 + $163,800 ) / 3 = $158,200 Page 55 62

63 Analyzing Sales Comparison Grid The appraiser discusses how he/she weighted each comparable and arrived at the indicated value. The arrived at conclusion should be: Weighted Average Consistent with the data provided in the report. All comments provided by the appraiser. All data sources used to verify the report. Should be supported by everything on the appraisal. Page 55 63

64 Reconciliation The Appraisal is Made As Is If any other box is checked, the appraiser or a subject matter expert will have to inspect the property after work is completed. Last Line Appraised Value Appraisal Date Inspection Date Good for twelve months If more than four months on note date, update must be provided Page 55 64

65 Comments Read Comments Section Carefully Look for anything impacting: Value Structural Integrity Marketability Page 55 65

66 Statement of Assumptions/Ltd Conditions Page 59 66

67 Appraiser/Supervisory Appraiser Signatures Page 60 67

68 Common Red Flags Common Red Flags Include Choosing dated comps, in the absence of sufficient explanation, particularly when there are more recent comps available. Not relying upon the indicated value from the most similar comparable property. Closest. Most recent sale. Most similar property. Indicated value outside the predominant range for the neighborhood. High land to value percentage without explanation. Photos show a feature/situation not reflected in the appraisal. Major Farm structures or livestock may evidence farm use. Appraisers should explain unusual circumstances and confirm that the land is used solely residentially. Page 61 68

69 Common Red Flags Common Red Flags Include Gross adjustments in excess of 25% of the original sales price on several comps without sufficient explanation and justification. Not identifying an area as declining when credible evidence suggests a decline. Lack of bracketing for price, age and/or square footage. Lack of comments from the appraiser relating to the property, comps, market or trends in the area. Boilerplate appraiser statements, such as best comps were selected or there are no additional comps available. Page 61 69

70 Genworth MI Coverage and Appraisals Sales Comparison Considerations: Underwriting Loans for Genworth MI Coverage Genworth Appraisal Guidelines can be found online Under the Rates and Guidelines tab. Value Not Supported by Comparables is cited on Genworth s Top MI Decision Errors as a common underwriting issue. Genworth follows Agency Appraisal Standards and Uniform Standards of Professional Appraisal Practice (USPAP) guidelines. When Genworth s underwriting manual is silent and does not address a guideline, the lender must follow Agency Standard guidelines. See the Delegated MI Underwriting Decision Tips flier for additional information. Page 62 70

71 Genworth Appraisal Review Checklist 71

72 Questions? 72

73 Thank You! 73

74 Legal Disclaimer Genworth Mortgage Insurance is happy to provide you with these training materials. While we strive for accuracy, we also know that any discussion of laws and their application to particular facts is subject to individual interpretation, change, and other uncertainties. Our training is not intended as legal advice, and is not a substitute for advice of counsel. You should always check with your own legal advisors for interpretations of legal and compliance principles applicable to your business. GENWORTH EXPRESSLY DISCLAIMS ANY AND ALL WARRANTIES, EXPRESS OR IMPLIED, INCLUDING WITHOUT LIMITATION WARRANTIES OF MERCHANTABILITY AND FITNESS FOR A PARTICULAR PURPOSE, WITH RESPECT TO THESE MATERIALS AND THE RELATED TRAINING. IN NO EVENT SHALL GENWORTH BE LIABLE FOR ANY DIRECT, INDIRECT, INCIDENTAL, PUNITIVE, OR CONSEQUENTIAL DAMAGES OF ANY KIND WHATSOEVER WITH RESPECT TO THE TRAINING AND THE MATERIALS. Desktop Underwriter, DU, and MyCommunity Mortgage are registered trademarks of Fannie Mae. Loan Prospector and Home Possible Mortgage are registered trademarks of Freddie Mac. The Appraisal Foundation owns the copyright to the Uniform Standards of Professional Appraisal Practice (USPAP). Simply Underwrite SM is a registered service mark of Genworth Financial. 74

Appraisal Review: Analyzing the 1004

Appraisal Review: Analyzing the 1004 1 LIVE ONLINE PARTICIPANT GUIDE Version: 8.12 Table of Contents The Purpose of the Appraisal... 3 Define Market Value... 3 Scenario 1 (John Johnson report) - 1004 Uniform

Appraisal Review: Analyzing the 1004 1 LIVE ONLINE PARTICIPANT GUIDE Version: 8.12 Table of Contents The Purpose of the Appraisal... 3 Define Market Value... 3 Scenario 1 (John Johnson report) - 1004 Uniform

Appraisal Review Reminders

Use the following list of reminders as a tool when underwriting the appraisal report. For complete information on appraisal requirements, refer to the Freddie Mac Seller/Servicer Guide (Guide) Chapter

Use the following list of reminders as a tool when underwriting the appraisal report. For complete information on appraisal requirements, refer to the Freddie Mac Seller/Servicer Guide (Guide) Chapter

Appraisal Review Reminders

Use the following list of reminders as a tool when underwriting the appraisal report. For complete information on appraisal requirements, refer to the Freddie Mac Seller/Servicer Guide (Guide) Chapter

Use the following list of reminders as a tool when underwriting the appraisal report. For complete information on appraisal requirements, refer to the Freddie Mac Seller/Servicer Guide (Guide) Chapter

2. Is the information in the contract section complete and accurate? Yes No Not Applicable If Yes, provide a brief summary.

The purpose of this appraisal field review report is to provide the lender/client with an opinion on the accuracy of the appraisal report under review. Property Address City State Zip Code Borrower Owner

The purpose of this appraisal field review report is to provide the lender/client with an opinion on the accuracy of the appraisal report under review. Property Address City State Zip Code Borrower Owner

SIRVA Mortgage Order Instructions

SIRVA Mortgage Order Instructions Appraiser Trainees: This client does not permit Trainees to sign the appraisal report, however USPAP requirements apply when significant assistance has been provided by

SIRVA Mortgage Order Instructions Appraiser Trainees: This client does not permit Trainees to sign the appraisal report, however USPAP requirements apply when significant assistance has been provided by

APPRAISAL OF REAL PROPERTY

Home Appraisals, Inc. (866) 533-7173 APPRAISAL OF REAL PROPERTY File # LOCATED AT Field Review Form Sample FOR OPINION OF VALUE 35, AS OF 11/1/7 TABLE OF CONTENTS One-Unit Field Review... 1 General Text

Home Appraisals, Inc. (866) 533-7173 APPRAISAL OF REAL PROPERTY File # LOCATED AT Field Review Form Sample FOR OPINION OF VALUE 35, AS OF 11/1/7 TABLE OF CONTENTS One-Unit Field Review... 1 General Text

Agency Guideline Revisions Note: SunTrust Mortgage specific overlays are underlined.

Accessory Units Correspondent Section 1.07 Appraisal Guidelines & Correspondent Section.01 Agency Loan Programs- Guideline Standard Agency Agency Plus Home Possible Mortgage Section 1.07 Appraisal Guidelines

Accessory Units Correspondent Section 1.07 Appraisal Guidelines & Correspondent Section.01 Agency Loan Programs- Guideline Standard Agency Agency Plus Home Possible Mortgage Section 1.07 Appraisal Guidelines

Appraisal and Property Related Frequently Asked Questions (FAQs) Updated September 2014

Updated September 2014") Appraisal and Property Related Frequently Asked Questions (FAQs) Updated September 2014 This FAQ document provides responses to common questions related to Fannie Mae s property eligibility and appraisal

Appraisal and Property Related Frequently Asked Questions (FAQs) Updated September 2014 This FAQ document provides responses to common questions related to Fannie Mae s property eligibility and appraisal

UNIFORM APPRAISAL DATASET (UAD) FHA SPOTLIGHT - SELECTION AND VERIFICATION OF COMPARABLE SALES

FHA SPOTLIGHT - SELECTION AND VERIFICATION OF COMPARABLE SALES") Spring 2011 Issue 3 FHA APPRAISER In This Issue: Welcome to the third issue of the Federal Housing Administration Appraiser Roster Newsletter. We hope you will find it informative. Uniform Appraisal Dataset

Spring 2011 Issue 3 FHA APPRAISER In This Issue: Welcome to the third issue of the Federal Housing Administration Appraiser Roster Newsletter. We hope you will find it informative. Uniform Appraisal Dataset

Overall Trend Section Example Seller Concessions Foreclosure Sales and Summary/Analysis of Data... 13

Appraisal and Property-Related Frequently Asked Questions (FAQs) This FAQ document provides responses to common questions related to Fannie Mae s property eligibility and appraisal policies. Following

Appraisal and Property-Related Frequently Asked Questions (FAQs) This FAQ document provides responses to common questions related to Fannie Mae s property eligibility and appraisal policies. Following

Chapter 8 Qualifying Property

The 3 "Cs" of Lending Capacity to Pay does the borrower make enough money to repay loan? lenders use qualifying ratios Creditworthiness [Character] is the borrower likely to repay loan on time? lenders

The 3 "Cs" of Lending Capacity to Pay does the borrower make enough money to repay loan? lenders use qualifying ratios Creditworthiness [Character] is the borrower likely to repay loan on time? lenders

Freddie Mac UCDP Proprietary Messages

UCDP Proprietary Messages -specific feedback messages for appraisals submitted to in the Uniform Collateral Data Portal (UCDP ). The content in brackets represents dynamic values. *Message text updated

UCDP Proprietary Messages -specific feedback messages for appraisals submitted to in the Uniform Collateral Data Portal (UCDP ). The content in brackets represents dynamic values. *Message text updated

Guidance for Lenders and Appraisers April 2009

Guidance for Lenders and Appraisers April 2009 Fannie Mae views lenders as our partners in ensuring the continued viability of the residential lending market and the continued availability of affordable

Guidance for Lenders and Appraisers April 2009 Fannie Mae views lenders as our partners in ensuring the continued viability of the residential lending market and the continued availability of affordable

Announcement July 13, Collateral Valuation Practices and Declining Markets

Announcement 07-11 July 13, 2007 Amends these Guides: Selling Collateral Valuation Practices and Declining Markets Introduction An accurate value for the property securing a mortgage loan is important

Announcement 07-11 July 13, 2007 Amends these Guides: Selling Collateral Valuation Practices and Declining Markets Introduction An accurate value for the property securing a mortgage loan is important

Date Listed Date Sold List Price Sale Price Notes 07/08/ $14, WITHDRAWN AFTER 133 DAYS

Standard BPO, Drive-By v2 3802 Crockett Street, San Angelo, TX 76903 Please Note: This report was completed with the following assumptions: Market Approach: Distressed Price, Marketing Time: Abbreviated.

Standard BPO, Drive-By v2 3802 Crockett Street, San Angelo, TX 76903 Please Note: This report was completed with the following assumptions: Market Approach: Distressed Price, Marketing Time: Abbreviated.

As Of: Prepared For: Prepared By:

of 216 SW 131st St As Of: 06/11/11 Prepared For: Prime Pacific Bank 2502 196th St SW Lynnwood WA 98036 Prepared By: Cynthia A. Nagle, CREA 922 N Cedar St Tacoma, WA 98406 RESTRICTED APPRAISAL REPORT Restriction

of 216 SW 131st St As Of: 06/11/11 Prepared For: Prime Pacific Bank 2502 196th St SW Lynnwood WA 98036 Prepared By: Cynthia A. Nagle, CREA 922 N Cedar St Tacoma, WA 98406 RESTRICTED APPRAISAL REPORT Restriction

Pro-Series Webinar: Fannie Mae Update Collateral Policy and Technology Guidance For Appraisers

Pro-Series Webinar: Fannie Mae Update Collateral Policy and Technology Guidance For Appraisers March 29, 2017 Presenters: Julie Jones & Jeremy Staudenmaier Webinar Audio (phone only): 1 - (866) 218-8865

Pro-Series Webinar: Fannie Mae Update Collateral Policy and Technology Guidance For Appraisers March 29, 2017 Presenters: Julie Jones & Jeremy Staudenmaier Webinar Audio (phone only): 1 - (866) 218-8865

Kathy Coon, SRA Appraisal Review: CSI Style ( )

") Appraisal Review: CSI Style Southern California Chapter Appraisal Institute July 16, 2009 Kathy Coon, SRA Chief Appraiser/Director-Appraisal Appraisal Quality Control FNC, Inc. www.fncinc.com com When

Appraisal Review: CSI Style Southern California Chapter Appraisal Institute July 16, 2009 Kathy Coon, SRA Chief Appraiser/Director-Appraisal Appraisal Quality Control FNC, Inc. www.fncinc.com com When

To all Appraisers: Brief Overview:

To all Appraisers: As the appraisal industry continues to change, the demand for alternative valuation solutions grows. That is why is excited to announce the addition of a new product - the Desktop Appraisal

To all Appraisers: As the appraisal industry continues to change, the demand for alternative valuation solutions grows. That is why is excited to announce the addition of a new product - the Desktop Appraisal

Uniform Appraisal Dataset (UAD) Frequently Asked Questions

Frequently Asked Questions") Uniform Appraisal Dataset (UAD) Frequently Asked Questions July 13, 2014 Updated for formatting May 15, 2017 The following provides answers to questions frequently asked about Fannie Mae s and Freddie

Uniform Appraisal Dataset (UAD) Frequently Asked Questions July 13, 2014 Updated for formatting May 15, 2017 The following provides answers to questions frequently asked about Fannie Mae s and Freddie

Dear Valuation Professional

Dear Valuation Professional First American Mortgage Solutions LLC has a new product offering that we would like you to consider adding to your list of services with us - (Property Assessment Collateral

Dear Valuation Professional First American Mortgage Solutions LLC has a new product offering that we would like you to consider adding to your list of services with us - (Property Assessment Collateral

REDSTONE from Bradford Technologies

REDSTONE from Bradford Technologies New Redstone to ClickFORMS Data Transfer Redstone Market Area Summary Sales Comparable Selection Market Adjustment Factors Market Trends Market Characteristics 004MC

REDSTONE from Bradford Technologies New Redstone to ClickFORMS Data Transfer Redstone Market Area Summary Sales Comparable Selection Market Adjustment Factors Market Trends Market Characteristics 004MC

Evaluating Your Appraisal

Evaluating Your Appraisal April 28, 2011 Presented by: Brady W. Meadows Mortgage Compliance Advisors Instructions Because of the large number of registrants, the lines will be muted. To ask a question,

Evaluating Your Appraisal April 28, 2011 Presented by: Brady W. Meadows Mortgage Compliance Advisors Instructions Because of the large number of registrants, the lines will be muted. To ask a question,

Uniform Residential Appraisal Report (URAR) Model Appraisal

Model Appraisal") Basic Appraisal Procedures Residential Applications & Model Appraisals 15-13 Uniform Residential Appraisal Report (URAR) Model Appraisal On the following pages are examples of a completed Fannie Mae/Freddie

Basic Appraisal Procedures Residential Applications & Model Appraisals 15-13 Uniform Residential Appraisal Report (URAR) Model Appraisal On the following pages are examples of a completed Fannie Mae/Freddie

March 23, 2009 MORTGAGEE LETTER

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT WASHINGTON, DC 20410-8000 ASSISTANT SECRETARY FOR HOUSING- FEDERAL HOUSING COMMISSIONER March 23, 2009 MORTGAGEE LETTER 2009-09 TO: SUBJECT: ALL APPROVED

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT WASHINGTON, DC 20410-8000 ASSISTANT SECRETARY FOR HOUSING- FEDERAL HOUSING COMMISSIONER March 23, 2009 MORTGAGEE LETTER 2009-09 TO: SUBJECT: ALL APPROVED

Mike Dalton Jr. and Associates. Christina Adams INVOICE NUMBER Mike Dalton Jr. and Associates 8191 Wethersfield Drive. PB125 Germantown, TN 38138

Mike Dalton Jr. and Associates FROM: INVOICE Christina Adams INVOICE NUMBER Mike Dalton Jr. and Associates 8191 Wethersfield Drive Germantown, TN 38138 DATE 08/14/2016 Telephone Number: (901) 674-0239

Mike Dalton Jr. and Associates FROM: INVOICE Christina Adams INVOICE NUMBER Mike Dalton Jr. and Associates 8191 Wethersfield Drive Germantown, TN 38138 DATE 08/14/2016 Telephone Number: (901) 674-0239

APPRAISAL REQUIREMENTS FOR SUNTENDER VALUATIONS, INC. Updated 03/26/2018

APPRAISAL REQUIREMENTS FOR SUNTENDER VALUATIONS, INC. Updated 03/26/2018 STOP Call Suntender Valuations if subject is a refinance transaction however it has been listed for sale in the past 3 months, unless

APPRAISAL REQUIREMENTS FOR SUNTENDER VALUATIONS, INC. Updated 03/26/2018 STOP Call Suntender Valuations if subject is a refinance transaction however it has been listed for sale in the past 3 months, unless

Date Listed Date Sold List Price Sale Price Notes

Standard BPO, Drive-By v2 2036 Lester Fork Road, Grundy, VA 24614 Please Note: This report was completed with the following assumptions: Market Approach: Distressed Price, Marketing Time: Abbreviated.

Standard BPO, Drive-By v2 2036 Lester Fork Road, Grundy, VA 24614 Please Note: This report was completed with the following assumptions: Market Approach: Distressed Price, Marketing Time: Abbreviated.

Appraisal Engagement Instructions

Appraisal Engagement Instructions OVERVIEW The appraisal report must be prepared by a state licensed or certified appraiser and must comply with the Appraiser Independence Requirements (AIR), Uniform Standards

Appraisal Engagement Instructions OVERVIEW The appraisal report must be prepared by a state licensed or certified appraiser and must comply with the Appraiser Independence Requirements (AIR), Uniform Standards

Residential Appraising What Lenders Want

Residential Appraising What Lenders Want Introductions Ken DeFeo 25 years appraising have worked for lenders for 20 years Lets get to know a little about the audience How many appraisers do we have? How

Residential Appraising What Lenders Want Introductions Ken DeFeo 25 years appraising have worked for lenders for 20 years Lets get to know a little about the audience How many appraisers do we have? How

Colorado Appraisal Consultants

Colorado Appraisal Consultants SUBJECT Individual Condominium Unit Appraisal Report File # The purpose of this summary appraisal report is to provide the lender/client with an accurate, and adequately

Colorado Appraisal Consultants SUBJECT Individual Condominium Unit Appraisal Report File # The purpose of this summary appraisal report is to provide the lender/client with an accurate, and adequately

The High Performance Appraisal Process Unveiled By Sandra K. Adomatis, SRA, LEED Green Associate

The High Performance Appraisal Process Unveiled By Sandra K. Adomatis, SRA, LEED Green Associate Email: Adomatis@Hotmail.com Twitter: https://twitter.com/sadomatis Web: www.adomatisappraisalservice.com

The High Performance Appraisal Process Unveiled By Sandra K. Adomatis, SRA, LEED Green Associate Email: Adomatis@Hotmail.com Twitter: https://twitter.com/sadomatis Web: www.adomatisappraisalservice.com

APPRAISAL OF REAL PROPERTY LOCATED AT: FOR: AS OF: BY:

APPRAISAL OF REAL PROPERTY LOCATED AT: 489 MEADOWS EDGE COURT DEED BOOK 2896, PAGE 2759 CLEMMONS, NC 27012 FOR: ESTATE OF WILLIAM C. McINTOSH % BAILEY & THOMAS P.O. BOX 52 WINSTON-SALEM, NC 27102 AS OF:

APPRAISAL OF REAL PROPERTY LOCATED AT: 489 MEADOWS EDGE COURT DEED BOOK 2896, PAGE 2759 CLEMMONS, NC 27012 FOR: ESTATE OF WILLIAM C. McINTOSH % BAILEY & THOMAS P.O. BOX 52 WINSTON-SALEM, NC 27102 AS OF:

Freddie Mac Condominium Unit Mortgages

For all mortgages secured by a Condominium Unit in a Condominium Project, the Seller must perform an underwriting review of the Condominium Project to ensure the mortgage and the project meet the requirements

For all mortgages secured by a Condominium Unit in a Condominium Project, the Seller must perform an underwriting review of the Condominium Project to ensure the mortgage and the project meet the requirements

Appraisal Stream Restricted Use Residential Appraisal Report

Appraisal Stream Restricted Use Residential Appraisal Report File No. 769kemplin This report is limited to the sole and exclusive use of the client. The appraiser's opinions and conclusions set forth in

Appraisal Stream Restricted Use Residential Appraisal Report File No. 769kemplin This report is limited to the sole and exclusive use of the client. The appraiser's opinions and conclusions set forth in

Restricted Use Appraisal Report Residential

Client File #: Appraisal File #: Restricted Use Appraisal Report Residential Appraisal Company: Address: Form 200.04* Phone: Fax: Website: Appraiser: Co-Appraiser: AI Membership (if any): SRA MAI SRPA

Client File #: Appraisal File #: Restricted Use Appraisal Report Residential Appraisal Company: Address: Form 200.04* Phone: Fax: Website: Appraiser: Co-Appraiser: AI Membership (if any): SRA MAI SRPA

GAAR Harness the Power of Technology to Create the BEST Appraisal Reviews Possible

GAAR Harness the Power of Technology to Create the BEST Appraisal Reviews Possible Presented by FNC March 21, 2012 INTRODUCTION General Information: Conference Web Page Audio & Supporting Documents Submit

GAAR Harness the Power of Technology to Create the BEST Appraisal Reviews Possible Presented by FNC March 21, 2012 INTRODUCTION General Information: Conference Web Page Audio & Supporting Documents Submit

10454 South Green Bay Avenue Chicago, IL Client and Order Detail. Subject Property Information

Client and Order Detail Client: Address: 10454 South Green Bay Avenue Client Loan Number: C/S/Z: Order Number: 0290016663 County: Cook Inspection Type: BPO-Interior BPO Agent: Lopez, Leo Mortgagor's Name:

Client and Order Detail Client: Address: 10454 South Green Bay Avenue Client Loan Number: C/S/Z: Order Number: 0290016663 County: Cook Inspection Type: BPO-Interior BPO Agent: Lopez, Leo Mortgagor's Name:

Individual Cooperative Interest Appraisal Report

PURPOSE Individual Cooperative Interest Appraisal Report The purpose of this appraisal report is to provide the client with a credible opinion of the defined value of the subject property, given the intended

PURPOSE Individual Cooperative Interest Appraisal Report The purpose of this appraisal report is to provide the client with a credible opinion of the defined value of the subject property, given the intended

UNIFORM APPRAISAL DATASET

[Pick the date] [UNIFORM APPRAISAL DATASET] This document will provide Realtors knowledge about the new Fannie Mae and Freddy Mac appraisal requirements. Providing information discussed in this document

[Pick the date] [UNIFORM APPRAISAL DATASET] This document will provide Realtors knowledge about the new Fannie Mae and Freddy Mac appraisal requirements. Providing information discussed in this document

Exterior Only Inspection Residential Appraisal Report File #

SUBJECT Summary Appraisal Report Brian J. Davis & Associates Exterior Only Inspection Residential Appraisal Report File # Page #3 The purpose of this summary appraisal report is to provide the lender/client

SUBJECT Summary Appraisal Report Brian J. Davis & Associates Exterior Only Inspection Residential Appraisal Report File # Page #3 The purpose of this summary appraisal report is to provide the lender/client

Collateral Underwriter Overview. National Association of REALTORS January 23, 2015

Collateral Underwriter Overview National Association of REALTORS January 23, 2015 2014 Fannie Mae. Trademarks of Fannie Mae. Introduction to Collateral Underwriter I January 2015 What Is Collateral Underwriter?

Collateral Underwriter Overview National Association of REALTORS January 23, 2015 2014 Fannie Mae. Trademarks of Fannie Mae. Introduction to Collateral Underwriter I January 2015 What Is Collateral Underwriter?

Fannie Mae Update: Collateral Policy & Technology Guidance for Appraisers. Presenter: Julie Jones August 23, 2017

Fannie Mae Update: Presenter: Julie Jones August 23, 2017 2017 Fannie Mae. Trademarks of Fannie Mae. 1 Disclaimer An Important Note about the Seminar Content While every effort has been made to ensure

Fannie Mae Update: Presenter: Julie Jones August 23, 2017 2017 Fannie Mae. Trademarks of Fannie Mae. 1 Disclaimer An Important Note about the Seminar Content While every effort has been made to ensure

Freddie Mac Condominium Unit Mortgages

For all mortgages secured by a Unit in a Project, Sellers must meet the requirements of Freddie Mac Single-Family Seller/Servicer Guide (Guide) Chapter 5701, Special for s, and the Seller s other Purchase

For all mortgages secured by a Unit in a Project, Sellers must meet the requirements of Freddie Mac Single-Family Seller/Servicer Guide (Guide) Chapter 5701, Special for s, and the Seller s other Purchase

Condo - PUD Project Review Manual

Table of Contents Condo - PUD Project Review Manual Section 1: PRMG Project Approval Section 2: Limited/Streamlined Condo Project Review Section 3: CPM Review Section 4: Lender Full Condo Review Section

Table of Contents Condo - PUD Project Review Manual Section 1: PRMG Project Approval Section 2: Limited/Streamlined Condo Project Review Section 3: CPM Review Section 4: Lender Full Condo Review Section

Haley-Worsham & Associates LLC. HW Cordova, TN REFERENCE TO:

Haley-Worsham & Associates LLC FROM: INVOICE Michael Bray INVOICE NUMBER Haley-Worsham & Associates LLC 1176 Vickery Lane HW171254 Cordova, TN 816 DATE 12/11/217 Telephone Number: 91-755-146 Fax Number:

Haley-Worsham & Associates LLC FROM: INVOICE Michael Bray INVOICE NUMBER Haley-Worsham & Associates LLC 1176 Vickery Lane HW171254 Cordova, TN 816 DATE 12/11/217 Telephone Number: 91-755-146 Fax Number:

Individual Condominium Unit Appraisal Report

The purpose of this summary appraisal report is to provide the lender/client with an accurate, and adequately supported, opinion of the market value of the subject property. SUBJECT Property Address Unit

The purpose of this summary appraisal report is to provide the lender/client with an accurate, and adequately supported, opinion of the market value of the subject property. SUBJECT Property Address Unit

Freddie Mac Condominium Unit Mortgages

For all mortgages secured by a Condominium Unit in a Condominium Project, you must meet the requirements of Freddie Mac Single-Family Seller/Servicer Guide (Guide) Chapter 5701, Special for Condominiums,

For all mortgages secured by a Condominium Unit in a Condominium Project, you must meet the requirements of Freddie Mac Single-Family Seller/Servicer Guide (Guide) Chapter 5701, Special for Condominiums,

BPO Best Practices Guide

BPO Best Practices Guide A Step by Step Guide for Completing BPO Reports Version: 1.0.0 Published: 03/01/2011 Global DMS, 1555 Bustard Road, Suite 300, Lansdale, PA 19446 2014, All Rights Reserved. Table

BPO Best Practices Guide A Step by Step Guide for Completing BPO Reports Version: 1.0.0 Published: 03/01/2011 Global DMS, 1555 Bustard Road, Suite 300, Lansdale, PA 19446 2014, All Rights Reserved. Table

SUBJECT: SELLING UPDATES

TO: Freddie Mac Sellers June 27, 2018 2018-10 SUBJECT: SELLING UPDATES This Guide Bulletin announces: Property eligibility and appraisal requirements Eligibility of Condominium Units for automated collateral

TO: Freddie Mac Sellers June 27, 2018 2018-10 SUBJECT: SELLING UPDATES This Guide Bulletin announces: Property eligibility and appraisal requirements Eligibility of Condominium Units for automated collateral

Continental Real Estate Services, Inc. ACTIVE TO SOLD ADJUSTMENT File No. Case No. Borrower Property Address City County State Zip Code

ACTIVE TO SOLD ADJUSTMENT Property Generally, when an appraiser appraises a unit in a cooperative project, he or she should use sales of cooperative units as comparables. However, the appraiser may use

ACTIVE TO SOLD ADJUSTMENT Property Generally, when an appraiser appraises a unit in a cooperative project, he or she should use sales of cooperative units as comparables. However, the appraiser may use

PCV Murcor/BPO - Basic Information

PCV Murcor/BPO - Basic Information https://bpo.pcvmurcor.com/order/basicinformation.aspx Page 1 of 1 Requirements Basic Info N'hood Info Prop Info Sales Comps Listing Comps Valuation Photos CMA Preview

PCV Murcor/BPO - Basic Information https://bpo.pcvmurcor.com/order/basicinformation.aspx Page 1 of 1 Requirements Basic Info N'hood Info Prop Info Sales Comps Listing Comps Valuation Photos CMA Preview

Selling Part VII - Property and Appraisal Analysis

Selling Part VII - Property and Appraisal Analysis This Part--Property and Appraisal Analysis--details our general requirements for analyzing the property appraisal aspects of conventional mortgages secured

Selling Part VII - Property and Appraisal Analysis This Part--Property and Appraisal Analysis--details our general requirements for analyzing the property appraisal aspects of conventional mortgages secured

Division of Real Estate. Summary of BOREA Investigations

Division of Real Estate Summary of BOREA Investigations Complaint Stats for Prior 12 Months BOREA Checklist for Investigations Generally follows the FNMA 1004 layout Neighborhood and Market Analyses Site

Division of Real Estate Summary of BOREA Investigations Complaint Stats for Prior 12 Months BOREA Checklist for Investigations Generally follows the FNMA 1004 layout Neighborhood and Market Analyses Site

Copyright, 1999, 2002, 2004, Freddie Mac. All Rights Reserved.

Page 1 of 13 Engineering Requirements/Chapter 12: Appraiser and Appraisal Requirements/12.1: General requirements 12.1: General requirements For all multifamily purchase programs and products, the Seller/Servicer

Page 1 of 13 Engineering Requirements/Chapter 12: Appraiser and Appraisal Requirements/12.1: General requirements 12.1: General requirements For all multifamily purchase programs and products, the Seller/Servicer

This chapter describes Fannie Mae s project standards, policies, and requirements.

Chapter 2, Project Standards Chapter B4-2, Project Standards Project Standards Click to see prior version of topic Introduction This chapter describes Fannie Mae s project standards, policies, and requirements.

Chapter 2, Project Standards Chapter B4-2, Project Standards Project Standards Click to see prior version of topic Introduction This chapter describes Fannie Mae s project standards, policies, and requirements.

Page 1 of 1 8/24/213 Case# 4174439 Borrower: ERNEST L CURRY, Address: 1429 Olney Dr SAINT LOUIS MO 63136 SAINT LOUIS County Multi-Page Order Info Subject/Neighborhood HOA Sales Listings Subject Repair

Page 1 of 1 8/24/213 Case# 4174439 Borrower: ERNEST L CURRY, Address: 1429 Olney Dr SAINT LOUIS MO 63136 SAINT LOUIS County Multi-Page Order Info Subject/Neighborhood HOA Sales Listings Subject Repair

RevuPro Appraisal Review

RevuPro Appraisal Review Getting It Right ELLIOTT introduces its flagship review product RevuPro, as an independent appraisal review service. Q. What is it and what does it do? A. RevuPro is a fast, economical

RevuPro Appraisal Review Getting It Right ELLIOTT introduces its flagship review product RevuPro, as an independent appraisal review service. Q. What is it and what does it do? A. RevuPro is a fast, economical

Chapter 35. The Appraiser's Sales Comparison Approach INTRODUCTION

Chapter 35 The Appraiser's Sales Comparison Approach INTRODUCTION The most commonly used appraisal technique is the sales comparison approach. The fundamental concept underlying this approach is that market

Chapter 35 The Appraiser's Sales Comparison Approach INTRODUCTION The most commonly used appraisal technique is the sales comparison approach. The fundamental concept underlying this approach is that market

Broker Price Opinion

Broker Price Opinion + Exterior Inspection Interior Inspection Property Address: 15631 S. Tarrant Ave Vendor ID: 4557523 City, State, Zip: Deal Name: Loan Number: 15631STARRANTAVE Inspection Date: 6/06/2018

Broker Price Opinion + Exterior Inspection Interior Inspection Property Address: 15631 S. Tarrant Ave Vendor ID: 4557523 City, State, Zip: Deal Name: Loan Number: 15631STARRANTAVE Inspection Date: 6/06/2018

Fannie Mae Single Family/2007 Selling Guide/Part XI: Property and Appraisal Guidelines/Part XI: Property and Appraisal Guidelines

Fannie Mae Single Family/2007 Selling Guide/Part XI: Property and Appraisal Guidelines/Part XI: Property and Appraisal Guidelines Part XI: Property and Appraisal Guidelines Copyright, 2001-2007, Fannie

Fannie Mae Single Family/2007 Selling Guide/Part XI: Property and Appraisal Guidelines/Part XI: Property and Appraisal Guidelines Part XI: Property and Appraisal Guidelines Copyright, 2001-2007, Fannie

Use of Comparables. Claims Prevention Bulletin [CP-17-E] March 1996

![Use of Comparables. Claims Prevention Bulletin [CP-17-E] March 1996](/thumbs/82/87011536.jpg "Use of Comparables. Claims Prevention Bulletin [CP-17-E] March 1996") March 1996 The use of comparables arises almost daily for all appraisers. especially those engaged in residential practice, where appraisals are being prepared for mortgage underwriting purposes. That

March 1996 The use of comparables arises almost daily for all appraisers. especially those engaged in residential practice, where appraisals are being prepared for mortgage underwriting purposes. That

Collateral Underwriter. Preview and Implementation Information

Collateral Underwriter Preview and Implementation Information 2015 Fannie Mae. Trademarks of Fannie Mae. UCDP and CU Release Overview I January 2015 Seminar Guidelines Please do not place the call on Hold

Collateral Underwriter Preview and Implementation Information 2015 Fannie Mae. Trademarks of Fannie Mae. UCDP and CU Release Overview I January 2015 Seminar Guidelines Please do not place the call on Hold

Section Condominium and PUD Approval Requirements

Section 1.06 - Condominium and PUD Approval Requirements In This Section This section contains the following topics. Overview... 2 Related Bulletins... 3 Agency... 4 General Information on Condominium

Section 1.06 - Condominium and PUD Approval Requirements In This Section This section contains the following topics. Overview... 2 Related Bulletins... 3 Agency... 4 General Information on Condominium

BPOSG BROKER PRICE OPINION. Guidelines. Version 3.1 May 20, BSB BPO Standards Board

BPOSG BROKER PRICE OPINION Standards & Version 3.1 May 20, 2009 BSB BPO Standards Board BSB BPO Standards Board 6619 North Scottsdale Road Scottsdale, Arizona 85250 Standards and : BPOSG is a compilation

BPOSG BROKER PRICE OPINION Standards & Version 3.1 May 20, 2009 BSB BPO Standards Board BSB BPO Standards Board 6619 North Scottsdale Road Scottsdale, Arizona 85250 Standards and : BPOSG is a compilation

UNDERSTANDING HOW USPAP APPLIES TO REAL PROPERTY APPRAISAL PRACTICE USPAP Matrix

UNDERSTANDING HOW USPAP APPLIES TO REAL PROPERTY APPRAISAL PRACTICE - 2014-2015 USPAP Matrix This matrix assumes an Appraisal Report Format under S. R. 2-2(a). *Last updated 9/11/14* GENERAL Violation

UNDERSTANDING HOW USPAP APPLIES TO REAL PROPERTY APPRAISAL PRACTICE - 2014-2015 USPAP Matrix This matrix assumes an Appraisal Report Format under S. R. 2-2(a). *Last updated 9/11/14* GENERAL Violation

Announcement March 24, 2005

Announcement 05-02 March 24, 2005 Amends these Guides: Selling Final Appraisal Report Forms Part XI: Property and Appraisal Analysis Guidelines In Lender Announcement 04-07 dated November 8, 2004, we released

Announcement 05-02 March 24, 2005 Amends these Guides: Selling Final Appraisal Report Forms Part XI: Property and Appraisal Analysis Guidelines In Lender Announcement 04-07 dated November 8, 2004, we released

Small Residential Income Property Appraisal Report File #

SUBJECT Summary Appraisal Report Brian J. Davis & Associates Small Residential Income Property Appraisal Report File # Page #4 The purpose of this summary appraisal report is to provide the lender/client

SUBJECT Summary Appraisal Report Brian J. Davis & Associates Small Residential Income Property Appraisal Report File # Page #4 The purpose of this summary appraisal report is to provide the lender/client

Restricted Use Appraisal Report Residential

Client File #: Appraisal File #: Restricted Use Appraisal Report Residential Form 200.04 * Appraiser: AI Membership (if any): SRA MAI SRPA AI Affiliation (if any): Candidate for Designation Practicing

Client File #: Appraisal File #: Restricted Use Appraisal Report Residential Form 200.04 * Appraiser: AI Membership (if any): SRA MAI SRPA AI Affiliation (if any): Candidate for Designation Practicing

DEMO ITEM SUBJECT COMPARABLE SOLD # 1 COMPARABLE SOLD # 2 COMPARABLE SOLD # 3

Residential Broker Price Opinion FHA CASE #: ASSIGNED LLB: PROPERTY ADDRESS: I. GENERAL MARKET CONDITIONS II. Current market condition: Depressed Slow Stable Improving Excellent Employment conditions:

Residential Broker Price Opinion FHA CASE #: ASSIGNED LLB: PROPERTY ADDRESS: I. GENERAL MARKET CONDITIONS II. Current market condition: Depressed Slow Stable Improving Excellent Employment conditions:

RESIDENTIAL APPRAISAL SUMMARY REPORT

APPRAISAL SUMMARY REPORT SUBJECT ASSIGNMENT SALES COMPARISON APPROACH Lic #: 4800004017 Page #1 File No.: : City: Rye State: NY Zip Code: County: WESTCHESTER Legal Description: Assessor's Parcel #: (SUMMARY

APPRAISAL SUMMARY REPORT SUBJECT ASSIGNMENT SALES COMPARISON APPROACH Lic #: 4800004017 Page #1 File No.: : City: Rye State: NY Zip Code: County: WESTCHESTER Legal Description: Assessor's Parcel #: (SUMMARY

Uniform Residential Appraisal Report File #

D.S. Murphy & Associates FHA/VA Case No. SUBJECT The purpose of this summary appraisal report is to provide the lender/client with an accurate, and adequately supported, opinion of the market value of

D.S. Murphy & Associates FHA/VA Case No. SUBJECT The purpose of this summary appraisal report is to provide the lender/client with an accurate, and adequately supported, opinion of the market value of

Chapter 7. Valuation Using the Sales Comparison and Cost Approaches. Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter 7 Valuation Using the Sales Comparison and Cost Approaches McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. Decision Making in Commercial Real Estate Centers

Chapter 7 Valuation Using the Sales Comparison and Cost Approaches McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. Decision Making in Commercial Real Estate Centers

Section Condominium and PUD Approval Requirements

Section 1.06 - Condominium and PUD Approval Requirements In This Section This section contains the following topics. Overview... 2 Related Bulletins... 3 Agency... 4 General Information on Condominium

Section 1.06 - Condominium and PUD Approval Requirements In This Section This section contains the following topics. Overview... 2 Related Bulletins... 3 Agency... 4 General Information on Condominium

APPRAISAL OF. A Single Family Attached Condominium Unit LOCATED AT: (REMOVED FOR SAMPLE) Chester, NY FOR: (REMOVED FOR SAMPLE) BORROWER:

Chester, NY FOR: (REMOVED FOR SAMPLE) BORROWER:") 048748784840 File No. 2007_Sample_1073 APPRAISAL OF A Single Family Attached Condominium Unit LOCATED AT: (REMOVED FOR SAMPLE) Chester, NY 10918 FOR: (REMOVED FOR SAMPLE) BORROWER: (REMOVED FOR SAMPLE)

048748784840 File No. 2007_Sample_1073 APPRAISAL OF A Single Family Attached Condominium Unit LOCATED AT: (REMOVED FOR SAMPLE) Chester, NY 10918 FOR: (REMOVED FOR SAMPLE) BORROWER: (REMOVED FOR SAMPLE)

The Buyer Consultation: Demonstrating & Articulating Value. Interactive Workshop. Student Workbook

The Buyer Consultation: Demonstrating & Articulating Value Interactive Workshop Student Workbook The Buyer Consultation: Demonstrating and Articulating your Value What is a Buyer Consultation? What is

The Buyer Consultation: Demonstrating & Articulating Value Interactive Workshop Student Workbook The Buyer Consultation: Demonstrating and Articulating your Value What is a Buyer Consultation? What is

Absolute Priority Appraisals, Inc. Other (describe)

") File No. 2 Case No. 18939 IMPROVEMENTS SITE NEIGHBORHOOD CONTRACT Uniform Residential Appraisal Report The purpose this summary appraisal report is to provide the lender/client with an accurate, and adequately

File No. 2 Case No. 18939 IMPROVEMENTS SITE NEIGHBORHOOD CONTRACT Uniform Residential Appraisal Report The purpose this summary appraisal report is to provide the lender/client with an accurate, and adequately

March 20, TO: All MAAO Members FROM: MAAO President Stephen C. Behrenbrinker, CAE, RE: MAAO-DOR Foreclosure Advisory Document

March 20, 2008 TO: All MAAO Members FROM: MAAO President Stephen C. Behrenbrinker, CAE, RE: MAAO-DOR Foreclosure Advisory Document Greetings! On behalf of the Minnesota Association of Assessing Officers

March 20, 2008 TO: All MAAO Members FROM: MAAO President Stephen C. Behrenbrinker, CAE, RE: MAAO-DOR Foreclosure Advisory Document Greetings! On behalf of the Minnesota Association of Assessing Officers

Page 1 of 6 Search: Broker BPO Results - FNMA BPO Form (V3) Valuations Logout Commands Broker BPO Results - FNMA BPO Form (V3) Property Address: 635 CAREFREE DR SAN DIEGO, CA 92114 (F-V8) BROKER'S PRICE

Page 1 of 6 Search: Broker BPO Results - FNMA BPO Form (V3) Valuations Logout Commands Broker BPO Results - FNMA BPO Form (V3) Property Address: 635 CAREFREE DR SAN DIEGO, CA 92114 (F-V8) BROKER'S PRICE

How to Read a Real Estate Appraisal Report

How to Read a Real Estate Appraisal Report Much of the private, corporate and public wealth of the world consists of real estate. The magnitude of this fundamental resource creates a need for informed

How to Read a Real Estate Appraisal Report Much of the private, corporate and public wealth of the world consists of real estate. The magnitude of this fundamental resource creates a need for informed

Basic Appraisal Procedures

Hondros Learning Basic Appraisal Procedures Timed Outline Topic Area Reference(s) Learning Objectives The student will be able to identify and/or apply: Teaching Method Time Segment (Minutes) Day 1 Chapter

Hondros Learning Basic Appraisal Procedures Timed Outline Topic Area Reference(s) Learning Objectives The student will be able to identify and/or apply: Teaching Method Time Segment (Minutes) Day 1 Chapter

SUBJECT: The Appraisal of Real Property That May Be Impacted by Environmental Contamination

1 ADVISORY OPINION 9 (AO-9) 1 2 3 4 This communication by the Appraisal Standards Board (ASB) does not establish new standards or interpret existing standards. Advisory Opinions are issued to illustrate

1 ADVISORY OPINION 9 (AO-9) 1 2 3 4 This communication by the Appraisal Standards Board (ASB) does not establish new standards or interpret existing standards. Advisory Opinions are issued to illustrate

APPENDIX A: VALUATION OF REAL ESTATE OWNED PROPERTIES A-1 REAL ESTATE OWNED (REO)

") APPENDIX A: VALUATION OF REAL ESTATE OWNED PROPERTIES 4150.2 A-1 REAL ESTATE OWNED (REO) FHA s Real Estate Owned (REO) properties are a result of paying a claim to a lending institution and the lender

APPENDIX A: VALUATION OF REAL ESTATE OWNED PROPERTIES 4150.2 A-1 REAL ESTATE OWNED (REO) FHA s Real Estate Owned (REO) properties are a result of paying a claim to a lending institution and the lender

Considering current and near future market trends and conditions, and all other information contained herein, our opinion is:

To be completed by Realtor and returned to Transferee/ BGRS Transferee Name: Property Address: Market Value Vacant Occupied by owner Occupied by tenant Considering current and near future market trends

To be completed by Realtor and returned to Transferee/ BGRS Transferee Name: Property Address: Market Value Vacant Occupied by owner Occupied by tenant Considering current and near future market trends

RESIDENTIAL APPRAISAL SUMMARY REPORT

APPRAISAL SUMMARY REPORT SUBJECT ASSIGNMENT SALES COMPARISON APPROACH Lic #: 80000019 Page #1 File No.: : City: WHITE PLAINS State: NY Zip Code: County: WESTCHESTER Legal Description: Assessor's Parcel

APPRAISAL SUMMARY REPORT SUBJECT ASSIGNMENT SALES COMPARISON APPROACH Lic #: 80000019 Page #1 File No.: : City: WHITE PLAINS State: NY Zip Code: County: WESTCHESTER Legal Description: Assessor's Parcel

BPOSG BROKER PRICE OPINION. Version 4.0 September 16, BSB BPO Standards Board

BPOSG BROKER PRICE OPINION Standards & Version 4.0 September 16, 2010 BSB BPO Standards Board BSB BPO Standards Board 6619 North Scottsdale Road Scottsdale, Arizona 85250 BPOSG Table of Contents: Para

BPOSG BROKER PRICE OPINION Standards & Version 4.0 September 16, 2010 BSB BPO Standards Board BSB BPO Standards Board 6619 North Scottsdale Road Scottsdale, Arizona 85250 BPOSG Table of Contents: Para

Seminar Topics. Seminar Schedule. Fannie Mae Collateral Underwriter and Appraiser Quality Management An Overview 4/6/2016

Fannie Mae and Appraiser Quality Management An Overview Missouri Appraiser Advisory Council Educational Conference Jefferson City, Missouri April 8, 2016 Greg Stephens, SRA, MNAA, CDEI Chief Appraiser,

Fannie Mae and Appraiser Quality Management An Overview Missouri Appraiser Advisory Council Educational Conference Jefferson City, Missouri April 8, 2016 Greg Stephens, SRA, MNAA, CDEI Chief Appraiser,

https://ort.quandis.com/decision/importformrender.aspx?importformid=

Page 1 of 5 Search: Broker BPO Results - FNC BPO Form Valuations Logout Commands Broker BPO Results - FNC BPO Form Property Address: 4318 S KING DR, Unit: 3S CHICAGO, IL 60653 (CNF-V1) BROKER'S PRICE OPINION

Page 1 of 5 Search: Broker BPO Results - FNC BPO Form Valuations Logout Commands Broker BPO Results - FNC BPO Form Property Address: 4318 S KING DR, Unit: 3S CHICAGO, IL 60653 (CNF-V1) BROKER'S PRICE OPINION

Released: February 8, 2011

Released: February 8, 2011 Commentary 2 The Numbers That Drive Real Estate 3 Recent Government Action 10 Topics for Home Buyers, Sellers, and Owners 13 Brought to you by: KW Research Commentary Gradual

Released: February 8, 2011 Commentary 2 The Numbers That Drive Real Estate 3 Recent Government Action 10 Topics for Home Buyers, Sellers, and Owners 13 Brought to you by: KW Research Commentary Gradual

Guide to Appraisal Reports

Guide to Appraisal Reports What is an appraisal? An appraisal is an independent valuation of real property prepared by a qualified Appraiser and fully documented in a report. Based on a series of appraisal

Guide to Appraisal Reports What is an appraisal? An appraisal is an independent valuation of real property prepared by a qualified Appraiser and fully documented in a report. Based on a series of appraisal

Section 1.07 Appraisal Guidelines

Section 1.07 Appraisal Guidelines In This Policy Section This policy section contains the following topics. Overview... 3 Introduction... 3 Guideline Summary... 3 Related Bulletins... 6 Appraisers... 7

Section 1.07 Appraisal Guidelines In This Policy Section This policy section contains the following topics. Overview... 3 Introduction... 3 Guideline Summary... 3 Related Bulletins... 6 Appraisers... 7

EMPLOYEE RELOCATION COUNCIL SUMMARY APPRAISAL REPORT

EMPLOYEE RELOCATION COUNCIL SUMMARY APPRAISAL REPORT Client: Client File #: Client Address: Suite #: Homeowner: Subject Property Address: County: Appraiser Company Name: TOMAINO APPRAISAL Appraiser File

EMPLOYEE RELOCATION COUNCIL SUMMARY APPRAISAL REPORT Client: Client File #: Client Address: Suite #: Homeowner: Subject Property Address: County: Appraiser Company Name: TOMAINO APPRAISAL Appraiser File

Section Leasehold Estate Guidelines

Section 1.10 - In This Section This section contains the following topics: Overview... 2 General... 2 Related Bulletins... 3 Identifying a Leasehold Estate... 4 Occupancy/Property Types... 5 Eligible Occupancy/

Section 1.10 - In This Section This section contains the following topics: Overview... 2 General... 2 Related Bulletins... 3 Identifying a Leasehold Estate... 4 Occupancy/Property Types... 5 Eligible Occupancy/

LETTER OF TRANSMITTAL

Bradford Technologies, Inc CVR Specialist 302 Piercy Rd San Jose, CA 95138 LETTER OF TRANSMITTAL To: Strong Dollar Reserves 1-122 Wall Street New York, NY 10043 Re: File Number: Client Ref: 00018210 In

Bradford Technologies, Inc CVR Specialist 302 Piercy Rd San Jose, CA 95138 LETTER OF TRANSMITTAL To: Strong Dollar Reserves 1-122 Wall Street New York, NY 10043 Re: File Number: Client Ref: 00018210 In

Following is an example of an income and expense benchmark worksheet:

After analyzing income and expense information and establishing typical rents and expenses, apply benchmarks and base standards to the reappraisal area. Following is an example of an income and expense

After analyzing income and expense information and establishing typical rents and expenses, apply benchmarks and base standards to the reappraisal area. Following is an example of an income and expense

EXTERIOR APPRAISAL OF A TWO FAMILY HOUSE

Form GA1V - "TOTAL" appraisal software by a la mode, inc. - 1-800-ALAMODE EXTERIOR APPRAISAL OF A TWO FAMILY HOUSE LOCATED AT -6118 Volume 8558 page 216 FOR William W. Ward, Esq 1318 Bedford St Stamford,

Form GA1V - "TOTAL" appraisal software by a la mode, inc. - 1-800-ALAMODE EXTERIOR APPRAISAL OF A TWO FAMILY HOUSE LOCATED AT -6118 Volume 8558 page 216 FOR William W. Ward, Esq 1318 Bedford St Stamford,

Chapter 5 Fee Appraiser Responsibilities

Chapter 5 Fee Appraiser Responsibilities The fee appraiser is responsible for all aspects of the appraisal process. Important: Certain key appraisal functions may not be delegated to anyone else. Failure

Chapter 5 Fee Appraiser Responsibilities The fee appraiser is responsible for all aspects of the appraisal process. Important: Certain key appraisal functions may not be delegated to anyone else. Failure

Fannie Mae Selling Guide (04/12/2002) Part XI - Property and Appraisal Guidelines

Part XI - Property and Appraisal Guidelines") Fannie Mae Selling Guide (04/12/2002) Part XI - Property and Appraisal Guidelines This Part-Property and Appraisal Guidelines-details our general requirements for analyzing the property appraisal aspects

Fannie Mae Selling Guide (04/12/2002) Part XI - Property and Appraisal Guidelines This Part-Property and Appraisal Guidelines-details our general requirements for analyzing the property appraisal aspects

Interagency Appraisal and

Interagency Appraisal and Evaluation (IAEG) Workshop Purpose (77456) Supersedes the 1994 Interagency Appraisal & Evaluation Guidelines Address supervisory matters relating to real estate appraisal and

Interagency Appraisal and Evaluation (IAEG) Workshop Purpose (77456) Supersedes the 1994 Interagency Appraisal & Evaluation Guidelines Address supervisory matters relating to real estate appraisal and

A Demonstration Appraisal Report. Of a. Located at. Date of Appraisal. Prepared for. Prepared by

A Demonstration Appraisal Report Of a Located at Date of Appraisal Prepared for Prepared by International Association of Assessing Officers Professional Designation Subcommittee 314 W. 10 th Street Kansas

A Demonstration Appraisal Report Of a Located at Date of Appraisal Prepared for Prepared by International Association of Assessing Officers Professional Designation Subcommittee 314 W. 10 th Street Kansas