The Accuracy of Automated Valuation Models

|

|

|

- Irma Underwood

- 5 years ago

- Views:

Transcription

1 The Accuracy of Automated Valuation Models European Valuation Conference Belgrade 20 th -22 nd April 2017 Professor George Matysiak

2 Agenda AVMs Examples of valuation accuracy More transparency

3 Study work in progress Invited by TEGoVA to look at AVMs, including the valuation accuracy of AVMs. Despite AVMs having been developed and refined over the years, they are still regarded as having shortcomings and their accuracy record in assessing market prices or values appears to be mixed. Several lines of investigation have been followed, including: - Identifying publicly available information - Identifying/contacting selected providers of AVMs in the UK and the US - Identifying relevant reports/papers prepared by professional bodies - Identifying academic work in the area - Identifying trade press material and commentary on AVMs - Identifying relevant AVM Websites - Sifting through popular commentary (of which there is much) dotted around the web and various trade sources. It should be stated at the outset, the information available on US AVM providers far outweighed that for European AVMs.

4 Introduction AVMs AVMs have their origins in North America, the first commercial application being in 1981, and began to be developed in the UK in the 1990s. Despite traditional approaches being extensively employed in the valuation profession, there has been a significant growth in independent residential Automated Valuation Model (AVM) providers, who offer their services routinely on a fee-based basis, to both lenders and the fee-paying public. AVMs are widely used by lenders and institutional investors, largely for monitoring purposes, and are seen as complementary to traditional valuations. The widespread use of AVMs is now firmly established. These computer-assisted quantitative methods have some advantage in that they are systematic and fast, thereby reducing reliance on labour input in providing an end-to-end valuation. By removing the human element, it is claimed by some advocates, it also reduces inaccuracies due to reliance on human judgement. This is an unsubstantiated assertion. However, the overall attitude and degree of acceptance of such automated approachs to valuation varies.

5 What is an AVM 1? Although different underlying AVM models are employed by vendors, fundamental to the approach are statistical, data mining and computing technicalities. TEGoVA provide the following, Definition 2.1, in their European Valuation Standards EVIP 6: Automated Valuation Models (AVMs) can be defined as statistic-based computer programmes, which use property information (e.g. comparable sales and property characteristics etc.) to generate property-related values or suggested values. The International Association of Assessing Officers, IAAO (2003), describes an AVM as a mathematically based computer software programme that produces an estimate of market value based on analysis of location, market conditions, and real estate characteristics from information collected. The distinguishing feature of an AVM is that it produces a market valuation through mathematical modelling. The credibility of an AVM is dependent on the data used and the skills of the modeller producing the AVM.

6 What is an AVM 2? The following definition of an Automated Valuation Model is provided by the RICS AVM Standards Working Group: Automated Valuation Models use one or more mathematical techniques to provide an estimate of value of a specified property at a specified date, accompanied by a measure of confidence in the accuracy of the result, without human intervention post-initiation. (RICS 2013). A key component in the RICS definition is the qualification accompanied by a measure of confidence in the accuracy of the result. All three definitions of an AVM exclude any valuer involvement in arriving at a value.

7 An AVM prediction?

8 Practitioner attitudes towards AVMs An international survey undertaken in 2008 on AVMs and the integration of AVMs within the valuation process provides some interesting findings. There were 473 valuer responses, representing both lending and valuation organisations, and described as senior professional members with much experience of mortgage valuations. The results of the survey include the following : 71% of the valuers agreed that AVMs were inadequate for loan valuations as a result of no physical inspection. 87% of the valuers agreed that physical valuations were more accurate than AVMs, as a result of local knowledge. 90% of valuers agreed that the ability to evaluate comparables was a major advantage over AVMs. It would be interesting to revisit the findings as the AVM market will have developed since the survey was undertaken.

9 Qualifying the role of AVMs Emphasising the effective role and use of AVMs, Hometrack s view is: Understanding the inputs and processes is key but it s the accuracy, quality and consistency of the outputs against a clear benchmark valuation that is most relevant to end users. Knowing when not to use an AVM is as important as having the confidence to use one. The vendors themselves recognise that their AVM s will not provide accurate valuations in all situations, and caution the conditions under which their use is appropriate. Filtering processes are put in place in order to exclude outliers.

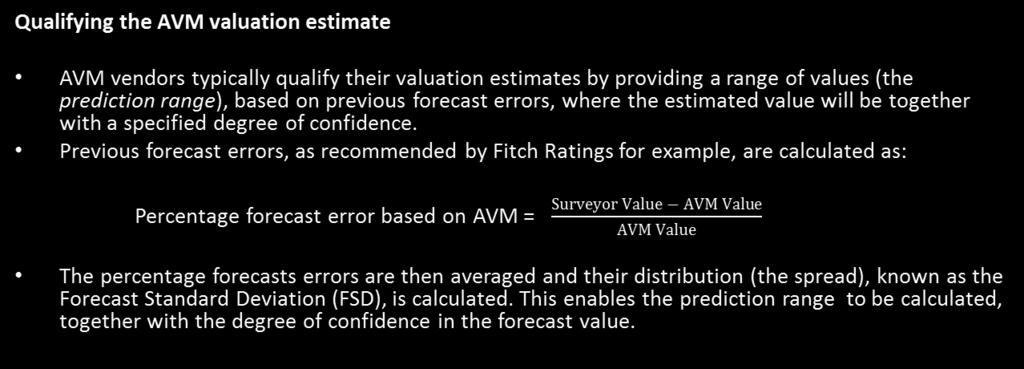

10 Measuring accuracy 1 A variety of ways to measure AVM valuation error. First, a benchmark reference needs to be established: Issues. - is the AVM forecast measured relative to a valuer s estimate of the property s price or, - is the AVM forecast measured relative to the market price achieved in the market? Fitch, for example, evaluate model accuracy based on surveyors assessment of values. UK vendors did not provide any details.

11 Measuring accuracy 2 US vendors publish results based on achieved market prices. How can accuracy be shown? Several ways: - can look at the percentage of AVMs falling within a specified range of error, for example within: +/- 5%, +/-10%, or +/-20% - the spread around the average of all errors (FSD) - the median (50% of values are less than the median and 50% of values are greater than the median). - average of the absolute errors (MAD/MAPE)

12

13 Information on AVMs 1 Debate regarding the role and accuracy of AVM valuations is an ongoing topic of discussion. For there to be a meaningful debate, AVM vendors need to make available access to their models for independent testing and verification of the models output and accuracy of the results. Whilst there are a large number of AVM vendors, the inner functioning of the models and details of their specification are not released, nor are accuracy figures disclosed. Vendors claim they test their models regularly for accuracy, and some may have the figures independently assessed. However, this non-disclosure puts a constraint on the analysis which can be externally undertaken as regards the assessment of the reliability and accuracy of the models. Despite exchange of correspondence with UK vendors and the European AVM Alliance (EAA), only broad promotional material was provided. The upshot is that all were very guarded in terms of the details which they were willing to release.

14 Information on AVMs 2 Other than submitting information to rating agencies, UK AVM operators are unwilling to have their data/methodologies exposed to independent scrutiny. Vendors argue that their accuracy figures need to be put into a wider perspective. The overall impression is that the UK AVM vendors are unwilling to engage in a discussion about the valuation accuracy of their products. US AVM market is highly developed and accuracy figures are available on websites in the following two examples of accuracy, figures are based on US data.

15 Some accuracy figures - HouseCanary The Table shows the minimum/maximum percentage of AVM valued properties within a range of +/- 10% of the sales price, and the minimum and maximum median figures across 50 US States for the US AVM vendor HouseCanary (who operate 8 individual AVMs). HouseCanary: Distribution of Valuation accuracy across 50 USA States, February 2017 Statistic Within +/- 10% Median Min 39.9% 3.4% Max 81.5% 15.0% Source: HouseCanary Website There are considerable differences in the distribution of accuracy across the 50 States. HouseCanary claim they provide the most accurate AVM valuations online which are independently verified.

16 More accuracy figures 1 Zillow Zillow claim to be the largest AVM provider in the US. The following three histograms show the distribution of Zillow s AVM accuracy rates for 666 US Counties. - they show the distribution of AVM valuation accuracy within each of the individual 666 Counties.

17 A1: Zillow s distribution of Valuation accuracy within +/- 5% of Sales Price

18 A2: Zillow s distribution of Valuation accuracy within +/- 10% of Sales Price

19 A3: Zillow s distribution of Valuation accuracy within +/- 20% of Sales Price

20 More accuracy figures 2 Zillow Figure A1: shows +/- 5% valuation accuracy rates; Figure A2: +/- 10% valuation accuracy rates and Figure A3: +/- 20% valuation accuracy rates. The Histograms provide a detailed visual insight across the 666 US Counties. The average accuracy across all counties is superimposed in order to provide a reference point. On balance, it appears that some 50% of the valuations are likely be outside the +/- 5% range of achieved sales price, which falls to 30% for the +/- 10% range and 15% for the +/- 20% range, as reported in Table 3. As can be seen from the histograms, given the skewed nature of the distributions, even at the wider range of +/- 20%, there exist a significant proportion of valuations in many locations, which lie outside the specified ranges of accuracy.

21 Summarising Zillow s accuracy figures The figures show the following: - The median level of valuation error across 666 Counties in the US is 6.0%. Meaning, half of the errors nationwide were within 6% of the final selling price, and half exceed 6.0% errors. - At the individual County level, the median ranged from 3% to 25%, which represents a wide range of variation across the different locations. - On average, almost half of all valuations across all Counties were within +/- 5% of the sales price, half being excess of +/- 5%. However, in one County only 9% of the valuations were within the 5% bracket, with highest recorded accuracy figure being 76%. - On average, the percentage of valuations across all Counties falling within +/- 10 % of the sales price is 70%. This can vary between 20% and 92%, depending on the County. - On average, the percentage of valuations across all Counties falling within +/- 20% of the sales price is 85%. However, this can vary between 37% and 100%, depending on the County.

22 Margin for Error What is an acceptable margin for error level? - a long established concept developed in case law. Very little evidence for residential property markets. Market conditions will likely raise or lower the margin. Evidence from commercial real estate markets may provide an indication of an upper limit on accuracy. Some examples: - valuations compared against achieved market prices. - European countries: Averages over and 2015() Country Average Absolute Difference (%) Netherlands 9.0 (7.2) Italy 9.8 (8.8) Germany 11.9 (9.4) UK 9.9 (10.2) France 10.7 (12.7) Sweden 12.6 (12.9) Switzerland 10.7 (14.0) Source MSCI: Figs are weighted averages

23 Valuations under different conditions Is the margin for error unchanging i.e. constant? No, it will vary under different conditions. There is a whole series of circumstances which would need to be taken into consideration when looking to assess what would be an acceptable margin for error in valuing residential properties, including the following: - different market environments, such as rising/falling prices - different size/valued properties - quality of property - age of property - market liquidity e.g. dependent on the volume of transactions - geographic location/different neighbourhoods - type of property All are likely to vary by country!

24 Observations and questions 1 The distribution of the accuracy figures of the US models, across both locations and within locations, appears to provide tolerable results within what could be considered acceptable levels of statistical confidence. However, a purely statistically derived or data-mined valuation (an AVM) risks being widely off the mark, lying well outside the +/- percentage ranges, as shown in the Zillow charts for example. Does the valuer possess additional information to that contained in the AVM? Are AVMs more accurate than physical valuations?

25 Observations and questions 2 Despite the high degree of accuracy reported by some US AVM vendors, there still remains a requirement for professional judgement to augment model-based valuations in arriving at a more broadly considered opinion of value. Requirement for more discussion about what is a fitting framework for assessing and evaluating AVMs. Effective independent validation of AVMs is hampered by the lack of industry standardisation across virtually all aspects of the AVM process, including access to underlying data, models and accuracy results. Vendors concerns about commercial sensitivity/intellectual property of their products prevail.

26 Making headway 1 challenges The independent validation and standards of validation of European AVMs needs to be promoted more vigorously, otherwise the role of AVMs will continue to be contested. How best to proceed? In the absence of regulatory/enforcible controls, there has to be a commercial or reputational benefit to the vendor in order to make it worthwhile for them to provide information. Independent professional bodies qualified to scrutinise AVMs - setting a standard of best practice for AVM vendors - access to the underlying models - access to database(s) on which the models are calibrated/estimated/tested - access to AVM output under different market environments and any adjustment made to pure model forecasts - AVM accuracy/standardisation of published accuracy measures - clear definitions/standards for transparent testing of AVMs procedures

27 Making headway 2 challenges Certification, implying positive publicity. Alternatively, more voluntary information from AVM vendors, but issues of impartiality arise. User education. Users AVM experience.

28 The Accuracy of Automated Valuation Models European Valuation Conference Belgrade 20 th -22 nd April 2017 Professor George Matysiak

Residential Automated Valuation models - AVMs. Examples of AVM valuation (appraisal) accuracy

accuracy") Agenda Residential Automated Valuation models - AVMs Examples of AVM valuation (appraisal) accuracy Challenges Ongoing work analysing prices and AVM valuations analysing errors Importance of accurate residential

Agenda Residential Automated Valuation models - AVMs Examples of AVM valuation (appraisal) accuracy Challenges Ongoing work analysing prices and AVM valuations analysing errors Importance of accurate residential

ASSESSING THE ACCURACY OF INDIVIDUAL PROPERTY VALUES ESTIMATED BY AUTOMATED VALUATION MODELS GEORGE ANDREW MATYSIAK

ASSESSING THE ACCURACY OF INDIVIDUAL PROPERTY VALUES ESTIMATED BY AUTOMATED VALUATION MODELS GEORGE ANDREW MATYSIAK ABOUT ABOUT THE AUTHOR PROFESSOR GEORGE ANDREW MATYSIAK 2 George Matysiak is a financial

ASSESSING THE ACCURACY OF INDIVIDUAL PROPERTY VALUES ESTIMATED BY AUTOMATED VALUATION MODELS GEORGE ANDREW MATYSIAK ABOUT ABOUT THE AUTHOR PROFESSOR GEORGE ANDREW MATYSIAK 2 George Matysiak is a financial

EVGN 11. The Valuer s Use of Statistical Tools

EVGN 11 The Valuer s Use of Statistical Tools 1. Introduction 2. Preconditions for the use of AVMs 3. Limitations on the use of AVMs once the preconditions have been met 4. Portfolio valuation 1. Introduction

EVGN 11 The Valuer s Use of Statistical Tools 1. Introduction 2. Preconditions for the use of AVMs 3. Limitations on the use of AVMs once the preconditions have been met 4. Portfolio valuation 1. Introduction

AVM Validation. Evaluating AVM performance

AVM Validation Evaluating AVM performance The responsible use of Automated Valuation Models in any application begins with a thorough understanding of the models performance in absolute and relative terms.

AVM Validation Evaluating AVM performance The responsible use of Automated Valuation Models in any application begins with a thorough understanding of the models performance in absolute and relative terms.

Glossary of Terms & Definitions

Glossary of Terms & Definitions European AVM Alliance Independent - Transparent - Unbiased Key AVM Terms Term Definition Remarks Automated Model (AVM) AVM Performance AVM Coverage AVM Accuracy A system

Glossary of Terms & Definitions European AVM Alliance Independent - Transparent - Unbiased Key AVM Terms Term Definition Remarks Automated Model (AVM) AVM Performance AVM Coverage AVM Accuracy A system

EVS Wolfgang Kaelberer, Hon REV. Global Valuation Opportunities and Challenges: European Valuation Standards

Global Valuation Opportunities and Challenges: European Valuation Standards EVS 2016 Wolfgang Kaelberer, Hon REV Member of the Board of TEGoVA Member of the EVS Standards Board 1 Resolved to: remain clearly

Global Valuation Opportunities and Challenges: European Valuation Standards EVS 2016 Wolfgang Kaelberer, Hon REV Member of the Board of TEGoVA Member of the EVS Standards Board 1 Resolved to: remain clearly

Automated Valuation Model

Automated Valuation Model An innovative tool for Market Intelligence and Risk Management June 2015 Regulated by RICS EPS - Introduction Established presence in SEE: Greece (since 2000) & Romania, Bulgaria

Automated Valuation Model An innovative tool for Market Intelligence and Risk Management June 2015 Regulated by RICS EPS - Introduction Established presence in SEE: Greece (since 2000) & Romania, Bulgaria

International Conference A comprehensive approach to NPL resolution international experiences Collateral valuation an appraisers perspective

International Conference A comprehensive approach to NPL resolution international experiences Collateral valuation an appraisers perspective Krzysztof Grzesik FRICS REV Chairman TEGoVA Vienna 16 th May

International Conference A comprehensive approach to NPL resolution international experiences Collateral valuation an appraisers perspective Krzysztof Grzesik FRICS REV Chairman TEGoVA Vienna 16 th May

*Predicted median absolute deviation of a CASA value estimate from the sale price

PLATINUMdata Premier AVM Products ACA The AVM offers lenders a concise one-page summary of a property s current estimated value, complete with five recent comparable sales, neighborhood value data, homeowner

PLATINUMdata Premier AVM Products ACA The AVM offers lenders a concise one-page summary of a property s current estimated value, complete with five recent comparable sales, neighborhood value data, homeowner

CLIENT PERCEPTIONS OF THE QUALITY OF VALUATION REPORTS IN AUSTRALIA

CLIENT PERCEPTIONS OF THE QUALITY OF VALUATION REPORTS IN AUSTRALIA ABSTRACT GRAEME NEWELL University of Western Sydney A survey of external users of commercial valuation reports was conducted in April

CLIENT PERCEPTIONS OF THE QUALITY OF VALUATION REPORTS IN AUSTRALIA ABSTRACT GRAEME NEWELL University of Western Sydney A survey of external users of commercial valuation reports was conducted in April

Surveyors Professional Supplementary Survey and Valuation

Surveyors Professional Supplementary Survey and Valuation Instructions To be completed where the Proposer/Insured carries out Survey and Valuation activities. If there is insufficient space to provide

Surveyors Professional Supplementary Survey and Valuation Instructions To be completed where the Proposer/Insured carries out Survey and Valuation activities. If there is insufficient space to provide

THE ACCURACY OF COMMERCIAL PROPERTY VALUATIONS

THE ACCURACY OF COMMERCIAL PROPERTY VALUATIONS ASSOCIATE PROFESSOR GRAEME NEWELL School of Land Economy University of Western Sydney, Hawkesbury and ROHIT KISHORE School of Land Economy University of Western

THE ACCURACY OF COMMERCIAL PROPERTY VALUATIONS ASSOCIATE PROFESSOR GRAEME NEWELL School of Land Economy University of Western Sydney, Hawkesbury and ROHIT KISHORE School of Land Economy University of Western

Viability and the Planning System: The Relationship between Economic Viability Testing, Land Values and Affordable Housing in London

Viability and the Planning System: The Relationship between Economic Viability Testing, Land Values and Affordable Housing in London Executive Summary & Key Findings A changed planning environment in which

Viability and the Planning System: The Relationship between Economic Viability Testing, Land Values and Affordable Housing in London Executive Summary & Key Findings A changed planning environment in which

Fair value implications for the real estate sector and example disclosures for real estate entities. Applying IFRS in Real Estate

Applying IFRS in Real Estate IFRS 13 Fair Value Measurement Fair value implications for the real estate sector and example disclosures for real estate entities January 2013 Contents Introduction... 2 Section

Applying IFRS in Real Estate IFRS 13 Fair Value Measurement Fair value implications for the real estate sector and example disclosures for real estate entities January 2013 Contents Introduction... 2 Section

Interagency Appraisal and

Interagency Appraisal and Evaluation (IAEG) Workshop Purpose (77456) Supersedes the 1994 Interagency Appraisal & Evaluation Guidelines Address supervisory matters relating to real estate appraisal and

Interagency Appraisal and Evaluation (IAEG) Workshop Purpose (77456) Supersedes the 1994 Interagency Appraisal & Evaluation Guidelines Address supervisory matters relating to real estate appraisal and

86 years in the making Caspar G Haas 1922 Sales Prices as a Basis for Estimating Farmland Value

2 Our Journey Begins 86 years in the making Caspar G Haas 1922 Sales Prices as a Basis for Estimating Farmland Value Starting at the beginning. Mass Appraisal and Single Property Appraisal Appraisal

2 Our Journey Begins 86 years in the making Caspar G Haas 1922 Sales Prices as a Basis for Estimating Farmland Value Starting at the beginning. Mass Appraisal and Single Property Appraisal Appraisal

International Accounting Standards Board Press Release

International Accounting Standards Board Press Release 31 March 2004 IASB ISSUES STANDARDS ON BUSINESS COMBINATIONS, GOODWILL AND INTANGIBLE ASSETS The International Accounting Standards Board (IASB) today

International Accounting Standards Board Press Release 31 March 2004 IASB ISSUES STANDARDS ON BUSINESS COMBINATIONS, GOODWILL AND INTANGIBLE ASSETS The International Accounting Standards Board (IASB) today

The purpose of the appraisal was to determine the value of this six that is located in the Town of St. Mary s.

The purpose of the appraisal was to determine the value of this six that is located in the Town of St. Mary s. The subject property was originally acquired by Michael and Bonnie Etta Mattiussi in August

The purpose of the appraisal was to determine the value of this six that is located in the Town of St. Mary s. The subject property was originally acquired by Michael and Bonnie Etta Mattiussi in August

TOWARDS E-LAND ADMINISTRATION - ELECTRONIC PLANS OF SUBDIVISIONS IN VICTORIA

TOWARDS E-LAND ADMINISTRATION - ELECTRONIC PLANS OF SUBDIVISIONS IN VICTORIA Mohsen Kalantari 1, Chris Lester 2, David R Boyle 3, Neil Coupar 4 1 eplan Coordinator 2 SPEAR Manager 3 Deputy Surveyor General

TOWARDS E-LAND ADMINISTRATION - ELECTRONIC PLANS OF SUBDIVISIONS IN VICTORIA Mohsen Kalantari 1, Chris Lester 2, David R Boyle 3, Neil Coupar 4 1 eplan Coordinator 2 SPEAR Manager 3 Deputy Surveyor General

Property valuation is an integral part of the housing industry

Spotlight AVMs The Next Generation of AVMs Clifford A. Lipscomb, Ph.D., MRICS Editor s Note: This article is adapted from Building a Better Home Value Mousetrap, which appeared in the December 2016 issue

Spotlight AVMs The Next Generation of AVMs Clifford A. Lipscomb, Ph.D., MRICS Editor s Note: This article is adapted from Building a Better Home Value Mousetrap, which appeared in the December 2016 issue

The TAUREAN Residential Valuation System An Overview

The TAUREAN Residential Valuation System An Overview By Michael L. Robbins, Ph.D., CRE Taurean Residential Valuation Services, LLC 150 N. Sunny Slope Road, Suite 225, Brookfield, WI 53005 Phone: (262)

The TAUREAN Residential Valuation System An Overview By Michael L. Robbins, Ph.D., CRE Taurean Residential Valuation Services, LLC 150 N. Sunny Slope Road, Suite 225, Brookfield, WI 53005 Phone: (262)

D DAVID PUBLISHING. Mass Valuation and the Implementation Necessity of GIS (Geographic Information System) in Albania

in Albania") Journal of Civil Engineering and Architecture 9 (2015) 1506-1512 doi: 10.17265/1934-7359/2015.12.012 D DAVID PUBLISHING Mass Valuation and the Implementation Necessity of GIS (Geographic Elfrida Shehu

Journal of Civil Engineering and Architecture 9 (2015) 1506-1512 doi: 10.17265/1934-7359/2015.12.012 D DAVID PUBLISHING Mass Valuation and the Implementation Necessity of GIS (Geographic Elfrida Shehu

APES 225 Valuation Services

APES 225 Valuation Services [Supersedes APES 225 Valuation Services issued in July 2008 and revised in May 2012] Prepared and issued by Accounting Professional & Ethical Standards Board Limited REVISED:

APES 225 Valuation Services [Supersedes APES 225 Valuation Services issued in July 2008 and revised in May 2012] Prepared and issued by Accounting Professional & Ethical Standards Board Limited REVISED:

TECHNICAL INFORMATION PAPER VALUATION OF SELF STORAGE FACILITIES

TECHNICAL INFORMATION PAPER VALUATION OF SELF STORAGE FACILITIES Reference ANZVTIP 5 Valuation of Self Storage Facilities Effective 23 November 2016 Review Owner National Manager Professional Standards

TECHNICAL INFORMATION PAPER VALUATION OF SELF STORAGE FACILITIES Reference ANZVTIP 5 Valuation of Self Storage Facilities Effective 23 November 2016 Review Owner National Manager Professional Standards

TECHNICAL INFORMATION PAPER - VALUATIONS OF REAL PROPERTY, PLANT & EQUIPMENT FOR USE IN AUSTRALIAN FINANCIAL REPORTS

TECHNICAL INFORMATION PAPER - VALUATIONS OF REAL PROPERTY, PLANT & EQUIPMENT FOR USE IN AUSTRALIAN FINANCIAL REPORTS Reference ANZVTIP 8 Valuations of Real Property, Plant & Equipment for Use in Australian

TECHNICAL INFORMATION PAPER - VALUATIONS OF REAL PROPERTY, PLANT & EQUIPMENT FOR USE IN AUSTRALIAN FINANCIAL REPORTS Reference ANZVTIP 8 Valuations of Real Property, Plant & Equipment for Use in Australian

ENGLISH RURAL HOUSING ASSOCIATION

ENGLISH RURAL HOUSING ASSOCIATION VALUE FOR MONEY STATEMENT 2015 ENGLISH RURAL HOUSING ASSOCIATION VALUE FOR MONEY STATEMENT 2015 Contents 1. What do we mean by Value for Money? 2. How do our assets perform,

ENGLISH RURAL HOUSING ASSOCIATION VALUE FOR MONEY STATEMENT 2015 ENGLISH RURAL HOUSING ASSOCIATION VALUE FOR MONEY STATEMENT 2015 Contents 1. What do we mean by Value for Money? 2. How do our assets perform,

VALUATION REPORTING REVISED Introduction. 3.0 Definitions. 2.0 Scope INTERNATIONAL VALUATION STANDARDS 3

4.4 INTERNATIONAL VALUATION STANDARDS 3 REVISED 2007 1.0 Introduction 1.1 The critical importance of a Valuation Report, the final step in the valuation process, lies in communicating the value conclusion

4.4 INTERNATIONAL VALUATION STANDARDS 3 REVISED 2007 1.0 Introduction 1.1 The critical importance of a Valuation Report, the final step in the valuation process, lies in communicating the value conclusion

Real Estate Reference Material

Valuation Land valuation Land is the basic essential of property development and unlike building commodities - such as concrete, steel and labour - it is in relatively limited supply. Quality varies between

Valuation Land valuation Land is the basic essential of property development and unlike building commodities - such as concrete, steel and labour - it is in relatively limited supply. Quality varies between

Welsh Government Housing Policy Regulation

www.cymru.gov.uk Welsh Government Housing Policy Regulation Regulatory Assessment Report Wales & West Housing Association Ltd L032 December 2015 Welsh Government Regulatory Assessment The Welsh Ministers

www.cymru.gov.uk Welsh Government Housing Policy Regulation Regulatory Assessment Report Wales & West Housing Association Ltd L032 December 2015 Welsh Government Regulatory Assessment The Welsh Ministers

next generation automated collateral risk solution for those who demand true valuation

next generation automated collateral risk solution for those who demand true valuation ValueGUARD provides you with the added confidence to make sound financial decisions. Key Benefits Easy to understand

next generation automated collateral risk solution for those who demand true valuation ValueGUARD provides you with the added confidence to make sound financial decisions. Key Benefits Easy to understand

The Influence of EU Regulation and European Valuation Standards on Real Estate Valuation

The Influence of EU Regulation and European Valuation Standards on Real Estate Valuation Thessaloniki 9 th October 2015 Krzysztof Grzesik REV Chairman TEGoVA The European Group of Valuers Associations

The Influence of EU Regulation and European Valuation Standards on Real Estate Valuation Thessaloniki 9 th October 2015 Krzysztof Grzesik REV Chairman TEGoVA The European Group of Valuers Associations

A conceptual framework for enhancing effectiveness in the service charge process Received (in revised form): 19 th January 2010

: 19 th January 2010") Original Article A conceptual framework for enhancing effectiveness in the service charge process Received (in revised form): 19 th January 2010 Timothy Eccles is Senior Lecturer at Kingston University,

Original Article A conceptual framework for enhancing effectiveness in the service charge process Received (in revised form): 19 th January 2010 Timothy Eccles is Senior Lecturer at Kingston University,

NCC Group plc. Preliminary Annual Results for the year ended 31 May 2009

NCC Group plc Preliminary Annual Results for the year ended 31 May 2009 July 2009 AGENDA Agenda Highlights Track record Group structure Group financials Group strategy Group sector concentrations Group

NCC Group plc Preliminary Annual Results for the year ended 31 May 2009 July 2009 AGENDA Agenda Highlights Track record Group structure Group financials Group strategy Group sector concentrations Group

Appraisal Review & Advisory Opinion 20 Controversy. Presenter: Lisa Kimbro, MAI, AI-GRS

Appraisal Review & Advisory Opinion 20 Controversy Presenter: Lisa Kimbro, MAI, AI-GRS Practicing appraisers know USPAP, and appraisers that complete review work know USPAP s Standard 3. But what about

Appraisal Review & Advisory Opinion 20 Controversy Presenter: Lisa Kimbro, MAI, AI-GRS Practicing appraisers know USPAP, and appraisers that complete review work know USPAP s Standard 3. But what about

TECHNICAL INFORMATION PAPER - MARKET VALUE OF PROPERTY, PLANT & EQUIPMENT IN A BUSINESS

TECHNICAL INFORMATION PAPER - MARKET VALUE OF PROPERTY, PLANT & EQUIPMENT IN A BUSINESS Please view the video for this Technical Information Paper Reference ANZVTIP 2 Effective 1 st July 2015 Owner National

TECHNICAL INFORMATION PAPER - MARKET VALUE OF PROPERTY, PLANT & EQUIPMENT IN A BUSINESS Please view the video for this Technical Information Paper Reference ANZVTIP 2 Effective 1 st July 2015 Owner National

86M 4.2% Executive Summary. Valuation Whitepaper. The purposes of this paper are threefold: At a Glance. Median absolute prediction error (MdAPE)

") Executive Summary HouseCanary is developing the most accurate, most comprehensive valuations for residential real estate. Accurate valuations are the result of combining the best data with the best models.

Executive Summary HouseCanary is developing the most accurate, most comprehensive valuations for residential real estate. Accurate valuations are the result of combining the best data with the best models.

Real Estate Companies A Business Valuation Primer (Series 1)

") Article Real Estate Companies A Business Valuation Primer (Series 1) May 2018 Families and organizations that own and operate portfolios of real estate make up a significant segment of MPI s clients. We

Article Real Estate Companies A Business Valuation Primer (Series 1) May 2018 Families and organizations that own and operate portfolios of real estate make up a significant segment of MPI s clients. We

Acquisition of investment properties asset purchase or business combination?

Acquisition of investment properties asset purchase or business combination? Our IFRS Viewpoint series provides insights from our global IFRS team on applying IFRSs in challenging situations. Each edition

Acquisition of investment properties asset purchase or business combination? Our IFRS Viewpoint series provides insights from our global IFRS team on applying IFRSs in challenging situations. Each edition

Name, title, address of national authority

Name, title, address of national authority Dear TEGoVA Guidance to EU Member States and Candidate Member States on Development of Reliable Valuation Standards in Accordance with Art. 19 of Directive 2014/17/EU

Name, title, address of national authority Dear TEGoVA Guidance to EU Member States and Candidate Member States on Development of Reliable Valuation Standards in Accordance with Art. 19 of Directive 2014/17/EU

Agreements for the Construction of Real Estate

HK(IFRIC)-Int 15 Revised August 2010September 2018 Effective for annual periods beginning on or after 1 January 2009* HK(IFRIC) Interpretation 15 Agreements for the Construction of Real Estate * HK(IFRIC)-Int

HK(IFRIC)-Int 15 Revised August 2010September 2018 Effective for annual periods beginning on or after 1 January 2009* HK(IFRIC) Interpretation 15 Agreements for the Construction of Real Estate * HK(IFRIC)-Int

An Assessment of Recent Increases of House Prices in Austria through the Lens of Fundamentals

An Assessment of Recent Increases of House Prices in Austria 1 Introduction Martin Schneider Oesterreichische Nationalbank The housing sector is one of the most important sectors of an economy. Since residential

An Assessment of Recent Increases of House Prices in Austria 1 Introduction Martin Schneider Oesterreichische Nationalbank The housing sector is one of the most important sectors of an economy. Since residential

Research Programme. Residual Land Values: Measuring Performance and Investigating Viability

Research Programme Residual Land Values: Measuring Performance and Investigating Viability APRIL 2018 SUMMARY REPORT This research was commissioned by by the the IPF IPF Research Programme 2015 2015 2018

Research Programme Residual Land Values: Measuring Performance and Investigating Viability APRIL 2018 SUMMARY REPORT This research was commissioned by by the the IPF IPF Research Programme 2015 2015 2018

Use of Comparables. Claims Prevention Bulletin [CP-17-E] March 1996

![Use of Comparables. Claims Prevention Bulletin [CP-17-E] March 1996](/thumbs/82/87011536.jpg "Use of Comparables. Claims Prevention Bulletin [CP-17-E] March 1996") March 1996 The use of comparables arises almost daily for all appraisers. especially those engaged in residential practice, where appraisals are being prepared for mortgage underwriting purposes. That

March 1996 The use of comparables arises almost daily for all appraisers. especially those engaged in residential practice, where appraisals are being prepared for mortgage underwriting purposes. That

Impact Assessment (IA)

") Title: Permission in principle for development plans and brownfield registers IA No: RPC-3069(2)-CLG Lead department or agency: Department for Communities and Local Government Other departments or agencies:

Title: Permission in principle for development plans and brownfield registers IA No: RPC-3069(2)-CLG Lead department or agency: Department for Communities and Local Government Other departments or agencies:

Valuation and the Real Estate Market; a new paradigm for a new decade

Valuation and the Real Estate Market; a new paradigm for a new decade Nick French Professor in Real Estate & DTZ Fellow in Commercial Property Department of Real Estate & Construction Oxford Brookes University

Valuation and the Real Estate Market; a new paradigm for a new decade Nick French Professor in Real Estate & DTZ Fellow in Commercial Property Department of Real Estate & Construction Oxford Brookes University

Securing Land Rights for Broadband Land Acquisition for Utilities in Sweden

Securing Land Rights for Broadband Land Acquisition for Utilities in Sweden Marija JURIC and Kristin LAND, Sweden Key words: broadband, land acquisition, cadastral procedure, Sweden SUMMARY The European

Securing Land Rights for Broadband Land Acquisition for Utilities in Sweden Marija JURIC and Kristin LAND, Sweden Key words: broadband, land acquisition, cadastral procedure, Sweden SUMMARY The European

CONTACT(S) Raghava Tirumala +44 (0) Woung Hee Lee +44 (0)

Raghava Tirumala +44 (0) Woung Hee Lee +44 (0)") IASB Agenda ref 18A STAFF PAPER IASB Meeting Project Paper topic Goodwill and Impairment research project Summary of discussions to date CONTACT(S) Raghava Tirumala rtirumala@ifrs.org +44 (0)20 7246 6953

IASB Agenda ref 18A STAFF PAPER IASB Meeting Project Paper topic Goodwill and Impairment research project Summary of discussions to date CONTACT(S) Raghava Tirumala rtirumala@ifrs.org +44 (0)20 7246 6953

REDSTONE. Regression Fundamentals.

REDSTONE from Bradford Advanced Analytics Technologies for Appraisers Regression Fundamentals www.bradfordsoftware.com/redstone Bradford Technologies, Inc. 302 Piercy Road San Jose, CA 95138 800-622-8727

REDSTONE from Bradford Advanced Analytics Technologies for Appraisers Regression Fundamentals www.bradfordsoftware.com/redstone Bradford Technologies, Inc. 302 Piercy Road San Jose, CA 95138 800-622-8727

International Valuation Standards Update

International Valuation Standards Update Adam Smith Interim Technical Director of Business Valuation Standards OIV International Business Valuation Conference January 16, 2017 INTERNATIONAL VALUATION STANDARDS

International Valuation Standards Update Adam Smith Interim Technical Director of Business Valuation Standards OIV International Business Valuation Conference January 16, 2017 INTERNATIONAL VALUATION STANDARDS

Quality assurance of appraisal: guidance notes

Quality assurance of appraisal: guidance notes NHS England INFORMATION READER BOX Directorate Medical Commissioning Operations Patients and Information Nursing Trans. & Corp. Ops. Commissioning Strategy

Quality assurance of appraisal: guidance notes NHS England INFORMATION READER BOX Directorate Medical Commissioning Operations Patients and Information Nursing Trans. & Corp. Ops. Commissioning Strategy

Appraisers and Assessors of Real Estate

http://www.bls.gov/oco/ocos300.htm Appraisers and Assessors of Real Estate * Nature of the Work * Training, Other Qualifications, and Advancement * Employment * Job Outlook * Projections Data * Earnings

http://www.bls.gov/oco/ocos300.htm Appraisers and Assessors of Real Estate * Nature of the Work * Training, Other Qualifications, and Advancement * Employment * Job Outlook * Projections Data * Earnings

ASSESSMENT METHODOLOGY

2019 ASSESSMENT METHODOLOGY COMMERCIAL RETAIL AND OFFICE CONDOMINIUMS A summary of the methods used by the City of Edmonton in determining the value of commercial retail and office condominium properties

2019 ASSESSMENT METHODOLOGY COMMERCIAL RETAIL AND OFFICE CONDOMINIUMS A summary of the methods used by the City of Edmonton in determining the value of commercial retail and office condominium properties

Owners Full Name(s): (hereinafter, Sellers )"

: (hereinafter, Sellers )") LIMITED REPRESENTATION AGREEMENT 1 of 10 Date: Owners Full Name(s): (hereinafter, Sellers ) This Listing Agreement is by and between Sellers and Home Max, LLC., doing business as Home Max Realty, MLS Direct,

LIMITED REPRESENTATION AGREEMENT 1 of 10 Date: Owners Full Name(s): (hereinafter, Sellers ) This Listing Agreement is by and between Sellers and Home Max, LLC., doing business as Home Max Realty, MLS Direct,

Introducing Property Valuation

Introducing Property Valuation Michael Blackledge Routledge Taylor & Francis Group LONDON AND NEW YORK Illustrations Cases Acknowledgements Disclaimers x xii xiv xv 1: Background 1 Economic context 3 1.1

Introducing Property Valuation Michael Blackledge Routledge Taylor & Francis Group LONDON AND NEW YORK Illustrations Cases Acknowledgements Disclaimers x xii xiv xv 1: Background 1 Economic context 3 1.1

ASSESSMENT REVIEW BOARD. The City of Edmonton JASPER AVENUE Assessment and Taxation Branch

ASSESSMENT REVIEW BOARD Churchill Building 10019 103 Avenue Edmonton AB T5J 0G9 Phone: (780) 496-5026 NOTICE OF DECISION NO. 0098 101/11 CVG The City of Edmonton 1200-10665 JASPER AVENUE Assessment and

ASSESSMENT REVIEW BOARD Churchill Building 10019 103 Avenue Edmonton AB T5J 0G9 Phone: (780) 496-5026 NOTICE OF DECISION NO. 0098 101/11 CVG The City of Edmonton 1200-10665 JASPER AVENUE Assessment and

Table of Contents. Appraiser Independence Policy Forms

Table of Contents Table of Contents... 1 Appraiser Independence... 2 Policies Applicable to All Company Operating Areas... 2 Appraiser Selection and Approval... 3 Appraiser Approval Process... 3 Approved

Table of Contents Table of Contents... 1 Appraiser Independence... 2 Policies Applicable to All Company Operating Areas... 2 Appraiser Selection and Approval... 3 Appraiser Approval Process... 3 Approved

TERMS OF ENGAGEMENT Name of the firm. Previous involvement with the property or parties to the case:

The headings contained in this framework for terms of engagement are based directly upon the list of mandatory required content set out in VPS 1 para 3.1, page 39 and the commentary which follows on pages

The headings contained in this framework for terms of engagement are based directly upon the list of mandatory required content set out in VPS 1 para 3.1, page 39 and the commentary which follows on pages

NATIONAL PLANNING AUTHORITY. The Role of Surveyors in Achieving Uganda Vision 2040

NATIONAL PLANNING AUTHORITY The Role of Surveyors in Achieving Uganda Vision 2040 Key Note Address By Dr. Joseph Muvawala Executive Director National Planning Authority At the Annual General Meeting and

NATIONAL PLANNING AUTHORITY The Role of Surveyors in Achieving Uganda Vision 2040 Key Note Address By Dr. Joseph Muvawala Executive Director National Planning Authority At the Annual General Meeting and

Thank you for the opportunity to comment on the above referenced Exposure Draft.

International Accounting Standards Board 1 st Floor 30 Cannon Street London, EC4M 6XH United Kingdom Financial Accounting Standards Board 401 Merritt 7 PO Box 5116 Norwalk, CT 06856 5116 United States

International Accounting Standards Board 1 st Floor 30 Cannon Street London, EC4M 6XH United Kingdom Financial Accounting Standards Board 401 Merritt 7 PO Box 5116 Norwalk, CT 06856 5116 United States

Standard on Automated Valuation Models (AVMs)

") Standard on Automated Valuation Models (AVMs) Approved September 2003 Revised approved July, 2018 Contents 1. Scope...4 2. Principles...4 3. Introduction...5 3.1 Definition of automated valuation model

Standard on Automated Valuation Models (AVMs) Approved September 2003 Revised approved July, 2018 Contents 1. Scope...4 2. Principles...4 3. Introduction...5 3.1 Definition of automated valuation model

About the Appraisal Institute

About the Appraisal Institute About the Appraisal Institute: Setting the Standard for Quality Whether you re seeking the services of a qualified real estate appraiser, are interested in a career in appraising

About the Appraisal Institute About the Appraisal Institute: Setting the Standard for Quality Whether you re seeking the services of a qualified real estate appraiser, are interested in a career in appraising

Property report 7/15-23 Redondo Street Ningi QLD 4511

Property report 7/15-23 Redondo Street Ningi QLD 4511 Prepared for: Prepared on: Prepared by: Phone: Email: Paul Jabbor Derek Andrew Potter 0475958253 andrew.potter@nab.com.au 2 2 1 261m 2 u Property details

Property report 7/15-23 Redondo Street Ningi QLD 4511 Prepared for: Prepared on: Prepared by: Phone: Email: Paul Jabbor Derek Andrew Potter 0475958253 andrew.potter@nab.com.au 2 2 1 261m 2 u Property details

Assessment-To-Sales Ratio Study for Division III Equalization Funding: 1999 Project Summary. State of Delaware Office of the Budget

Assessment-To-Sales Ratio Study for Division III Equalization Funding: 1999 Project Summary prepared for the State of Delaware Office of the Budget by Edward C. Ratledge Center for Applied Demography and

Assessment-To-Sales Ratio Study for Division III Equalization Funding: 1999 Project Summary prepared for the State of Delaware Office of the Budget by Edward C. Ratledge Center for Applied Demography and

PROPERTY DEVELOPMENT REPORT

THE CITY OF CAMPBELLTOWN PROPERTY DEVELOPMENT REPORT Location: 123 Sample Street, Campbelltown Parcel ID: Report Processed: 28/04/2016 Max Volume: 4 ipdata Pty Ltd Disclaimer Whilst all reasonable effort

THE CITY OF CAMPBELLTOWN PROPERTY DEVELOPMENT REPORT Location: 123 Sample Street, Campbelltown Parcel ID: Report Processed: 28/04/2016 Max Volume: 4 ipdata Pty Ltd Disclaimer Whilst all reasonable effort

NZ property report OCTOBER 2016

NZ property report OCTOBER 2016 Report Definitions Sales by registration type; rolling three month, year-on-year growth This data set provides an insight into who is active in the market compared to the

NZ property report OCTOBER 2016 Report Definitions Sales by registration type; rolling three month, year-on-year growth This data set provides an insight into who is active in the market compared to the

Welsh Government Housing Policy Regulation

www.cymru.gov.uk Welsh Government Housing Policy Regulation Regulatory Assessment Report August 2015 Welsh Government Regulatory Assessment The Welsh Ministers have powers under the Housing Act 1996 to

www.cymru.gov.uk Welsh Government Housing Policy Regulation Regulatory Assessment Report August 2015 Welsh Government Regulatory Assessment The Welsh Ministers have powers under the Housing Act 1996 to

CAUTION SMOKE & MIRRORS AHEAD! Question the Source & Know the Facts. Why Using Zillow & Zestimates Are Not in Your Best Interest

CAUTION SMOKE & MIRRORS AHEAD! Why Using Zillow & Zestimates Are Not in Your Best Interest Question the Source & Know the Facts Background: Zillow is an online real estate database company founded in 2006.

CAUTION SMOKE & MIRRORS AHEAD! Why Using Zillow & Zestimates Are Not in Your Best Interest Question the Source & Know the Facts Background: Zillow is an online real estate database company founded in 2006.

Benchmarking Cadastral Systems Results of the Working Group 7.1

Benchmarking Cadastral Systems Results of the Working Group 7.1 Jürg KAUFMANN, Switzerland Key words: ABSTRACT In 1998, FIG-Commission 7 launched three new working groups for the period 1998-2002. Working

Benchmarking Cadastral Systems Results of the Working Group 7.1 Jürg KAUFMANN, Switzerland Key words: ABSTRACT In 1998, FIG-Commission 7 launched three new working groups for the period 1998-2002. Working

Bargara Property Factsheet

Bargara Property Factsheet 1st Half 2018 OVERVIEW Bargara* is located in the Bundaberg Region of south-east Queensland, approximately 384km north of Brisbane s CBD. Over the last 7 years the population

Bargara Property Factsheet 1st Half 2018 OVERVIEW Bargara* is located in the Bundaberg Region of south-east Queensland, approximately 384km north of Brisbane s CBD. Over the last 7 years the population

Economic Significance of the Property Industry to the. WELLINGTON Economy PREPARED FOR PROPERTY COUNCIL NEW ZEALAND BY URBAN ECONOMICS

Economic Significance of the Property Industry to the WELLINGTON Economy PREPARED FOR PROPERTY COUNCIL NEW ZEALAND BY URBAN ECONOMICS 2016 ABOUT PROPERTY COUNCIL NEW ZEALAND Property Council New Zealand

Economic Significance of the Property Industry to the WELLINGTON Economy PREPARED FOR PROPERTY COUNCIL NEW ZEALAND BY URBAN ECONOMICS 2016 ABOUT PROPERTY COUNCIL NEW ZEALAND Property Council New Zealand

If you want even more information, look for the advanced training, which includes more use cases and demonstrates CU s full functionality.

Thank you for attending the Collateral Underwriter user interface basic training. My name is Steve Jones and I will be taking you through the course. Our objective today is to provide a foundational understanding

Thank you for attending the Collateral Underwriter user interface basic training. My name is Steve Jones and I will be taking you through the course. Our objective today is to provide a foundational understanding

Report of the Independent Auditor

Independent auditor s report to the members of (Incorporated in Hong Kong with limited liability) Opinion We have audited the consolidated financial statements of ( the Company ) and its subsidiaries (

Independent auditor s report to the members of (Incorporated in Hong Kong with limited liability) Opinion We have audited the consolidated financial statements of ( the Company ) and its subsidiaries (

PROPERTY PROFILE. 402/18 Bent Street Kensington VIC 3031

PROPERTY PROFILE Prepared on: 2 1 1 2,135m 2 Page 2 u PROPERTY DETAILS Here we summarise the property s key details (which are accurate at the time of last sale). Address: 402/18 Bent Street Kensington

PROPERTY PROFILE Prepared on: 2 1 1 2,135m 2 Page 2 u PROPERTY DETAILS Here we summarise the property s key details (which are accurate at the time of last sale). Address: 402/18 Bent Street Kensington

Economic Significance of the Property Industry to the. OTAGO Economy PREPARED FOR PROPERTY COUNCIL NEW ZEALAND BY URBAN ECONOMICS

Economic Significance of the Property Industry to the OTAGO Economy PREPARED FOR PROPERTY COUNCIL NEW ZEALAND BY URBAN ECONOMICS 2016 ABOUT PROPERTY COUNCIL NEW ZEALAND Property Council New Zealand is

Economic Significance of the Property Industry to the OTAGO Economy PREPARED FOR PROPERTY COUNCIL NEW ZEALAND BY URBAN ECONOMICS 2016 ABOUT PROPERTY COUNCIL NEW ZEALAND Property Council New Zealand is

Member briefing: The Social Housing Rent Settlement from 2015/16

28 May 2014 Member briefing: The Social Housing Rent Settlement from 2015/16 1. Introduction On Friday 23 May Government issued the final policy for Rents for Social Housing from 2015/16, following a consultation

28 May 2014 Member briefing: The Social Housing Rent Settlement from 2015/16 1. Introduction On Friday 23 May Government issued the final policy for Rents for Social Housing from 2015/16, following a consultation

International Financial Reporting Standards (IFRS)

") FACT SHEET February 2011 IAS 40 Investment Property (This fact sheet is based on the standard as at 1 January 2011.) Important note: This fact sheet is based on the requirements of the International Financial

FACT SHEET February 2011 IAS 40 Investment Property (This fact sheet is based on the standard as at 1 January 2011.) Important note: This fact sheet is based on the requirements of the International Financial

How to use home valuations to connect with prospects and build your business

How to use home valuations to connect with prospects and build your business Using Homes.com Home Values to make connections and build business By Charles Warnock, Homes Media Solutions In recent years,

How to use home valuations to connect with prospects and build your business Using Homes.com Home Values to make connections and build business By Charles Warnock, Homes Media Solutions In recent years,

Training the Next Generation of Appraisers The S.T.A.R.T. Program - Standards to Assure Responsible Training:

Training the Next Generation of Appraisers The S.T.A.R.T. Program - Standards to Assure Responsible Training: An Industry Solution to the Declining Number of Appraisers Entering the Profession and Practical

Training the Next Generation of Appraisers The S.T.A.R.T. Program - Standards to Assure Responsible Training: An Industry Solution to the Declining Number of Appraisers Entering the Profession and Practical

Response to implementing social housing reform: directions to the Social Housing Regulator.

Briefing 11-44 August 2011 Response to implementing social housing reform: directions to the Social Housing Regulator. To: All English Contacts For information: All contacts in Scotland, Northern Ireland

Briefing 11-44 August 2011 Response to implementing social housing reform: directions to the Social Housing Regulator. To: All English Contacts For information: All contacts in Scotland, Northern Ireland

CONTACT(S) Annamaria Frosi +44 (0) Rachel Knubley +44 (0)

Annamaria Frosi +44 (0) Rachel Knubley +44 (0)") IASB Agenda ref 11 STAFF PAPER IASB Meeting Project Paper topic Materiality Practice Statement Sweep issues covenants CONTACT(S) Annamaria Frosi afrosi@ifrs.org +44 (0)20 7246 6907 Rachel Knubley rknubley@ifrs.org

IASB Agenda ref 11 STAFF PAPER IASB Meeting Project Paper topic Materiality Practice Statement Sweep issues covenants CONTACT(S) Annamaria Frosi afrosi@ifrs.org +44 (0)20 7246 6907 Rachel Knubley rknubley@ifrs.org

Demonstration Properties for the TAUREAN Residential Valuation System

Demonstration Properties for the TAUREAN Residential Valuation System Taurean has provided a set of four sample subject properties to demonstrate many of the valuation system s features and capabilities.

Demonstration Properties for the TAUREAN Residential Valuation System Taurean has provided a set of four sample subject properties to demonstrate many of the valuation system s features and capabilities.

My House Property Valuation

My House Property Valuation Prepared on: 21 March 2016 Property Description Sandgate, QLD, 4017 4 2 1 159m2 Real Property Property Type Name Land Use Primary LGA Name Lot Plan L4 SP155329:PAR NUNDAH Unit:

My House Property Valuation Prepared on: 21 March 2016 Property Description Sandgate, QLD, 4017 4 2 1 159m2 Real Property Property Type Name Land Use Primary LGA Name Lot Plan L4 SP155329:PAR NUNDAH Unit:

GOOD SURVEY PRACTICE

FEEDBACK VERSION 2.4 31 October 2018 GOOD SURVEY PRACTICE 1. Forward 1.1 Surveying The art and science of surveying relates to the capture of measurements, and completion of computations to determine the

FEEDBACK VERSION 2.4 31 October 2018 GOOD SURVEY PRACTICE 1. Forward 1.1 Surveying The art and science of surveying relates to the capture of measurements, and completion of computations to determine the

Minimum Educational Requirements

Minimum Educational Requirements (MER) For all persons elected to practice in each Member Association With effect from 1 January 2011 1 Introduction 1.1 The European Group of Valuers Associations (TEGoVA)

Minimum Educational Requirements (MER) For all persons elected to practice in each Member Association With effect from 1 January 2011 1 Introduction 1.1 The European Group of Valuers Associations (TEGoVA)

This article is relevant to the Diploma in International Financial Reporting and ACCA Qualification Papers F7 and P2

REVENUE RECOGNITION This article is relevant to the Diploma in International Financial Reporting and ACCA Qualification Papers F7 and P2 For almost all entities other than financial institutions, revenue

REVENUE RECOGNITION This article is relevant to the Diploma in International Financial Reporting and ACCA Qualification Papers F7 and P2 For almost all entities other than financial institutions, revenue

Past & Present Adjustments & Parcel Count Section... 13

Assessment 2017 Report This report includes specific information regarding the 2017 assessment as well as general information about both the appeals and assessment processes. Contents Introduction... 3

Assessment 2017 Report This report includes specific information regarding the 2017 assessment as well as general information about both the appeals and assessment processes. Contents Introduction... 3

In December 2003 the Board issued a revised IAS 40 as part of its initial agenda of technical projects.

IAS Standard 40 Investment Property In April 2001 the International Accounting Standards Board (the Board) adopted IAS 40 Investment Property, which had originally been issued by the International Accounting

IAS Standard 40 Investment Property In April 2001 the International Accounting Standards Board (the Board) adopted IAS 40 Investment Property, which had originally been issued by the International Accounting

IAG Conference Accounting Update Emerging issues in the public sector 20 November 2014 Michael Crowe Yannick Maurice

www.pwc.com.au IAG Conference Accounting Update Emerging issues in the public sector 20 November 2014 Michael Crowe Yannick Maurice Agenda Introduction Key topics o Fair value o PPP Projects Refinancing

www.pwc.com.au IAG Conference Accounting Update Emerging issues in the public sector 20 November 2014 Michael Crowe Yannick Maurice Agenda Introduction Key topics o Fair value o PPP Projects Refinancing

In December 2003 the IASB issued a revised IAS 40 as part of its initial agenda of technical projects.

International Accounting Standard 40 Investment Property In April 2001 the International Accounting Standards Board (IASB) adopted IAS 40 Investment Property, which had originally been issued by the International

International Accounting Standard 40 Investment Property In April 2001 the International Accounting Standards Board (IASB) adopted IAS 40 Investment Property, which had originally been issued by the International

The Digital Cadastral Database and the Role of the Private Licensed Surveyors in Denmark

IRISH INSTITUTE OF SURVEYORS, DUBLIN INSTITUTE OF TECHNOLOGY, 23 NOVEMBER 2005 PUBLISHED IN IIS NEWS, WINTHER 2006. The Digital Cadastral Database and the Role of the Private Licensed Surveyors in Denmark

IRISH INSTITUTE OF SURVEYORS, DUBLIN INSTITUTE OF TECHNOLOGY, 23 NOVEMBER 2005 PUBLISHED IN IIS NEWS, WINTHER 2006. The Digital Cadastral Database and the Role of the Private Licensed Surveyors in Denmark

2011 ASSESSMENT RATIO REPORT

2011 Ratio Report SECTION I OVERVIEW 2011 ASSESSMENT RATIO REPORT The Department of Assessments and Taxation appraises real property for the purposes of property taxation. Properties are valued using

2011 Ratio Report SECTION I OVERVIEW 2011 ASSESSMENT RATIO REPORT The Department of Assessments and Taxation appraises real property for the purposes of property taxation. Properties are valued using

How to Read a Real Estate Appraisal Report

How to Read a Real Estate Appraisal Report Much of the private, corporate and public wealth of the world consists of real estate. The magnitude of this fundamental resource creates a need for informed

How to Read a Real Estate Appraisal Report Much of the private, corporate and public wealth of the world consists of real estate. The magnitude of this fundamental resource creates a need for informed

LSL New Build Index. The market indicator for New Builds March Political events

LSL New Build Index The market indicator for New Builds March 2018 In the year to end February 2018 new build house prices rose on average by 9.7% across the UK which is up on last year s figure of 5.3%

LSL New Build Index The market indicator for New Builds March 2018 In the year to end February 2018 new build house prices rose on average by 9.7% across the UK which is up on last year s figure of 5.3%

Frequently Asked Questions: Residential Property Price Index

CENTRAL BANK OF CYPRUS EUROSYSTEM Frequently Asked Questions: Residential Property Price Index 1. What is a Residential Property Price Index (RPPI)? An RPPI is an indicator which measures changes in the

CENTRAL BANK OF CYPRUS EUROSYSTEM Frequently Asked Questions: Residential Property Price Index 1. What is a Residential Property Price Index (RPPI)? An RPPI is an indicator which measures changes in the

Table of Contents. Chapter 1: Introduction (Mobile Technology Evolution) 1

1") Chapter 1: Introduction (Mobile Technology Evolution) 1 I. WHY APPRAISAL IS IMPORTANT (p. 3) II. DEFINITION OF APPRAISAL (p. 4) A. Opinion (p. 4) B. Value (p. 5) C. Appraisal Art or Science? (p. 5) D.

Chapter 1: Introduction (Mobile Technology Evolution) 1 I. WHY APPRAISAL IS IMPORTANT (p. 3) II. DEFINITION OF APPRAISAL (p. 4) A. Opinion (p. 4) B. Value (p. 5) C. Appraisal Art or Science? (p. 5) D.

TECHNICAL INFORMATION PAPER VALUATION OF SELF STORAGE FACILITIES

TECHNICAL INFORMATION PAPER VALUATION OF SELF STORAGE FACILITIES Reference ANZVTIP 5 Valuation of Self Storage Facilities Effective 23 November 2016 Owner National Manager Professional Standards Australian

TECHNICAL INFORMATION PAPER VALUATION OF SELF STORAGE FACILITIES Reference ANZVTIP 5 Valuation of Self Storage Facilities Effective 23 November 2016 Owner National Manager Professional Standards Australian

concepts and techniques

concepts and techniques S a m p l e Timed Outline Topic Area DAY 1 Reference(s) Learning Objective The student will learn Teaching Method Time Segment (Minutes) Chapter 1: Introduction to Sales Comparison

concepts and techniques S a m p l e Timed Outline Topic Area DAY 1 Reference(s) Learning Objective The student will learn Teaching Method Time Segment (Minutes) Chapter 1: Introduction to Sales Comparison

Guide Note 6 Consideration of Hazardous Substances in the Appraisal Process

Guide Note 6 Consideration of Hazardous Substances in the Appraisal Process Introduction The consideration of environmental conditions along with social, economic, and governmental conditions is fundamental

Guide Note 6 Consideration of Hazardous Substances in the Appraisal Process Introduction The consideration of environmental conditions along with social, economic, and governmental conditions is fundamental

CONTACT(S) Annamaria Frosi +44 (0) Rachel Knubley +44 (0)

Annamaria Frosi +44 (0) Rachel Knubley +44 (0)") IASB Agenda ref 11 STAFF PAPER IASB Meeting Project Paper topic Materiality Practice Statement Sweep issues covenants CONTACT(S) Annamaria Frosi afrosi@ifrs.org +44 (0)20 7246 6907 Rachel Knubley rknubley@ifrs.org

IASB Agenda ref 11 STAFF PAPER IASB Meeting Project Paper topic Materiality Practice Statement Sweep issues covenants CONTACT(S) Annamaria Frosi afrosi@ifrs.org +44 (0)20 7246 6907 Rachel Knubley rknubley@ifrs.org

Real Property Assets Policy and Procedures

Real Property Assets Policy and Procedures Summary: Due Diligence process Prior to the execution of a binding contract to purchase a property by a DomaCom sub-fund, a review of the Real Property Asset

Real Property Assets Policy and Procedures Summary: Due Diligence process Prior to the execution of a binding contract to purchase a property by a DomaCom sub-fund, a review of the Real Property Asset