Courthouse Audit. March 14, Report # 646

|

|

|

- Shanon Gilmore

- 5 years ago

- Views:

Transcription

1 Courthouse Audit March 14, 2008 Report # 646 Released on April 14, 2008

2 AUDIT REPORT #646 INTRODUCTION STATEMENT OF OBJECTIVES STATEMENT OF SCOPE AND METHODOLOGY STATEMENT OF AUDITING STANDARDS OVERALL AUDIT CONCLUSION AUDIT OBJECTIVE # AUDIT OBJECTIVE # AUDIT OBJECTIVE # ATTACHMENT A ATTACHMENT B ATTACHMENT C ATTACHMENT D

3 OFFICE OF THE COUNCIL AUDITOR Suite 200, St. James Building March 14, 2008 Report # 646 Honorable Members of the City Council City of Jacksonville INTRODUCTION In response to an October 18, 2007 letter from the State Attorney, we conducted an audit of the City of Jacksonville s county courthouse construction project. This construction project was authorized and funded as part of the City s Better Jacksonville Plan (BJP). Contractors The original project team consisted of a Program Management Consultant 1 (Jacobs Engineering hired in November 2001), an Architect / Engineer (Cannon Design hired in October 2002) and a Construction Risk (Skanska Dynamic Partners hired in May 2003). By the end of November 2004, the City terminated its contracts with Jacobs, Cannon, and Skanska and halted the project due to the apparent inability of these firms to construct the courthouse within the City s project budget. On January 29, 2007, the City hired a design-build firm (Auchter/Perry-McCall) to design and construct the courthouse. The City terminated this contract in May 2007 due to concerns over Auchter s financial condition. The City then hired a second design-build firm (Turner Construction) in December Budget BJP passed with $190 million allocated for the courthouse project. The administration authorized the movement of $21 million in contingency funds to supplement the original allocation, increasing the project budget to $211 million. When it became apparent that $211 million was still not enough, the City Council increased the budget, first to $232 million and then to $263.5 million. At present, proposed legislation is before the Council to increase the project budget to $395.3 million. It is anticipated that a substitute bill will be proposed by the Administration setting a new cap of $350 million. 1 Note that this report contains terminology that may be specific to the construction industry. We have attached a glossary with definitions provided to us by the Public Works Department. This can be found at ATTACHMENT A. 117 West Duval Street Jacksonville, Florida Telephone (904) Fax (904)

4 STATEMENT OF OBJECTIVES The objectives of the audit were as follows: 1. To compile all courthouse costs expended to date and break the costs down by expense category. 2. To analyze all bid documents and contracts related to the construction of the courthouse to determine how the project was bid, how contractors were selected, and the sufficiency of the contracts. 3. To analyze ancillary courthouse projects, especially with regard to their cost (capital and operating) to the City and its independent agencies and the sufficiency of the delivered project. The ancillary courthouse projects identified are JEA s chilled water plant, the courthouse parking garage, and the Old Federal Courthouse. STATEMENT OF SCOPE AND METHODOLOGY The scope of our work was the Better Jacksonville Plan Courthouse Project from inception through September 30, We reviewed procurement documents, contracts, invoices, and communications between project participants. We also compiled and analyzed accounting data and interviewed project participants. STATEMENT OF AUDITING STANDARDS We conducted our audit in accordance with generally accepted government auditing standards issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to afford a reasonable basis for our judgments and conclusions regarding the organization, program, activity, or function under audit. This audit also included an assessment of applicable management controls and compliance with requirements of laws and regulations when necessary to satisfy audit objectives. We believe that our audit provides a reasonable basis for our conclusions. AUDITEE RESPONSES Responses from the auditee have been inserted in italics after the respective finding and recommendation. We received these responses from Alan Mosley, Chief Administrative Officer for the City in a memorandum dated April 11, Mr. Mosley s memorandum stated the following: Thank you for the opportunity to review the subject draft audit and offer a written response thereto. I believe it was done very fairly and impartially. We appreciate your findings, and have revised certain operating procedures consistent with your recommendations. There were certain Findings and Recommendations to which I would like to respond and/or provide clarification from the Administration

5 OVERALL AUDIT CONCLUSION The reason the new courthouse has not yet been built is because the available funding was not enough for a courthouse of the design, size, and location that the City pursued. Rather than give up, the City tried to find ways to supplement the funding available in the Better Jacksonville Plan and make the project happen. AUDIT OBJECTIVE #1 Our first audit objective was to compile all costs expended to date and break the costs down by expense category. We obtained this information from the City s general ledger. Audit Objective #1 Conclusion As of September 30, 2007 a total of $64,619, was charged to the courthouse project (specifically Project PW1074 within the City s accounting system). Of this total, approximately $1.9 million was spent on renovations to the existing courthouse at 330 E Bay St and to the City Hall Annex. The source of funding for these renovations was established in ordinance E. Land 23,118,666 Engineering 10,732,156 Other Construction Costs 30,571,115 Materials 197,263 Total : (difference is rounding) $64,619,200 Table 1 : Cost Breakdown by Category 2 Note that the above figures do not include expenses associated with construction of the JEA chilled water plant, the construction of the courthouse parking garage, or the acquisition of the old federal courthouse. Finding #1 The courthouse project was under-budgeted from the start. We have been unable to find a single document that substantiates that the project could have been built on the selected site or any new site (as opposed to building on the existing courthouse/city hall annex site) for the $190,000,000 cost included in the Better Jacksonville Plan. In performing our audit work, we did note the following: A Duval County Judicial Master Plan Draft Preliminary Cost Estimate dated October 20, 1999 for a courthouse on a new site totaled $193,989,133. This estimate did not include site acquisition costs; the land for the site chosen ended up costing $23,118, See ATTACHMENT B for breakdown including major contractors

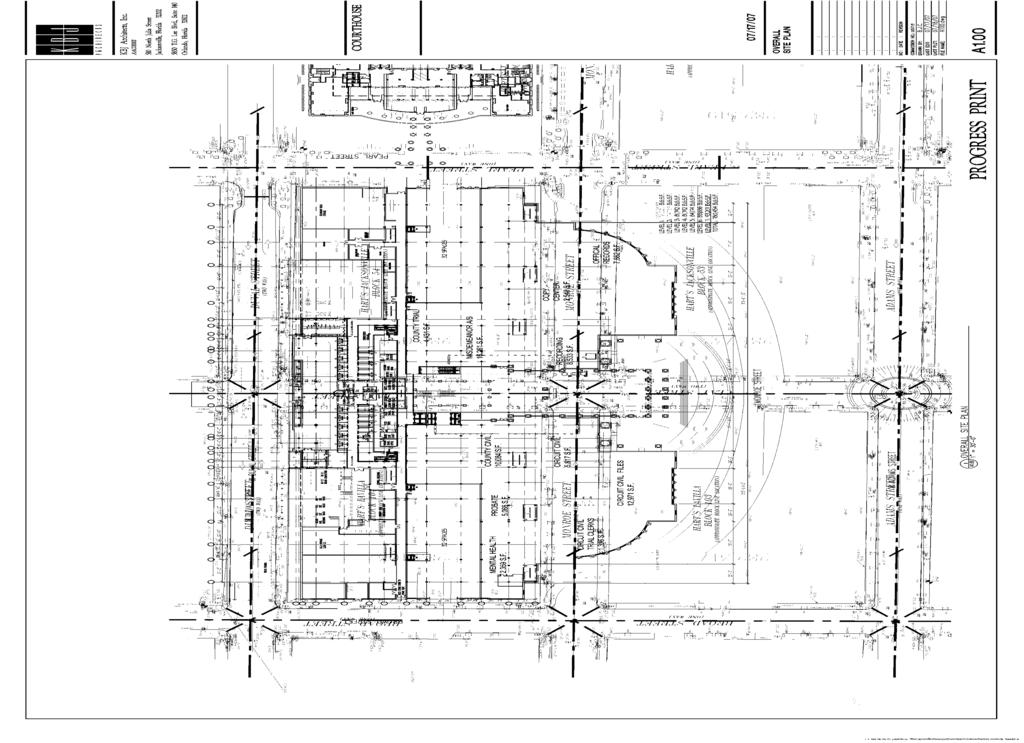

6 A Programming Status Report prepared by Dan Wiley and Associates, dated September 10, 2001, expressed concern about the adequacy of the $190,000,000 budget. In the Preliminary Program Budget Validation prepared by Jacobs, the Program Manager, we found a schedule indicating that a courthouse of 896,303 square feet would cost approximately $257 million, which included $25 million for land acquisition. This document is dated September 12, In minutes from a meeting held on December 12, 2001, we found the following, It was determined that the final budget for the courthouse, including all costs would be $223 million, excluding parking. This figure also includes the cost of renovating the old Federal courthouse. Attendees included the Mayor, the Public Works director, the courthouse project manager and other senior leadership. In a January 15, 2002 interoffice memo from Jacobs we found the following, We should go back to the City and indicate that we need the additional $10 to $15 million (above the $21 million) that was requested by Chris [Boruch] in order to have an acceptable design to program. Per the City s original Project Manager for the courthouse project, he knew and publicly stated at the June 2002 design competition that the courthouse could not be constructed within the proposed budget. We have been unable to verify this statement because City Procurement has been unable to find the recording of the design competition deliberation. Recommendation #1 We recommend that the City fund construction of a new unified courthouse at the proposed site, for the following reasons: the City is legally obligated, by the State of Florida, to provide a county courthouse the City has already acquired the new site JEA has constructed the chilled water infrastructure to serve a courthouse at the new site the parking garage for the courthouse has been constructed at the new site Response to Recommendation #1 We concur and have introduced legislation ( ) to fund construction of a unified courthouse. That legislation is presently under consideration by City Council. Finding #2 The City s decision to build out instead of up increased the cost of the project significantly. The Federal Government built its courthouse as a 14 story tower on one block in downtown Jacksonville. In contrast, the City opted for a courthouse campus of 7 blocks, with one block being the site of the old federal courthouse and one block being used for a parking garage. The City acquired the old federal courthouse in exchange for a long-term parking lease valued at $875,000. The City spent $23,118,666 to acquire the other six blocks. The City s costs include much more than just the compensation for the land. The costs include appraiser and attorney s fees, tenant relocation costs, expert witness fees, and demolition costs. The decision to build out also increased costs by closing streets and incorporating their former footprint in the footprint of the new courthouse. This decision caused the City to incur millions of dollars of expense to relocate the utilities that ran within the right of way of the former streets

7 The City s current planned design (the Turner design) occupies four blocks of land. The footprint occupies two blocks completely and partially occupies two more blocks with plazas filling the remainder of these blocks to allow for the setback of the building so that its facade can be seen and appreciated. This design leaves one block available for future use. Recommendation #2 Consideration should be given to constructing the new courthouse on one or two blocks of the available five block site. The unused blocks could be sold to put the property back on the tax rolls and generate additional funding for the courthouse project. If the decision is made to construct the courthouse on only one or two blocks, then consideration should be given to its location in proximity to the parking garage. Response to Recommendation #2 We respectfully disagree. A low rise building design setting offers the opportunity to save substantially on operating costs once the building is operational. It is estimated that savings may be $600,000 annually. My research into why communities build vertically suggests that communities do this for one of two reasons; either they have a constrained site that will only accommodate a tall building or they wish to enhance their skyline. Neither applies in Jacksonville. Also, a vertical structure would require that the Clerk of Court's offices and functions be spread across several floors. This space is most accessed by the public and therefore, we believe, it should be located on one floor the ground floor and should be large enough to accommodate most Clerk functions without asking the public to traverse multiple stories by stairs, escalators or elevators. Finding #3 We believe that millions of dollars can be saved by choosing less expensive interior and exterior finishes for the courthouse. The interior finishes planned for some floors will cost more than double the interior finishes planned for other floors. The current design (ATTACHMENT C) includes columns and cantilevered areas, which increase the cost of the building, but have no function. The current design footprint (ATTACHMENT D) will require the relocation of Monroe Street to the south and leaves small odd shaped portions of two blocks that are not usable for anything other than small parks or plazas. Response to Finding #3 No building design has been agreed upon and, therefore, no interior or exterior finishes have been determined. As this process moves forward, life-cycle cost and durability will be primary factors for consideration in the selection of finishes. Recommendation #3 We recommend that the Administration bring the various alternatives for the courthouse s footprint, design, interior, and exterior finishes to the City Council or a committee thereof for their review and approval. The overriding concerns should be functionality and cost. Response to Recommendation #3 Ordinance continues the Courthouse Architectural Review Committee (CARC) also known as the Rinaman Committee -which was established in Ordinance The CARC - 5 -

8 includes two members of City Council, (the President and District 4 member), as well as five (5) others from various City and judicial offices, the Jacksonville Bar Association and BJP Citizens Oversight Committee. Under , CARC will be responsible for approving both the exterior and interior design of the courthouse to ensure it meets the goals of quality, durability, security and functionality for the public and the judiciary. Finding #4 It appears that the City gained little or nothing for the monies paid to the design-build firm Auchter/Perry-McCall. Approximately $1.2 million was spent on this contract. Another $200,000+ is being claimed by Auchter and subsidiary firms. According to the City s current courthouse project manager, the City s current design build firm, Turner Construction / KBJ, is not reusing the design work begun by Auchter/Perry-McCall. As such, in hindsight, the work was a waste of taxpayer dollars. Response to Finding #4 The work done by the former design-build team, Auchter Perry-McCall (APM), provided value on the Courthouse project. APM prepared a courts facility master plan that reaches to 2035, studied multiple alternative phasing scenarios, and provided cost estimates for each alternative. APM's analysis allowed us to go from considering a criminal court function only scenario ( ) to the unified legislation currently before City Council ( ). APM's scope of work in its $1.17 Million authorization did not contain any design work so there was no design work to reuse. Rather, their work product contained alternative concepts and scenarios as described above that will continue to provide value as we move to the next phase of this project. Recommendation #4 We recommend that the committee referenced in Recommendation #3 review the plans prepared by Auchter/Perry-McCall to determine what, if anything, can be salvaged. Finding #5 Old Federal Courthouse acquisition costs of $875,000 were not assigned to the courthouse project. Therefore, total courthouse expenditures are understated by this amount. Recommendation #5 For proper accounting purposes, the $875,000 of acquisition costs for the old federal courthouse should be charged to the courthouse project. Response to Recommendation #5 We respectfully disagree. The old federal courthouse was acquired from the General Services Administration via an economic development conveyance and there was not a plan for a courthouse at that time. The transaction was comprised of a commitment to provide the GSA parking spaces that were not being used in the Water Street garage for a period of 20 years. Council Auditor Rebuttal Proper accounting dictates that the acquisition costs be charged to the courthouse project

9 AUDIT OBJECTIVE #2 Our second audit objective was to analyze all bid documents and contracts related to the construction of the courthouse to determine how the project was bid, how contractors were selected, and the sufficiency of the contracts. We obtained the courthouse contracts from the Public Works Department and we reviewed bid/source selection documentation maintained by the Procurement Division. Audit Objective #2 Conclusion We noted a number of flaws with the wording and management of City contracts. For example, We noted contract payments based on the passage of time. We noted inconsistencies between, and within, contracts. This was also a finding in our audits of the Main Library (Report #612) and HDR (Report #613). We noted contracts where the City s interests were not adequately protected. We found that City representatives authorized contractors to perform work prior to execution of a contract and/or amendment. We also noted instances where City funds were expended unnecessarily. Finding #6 The contracts for the Construction Manager and the Architect/Engineer were flawed in that the payments for contract services were determined by a schedule that was based on the passage of time rather than the percentage of completion of the project. In our review we found correspondence between the City s previous project manager and a City attorney where the project manager stated that the reason for a passage of time basis of payment was to reduce the administrative burden of detailed payment review. As a result of a passage of time basis and the ongoing courthouse delays, the City paid $6,669,830 in construction manager fees when no vertical construction had begun. Recommendation #6 Payments to contractors should be based on the percentage of completion of a project or some other logical methodology, not on the passage of time. Response to Recommendation #6 We agree. Payments made to contractors building something, and engineers/architects designing something, are paid based on percentage of completion. Consultants who are strictly providing management services are paid hourly, very much like how City employees are paid. Finding #7 The contract between the City and Auchter/Perry-McCall for design-build services is dated January 29, Article 8.1.1(a) states that payments for the lump sum pre-design phase services totaling $1,170, shall be paid in proportion to the percentage of work completed. The contractor submitted its first invoice on February 1, 2007, just three days after the contract - 7 -

10 was executed. The City paid the invoice in the amount of $672,514, which represents 57% of the contract amount. It is not possible that the contractor completed 57% of the work in three days. If a contractor performs work without a signed contract, but with the City s knowledge, the City could be forced to pay for this work even if a contract is never executed. Recommendation #7 Although City contract documents and bid specifications state that contractors should not start work early, the City should consider moving this language to a more prominent location in procurement documents. As part of their training, City employees who participate in the procurement of goods and services need to be educated regarding the negative consequences to the City if an employee encourages a contractor to begin work prior to execution of a contract or even if a City employee knows that the contractor is actively working on the contract, but chooses to look the other way. Response to Recommendation #7 We agree and will insert the "do not start" language in a more prominent place in the procurement documents. Finding #8 In the Cannon contract for Architect/Engineer services, per paragraph 4.1.1, the amount of each invoice shall be based on a payment schedule for each design phase to be mutually agreed between the City and the AE for each design phase, as soon as practical after (emphasis added) the issuance of the Notice to Proceed. Recommendation #8 The City should not enter into any contract where ambiguity surrounds payment terms. No part of a contract should be left blank, to be decided in the future. All terms should be decided and included prior to execution of the contract. Response to Recommendation #8 We concur. Finding #9 Cannon Design, the City s AE firm, was not contractually required to estimate the cost of their design. The agreement originally called for Cannon to provide estimating services, but this requirement was removed to reduce cost and to stifle any thoughts that Cannon estimating against its own design was a conflict of interest. Instead the City paid Jacobs (the program manager) and Skanska (the construction manager) to perform cost estimates. Recommendation #9 The City should consider requiring all architects to estimate the cost of their design

11 Response to Recommendation #9 We concur in the case that a project is design-bid-build. However, when a construction manager at risk is under contract with the City to build the A/E's design, the construction manager's estimate governs. Finding #10 We noted the following instances where we believe that City funds were expended unnecessarily: As part of Skanska s compensation, an earned fee was to be awarded each quarter, if Skanska met certain requirements. A committee graded Skanska on various aspects of their job (safety, quality, etc) and, assuming a high grade was awarded, Skanska was paid $126,667. Skanska was paid the earned fee for four quarters for a total of $506,668. It is astonishing that no City representative worked to halt payment of these earned fees and realign the earned fee structure with the actual construction. $298,498 was paid to Skanska as compensation for their management of the underground utilities relocation. This management service was within the scope of their contract; however City staff authorized this $298,498 to be paid as compensation above their contract fee. If the services were truly above and beyond those contemplated in their contract, then a change order should have been executed. No such change order was executed. The City paid a former employee $1,250 for his time and expenses associated with testifying in eminent domain proceedings. The employee was subpoenaed. There was no reason to pay him. Recommendation #10 As part of their training, City employees who negotiate contracts and/or approve payments should be reminded that they are stewards of public funds and as such, they are responsible for protecting and using these funds in a prudent manner. The tone at the top must assure employees that not only will management be supportive if they question payments or costs, but that this is expected. Response to Recommendation #10 We concur with the recommendation and will appropriately move forward. Finding #11 Even though project estimates were over budget in violation of the Architect/Engineer contract (with Cannon Design), the City did not force compliance or stop the project. Section of the Architect/Engineer contract requires that The estimated cost of the Project will not exceed the budget at the end of each design phase. This will include cost reconciliation with the CM and PMC prior to authorization by the City to proceed with the next phase of design. Section states that AE must design and PROJECT must be capable of being constructed within the budget established by CITY as set forth in Exhibit F. We found reconciliations that came in over budget, yet the City authorized Cannon to proceed into the next phase of design

12 Recommendation #11 The City should hold its contract managers responsible for enforcing the provisions of the contracts they are managing. Response to Recommendation #11 We concur. Finding #12 City Engineers authorized Auchter/Perry-McCall to perform approximately $200,000 of work that was outside the scope of the contract with the intention of including the work in a future amendment. Recommendation #12 See recommendations #10 and #11. Response to Recommendation #12 We concur. Finding #13 The 13 contracts we reviewed are not standard and uniform. We found language to be inconsistent from one contract to the next as noted in the examples below: In the event of an internal inconsistency within a set of contract documents, an order of precedence clause establishes, in writing, the order in which the documents will govern. We found a myriad of differences between the order of precedence clauses in the contracts we reviewed. We also noted two contracts that did not include a precedence clause. In the City s contract with the Construction Manager, Skanska, we found that there are two order of precedence clauses, which contradict each other. We found inconsistent use of contract fee summaries, specifically in contract amendments. At times, the fee summary indicates only the dollar value of the amendment and at other times, it includes the amount of the base contract plus the amendment. We found these inconsistencies even from one amendment to the next within the same contract. As an example, the first amendment to the Program Manager contract (Jacobs) is unclear. It is arguable whether the contract sum, subsequent to the first amendment, was $350,000 or $600,000. We found one contract without an audit rights clause. We found that the audit rights clauses in the remaining contracts were not uniform and did not sufficiently provide for the City s benefit. A sample invoice is contained within the Cannon agreement (Exhibit I); however the contract contains no language requiring that submitted invoices be in the form of the sample. We also noted similar findings in our audit report (#612 released on May 3, 2006) on the Main Library Project and our audit report (#613 released on March 24, 2006) on the HDR Engineering

13 Contract. Discrepancies were noted between contract language and contract exhibits, specifically in the area of compensation. Recommendation #13 1. The City needs to adopt standard contracts as well as a process to update standard contracts when the need arises. 2. The Office of the General Counsel should insure that the interaction between agreement language and exhibits create no ambiguity as to their combined meaning. Language should be clear and consistent throughout the entire contract, including attachments and exhibits. 3. Specific to order of precedence clauses, the City should also include exhibits to amendments. 4. Public Works should modify the standard contract fee summary to include the Prior Contract Amount, the Amendment Amount, and the Amended Contract Amount. 5. Regarding audit rights clauses, we recommend the use of stronger, more detailed language. We have an example from a State of Florida contract, which we will be happy to provide. Response to Recommendation #13 1. The City does have standard contracts for design professional contracts, professional services for non design professionals, and bid contracts. The apparent problem with this matter is that the several contracting parties offered their own contracts. What should be done is to attach the City contract format to all requests for proposals with the notation that the city contract will be used. 2. The OGC agrees that contract language should be clear and consistent throughout the entire contract. 3. The OGC agrees that order of precedence provisions should include exhibits. Indeed the order of precedence is driven by what is contained in the exhibits on a project-by-project basis. Typically the order of precedence, in the event of a conflict, could be, in decreasing precedence, (1) the language of written amendments to the contract; (2) the language of the contract and (3) the language of exhibits to the contract, but only to the extent of the conflict. On the other hand, depending upon the exhibits the order of precedence could be, in decreasing precedence, (1) the language of written amendments to the contract; (2) the language of the exhibit and (3) the language of the contract. There is no consistent order of precedence, but only to the extent of the conflict. It would always be fact driven based on the circumstances of the contract. The important thing is to have the provision in the best interest of the City. OGC does not agree with the recommendation that an order of precedence include "exhibits to amendments" because once the amendment is signed by the parties to the contract, the amendment becomes part of the contract, not of the amendment. 4. OGC is able to work with existing forms and takes no position as to this recommendation. 5. OGC takes no position as to the audits rights clause. However if the Council Auditor has something that will better protect the city, OGC will be pleased to revise its standard forms

14 Finding #14 The Florida Department of Revenue (FDOR) gave the City permission to implement a sales tax savings program for Better Jacksonville Program (BJP) projects, contingent on the inclusion of specific language within the contract. This program allows the City to directly purchase construction materials, thereby saving the sales tax that would have been paid if the contractor had purchased the materials. The City Council approved the use of the program in Ordinance E. The ordinance, by itself, does not appear to satisfy FDOR s requirement. Recommendation #14 The City should include the explanation and requirements of the sales tax savings program in all bid specifications, RFPs and contracts to allow the City to engage the program, anytime it chooses. The Administration should contact FDOR to obtain an opinion on whether the City can use the recovery program on construction projects outside of BJP. If the City receives a favorable opinion, Chapter 126 of the municipal code could be amended to allow the use of a tax recovery program on construction activities outside of BJP. Response to Recommendation #14 We concur and will pursue expansion. Finding #15 None of the courthouse project contracts adequately define the term value engineering. We found that what was called value engineering may have been more appropriately referred to as scope reduction or expense delaying. For example, a reduction in ceiling heights would be better described as a scope reduction whereas the shelling of courtrooms would better be described as expense delaying. Recommendation #15 Construction contracts should include definitions of ambiguous terms (e.g. value engineering) to facilitate the ease of understanding between the City and the various parties involved. Response to Recommendation #15 We concur that all ambiguous terms should be defined. However, it should be noted that value engineering (and others), for example, are construction industry terms generally well understood by the contractors and engineers under contract to the City. AUDIT OBJECTIVE #3 Our third audit objective was to analyze ancillary courthouse projects, especially with regard to their cost (capital and operating) to the City and its independent agencies and the sufficiency of the delivered project. We reviewed the agreements between the City and JEA for chilled water, the agreement between the City and Metropolitan Parking Solution (MPS) for the construction and operation of the courthouse parking garage, and the agreement between the City and the Federal Government for the Old Federal Courthouse. We also reviewed accounting data for the projects and discussed the projects with various City, JEA, and JEDC employees

15 Audit Objective #3 Conclusion The chilled water system, the courthouse parking garage, and the old federal courthouse building all appear to be sufficient, meaning that they appear to be adequate for their intended purposes. Nothing has come to our attention to indicate otherwise. Regarding costs, the courthouse project is not being charged for any capital or operating costs for the chilled water project, the courthouse parking garage, or the acquisition of the old federal courthouse. We noted nothing that would make us think that the capital cost incurred by JEA to construct the chilled water system is not reasonable. We noted nothing that would make us think that the capital cost incurred by MPS to construct the parking garage is not reasonable. The cost to acquire the old federal courthouse appears to have been a very good deal for the City. The General Services Administration of the Federal Government traded the old federal courthouse to the City in exchange for a parking lease valued at $875,000 when the land alone is worth several million dollars. The City Public Buildings Division pays the utility bills for public buildings and therefore is paying the chilled water operating costs for the courthouse. JEDC is using funds from the Northbank Tax Increment District to make the cash flow loans to MPS for the parking garage. The City s Public Parking Division has lost the revenue from the 104 parking spaces leased to the General Services Administration for 20 years in exchange for the old federal courthouse. Finding #16 Per its contract with JEA, the City is paying JEA demand charges for chilled water of $29, per month ($355,770 annually) from September 1, 2007 through August 31, 2009 at which time the demand charges increase to $89, per month ($1,074,546 annually). This is wasted money on the City s part since the City has no need to heat and cool a courthouse which it has not constructed. JEA constructed its chilled water plant to meet the City s needs and timetable for the courthouse and main library. The library is currently using chilled water and the new City Hall Annex (former YMCA building) will also use chilled water for its heating and cooling needs. Demand charges are JEA s way of covering its fixed costs, such as debt service, that it has to pay, regardless of the amount of system usage. Recommendation #16 Refer to Recommendation #1. Response to Recommendation #16 We concur and have introduced legislation ( ) to fund a unified courthouse. That legislation is presently under consideration by City Council. Finding #17 City loans to MPS for the purchase of the parking garage sites and for the funding of parking garage operating deficits are not recorded in the City s general ledger. Per the contract between the City and MPS, the City is financing MPS purchase of the parking garage sites. These loans total $8,040, as of March 14, 2008, but date back as far as March 1, 2005 for the first $2,000,000 which was for the land beneath the arena and sports complex garages. When asked why the loans were not recorded on the City s general ledger, JEDC responded that they met

16 with GAD (General Accounting Division) not too long ago and were in the process of booking the loans. While we appreciate that things are probably moving in the right direction, these notes should be recorded promptly, not months or years later. Recommendation #17 The Administration should record the loans to MPS as an asset on the City s general ledger as expeditiously as possible. Response to Recommendation #17 As of 9/30/08, the City will report the loan and/or liability as either a contingent liability or a loan receivable. Finding #18 One of the selling points of the JEDC Redevelopment deal for MPS to construct and operate the parking garages for the courthouse, the sports complex, and the arena was that MPS would pay property taxes. However, the City may not receive the financial benefit of the taxes for decades, as explained below. Contract section 6.1 requires the City to make loans to the developer to enable the developer to have sufficient cash flow to cover all Project operating expenses, debt service on the project bonds plus required reserves, and an 8 to 10 percent return on the developer s $3,000,000 equity investment in the project. Property taxes are an expense of the project. Because the project operates at a deficit, the City is effectively loaning the money to MPS to pay the City its property taxes. Exhibit Q to the Redevelopment Agreement is a schedule of project projections. Based on this schedule, the City can expect to start receiving principal payments on its loans in year 28 of the project. That is the earliest time that the City will start receiving the benefit of the property taxes. We also noted that MPS paid the 2006 property taxes late (in July), not only failing to take advantage of the discount for early payment, but incurring a penalty for late payment. As of March 14, 2008, MPS has not yet paid the 2007 property taxes. Recommendation #18 If the amount of loans to MPS exceeds $16,000,000 at the end of 2011, the City has an option to purchase the parking garages pursuant to Section 6.3 of the Redevelopment Agreement. We recommend that the City do this in order to reduce the City s future cash outflows under the Agreement and to take advantage of the most favorable purchase price, which ends 60 days after the 2011 financial results are delivered to the City. After this window of opportunity closes, the parking garages can still be purchased pursuant to Section 6.1 of the Redevelopment Agreement, but the purchase price increases significantly pursuant to this section. Should the City not be able to purchase the garages pursuant to Section 6.3, it will have to evaluate whether or not it makes financial sense to purchase the garages pursuant to Section 6.1. Response to Recommendation #18 The City will actively consider the acquisition if and when the trigger opportunity arises to most efficiently address the current and future obligations associated therewith

17 Finding #19 The City s incentives to MPS to construct and operate the parking garages for the courthouse, arena, and sports complex are expensive and still require considerable time and attention from City employees. The project requires the on-going involvement of City employees in JEDC, Office of General Counsel, General Accounting, and Treasury. Twice annually, developer reports are received and reviewed, cash flow subsidy payments must be made, loans are accrued, and notes are recorded. The City is loaning millions of dollars, which will likely become tens of millions, to the developer for a project in which the City does not hold an ownership interest. We noted that the City does not even hold a first mortgage on the property sold to MPS. Instead, the City holds a subordinated promissory note. While we do not believe that a subordinate promissory note is adequate collateral for the $5.7 million of land which the City sold to the developer, we understand that the lack of a first mortgage has to do with the structure of the deal that the City agreed to. The investors who purchased the bonds used to fund construction of the garages hold the first mortgage on the land. Recommendation #19 To more fully describe an economic development proposal, JEDC fact sheets should be modified to disclose lifecycle costs for City personnel as well as lifecycle project costs and the City s security for its investment. Response to Recommendation #19 Where extraordinary circumstances warrant and the costs are reasonably calculable, the City will attempt to introduce life cycle costing in economic development proposal analyses. ADDITIONAL FINDINGS Finding #20 The Committee which judged the design competition and selected the winning design only contained one engineer. The City s Professional Services Evaluation Committee (PSEC) selected the design of the courthouse from the four finalists. The membership of PSEC is as follows: Procurement Chief or his designee, who will serve as the chair One representative from the Finance Department One representative from the Office of the General Counsel Two representatives from the using agency for which the professional services will be performed; these two individuals will also serve as the PSEC subcommittee In reviewing the tabulation of the rankings of the design competition, we noted that the engineer was the only member of PSEC who did not rank the Cannon design first. The design competition did have a Competition Advisory Committee. This committee did have a component of individuals with an engineering background. However, (a) the committee had no

18 voting rights and (b) the role of the Advisory Committee was unclear. The competition program described the Advisory Committee as follows: The Competition Advisory Committee is charged with the responsibility of reviewing all submissions of the selected Design Competition architects. Recommendation #20 For design competitions, the makeup of the selection committee should be changed to include a substantial representation from architects and engineers. In addition, the City should consider the use of a scoring matrix for design competitions which would award points for categories such as constructability, construction cost, future maintenance costs, etc. The City may wish to study the approach used by the U.S. General Services Administration (GSA). The GSA utilizes a fiveperson Evaluation Board comprised of experts in the fields of architecture and engineering to evaluate design submissions. No indication of authorship is allowed on the presentation boards. The Lead Designer and his/her team are listed in a sealed envelope attached to the back of the presentation boards. Response to Recommendation #20 I will direct Public Works and Procurement to jointly pursue the implementation of an improved process for design competitions. Finding #21 The role of the City s contracted Program Manager (who was paid $6,581,721.12) seems to be duplicative of the services that should have been provided or were being provided by the Construction Manager and the City s own engineers. Response to Finding #21 The Program Manager consultant was hired for the courthouse to avoid permanently growing Public Works' staff. This approach was successful on the arena, ball park, libraries and roadway programs. Recommendation #21 The City should consider hiring more full-time engineers to oversee projects rather than hiring contractors and consultants. We believe that full-time employees will actually be less expensive and are more likely to look out for the City s best interests. Response to Recommendation #21 We generally concur with your recommendation and would consider hiring more in-house engineers on a project by project basis. In the specific case of the courthouse, we are not hiring a new program manager, but are rather managing the project using current City employees. Finding #22 We noted the following problems with the PSEC evaluation matrix. Although the matrix scoring was revised in the 2004 procurement code rewrite, we still believe that the matrix could be improved upon

19 The PSEC evaluation matrix has two criteria (volume of work and past record of performance) which work against each other. Essentially it is impossible to be awarded the highest score (i.e. 100%). We question the appropriateness of a scoring matrix with an unattainable measure. During the Pre-Bid Proposal Conference for the CM (Construction Risk (June 2002), a City engineer described the evaluation matrix. In describing at least two of the 10 categories, it was said that the entire 10 point range of the category would not be used. Specifically, this was mentioned for the Current Workload and the Quotation of Rates, Fees, Charges. In addition, verbal commentary indicated that the Approach/Workplan category was probably the most important, but it was reiterated that the category would still be worth only 10 points (the same as every other). If this category was truly the most important, it seems that it should have been worth more points than other categories. Financial Responsibility is one of the ten criteria used to judge the best qualified proposer. Even if PSEC ranks a proposer low on financial responsibility, the proposer could still be awarded City business. Proposers should not be allowed to compete if they are not financially responsible. The real question may be whether or not the proposer can obtain a performance bond for the contract. Recommendation #22 The City should review its scoring matrix to determine the most effective criteria and the appropriate weighting of said criteria. City Procurement officials should not reduce the allowable score values for a given criterion after the RFP has been issued. If the intent of the procurement is to give certain criterion a lower weight, this should be described in the RFP itself; PSEC should not arbitrarily reduce the score range after the fact. Response to Recommendation #22 We generally concur with this recommendation that not all categories should be equally weighted and I will direct Public Works and Procurement to jointly pursue revising the Code and scoring matrix to more truly reflect the desired qualities and weights of each criterion. We appreciate the assistance and cooperation we received from JEA, the JEDC, the Office of the General Counsel, the Procurement Division, the Public Parking Division and the Public Works Department through the course of this audit. Respectfully submitted, Kirk A. Sherman Kirk A. Sherman, CPA Council Auditor

20 ATTACHMENT A Glossary of Construction Terminology Prepared by City of Jacksonville Public Works Department Architect / Engineer A firm or person licensed under Florida Statutes to perform professional architectural or engineering services. The City contracts with A/E's to design our Public Works projects through the Request for Proposals process based on qualifications. Construction Documents The phase of design after Design Development where all construction details are defined and drawn, all finishes are defined and specified, and general requirements of the construction are specified. This is the set of drawings the contractor builds the project by. Construction Manager A general contractor who does not actually self perform any of the construction work on a project, but rather bids the parts of the project out to subcontractors who build the work under the supervision of the construction manager. Construction management is a professional service whereby the firm is selected based on its qualifications, not price. Construction Risk Same as above, except now the construction manager, at some point in the project, guarantees the maximum price the project will cost for a specific scope, and is responsible for covering any costs that exceed the guarantee. This process usually includes some incentive (additional profit) for completing the project below the guaranteed maximum price. Design / Bid / Build A project delivery system where the owner contracts directly with an architectural/engineering (A/E) firm to design a project under the supervision of the owner. When the design is complete, the owner solicits bids from general contractors to build the project in accordance with the A/E's plans, and awards the contract to the lowest responsible bidder. Design / Build A project delivery system where a single entity is responsible for both designing and building a project. Design Development The phase of design of a vertical project where all spaces and systems in the building are defined and designed, but many details lacking. Fast Track General term which typically means that construction will start before design is complete. Only applies to Design-Build and Construction Manager project delivery systems.

21 Guaranteed Maximum Cost This is not a term or phrase that Public Works uses. Guaranteed Maximum Price The maximum amount of money the construction manager offers to build the project for with a specified scope. Any costs above that amount are the responsibility of the construction manager, not the owner. Lump Sum Payment Type A fixed fee for a fixed scope of work, payable when the fixed scope of work has been satisfactorily completed regardless of the expense incurred by the vendor in completing the scope. Maximum Not To Exceed Payment Type Primarily used when a lump sum payment amount cannot be mutually negotiated and agreed upon - perhaps the scope is a bit unclear. Payment is made based on the vendor's actual cost incurred in good faith to complete the scope of work, but not to exceed the agreed upon maximum. Program A series of related projects governed by one overall program budget, but not necessarily restricted by specific budgets for each individual project in the program. Program Manager A consulting firm hired by the City to lead the implementation of a program by directing and leading the designers and construction contractors of the projects in the program. Project A single specific work (involving procurement, engineering and construction) with a defined scope and fixed budget. Value Engineering The process of reducing the cost of a project without cutting scope, but rather by changing materials, construction means and methods, finishes, façades, etc., such that the original functionality and operational goals are still achieved.

22 ATTACHMENT B Council Auditor's Office Courthouse Audit Breakdown of Monies Spent Table 1 from Report Body Land $ 23,118,666 Engineering 10,732,156 Other Construction 30,571,115 Materials 197,263 Total : $ 64,619,200 Breakdown Including Major Contractors Auchter/Perry-McCall Joint Venture $ 1,170,441 Bellsouth Telecommunications 415,000 Cannon Design 8,548,319 Dan Wiley & Associates 321,205 Global Performance 466,668 Jacobs Engineering 6,581,721 R.B. Gay Construction 1,848,503 Skanska 15,860,109 Other Construction & Engineering 4,215,566 Subtotal : 39,427,531 Land 23,118,666 Materials 197,263 Expenditures on Current C/H and City Hall Annex 1,875,738 Total : $ 64,619,198 ** Any difference is due to rounding **

23 ATTACHMENT C

24 ATTACHMENT D

State Housing Initiatives Partnership Audit - #769 Executive Summary

Council Auditor s Office City of Jacksonville, Fl State Housing Initiatives Partnership Audit - #769 Executive Summary Why CAO Did This Review Pursuant to Section 5.10 of the Charter of the City of Jacksonville

Council Auditor s Office City of Jacksonville, Fl State Housing Initiatives Partnership Audit - #769 Executive Summary Why CAO Did This Review Pursuant to Section 5.10 of the Charter of the City of Jacksonville

Request for Proposals

Request for Proposals On Call Right-of-Way and Easement Acquisition and Related Services Requested by: Charter Township of Shelby Department of Public Works 6333 23 Mile Road Shelby Township, MI 48316

Request for Proposals On Call Right-of-Way and Easement Acquisition and Related Services Requested by: Charter Township of Shelby Department of Public Works 6333 23 Mile Road Shelby Township, MI 48316

Hillwood Master Disposition & Development Agreement Audit - #809 Executive Summary

Council Auditor s Office City of Jacksonville, Fl Hillwood Master Disposition & Development Agreement Audit - #809 Executive Summary Why CAO Did This Review Pursuant to Section 5.10 of the Charter of the

Council Auditor s Office City of Jacksonville, Fl Hillwood Master Disposition & Development Agreement Audit - #809 Executive Summary Why CAO Did This Review Pursuant to Section 5.10 of the Charter of the

RECITALS STATEMENT OF AGREEMENT. Draft: November 30, 2018

MEMORANDUM OF AGREEMENT TO FACILITATE THE EXPANSION, RENOVATION, AND EFFICIENT AND SAFE OPERATION OF THE ALBEMARLE CIRCUIT COURT, THE ALBEMARLE GENERAL DISTRICT COURT, AND THE CHARLOTTESVILLE GENERAL DISTRICT

MEMORANDUM OF AGREEMENT TO FACILITATE THE EXPANSION, RENOVATION, AND EFFICIENT AND SAFE OPERATION OF THE ALBEMARLE CIRCUIT COURT, THE ALBEMARLE GENERAL DISTRICT COURT, AND THE CHARLOTTESVILLE GENERAL DISTRICT

PERRY CITY UTAH REQUEST FOR PROPOSALS REAL ESTATE BROKER SERVICES

PERRY CITY UTAH REQUEST FOR PROPOSALS REAL ESTATE BROKER SERVICES Overview The City of Perry, Utah is hereby requesting proposals from qualified, real estate brokers to assist with the sale of approximately

PERRY CITY UTAH REQUEST FOR PROPOSALS REAL ESTATE BROKER SERVICES Overview The City of Perry, Utah is hereby requesting proposals from qualified, real estate brokers to assist with the sale of approximately

Town of North Castle New York REQUEST FOR PROPOSALS REAL ESTATE BROKER SERVICES

Town of North Castle New York REQUEST FOR PROPOSALS REAL ESTATE BROKER SERVICES 1. Overview The Town of North Castle, New York is hereby requesting proposals from qualified, real estate brokers to assist

Town of North Castle New York REQUEST FOR PROPOSALS REAL ESTATE BROKER SERVICES 1. Overview The Town of North Castle, New York is hereby requesting proposals from qualified, real estate brokers to assist

Purchasing Guide. MTAS MORe. Published on MTAS ( November 06, 2018

Published on MTAS (http://www.mtas.tennessee.edu) November 06, 2018 Purchasing Guide Dear Reader: The following document was created from the MTAS electronic library known as MORe (www.mtas.tennessee.edu/more).

Published on MTAS (http://www.mtas.tennessee.edu) November 06, 2018 Purchasing Guide Dear Reader: The following document was created from the MTAS electronic library known as MORe (www.mtas.tennessee.edu/more).

H. UNIVERSITY PROCUREMENT CODE

Page 1 H. UNIVERSITY PROCUREMENT CODE 3-801 General A. Applicability 1. This Article H ( University Procurement Code ) shall consist of rules prescribing procurement policies and procedures for the Arizona

Page 1 H. UNIVERSITY PROCUREMENT CODE 3-801 General A. Applicability 1. This Article H ( University Procurement Code ) shall consist of rules prescribing procurement policies and procedures for the Arizona

ISC: UNRESTRICTED AC Attachment. Attainable Homes Acquisition and Development Cycle Audit

Attainable Homes Acquisition and Development Cycle Audit April 6, 2016 THIS PAGE LEFT INTENTIONALLY BLANK ISC: UNRESTRICTED Table of Contents Executive Summary... 5 1.0 Background... 6 2.0 Audit Objectives,

Attainable Homes Acquisition and Development Cycle Audit April 6, 2016 THIS PAGE LEFT INTENTIONALLY BLANK ISC: UNRESTRICTED Table of Contents Executive Summary... 5 1.0 Background... 6 2.0 Audit Objectives,

EAST BATON ROUGE REDEVELOPMENT AUTHORITY ADMINISTRATIVE POLICY PROCUREMENT CONTRACTING AND DBE POLICY FOR FEDERALLY FUNDED PROJECTS.

EAST BATON ROUGE REDEVELOPMENT AUTHORITY ADMINISTRATIVE POLICY PROCUREMENT CONTRACTING AND DBE POLICY FOR FEDERALLY FUNDED PROJECTS February 5, 2013 East Baton Rouge Redevelopment Authority 801 North Blvd,

EAST BATON ROUGE REDEVELOPMENT AUTHORITY ADMINISTRATIVE POLICY PROCUREMENT CONTRACTING AND DBE POLICY FOR FEDERALLY FUNDED PROJECTS February 5, 2013 East Baton Rouge Redevelopment Authority 801 North Blvd,

Maryland Agricultural Land Preservation Fund

Audit Report Maryland Agricultural Land Preservation Fund Fiscal Year Ended June 30, 2006 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related

Audit Report Maryland Agricultural Land Preservation Fund Fiscal Year Ended June 30, 2006 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related

A. The purpose of this policy is to establish purchasing guidelines. This policy is applicable to all purchasing for the City of Moscow Mills.

Chapter 25 -- Expenditure of City Funds 25.010. Appropriations. In all cases where the City shall be indebted to any person, company, or corporation on any account, when the said account has been duly

Chapter 25 -- Expenditure of City Funds 25.010. Appropriations. In all cases where the City shall be indebted to any person, company, or corporation on any account, when the said account has been duly

How to Read a Real Estate Appraisal Report

How to Read a Real Estate Appraisal Report Much of the private, corporate and public wealth of the world consists of real estate. The magnitude of this fundamental resource creates a need for informed

How to Read a Real Estate Appraisal Report Much of the private, corporate and public wealth of the world consists of real estate. The magnitude of this fundamental resource creates a need for informed

SCHOOL BUSINESS LAW: THINGS YOU NEED TO KNOW IN THIS ECONOMY

SCHOOL BUSINESS LAW: THINGS YOU NEED TO KNOW IN THIS ECONOMY Presentation by Chris Burger & Bill Hornback August 7, 2009 I. E-RATE RULES A. CMAS. Use of the state master contracts, known as CMAS contracts,

SCHOOL BUSINESS LAW: THINGS YOU NEED TO KNOW IN THIS ECONOMY Presentation by Chris Burger & Bill Hornback August 7, 2009 I. E-RATE RULES A. CMAS. Use of the state master contracts, known as CMAS contracts,

Common Audit Findings Related to Purchasing and How to Avoid Them

Common Audit Findings Related to Purchasing and How to Avoid Them Jennifer L. Smith, CPA, Senior Manager 1 Audit Reports and Types of Audit Findings Report on Internal Control over Financial Reporting

Common Audit Findings Related to Purchasing and How to Avoid Them Jennifer L. Smith, CPA, Senior Manager 1 Audit Reports and Types of Audit Findings Report on Internal Control over Financial Reporting

Clerk of the Circuit Court Board of County Commissioners Marion County

Clerk of the Circuit Court Board of County Commissioners Marion County Internal Audit Division David R. Ellspermann Clerk of the Circuit Court Post Office Box 1030, Ocala, Florida 34478-1030 elephone:

Clerk of the Circuit Court Board of County Commissioners Marion County Internal Audit Division David R. Ellspermann Clerk of the Circuit Court Post Office Box 1030, Ocala, Florida 34478-1030 elephone:

EN Official Journal of the European Union L 320/373

29.11.2008 EN Official Journal of the European Union L 320/373 INTERNATIONAL FINANCIAL REPORTING STANDARD 3 Business combinations OBJECTIVE 1 The objective of this IFRS is to specify the financial reporting

29.11.2008 EN Official Journal of the European Union L 320/373 INTERNATIONAL FINANCIAL REPORTING STANDARD 3 Business combinations OBJECTIVE 1 The objective of this IFRS is to specify the financial reporting

CHAPTER 82 HOUSING FINANCE

82.01 INTRODUCTION CHAPTER 82 HOUSING FINANCE Latest Revision 1994 In 1982 the Ohio Constitution was amended to allow the state to assist in providing single family first time home buyer housing and multi-family

82.01 INTRODUCTION CHAPTER 82 HOUSING FINANCE Latest Revision 1994 In 1982 the Ohio Constitution was amended to allow the state to assist in providing single family first time home buyer housing and multi-family

Chapter 9. Competitive Sealed Bidding: Evaluating Bids

Chapter 9. Competitive Sealed Bidding: Evaluating Bids Summary This chapter describes the steps to be taken in order to properly evaluate each bid received in response to an invitation for bids. The two

Chapter 9. Competitive Sealed Bidding: Evaluating Bids Summary This chapter describes the steps to be taken in order to properly evaluate each bid received in response to an invitation for bids. The two

REQUEST FOR PROPOSALS Professional Engineering Services for Lift Station In the Rural Municipality of Wellington

REQUEST FOR PROPOSALS Professional Engineering Services for Lift Station In the Rural Municipality of Wellington Issue Date: March 2, 2018 Prepared By: Rural Municipality of Wellington Wellington, PEI

REQUEST FOR PROPOSALS Professional Engineering Services for Lift Station In the Rural Municipality of Wellington Issue Date: March 2, 2018 Prepared By: Rural Municipality of Wellington Wellington, PEI

FLORIDA DEPARTMENT OF TRANSPORTATION

FLORIDA DEPARTMENT OF TRANSPORTATION ADDENDUM NO. 1 DATE: 5/15/2015 RE: BID/RFP #: ITN-DOT-15/16-1012BT BID/RFP TITLE: District Wide Appraisal and Appraisal Review Services OPENING DATE: June 22, 2015

FLORIDA DEPARTMENT OF TRANSPORTATION ADDENDUM NO. 1 DATE: 5/15/2015 RE: BID/RFP #: ITN-DOT-15/16-1012BT BID/RFP TITLE: District Wide Appraisal and Appraisal Review Services OPENING DATE: June 22, 2015

Chapter 11. Competitive Negotiation: Procedure

Chapter 11. Competitive Negotiation: Procedure Summary This chapter provides an overview of the procedure for procuring goods and services using the competitive negotiation procedure. The competitive negotiation

Chapter 11. Competitive Negotiation: Procedure Summary This chapter provides an overview of the procedure for procuring goods and services using the competitive negotiation procedure. The competitive negotiation

TEXAS GENERAL LAND OFFICE PROCUREMENT GUIDANCE FOR RECIPIENTS AND SUBRECIPIENTS UNDER 2 CFR PART 200 (UNIFORM RULES)

") TEXAS GENERAL LAND OFFICE COMMUNITY DEVELOPMENT & REVITALIZATION PROCUREMENT GUIDANCE FOR RECIPIENTS AND SUBRECIPIENTS UNDER 2 CFR PART 200 (UNIFORM RULES) This checklist will assist the Texas General

TEXAS GENERAL LAND OFFICE COMMUNITY DEVELOPMENT & REVITALIZATION PROCUREMENT GUIDANCE FOR RECIPIENTS AND SUBRECIPIENTS UNDER 2 CFR PART 200 (UNIFORM RULES) This checklist will assist the Texas General

PROCUREMENT CODE. Part A Project Delivery and Selection Methods

PROCUREMENT CODE ARTICLE 6 CONSTRUCTION AND RELATED SERVICES Part A Project Delivery and Selection Methods 6-101 Project Delivery Methods. 1. Determination. The Director shall make a determination regarding

PROCUREMENT CODE ARTICLE 6 CONSTRUCTION AND RELATED SERVICES Part A Project Delivery and Selection Methods 6-101 Project Delivery Methods. 1. Determination. The Director shall make a determination regarding

Office of the County Auditor. Broward County Property Appraiser Report on Transition Review Services

Office of the County Auditor Broward County Property Appraiser Report on Transition Review Services January 14, 2005 Table of Contents BACKGROUND AND SCOPE...3 FINDINGS AND RECOMMENDATIONS...3 1. Financial

Office of the County Auditor Broward County Property Appraiser Report on Transition Review Services January 14, 2005 Table of Contents BACKGROUND AND SCOPE...3 FINDINGS AND RECOMMENDATIONS...3 1. Financial

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 2015 S 2 SENATE BILL 554 Education/Higher Education Committee Substitute Adopted 6/24/16

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION S SENATE BILL Education/Higher Education Committee Substitute Adopted // Short Title: School Building Leases. (Public) Sponsors: Referred to: March 0, 1 0 1 A

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION S SENATE BILL Education/Higher Education Committee Substitute Adopted // Short Title: School Building Leases. (Public) Sponsors: Referred to: March 0, 1 0 1 A

EASTERN WEST VIRGINIA COMMUNITY & TECHNICAL COLLEGE REGULATION No. AR- 7.10

EASTERN WEST VIRGINIA COMMUNITY & TECHNICAL COLLEGE REGULATION No. AR- 7.10 TITLE: PURCHASE OR ACQUISITION OF MATERIALS, SUPPLIES, EQUIPMENT, SERVICES AND PRINTING General Summary Statement of Administrative

EASTERN WEST VIRGINIA COMMUNITY & TECHNICAL COLLEGE REGULATION No. AR- 7.10 TITLE: PURCHASE OR ACQUISITION OF MATERIALS, SUPPLIES, EQUIPMENT, SERVICES AND PRINTING General Summary Statement of Administrative

Attachment 2 Civil Engineering

A. Phase 1, Programming and Schematic Design: The CONSULTANT shall for each project: 1. Ascertain the project s requirements through a meeting with the COUNTY, and a review of an existing schematic layout

A. Phase 1, Programming and Schematic Design: The CONSULTANT shall for each project: 1. Ascertain the project s requirements through a meeting with the COUNTY, and a review of an existing schematic layout

CHAPTER 10 PURCHASING

CHAPTER 10 PURCHASING GENERAL PROVISIONS 1000. County Purchases. All contracts for the purchase or lease of supplies, materials, equipment, or services, except as to personal and professional services

CHAPTER 10 PURCHASING GENERAL PROVISIONS 1000. County Purchases. All contracts for the purchase or lease of supplies, materials, equipment, or services, except as to personal and professional services

LWDB PROCUREMENT / PROPERTY MANAGEMENT POLICY

NWPA WDB POLICY - 100 Rev. Level: C LWDB PROCUREMENT / PROPERTY MANAGEMENT POLICY The system of property and procurement management must have procedures to determine the actions of responsible parties

NWPA WDB POLICY - 100 Rev. Level: C LWDB PROCUREMENT / PROPERTY MANAGEMENT POLICY The system of property and procurement management must have procedures to determine the actions of responsible parties

BOARD OF TRUSTEES JEFFERSON TOWNSHIP, MONTGOMERY COUNTY, OHIO RESOLUTION NO 16-38

BOARD OF TRUSTEES JEFFERSON TOWNSHIP, MONTGOMERY COUNTY, OHIO RESOLUTION NO 16-38 ESTABLISHING A PROCUREMENT AND PURCHASING POLICY FOR ASSISTANCE TO FIREFIGHTER GRANTS The Board of Trustees of Jefferson

BOARD OF TRUSTEES JEFFERSON TOWNSHIP, MONTGOMERY COUNTY, OHIO RESOLUTION NO 16-38 ESTABLISHING A PROCUREMENT AND PURCHASING POLICY FOR ASSISTANCE TO FIREFIGHTER GRANTS The Board of Trustees of Jefferson

Audit of City Lease Administration

July 22, 2009 Audit of City Lease Administration Sam M. McCall, Ph.D., CPA, CGFM, CIA, CGAP City Auditor HIGHLIGHTS Highlights of City Auditor Report #0917, a report to the City Commission and City management

July 22, 2009 Audit of City Lease Administration Sam M. McCall, Ph.D., CPA, CGFM, CIA, CGAP City Auditor HIGHLIGHTS Highlights of City Auditor Report #0917, a report to the City Commission and City management

File Reference No Re: Proposed Accounting Standards Update, Leases (Topic 842): Targeted Improvements

: Targeted Improvements") Deloitte & Touche LLP 695 East Main Street Stamford, CT 06901-2141 Tel: + 1 203 708 4000 Fax: + 1 203 708 4797 www.deloitte.com Ms. Susan M. Cosper Technical Director Financial Accounting Standards Board

Deloitte & Touche LLP 695 East Main Street Stamford, CT 06901-2141 Tel: + 1 203 708 4000 Fax: + 1 203 708 4797 www.deloitte.com Ms. Susan M. Cosper Technical Director Financial Accounting Standards Board

Implementing GASB s Lease Guidance

The effective date of the Governmental Accounting Standards Board s (GASB) new lease guidance is drawing nearer. Private sector companies also have recently adopted significantly revised lease guidance;

The effective date of the Governmental Accounting Standards Board s (GASB) new lease guidance is drawing nearer. Private sector companies also have recently adopted significantly revised lease guidance;

S 2001 S T A T E O F R H O D E I S L A N D

======== LC00 ======== 01 -- S 001 S T A T E O F R H O D E I S L A N D IN GENERAL ASSEMBLY JANUARY SESSION, A.D. 01 J O I N T R E S O L U T I O N AND A N A C T AUTHORIZING THE STATE TO ENTER INTO FINANCING

======== LC00 ======== 01 -- S 001 S T A T E O F R H O D E I S L A N D IN GENERAL ASSEMBLY JANUARY SESSION, A.D. 01 J O I N T R E S O L U T I O N AND A N A C T AUTHORIZING THE STATE TO ENTER INTO FINANCING

NSP Rental Basics: A Primer on Using Rental Projects to Meet NSP Obligation and 25% Set-Aside Requirement. About this Tool

NSP Rental Basics: A Primer on Using Rental Projects to Meet NSP Obligation and 25% Set-Aside Requirement About this Tool Description: This tool is intended for NSP grantees and their partners seeking

NSP Rental Basics: A Primer on Using Rental Projects to Meet NSP Obligation and 25% Set-Aside Requirement About this Tool Description: This tool is intended for NSP grantees and their partners seeking

Topic 842 Technical Corrections Summary of Comments Received

Contact(s) David Hoyer Co-Author Ext. 462 Andy Bologna Co-Author Ext. 356 Thomas Faineteau Co-Author Ext. 362 Chris Roberge Co-Author Ext. 274 Amy Park Co-Author Ext. 476 Shayne Kuhaneck Assistant Director

Contact(s) David Hoyer Co-Author Ext. 462 Andy Bologna Co-Author Ext. 356 Thomas Faineteau Co-Author Ext. 362 Chris Roberge Co-Author Ext. 274 Amy Park Co-Author Ext. 476 Shayne Kuhaneck Assistant Director

LOCAL GOVERNMENT PROMPT PAYMENT ACT

LOCAL GOVERNMENT PROMPT PAYMENT ACT 218.70 Popular name. 218.71 Purpose and policy. 218.72 Definitions. 218.73 Timely payment for nonconstruction services. 218.735 Timely payment for purchases of construction

LOCAL GOVERNMENT PROMPT PAYMENT ACT 218.70 Popular name. 218.71 Purpose and policy. 218.72 Definitions. 218.73 Timely payment for nonconstruction services. 218.735 Timely payment for purchases of construction

REQUEST FOR PROPOSALS (RFP) SECTION 8 CONTRACT ADMINISTRATION SERVICES

SECTION 8 CONTRACT ADMINISTRATION SERVICES") REQUEST FOR PROPOSALS (RFP) 09-331 SECTION 8 CONTRACT ADMINISTRATION SERVICES FOR THE HOUSING AUTHORITY OF THE CITY OF WINSTON-SALEM WINSTON-SALEM, NORTH CAROLINA 1 TABLE OF CONTENTS 1. Introduction 2.

REQUEST FOR PROPOSALS (RFP) 09-331 SECTION 8 CONTRACT ADMINISTRATION SERVICES FOR THE HOUSING AUTHORITY OF THE CITY OF WINSTON-SALEM WINSTON-SALEM, NORTH CAROLINA 1 TABLE OF CONTENTS 1. Introduction 2.

IAS Revenue. By:

IAS - 18 Revenue International Accounting Standard No 18 (IAS 18) Revenue In 1998, IAS 39, Financial Instruments: Recognition and Measurement, amended paragraph 11 of IAS 18, adding a cross-reference to

IAS - 18 Revenue International Accounting Standard No 18 (IAS 18) Revenue In 1998, IAS 39, Financial Instruments: Recognition and Measurement, amended paragraph 11 of IAS 18, adding a cross-reference to

Charleston County School District. Procurement Services

Vendor Guide Procurement Services July 2006 Vendor Guide Page 1 Table of Contents Introduction...2 About Charleston School District...2 About Procurement Servcies...2 District Procurement Code...3 Direct

Vendor Guide Procurement Services July 2006 Vendor Guide Page 1 Table of Contents Introduction...2 About Charleston School District...2 About Procurement Servcies...2 District Procurement Code...3 Direct

Exposure Draft ED/2013/6, issued by the International Accounting Standards Board (IASB)

") Leases Exposure Draft ED/2013/6, issued by the International Accounting Standards Board (IASB) Comments from ACCA 13 September 2013 ACCA (the Association of Chartered Certified Accountants) is the global

Leases Exposure Draft ED/2013/6, issued by the International Accounting Standards Board (IASB) Comments from ACCA 13 September 2013 ACCA (the Association of Chartered Certified Accountants) is the global

ROAD HOME CORPORATION d/b/a LOUISIANA LAND TRUST STATE OF LOUISIANA

ROAD HOME CORPORATION d/b/a LOUISIANA LAND TRUST STATE OF LOUISIANA FINANCIAL STATEMENT AUDIT ISSUED NOVEMBER 24, 2010 LEGISLATIVE AUDITOR 1600 NORTH THIRD STREET POST OFFICE BOX 94397 BATON ROUGE, LOUISIANA

ROAD HOME CORPORATION d/b/a LOUISIANA LAND TRUST STATE OF LOUISIANA FINANCIAL STATEMENT AUDIT ISSUED NOVEMBER 24, 2010 LEGISLATIVE AUDITOR 1600 NORTH THIRD STREET POST OFFICE BOX 94397 BATON ROUGE, LOUISIANA

CARLSBAD MUNICIPAL SCHOOLS INVITATION TO SUBMIT SEALED BID. BID # SAXON PHONICS NIGP Code: 78587

CARLSBAD MUNICIPAL SCHOOLS INVITATION TO SUBMIT SEALED BID BID # 2017-2018-01 SAXON PHONICS NIGP Code: 78587 ISSUE DATE: August 9, 2017 SUBMISSION DEADLINE: Thursday, August 24, 2017 2:00 PM Mountain Time

CARLSBAD MUNICIPAL SCHOOLS INVITATION TO SUBMIT SEALED BID BID # 2017-2018-01 SAXON PHONICS NIGP Code: 78587 ISSUE DATE: August 9, 2017 SUBMISSION DEADLINE: Thursday, August 24, 2017 2:00 PM Mountain Time

Technical Line SEC staff guidance

No. 2013-20 Updated 27 August 2015 Technical Line SEC staff guidance How to apply S-X Rule 3-14 to real estate acquisitions In this issue: Overview... 1 Applicability of Rule 3-14... 2 Measuring significance...

No. 2013-20 Updated 27 August 2015 Technical Line SEC staff guidance How to apply S-X Rule 3-14 to real estate acquisitions In this issue: Overview... 1 Applicability of Rule 3-14... 2 Measuring significance...

CENTRAL GOVERNMENT ACCOUNTING STANDARDS

CENTRAL GOVERNMENT ACCOUNTING STANDARDS NOVEMBER 2016 STANDARD 4 Requirements STANDARD 5 INTANGIBLE ASSETS INTRODUCTION... 75 I. CENTRAL GOVERNMENT S SPECIALISED ASSETS... 75 I.1. The collection of sovereign

CENTRAL GOVERNMENT ACCOUNTING STANDARDS NOVEMBER 2016 STANDARD 4 Requirements STANDARD 5 INTANGIBLE ASSETS INTRODUCTION... 75 I. CENTRAL GOVERNMENT S SPECIALISED ASSETS... 75 I.1. The collection of sovereign

MUNISTAT SERVICES INC. Municipal Finance Advisory Service

Phone: (631) 331-8888 Fax: (631) 331-8834 MUNISTAT SERVICES INC. Municipal Finance Advisory Service Website: www.munistat.com Serving Municipalities and School Districts in New York State Since 1977 12

Phone: (631) 331-8888 Fax: (631) 331-8834 MUNISTAT SERVICES INC. Municipal Finance Advisory Service Website: www.munistat.com Serving Municipalities and School Districts in New York State Since 1977 12

REQUEST FOR PROPOSAL (RFP) RFP AS. Appraisal Services Valuation of DBHA Properties

RFP AS. Appraisal Services Valuation of DBHA Properties") REQUEST FOR PROPOSAL (RFP) RFP 2019-01AS Appraisal Services Valuation of DBHA Properties Daytona Beach Housing Authority (DBHA) 211 N Ridgewood Ave Suite 300 Daytona Beach, FL 32114 (386) 253-5653 Terril

REQUEST FOR PROPOSAL (RFP) RFP 2019-01AS Appraisal Services Valuation of DBHA Properties Daytona Beach Housing Authority (DBHA) 211 N Ridgewood Ave Suite 300 Daytona Beach, FL 32114 (386) 253-5653 Terril

CONTRACTING - BID LAWS

LEGAL COMPLIANCE AUDIT GUIDE Introduction A municipality entering into an agreement for the sale or purchase of supplies, materials, equipment or the rental thereof, or the construction, alteration, repair

LEGAL COMPLIANCE AUDIT GUIDE Introduction A municipality entering into an agreement for the sale or purchase of supplies, materials, equipment or the rental thereof, or the construction, alteration, repair

HPL PROCUREMENT POLICIES HAMBURG PUBLIC LIBRARY PROCUREMENT POLICIES AND PROCEDURES AS REQUIRED UNDER GENERAL MUNICIPAL LAW SECTIONS 103 and 104-B.

HPL PROCUREMENT POLICIES HAMBURG PUBLIC LIBRARY PROCUREMENT POLICIES AND PROCEDURES AS REQUIRED UNDER GENERAL MUNICIPAL LAW SECTIONS 103 and 104-B. STATEMENT OF PURPOSE The purpose of these policies and

HPL PROCUREMENT POLICIES HAMBURG PUBLIC LIBRARY PROCUREMENT POLICIES AND PROCEDURES AS REQUIRED UNDER GENERAL MUNICIPAL LAW SECTIONS 103 and 104-B. STATEMENT OF PURPOSE The purpose of these policies and

HUNTINGDON SPECIAL SCHOOL DISTRICT PROCUREMENT PLAN CHILD NUTRITION PROGRAM

HUNTINGDON SPECIAL SCHOOL DISTRICT PROCUREMENT PLAN CHILD NUTRITION PROGRAM This procurement plan contained on the following pages 1 through 10 will be implemented on July 1, 2016 from that date forward

HUNTINGDON SPECIAL SCHOOL DISTRICT PROCUREMENT PLAN CHILD NUTRITION PROGRAM This procurement plan contained on the following pages 1 through 10 will be implemented on July 1, 2016 from that date forward

SECTION F: Facilities Development

SECTION F: Facilities Development Section F of the EPS/NSBA policy classification system provides a repository for statements on school construction, remodeling and modernizing, temporary facilities, and

SECTION F: Facilities Development Section F of the EPS/NSBA policy classification system provides a repository for statements on school construction, remodeling and modernizing, temporary facilities, and

REAL ESTATE TOPICS JUNE 1, 2008 NEGOTIATING AND STRUCTURING JOINT VENTURE AND LLC AGREEMENTS

BENNETT VALLEY LAW REAL ESTATE TOPICS JUNE 1, 2008 NEGOTIATING AND STRUCTURING JOINT VENTURE AND LLC AGREEMENTS Parties negotiate joint venture agreements in the spirit of optimism. Anxious to combine

BENNETT VALLEY LAW REAL ESTATE TOPICS JUNE 1, 2008 NEGOTIATING AND STRUCTURING JOINT VENTURE AND LLC AGREEMENTS Parties negotiate joint venture agreements in the spirit of optimism. Anxious to combine

State of New York Office of the State Comptroller Division of Management Audit and State Financial Services

State of New York Office of the State Comptroller Division of Management Audit and State Financial Services NEW YORK CITY DEPARTMENT OF HOUSING PRESERVATION AND DEVELOPMENT REHABILITATION AND DISPOSAL

State of New York Office of the State Comptroller Division of Management Audit and State Financial Services NEW YORK CITY DEPARTMENT OF HOUSING PRESERVATION AND DEVELOPMENT REHABILITATION AND DISPOSAL

OFFICE OF INSPECTOR GENERAL PALM BEACH COUNTY

PALM BEACH COUNTY CONTRACT OVERSIGHT NOTIFICATION () John A. Carey Inspector General ISSUE DATE: SEPTEMBER 26, 2014 Enhancing Public Trust in Government Track K Land Sale SUMMARY What We Did Pursuant to

PALM BEACH COUNTY CONTRACT OVERSIGHT NOTIFICATION () John A. Carey Inspector General ISSUE DATE: SEPTEMBER 26, 2014 Enhancing Public Trust in Government Track K Land Sale SUMMARY What We Did Pursuant to

COMPETITIVE BIDDING NOTICE INVITATION TO BID. The County of Waller proposes to purchase the following items on competitive bid: HYDRATED LIME

COMPETITIVE BIDDING NOTICE INVITATION TO BID The County of Waller proposes to purchase the following items on competitive bid: HYDRATED LIME Bids will be received by the Waller County Auditor, Alan Younts,

COMPETITIVE BIDDING NOTICE INVITATION TO BID The County of Waller proposes to purchase the following items on competitive bid: HYDRATED LIME Bids will be received by the Waller County Auditor, Alan Younts,

CHAUTAUQUA COUNTY LAND BANK CORPORATION

EXHIBIT H CHAUTAUQUA COUNTY LAND BANK CORPORATION LAND ACQUISITION AND DISPOSITION POLICIES AND PRIORITIES November 14, 2012 *This document is intended to provide guidance to the Chautauqua County Land

EXHIBIT H CHAUTAUQUA COUNTY LAND BANK CORPORATION LAND ACQUISITION AND DISPOSITION POLICIES AND PRIORITIES November 14, 2012 *This document is intended to provide guidance to the Chautauqua County Land

July 17, Technical Director File Reference No Re:

July 17, 2009 Technical Director File Reference No. 1680-100 Re: Financial Accounting Standards Board ( FASB ) and International Accounting Standards Board ( IASB ) Discussion Paper titled Leases: Preliminary

July 17, 2009 Technical Director File Reference No. 1680-100 Re: Financial Accounting Standards Board ( FASB ) and International Accounting Standards Board ( IASB ) Discussion Paper titled Leases: Preliminary

NEW YORK CITY ECONOMIC DEVELOPMENT CORPORATION POLICY REGARDING THE ACQUISITION AND DISPOSITION OF REAL PROPERTY

NEW YORK CITY ECONOMIC DEVELOPMENT CORPORATION POLICY REGARDING THE ACQUISITION AND DISPOSITION OF REAL PROPERTY I. Introduction In accordance with the requirements of Title 5-A of Article 9 and Section

NEW YORK CITY ECONOMIC DEVELOPMENT CORPORATION POLICY REGARDING THE ACQUISITION AND DISPOSITION OF REAL PROPERTY I. Introduction In accordance with the requirements of Title 5-A of Article 9 and Section

In December 2003 the Board issued a revised IAS 40 as part of its initial agenda of technical projects.

IAS 40 Investment Property In April 2001 the International Accounting Standards Board (the Board) adopted IAS 40 Investment Property, which had originally been issued by the International Accounting Standards

IAS 40 Investment Property In April 2001 the International Accounting Standards Board (the Board) adopted IAS 40 Investment Property, which had originally been issued by the International Accounting Standards

SUBPART B. REAL PROPERTY DISPOSITIONS

SUBPART B. REAL PROPERTY DISPOSITIONS Sec. 122.421. General; exemptions. Except as provided in this Section, the sale, lease or other transfer (referred to in this Subpart B as "sale") of all real property