For updates to publications, guides and forms, please refer to the Ministry of Finance, Tax Revenue Division, website at: www trd fin gov on ca For fu

|

|

|

- Linette Harmon

- 5 years ago

- Views:

Transcription

1 A GUIDE FOR REAL ESTATE PRACTITIONERS Land Transfer Tax and the Electronic Registration of Conveyances of Land in Ontario This publication is intended as a guide only and is not a substitute for the provisions of the Land Transfer Tax Act and Regulations November 2004

2 For updates to publications, guides and forms, please refer to the Ministry of Finance, Tax Revenue Division, website at: www trd fin gov on ca For further information about the Land Transfer Tax Act or this guide, please call the following numbers or write to the address noted below: Land Transfer Tax General Enquiry Line (Oshawa) :30am - 5:00pm (ET) Facsimile Tax Fax TAX-FAX Teletypewriter (TTY) Ministry of Finance Motor Fuels and Tobacco Tax Branch Land Transfer Tax Program P O Box King Street West Oshawa ON L1H 8H9 Ce aide-memoire est disponible en français Vous pouvez obtenir un exemplaire de ce guide en appelant le

3 Table of Contents Introduction 1 Land Transfer Tax 2 Deponents 3 Value of Consideration Greater Than $400,000 5 Consideration 6 Nominal 8 Explanations 9 Exemptions 11 Assessment Number 14 School Tax 14

4 Introduction This guide has been prepared as a resource for legal and real estate professionals involved in the electronic registration of conveyances of land in Ontario It is assumed that users of this handbook have a working knowledge of conveyancing and electronic registration For specific examples and other issues and common problems relating to land transfer tax, please see A Guide for Real Estate Practitioners with respect to Land Transfer Tax and the Registration of Conveyances of Land in Ontario which is available on our website This publication contains general information and is provided for convenience and guidance for the land transfer tax portion of Teraview only It is not a substitute for the provisions of the Land Transfer Tax Act (Act) or Regulations Should there be a discrepancy between this document, the Act and its regulations, the provisions of the Act and regulations apply For updates to publications, guides and forms, please refer to the Ministry of Finance, Tax Revenue Division, website at: www trd fin gov on ca For further information about the Act or this guide, taxpayers may call the following numbers or write to the address noted below: Land Transfer Tax General Enquiry Line (Oshawa): (8:30 AM to 5:00 PM) Facsimile: Tax Fax: TAX-FAX Teletypewriter (TTY): Ministry of Finance Motor Fuels and Tobacco Tax Branch Land Transfer Tax Program P O Box King Street West Oshawa ON L1H 8H9 Ce aide-memoire est disponible en français Vous pouvez obtenir un exemplaire de ce guide en appelant le

5 Land Transfer Tax The TAX option in the menu below launches the Land Transfer Tax functions enabling the user to select the tabs required to complete the Land Transfer Tax Statements When the TAX function is selected the Land Transfer Tax window opens and the following tabs are presented: Failure to complete a mandatory tab or field will generate an error message and prevent successful completion of the electronic registration In some cases supplementary evidence may be required for presentation to the registry office before certification of title can take place 2

6 Deponents Completion of this section is mandatory for all electronic conveyances Deponents are the individuals who make statements and declare in what capacity they are completing the statements If more than one deponent, and each deponent is not in the same capacity, more than one deponent tab must be completed To add a deponent, click on the + sign on the toolbar To delete a deponent, click on the - sign on the toolbar This section may be completed by an agent authorized in writing to act on behalf of a transferee(s), or by a solicitor A corporation cannot be a deponent If a corporation is a transferee, either paragraph (d) or (e) must be selected Where transferees are spouses or same-sex partners, either spouse or same-sex partner may complete paragraph (f) or (g) on behalf of both of them If any of paragraphs (d), (e), (f) or (g) are selected, a paragraph reference must be made and the individual or corporation being represented must be inserted by clicking the grey box to the right of the text box and selecting the appropriate party 3

from the drop down menu, as illustrated")

7 Deponents (cont d) The transferor may complete the statements where no tax is payable under the Land Transfer Tax Act and the transferor has sufficient information to enable the transferor to make the statements The name of the transferor may be inserted manually or by clicking the grey box to the right of the text box and selecting the transferor(s) from the drop down menu, as illustrated below No further statement should be selected on the Deponent tab, however statement 9120 or 9121 must be selected from the Explanations tab Note: The Teraview system does not allow for the transferor(s) to make statements if they consist of a combination of a person and a company 4

of the Act allows for an")

8 Value of Consideration > $400,000 This section must be completed ONLY where the consideration is greater than $400, A higher rate of tax applies to any consideration over $400, where the lands contain at least one and not more than two single family residences Statement 9031 MUST be made together with one of 9032, 9033 or 9038 Note: Subsection 2 1(2) of the Act allows for an apportionment of the consideration where the total consideration exceeds $400,000 and part of the land being conveyed has a use other than just residential (please note that "vacant" or "no use" is not considered to be another use) This results in a lower tax payable than would normally be calculated had the apportionment not been claimed If the value of consideration can be apportioned, statements 9031 and 9038 must be selected and completed When 9038 is selected you must enter the total consideration attributed to the single family residence only in "AMOUNT" and the use of the remainder of the lands must be described in "TEXT" The system will calculate the appropriate amount of land transfer tax based on the consideration entered on both the consideration tab and the amount entered in statement 9038 for the single family residence Note: When completing the "AMOUNT", use only numerical values and do not use any dollar signs, commas or decimal points 5

")

9 Consideration By definition, consideration includes the gross sale price paid or to be paid by or on behalf of the transferee, the value expressed in money of any liability assumed by or on behalf of the transferee, and the value of any benefit conferred, either directly or indirectly by the transferee, as part of the arrangement relating to the transfer The consideration must be allocated to (a) through (f) on the consideration screen 1 (c) Property transferred in exchange Statement 9021 Where the transfer is pursuant to an exchange of lands, the value of the property involved in the exchange must be entered in paragraph (c) After entering an amount in paragraph (c), go to the "Explanations Tab," select statement 9021, and enter a brief legal description of the lands transferred in exchange 1 (d) Fair Market Value of the land(s) Statements 9022 and 9011, 9012, 9013, 9014 or 9015 In certain circumstances, the Land Transfer Tax Act deems the value of consideration to be the fair market value of the land The fair market value of the land must be entered in paragraph (d) After entering an amount in paragraph (d), go to the "Explanations Tab," select statement 9022, and one of 9011, 9012, 9013, 9014 or

10 Consideration (cont d) The following are situations where the value of consideration is deemed to be equal to the fair market value of the land as of the date of registration: Statement 9011 Any transfer to a corporation where shares of the transferee corporation form all or part of the consideration Statement 9012 Any transfer from a corporation where the transferee is a shareholder of the transferor Statement 9013 Any transfer of a leasehold interest where the lease can exceed 50 years Statement 9014 In the case of a final order of foreclosure, the transferee is given the option of setting out as the consideration the lessor of (i) the amounts outstanding on the mortgage being foreclosed together with all prior mortgages and any subsequent mortgages held by the transferee OR (ii) the fair market value of the land as of the date of registration If the latter is used, then this value should be entered in paragraph (d) Statement 9015 Other This is a text field that allows the user to provide other explanations such as a transfer to a mortgagee from a mortgagor as a result of a default on the mortgage and the transfer is being made in lieu of a foreclosure 1 (f) Other valuable consideration subject to land transfer tax Statement 9023 Where an amount is entered in paragraph (f), you must go to the "Explanations Tab" and select statement 9023 and enter a description of the consideration Where a partial exemption is being claimed, the non-exempt portion of the consideration should be entered here and then you must go to the "Explanations Tab" and select statement 9023 and enter an explanation for the partial exemption 1 (g) VALUE of land, building, fixtures & goodwill subject to Land Transfer Tax Statement 9024 The Land Transfer Tax payable will be calculated on the total consideration automatically inserted in paragraph (g) The amount of tax payable will appear on the screen and will be adjusted according to any subsequent claims for exemption 1 (h) VALUE OF ALL CHATTELS items of tangible personal property e g furniture Retail Sales Tax will also be calculated on any consideration shown in paragraph (h) 1 (i) Other considerations for transaction not included in (g) or (h) Statement 9024 Where an amount is entered in paragraph (i), you must go to the "Explanations Tab" and select statement 9024 and enter a description of the other consideration Amounts entered in paragraph (i) must not be taxable under the Land Transfer Tax Act and may include amounts paid for chattels, but not subject to Retail Sales Tax 7

11 Nominal Statements may be selected here ONLY in situations where there is NO CONSIDERATION OF ANY KIND OR THE VALUE OF CONSIDERATION IS LESS THAN $200 for the conveyance This section must not be completed if an exemption is claimed Statement 9049 must be chosen together with one of 9050, 9051, 9052, 9053, 9054, 9055, 9056, 9057, 9058, 9066, 9060, 9061, 9063 or 9064 If 9064 is selected then "TEXT" must be entered If 9051, 9052 or 9053 are selected, title will not be certified until the supplementary trust affidavit is submitted to the Land Registry Office If 9058 or 9060 are selected, then either statement 9047 or 9048 must be made Note: If 9047 is chosen, then the amount of the encumbrance must be entered on line 1(b)(I) of the "Consideration Tab" section and all previously selected statements should be removed from the Nominal Tab The tax will be calculated accordingly, as there is no exemption available on a transfer that is a gift or a donation to a charity where there is an existing encumbrance on the land 8

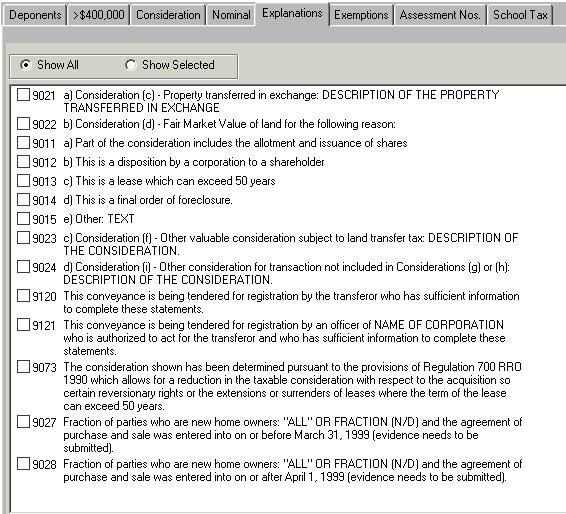

12 Explanations 9

13 Explanations (cont d) Consideration Explanation required In certain circumstances, explanations are required where a figure is entered in "c", "d", "f" and "i" on the "Consideration" tab Please see the "Consideration" section of this guide for details The "Explanation" tab should also be used when a partial exemption is being claimed Please see the "Consideration" section of this guide for details Land Transfer Tax Statements by the Transferor Statement 9120 Individual(s) This statement only applies where the transferor(s) is an individual(s) who has sufficient information to complete these statements Statement 9121 Corporation This statement only applies where the transferor is a corporation The person making the statements must be an officer of the corporation authorized to act for the transferor and who has sufficient information to complete these statements Note: The transferor can only make the statements if no tax is payable Regulation 700, RRO 1990 If a reduction in the consideration is being made pursuant to Regulation 700, RRO 1990, then statement 9073 must be completed Refund for a First Time Homebuyer of a Newly Constructed Home Select statement 9027 or 9028, depending on the date that the agreement of purchase and sale was entered into Double click on the "ALL" OR FRACTION (N/D) to open a new window Delete existing text and input ALL, fraction or percentage of parties who are First Time Homebuyers Ensure the land transfer tax has been reduced by the refund amount before registering Forward the Land Transfer Tax Refund Affidavit to the Land Registry Office 10

14 Exemptions This section is to be completed only where consideration is paid but an exemption is claimed and therefore no tax is payable Transfer of an Easement to Oil or Gas Pipeline Company Statement 9071 This conveyance qualifies for an exemption from tax under Regulation 695 RRO 1990 for certain transfers of easements to an oil or gas pipeline company Transfer between Spouse or Same-sex Partner Statement 9085 must be chosen together with one of 9086, 9087 or 9088 These statements only apply to inter-spousal transfers that qualify for exemption under regulation 696 RRO 1990 and should not be used if other statements have been selected from the Nominal tab 11

15 Exemptions (cont d) Notice of Purchaser s Lien for Default Statement 9074 This conveyance qualifies for an exemption from tax under Regulation 701 RRO 1990 for certain transfers involving a Notice of Purchaser's Lien for Default Taxation of Mineral Rights Statement 9075 This statement can be selected if the conveyance is of minerals rights only or a transfer of a surface rights option Any conveyance which contains both mineral rights and surface rights must be pre-approved by the Ministry prior to registration Such conveyances would include any lease which can exceed 50 years and contains surface rights as well as the exercise of a surface rights option Transfer to the Crown or Crown Agency Statement 9076 This conveyance qualifies for an exemption from tax under subsection 2(8) of the Land Transfer Tax Act Ministry of Finance Endorsement Statement 9089 & 9090 These statements can only be selected after the Ministry has signified its approval prior to registration The Evidence to be submitted includes the draft document bearing the Ministry s endorsement and must be presented to the Land Registry Office before title can be certified When selecting statement 9089, the payment receipt number issued by the Ministry will be entered in the NUMBER text box These statements should not be used as a means of avoiding a second payment of tax where tax was previously paid at the land registry office on registration of a notice, caution or other conveyance Tax Previously Paid - Statement Where a transfer document is being registered and tax was previously paid, the document type should be described as either a notice or caution and the instrument number attached to the notice or caution should be entered Note: the value of consideration must be entered on the consideration screen Acquisition and Reversion of a life lease interest - Statements 9124 and Where a document is being registered that conveys a life lease interest to a purchaser or the reversion of a life lease interest back to the owner of the life lease development, select whichever statement is applicable 12

16 Exemptions (cont d) Family Farm Exemption - Statement This exemption is available for transfers from individuals to other individuals who are members of the same family to continue farming on the lands Family Farm Exemption Statements 9078, 9079, 9080, 9081, 9082 and 9084 This conveyance qualifies for an exemption from tax under Regulation 697 RRO 1990 for the Family Farm Exemption Statements 9079, 9080 and 9081 require additional information to be entered in the applicable text boxes Note: The exemption for a conveyance to a family business corporation cannot be claimed electronically The proper documentation to claim this exemption must be submitted directly to the Ministry of Finance and the applicable endorsement obtained Hospital Restructuring Statement 9099 This conveyance qualifies for an exemption from tax under Regulation 676 RRO 1998 for certain hospital restructuring 13

17 Assessment Number The Assessment Roll Number is vital for purposes of accurately determining municipal property tax School Tax If no statement is selected on the School Tax tab, the system will default to English-Public 14

18 You can obtain the most current electronic copy of this publication by visiting our website at www trd fin gov on ca Ce document est disponible en français sous le titre : Un guide à l intention des spécialistes de l immobilière Droits de cession immobilière et enregistrement électronique des cessions de biens-fonds en Ontario Queen s Printer for Ontario, 2004 ISBN:

A GUIDE FOR REAL ESTATE PRACTITIONERS

A GUIDE FOR REAL ESTATE PRACTITIONERS Land Transfer Tax and the Registration of Conveyances of Land in Ontario This publication is intended as a guide only and is not a substitute for the provisions of

A GUIDE FOR REAL ESTATE PRACTITIONERS Land Transfer Tax and the Registration of Conveyances of Land in Ontario This publication is intended as a guide only and is not a substitute for the provisions of

etransfer Form User Guide The Property Registry s

s etransfer Form User Guide A service provider for the Province of Manitoba Most recent update: 2018-01-08 Version 2.03 Table of Contents Purpose... 4 General Guidelines for Completion... 4 Requirements...

s etransfer Form User Guide A service provider for the Province of Manitoba Most recent update: 2018-01-08 Version 2.03 Table of Contents Purpose... 4 General Guidelines for Completion... 4 Requirements...

Electronic Registration Procedures Guide. Ministry of Government and Consumer Services

Electronic Registration Procedures Guide Ministry of Government and Consumer Services Queen s Printer for Ontario, 2017 COPYRIGHT INFORMATION Copyright 2017 by Queen s Printer for Ontario. All rights reserved.

Electronic Registration Procedures Guide Ministry of Government and Consumer Services Queen s Printer for Ontario, 2017 COPYRIGHT INFORMATION Copyright 2017 by Queen s Printer for Ontario. All rights reserved.

TSLEIL-WAUTUTH NATION PROPERTY TRANSFER TAX EXEMPTION RETURN

TSLEIL-WAUTUTH NATION PROPERTY TRANSFER TAX EXEMPTION RETURN Use this form only if you are claiming an exemption from the tax under section 12 or 20 of the Tsleil-Waututh Nation Property Transfer Tax Law,

TSLEIL-WAUTUTH NATION PROPERTY TRANSFER TAX EXEMPTION RETURN Use this form only if you are claiming an exemption from the tax under section 12 or 20 of the Tsleil-Waututh Nation Property Transfer Tax Law,

PROPERTY TRANSFER TAX FORM #2 - EXEMPTION RETURN

DATE TK EMLÚPS TE SECWÉPEMC TAX PAID $ EXEMPTION CODE CLAIMED: PROPERTY TRANSFER TAX FORM #2 - EXEMPTION RETURN Use this form only if you are claiming an exemption from the tax under section 12 or 20 of

DATE TK EMLÚPS TE SECWÉPEMC TAX PAID $ EXEMPTION CODE CLAIMED: PROPERTY TRANSFER TAX FORM #2 - EXEMPTION RETURN Use this form only if you are claiming an exemption from the tax under section 12 or 20 of

To: Property Appraisers, Taxing Authorities and Interested Parties From: James McAdams Date: June 5, 2012 Bulletin: PTO 12-04

Property Tax Oversight Bulletin: PTO 12-04 To: Property Appraisers, Taxing Authorities and Interested Parties From: James McAdams Date: Bulletin: PTO 12-04 FLORIDA DEPARTMENT OF REVENUE PROPERTY TAX INFORMATIONAL

Property Tax Oversight Bulletin: PTO 12-04 To: Property Appraisers, Taxing Authorities and Interested Parties From: James McAdams Date: Bulletin: PTO 12-04 FLORIDA DEPARTMENT OF REVENUE PROPERTY TAX INFORMATIONAL

Withholding Requirements for Sales or Transfers of Real Property by Nonresidents

08/2008 Withholding Requirements for Sales or Transfers of Real Property by Nonresidents INDEX Introduction Act 2008-504.. Answers to Frequently Asked Questions.. List of Forms.. Forms.. Act 2008-504 INTRODUCTION

08/2008 Withholding Requirements for Sales or Transfers of Real Property by Nonresidents INDEX Introduction Act 2008-504.. Answers to Frequently Asked Questions.. List of Forms.. Forms.. Act 2008-504 INTRODUCTION

@ Ontario. Capacity Changes. Registry Act. InterestlEstate EstatesIQualifier TeraviewB 5.3

@ Ontario Ministry of Government Services Registration Division Title and Survey Services Office 1 BULLETIN NO. 2005-05 Land Titles Act Registry Act DATE: JULY 13,2005 InterestlEstate EstatesIQualifier

@ Ontario Ministry of Government Services Registration Division Title and Survey Services Office 1 BULLETIN NO. 2005-05 Land Titles Act Registry Act DATE: JULY 13,2005 InterestlEstate EstatesIQualifier

REAL PROPERTY TRANSFER TAX ACT

c t REAL PROPERTY TRANSFER TAX ACT PLEASE NOTE This document, prepared by the Legislative Counsel Office, is an office consolidation of this Act, current to October 1, 2016. It is intended for information

c t REAL PROPERTY TRANSFER TAX ACT PLEASE NOTE This document, prepared by the Legislative Counsel Office, is an office consolidation of this Act, current to October 1, 2016. It is intended for information

THE CORPORATION OF THE CITY OF BRAMPTON BY-LAW. To confirm the proceedings of Council at its Special Meeting held on June 7,2006

THE CORPORATION OF THE CITY OF BY-LAW Number_..:.-J '.:...-9_-_2_~_' To confirm the proceedings of Council at its Special Meeting held on June 7,2006 The Council of the Corporation of the City of Brampton

THE CORPORATION OF THE CITY OF BY-LAW Number_..:.-J '.:...-9_-_2_~_' To confirm the proceedings of Council at its Special Meeting held on June 7,2006 The Council of the Corporation of the City of Brampton

CONFIRMATION OF REPRESENTATION In representing the parties in the negotiations for the purchase and sale of the Property:

CONDOMINIUM UNIT FORM OF OFFER TO PURCHASE This form of offer is prescribed under The Real Estate Brokers Act for use by brokers in the purchase of a completed condominium unit in a registered Condominium

CONDOMINIUM UNIT FORM OF OFFER TO PURCHASE This form of offer is prescribed under The Real Estate Brokers Act for use by brokers in the purchase of a completed condominium unit in a registered Condominium

S 2613 S T A T E O F R H O D E I S L A N D

LC00 01 -- S 1 S T A T E O F R H O D E I S L A N D IN GENERAL ASSEMBLY JANUARY SESSION, A.D. 01 A N A C T RELATING TO TAXATION -- REAL ESTATE CONVEYANCE Introduced By: Senator Gayle L. Goldin Date Introduced:

LC00 01 -- S 1 S T A T E O F R H O D E I S L A N D IN GENERAL ASSEMBLY JANUARY SESSION, A.D. 01 A N A C T RELATING TO TAXATION -- REAL ESTATE CONVEYANCE Introduced By: Senator Gayle L. Goldin Date Introduced:

Transfer duty on efiling

Transfer duty on efiling A QUICK GUIDE A CONTENTS 1. Overview...1 2. Transfer duty declarations...1 3. Forms and documents required...2 4. Completing the transfer duty process on the efiling website...3

Transfer duty on efiling A QUICK GUIDE A CONTENTS 1. Overview...1 2. Transfer duty declarations...1 3. Forms and documents required...2 4. Completing the transfer duty process on the efiling website...3

PART 1 Withholding Tax on the Sale of Real Property by Nonresidents

280-RICR-20-10-1 TITLE 280 DEPARTMENT OF REVENUE CHAPTER 20 DIVISION OF TAXATION SUBCHAPTER 10 PERSONAL INCOME TAX PART 1 Withholding Tax on the Sale of Real Property by Nonresidents 1.1 Purpose The purpose

280-RICR-20-10-1 TITLE 280 DEPARTMENT OF REVENUE CHAPTER 20 DIVISION OF TAXATION SUBCHAPTER 10 PERSONAL INCOME TAX PART 1 Withholding Tax on the Sale of Real Property by Nonresidents 1.1 Purpose The purpose

ELECTRONIC CONVEYANCING IN ESTATE SITUATIONS. by Bonnie Yagar, Pallett Valo LLP

ELECTRONIC CONVEYANCING IN ESTATE SITUATIONS by Bonnie Yagar, Pallett Valo LLP Although there are some differences in the way conveyancing is done in the electronic format, and still some bugs to be worked

ELECTRONIC CONVEYANCING IN ESTATE SITUATIONS by Bonnie Yagar, Pallett Valo LLP Although there are some differences in the way conveyancing is done in the electronic format, and still some bugs to be worked

address address branch address Fee Simple Absolute See Schedule G attached

Form 15.1 Collateral Mortgage Land Titles Act, S.N.B. 1981, c.l-1.1, s.25 Standard Forms of Conveyances Act, S.N.B. 1980, c.s-12.2, s.2 Parcel Identifier: Mortgagor: name address name address Spouse of:

Form 15.1 Collateral Mortgage Land Titles Act, S.N.B. 1981, c.l-1.1, s.25 Standard Forms of Conveyances Act, S.N.B. 1980, c.s-12.2, s.2 Parcel Identifier: Mortgagor: name address name address Spouse of:

Treasury Regulations 1.42

Treasury Regulations 1.42 1.42-1 [Reserved] 1.42-1T Limitation on low-income housing credit allowed with respect to qualified lowincome buildings receiving housing credit allocations from a State or local

Treasury Regulations 1.42 1.42-1 [Reserved] 1.42-1T Limitation on low-income housing credit allowed with respect to qualified lowincome buildings receiving housing credit allocations from a State or local

Schedule A. Citation 1 These regulations may be cited as the Land Registration Administration Regulations. Definitions 2 (1) In these regulations,

In these regulations,") Schedule A Regulations Respecting Administration of the Land Registration Act made by the Minister of Service Nova Scotia and Municipal Relations under Section 94 of Chapter 6 of the Acts of 2001, the

Schedule A Regulations Respecting Administration of the Land Registration Act made by the Minister of Service Nova Scotia and Municipal Relations under Section 94 of Chapter 6 of the Acts of 2001, the

The Bank of Nova Scotia Collateral Mortgage NOTES TO SOLICITORS

The Bank of Nova Scotia Collateral Mortgage (Land Titles Act and Registry Act) Standard Charge Terms No. 200012 NOTES TO SOLICITORS Notes for Solicitors not using e-reg 1 Discard Electronic Document Agreement

The Bank of Nova Scotia Collateral Mortgage (Land Titles Act and Registry Act) Standard Charge Terms No. 200012 NOTES TO SOLICITORS Notes for Solicitors not using e-reg 1 Discard Electronic Document Agreement

MUNICIPAL REPORTING SYSTEM. SOE Assessment (SOE-A) User Guide June 2018

User Guide June 2018") MUNICIPAL REPORTING SYSTEM SOE Assessment (SOE-A) User Guide June 2018 Crown copyright, Province of Nova Scotia, 2018 Municipal Reporting System SOE Assessment (SOE-A) User Guide Municipal Affairs June

MUNICIPAL REPORTING SYSTEM SOE Assessment (SOE-A) User Guide June 2018 Crown copyright, Province of Nova Scotia, 2018 Municipal Reporting System SOE Assessment (SOE-A) User Guide Municipal Affairs June

First Time Home Buyers Program Property Transfer Tax

Bulletin PTT 004 REVISED: FEBRUARY 2003 UPDATED: FEBRUARY 2005 First Time Home Buyers Program Property Transfer Tax Effective February 16, 2005 First Time Home Buyers Program threshold increases The First

Bulletin PTT 004 REVISED: FEBRUARY 2003 UPDATED: FEBRUARY 2005 First Time Home Buyers Program Property Transfer Tax Effective February 16, 2005 First Time Home Buyers Program threshold increases The First

RATE AND METHOD OF APPORTIONMENT FOR CASITAS MUNICIPAL WATER DISTRICT COMMUNITY FACILITIES DISTRICT NO (OJAI)

") RATE AND METHOD OF APPORTIONMENT FOR CASITAS MUNICIPAL WATER DISTRICT COMMUNITY FACILITIES DISTRICT NO. 2013-1 (OJAI) A Special Tax shall be levied on all Assessor s Parcels of Taxable Property in Casitas

RATE AND METHOD OF APPORTIONMENT FOR CASITAS MUNICIPAL WATER DISTRICT COMMUNITY FACILITIES DISTRICT NO. 2013-1 (OJAI) A Special Tax shall be levied on all Assessor s Parcels of Taxable Property in Casitas

2010 No. 11 LAND REGISTRATION. Land Registry (Fees) Order (Northern Ireland) 2010

Order (Northern Ireland) 2010") STATUTORY RULES OF NORTHERN IRELAND 2010 No. 11 LAND REGISTRATION Land Registry (Fees) Order (Northern Ireland) 2010 Made - - - - 21st January 2010 Affirmed by resolution of the Assembly on 1st March 2010

STATUTORY RULES OF NORTHERN IRELAND 2010 No. 11 LAND REGISTRATION Land Registry (Fees) Order (Northern Ireland) 2010 Made - - - - 21st January 2010 Affirmed by resolution of the Assembly on 1st March 2010

Deed Recording Fee SOUTH CAROLINA DEPARTMENT OF REVENUE OFFICE OF GENERAL COUNSEL / POLICY SECTION

Deed Recording Fee SOUTH CAROLINA DEPARTMENT OF REVENUE OFFICE OF GENERAL COUNSEL / POLICY SECTION JUNE 2015 DISCLAIMER This publication is written in general terms for widest possible use and may not

Deed Recording Fee SOUTH CAROLINA DEPARTMENT OF REVENUE OFFICE OF GENERAL COUNSEL / POLICY SECTION JUNE 2015 DISCLAIMER This publication is written in general terms for widest possible use and may not

COMPLETION INSTRUCTIONS FOR ELECTRONIC FORMS

COMPLETION INSTRUCTIONS FOR ELECTRONIC FORMS Craig D. Johnston, Director of Land Titles November 20, 2017 Version 1.2 Copyright 2016, Land Title and Survey Authority of BC All rights reserved 1 Contents

COMPLETION INSTRUCTIONS FOR ELECTRONIC FORMS Craig D. Johnston, Director of Land Titles November 20, 2017 Version 1.2 Copyright 2016, Land Title and Survey Authority of BC All rights reserved 1 Contents

NC General Statutes - Chapter 47C Article 4 1

Article 4. Protection of Purchasers. 47C-4-101. Applicability; waiver. (a) This Article applies to all units subject to this chapter, except as provided in subsection (b) or as modified or waived by agreement

Article 4. Protection of Purchasers. 47C-4-101. Applicability; waiver. (a) This Article applies to all units subject to this chapter, except as provided in subsection (b) or as modified or waived by agreement

A BILL TO BE ENTITLED AN ACT

12 LC 34 3484S/AP House Bill 386 (AS PASSED HOUSE AND SENATE) By: Representatives Channell of the 116th, O`Neal of the 146th, Jones of the 46th, and Peake of the 137th A BILL TO BE ENTITLED AN ACT To amend

12 LC 34 3484S/AP House Bill 386 (AS PASSED HOUSE AND SENATE) By: Representatives Channell of the 116th, O`Neal of the 146th, Jones of the 46th, and Peake of the 137th A BILL TO BE ENTITLED AN ACT To amend

Bulletin No September 1, 2011

Ministry of Government Services Service Policy and Regulatory Services Branch Bulletin No. 2011-04 Boundaries Act, Condominium Act, 1998, Land Registration Reform Act, Land Titles Act, Registry Act Date:

Ministry of Government Services Service Policy and Regulatory Services Branch Bulletin No. 2011-04 Boundaries Act, Condominium Act, 1998, Land Registration Reform Act, Land Titles Act, Registry Act Date:

The Homesteads Act, 1989

1 HOMESTEADS, 1989 c. H-5.1 The Homesteads Act, 1989 being Chapter H-5.1 of the Statutes of Saskatchewan, 1989-90 (effective December 1, 1989) as amended by the Statutes of Saskatchewan, 1992, c.27; 1993,

1 HOMESTEADS, 1989 c. H-5.1 The Homesteads Act, 1989 being Chapter H-5.1 of the Statutes of Saskatchewan, 1989-90 (effective December 1, 1989) as amended by the Statutes of Saskatchewan, 1992, c.27; 1993,

*Charter references: Power of city to impose and collect tax on transfer of real property, subpart A,

ARTICLE III. REALTY TRANSFER TAX* Page 1 of8 ARTICLE III. REAL TV TRANSFER TAX* *Charter references: Power of city to impose and collect tax on transfer of real property, subpart A, 3. Sec. 102-71. Definitions.

ARTICLE III. REALTY TRANSFER TAX* Page 1 of8 ARTICLE III. REAL TV TRANSFER TAX* *Charter references: Power of city to impose and collect tax on transfer of real property, subpart A, 3. Sec. 102-71. Definitions.

Community Land Trust Ground Lease Rider

Community Land Trust Ground Lease Rider [For use with CLT ground leases substantially based on either the Institute for Community Economics or the National Community Land Trust Network model ground lease

Community Land Trust Ground Lease Rider [For use with CLT ground leases substantially based on either the Institute for Community Economics or the National Community Land Trust Network model ground lease

THROUGH ITS AGENT. 2. Policy (or Policies) to be issued: Policy Amount

to be issued: Policy Amount") Commitment for Title Insurance BY Schedule A First American Title Insurance Company THROUGH ITS AGENT Best Homes Title Agency, LLC 1. Commitment Date: 09/23/2016 at 8:00 AM Commitment No.: GRC-94850 2.

Commitment for Title Insurance BY Schedule A First American Title Insurance Company THROUGH ITS AGENT Best Homes Title Agency, LLC 1. Commitment Date: 09/23/2016 at 8:00 AM Commitment No.: GRC-94850 2.

(a)-(g) [Reserved]. For further guidance, see T(a) through (g).

![(a)-(g) [Reserved]. For further guidance, see T(a) through (g).](/thumbs/93/111110189.jpg "(a)-(g) [Reserved]. For further guidance, see T(a) through (g).") 1.42-1 Limitation on low-income housing credit allowed with respect to qualified lowincome buildings receiving housing credit allocations from a State or local housing credit agency. (a)-(g) [Reserved].

1.42-1 Limitation on low-income housing credit allowed with respect to qualified lowincome buildings receiving housing credit allocations from a State or local housing credit agency. (a)-(g) [Reserved].

SECOND AMENDED RATE AND METHOD OF APPORTIONMENT OF SPECIAL TAXES FOR TUSTIN UNIFIED SCHOOL DISTRICT COMMUNITY FACILITIES DISTRICT NO

SECOND AMENDED RATE AND METHOD OF APPORTIONMENT OF SPECIAL TAXES FOR TUSTIN UNIFIED SCHOOL DISTRICT COMMUNITY FACILITIES DISTRICT NO. 07-1 (ORCHARD HILLS) A Special Tax shall be levied and collected within

SECOND AMENDED RATE AND METHOD OF APPORTIONMENT OF SPECIAL TAXES FOR TUSTIN UNIFIED SCHOOL DISTRICT COMMUNITY FACILITIES DISTRICT NO. 07-1 (ORCHARD HILLS) A Special Tax shall be levied and collected within

C O N F I D E N T I A L

00320540000001 Bexar Appraisal District COMMON ACCT.# PID: RETURN COMPLETED RENDITION BY 1 APRIL 2018 NAME OF BUSINESS (DBA) AND LOCATION OF PROPERTY: IF OUT OF BUSINESS GIVE DATE (OPTIONAL) C O N F I

00320540000001 Bexar Appraisal District COMMON ACCT.# PID: RETURN COMPLETED RENDITION BY 1 APRIL 2018 NAME OF BUSINESS (DBA) AND LOCATION OF PROPERTY: IF OUT OF BUSINESS GIVE DATE (OPTIONAL) C O N F I

DEED OF TRUST PUBLIC TRUSTEE

DEED OF TRUST PUBLIC TRUSTEE THIS DEED OF TRUST is a conveyance in trust of real property to the Public Trustee of the county in Colorado in which the Property described below is located. It has been signed

DEED OF TRUST PUBLIC TRUSTEE THIS DEED OF TRUST is a conveyance in trust of real property to the Public Trustee of the county in Colorado in which the Property described below is located. It has been signed

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 2015 S 1 SENATE BILL 869. Short Title: Market-Based Sourcing. (Public)

") GENERAL ASSEMBLY OF NORTH CAROLINA SESSION S 1 SENATE BILL Short Title: Market-Based Sourcing. (Public) Sponsors: Referred to: Senators Rucho, Rabon (Primary Sponsors); Curtis, Ford, and Hise. Finance

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION S 1 SENATE BILL Short Title: Market-Based Sourcing. (Public) Sponsors: Referred to: Senators Rucho, Rabon (Primary Sponsors); Curtis, Ford, and Hise. Finance

AGREEMENT FOR PAYMENT IN LIEU OF TAXES FOR REAL PROPERTY AND PERSONAL PROPERTY. between. and THE TOWN OF DOUGLAS

AGREEMENT FOR PAYMENT IN LIEU OF TAXES FOR REAL PROPERTY AND PERSONAL PROPERTY between and THE TOWN OF DOUGLAS dated as of November, 2011 AGREEMENT FOR PAYMENT IN LIEU OF TAXES FOR REAL PROPERTY AND PERSONAL

AGREEMENT FOR PAYMENT IN LIEU OF TAXES FOR REAL PROPERTY AND PERSONAL PROPERTY between and THE TOWN OF DOUGLAS dated as of November, 2011 AGREEMENT FOR PAYMENT IN LIEU OF TAXES FOR REAL PROPERTY AND PERSONAL

12B Taxable Documents. (1) Signature Required: Tax is on Promise to Pay and each renewal thereof and to be note or obligation it must be signed

Signature Required: Tax is on Promise to Pay and each renewal thereof and to be note or obligation it must be signed") 12B-4.053 Taxable Documents. (1) Signature Required: Tax is on Promise to Pay and each renewal thereof and to be note or obligation it must be signed by the maker or obligor to be taxable. (Lee v. Quincy

12B-4.053 Taxable Documents. (1) Signature Required: Tax is on Promise to Pay and each renewal thereof and to be note or obligation it must be signed by the maker or obligor to be taxable. (Lee v. Quincy

Mortgage Broker e-info Newsletter Issue Issue 4 7

Issue Issue 4 7 The provides updates on the implementation of Ontario s new Mortgage Brokerages, Lenders and Administrators Act, 2006, regulations, and new education requirements for mortgage brokers and

Issue Issue 4 7 The provides updates on the implementation of Ontario s new Mortgage Brokerages, Lenders and Administrators Act, 2006, regulations, and new education requirements for mortgage brokers and

IC Application of chapter Sec. 1. This chapter applies to each unit having a commission. As added by P.L (ss), SEC.18.

, SEC.18.") IC 36-7-14.5 Chapter 14.5. Redevelopment Authority IC 36-7-14.5-1 Application of chapter Sec. 1. This chapter applies to each unit having a commission. As added by P.L.380-1987(ss), SEC.18. IC 36-7-14.5-2

IC 36-7-14.5 Chapter 14.5. Redevelopment Authority IC 36-7-14.5-1 Application of chapter Sec. 1. This chapter applies to each unit having a commission. As added by P.L.380-1987(ss), SEC.18. IC 36-7-14.5-2

Duties Amendment (Land Rich) Act 2004 No 96

Act 2004 No 96") New South Wales Duties Amendment (Land Rich) Act 2004 No 96 Contents Page 1 Name of Act 2 2 Commencement 2 3 Amendment of Duties Act 1997 No 123 2 Schedule 1 Land rich amendments 3 Schedule 2 Other amendments

New South Wales Duties Amendment (Land Rich) Act 2004 No 96 Contents Page 1 Name of Act 2 2 Commencement 2 3 Amendment of Duties Act 1997 No 123 2 Schedule 1 Land rich amendments 3 Schedule 2 Other amendments

Registered Land CAP

Registered Land CAP. 8.01 71 [Subsidiary] REGISTERED LAND RULES (S.R.O.s 35 of 1978, 70 of 1980 and 9 of 1981 Commencement [13 December 1978] Short title 1. These Rules may be cited as the Registered Land

Registered Land CAP. 8.01 71 [Subsidiary] REGISTERED LAND RULES (S.R.O.s 35 of 1978, 70 of 1980 and 9 of 1981 Commencement [13 December 1978] Short title 1. These Rules may be cited as the Registered Land

THE CORPORATION OF THE TOWNSHIP OF LEEDS AND THE THOUSAND ISLANDS BY-LAW

THE CORPORATION OF THE TOWNSHIP OF LEEDS AND THE THOUSAND ISLANDS BY-LAW 16-068 BEING A BY-LAW TO AUTHORIZE THE PURCHASE OF PART OF LOT 18, CONCESSION 2, PART 1 28R14660, TOWNSHIP OF LEEDS AND THE THOUSAND

THE CORPORATION OF THE TOWNSHIP OF LEEDS AND THE THOUSAND ISLANDS BY-LAW 16-068 BEING A BY-LAW TO AUTHORIZE THE PURCHASE OF PART OF LOT 18, CONCESSION 2, PART 1 28R14660, TOWNSHIP OF LEEDS AND THE THOUSAND

Contract of Sale of Real Estate

Contract of Sale of Real Estate Vendor: Anthony Paul Smith and Lauren Ashlea Hollioake Property: 117 Canadian Lakes Boulevard, Canadian CONTRACT OF SALE OF REAL ESTATE Part 1 of the standard form of contract

Contract of Sale of Real Estate Vendor: Anthony Paul Smith and Lauren Ashlea Hollioake Property: 117 Canadian Lakes Boulevard, Canadian CONTRACT OF SALE OF REAL ESTATE Part 1 of the standard form of contract

Instructions for Form NYC-RPT Real Property Transfer Tax Return

Instructions for Form NYC-RPT Page 1 Instructions for Form NYC-RPT Real Property Transfer Tax Return IMPORTANT 1. Always submit pages 1-4 of the return. Attach Schedules A through H, Schedule M and Schedule

Instructions for Form NYC-RPT Page 1 Instructions for Form NYC-RPT Real Property Transfer Tax Return IMPORTANT 1. Always submit pages 1-4 of the return. Attach Schedules A through H, Schedule M and Schedule

located in the 14. City/Township of CLEARWATER, County of WRIGHT, 15. State of Minnesota, PID # (s) 16.

16.") 2. BUYER (S): 3. 4. Buyer's earnest money in the amount of COMMERCIAL PURCHASE AGREEMENT This form approved by the Minnesota Association of REALTORS and the Minnesota Commercial Association of REALTORS,

2. BUYER (S): 3. 4. Buyer's earnest money in the amount of COMMERCIAL PURCHASE AGREEMENT This form approved by the Minnesota Association of REALTORS and the Minnesota Commercial Association of REALTORS,

Sample of the Draft PTT form V26

Property Transfer Tax Inquiries Victoria: 250 387-0604 Vancouver: 604 660-2421 Toll-free: 1 888 355-2700 gov.bc.ca/propertytransfertax PROPERTY TRANSFER TA RETURN Freedom of Information and Protection

Property Transfer Tax Inquiries Victoria: 250 387-0604 Vancouver: 604 660-2421 Toll-free: 1 888 355-2700 gov.bc.ca/propertytransfertax PROPERTY TRANSFER TA RETURN Freedom of Information and Protection

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 2015 HOUSE BILL 174 RATIFIED BILL

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 2015 HOUSE BILL 174 RATIFIED BILL AN ACT TO AMEND AND ENHANCE CERTAIN NOTICE REQUIREMENTS AND PROTECTIONS FOR TENANTS OF REAL PROPERTIES IN FORECLOSURE AND TO

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 2015 HOUSE BILL 174 RATIFIED BILL AN ACT TO AMEND AND ENHANCE CERTAIN NOTICE REQUIREMENTS AND PROTECTIONS FOR TENANTS OF REAL PROPERTIES IN FORECLOSURE AND TO

ST CHRISTOPHER AND NEVIS CHAPTER CONDOMINIUM ACT

Laws of Saint Christopher Condominium Act Cap 10.03 1 ST CHRISTOPHER AND NEVIS CHAPTER 10.03 CONDOMINIUM ACT and Subsidiary Legislation Revised Edition showing the law as at 31 December 2009 This is a

Laws of Saint Christopher Condominium Act Cap 10.03 1 ST CHRISTOPHER AND NEVIS CHAPTER 10.03 CONDOMINIUM ACT and Subsidiary Legislation Revised Edition showing the law as at 31 December 2009 This is a

Agreement of Purchase and Sale

Agreement of Purchase and Sale Form 100 for use in the Province of Ontario This Agreement of Purchase and Sale dated this... day of... 20... BUYER,..., agrees to purchase from (Full legal names of all

Agreement of Purchase and Sale Form 100 for use in the Province of Ontario This Agreement of Purchase and Sale dated this... day of... 20... BUYER,..., agrees to purchase from (Full legal names of all

Agreement of Purchase and Sale

Agreement of Purchase and Sale Co-operative Building Resale Agreement Form 102 for use in the Province of Ontario This Agreement of Purchase and Sale dated this... day of... 20... BUYER,..., agrees to

Agreement of Purchase and Sale Co-operative Building Resale Agreement Form 102 for use in the Province of Ontario This Agreement of Purchase and Sale dated this... day of... 20... BUYER,..., agrees to

Understanding Mississippi Property Taxes

Understanding Mississippi Property Taxes Property tax revenues are a vital component of the budgets of Mississippi s local governments. Property tax revenues allow these governments to provide important

Understanding Mississippi Property Taxes Property tax revenues are a vital component of the budgets of Mississippi s local governments. Property tax revenues allow these governments to provide important

The Homesteads Forms Regulations

1 The Homesteads Forms Regulations being Chapter H-5.1 Reg 1 (effective December 1, 1989) as amended by Saskatchewan Regulations 81/2001. NOTE: This consolidation is not official. Amendments have been

1 The Homesteads Forms Regulations being Chapter H-5.1 Reg 1 (effective December 1, 1989) as amended by Saskatchewan Regulations 81/2001. NOTE: This consolidation is not official. Amendments have been

Instructions for Form NYC-RPT Real Property Transfer Tax Return

Instructions for Form NYC-RPT Page 1 Instructions for Form NYC-RPT Real Property Transfer Tax Return IMPORTANT 1. Always submit pages 1-4 of the return. Attach Schedules A through H, Schedule M and Schedule

Instructions for Form NYC-RPT Page 1 Instructions for Form NYC-RPT Real Property Transfer Tax Return IMPORTANT 1. Always submit pages 1-4 of the return. Attach Schedules A through H, Schedule M and Schedule

(2) Qualified tangible personal property purchased for use by a qualified person to be used primarily in research and development.

Qualified tangible personal property purchased for use by a qualified person to be used primarily in research and development.") Final Text of California Code of Regulations, Title 18, Section 1525.4, Manufacturing and Research & Development Equipment (A new regulation to be added to the California Code of Regulations) 1525.4. Manufacturing

Final Text of California Code of Regulations, Title 18, Section 1525.4, Manufacturing and Research & Development Equipment (A new regulation to be added to the California Code of Regulations) 1525.4. Manufacturing

see schedule 3. ENCUMBRANCES, LIENS AND INTERESTS The within document is subject to instrument number(s)

") MORTGAGE Form 6.1 Mortgage Encumbrance Mortgage of Mortgage/Encumbrance 1. MORTGAGOR(S)/GRANTOR(S) OF ENCUMBRANCE (Encumbrancee(s)) 2. LAND DESCRIPTION TITLE NO.(S) MORTGAGE/ENCUMBRANCE NO.(S) 3. ENCUMBRANCES,

MORTGAGE Form 6.1 Mortgage Encumbrance Mortgage of Mortgage/Encumbrance 1. MORTGAGOR(S)/GRANTOR(S) OF ENCUMBRANCE (Encumbrancee(s)) 2. LAND DESCRIPTION TITLE NO.(S) MORTGAGE/ENCUMBRANCE NO.(S) 3. ENCUMBRANCES,

Reg. Section 15a.453-1(b)(3)(i) Installment method reporting for sales of real property and casual sales of personal property

(3)(i) Installment method reporting for sales of real property and casual sales of personal property") CLICK HERE to return to the home page Reg. Section 15a.453-1(b)(3)(i) Installment method reporting for sales of real property and casual sales of personal property (a) In general. Unless the taxpayer otherwise

CLICK HERE to return to the home page Reg. Section 15a.453-1(b)(3)(i) Installment method reporting for sales of real property and casual sales of personal property (a) In general. Unless the taxpayer otherwise

Transfer of Business

This document should be read in conjunction with section 20(2)(c) of the Vat Consolidation Act 2010. (VATCA 2010) Document last reviewed December 2017 Table of Contents Introduction...1 2 What are transfers

This document should be read in conjunction with section 20(2)(c) of the Vat Consolidation Act 2010. (VATCA 2010) Document last reviewed December 2017 Table of Contents Introduction...1 2 What are transfers

OLD REPUBLIC NATIONAL TITLE INSURANCE COMPANY

Schedule A 1. Effective Date: August 31, 2012 at 08:00 AM File Number: HU12081663CO The policy or policies to be issued are: 2. Amount (a) Owner's Policy: ALTA Own. Policy (06/17/06) Proposed Insured:

Schedule A 1. Effective Date: August 31, 2012 at 08:00 AM File Number: HU12081663CO The policy or policies to be issued are: 2. Amount (a) Owner's Policy: ALTA Own. Policy (06/17/06) Proposed Insured:

All information and reports concerning properties can be found by clicking on the Properties tab in your black toolbar along the top of your page.

support@payprop.co.za 087 820 7368 TRAINING MANUAL: PROPERTIES All information and reports concerning properties can be found by clicking on the Properties tab in your black toolbar along the top of your

support@payprop.co.za 087 820 7368 TRAINING MANUAL: PROPERTIES All information and reports concerning properties can be found by clicking on the Properties tab in your black toolbar along the top of your

Credit Union Leasing of America Residual Web Users Guide Consumer Lease Program. January 2018

Credit Union Leasing of America Residual Web Consumer Lease Program January 2018 i CULA Residual Web - Consumer Lease Program Table of Contents Table of Contents Accessing CULA Residual Web... 3 Creating

Credit Union Leasing of America Residual Web Consumer Lease Program January 2018 i CULA Residual Web - Consumer Lease Program Table of Contents Table of Contents Accessing CULA Residual Web... 3 Creating

Province of Alberta LAND TITLES ACT FORMS REGULATION. Alberta Regulation 480/1981. With amendments up to and including Alberta Regulation 170/2012

Province of Alberta LAND TITLES ACT FORMS REGULATION Alberta Regulation 480/1981 With amendments up to and including Alberta Regulation 170/2012 Office Consolidation Published by Alberta Queen s Printer

Province of Alberta LAND TITLES ACT FORMS REGULATION Alberta Regulation 480/1981 With amendments up to and including Alberta Regulation 170/2012 Office Consolidation Published by Alberta Queen s Printer

The ecrv Submit application opens with the following important warning message on privacy:

Submit Form Tabs Buyers and Sellers Property Sales Agreement Supplementary Submitter The ecrv form is a single Web-page form with entry fields, choices and selections in multiple tabs for submitting a

Submit Form Tabs Buyers and Sellers Property Sales Agreement Supplementary Submitter The ecrv form is a single Web-page form with entry fields, choices and selections in multiple tabs for submitting a

Chicago Title Insurance Company

Chicago Title Insurance Company COMMITMENT FOR TITLE INSURANCE Issued by Chicago Title Insurance Company Chicago Title Insurance Company, a Nebraska Corporation ('Company'), for a valuable consideration,

Chicago Title Insurance Company COMMITMENT FOR TITLE INSURANCE Issued by Chicago Title Insurance Company Chicago Title Insurance Company, a Nebraska Corporation ('Company'), for a valuable consideration,

Guide to Farming Taxation Measures in Finance Act Income Averaging (section 657 Taxes Consolidation Act 1997)

") Guide to Farming Taxation Measures in Finance Act 2014 Note: This Guide reflects the legislation in place as at 1 January 2015 only. For further information on the up to date position please refer to the

Guide to Farming Taxation Measures in Finance Act 2014 Note: This Guide reflects the legislation in place as at 1 January 2015 only. For further information on the up to date position please refer to the

Ministry of Environment and Climate Change Strategy and Ministry of Forests, Lands, Natural Resource Operations and Rural Development

Ministry of Environment and Climate Change Strategy and Ministry of Forests, Lands, Natural Resource Operations and Rural Development NAME OF POLICY: APPLICATION: ISSUANCE: IMPLEMENTATION: LEGISLATIVE

Ministry of Environment and Climate Change Strategy and Ministry of Forests, Lands, Natural Resource Operations and Rural Development NAME OF POLICY: APPLICATION: ISSUANCE: IMPLEMENTATION: LEGISLATIVE

AN ACT RELATING TO PROPERTY; LIMITING THE ISSUANCE OF GENERAL OBLIGATION BONDS FOR INFRASTRUCTURE IMPROVEMENTS IN PUBLIC

AN ACT RELATING TO PROPERTY; LIMITING THE ISSUANCE OF GENERAL OBLIGATION BONDS FOR INFRASTRUCTURE IMPROVEMENTS IN PUBLIC IMPROVEMENT DISTRICTS; REQUIRING AN APPLICATION FOR FORMATION OF A PUBLIC IMPROVEMENT

AN ACT RELATING TO PROPERTY; LIMITING THE ISSUANCE OF GENERAL OBLIGATION BONDS FOR INFRASTRUCTURE IMPROVEMENTS IN PUBLIC IMPROVEMENT DISTRICTS; REQUIRING AN APPLICATION FOR FORMATION OF A PUBLIC IMPROVEMENT

COMMITMENT FOR TITLE INSURANCE Issued by

ALTA Commitment (6/17/06) ALTA Commitment Form COMMITMENT FOR TITLE INSURANCE Issued by STEWART TITLE GUARANTY COMPANY, a Texas Corporation ( Company ), for a valuable consideration, commits to issue its

ALTA Commitment (6/17/06) ALTA Commitment Form COMMITMENT FOR TITLE INSURANCE Issued by STEWART TITLE GUARANTY COMPANY, a Texas Corporation ( Company ), for a valuable consideration, commits to issue its

THROUGH ITS AGENT. 2. Policy (or Policies) to be issued: Policy Amount

to be issued: Policy Amount") Schedule A 1. Commitment Date: 12/28/2016 at 8:00 AM Commitment No.: GRC-92528 Revision No. 2 2. Policy (or Policies) to be issued: Policy Amount a. ALTA Owner's Policy of Title Insurance (6-17-06) Proposed

Schedule A 1. Commitment Date: 12/28/2016 at 8:00 AM Commitment No.: GRC-92528 Revision No. 2 2. Policy (or Policies) to be issued: Policy Amount a. ALTA Owner's Policy of Title Insurance (6-17-06) Proposed

CHAPTER Senate Bill No. 4-D

CHAPTER 2007-339 Senate Bill No. 4-D An act relating to ad valorem taxation; authorizing the Department of Revenue to adopt emergency rules; providing for application and renewal thereof; requiring the

CHAPTER 2007-339 Senate Bill No. 4-D An act relating to ad valorem taxation; authorizing the Department of Revenue to adopt emergency rules; providing for application and renewal thereof; requiring the

DOCUMENTARY STAMP TAX COMBINED SUBJECT INDEX TO STATUTES & RULES. FLORIDA STATUTE CHAPTERS 201, 608, 620, 689 RULE 12B-4, F.A.C. Revised Oct.

DOCUMENTARY STAMP TAX COMBINED SUBJECT INDEX TO STATUTES & RULES FLORIDA STATUTE CHAPTERS 201, 608, 620, 689 RULE 12B-4, F.A.C. Revised Oct. 2004 -A- Acceptances: Bankers or Trade, 12B-4.053(16)(26), 12B-4.054(20)

DOCUMENTARY STAMP TAX COMBINED SUBJECT INDEX TO STATUTES & RULES FLORIDA STATUTE CHAPTERS 201, 608, 620, 689 RULE 12B-4, F.A.C. Revised Oct. 2004 -A- Acceptances: Bankers or Trade, 12B-4.053(16)(26), 12B-4.054(20)

November 16, 2016 Page 1 of 21

November 16, 2016 Page 1 of 21 MUNICIPALITY OF MIDDLESEX CENTRE BY-LAW NUMBER 2016-123 BEING A BY-LAW TO AUTHORIZE THE EXECUTION OF AN AGREEMENT BETWEEN THE MUNICIPALITY OF MIDDLESEX CENTRE AND BELLA LAGO

November 16, 2016 Page 1 of 21 MUNICIPALITY OF MIDDLESEX CENTRE BY-LAW NUMBER 2016-123 BEING A BY-LAW TO AUTHORIZE THE EXECUTION OF AN AGREEMENT BETWEEN THE MUNICIPALITY OF MIDDLESEX CENTRE AND BELLA LAGO

Maine Condo Statutes

Maine Revised Statutes Title 33: PROPERTY Chapter 31: MAINE CONDOMINIUM ACT Article 1: GENERAL PROVISIONS Maine Condo Statutes 1601-101. Short title This Act shall be known and may be cited as the Maine

Maine Revised Statutes Title 33: PROPERTY Chapter 31: MAINE CONDOMINIUM ACT Article 1: GENERAL PROVISIONS Maine Condo Statutes 1601-101. Short title This Act shall be known and may be cited as the Maine

Agreement of Purchase and Sale

Agreement of Purchase and Sale Condominium Resale Form 101 for use in the Province of Ontario This Agreement of Purchase and Sale dated this... day of... 20... BUYER,..., agrees to purchase from (Full

Agreement of Purchase and Sale Condominium Resale Form 101 for use in the Province of Ontario This Agreement of Purchase and Sale dated this... day of... 20... BUYER,..., agrees to purchase from (Full

CHAUTAUQUA COUNTY LAND BANK CORPORATION

EXHIBIT H CHAUTAUQUA COUNTY LAND BANK CORPORATION LAND ACQUISITION AND DISPOSITION POLICIES AND PRIORITIES November 14, 2012 *This document is intended to provide guidance to the Chautauqua County Land

EXHIBIT H CHAUTAUQUA COUNTY LAND BANK CORPORATION LAND ACQUISITION AND DISPOSITION POLICIES AND PRIORITIES November 14, 2012 *This document is intended to provide guidance to the Chautauqua County Land

Common Interest Ownership Act Key Points

Common Interest Ownership Act Key Points Declaration A common interest community may be created only by recording a declaration executed in the same manner as a deed. In a cooperative, it is created by

Common Interest Ownership Act Key Points Declaration A common interest community may be created only by recording a declaration executed in the same manner as a deed. In a cooperative, it is created by

Automatic Rent Reductions and Tax Decreases

Automatic Rent Reductions and Tax Decreases When are rents automatically reduced? Most tenants do not pay property taxes separately from their rent. In most situations, the rent a landlord charges a tenant

Automatic Rent Reductions and Tax Decreases When are rents automatically reduced? Most tenants do not pay property taxes separately from their rent. In most situations, the rent a landlord charges a tenant

GST/HST Memoranda Series

GST/HST Memoranda Series 19.2.1 Residential Real Property Sales Overview This section of Chapter 19 examines the tax status of most types of residential real property sales. Leases of residential real

GST/HST Memoranda Series 19.2.1 Residential Real Property Sales Overview This section of Chapter 19 examines the tax status of most types of residential real property sales. Leases of residential real

OFFICE OF REAL ESTATE

OFFICE OF REAL ESTATE DATE: October 25, 2017 TO: FROM: RE: Users of the Real Estate Manual Wayne Pace, Manager Acquisition Unit Changes and Updates to the Real Estate Manual The only current and accurate

OFFICE OF REAL ESTATE DATE: October 25, 2017 TO: FROM: RE: Users of the Real Estate Manual Wayne Pace, Manager Acquisition Unit Changes and Updates to the Real Estate Manual The only current and accurate

If GST is included as part of consideration, stamp duty is payable on the GST inclusive amount (Section 15A).

.") INTRODUCTION This guide has been prepared to assist in calculating the stamp duty payable on the documents available for self-stamping on RevenueSA Online or through the RevenueSA Periodic Return Arrangement.

INTRODUCTION This guide has been prepared to assist in calculating the stamp duty payable on the documents available for self-stamping on RevenueSA Online or through the RevenueSA Periodic Return Arrangement.

GST/HST New Residential Rental Property Rebate

GST/HST New Residential Rental Property Rebate Includes Forms GST524 and GST525 RC4231(E) Rev.06 Before you start What s new Effective July 1, 2006, under proposed legislation, the GST rate will be reduced

GST/HST New Residential Rental Property Rebate Includes Forms GST524 and GST525 RC4231(E) Rev.06 Before you start What s new Effective July 1, 2006, under proposed legislation, the GST rate will be reduced

ALBERTA REGULATION 480/81 Land Titles Act FORMS REGULATION

(Consolidated up to 149/2007 ALBERTA REGULATION 480/81 1 The forms in the Schedule are the forms prescribed for the purposes of the sections indicated on the forms. AR 480/81 s1 2 For the purpose of ensuring

(Consolidated up to 149/2007 ALBERTA REGULATION 480/81 1 The forms in the Schedule are the forms prescribed for the purposes of the sections indicated on the forms. AR 480/81 s1 2 For the purpose of ensuring

TP-584-I. Instructions for Form TP-584. Summary of September 2003 Changes. Who must file. When and where to file. Instructions for Schedule A

New York State Department of Taxation and Finance TP-584-I Instructions for Form TP-584 (10/03) Combined Real Estate Transfer Tax Return, Credit Line Mortgage Certificate, and Certification of Exemption

New York State Department of Taxation and Finance TP-584-I Instructions for Form TP-584 (10/03) Combined Real Estate Transfer Tax Return, Credit Line Mortgage Certificate, and Certification of Exemption

Sale and Other Disposition of Land Policy

Section Community & Development Services Subsection Sale and Other Disposition of Land DATE Approved by By-law : December 12, 2017 158-2017 Supersedes By-law : 138-2000 PAGE OF 1 1.0 Purpose 1.1 To provide

Section Community & Development Services Subsection Sale and Other Disposition of Land DATE Approved by By-law : December 12, 2017 158-2017 Supersedes By-law : 138-2000 PAGE OF 1 1.0 Purpose 1.1 To provide

THIS COMMUNITY LAND TRUST GROUND LEASE RIDER (the Rider ) is made this day of,, and amends and supplements a certain ground lease (the CLT Ground

is made this day of,, and amends and supplements a certain ground lease (the CLT Ground") Form 490 Community Land Trust Ground Lease Rider THIS COMMUNITY LAND TRUST GROUND LEASE RIDER (the Rider ) is made this day of,, and amends and supplements a certain ground lease (the CLT Ground Lease

Form 490 Community Land Trust Ground Lease Rider THIS COMMUNITY LAND TRUST GROUND LEASE RIDER (the Rider ) is made this day of,, and amends and supplements a certain ground lease (the CLT Ground Lease

THE CORPORATION OF THE TOWNSHIP OF WHITEWATER REGION. By-Law # Land Required For Municipal Planning and Road Purposes

THE CORPORATION OF THE TOWNSHIP OF WHITEWATER REGION By-Law # 13-07-637 Land Required For Municipal Planning and Road Purposes WHEREAS the Municipal Act Chapter 25, Statutes of Ontario 2001 Section 11

THE CORPORATION OF THE TOWNSHIP OF WHITEWATER REGION By-Law # 13-07-637 Land Required For Municipal Planning and Road Purposes WHEREAS the Municipal Act Chapter 25, Statutes of Ontario 2001 Section 11

SECTION: FINANCE AND CONTROL NO: FI TA REFERENCE: TAXES Date: March 17, 2008

PROCEDURES SECTION: FINANCE AND CONTROL NO: FI TA - 02 REFERENCE: TAXES Date: March 17, 2008 Next Review Date: March 2010 TITLE: PROPERTY TAX REBATE PROGRAM 1. 0 PURPOSE 1.1 To provide a program with clear

PROCEDURES SECTION: FINANCE AND CONTROL NO: FI TA - 02 REFERENCE: TAXES Date: March 17, 2008 Next Review Date: March 2010 TITLE: PROPERTY TAX REBATE PROGRAM 1. 0 PURPOSE 1.1 To provide a program with clear

Authorized Subscriber Register Pre-qualified Forms and Natures of Interest

Authorized Subscriber Register Pre-qualified Forms and Natures of Interest Provincial Statutory Officer The list below contains the pre-approved forms and natures of interest for a candidate who will be

Authorized Subscriber Register Pre-qualified Forms and Natures of Interest Provincial Statutory Officer The list below contains the pre-approved forms and natures of interest for a candidate who will be

and Notice of Public Hearing Changes in Use Under Section 168(i)(5)

(5)") Notice of Proposed Rulemaking and Notice of Public Hearing Changes in Use Under Section 168(i)(5) REG 138499 02 AGENCY: Internal Revenue Service (IRS), Treasury. ACTION: Notice of proposed rulemaking and

Notice of Proposed Rulemaking and Notice of Public Hearing Changes in Use Under Section 168(i)(5) REG 138499 02 AGENCY: Internal Revenue Service (IRS), Treasury. ACTION: Notice of proposed rulemaking and

APPLICATION TO THE ASSESSOR FOR CLASSIFICATION OF LAND AS FOREST LAND

STATE OF CONNECTICUT FORM M-39, REVISED 6/2016 APPROVED BY THE COMMISSIONER DEPARTMENT OF ENERGY & ENVIRONMENTAL PROTECTION APPLICATION TO THE ASSESSOR FOR CLASSIFICATION OF LAND AS FOREST LAND Declaration

STATE OF CONNECTICUT FORM M-39, REVISED 6/2016 APPROVED BY THE COMMISSIONER DEPARTMENT OF ENERGY & ENVIRONMENTAL PROTECTION APPLICATION TO THE ASSESSOR FOR CLASSIFICATION OF LAND AS FOREST LAND Declaration

Single Family Housing Policy Handbook: FHA Connection 203k Calculator and Other System Enhancements

Office of Single Family Program Development Single Family Housing Policy Handbook: FHA Connection 203k Calculator and Other System Enhancements April 28, 2016 Last Updated: 4/27/16 Presented by: Kevin

Office of Single Family Program Development Single Family Housing Policy Handbook: FHA Connection 203k Calculator and Other System Enhancements April 28, 2016 Last Updated: 4/27/16 Presented by: Kevin

TRUSTEE S MEMORANDUM OF FORECLOSURE SALE OF REAL PROPERTY OF

TRUSTEE S MEMORANDUM OF FORECLOSURE SALE OF REAL PROPERTY OF In consideration of the premises and other good and valuable consideration, the adequacy and receipt of which are acknowledged, the undersigned

TRUSTEE S MEMORANDUM OF FORECLOSURE SALE OF REAL PROPERTY OF In consideration of the premises and other good and valuable consideration, the adequacy and receipt of which are acknowledged, the undersigned

CTAS e-li. Published on e-li (http://ctas-eli.ctas.tennessee.edu) July 11, 2018 Register of Deeds Records

July 11, 2018 Register of Deeds Records") Published on e-li (http://ctas-eli.ctas.tennessee.edu) July 11, 2018 Dear Reader: The following document was created from the CTAS electronic library known as e-li. This online library is maintained daily

Published on e-li (http://ctas-eli.ctas.tennessee.edu) July 11, 2018 Dear Reader: The following document was created from the CTAS electronic library known as e-li. This online library is maintained daily

Configuring Service Charge Settlement in Flexible Real Estate Management (RE FX)

") Configuring Service Charge Settlement in Flexible Real Estate Management (RE FX) Applies to: Any consultant who wants to configure the Service Charge Settlement settings for user requirements in SAP flexible

Configuring Service Charge Settlement in Flexible Real Estate Management (RE FX) Applies to: Any consultant who wants to configure the Service Charge Settlement settings for user requirements in SAP flexible

CONDOMINIUM MORTGAGE FINANCING

CONDOMINIUM MORTGAGE FINANCING INTRODUCTION: Condominium mortgage financing is generally in one of two forms. During development of the project, the owner/declarant will have blanket mortgage financing

CONDOMINIUM MORTGAGE FINANCING INTRODUCTION: Condominium mortgage financing is generally in one of two forms. During development of the project, the owner/declarant will have blanket mortgage financing

Table of Contents. Sections. Tables. Appendices

- Table of Contents Sections Section 1. Bond Profile 1 Section 2. Fund Information 2 Section 3. Special Tax Information 3 Section 4. Owner and Development Status Information 4 Section 5. Payment History

- Table of Contents Sections Section 1. Bond Profile 1 Section 2. Fund Information 2 Section 3. Special Tax Information 3 Section 4. Owner and Development Status Information 4 Section 5. Payment History

SUBJECT: DUTY TO SERVE AFFORDABLE HOUSING PRESERVATION AND RURAL HOUSING

TO: Freddie Mac Sellers and Servicers September 26, 2018 2018-16 SUBJECT: DUTY TO SERVE AFFORDABLE HOUSING PRESERVATION AND RURAL HOUSING Making housing available and affordable nationwide is fundamental

TO: Freddie Mac Sellers and Servicers September 26, 2018 2018-16 SUBJECT: DUTY TO SERVE AFFORDABLE HOUSING PRESERVATION AND RURAL HOUSING Making housing available and affordable nationwide is fundamental

LAND (DUTIES AND TAXES) Act 46 of July 1984

Act 46 of July 1984") PART I PRELIMINARY 1 Short title 2 Interpretation PART II REGISTRATION DUTY 3 Duty leviable PART III LAND TRANSFER TAX 4 Levy of land transfer tax 5 Exemption 6 Declaration by transferor 7 Penalty for

PART I PRELIMINARY 1 Short title 2 Interpretation PART II REGISTRATION DUTY 3 Duty leviable PART III LAND TRANSFER TAX 4 Levy of land transfer tax 5 Exemption 6 Declaration by transferor 7 Penalty for

STANDARD COMMERCIAL PURCHASE AND SALE AGREEMENT (With Contingencies)

") STANDARD COMMERCIAL PURCHASE AND SALE AGREEMENT (With Contingencies) The parties make this Agreement this day of,. This Agreement supersedes and replaces all obligations made in any prior Letter of Intent,

STANDARD COMMERCIAL PURCHASE AND SALE AGREEMENT (With Contingencies) The parties make this Agreement this day of,. This Agreement supersedes and replaces all obligations made in any prior Letter of Intent,