Historic Tax Credits: Leveraging History to Rebuild Legacy Cities. Jason Yots, Esq. ~ November 14, 2016

|

|

|

- Caitlin Jennings

- 5 years ago

- Views:

Transcription

1 Historic Tax Credits: Leveraging History to Rebuild Legacy Cities Jason Yots, Esq. ~ November 14, 2016

2 Today s Discussion Why do legacy cities need tax credits? The historic tax credit program The Mattress Factory: a case study Hot Tax Topics Involving HTCs

3 Why do legacy cities need tax credits? Historic Tax Credits: Leveraging Heritage to Rebuild Legacy Cities

4 Source:

5 Source:

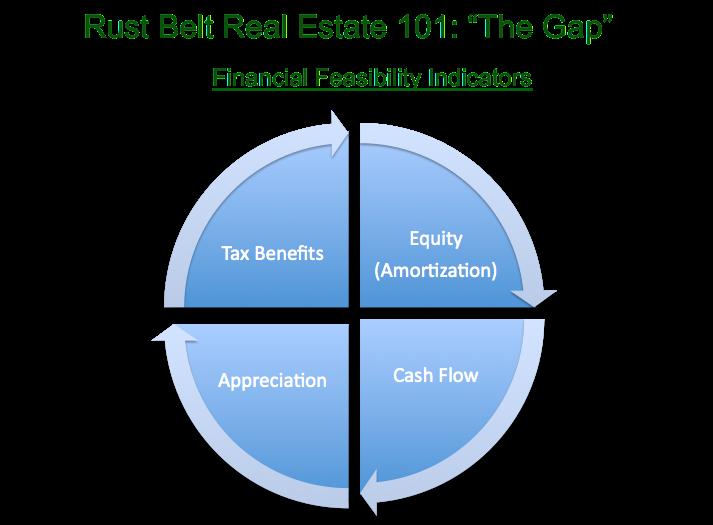

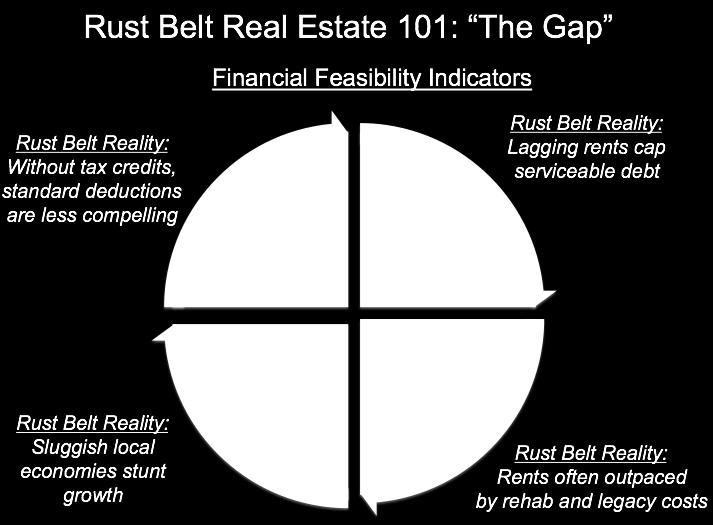

6 Capital Costs Capital Sources Rust Belt Real Estate 101: The Gap

7

8 The historic tax credit program Historic Tax Credits: Leveraging Heritage to Rebuild Legacy Cities

9 Historic Tax Credits $78.3 Billion Total HTC Investment 2.36 Million Total Jobs Generated 527,866 (28%) Housing Units ( Affordable )

10 State Tax Credit Programs Source: Sarah Vonesh

11 Source: Sarah Vonesh

12 Data Source National Park Service / Graphic: National Trust for Historic Preservation and Historic Tax Credit Coalition

13 State of New York Economic Impacts of HTC Investment, Total Number of Projects Rehabilitated: 406 Total Development Costs: $3,874,334,894 Total Qualified Rehabilitation Expenditures: $3,215,697,962 Federal HTC Amount: $643,139,592 Total Number of Jobs Created: 49,249 Construction: 22,121 Permanent: 27,128 Total Income (Net of Taxes) Generated: $3,965,877,900 Household: $2,149,151,400 Business: $1,816,726,500 Total Taxes Generated: $893,531,600 Local: $135,045,000 State: $131,871,100 Federal: $626,615,500 Data Source National Park Service / Graphic: National Trust for Historic Preservation and Historic Tax Credit Coalition

14 1. Does your building qualify? Threshold Issues 2. Will your rehab qualify? 3. Estimate your project s costs and HTCs 4. Make a financing plan 5. Assemble your team: a. Architect b. Contractor c. Accountant d. Attorney e. Consultant

15 The Mattress Factory: a case study Historic Tax Credits: Leveraging Heritage to Rebuild Legacy Cities

16

17 Use: Use: Source: Source: Source: Source: Type Amount Lender HTCs Dev Equity Def Dev Fee Acquisition $700,000 $0 $700,000 $0 Hard Costs $4,000,000 $4,000,000 $0 $0 Softs Costs $600,000 $0 $600,000 $0 Developer Fee $500,000 $0 $165,675 $0 $334,325 Totals $5,800,000 $4,000,000 $1,465,675 $0 $334,325 SOURCES & USES OF FUNDS

18 Use: Use: Type Amount QREs Acquisition $700,000 $0 Hard Costs & FF&E $4,000,000 $3,800,000 Soft & Financing Costs $600,000 $570,000 Developer Fee $500,000 $500,000 Totals $5,800,000 $4,870,000 QUALIFIED REHABILITATION EXPENDITURES

19 QREs $4,870,000 Federal/NY HTC % x 40% Federal/NY HTCs $1,948,000 HTC investor s interest % 99% HTCs to HTC investor $1,928,520 Blended price for HTCs x $0.76 Gross equity invested $1,465,675

20 Percentage Invested Milestones 20% Loan closing; HTC investor admission 65% P.I.S.; Part 3 approval; Cost certification; Perm. loan conversion 15% Schedule K-1s; Tax returns filed

21 Year Income, growth= 3% PGI 396, , , , ,701 Misc Income Less Vacancy 5% -19,800-20,394-21,006-21,636-22,285 Adjusted PGI 376, , , , ,416 Expense, growth= 3% Real Estate Taxes 21,453 21,453 21,453 21,453 21,453 Property Insurance 7,500 7,725 7,957 8,195 8,441 Utilities 6,000 6,180 6,365 6,556 6,753 Property Mgt 6% 22,572 23,249 23,947 24,665 25,405 Admin, overhead 12,000 12,360 12,731 13,113 13,506 Maintenance 4,000 4,000 4,000 4,000 4,000 Reserves Total Expenses 73,525 74,967 76,453 77,983 79,558 Net Operating Income 302, , , , ,858 Debt Service Principal Payment 1st 41,310 43,424 45,645 47,981 50,435 Interest Payment 1st 139, , , , ,937 Total Debt Service Payments 180, , , , ,372 Net Available for Dist 122, , , , ,486 Asset Mgmt Fee - HTC investor 2,500 2,500 2,500 2,500 2,500 Annual Priority Return - HTC investor 19,222 19,222 19,222 19,222 19,222 19,222 Repay DDF (80%) 347,957 80,465 88,340 96, ,806 0 Cash Flow after DDF 20,116 22,085 24,113 26, ,764 MM Distribution ,418 IM Distribution 19,915 21,864 23,872 25, ,346 DSCR

22 Hot Tax Topics Involving HTCs Historic Tax Credits: Leveraging Heritage to Rebuild Legacy Cities

23 Hot Tax Topics Involving HTCs Safe harbor compliance - Rev. Proc

24 Historic Boardwalk Hall LLC vs. Commissioner of IRS IRS: sham partnership ; reallocation of historic tax credits U.S. Tax Court: IRS was wrong (2009) US Court of Appeals (3 rd Circuit): IRS was right (2012)

25 Terms Developer Minimum Interest Investor Minimum Interest Minimum equity contribution prior to P.I.S. Priority Returns Guaranties Cash Flow Put/Call Terms Before Historic Boardwalk Hall.01%.01% None 2% - 3% cash-on-cash annual preferred return 1.Tax credit recapture 2.Operating deficits 3.Environmental liability 4.Construction completion 5.Escrows permitted After waterfall, investor often is allocated 99% of $0 each year Call fair market value Put x% cash-on-cash After Rev. Proc % 5% 20% contributed; 75% fixed Varies, but generally lower, if meaningful cash flows to investor Similar, but developer may not guaranty deal structure or provide funded guarantees (other than limited operating deficit) More meaningful cash flow to investor Call: prohibited but flip OK Put minimum = FMV

26 Hot Tax Topics Involving HTCs Master lease transactions I.R.C. 50(d)

27 Organizational chart Main Street, Upstate, NY 2016 Borrelli & Yots PLLC Historic tax credit (HTC) syndication structure Manager Members Jill Sponsor Joe Sponsor Investor Members Multiple Investors 50% 50% 123 Main Street Managing Member LLC HTC Investor 1% 99% Managing Investor Member Member 123 Main Street LLC (Fee Simple Title Holder) Leases Residential and commercial tenants

28 Master lease structure chart Main Street, Upstate, NY 2016 Borrelli & Yots PLLC Historic tax credit (HTC) syndication structure Class A Members Joe Sponsor Jill Sponsor (50%) Class B Members Multiple Investors (50%) 123 Main Street Managing Member LLC 123 Main Street Master Tenant LLC 123 Main Street Managing Member LLC Upstate Bank 90% 10% 1% 99% Member Investor Managing Investor Member Member Member 123 Main Street LLC (Master Lessor, Fee Simple Title Holder) Master Lease and Tax Credit Pass-Through* 123 Main Street Master Tenant LLC (Master Tenant) Subleases Residential and commercial subtenants *Pursuant to an IRC 50(d) election, historic tax credits flow to 123 Main Street Master Tenant LLC

29 Partnership Structure Basis Adjustment Landlord Before I.R.C. 50(d) Regs No partnership basis reduction Basis Adjustment - Tenant No partnership basis reduction; Tenant partnership amortizes 50(d) income over shortest applicable recovery period 50(d) Income Treatment Partnership Level Item vs. 50(d) income increases partners outside basis in the Tenant partnership 50(d) income is a Tenant partnership level item Partner Level Item 50(d) Income Acceleration Some practitioners accelerated all or a portion of unamortized 50(d) income upon investor s exit from Tenant partnership

30 Partnership Structure Basis Adjustment Landlord After I.R.C. 50(d) Regs Same Basis Adjustment - Tenant Same 50(d) Income Treatment Partnership Level Item vs. Partner Level Item 50(d) Income Acceleration 50(d) income DOES NOT increase partners outside basis in the Tenant partnership 50(d) income is a PARTNER LEVEL item ( ultimate credit claimant ) NO ACCELERATION, unless actively elected upon exit

income recognized $ 871,795 Unamortized")

31 Sample 50(d) Income Calculation $1,000,000 Amount of federal HTC claimed 39 years Asset recovery period $ 25,641 Annual 50(d) income x 5 years HTC recapture period $ 128,205 50(d) income recognized $ 871,795 Unamortized 50(d) income

32 Questions?

Historic Tax Credit Presentation Date: March 22, 2016

Historic Tax Credit Presentation Date: March 22, 2016 Today s Presenter(s): Lynn Wickham Hartman (319) 896-4083 lhartman@simmonsperrine.com Matthew J. Hektoen (319) 896-4030 mhektoen@simmonsperrine.com

Historic Tax Credit Presentation Date: March 22, 2016 Today s Presenter(s): Lynn Wickham Hartman (319) 896-4083 lhartman@simmonsperrine.com Matthew J. Hektoen (319) 896-4030 mhektoen@simmonsperrine.com

Financing Historic Theaters Historic Preservation Tax Credits

Financing Historic Theaters Historic Preservation Tax Credits Heritage Ohio Annual Revitalization and Preservation Conference October 6, 2015 Chad Arfons, McDonald Hopkins LLC Federal Historic Preservation

Financing Historic Theaters Historic Preservation Tax Credits Heritage Ohio Annual Revitalization and Preservation Conference October 6, 2015 Chad Arfons, McDonald Hopkins LLC Federal Historic Preservation

Developer Non Managing Member- Historic Tax Credit Investor. Managing Member- Developer. Developer Fee Capital Contribution Tax Capital Contributions

Developer Managing Member- Developer Non Managing Member- Historic Tax Credit Investor Developer Fee Capital Contribution Tax Credits Capital Contributions Building Owner LLC/ Master Landlord Managing

Developer Managing Member- Developer Non Managing Member- Historic Tax Credit Investor Developer Fee Capital Contribution Tax Credits Capital Contributions Building Owner LLC/ Master Landlord Managing

DISABILITY HOUSING NETWORK LOW INCOME HOUSING TAX CREDIT DEVELOPMENT

DISABILITY HOUSING NETWORK LOW INCOME HOUSING TAX CREDIT DEVELOPMENT OCTOBER 24, 2012 OHIO CAPITAL CORPORATION FOR HOUSING OCCH s mission is: to cause the construction, rehabilitation, and preservation

DISABILITY HOUSING NETWORK LOW INCOME HOUSING TAX CREDIT DEVELOPMENT OCTOBER 24, 2012 OHIO CAPITAL CORPORATION FOR HOUSING OCCH s mission is: to cause the construction, rehabilitation, and preservation

Tax Credit Finance Primer. Tim Favaro. Partner Cannon Heyman & Weiss, LLP.

Tax Credit Finance Primer Tim Favaro Partner Cannon Heyman & Weiss, LLP tfavaro@chwattys.com New Markets Tax Credit & Historic Tax Credit 101 New Markets Tax Credit Program: Background Codified in Section

Tax Credit Finance Primer Tim Favaro Partner Cannon Heyman & Weiss, LLP tfavaro@chwattys.com New Markets Tax Credit & Historic Tax Credit 101 New Markets Tax Credit Program: Background Codified in Section

The Legal and Financial Facets of Historic Tax Credits

California Preservation Foundation From Dollars & Cents to Success: Financial Incentive Programs for Historic Preservation February 10, 2016 The Legal and Financial Facets of Historic Tax Credits Roy Chou,

California Preservation Foundation From Dollars & Cents to Success: Financial Incentive Programs for Historic Preservation February 10, 2016 The Legal and Financial Facets of Historic Tax Credits Roy Chou,

Contents TABLE OF CONTENTS

Contents CHAPTER 1 Low-Income Housing Tax Credits and Year 15 17 1.01 Introduction 17 1.02 Overview of the LIHTC Program 18 [1] Land Use Restriction Agreement (LURA) 20 [2] Extended-Use Period 21 1.03

Contents CHAPTER 1 Low-Income Housing Tax Credits and Year 15 17 1.01 Introduction 17 1.02 Overview of the LIHTC Program 18 [1] Land Use Restriction Agreement (LURA) 20 [2] Extended-Use Period 21 1.03

Rehabilitation Tax Credits

Rehabilitation Tax Credits Selected Issues in Master Lease Pass-Through Transactions Steven L. Paul Nicholas Romanos February 1, 2010 REHABILITATION TAX CREDITS Selected Issues in Master Lease Pass-Through

Rehabilitation Tax Credits Selected Issues in Master Lease Pass-Through Transactions Steven L. Paul Nicholas Romanos February 1, 2010 REHABILITATION TAX CREDITS Selected Issues in Master Lease Pass-Through

Retail Acquisition Example

Property Information Retail Acquisition Example Project Assumptions Acquisition Assumptions Property Name Retail Acquisition Example Project Type Acquisition Location Austin, TX Acquisition Cost $1,800,000

Property Information Retail Acquisition Example Project Assumptions Acquisition Assumptions Property Name Retail Acquisition Example Project Type Acquisition Location Austin, TX Acquisition Cost $1,800,000

INTRODUCTION TO FEDERAL LOW INCOME HOUSING TAX CREDITS. 1. Applicable Percentage

INTRODUCTION TO FEDERAL LOW INCOME HOUSING TAX CREDITS I. THE TAX CREDIT GENERALLY a. Established under the Tax Reform Act of 1986. Essentially an effort to partially privatize the affordable housing industry.

INTRODUCTION TO FEDERAL LOW INCOME HOUSING TAX CREDITS I. THE TAX CREDIT GENERALLY a. Established under the Tax Reform Act of 1986. Essentially an effort to partially privatize the affordable housing industry.

TAX ALERT. Master tenant HTC transactions: IRS treatment of 50(d) income

income") AUG. 2, 2016 Mark Snider 614.227.2510 msnider@porterwright.com Master tenant HTC transactions: IRS treatment of 50(d) income Dave Tumen 614.227.2260 dtumen@porterwright.com The historic tax credit industry

AUG. 2, 2016 Mark Snider 614.227.2510 msnider@porterwright.com Master tenant HTC transactions: IRS treatment of 50(d) income Dave Tumen 614.227.2260 dtumen@porterwright.com The historic tax credit industry

New York State and Federal Historic

1 New York State and Federal Historic Rehabilitation Tax Credits Co Sponsor: Preservation League of New York State www.preservenys.org 2 New York State and Federal Historic Rehabilitation Tax Credits New

1 New York State and Federal Historic Rehabilitation Tax Credits Co Sponsor: Preservation League of New York State www.preservenys.org 2 New York State and Federal Historic Rehabilitation Tax Credits New

Profitable Pre$ervation

Profitable Pre$ervation Accessing Historic Tax Credits Jason Yots, Preservation Studios www.preservationstudios.com Historic Tax Credits 2012 - By The Numbers 57,783 - Jobs created by HTCs 17,991 - Housing

Profitable Pre$ervation Accessing Historic Tax Credits Jason Yots, Preservation Studios www.preservationstudios.com Historic Tax Credits 2012 - By The Numbers 57,783 - Jobs created by HTCs 17,991 - Housing

Historic Tax Credits Overview

Historic Tax Credits Overview 20% or 10% tax credit to rehabilitate a certified historic or very old structure (built prior to 1936) Must be taxable income producing property and rehabilitation must be

Historic Tax Credits Overview 20% or 10% tax credit to rehabilitate a certified historic or very old structure (built prior to 1936) Must be taxable income producing property and rehabilitation must be

Putting Real Estate To Good Use: Current Issues with Obtaining

Putting Real Estate To Good Use: Current Issues with Obtaining Conservation Easement Deductions and Rehabilitation Tax Credits Panelists: Robert Honigman, Arent Fox LLP Lee Sheller, DLA Piper ABA Tax Section

Putting Real Estate To Good Use: Current Issues with Obtaining Conservation Easement Deductions and Rehabilitation Tax Credits Panelists: Robert Honigman, Arent Fox LLP Lee Sheller, DLA Piper ABA Tax Section

The Housing Authority of the County of Contra Costa. Subsidy Layering Review Checklist for Low-Income Housing Tax Credit Projects

The Housing Authority of the County of Contra Costa Subsidy Layering Review Checklist for Low-Income Housing Tax Credit Projects Projection Name: Location: Narrative description of project including: Sources

The Housing Authority of the County of Contra Costa Subsidy Layering Review Checklist for Low-Income Housing Tax Credit Projects Projection Name: Location: Narrative description of project including: Sources

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2014

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2014 Presented By: Karen Kent, CPA, Partner, Kevin P. Martin & Associates, P.C. Kenneth Lund,

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2014 Presented By: Karen Kent, CPA, Partner, Kevin P. Martin & Associates, P.C. Kenneth Lund,

Combining the Historic Tax Credit with Other Tax Credits (New Markets) February 5, 2009

February 5, 2009") Combining the Historic Tax Credit with Other Tax Credits (New Markets) February 5, 2009 Don Nimey don.nimey@reznickgroup.com Phone: 301-280-1846 New Markets Tax Credit Program Enacted on December 21, 2000

Combining the Historic Tax Credit with Other Tax Credits (New Markets) February 5, 2009 Don Nimey don.nimey@reznickgroup.com Phone: 301-280-1846 New Markets Tax Credit Program Enacted on December 21, 2000

Neighborhood Stabilization Program

Neighborhood Stabilization Program Neighborhood Stabilization Program What is the Neighborhood Stabilization Program? NSP was funded in 3 rounds to provide assistance to state and local governments to

Neighborhood Stabilization Program Neighborhood Stabilization Program What is the Neighborhood Stabilization Program? NSP was funded in 3 rounds to provide assistance to state and local governments to

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2016

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2016 Presented By: Karen Kent, CPA, Partner, Kevin P. Martin & Associates, P.C. Kenneth Lund,

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2016 Presented By: Karen Kent, CPA, Partner, Kevin P. Martin & Associates, P.C. Kenneth Lund,

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2011

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2011 Presented By: Marianne Heard, CPA, MST, Tax Director, Kevin P. Martin & Associates, P.C.

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2011 Presented By: Marianne Heard, CPA, MST, Tax Director, Kevin P. Martin & Associates, P.C.

EXHIBIT E LOW INCOME HOUSING TAX CREDIT APPLICATION REQUIREMENTS

EXHIBIT E LOW INCOME HOUSING TAX CREDIT APPLICATION REQUIREMENTS A. Application for Tax Credit Reservation or Tax-Exempt Bond Conditional Commitment shall Include: 1. Complete application form (current

EXHIBIT E LOW INCOME HOUSING TAX CREDIT APPLICATION REQUIREMENTS A. Application for Tax Credit Reservation or Tax-Exempt Bond Conditional Commitment shall Include: 1. Complete application form (current

CHAPTER TAX CREDITS AND SUBSIDY LAYERING. The Table of Contents

UNIT 12.0 PRESERVATION CHAPTER 12.10 TAX CREDITS AND SUBSIDY LAYERING The Table of Contents 12.10.1 Purpose.. I-1 12.10.2 Applicability.. I-2 12.10.3 Definitions and Acronyms... I-2 12.10.4 LIHTC s and

UNIT 12.0 PRESERVATION CHAPTER 12.10 TAX CREDITS AND SUBSIDY LAYERING The Table of Contents 12.10.1 Purpose.. I-1 12.10.2 Applicability.. I-2 12.10.3 Definitions and Acronyms... I-2 12.10.4 LIHTC s and

Housing Tax Credit Carryover, 10 Percent Test, Evidence of Construction Start and Final Allocation Application Training Workshop. September 20, 2018

Housing Tax Credit Carryover, 10 Percent Test, Evidence of Construction Start and Final Allocation Application Training Workshop September 20, 2018 Table of Contents Topic Page Carryover Allocation Application

Housing Tax Credit Carryover, 10 Percent Test, Evidence of Construction Start and Final Allocation Application Training Workshop September 20, 2018 Table of Contents Topic Page Carryover Allocation Application

The construction loan collapses a series of costs (cash outflows) incurred during the construction process into a single value

incurred during the construction process into a single value") he construction loan collapses a series of costs (cash outflows) incurred during the construction process into a single value as of a single (future) point in time (the projected completion date of the

he construction loan collapses a series of costs (cash outflows) incurred during the construction process into a single value as of a single (future) point in time (the projected completion date of the

Tax Credits 101. Wednesday, November 7 10:45am 12:00pm

Tax Credits 101 Wednesday, November 7 10:45am 12:00pm Today s Panel Kevin Clark Ohio Housing Finance Agency (OHFA) Brian Graney Ohio Capital Corporation for Housing Meg Manley PIRHL, LLC Tim Swiney Wallick

Tax Credits 101 Wednesday, November 7 10:45am 12:00pm Today s Panel Kevin Clark Ohio Housing Finance Agency (OHFA) Brian Graney Ohio Capital Corporation for Housing Meg Manley PIRHL, LLC Tim Swiney Wallick

Low Income Housing Tax Credits 101 (and a little beyond 101) James Lehnhoff, Municipal Advisor

James Lehnhoff, Municipal Advisor") Low Income Housing Tax Credits 101 (and a little beyond 101) James Lehnhoff, Municipal Advisor 9/29/2017 1 Affordable Housing Need What is Affordable? Overview Why do affordable housing projects need financial

Low Income Housing Tax Credits 101 (and a little beyond 101) James Lehnhoff, Municipal Advisor 9/29/2017 1 Affordable Housing Need What is Affordable? Overview Why do affordable housing projects need financial

Financing Downtown Projects Using Historic Tax Credits and Other Sources Downtown Institute January 21, 2015 Greg Paxton, Maine Preservation

Financing Downtown Projects Using Historic Tax Credits and Other Sources Downtown Institute January 21, 2015 Greg Paxton, Maine Preservation Lemont Block, Brunswick Wyler s Outlet (Maine goods) Economic

Financing Downtown Projects Using Historic Tax Credits and Other Sources Downtown Institute January 21, 2015 Greg Paxton, Maine Preservation Lemont Block, Brunswick Wyler s Outlet (Maine goods) Economic

Housing Consortium of Everett and Snohomish County 2013 Affordable Housing 101. Paul Purcell President, Beacon Development Group

Housing Consortium of Everett and Snohomish County 2013 Affordable Housing 101 Paul Purcell President, Beacon Development Group Session Outline 1. What is affordable housing? How is it defined? Who does

Housing Consortium of Everett and Snohomish County 2013 Affordable Housing 101 Paul Purcell President, Beacon Development Group Session Outline 1. What is affordable housing? How is it defined? Who does

Leveraging Federal Funds

Saipan Economic Development Forum June 4, 2013 Jesse Wu, Director Office of Public Housing (HUD Honolulu Field Office) U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT The Development s (HUD) mission is

Saipan Economic Development Forum June 4, 2013 Jesse Wu, Director Office of Public Housing (HUD Honolulu Field Office) U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT The Development s (HUD) mission is

DSHA Underwriting Guidelines

DSHA Underwriting Guidelines NOTE: All applicants must utilize DSHA s LIHTC Application Part II - Pro Forma. No addition of tabs, changes to formulas, or manipulations of any kind are allowed. Any deviations

DSHA Underwriting Guidelines NOTE: All applicants must utilize DSHA s LIHTC Application Part II - Pro Forma. No addition of tabs, changes to formulas, or manipulations of any kind are allowed. Any deviations

REPORT TO THE HOUSING AUTHORITY OF THE CITY OF SAN DIEGO

ITEM 2 REPORT TO THE HOUSING AUTHORITY OF THE CITY OF SAN DIEGO DATE ISSUED: March 20, 2018 REPORT NO: HAR18-014 ATTENTION: SUBJECT: Chair and Members of the Housing Authority of the City of San Diego

ITEM 2 REPORT TO THE HOUSING AUTHORITY OF THE CITY OF SAN DIEGO DATE ISSUED: March 20, 2018 REPORT NO: HAR18-014 ATTENTION: SUBJECT: Chair and Members of the Housing Authority of the City of San Diego

Analyzing the Impact of the Financial Crisis on LIHTC Property Values. National Council of Affordable Housing Marketing Analysts November 9, 2009

Analyzing the Impact of the Financial Crisis on LIHTC Property Values National Council of Affordable Housing Marketing Analysts November 9, 2009 David Fournier dfournier@arausa.com THE CLIFF Total Apartments

Analyzing the Impact of the Financial Crisis on LIHTC Property Values National Council of Affordable Housing Marketing Analysts November 9, 2009 David Fournier dfournier@arausa.com THE CLIFF Total Apartments

2019 9% Competitive Housing Credit Application

2019 9% Competitive Housing Credit Application Application Checklist This checklist includes all the items from the CFA application and the LIHTC Addendum that are required for the 2019 9% Application

2019 9% Competitive Housing Credit Application Application Checklist This checklist includes all the items from the CFA application and the LIHTC Addendum that are required for the 2019 9% Application

Adventures in Section 1031

NYSBA Real Estate Section Advanced Real Estate Topics Adventures in Section 1031 Lana Kalickstein Roberts & Holland LLP December 12, 2016 1 Acquisition of Property for $150 A (an individual) LLC 1 $100

NYSBA Real Estate Section Advanced Real Estate Topics Adventures in Section 1031 Lana Kalickstein Roberts & Holland LLP December 12, 2016 1 Acquisition of Property for $150 A (an individual) LLC 1 $100

Responsible Partnerships Between For profits and Nonprofits

Responsible Partnerships Between For profits and Nonprofits 23nd Annual Statewide Affordable Housing Conference Florida Housing Coalition September 21, 2010 Tim Morgan Development Partner, The NRP Group

Responsible Partnerships Between For profits and Nonprofits 23nd Annual Statewide Affordable Housing Conference Florida Housing Coalition September 21, 2010 Tim Morgan Development Partner, The NRP Group

9/9/2015. VitalSpirit LLC. Project Planning. Determine Housing Needs Population. Determine Housing Needs New Construction

Low Income Housing Tax Credits Program Setup: Finance Workshop Southwest Tribal Housing Alliance 7 th Annual Housing Forum Casino Del Sol Resort Tucson, AZ July 30, 2015 VitalSpirit LLC Team of six professionals

Low Income Housing Tax Credits Program Setup: Finance Workshop Southwest Tribal Housing Alliance 7 th Annual Housing Forum Casino Del Sol Resort Tucson, AZ July 30, 2015 VitalSpirit LLC Team of six professionals

Rental Assistance Demonstration Program GOING BIG IN EL PASO

Rental Assistance Demonstration Program GOING BIG IN EL PASO WHAT WERE WE THINKING? Full Portfolio Conversion Aging housing stock - majority of portfolio was over 40 years old - would have taken 20

Rental Assistance Demonstration Program GOING BIG IN EL PASO WHAT WERE WE THINKING? Full Portfolio Conversion Aging housing stock - majority of portfolio was over 40 years old - would have taken 20

PENNSYLVANIA HOUSING FINANCE AGENCY (2019 UNDERWRITING APPLICATION)

") DEVELOPMENT COST LIMITS The development costs, fees, and expenses contained herein are the maximum amounts that may be included in total development cost and, if applicable, the Tax Credit eligible basis

DEVELOPMENT COST LIMITS The development costs, fees, and expenses contained herein are the maximum amounts that may be included in total development cost and, if applicable, the Tax Credit eligible basis

Historic Preservation Alliance of Arkansas (Preserve Arkansas) Property Assistance Program Application

Property Assistance Program Application") Historic Preservation Alliance of Arkansas (Preserve Arkansas) Property Assistance Program Application The mission of the Historic Preservation Alliance of Arkansas (Preserve Arkansas) is to work to build

Historic Preservation Alliance of Arkansas (Preserve Arkansas) Property Assistance Program Application The mission of the Historic Preservation Alliance of Arkansas (Preserve Arkansas) is to work to build

Opening Doors to Affordable Mixed-Use Development

Opening Doors to Affordable Mixed-Use Development 1 Housing Colorado October 5, 2016 2 Session Objectives Learn: The Basics of Low-Income and Historic Tax Credits, including recent Colorado LIHTC program

Opening Doors to Affordable Mixed-Use Development 1 Housing Colorado October 5, 2016 2 Session Objectives Learn: The Basics of Low-Income and Historic Tax Credits, including recent Colorado LIHTC program

Planning Successful Historic Tax Credit Rehabilitation Projects

Lafayette Building, Butler, PA Planning Successful Historic Tax Credit Rehabilitation Projects Program overview Who uses the credit? Eligibility requirements Application and review process Best practices

Lafayette Building, Butler, PA Planning Successful Historic Tax Credit Rehabilitation Projects Program overview Who uses the credit? Eligibility requirements Application and review process Best practices

Maximizing Credits in Year 1

Maximizing Credits in Year 1 George F. Littlejohn, CPA, HCCP Novogradac & Company LLP george.littlejohn@novoco.com Let s go over Basic Concepts Multiple Building Election Minimum Set-Aside PIS Date (When

Maximizing Credits in Year 1 George F. Littlejohn, CPA, HCCP Novogradac & Company LLP george.littlejohn@novoco.com Let s go over Basic Concepts Multiple Building Election Minimum Set-Aside PIS Date (When

The Basics of Community Economic Development

The Basics of Community Economic Development May 25, 2017 Presented by: Lillian Plata, Esq., MS&B Jong Sook Nee, Esq., MS&B Amelia Rideau, Esq., PNC Bank, N.A. The Basics of Community Economic Development

The Basics of Community Economic Development May 25, 2017 Presented by: Lillian Plata, Esq., MS&B Jong Sook Nee, Esq., MS&B Amelia Rideau, Esq., PNC Bank, N.A. The Basics of Community Economic Development

Welcome to the 9 th Annual Spring Housing Conference

Welcome to the 9 th Annual Spring Housing Conference Session One: The Washington Update 1 Opportunity In Focus: Latest Pronouncements from RAD/FHA Update Session Two: QOZ s Optimizing Opportunities 2 Qualified

Welcome to the 9 th Annual Spring Housing Conference Session One: The Washington Update 1 Opportunity In Focus: Latest Pronouncements from RAD/FHA Update Session Two: QOZ s Optimizing Opportunities 2 Qualified

Mastering Partnership Minimum Gain Chargeback Provisions for the Tax Professional

FOR LIVE PROGRAM ONLY Mastering Partnership Minimum Gain Chargeback Provisions for the Tax Professional THURSDAY, JULY 6, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program

FOR LIVE PROGRAM ONLY Mastering Partnership Minimum Gain Chargeback Provisions for the Tax Professional THURSDAY, JULY 6, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program

AFFORDABLE HOUSING 101. Jimmy McCune - OCCH Tim Swiney Wallick Communities Roy Lowenstein Lowenstein Development

AFFORDABLE HOUSING 101 Jimmy McCune - OCCH Tim Swiney Wallick Communities Roy Lowenstein Lowenstein Development Affordability in Housing Defined Generally refers to housing affordable to those who earn

AFFORDABLE HOUSING 101 Jimmy McCune - OCCH Tim Swiney Wallick Communities Roy Lowenstein Lowenstein Development Affordability in Housing Defined Generally refers to housing affordable to those who earn

Innovations in Solar Financing for Non-Profits and Affordable Housing CESA Workshop on Deploying Solar in Public and Affordable Housing

Innovations in Solar Financing for Non-Profits and Affordable Housing CESA Workshop on Deploying Solar in Public and Affordable Housing Bracken Hendricks CEO, Urban Ingenuity October 17, 2017 Ingenuity

Innovations in Solar Financing for Non-Profits and Affordable Housing CESA Workshop on Deploying Solar in Public and Affordable Housing Bracken Hendricks CEO, Urban Ingenuity October 17, 2017 Ingenuity

DIFFERENCES BETWEEN THE HISTORIC REHABILITATION TAX CREDIT AND THE LOW-INCOME HOUSING TAX CREDIT

DIFFERENCES BETWEEN THE HISTORIC REHABILITATION TAX CREDIT AND THE LOW-INCOME HOUSING TAX CREDIT Andrew S. Potts NIXON PEABODY LLP 401 Ninth Street NW Washington, D.C. 20004 apotts@nixonpeabody.com. 202-585-8337

DIFFERENCES BETWEEN THE HISTORIC REHABILITATION TAX CREDIT AND THE LOW-INCOME HOUSING TAX CREDIT Andrew S. Potts NIXON PEABODY LLP 401 Ninth Street NW Washington, D.C. 20004 apotts@nixonpeabody.com. 202-585-8337

development + acquisitions

development + acquisitions What are development + acquisitions? What do those people do? How long does it really take? Who are lenders + equity investors? And why are there always problems? current portfolio.

development + acquisitions What are development + acquisitions? What do those people do? How long does it really take? Who are lenders + equity investors? And why are there always problems? current portfolio.

By Delphine G. Carnes

2014 LEGAL SEMINAR By Delphine G. Carnes Crenshaw, Ware & Martin, P.L.C. WHY RAD? Enormous backlog in needed renovations to public housing units Insufficient federal funding HOPE VI and CNI are no longer

2014 LEGAL SEMINAR By Delphine G. Carnes Crenshaw, Ware & Martin, P.L.C. WHY RAD? Enormous backlog in needed renovations to public housing units Insufficient federal funding HOPE VI and CNI are no longer

Real Estate & REIT Modeling: Quiz Questions Module 1 Accounting, Overview & Key Metrics

Real Estate & REIT Modeling: Quiz Questions Module 1 Accounting, Overview & Key Metrics 1. How are REITs different from normal companies? a. Unlike normal companies, REITs are not required to pay income

Real Estate & REIT Modeling: Quiz Questions Module 1 Accounting, Overview & Key Metrics 1. How are REITs different from normal companies? a. Unlike normal companies, REITs are not required to pay income

Building Wealth With Real Estate

Building Wealth With Real Estate - Broker/Property Manager/Loan Officer Goal of My Presentation- Understand These Topics 2 How To Build Wealth And Retire Sooner Types of Income Income Tax Rates Cash Flow

Building Wealth With Real Estate - Broker/Property Manager/Loan Officer Goal of My Presentation- Understand These Topics 2 How To Build Wealth And Retire Sooner Types of Income Income Tax Rates Cash Flow

Subject to the following limitations: 40 years on a fully amortizing basis. Subject to market conditions.

HUD SECTION 221(D)4 MORTGAGE INSURANCE PROGRAM FOR NEW CONSTRUCTION AND SUBSTANTIAL REHABILITATION OF MARKET RATE RENTAL HOUSING Cambridge Realty Capital Companies and the HUD Section 221(d)4 Program provide

HUD SECTION 221(D)4 MORTGAGE INSURANCE PROGRAM FOR NEW CONSTRUCTION AND SUBSTANTIAL REHABILITATION OF MARKET RATE RENTAL HOUSING Cambridge Realty Capital Companies and the HUD Section 221(d)4 Program provide

PACE is transforming energy and water performance

PACE is transforming energy and water performance Property Assessed Clean Energy (PACE) is a government financing policy that classifies building energy-improvement upgrades as a public benefit like a

PACE is transforming energy and water performance Property Assessed Clean Energy (PACE) is a government financing policy that classifies building energy-improvement upgrades as a public benefit like a

EXECUTIVE SUMMARY PARTNERSHIP INFORMATION PARTNERSHIP NAME: GENERAL PARTNER: GUARANTOR: PROPERTY INFORMATION

EXECUTIVE SUMMARY PARTNERSHIP INFORMATION PARTNERSHIP NAME: GENERAL PARTNER: GUARANTOR: PROPERTY INFORMATION PROPERTY NAME: PROPERTY LOCATION: PROPERTY TYPE Rural Urban Suburban CONSTRUCTION TYPE: New

EXECUTIVE SUMMARY PARTNERSHIP INFORMATION PARTNERSHIP NAME: GENERAL PARTNER: GUARANTOR: PROPERTY INFORMATION PROPERTY NAME: PROPERTY LOCATION: PROPERTY TYPE Rural Urban Suburban CONSTRUCTION TYPE: New

Federal Rehabilitation Tax Credit

Federal Rehabilitation Tax Credit Wilmington, NC February 11,2008 IRS National Coordinator Colleen Gallagher Bloomington, MN Colleen.k.gallagher@irs.gov 651-726-1480 Advice Advice Oral or Written Advice

Federal Rehabilitation Tax Credit Wilmington, NC February 11,2008 IRS National Coordinator Colleen Gallagher Bloomington, MN Colleen.k.gallagher@irs.gov 651-726-1480 Advice Advice Oral or Written Advice

9% Low Income Housing Tax Credits Pre-Applications with Texas Department of Housing and Community Affairs for 2008 Funding Year.

9% Low Income Housing Tax Credits Pre-Applications with Texas Department of Housing and Community Affairs for 2008 Funding Year A Briefing To The Housing Committee Housing Department February 4, 2008 Purpose

9% Low Income Housing Tax Credits Pre-Applications with Texas Department of Housing and Community Affairs for 2008 Funding Year A Briefing To The Housing Committee Housing Department February 4, 2008 Purpose

UNIT INFORMATION (Complete the yellow-shaded areas) Gross monthly rent per. # of baths

Gross monthly rent per. # of baths") Project Name: Project #: UNIT INFORMATION (Complete the yellowshaded areas) Residential Finished Sq. Ft. per unit* Gross monthly rent per Less tenant paid Net monthly rent per # of bedrooms per unit #

Project Name: Project #: UNIT INFORMATION (Complete the yellowshaded areas) Residential Finished Sq. Ft. per unit* Gross monthly rent per Less tenant paid Net monthly rent per # of bedrooms per unit #

Broker. Investment Real Estate. Chapter 15. Copyright Gold Coast Schools 1

Broker Chapter 15 Investment Real Estate Copyright Gold Coast Schools 1 Learning Objectives Matching an investor with the right property Evaluating the sites and improvements of income properties Determining

Broker Chapter 15 Investment Real Estate Copyright Gold Coast Schools 1 Learning Objectives Matching an investor with the right property Evaluating the sites and improvements of income properties Determining

Investment Terms. Glossary

Investment Terms Glossary DOOR Industry term used instead of Unit. T 12 Trailing 12 P&L (Profit & Loss). T 3 Trailing 3 P&L (Profit & Loss). PRO FORMA/UNDERWRITING Industry term referring to financially

Investment Terms Glossary DOOR Industry term used instead of Unit. T 12 Trailing 12 P&L (Profit & Loss). T 3 Trailing 3 P&L (Profit & Loss). PRO FORMA/UNDERWRITING Industry term referring to financially

Agenda. District of Columbia Housing Finance Agency Before Stimulus and Current Market Conditions. DCHFA Deal Types DCHFA Team

Doing Business with the NEW DCHFA Harry D. Sewell, Executive Director May 25, 2010 Agenda Before Stimulus and Current Market Conditions New Issue Bond Program DCHFA Deal Types DCHFA Team Getting Started

Doing Business with the NEW DCHFA Harry D. Sewell, Executive Director May 25, 2010 Agenda Before Stimulus and Current Market Conditions New Issue Bond Program DCHFA Deal Types DCHFA Team Getting Started

WELCOME Multifamily Housing Seminar: Trends & Topics for Developers and Owners

WELCOME Multifamily Housing Seminar: Trends & Topics for Developers and Owners May 8, 2013 TAX ABATEMENT FOR HOUSING INCENTIVES May 8, 2013 Charles Renner Husch Blackwell LLP 1 Tax Abatement/Exemption

WELCOME Multifamily Housing Seminar: Trends & Topics for Developers and Owners May 8, 2013 TAX ABATEMENT FOR HOUSING INCENTIVES May 8, 2013 Charles Renner Husch Blackwell LLP 1 Tax Abatement/Exemption

Social Housing Seminar. 26 April 2018

Social Housing Seminar 26 April 2018 Welcome Vanessa Byrne, Partner & Co Head, Real Estate, Mason Hayes & Curran Private Sector Delivery Mechanisms Nicola Byrne, Partner, Mason Hayes & Curran Social Housing

Social Housing Seminar 26 April 2018 Welcome Vanessa Byrne, Partner & Co Head, Real Estate, Mason Hayes & Curran Private Sector Delivery Mechanisms Nicola Byrne, Partner, Mason Hayes & Curran Social Housing

Section 8: Low Income Housing Tax Credit Program Description and Requirements

Section 8: Low Income Housing Tax Credit Program Description and Requirements 2010 Consolidated Funding Cycle Application LIHTC Program Description & Requirements - Page 1 of 25 LOW INCOME HOUSING TAX

Section 8: Low Income Housing Tax Credit Program Description and Requirements 2010 Consolidated Funding Cycle Application LIHTC Program Description & Requirements - Page 1 of 25 LOW INCOME HOUSING TAX

1173 Fortune Boulevard, Shiloh, Illinois Office (618) Fax (618)

Fax (618)") 6,240 Sq. Ft 2 levels 100% Leased to Long Term Tenants 10.22% CAP Rate based on actual Low Operating Expenses New Roof & Remodeled 1 st Floor Located in Copper Bend Sale: $550,000 ($88.14 per Sq. Ft.)

6,240 Sq. Ft 2 levels 100% Leased to Long Term Tenants 10.22% CAP Rate based on actual Low Operating Expenses New Roof & Remodeled 1 st Floor Located in Copper Bend Sale: $550,000 ($88.14 per Sq. Ft.)

OKI Solar Ready Workshop Frisch s Education Center Cincinnati Zoo

OKI Solar Ready Workshop Frisch s Education Center Cincinnati Zoo Approach to Solar Energy PPA Project Finance John Merritt PNC Energy Capital, LLC 3/6/15 Solar Energy Projects: An Attractive Investment

OKI Solar Ready Workshop Frisch s Education Center Cincinnati Zoo Approach to Solar Energy PPA Project Finance John Merritt PNC Energy Capital, LLC 3/6/15 Solar Energy Projects: An Attractive Investment

THE APPRAISAL OF REAL ESTATE 3 RD CANADIAN EDITION BUSI 330

THE APPRAISAL OF REAL ESTATE 3 RD CANADIAN EDITION BUSI 330 REVIEW NOTES by CHUCK DUNN CHAPTER 20 Copyright 2010 by the Real Estate Division and Chuck Dunn. All rights reserved CHAPTER 20 - THE INCOME

THE APPRAISAL OF REAL ESTATE 3 RD CANADIAN EDITION BUSI 330 REVIEW NOTES by CHUCK DUNN CHAPTER 20 Copyright 2010 by the Real Estate Division and Chuck Dunn. All rights reserved CHAPTER 20 - THE INCOME

National Housing Trust Fund. Alissa Ice Missouri Housing Development Commission

National Housing Trust Fund Alissa Ice Missouri Housing Development Commission Purpose The National Housing Trust Fund (HTF) is a new affordable housing production program that will complement existing

National Housing Trust Fund Alissa Ice Missouri Housing Development Commission Purpose The National Housing Trust Fund (HTF) is a new affordable housing production program that will complement existing

CPACE Financing Overview

CPACE Financing Overview Commercial Property Assessed Clean Energy (CPACE) Introduction CPACE is an innovative financing tool that enables building owners to fund 100% of the cost of energy efficiency

CPACE Financing Overview Commercial Property Assessed Clean Energy (CPACE) Introduction CPACE is an innovative financing tool that enables building owners to fund 100% of the cost of energy efficiency

Funding Strategies for. Developing and Operating Extremely Low Income Housing

Funding Strategies for Developing and Operating Extremely Low Income Housing NLIHC Senior Advisor Ed Gramlich NLIHC COO Paul Kealey Former Homes for America President and CEO Nancy Rase Community Frameworks

Funding Strategies for Developing and Operating Extremely Low Income Housing NLIHC Senior Advisor Ed Gramlich NLIHC COO Paul Kealey Former Homes for America President and CEO Nancy Rase Community Frameworks

Combining NMTCs with LIHTCs. NH&RA 2008 Summer Institute

Combining NMTCs with LIHTCs NH&RA 2008 Summer Institute The Myth NMTCs and LIHTCs are mutually exclusive tax credits. Questions to Consider What are the statutory or regulatory prohibitions regarding low-income

Combining NMTCs with LIHTCs NH&RA 2008 Summer Institute The Myth NMTCs and LIHTCs are mutually exclusive tax credits. Questions to Consider What are the statutory or regulatory prohibitions regarding low-income

Eligible HOME & HTF Activities Chapter 2

Eligible HOME & HTF Activities Chapter 2 (Red font indicates changes) TABLE OF CONTENTS RENTAL Housing Activities... 6 Minimum/Maximum HOME and HTF Per-unit Subsidy... 6 mber of Assisted Projects and Funding...

Eligible HOME & HTF Activities Chapter 2 (Red font indicates changes) TABLE OF CONTENTS RENTAL Housing Activities... 6 Minimum/Maximum HOME and HTF Per-unit Subsidy... 6 mber of Assisted Projects and Funding...

Preserving and recapitalizing Affordable housing today

Preserving and recapitalizing Affordable housing today A Webinar sponsored by Multi-Housing News June 4, 2015 David A. Smith dsmith@recapadvisors.com +1 (617) 502-5913 Slide 1, 6/4/2015 The Game of Homes

Preserving and recapitalizing Affordable housing today A Webinar sponsored by Multi-Housing News June 4, 2015 David A. Smith dsmith@recapadvisors.com +1 (617) 502-5913 Slide 1, 6/4/2015 The Game of Homes

Distributions In General

Distributions In General Current Distributions 15-4 Liquidating Distributions Money Property 15-5 Proportionate v. Disproportionate Distributions Example 15-1 15-5 4 Example 15-1 15-5 Partnership Assets

Distributions In General Current Distributions 15-4 Liquidating Distributions Money Property 15-5 Proportionate v. Disproportionate Distributions Example 15-1 15-5 4 Example 15-1 15-5 Partnership Assets

Funding Strategies for. Developing and Operating Extremely Low Income Housing

Funding Strategies for Developing and Operating Extremely Low Income Housing 1 NLIHC Senior Advisor Ed Gramlich NLIHC COO Paul Kealey Supportive Housing Network of NY Member Services Coordinator Steve

Funding Strategies for Developing and Operating Extremely Low Income Housing 1 NLIHC Senior Advisor Ed Gramlich NLIHC COO Paul Kealey Supportive Housing Network of NY Member Services Coordinator Steve

CRE Proforma Development Project Summary of Before Tax Cash Flows by Year

CRE Proforma Development Project Input Data Marginal Tax Bracket 25.0% Mortgage LTV 75% Developer Cost of Carry 15.0% Depn Recovery Rate 20.0% Amort Term (Years) 30 Going Out Cap Rate 9.0% Capital Gain

CRE Proforma Development Project Input Data Marginal Tax Bracket 25.0% Mortgage LTV 75% Developer Cost of Carry 15.0% Depn Recovery Rate 20.0% Amort Term (Years) 30 Going Out Cap Rate 9.0% Capital Gain

REVISED REPORT TO THE HOUSING AUTHORITY OF SAN DIEGO

REVISED REPORT TO THE HOUSING AUTHORITY OF SAN DIEGO DATE ISSUED: October 3, 2016 REPORT NO: HAR16-035 ATTENTION: SUBJECT: Chair and Members of the Housing Authority of the City of San Diego For the Agenda

REVISED REPORT TO THE HOUSING AUTHORITY OF SAN DIEGO DATE ISSUED: October 3, 2016 REPORT NO: HAR16-035 ATTENTION: SUBJECT: Chair and Members of the Housing Authority of the City of San Diego For the Agenda

Housing Trust Fund Developer Advisory Group. Options and Considerations Related to the HTF Operating Assistance and Operating Assistance Reserves

Housing Trust Fund Developer Advisory Group Options and Considerations Related to the HTF Operating Assistance and Operating Assistance Reserves The national HTF Developers Advisory Group (http://bit.ly/1sj1uop)

Housing Trust Fund Developer Advisory Group Options and Considerations Related to the HTF Operating Assistance and Operating Assistance Reserves The national HTF Developers Advisory Group (http://bit.ly/1sj1uop)

PANEL OVERVIEW. Housing Credit 101: The Development Process

Thomas Giblin Partner Nixon Peabody LLP tgiblin@nixonpeabody.com Housing Credit 101 The Development Process Patrick Sheridan Executive Vice President, Housing Volunteers of America psheridan@voa.org Terry

Thomas Giblin Partner Nixon Peabody LLP tgiblin@nixonpeabody.com Housing Credit 101 The Development Process Patrick Sheridan Executive Vice President, Housing Volunteers of America psheridan@voa.org Terry

Draft Roosevelt Income Restricted Housing Analysis

APPENDIX F Draft Roosevelt Income Restricted Housing Analysis Prepared for: Presented by: Sound Transit May 5, 2016 C/o Jeff Lehman, KPFF 1601 5th Avenue, Suite1600 Seattle, WA 98101 (206) 622 5822 Jeff.Lehman@kpff.com

APPENDIX F Draft Roosevelt Income Restricted Housing Analysis Prepared for: Presented by: Sound Transit May 5, 2016 C/o Jeff Lehman, KPFF 1601 5th Avenue, Suite1600 Seattle, WA 98101 (206) 622 5822 Jeff.Lehman@kpff.com

Delaware State Housing Authority Low Income Housing Tax Credit Guidelines

2019 Delaware State Housing Authority Low Income Housing Tax Credit Guidelines 1. Underwriting Guidelines 2. Funding Supplement 3. Design and Construction / Rehabilitation Standards 4. Capital Needs Assessment

2019 Delaware State Housing Authority Low Income Housing Tax Credit Guidelines 1. Underwriting Guidelines 2. Funding Supplement 3. Design and Construction / Rehabilitation Standards 4. Capital Needs Assessment

Real Estate Contributions to REITs Tax, Legal and Securities Laws Considerations

Real Estate Contributions to REITs Tax, Legal and Securities Laws Considerations Stephanie Smith, USDA, Washington DC Theodore Grannatt, McCarter English, Boston, MA Christopher Roman, Fried Frank, NY,

Real Estate Contributions to REITs Tax, Legal and Securities Laws Considerations Stephanie Smith, USDA, Washington DC Theodore Grannatt, McCarter English, Boston, MA Christopher Roman, Fried Frank, NY,

Impact of lease accounting changes to corporate real estate

Impact of lease accounting changes to corporate real estate Overview In February 2016, the Financial Accounting Standards Board (FASB) issued its long-awaited revision to lease accounting Accounting Standards

Impact of lease accounting changes to corporate real estate Overview In February 2016, the Financial Accounting Standards Board (FASB) issued its long-awaited revision to lease accounting Accounting Standards

Final Repair Regulations and the Impact on Owners of Investment Real Estate

Tom Scarpello Managing Partner 877.410.5040 Final Repair Regulations and the Impact on Owners of Investment Real Estate On September 13, 2013, the IRS released final regulations providing comprehensive

Tom Scarpello Managing Partner 877.410.5040 Final Repair Regulations and the Impact on Owners of Investment Real Estate On September 13, 2013, the IRS released final regulations providing comprehensive

San Diego Housing Commission Preliminary Bond Authorization for Mariner s Village November 30, 2018

Preliminary Bond Authorization for Mariner s Village November 30, 2018 Tina Kessler Housing Programs Manager Real Estate Division Recommendations That the (SDHC): 1. Enter into an Option to Ground Lease

Preliminary Bond Authorization for Mariner s Village November 30, 2018 Tina Kessler Housing Programs Manager Real Estate Division Recommendations That the (SDHC): 1. Enter into an Option to Ground Lease

Managing a Section 8, Section 236, PRAC/LIHTC Project

Managing a Section 8, Section 236, PRAC/LIHTC Project www.lizbramletconsulting.com www.lbctrainingcenter.com www.lizbramlet.wordpress.com HUD-Assisted Projects and LIHTC Across the country, owners are

Managing a Section 8, Section 236, PRAC/LIHTC Project www.lizbramletconsulting.com www.lbctrainingcenter.com www.lizbramlet.wordpress.com HUD-Assisted Projects and LIHTC Across the country, owners are

OFFERING MEMORANDUM FOR INVESTORS LOOKING for a LEGITIMATE 10%+ IRR YIELD

OFFERING MEMORANDUM FOR INVESTORS LOOKING for a LEGITIMATE 10%+ IRR YIELD Property has years of 100% occupancy with waiting list Av. length of stay about 7 years, some as long as 16, some 2 nd generation

OFFERING MEMORANDUM FOR INVESTORS LOOKING for a LEGITIMATE 10%+ IRR YIELD Property has years of 100% occupancy with waiting list Av. length of stay about 7 years, some as long as 16, some 2 nd generation

Title Insurance & Leasehold Estates By: Yosi (Joe) Benlevi VP & Senior Underwriting Counsel

Benlevi VP & Senior Underwriting Counsel") By: Yosi (Joe) Benlevi VP & Senior Underwriting Counsel Title Insurance and Leasehold Estates a short history The 1975 leasehold policy Covers for increased cost of leasing an alternate space and limited

By: Yosi (Joe) Benlevi VP & Senior Underwriting Counsel Title Insurance and Leasehold Estates a short history The 1975 leasehold policy Covers for increased cost of leasing an alternate space and limited

INSTRUCTIONS ON HOW TO FILL OUT THE NEIGHBORHOOD LANDLORD APPLICATION

INSTRUCTIONS ON HOW TO FILL OUT THE NEIGHBORHOOD LANDLORD APPLICATION Example of a Potential Application: Landlord will be rehabbing or constructing a total of seven units in the application. 1 unit is

INSTRUCTIONS ON HOW TO FILL OUT THE NEIGHBORHOOD LANDLORD APPLICATION Example of a Potential Application: Landlord will be rehabbing or constructing a total of seven units in the application. 1 unit is

HOME Investment Partnerships (HOME) Program Funding Application

Program Funding Application") HOME Investment Partnerships (HOME) Program Funding Application City of New Rochelle Department of Development 515 North Avenue New Rochelle, NY 10801 May 2016 HOME FUNDING APPLICATION INTRODUCTION AND

HOME Investment Partnerships (HOME) Program Funding Application City of New Rochelle Department of Development 515 North Avenue New Rochelle, NY 10801 May 2016 HOME FUNDING APPLICATION INTRODUCTION AND

April 1, 2014 thru June 30, 2014 Performance Report

Grantee: Grant: Prince Georges County, MD B-11-UN-24-0002 April 1, 2014 thru June 30, 2014 Performance Report 1 Grant Number: B-11-UN-24-0002 Grantee Name: Prince Georges County, MD Grant Award Amount:

Grantee: Grant: Prince Georges County, MD B-11-UN-24-0002 April 1, 2014 thru June 30, 2014 Performance Report 1 Grant Number: B-11-UN-24-0002 Grantee Name: Prince Georges County, MD Grant Award Amount:

Family Office Real Estate

Family Office Real Estate Presented By Richard C. Wilson Sponsored by the Family Office Club & the Endowment Fund Association (EFA) The Family Office Club is the largest family office association globally

Family Office Real Estate Presented By Richard C. Wilson Sponsored by the Family Office Club & the Endowment Fund Association (EFA) The Family Office Club is the largest family office association globally

Analysis of a Troubled Deal. Keith Broadnax Joshua Ghena David Helm Josh White

Analysis of a Troubled Deal Keith Broadnax Joshua Ghena David Helm Josh White Identifying a Troubled Deal How to Spot and Fix Problem Deals Introduction to Presenters Josh Ghena- Lansing MI Director Special

Analysis of a Troubled Deal Keith Broadnax Joshua Ghena David Helm Josh White Identifying a Troubled Deal How to Spot and Fix Problem Deals Introduction to Presenters Josh Ghena- Lansing MI Director Special

ATTACHMENT A 2018 RESERVATION FEDERAL LOW INCOME RENTAL HOUSING TAX CREDIT PROGRAM CARRYOVER ALLOCATION REQUIREMENTS

ATTACHMENT A 2018 RESERVATION FEDERAL LOW INCOME RENTAL HOUSING TAX CREDIT PROGRAM CARRYOVER ALLOCATION REQUIREMENTS PART I The following requirements must be received in hard copy by the Agency by November

ATTACHMENT A 2018 RESERVATION FEDERAL LOW INCOME RENTAL HOUSING TAX CREDIT PROGRAM CARRYOVER ALLOCATION REQUIREMENTS PART I The following requirements must be received in hard copy by the Agency by November

U.S. Housing Act of 1937

SERC/NAHRO Conference Norfolk, Virginia June 25, 2018 U.S. Housing Act of 1937 Another New Deal initiative designed to relieve conditions in the nation's housing stock This was the beginning of Public

SERC/NAHRO Conference Norfolk, Virginia June 25, 2018 U.S. Housing Act of 1937 Another New Deal initiative designed to relieve conditions in the nation's housing stock This was the beginning of Public

Request for Proposals Wake County Affordable Housing Development Program for Tax Credit Developments

2015 Request for Proposals Wake County Affordable Housing Development Program for Tax Credit Developments 1) STATEMENT OF PURPOSE AND PROGRAM SUMMARY Wake County s Department of Housing and Community Revitalization

2015 Request for Proposals Wake County Affordable Housing Development Program for Tax Credit Developments 1) STATEMENT OF PURPOSE AND PROGRAM SUMMARY Wake County s Department of Housing and Community Revitalization

AAII Los Angeles Chapter Saturday Meeting Investment Seminar at the Skirball Center, September 15, 2012 TODD RUBINSTEIN

AAII Los Angeles Chapter Saturday Meeting Investment Seminar at the Skirball Center, September 15, 2012 TODD RUBINSTEIN S ENIOR PARTNER Rubinstein Group at TOLD Partners 818-601-7200 ToddR@told.com ToddR@realtor.com

AAII Los Angeles Chapter Saturday Meeting Investment Seminar at the Skirball Center, September 15, 2012 TODD RUBINSTEIN S ENIOR PARTNER Rubinstein Group at TOLD Partners 818-601-7200 ToddR@told.com ToddR@realtor.com

REPORT. DATE ISSUED: December 19, 2014 REPORT NO: HCR Chair and Members of the San Diego Housing Commission For the Agenda of January 16, 2015

REPORT DATE ISSUED: December 19, 2014 REPORT NO: HCR15-008 ATTENTION: SUBJECT: Chair and Members of the San Diego Housing Commission For the Agenda of January 16, 2015 COUNCIL DISTRICT: 9 REQUESTED ACTION

REPORT DATE ISSUED: December 19, 2014 REPORT NO: HCR15-008 ATTENTION: SUBJECT: Chair and Members of the San Diego Housing Commission For the Agenda of January 16, 2015 COUNCIL DISTRICT: 9 REQUESTED ACTION

DATE: TO OWNER: Washington State Housing Finance Commission Low-Income Housing Tax Credit Program 1000 Second Avenue Suite 2700 Seattle WA

INDEPENDENT CERTIFIED PUBLIC ACCOUNTANT'S REPORT on CARRYOVER ALLOCATION BASIS PURSUANT TO IRS SECTION 42 (h)(1)(e)(ii) and AMERICAN RECOVERY AND REINVESTMENT ACT (ARRA) EXCHANGE PROGRAM 30% TEST PURSUANT

INDEPENDENT CERTIFIED PUBLIC ACCOUNTANT'S REPORT on CARRYOVER ALLOCATION BASIS PURSUANT TO IRS SECTION 42 (h)(1)(e)(ii) and AMERICAN RECOVERY AND REINVESTMENT ACT (ARRA) EXCHANGE PROGRAM 30% TEST PURSUANT