ECOLOGICAL GIFTS PROGRAM

|

|

|

- Miles Potter

- 5 years ago

- Views:

Transcription

1 ECOLOGICAL GIFTS PROGRAM Laura Kucey, Environment Canada David Babineau, Appraisal Review Panel Chair OLTA GATHERING OCTOBER 2015

2 INTRODUCTIONS AND OVERVIEW Ontario EGP staff changes Presentation Overview Program goals Ontario gift specifics Program process overview focus on common questions Appraisal Review Panel Open Q&A Audience choice of topics: Conservation Easement Agreements Change in Use / Disposition requests Ownership Split receipting Page 2 - October 2015

3 DISCLAIMER Not providing advice. Simplified information for educational purposes EVERY SITUATION AND EACH PROPOSED GIFT IS UNIQUE! Tax questions? Call your financial planner. Accounting questions? Call your accountant. Legal Questions? Call your lawyer. Page 3 - October 2015

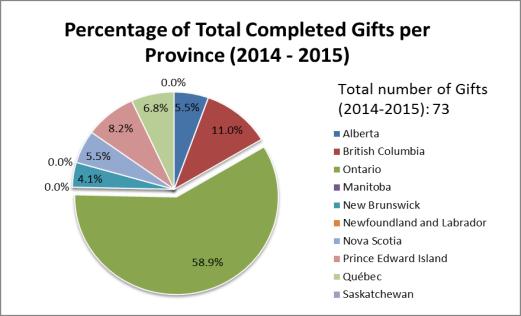

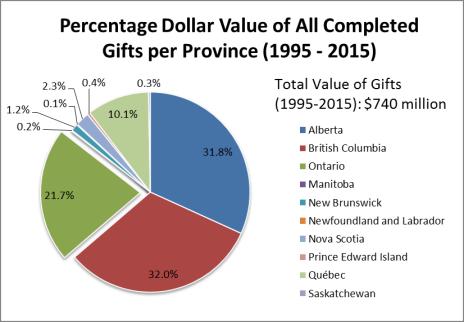

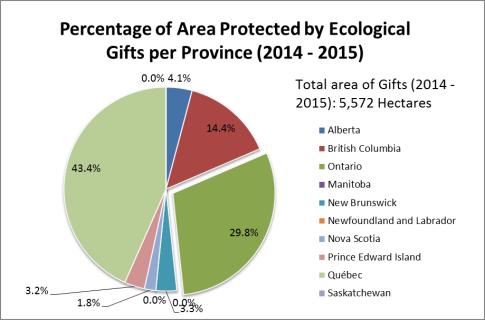

4 ECOLOGICAL GIFTS PROGRAM (EGP) Federal program made possible by the Income Tax Act Administered by Environment Canada in cooperation with many partners Landowners with ecologically sensitive land - significant tax benefits - contribute to the protection of biodiversity Qualified Recipients - ensure that the land s biodiversity and environmental heritage are conserved As of October 1, 2015: 1184 Ecological Gifts valued at over $741 million have been donated across Canada, protecting over 171,110 hectares Of these, 477 gifts valued at over $160 million were donated in Ontario Page 4 - October 2015

5 ONTARIO NUMBERS Current files: 47 open files 21 different recipients About a 65 / 35% split on fee simple vs. conservation easements A few on hold 19+ additional proposed gifts that recipients have mentioned will be coming to the program soon To date, 13 gifts have been completed in Ontario (SFMV issued) in 2015 Page 5 - October 2015

6 Page 6 - October 2015

7 Page 7 - October 2015

8 Page 8 - October 2015

9 Page 9 - October 2015

10 Page 10 - October 2015

11 Page 11 - October 2015

12 WHAT CONSTITUTES A GIFT? Donation must fully qualify as a gift under Canadian tax law: donor transfers ownership of /interest in property to a qualified recipient the transfer is voluntary no benefit is provided to the donor (or person selected by the donor) Question about whether the donation qualifies as a gift for tax purposes? Contact tax and legal advisors! Advance ruling possible from CRA (donor/recipient responsibility) EGP does not assess whether the donation qualifies as a gift under the Income Tax Act Page 12 - October 2015

")

13 TAX INCENTIVES For most gifts the taxable portion is 50% of the capital gain, BUT this is reduced to 0 for certified Ecological Gifts Non-refundable tax credit for individuals Tax deduction for corporate donors Any unused portion of the donation can be carried forward for 10 years (applies to gifts made on or after Feb 11, 2014) Page 13 - October 2015

14 RECIPIENTS Responsible for maintaining the biodiversity and environmental heritage values of the property May also help with initial assessment of the property's ecological sensitivity, arranging for an appraisal, and coordinating the necessary applications Currently more than 150 eligible recipients across Canada Environmental charities approved by the federal Minister of the Environment (land and heritage trusts, nature conservation groups) federal, provincial, territorial and municipal governments Page 14 - October 2015

15 EGP STRUCTURE Independent Appraisal Review Panel (across Canada) EGP National Secretariat (EC Ottawa) PYR Regional Coordinator PNR Regional Coordinators Ontario Regional Coordinators Québec Regional Coordinator Atlantic Regional Coordinator (Vancouver) (Winnipeg and Edmonton) (Toronto) (Québec City) (Sackville) Donors and Recipients Page 15 - October 2015

16 PROGRAM PROCESS Number of steps arranging the donation preparing information on ecological sensitivity and property appraisal appraisal review and determination of the fair market value of the donation Donor will receive: Certificate of Ecologically Sensitive Land Statement of Fair Market Value Official donation receipt from the recipient All three must be included with donor s income tax return Page 16 - October 2015

17 PROGRAM TIMING It can take several months to arrange a donation Up to six months or longer to work through the certifications PROGRAM TIMING IS DEPENDENT ON FULL AND COMPLETE SUBMISSIONS TO THE EGP Donors are advised to apply to the Ecological Gifts Program as early in the year as possible if they wish to use their ecological gift tax benefits that same year Regional Coordinators are available to help throughout the Ecological Gifts Program process Page 17 - October 2015

18 Donor / Recipient steps Timelines self dependent Ecological Sensitivity Submission Environment Canada steps Estimated timelines IF FULL AND COMPLETE SUBMISSIONS ARE RECEIVED Ecological Sensitivity Review Certificate of Ecological Sensitivity issued less than 3 weeks Appraisal & Application Submission Regional Appraisal Review National Secretariat Appraisal Review 2 weeks SIMPLIFIED EGP PROCESS AND TIMING Appraisal Review Panel Review and Recommendation Notice of Determination issued within 90 days Notice signed and returned to EC Land Transfer / Closing documents submitted to EC Complete File Review Statement of Fair Market Value issued 2 weeks Page 18 - October 2015

19 Donor / Recipient steps Timelines self dependent Ecological Sensitivity Submission Environment Canada steps Estimated timelines IF FULL AND COMPLETE SUBMISSIONS ARE RECEIVED Ecological Sensitivity Review Certificate of Ecological Sensitivity issued less than 3 weeks Appraisal & Application Submission Regional Appraisal Review National Secretariat Appraisal Review 2 weeks SIMPLIFIED EGP PROCESS AND TIMING Appraisal Review Panel Review and Recommendation Notice of Determination issued within 90 days Notice signed and returned to EC Land Transfer / Closing documents submitted to EC Complete File Review Statement of Fair Market Value issued 2 weeks Page 19 - October 2015

20 Donor / Recipient steps Timelines self dependent Environment Canada steps Estimated timelines IF FULL AND COMPLETE SUBMISSIONS ARE RECEIVED Ecological Sensitivity Submission should include: 1. Donor indication of intent 2. Recipient indication of acceptance Ecological Sensitivity Review Certificate of Ecological Sensitivity issued less than 3 weeks 3. Current Title Abstract 4. Ecological Sensitivity Application - Donation type / area - Assessment of ecological character - How EGP criteria is met Regional Coordinator: opens a file reviews and substantiates ecological sensitivity submission against national and provincial criteria prepares Certificate for delegated signing If applicable: 5. Conservation Easement 6. Designated signing authority Page 20 - October 2015 ECOLOGICAL SENSITIVITY

21 Page 21 - October 2015

22 Donor / Recipient steps Timelines self dependent Environment Canada steps Estimated timelines IF FULL AND COMPLETE SUBMISSIONS ARE RECEIVED Ecological Sensitivity Submission Appraisal & Application Submission Ecological Sensitivity Review Regional Appraisal Review Certificate of Ecological Sensitivity issued National Secretariat Appraisal Review less than 3 weeks 2 weeks Appraisal Review Panel Review and Recommendation Notice of Determination issued within 90 days Notice signed and returned to EC Land Transfer / Closing documents submitted to EC Complete File Review Statement of Fair Market Value issued 2 weeks Page 22 - October 2015

23 Donor / Recipient steps Timelines self dependent Environment Canada steps Estimated timelines IF FULL AND COMPLETE SUBMISSIONS ARE RECEIVED Appraisal AND Application Submission should include: Independent appraisal of the fair market value of the proposed donation conforming to EGP guidelines Regional Appraisal Review For completeness, accuracy and compliance National Secretariat Appraisal Review 2 weeks This Application demonstrates that the donor is aware and agrees with the appraised value of the proposed donation ALL ASPECTS OF THE APPRAISAL AND APPLICATION MUST MATCH INDEPENDENT Appraisal Review Panel Review and Recommendation Notice of Determination issued within 90 days APPRAISAL REVIEW NOTICE OF DETERMINATION Following a recommendation from the ARP, the federal Minister of the Environment certifies the fair market value of the donation If ARP requires more information, a memo will be issued and timelines go on hold Page 23 - October 2015

24 Page 24 - October 2015

25 Donor / Recipient steps Timelines self dependent Ecological Sensitivity Submission Environment Canada steps Estimated timelines IF FULL AND COMPLETE SUBMISSIONS ARE RECEIVED Ecological Sensitivity Review Certificate of Ecological Sensitivity issued less than 3 weeks Appraisal & Application Submission Regional Appraisal Review National Secretariat Appraisal Review 2 weeks SIMPLIFIED EGP PROCESS AND TIMING Appraisal Review Panel Review and Recommendation Notice of Determination issued within 90 days Notice signed and returned to EC Land Transfer / Closing documents submitted to EC Complete File Review Statement of Fair Market Value issued 2 weeks Page 25 - October 2015

26 Donor / Recipient steps Timelines self dependent Environment Canada steps Estimated timelines IF FULL AND COMPLETE SUBMISSIONS ARE RECEIVED Three options for the donor: Notice of Determination NOTICE OF DETERMINATION 1. Accept fair market value as determined, notify Environment Canada in writing, and complete the donation process 2. Request a redetermination within 90 days 3. Withdraw from EGP STATEMENT OF FAIR MARKET VALUE Notice signed and returned to EC Land Transfer / Closing documents submitted to EC Complete File Review Statement of Fair Market Value issued 2 weeks Final title abstract showing that the donation has occurred Including FINAL, SIGNED, REGISTERED conservation easement, if applicable Page 26 - October 2015 The value on the Statement should appear on the donation receipt issued by the recipient

27 SAFEGUARDS FOR ECOLOGICAL GIFTS Under the provisions of the Income Tax Act s Recipients are responsible for the long term conservation of the donation Unauthorized changes in use or dispositions of ecological gifts could result in a tax of 50% of the land s current market value Page 27 - October 2015

28 Appraisal Review Panel What is the Appraisal Review Panel, or ARP? The ARP is an independent advisory body of experts who have the responsibility to review appraisal reports and make recommendations to the federal Minister of the Environment on the fair market value of ecological gifts made under the Income Tax Act. Page 28 - October 2015

29 Appraisal Review Panel Composition Who sits on the Appraisal Review Panel? At present, the Appraisal Review Panel is comprised of five permanent appraisal experts and a legal policy specialist. Each of the five permanent appraisal experts represent one of the five Environment Canada regions. In addition, there are six Ad-hoc appraisal experts (two in Ontario), who are engaged on an occasional basis, to ensure our service is delivered in the most expedient manner. Page 29 - October 2015

30 Appraisal Review Panel Process What process does the Appraisal Review Panel employ? The Appraisal Review Panel examines each appraisal report submitted in the light of the Guidelines for Appraisals and the relevant appraisal standards that are in effect. In the case of members of the Appraisal Institute of Canada, the relevant standards would be the Canadian Uniform Standards of Professional Appraisal Practice. Emphasis is on the substantive contents of the appraisal report, rather than on its format or style. Page 30 - October 2015

31 ARP Areas of Concerns What are some of the common areas of concerns that the Appraisal Review Panel encounters? The use of unsupported assumptions As stated in the Guidelines for Appraisals, no unsupported assumptions will be permitted in the preparation of appraisals, including unsupported assumptions that have an impact on highest and best use. For example, a waterfront property can be valued to reflect a marina development, if that is the highest and best use, but the use cannot simply be assumed to be the highest and best use. Page 31 - October 2015

32 ARP Areas of Concerns (cont.) The use of hypothetical conditions, except when they are necessary for a reasonable analysis of the property. For example, an appraiser may include a hypothetical condition in an appraisal of an ecological gift where the hypothetical condition is necessary to value a proposed ecological gift comprised of a new lot that is not yet subdivided from a parent parcel or a conservation easement that is not yet registered. The inclusion of unsubstantiated opinions and unsupported conclusions. This is a contravention of the Canadian Uniform Standards of Professional Appraisal Practice and the Guidelines for Appraisals. Page 32 - October 2015

33 ARP Areas of Concerns (cont.) Timing of appraisals and the update process. In accordance with the Guidelines for Appraisals, the effective date of an appraisal must be no earlier than six months before the date that the donor submits the Application for Appraisal Review and Determination. If the effective date of the appraisal is more than six months before the application is submitted, the appraiser who completed the original appraisal must verify in writing that there has been: no material change in the use of the property, and no material change to the market in the area of the subject property Page 33 - October 2015

34 ARP How you can help us help you Provide the appraiser you engage with the most complete package of information you can. This could include leads on any comparable sales data. When the Appraisal Review Panel needs clarification about an appraisal report, they will either contact the appraiser directly (if permission to do so has been granted) or issue a memorandum to the Donor for distribution to the appraiser. Please explain this part of the process to the appraisers you engage and encourage them to be as co-operative with the ARP as possible. Their prompt response to any queries will make the entire process more expedient. Page 34 - October 2015

35 ARP New Developments The Guidelines for Appraisals are in the process of being redeveloped and they will include an expanded explanation of what is required in the update process and an appraisal checklist. Thank you. Page 35 - October 2015

36 HELPFUL HINTS All parties should obtain independent legal and financial advice Make sure the appraiser has all of the right information! Find out as much information as you can about: the property EGP CALL US! Pay attention to the application you are filling in Details are important when you are working under the ITA! EGP publications are available online and through your EGP coordinator Page 36 - October 2015

37 RESOURCES Environment Canada: Confirmation that Ecogifts are Eligible for Split-Receipting Application for Appraisal Review and Determination of the Fair Market Value of an Ecological Gift: Canada Revenue Agency (CRA): Gifts and Income Tax - website Gifts and Official Donation Receipt, IT-110R3 Proposed Guidelines on Split-Receipting, Income Tax Technicial News No. 26 Page 37 - October 2015

38 NEXT PORTION OF THE PRESENTATION CHOOSE YOUR OWN ADVENTURE 1 ST : Questions so far? We likely can t cover all of the items listed below, so 2 ND : Which of the following topics would you most like to discuss: 1. Conservation Easement Agreements 2. Change in Use / Disposition requests 3. Ownership estate, multiple donors, multiple properties, US owners 4. Split-receipting Page 38 - October 2015

39 COMMON CONSERVATION EASEMENT DEFICIENCIES Using a boiler plate type of easement for unique lands All conservation easement donations should be tailored to lands and the donors needs Conservation easement that does not protect sensitive features Intent doesn t match the ecological sensitivity criteria submitted Features (trails, etc.) or zones (agricultural, protected, residential) are not indicated on the maps Incomplete or poor quality submission Not submitting final, or near final, easement with appraisal Making changes to conservation easement after the appraisal this results in serious delays as the conservation easement MUST reroute back through the EGP and the Panel for review Not submitting baseline documentation Page 39 - October 2015

Referencing requirements for Environment Canada authorization of any change in")

40 STRENGTHENING CONSERVATION EASEMENTS The better the mapping now, the easier to interpret later Consideration of specific ecological features within the easement Spending time discussing the intent of the easement Consideration of future invasive and non-native species (protection of the ecologically sensitive features) Referencing requirements for Environment Canada authorization of any change in use / disposition under the Income Tax Act and Ontario Ministry of Natural Resources and Forestry under the Conservation Land Act, 1990 Page 40 - October 2015

41 DISPOSITION OR CHANGE IN USE To seek authorization, recipients should write to the Ecological Gifts Program office in their region in advance of making any dispositions or changes in land use EGP fact sheet: Disposition or Change in Use of Ecological Gifts Questions? Call your EGP Coordinator! Page 41 - October 2015

42 CHANGE IN USE / DISPOSITION REQUEST Each request for authorization of a proposed change in use (CIU) or disposition (DISP) of an ecological gift is unique and is considered on its own merit Environment Canada takes the following into account when evaluating a request for authorization: Spirit and intent of the original donation Will CIU/DISP result in protection that is at least equal to that provided under the existing arrangement? Is the CIU/DISP request beneficial to the long term conservation and management of the ecological sensitive features on the subject lands? Is the new recipient (of DISP) eligible to receive an ecological gift? What factors are driving the CIU/DISP request? Is the CIU/DISP within the control of the recipient? Page 42 - October 2015

43 HOW TO SUBMIT YOUR CIU / DISP REQUEST Send your letter of request to your regional EGP coordinator Formal letter of request addressed to the Regional Director Include maps, supporting documentation Discussions with the EGP coordinator can help clarify the details that should be included in the letter Environment Canada will only consider written requests that provide clear details with the precise nature of the proposed CIU/DISP Provide rationale for your request Make your case and justify your rationale! Provide a full assessment of the potential effects of the proposed CIU/DISP on the ecologically sensitive features of the lands Include details of proposed activities to be undertaken and any potential restoration work Page 43 - October 2015

44 AUTHORIZING A REQUEST Authorization of your request Authorization will come in the form of a letter from the Minister s delegated authority (Regional Director, Ontario) Submit proof of completed authorized actions to the EGP Gift file will be updated to reflect the changes Included CIU/DISP details in future recipient surveys What if my request is rejected? Rational for rejection will be included in the Ministerial letter Contact your regional coordinator if you have questions Yes, you can resubmit, but your request must be different than the originally rejected request Page 44 - October 2015

?")

45 CIU / DISP QUESTIONS Can we add trails to the property at a later point in time? We are working with an older easement that doesn t allow us to remove vegetation or use herbicides. How can we get rid of dog-strangling vine? How can recipients incorporate the potential future uses on a property (such as wetland management/restoration activities)? What happens if the lands are severed from the parent parcel at donation The new landowners, not the original donors, want to change some restrictions in the conservation easement, is this allowed? Page 45 - October 2015

46 EXPROPRIATION QUESTIONS Who can help when a property is faced with potential expropriation? Responsibilities and Authorities under the EGP Under the ITA, the Minister of the Environment (EC), or a designate: Certifies the ecological sensitivity of the land (or partial interest) Approves the recipient to receive the Ecological Gift. Determines the fair market value of the donation. Recipients of Ecological Gifts are responsible for: protecting and maintaining the biodiversity and environmental heritage values of the property the long-term management and conservation of the Ecological Gift and its ecologically sensitive features Page 46 - October 2015

47 EXPROPRIATION QUESTIONS In certain situations, a disposition or change in use will be outside of the recipient s control - Expropriation is an example of this Expropriation is one of the most powerful exercises of a public authority s power EGP staff will examine a range of factors, including details relating to the expropriating authority, land impacted, and stage of the expropriating activities in relation to Ecological Gifts Recipients are expected to do everything within their powers to work with parties to minimize potential impact to ecologically sensitive features of Ecological Gifts Environment Canada will work with its partners and stakeholders to communicate the importance of conserving nature and leaving a legacy for future generations EC staff can assist and participate in discussions with recipients and expropriating parties Page 47 - October 2015

")

48 OWNERSHIP Q&A Can a corporation give a an Ecological Gift? Yes, however every situation is unique Consult the Canadian Revenue Agencies Charity Directorate for the definition of a gift All EGP documentation is issued to the corporation (legal owner on title) EGP also requires legal documentation identifying signing authority Only very specific beneficiary trusts allow for inclusion of beneficiaries on issued documents Considerations: Like private donors, corporate donors should independently verify that their donation qualifies as a gift under the Income Tax Act Donations made as a condition of development are not gifts Donations of inventory lands may qualify as ecological gifts, but they are not eligible for the capital gains exemption Page 48 - October 2015

49 OWNERSHIP Q&A Can an Estate give an Ecological Gift? Yes Please provide legal documentation supporting the signing authority for the gift (often provided via a letter from the Estate s solicitor) Make sure documents MATCH the legal donor on title If donor is recently deceased, please provide legal documentation identifying death AND legal signing authority (such as a notarized will) How does a trustee relationship work? Who do I work with? Similar to an estate donation, a name may be on title that does not match the name of the person you are working with but the donor states they are a trustee Trustee relationships must be supported by legal, formal documentation (often a notarized trustee document). Always ensure you are working with the legal owner or legal designate Page 49 - October 2015

50 TITLE ABSTRACT VS. TITLE DEED What s the difference between an abstract and a deed and what is more important for my Ecological Gift submission? TITLE DEED legal documents outlining one transaction occurring on title evidence of transfer from donor to recipient TITLE ABSTRACTS outline all transactions on title, in chronological order, i.e. title history shows the legal donor(s) AND any liens and/or encumbrances An up to date title abstract (parcel register) is required for EVERY Ecological Gift application Page 50 - October 2015

as well as verifying that the donation transaction")

51 OWNERSHIP Q&A Why do you need title abstract documents at the beginning and end of the process? The title abstract / parcel register identifies all legal donors, provides a history of the parcel (any encumbrances) as well as verifying that the donation transaction has occurred according to the original submission Page 51 - October 2015

52 OWNERSHIP Q&A Only one of the legal donors is donating, the other is receiving cash, why do you issue documents to BOTH legal owners on title? Environment Canada is obligated to issue identical legal documentation to all parties listed on title The details of how the transaction transpires (i.e. recipient receipting) is up to the donor and recipient Example, Gift ON888: Two legal donors (two landowners listed on title), Environment Canada will issue documents to donors A and B, even if only Donor A is technically making a donation Appraised value is for the entire property and title documents this is the proposed donation Both donors are on title, but only Donor A will be able to use the documents as they are the donor with the charitable receipt Donor A will file documents related to ON888A Donor B will keep or destroy their documents Ensures all legal owners are aware lands are going through the EGP Page 52 - October 2015

53 TITLE ABSTRACT BEFORE GIFT Page 53 - October 2015

54 AFTER A CONSERVATION EASEMENT Page 54 - October 2015

55 Page 55 - October 2015

56 US OWNERSHIP What if a donor is a US citizen, or a CDN living in the US? Can they still give an Ecological Gift? Short answer: YES! Long answer: different tax advantages will be realized by the donor based on whether or not the donor(s) pay Canadian income tax Even longer answer: American Friends of Canadian Land Trusts (AFCLT) has been established and has growing in experience when it comes to promoting conservation without borders Unfortunately, AFCLT is not an eligible recipient and presently gifts donated (100%) to AFCLT cannot be considered an Ecological Gift There are options of having both a Canadian land trust and AFCLT hold title; however, this leaves the Canadian land trust with the responsibilities under section (of the ITA) EGP-ON has a couple of gifts that have gone through the process Page 56 - October 2015

57 EGP RECIPIENT AND AFCLT EXAMPLES What they wanted to do: Conserve islands while maximizing donor financial benefit 4/8 of the donors, holding 40% of the interest are Americans paying only US income tax 4/8 of the donors, holding 60% of the interest are Canadian and pay CDN income tax Donors wanted to participate in the EGP Considerations: The second recipient holding the lands is NOT an eligible EGP recipient as they are not recognized as a CDN Charity by CRA Recipient organized the transaction between all parties, everything in writing, including interests in land Donors investigated interests and benefits* Page 57 - October 2015

58 OWNERSHIP DETAILS Name Share American/Canadian Mr. B 1/5 20% Canadian Ms. G 1/5 20% American Mr. M 1/5 20% Canadian Mr. S 1/ % American Mr. Sp 1/ % American Ms. S 1/ % American Mr. G Ms. G 1/10 10% 1/10 10% Canadian Canadian 4/8 interested in participating in the EGP 60% Canadian Page 58 - October 2015

59 ENVIRONMENT CANADA Verified ownership and interests Completed EGP submission review Property management and long-term conservation plan reviewed and identified timelines for land transfer Non-benefitting owners were removed from Ministerial Certificates, and Statements Entire property was appraised and reviewed Full Fair Market Value considered, recipients/donor/lawyer to verify and issue their documents as per designated interest For more information: American Friends of Canadian Land Trusts Page 59 - October 2015

60 SPLIT RECEIPTING Situation where a recipient can issue a tax receipt to a donor for an eligible amount of a gift, namely the difference in the total value of the gift and the value of any consideration that the donor received in return for the gift How does it work? Gift is appraised and certified (FMV $500K) Donor transfers land to recipient Recipient gives donor $350K in cash and $150K in the form of a charitable receipt Environment Canada issues a Statement of Fair Market Value for $500K (the full value of the gift) which is accompanied by the charitable receipt at tax filing time A split receipt donation looks the same on title as a fee simple donation Page 60 - October 2015

61 THINK OF IT LIKE THIS.. Example: FMV Gift is 500K ** Total advantage back: 350K paid by land trust to the donor Total value of the gift : 150K supported by a charitable receipt donor uses charitable receipt + SFMV + Certificate to claim Ecological Gift tax benefits **example above is overly simplified Page 61 - October 2015

62 EGP EVOLUTION Program launched in 1995 as a result of amendments to the Income Tax Act (ITA) of Canada In 2000, the Program implemented a rigorous and accountable process for determining the fair market value of Ecological Gifts In 2003, split-receipting was permitted and in 2006, taxable capital gains on Ecological Gifts were eliminated In 2007, recipient certification processes were enhanced 2013 updates to ITA and split receipting formally adopted into the Act 2014 Any unused portion of the donation can be carried forward for 10 years (applies to gifts made on or after Feb 11, 2014) Page 62 - October 2015

63 REGIONAL CONTACT Laura Kucey Environment Canada 4905 Dufferin Street Toronto, ON M3H 5T BUT changing to Page 63 - October 2015

Land and Easement Donation Process and Requirements Summary

Land and Easement Donation Process and Requirements Summary Many of the steps involved in donating land or conservation easements to American Friends of Canadian Land Trusts (AF) will be familiar to people

Land and Easement Donation Process and Requirements Summary Many of the steps involved in donating land or conservation easements to American Friends of Canadian Land Trusts (AF) will be familiar to people

Fact Sheet for Canadian Appraisers of Conservation Gifts with Cross-Border Tax Consequences

Fact Sheet for Canadian Appraisers of Conservation Gifts with Cross-Border Tax Consequences Introduction American Friends of Canadian Land Trusts (American Friends) is a U.S. 501(c)(3) publicly supported

Fact Sheet for Canadian Appraisers of Conservation Gifts with Cross-Border Tax Consequences Introduction American Friends of Canadian Land Trusts (American Friends) is a U.S. 501(c)(3) publicly supported

The Canadian ECOLOGICAL GIFTS PROGRAM HANDBOOK A legacy for tomorrow... a tax break today. Environment Canada. Environnement Canada

The Canadian ECOLOGICAL GIFTS PROGRAM HANDBOOK 2005 A legacy for tomorrow... a tax break today Environment Canada Environnement Canada February 2005 ISBN Cat No 0-662-32864-7 For more information, please

The Canadian ECOLOGICAL GIFTS PROGRAM HANDBOOK 2005 A legacy for tomorrow... a tax break today Environment Canada Environnement Canada February 2005 ISBN Cat No 0-662-32864-7 For more information, please

Council Policy Name: Policy Statement and Rationale: Scope: Council Policy No.: C205 CAO 044. Date Approved by Council: May 26, 2015

Council Policy No.: C205 CAO 044 Council Policy Name: Date Approved by Council: May 26, 2015 Date revision approved by Council: Related SOP, Management Directive, Council Policy, Form Policy Statement

Council Policy No.: C205 CAO 044 Council Policy Name: Date Approved by Council: May 26, 2015 Date revision approved by Council: Related SOP, Management Directive, Council Policy, Form Policy Statement

Our Focus: Your Future A HERITAGE PROPERTY TAX RELIEF PROGRAM FOR THE TOWN OF FORT ERIE

Town of Fort Erie Our Focus: Your Future Corporate Services Prepared for Council-in-Committee Report No. CS-24-07 Agenda Date September 17,2007 File No. 230517 Subject A HERITAGE PROPERTY TAX RELIEF PROGRAM

Town of Fort Erie Our Focus: Your Future Corporate Services Prepared for Council-in-Committee Report No. CS-24-07 Agenda Date September 17,2007 File No. 230517 Subject A HERITAGE PROPERTY TAX RELIEF PROGRAM

Canadian Land Trust - Standards and Practices

Canadian Land Trust - Crosswalk Comparison: 2005 to Standard 1: Ethics, Mission and Community Engagement 1A Mission 1B Planning and 1B Mission, Planning and Evaluation Reworded: Practices 1A and 1B combined.

Canadian Land Trust - Crosswalk Comparison: 2005 to Standard 1: Ethics, Mission and Community Engagement 1A Mission 1B Planning and 1B Mission, Planning and Evaluation Reworded: Practices 1A and 1B combined.

The ECOLOGICAL GIFTS PROGRAM. Retaining the Right to Use Land Donated as an Ecological Gift

The ECOLOGICAL GIFTS PROGRAM Retaining the Right to Use Land Donated as an Ecological Gift Life Interests and Licences Usufruct, Right of Use, Superfi cies and Permission Agreements INTRODUCTION T HIS

The ECOLOGICAL GIFTS PROGRAM Retaining the Right to Use Land Donated as an Ecological Gift Life Interests and Licences Usufruct, Right of Use, Superfi cies and Permission Agreements INTRODUCTION T HIS

18 Sale and Other Disposition of Regional Lands Policy

Clause 18 in Report No. 7 of Committee of the Whole was adopted, without amendment, by the Council of The Regional Municipality of York at its meeting held on April 19, 2018. 18 Sale and Other Disposition

Clause 18 in Report No. 7 of Committee of the Whole was adopted, without amendment, by the Council of The Regional Municipality of York at its meeting held on April 19, 2018. 18 Sale and Other Disposition

IMPORTANT UPDATED ADVISORY ON TAX SHELTER ABUSE INVOLVING CONSERVATION DONATIONS

IMPORTANT UPDATED ADVISORY ON TAX SHELTER ABUSE INVOLVING CONSERVATION DONATIONS All Land Trust Alliance (the Alliance ) member land trusts adopt and commit to implement Land Trust Standards and Practices

IMPORTANT UPDATED ADVISORY ON TAX SHELTER ABUSE INVOLVING CONSERVATION DONATIONS All Land Trust Alliance (the Alliance ) member land trusts adopt and commit to implement Land Trust Standards and Practices

FILE: EFFECTIVE DATE: May 15, 2013 AMENDMENT: 1

APPROVED AMENDMENTS: Effective Date Briefing Note /Approval Summary of Changes: June 1, 2011 BN 175892 Policy and Procedure update to reflect reorganization of resource ministries April 2011 May 15, 2013

APPROVED AMENDMENTS: Effective Date Briefing Note /Approval Summary of Changes: June 1, 2011 BN 175892 Policy and Procedure update to reflect reorganization of resource ministries April 2011 May 15, 2013

11/11/2014. Takeaways. Making the Most of Provincial Tax Incentive Programs. Provincial Property Tax Incentive Programs

Making the Most of Provincial Tax Incentive Programs Fiona McKay, Ministry of Natural Resources and Forestry Ontario Land Trust Alliance Gathering October 24, 2014 TIPs and Tools Takeaways What provincial

Making the Most of Provincial Tax Incentive Programs Fiona McKay, Ministry of Natural Resources and Forestry Ontario Land Trust Alliance Gathering October 24, 2014 TIPs and Tools Takeaways What provincial

Establishing a Wetland Bank in Minnesota

Establishing a Wetland Bank in Minnesota Updated February 1, 2018 This document provides a general summary of the key steps in establishing an individual wetland bank site within the state wetland banking

Establishing a Wetland Bank in Minnesota Updated February 1, 2018 This document provides a general summary of the key steps in establishing an individual wetland bank site within the state wetland banking

Conservation Easements: Creating a Conservation Legacy for Private Property

Conservation Easements: Creating a Conservation Legacy for Private Property What is a Conservation Easement? For landowners who want to conserve their land and yet keep it in private ownership and use,

Conservation Easements: Creating a Conservation Legacy for Private Property What is a Conservation Easement? For landowners who want to conserve their land and yet keep it in private ownership and use,

TARGETED VERIFICATION DOCUMENTS

TARGETED VERIFICATION DOCUMENTS In an effort to reduce the amount of documentation provided in the overall application, the Commission has shifted some questions and documentation to the Pre-Application

TARGETED VERIFICATION DOCUMENTS In an effort to reduce the amount of documentation provided in the overall application, the Commission has shifted some questions and documentation to the Pre-Application

FYI For Your Information

TAXPAYER SERVICE DIVISION FYI For Your Information Gross Conservation Easement Credit OVERVIEW An income tax credit is available for tax years beginning on or after January 1, 2000, for the donation of

TAXPAYER SERVICE DIVISION FYI For Your Information Gross Conservation Easement Credit OVERVIEW An income tax credit is available for tax years beginning on or after January 1, 2000, for the donation of

Conservation Easement Stewardship

Conservation Easements are effective tools to preserve significant natural, historical or cultural resources. Conservation Easement Stewardship Level of Service Standards March 2013 The mission of the

Conservation Easements are effective tools to preserve significant natural, historical or cultural resources. Conservation Easement Stewardship Level of Service Standards March 2013 The mission of the

DESCRIPTION OF A LAND TRUST

DESCRIPTION OF A LAND TRUST What is a land trust? Land trusts are non-profit organizations that work hand-in-hand with landowners to protect our valuable natural resources. Land trusts have become increasingly

DESCRIPTION OF A LAND TRUST What is a land trust? Land trusts are non-profit organizations that work hand-in-hand with landowners to protect our valuable natural resources. Land trusts have become increasingly

Chapter VIII. Conservation Easements: Valuing Property Subject to a Qualified Conservation Contribution

A. Overview and Purpose Chap. VIII Conservation Easements: Valuing... Jacobson & Becker 91 Chapter VIII Conservation Easements: Valuing Property Subject to a Qualified Conservation Contribution Forest

A. Overview and Purpose Chap. VIII Conservation Easements: Valuing... Jacobson & Becker 91 Chapter VIII Conservation Easements: Valuing Property Subject to a Qualified Conservation Contribution Forest

CONSERVATION EASEMENTS FREQUENTLY ASKED QUESTIONS

CONSERVATION EASEMENTS FREQUENTLY ASKED QUESTIONS CCALT Founder and Steamboat rancher, Jay Fetcher notes, You shouldn t even be considering a conservation easement unless two things have happened: (1)

CONSERVATION EASEMENTS FREQUENTLY ASKED QUESTIONS CCALT Founder and Steamboat rancher, Jay Fetcher notes, You shouldn t even be considering a conservation easement unless two things have happened: (1)

1.3. The Policy is based on the City of London governing principles:

Real Property Acquisition Policy Policy Name: Real Property Acquisition Policy Legislative History: Enacted September 19, 2017 (By-law No. CPOL.-188-440); Amended July 24, 2018 (By-law No. CPOL.-188(a)-447)

Real Property Acquisition Policy Policy Name: Real Property Acquisition Policy Legislative History: Enacted September 19, 2017 (By-law No. CPOL.-188-440); Amended July 24, 2018 (By-law No. CPOL.-188(a)-447)

TRCA Administrative Fee Schedule for ENVIRONMENTAL ASSESSMENT and INFRASTRUCTURE PERMITTING SERVICES IMPLEMENTATION GUIDELINES May 2014

IMPLEMENTATION GUIDELINES Introduction TRCA s Fee Schedule for Environmental Assessment and Permitting Services was adopted by Resolution #A237/13 of the Authority Board on January 31, 2014. The Fee Schedule

IMPLEMENTATION GUIDELINES Introduction TRCA s Fee Schedule for Environmental Assessment and Permitting Services was adopted by Resolution #A237/13 of the Authority Board on January 31, 2014. The Fee Schedule

SUBJECT: MINISTERIAL CONSENTS UNDER THE SOCIAL HOUSING REFORM ACT, 2000

Social Services Department Social Housing Division The Corporation of the County of Simcoe DIRECTIVE EFFECTIVE DATE: May 26, 2003 NUMBER: 2003-11 The policies, procedures and County requirements in this

Social Services Department Social Housing Division The Corporation of the County of Simcoe DIRECTIVE EFFECTIVE DATE: May 26, 2003 NUMBER: 2003-11 The policies, procedures and County requirements in this

Summary of Changes: June 1, 2011 BN Policy and Procedure update to reflect reorganization of resource ministries April 2011

APPROVED AMENDMENTS: Effective Date Briefing Note /Approval Summary of Changes: June 1, 2011 BN 175892 Policy and Procedure update to reflect reorganization of resource ministries April 2011 FILE: 11040-00

APPROVED AMENDMENTS: Effective Date Briefing Note /Approval Summary of Changes: June 1, 2011 BN 175892 Policy and Procedure update to reflect reorganization of resource ministries April 2011 FILE: 11040-00

Saskatchewan Farmland Ownership

Saskatchewan Farmland Ownership Joint presentation to the Ministry of Agriculture by: Ducks Unlimited Canada Nature Conservancy of Canada Saskatchewan Wildlife Federation June 11, 2015 DUC Saskatchewan

Saskatchewan Farmland Ownership Joint presentation to the Ministry of Agriculture by: Ducks Unlimited Canada Nature Conservancy of Canada Saskatchewan Wildlife Federation June 11, 2015 DUC Saskatchewan

Conservation Easement Assistance Program

PENNSYLVANIA LAND TRUST ASSOCIATION Conservation Easement Assistance Program GUIDELINES last updated 3/12/2013 Introduction... 2 Qualify an Organization... 2 The Basics... 2 Open Application Period...

PENNSYLVANIA LAND TRUST ASSOCIATION Conservation Easement Assistance Program GUIDELINES last updated 3/12/2013 Introduction... 2 Qualify an Organization... 2 The Basics... 2 Open Application Period...

For more information on how to compile and submit project documentation see our website and the User Manual.

PROJECT DOCUMENTATION CHECKLIST Documentation for projects selected by the Commission is required as part of each renewal application. This checklist is required for each project selected, to help you

PROJECT DOCUMENTATION CHECKLIST Documentation for projects selected by the Commission is required as part of each renewal application. This checklist is required for each project selected, to help you

PRESERVATION EASEMENT

PRESERVATION EASEMENT Policies and Procedures for Donations The Preservation Resource Center s easement donation program enables a property ownertaxpayer to claim a charitable deduction on his or her tax

PRESERVATION EASEMENT Policies and Procedures for Donations The Preservation Resource Center s easement donation program enables a property ownertaxpayer to claim a charitable deduction on his or her tax

Project Name: Project Documentation Checklist for First-Time and Renewal June 2017 Page 1 of 6

PROJECT DOCUMENTATION CHECKLIST Documentation for projects selected by the Commission is required as part of each application for first-time accreditation and renewal of accreditation. This checklist is

PROJECT DOCUMENTATION CHECKLIST Documentation for projects selected by the Commission is required as part of each application for first-time accreditation and renewal of accreditation. This checklist is

Application Procedures for Easements or Rights of Way on City of Fort Collins Natural Areas and Conserved Lands March 2012

Application Procedures for Easements or Rights of Way on City of Fort Collins Natural Areas and Conserved Lands March 2012 IMPORTANT NOTE: This document was created to accompany the City of Fort Collins

Application Procedures for Easements or Rights of Way on City of Fort Collins Natural Areas and Conserved Lands March 2012 IMPORTANT NOTE: This document was created to accompany the City of Fort Collins

Conservation Plans, Vouchers, & PIRFs

Conservation Plans, Vouchers, & PIRFs Outline Conservation Plan Preparation Voucher Preparation PIRFs vs. Revision Requests Violations & Veg Guidelines Outline Conservation Plan Preparation Benefits of

Conservation Plans, Vouchers, & PIRFs Outline Conservation Plan Preparation Voucher Preparation PIRFs vs. Revision Requests Violations & Veg Guidelines Outline Conservation Plan Preparation Benefits of

Homeowner s Exemption (HOE)

") Homeowner s Exemption (HOE) Table of Contents CHEAT SHEETS... 3 Add HOE to a Parcel...3 Edit HOE Record...3 Remove HOE from a Parcel...3 Find the HOE Amount...3 Who is getting the exemption?...4 New Application

Homeowner s Exemption (HOE) Table of Contents CHEAT SHEETS... 3 Add HOE to a Parcel...3 Edit HOE Record...3 Remove HOE from a Parcel...3 Find the HOE Amount...3 Who is getting the exemption?...4 New Application

CONSERVATION EASEMENTS

CONSERVATION EASEMENTS Prepared for the Colorado Cattlemen's Agricultural Land Trust January 2007 By Lawrence R. Kueter, Esq. Isaacson, Rosenbaum, Woods & Levy, P.C. Suite 2200 633 17th Street Denver,

CONSERVATION EASEMENTS Prepared for the Colorado Cattlemen's Agricultural Land Trust January 2007 By Lawrence R. Kueter, Esq. Isaacson, Rosenbaum, Woods & Levy, P.C. Suite 2200 633 17th Street Denver,

Welcome. Tax & Ecology Seminar. presented by The Georgian Bay Land Trust

Welcome Tax & Ecology Seminar presented by The Georgian Bay Land Trust There are significant income and capital gains tax benefits available for Georgian Bay land owners who want to help protect the bay

Welcome Tax & Ecology Seminar presented by The Georgian Bay Land Trust There are significant income and capital gains tax benefits available for Georgian Bay land owners who want to help protect the bay

Hosted by: Berkeley County and Jefferson Farmland Protection Boards and Land Trust of the Eastern Panhandle February 27, Bowles Rice LLP

Hosted by: Berkeley County and Jefferson Farmland Protection Boards and Land Trust of the Eastern Panhandle February 27, 2016 2016 Bowles Rice LLP Conservation Easements, Taxes, and Estate Planning Presented

Hosted by: Berkeley County and Jefferson Farmland Protection Boards and Land Trust of the Eastern Panhandle February 27, 2016 2016 Bowles Rice LLP Conservation Easements, Taxes, and Estate Planning Presented

Wildlife Habitat Conservation and Management Program

EXHIBIT 1 PC-2015-4106 ODFW Guide Wildlife Habitat Conservation and Management Program Manual for Counties and Cities Oregon Department of Fish and Wildlife March 2006 Table of Contents 1. Introduction

EXHIBIT 1 PC-2015-4106 ODFW Guide Wildlife Habitat Conservation and Management Program Manual for Counties and Cities Oregon Department of Fish and Wildlife March 2006 Table of Contents 1. Introduction

2018 Requirements Manual An In-Depth Look at Changes to the Requirements

2018 Requirements Manual An In-Depth Look at Changes to the Requirements Executive Summary The Requirements Manual helps land trusts understand how the Land Trust Accreditation Commission verifies that

2018 Requirements Manual An In-Depth Look at Changes to the Requirements Executive Summary The Requirements Manual helps land trusts understand how the Land Trust Accreditation Commission verifies that

A SYNOPSIS ON PROTECTING AND COMMEMORATING HERITAGE TREES

A SYNOPSIS ON PROTECTING AND COMMEMORATING HERITAGE TREES Barbara Heidenreich, Heritage Tree Advisor Forests Ontario & Ontario Urban Forest Council January 2016 PROTECTING HERITAGE TREES: A SYNOPSIS This

A SYNOPSIS ON PROTECTING AND COMMEMORATING HERITAGE TREES Barbara Heidenreich, Heritage Tree Advisor Forests Ontario & Ontario Urban Forest Council January 2016 PROTECTING HERITAGE TREES: A SYNOPSIS This

Procedures for Transfer of a Woodlot Licence or Christmas Tree Permit Under Division 2 of the Forest Act

!! Procedures for Transfer of a Woodlot Licence or Christmas Tree Permit Under Division 2 of the Forest Act July 2011 Transfer Procedures Page 2! of! 13 The following procedures apply to Woodlot Licences

!! Procedures for Transfer of a Woodlot Licence or Christmas Tree Permit Under Division 2 of the Forest Act July 2011 Transfer Procedures Page 2! of! 13 The following procedures apply to Woodlot Licences

Acquisition IOWA 2015 CDBG MANAGEMENT GUIDE APPENDIX 2 PAGE: 79

Acquisition IOWA 2015 CDBG MANAGEMENT GUIDE APPENDIX 2 PAGE: 79 WHEN A PUBLIC AGENCY ACQUIRES YOUR PROPERTY Introduction U.S. Department of Housing And Urban Development Office of Community Planning and

Acquisition IOWA 2015 CDBG MANAGEMENT GUIDE APPENDIX 2 PAGE: 79 WHEN A PUBLIC AGENCY ACQUIRES YOUR PROPERTY Introduction U.S. Department of Housing And Urban Development Office of Community Planning and

Land Transaction Procedures Approved July 17, 2012

Land Transaction Procedures Approved July 17, 2012 Purpose: The Greenbelt Land Trust (GLT) acquires fee title or conservation easements for lands to fulfill its mission to conserve and protect in perpetuity

Land Transaction Procedures Approved July 17, 2012 Purpose: The Greenbelt Land Trust (GLT) acquires fee title or conservation easements for lands to fulfill its mission to conserve and protect in perpetuity

Guide to Planned Giving

Guide to Planned Giving Leave it to nature, forever. Tax ID# 91-1533402 For more information: Skagit Land Trust 1020 S Third Street - PO Box 1017 Mount Vernon, WA 98273 360.428.7878 Molly Doran, Executive

Guide to Planned Giving Leave it to nature, forever. Tax ID# 91-1533402 For more information: Skagit Land Trust 1020 S Third Street - PO Box 1017 Mount Vernon, WA 98273 360.428.7878 Molly Doran, Executive

ALC Bylaw Reviews. A Guide for Local Governments

2018 ALC Bylaw Reviews A Guide for Local Governments ALC Bylaw Reviews A Guide for Local Governments This version published on: August 14, 2018 Published by: Agricultural Land Commission #201-4940 Canada

2018 ALC Bylaw Reviews A Guide for Local Governments ALC Bylaw Reviews A Guide for Local Governments This version published on: August 14, 2018 Published by: Agricultural Land Commission #201-4940 Canada

PRE-APPLICATION FREQUENTLY ASKED QUESTIONS (FAQ) GENERAL PURCHASE OF DEVELOPMENT RIGHTS (PDR) FAQs

GENERAL PURCHASE OF DEVELOPMENT RIGHTS (PDR) FAQs") PRE-APPLICATION FREQUENTLY ASKED QUESTIONS (FAQ) Q: Question #26 asks me to describe how protecting my land will buffer and enhance important public natural areas. What types of natural areas do you mean?

PRE-APPLICATION FREQUENTLY ASKED QUESTIONS (FAQ) Q: Question #26 asks me to describe how protecting my land will buffer and enhance important public natural areas. What types of natural areas do you mean?

Proponent s Guide to the NCC s Federal Land Use, Design and Transaction Approvals Process

Proponent s Guide to the NCC s Federal Land Use, Design and Transaction Approvals Process September 2018 Table of Contents 1. INTRODUCTION 3 2. WHAT IS THE NATIONAL CAPITAL REGION? 4 3. WHEN IS APPROVAL

Proponent s Guide to the NCC s Federal Land Use, Design and Transaction Approvals Process September 2018 Table of Contents 1. INTRODUCTION 3 2. WHAT IS THE NATIONAL CAPITAL REGION? 4 3. WHEN IS APPROVAL

Crown Lands Act, the MOU with AMSA & NSW Men s Sheds

Crown Lands Act, the MOU with AMSA & NSW Men s Sheds Introduction The State Government Department responsible for Crown reserves is the Dept of Primary Industries. Reserves are created to protect and manage

Crown Lands Act, the MOU with AMSA & NSW Men s Sheds Introduction The State Government Department responsible for Crown reserves is the Dept of Primary Industries. Reserves are created to protect and manage

LESSON 4. Market Research and Subject Property Identification

LESSON 4 Market Research and Subject Property Identification Note: Selected readings can be found under "Online Readings" on your Course Resources webpage. ASSIGNED READING 1. UBC Real Estate Division.

LESSON 4 Market Research and Subject Property Identification Note: Selected readings can be found under "Online Readings" on your Course Resources webpage. ASSIGNED READING 1. UBC Real Estate Division.

Canadian Land Trust Standards and Practices

Canadian Land Trust Standards and Practices 2019 Table of Contents STANDARD 1 - Ethics, Mission and Community Engagement... 4 STANDARD 2 - Compliance with Laws... 5 STANDARD 3 - Board Accountability...

Canadian Land Trust Standards and Practices 2019 Table of Contents STANDARD 1 - Ethics, Mission and Community Engagement... 4 STANDARD 2 - Compliance with Laws... 5 STANDARD 3 - Board Accountability...

CONSERVATION EASEMENTS FREQUENTLY ASKED QUESTIONS

CONSERVATION EASEMENTS FREQUENTLY ASKED QUESTIONS CCALT Founder and Steamboat rancher, Jay Fetcher notes, You shouldn t even be considering a conservation easement unless two things have happened: (1)

CONSERVATION EASEMENTS FREQUENTLY ASKED QUESTIONS CCALT Founder and Steamboat rancher, Jay Fetcher notes, You shouldn t even be considering a conservation easement unless two things have happened: (1)

Our Proposal. The Proposal

Page 1 The Land Trust Alliance of BC and partners are promoting the establishment of a province-wide Conservation Tax Incentive Program (CTIP). This would be established through amendment of provincial

Page 1 The Land Trust Alliance of BC and partners are promoting the establishment of a province-wide Conservation Tax Incentive Program (CTIP). This would be established through amendment of provincial

PBRA RAD Conversion FASTForms Description

RBD does not act as a legal advisor nor as a regulatory governing agency. The recipient should understand that any materials or comments contained herein are not designed for, nor should be relied upon

RBD does not act as a legal advisor nor as a regulatory governing agency. The recipient should understand that any materials or comments contained herein are not designed for, nor should be relied upon

Revision of the Canadian Land Trust Standards and Practices - Preliminary Consultation

Revision of the Canadian Land Trust Standards and Practices - Preliminary Consultation Background Info The Canadian Land Trust Standards and Practices (CLT S&P) are the ethical and technical guidelines

Revision of the Canadian Land Trust Standards and Practices - Preliminary Consultation Background Info The Canadian Land Trust Standards and Practices (CLT S&P) are the ethical and technical guidelines

Digital Assets: Practitioner s Guide Canada

Digital Assets: Practitioner s Guide Canada This practitioner s guide has been prepared to assist Canadian practitioners with the issue of digital assets when taking instructions from clients for estate

Digital Assets: Practitioner s Guide Canada This practitioner s guide has been prepared to assist Canadian practitioners with the issue of digital assets when taking instructions from clients for estate

GIFT ACCEPTANCE POLICIES

732 West Central Avenue Saint Paul, Minnesota 55104 GIFT ACCEPTANCE POLICIES, (hereinafter collectively referred to as the Church ), not-for-profit entity organized under the laws of the State of Minnesota

732 West Central Avenue Saint Paul, Minnesota 55104 GIFT ACCEPTANCE POLICIES, (hereinafter collectively referred to as the Church ), not-for-profit entity organized under the laws of the State of Minnesota

Establishing an Individual Wetland Bank Site in Minnesota

Establishing an Individual Wetland Bank Site in Minnesota March 14, 2013 This document provides a general summary of the key steps in establishing a an individual wetland bank site within the state wetland

Establishing an Individual Wetland Bank Site in Minnesota March 14, 2013 This document provides a general summary of the key steps in establishing a an individual wetland bank site within the state wetland

REQUEST FOR APPLICATION (RFA)

") REQUEST FOR APPLICATION (RFA) Rental Housing Improvement Program (RHIP) 2014 APPLICATION SUBMISSION 1. Submission Deadline: No later than 4:30 pm (CDT) on June 12 th, 2014 2. Address to which submissions

REQUEST FOR APPLICATION (RFA) Rental Housing Improvement Program (RHIP) 2014 APPLICATION SUBMISSION 1. Submission Deadline: No later than 4:30 pm (CDT) on June 12 th, 2014 2. Address to which submissions

Planning with Conservation Easements

Planning with Conservation Easements Succession, Tax & Estate Planning Issues & Ideas for Legacy Land October 23, 2015 Intergenerational Planning for Legacy Land Begin with the end in mind. Your goals

Planning with Conservation Easements Succession, Tax & Estate Planning Issues & Ideas for Legacy Land October 23, 2015 Intergenerational Planning for Legacy Land Begin with the end in mind. Your goals

Town of Ajax Heritage Property Tax Rebate Program Information Brochure, 2008

Town of Ajax Heritage Property Tax Rebate Program Information Brochure, 2008 1733 Westney Road, North circa 1898 Designation By-law181-85 The Ontario Government has enabled local municipalities to offer

Town of Ajax Heritage Property Tax Rebate Program Information Brochure, 2008 1733 Westney Road, North circa 1898 Designation By-law181-85 The Ontario Government has enabled local municipalities to offer

Office of Community Planning and Development. Introduction

WHEN A PUBLIC AGENCY ACQUIRES YOUR PROPERTY www.hud.gov/relocation U.S. Department of Housing and Urban Development Office of Community Planning and Development Introduction This booklet describes important

WHEN A PUBLIC AGENCY ACQUIRES YOUR PROPERTY www.hud.gov/relocation U.S. Department of Housing and Urban Development Office of Community Planning and Development Introduction This booklet describes important

Working Together to Conserve Land

Working Together to Conserve Land A Resource for Landowners Protecting land for future generations About Loon Echo was formed as a 501(c)(3)nonprofit organization in 1987 to preserve land in the northern

Working Together to Conserve Land A Resource for Landowners Protecting land for future generations About Loon Echo was formed as a 501(c)(3)nonprofit organization in 1987 to preserve land in the northern

Land Conservation Agreements Project Guidance

Land Conservation Agreements Project Guidance Stakeholder Informed OTHER OPTIONS Introduction Enhanced or permanent protection of corporate lands through land conservation agreements means that companies

Land Conservation Agreements Project Guidance Stakeholder Informed OTHER OPTIONS Introduction Enhanced or permanent protection of corporate lands through land conservation agreements means that companies

Land Procedure: Allocation Procedures - Major Projects/Sales. Summary of Changes:

APPROVED AMENDMENTS: Effective Date Briefing Note /Approval Summary of Changes: June 1, 2011 BN 175892 Policy and Procedure update to reflect reorganization of resource ministries April 2011 FILE: 11480-00

APPROVED AMENDMENTS: Effective Date Briefing Note /Approval Summary of Changes: June 1, 2011 BN 175892 Policy and Procedure update to reflect reorganization of resource ministries April 2011 FILE: 11480-00

1 Adopting the Code. The Consumer Code Requirements and good practice Guidance. 1.1 Adopting the Code. 1.2 Making the Code available

The Non-mandatory Good Practice for Home Builders along The Consumer Code s and good practice 1 Adopting the Code 1.1 Adopting the Code Home Builders must comply with the s of the Consumer Code and have

The Non-mandatory Good Practice for Home Builders along The Consumer Code s and good practice 1 Adopting the Code 1.1 Adopting the Code Home Builders must comply with the s of the Consumer Code and have

MODEL CONSERVATION RESTRICTION AMENDMENT POLICY GUIDELINES Massachusetts Easement Defense Subcommittee March 6, 2007 PREAMBLE

MODEL CONSERVATION RESTRICTION AMENDMENT POLICY GUIDELINES Massachusetts Easement Defense Subcommittee March 6, 2007 PREAMBLE Because conservation restrictions are an important tool for permanently protecting

MODEL CONSERVATION RESTRICTION AMENDMENT POLICY GUIDELINES Massachusetts Easement Defense Subcommittee March 6, 2007 PREAMBLE Because conservation restrictions are an important tool for permanently protecting

ADMINISTRATIVE GUIDANCE

11 ADMINISTRATIVE GUIDANCE ON CONTAMINATED SITES Effective date: April 1, 2013 Version 1.1 May 2013 Expectations and Requirements for Contaminant Migration Introduction This guidance focusses on the ministry

11 ADMINISTRATIVE GUIDANCE ON CONTAMINATED SITES Effective date: April 1, 2013 Version 1.1 May 2013 Expectations and Requirements for Contaminant Migration Introduction This guidance focusses on the ministry

National Trust for Historic Preservation Collections Management Policy INTRODUCTION

National Trust for Historic Preservation Collections Management Policy INTRODUCTION The National Trust for Historic Preservation and its Collections. The National Trust for Historic Preservation in the

National Trust for Historic Preservation Collections Management Policy INTRODUCTION The National Trust for Historic Preservation and its Collections. The National Trust for Historic Preservation in the

COMPLETENESS OF APPLICATION:

Community Development Department 50 Dickson Street, 3 rd Floor, P.O. Box 669 Cambridge ON N1R 5W8 Tel: (519) 621-0740 ext. 4289 Fax: (519) 622-6184 TTY: (519) 623-6691 MINOR VARIANCE Application for a

Community Development Department 50 Dickson Street, 3 rd Floor, P.O. Box 669 Cambridge ON N1R 5W8 Tel: (519) 621-0740 ext. 4289 Fax: (519) 622-6184 TTY: (519) 623-6691 MINOR VARIANCE Application for a

LIVING LANDS BIODIVERSITY GRANTS: INFORMATION AND APPLICATION. Due: January 16, 2009

LIVING LANDS BIODIVERSITY GRANTS: INFORMATION AND APPLICATION Due: January 16, 2009 PURPOSE OF LIVING LANDS PROJECT Defenders of Wildlife s Living Lands project provides financial, technical and educational

LIVING LANDS BIODIVERSITY GRANTS: INFORMATION AND APPLICATION Due: January 16, 2009 PURPOSE OF LIVING LANDS PROJECT Defenders of Wildlife s Living Lands project provides financial, technical and educational

Presented on behalf of The Morris Land Trust September 11, 2009 By Melissa Spear Connecticut Conservation Practitioners, LLC

Presented on behalf of The Morris Land Trust September 11, 2009 By Melissa Spear Connecticut Conservation Practitioners, LLC Total Land Area 3,275,760 Acres CLEAR Data 2006 clear.uconn.edu CLEAR 2006 (clear.uconn.edu)

Presented on behalf of The Morris Land Trust September 11, 2009 By Melissa Spear Connecticut Conservation Practitioners, LLC Total Land Area 3,275,760 Acres CLEAR Data 2006 clear.uconn.edu CLEAR 2006 (clear.uconn.edu)

WHEN A PUBLIC AGENCY IS INTERESTED IN ACQUIRING AN EASEMENT

Form 6-H When a Public Agency is interested in Acquiring an Easement Booklet WHEN A PUBLIC AGENCY IS INTERESTED IN ACQUIRING AN EASEMENT Introduction This booklet describes important features of the Uniform

Form 6-H When a Public Agency is interested in Acquiring an Easement Booklet WHEN A PUBLIC AGENCY IS INTERESTED IN ACQUIRING AN EASEMENT Introduction This booklet describes important features of the Uniform

New York Agricultural Land Trust

New York Agricultural Land Trust P.O. Box 121 Preble, NY 13141 www.nyalt.org New York Agricultural Land Trust Agricultural Conservation Easements and Appraisals Introduction An agricultural conservation

New York Agricultural Land Trust P.O. Box 121 Preble, NY 13141 www.nyalt.org New York Agricultural Land Trust Agricultural Conservation Easements and Appraisals Introduction An agricultural conservation

Subject. Date: January 12, Chair and Members of Planning and Development Committee 2016/02/01

Originator s files: Date: January 12, 2016 CD 06 AFF To: From: Chair and Members of Planning and Development Committee Edward R. Sajecki, Commissioner of Planning and Building Meeting date: 2016/02/01

Originator s files: Date: January 12, 2016 CD 06 AFF To: From: Chair and Members of Planning and Development Committee Edward R. Sajecki, Commissioner of Planning and Building Meeting date: 2016/02/01

ARCHITECTURAL MODIFICATION GUIDELINES

ARCHITECTURAL MODIFICATION GUIDELINES The following Architectural Modification Guidelines have been adopted by the Board of Directors of the Madison Green Homeowner s Association to be consistent and expand

ARCHITECTURAL MODIFICATION GUIDELINES The following Architectural Modification Guidelines have been adopted by the Board of Directors of the Madison Green Homeowner s Association to be consistent and expand

Heathrow Expansion. Land Acquisition and Compensation Policies. Interim Property Hardship Scheme. Policy Terms

1 Introduction Heathrow Expansion Land Acquisition and Compensation Policies Interim Property Hardship Scheme Policy Terms 1.1 This document sets out the terms of the Interim Property Hardship Scheme (the

1 Introduction Heathrow Expansion Land Acquisition and Compensation Policies Interim Property Hardship Scheme Policy Terms 1.1 This document sets out the terms of the Interim Property Hardship Scheme (the

BUILT BOUNDARY CIP REDEVELOPMENT GRANT APPLICATION FORM

BUILT BOUNDARY CIP REDEVELOPMENT GRANT APPLICATION FORM Introduction The Redevelopment Grant Program provides support for eligible developments that realize key planning and growth management objectives

BUILT BOUNDARY CIP REDEVELOPMENT GRANT APPLICATION FORM Introduction The Redevelopment Grant Program provides support for eligible developments that realize key planning and growth management objectives

TOWN OF AURORA SUBDIVISION AND/OR CONDOMINIUM APPLICATION GUIDE

PLANNING & DEVELOPMENT SERVICES Phone: 905-727-3123 ext. 4226 Fax 905-726-4736 Email: planning@aurora.ca Town of Aurora 100 John West Way Box 1000, Aurora, ON L4G 6J1 www.aurora.ca February, 2014 TABLE

PLANNING & DEVELOPMENT SERVICES Phone: 905-727-3123 ext. 4226 Fax 905-726-4736 Email: planning@aurora.ca Town of Aurora 100 John West Way Box 1000, Aurora, ON L4G 6J1 www.aurora.ca February, 2014 TABLE

WESTERN ILLINOIS UNIVERSITY FOUNDATION REAL ESTATE GIFT ACCEPTANCE POLICY. As Adopted July 10,2013.

WESTERN ILLINOIS UNIVERSITY FOUNDATION REAL ESTATE GIFT ACCEPTANCE POLICY As Adopted July 10,2013. Purpose - This policy sets forth the requirements and guidelines governing acceptance ofreal estate gifts

WESTERN ILLINOIS UNIVERSITY FOUNDATION REAL ESTATE GIFT ACCEPTANCE POLICY As Adopted July 10,2013. Purpose - This policy sets forth the requirements and guidelines governing acceptance ofreal estate gifts

USOPF REAL ESTATE ACCEPTANCE POLICY

USOPF REAL ESTATE ACCEPTANCE POLICY The United States Olympic and Paralympic Foundation ( USOPF ) is a not-for-profit organization under the laws of the State of Colorado organized to encourage, solicit

USOPF REAL ESTATE ACCEPTANCE POLICY The United States Olympic and Paralympic Foundation ( USOPF ) is a not-for-profit organization under the laws of the State of Colorado organized to encourage, solicit

Questions to Ask of a Conservation Easement Appraiser (Before Retaining One)

") As a Colorado landowner, are you thinking about donating a conservation easement to one of Colorado s certified land trusts or governmental entities? First, make sure the organization you select to hold

As a Colorado landowner, are you thinking about donating a conservation easement to one of Colorado s certified land trusts or governmental entities? First, make sure the organization you select to hold

Crown Land Use Policy: Industrial - General APPROVED AMENDMENTS: Summary of Changes: /Approval

APPROVED AMENDMENTS: Effective Date Briefing Note /Approval Summary of Changes: March 22, 2011 BN175798 Amendment to clarify pricing for aquatic lands. March 31, 2011 BN 175892 Policy and Procedure update

APPROVED AMENDMENTS: Effective Date Briefing Note /Approval Summary of Changes: March 22, 2011 BN175798 Amendment to clarify pricing for aquatic lands. March 31, 2011 BN 175892 Policy and Procedure update

DELAWARE STATE HOUSING AUTHORITY LOW INCOME HOUSING TAX CREDIT QUALIFIED CONTRACT GUIDE

DELAWARE STATE HOUSING AUTHORITY LOW INCOME HOUSING TAX CREDIT QUALIFIED CONTRACT GUIDE 2018 INTRODUCTION Delaware State Housing Authority (DSHA) is a state housing finance agency and housing credit agency

DELAWARE STATE HOUSING AUTHORITY LOW INCOME HOUSING TAX CREDIT QUALIFIED CONTRACT GUIDE 2018 INTRODUCTION Delaware State Housing Authority (DSHA) is a state housing finance agency and housing credit agency

ILM Approved Factsheet on Section 117 Charities Act 2011 August 2012

Prepared for ILM by Henmans LLP Introduction Section 117 Charities Act 2011 (previously s36 Charities Act 1993) was enacted in order to ensure that charities are dealing properly with the disposition of

Prepared for ILM by Henmans LLP Introduction Section 117 Charities Act 2011 (previously s36 Charities Act 1993) was enacted in order to ensure that charities are dealing properly with the disposition of

City of St.Catharines Community Improvement Plan (2015CIP) Guidelines For the Brownfield Tax Assistance (BTA) Program

Guidelines For the Brownfield Tax Assistance (BTA) Program") City of St.Catharines Community Improvement Plan (2015CIP) Guidelines For the Brownfield Tax Assistance (BTA) Program Brownfield Tax Assistance (BTA) Program Guidelines The Brownfield Tax Assistance (BTA)

City of St.Catharines Community Improvement Plan (2015CIP) Guidelines For the Brownfield Tax Assistance (BTA) Program Brownfield Tax Assistance (BTA) Program Guidelines The Brownfield Tax Assistance (BTA)

AICPA Valuation Services VS Section Statements on Standards for Valuation Services VS Section 100 Valuation of a Business, Business Ownership

AICPA Valuation Services VS Section Statements on Standards for Valuation Services VS Section 100 Valuation of a Business, Business Ownership Interest, Security, or Intangible Asset Calculation Engagements

AICPA Valuation Services VS Section Statements on Standards for Valuation Services VS Section 100 Valuation of a Business, Business Ownership Interest, Security, or Intangible Asset Calculation Engagements

City of Philadelphia POLICIES FOR THE SALE AND REUSE OF CITY OWNED PROPERTY. Approved By Philadelphia City Council on December 11, 2014

City of Philadelphia POLICIES FOR THE SALE AND REUSE OF CITY OWNED PROPERTY Approved By Philadelphia City Council on December 11, 2014 City of Philadelphia Disposition Policies December 2014 1 Table of

City of Philadelphia POLICIES FOR THE SALE AND REUSE OF CITY OWNED PROPERTY Approved By Philadelphia City Council on December 11, 2014 City of Philadelphia Disposition Policies December 2014 1 Table of

Rental Construction Financing Initiative

Rental Construction Financing Initiative REQUIRED DOCUMENTATION The following checklist provides the minimum information and documentation required prior to the submission when the application is selected

Rental Construction Financing Initiative REQUIRED DOCUMENTATION The following checklist provides the minimum information and documentation required prior to the submission when the application is selected

Purchase of City-Owned Property Application * Department of Housing and Community Development Land Resources Division

Purchase of City-Owned Property Application * Department of Housing and Community Development Land Resources Division SUMMARY OF PROCESS The Baltimore City Department of Housing and Community Development

Purchase of City-Owned Property Application * Department of Housing and Community Development Land Resources Division SUMMARY OF PROCESS The Baltimore City Department of Housing and Community Development

FILE: EFFECTIVE DATE: June 1, 2011 AMENDMENT :

Land Procedure: Land Exchanges - General APPROVED AMENDMENTS: Effective Date Briefing Note /Approval Summary of Changes: June 1, 2011 BN 175892 Policy and Procedure update to reflect reorganization of

Land Procedure: Land Exchanges - General APPROVED AMENDMENTS: Effective Date Briefing Note /Approval Summary of Changes: June 1, 2011 BN 175892 Policy and Procedure update to reflect reorganization of

enter into land leases; 2. donate land; or 3. provide land at below market value.

4.4-1 Date: 2016/06/07 To: Chair and Members of Planning and Development Committee From: Edward R. Sajecki, Commissioner of Planning and Building Originator s files: CD.06.AFF Meeting date: 2016/06/27

4.4-1 Date: 2016/06/07 To: Chair and Members of Planning and Development Committee From: Edward R. Sajecki, Commissioner of Planning and Building Originator s files: CD.06.AFF Meeting date: 2016/06/27

Valuing Diamonds in the Rough: Utilizing Highest and Best Use Valuation Principles in a Mass Appraisal Environment

Valuing Diamonds in the Rough: Utilizing Highest and Best Use Valuation Principles in a Mass Appraisal Environment Topics of Discussion Revaluation of a former industrial district at the height of a building

Valuing Diamonds in the Rough: Utilizing Highest and Best Use Valuation Principles in a Mass Appraisal Environment Topics of Discussion Revaluation of a former industrial district at the height of a building

Complete applications are due by 2:00 p.m. on the submission cut-off date.

CONSENT APPLICATION PLEASE READ ALL INSTRUCTIONS WHAT IS A COMPLETE APPLICATION? Your application is complete when you have: o Discussed the application with a City of St. Catharines Planner Name of Planner:

CONSENT APPLICATION PLEASE READ ALL INSTRUCTIONS WHAT IS A COMPLETE APPLICATION? Your application is complete when you have: o Discussed the application with a City of St. Catharines Planner Name of Planner:

METHODOLOGY GUIDE VALUING LANDS IN TRANSITION IN ONTARIO. Valuation Date: January 1, 2016

METHODOLOGY GUIDE VALUING LANDS IN TRANSITION IN ONTARIO Valuation Date: January 1, 2016 August 2017 August 22, 2017 The Municipal Property Assessment Corporation (MPAC) is responsible for accurately assessing

METHODOLOGY GUIDE VALUING LANDS IN TRANSITION IN ONTARIO Valuation Date: January 1, 2016 August 2017 August 22, 2017 The Municipal Property Assessment Corporation (MPAC) is responsible for accurately assessing

NATIONAL POLICY ESCROW FOR INITIAL PUBLIC OFFERINGS TABLE OF CONTENTS

NATIONAL POLICY 46-201 ESCROW FOR INITIAL PUBLIC OFFERINGS TABLE OF CONTENTS PART Part I Part II Part III Part IV TITLE Purpose and Interpretation 1.1 What is the purpose of escrow? 1.2 Interpretation

NATIONAL POLICY 46-201 ESCROW FOR INITIAL PUBLIC OFFERINGS TABLE OF CONTENTS PART Part I Part II Part III Part IV TITLE Purpose and Interpretation 1.1 What is the purpose of escrow? 1.2 Interpretation

About Conservation Easements

Section Three: Farm Transfer Tools About Conservation Easements Editor s note: One question that our education collaborative has fielded consistently throughout the years is about conservation easements.

Section Three: Farm Transfer Tools About Conservation Easements Editor s note: One question that our education collaborative has fielded consistently throughout the years is about conservation easements.

CHARTER TOWNSHIP OF LYON APPLICATION FOR LAND DIVISION (LOT SPLIT)

") File #: Date Submitted: CHARTER TOWNSHIP OF LYON APPLICATION FOR LAND DIVISION (LOT SPLIT) NOTICE TO APPLICANT: Applications for land divisions (also called lot splits ) are reviewed in accordance with

File #: Date Submitted: CHARTER TOWNSHIP OF LYON APPLICATION FOR LAND DIVISION (LOT SPLIT) NOTICE TO APPLICANT: Applications for land divisions (also called lot splits ) are reviewed in accordance with

POLICY ON THE DISPOSAL OF SURPLUS COLLEGE PERSONAL PROPERTY

POLICY ON THE DISPOSAL OF SURPLUS COLLEGE PERSONAL PROPERTY I. PURPOSE This policy provides guidelines to assist Suffolk County Community College and Suffolk County Community College Association collectively

POLICY ON THE DISPOSAL OF SURPLUS COLLEGE PERSONAL PROPERTY I. PURPOSE This policy provides guidelines to assist Suffolk County Community College and Suffolk County Community College Association collectively

Escrow Basics. Chapter 6. Learning Objectives

Chapter 6 Escrow Basics Learning Objectives After reading this chapter, you will be able to: explain the basic regional differences of escrow instructions. define the general principles followed by all

Chapter 6 Escrow Basics Learning Objectives After reading this chapter, you will be able to: explain the basic regional differences of escrow instructions. define the general principles followed by all

02 Register with us 03 View with us 04 Making an offer 05 Helping you in your new home 06 Your utility bills 07 Move with us 08 Making your move

Tenant s Guide 1 2 02 Register with us 03 View with us 04 Making an offer 05 Helping you in your new home 06 Your utility bills 07 Move with us 08 Making your move simple 09 Rent with us 10 Customer care

Tenant s Guide 1 2 02 Register with us 03 View with us 04 Making an offer 05 Helping you in your new home 06 Your utility bills 07 Move with us 08 Making your move simple 09 Rent with us 10 Customer care

REPOSITORY AGREEMENT FOR EXPANDED COLLECTION ARCHAEOLOGICAL PROJECTS. Effective dates: [Date of MHS signing through end of that calendar year]

![REPOSITORY AGREEMENT FOR EXPANDED COLLECTION ARCHAEOLOGICAL PROJECTS. Effective dates: [Date of MHS signing through end of that calendar year]](/thumbs/87/96047718.jpg "REPOSITORY AGREEMENT FOR EXPANDED COLLECTION ARCHAEOLOGICAL PROJECTS. Effective dates: [Date of MHS signing through end of that calendar year]") SAMPLE REPOSITORY AGREEMENT FOR EXPANDED COLLECTION ARCHAEOLOGICAL PROJECTS Repository Agreement Number: [] Issued to: [] Effective dates: [Date of MHS signing through end of that calendar year] The Minnesota

SAMPLE REPOSITORY AGREEMENT FOR EXPANDED COLLECTION ARCHAEOLOGICAL PROJECTS Repository Agreement Number: [] Issued to: [] Effective dates: [Date of MHS signing through end of that calendar year] The Minnesota

etransfer Form User Guide The Property Registry s

s etransfer Form User Guide A service provider for the Province of Manitoba Most recent update: 2018-01-08 Version 2.03 Table of Contents Purpose... 4 General Guidelines for Completion... 4 Requirements...

s etransfer Form User Guide A service provider for the Province of Manitoba Most recent update: 2018-01-08 Version 2.03 Table of Contents Purpose... 4 General Guidelines for Completion... 4 Requirements...

Application for OFFICIAL PLAN AMENDMENT

Town of Northeastern Manitoulin & the Islands Application for OFFICIAL PLAN AMENDMENT and/or ZONING BY-LAW AMENDMENT Introduction: Application Fees: Authorization: Drawing: Supporting Information: The

Town of Northeastern Manitoulin & the Islands Application for OFFICIAL PLAN AMENDMENT and/or ZONING BY-LAW AMENDMENT Introduction: Application Fees: Authorization: Drawing: Supporting Information: The