Underwriting the FHA Appraisal

|

|

|

- Ethan Barnett

- 6 years ago

- Views:

Transcription

1 Disclosure The purpose of this presentation is an overview of the subject matter with summation and explanation of recent changes in FHA policy. It introduces and explains, rather than supplants, official policy issued in Handbooks and Mortgagee Letters. If you find a discrepancy between the presentation and Handbooks, Mortgagee Letters, etc., the official policies prevail. Please note the information provided in this training is subject to change. Please consult HUD online Handbooks at and Mortgagee Letters through for the most recent updates and current policy.

2 Underwriting the FHA Appraisal Presented by Marjorie Friesen, Megan Bartlett & Becky Shade 2

3 Contact FHA CALLFHA ( ) to sign up for HUD news and updates including upcoming trainings and webinars 08/16/10 3

4 Direct Endorsement lenders are reminded that if the appraiser they selected provides a poor or fraudulent appraisal that leads FHA to insure a mortgage at an inflated amount, the lender is held responsible, equally with the appraiser, for the integrity, accuracy and thoroughness of an appraisal submitted to FHA for mortgage insurance purposes. 4

5 With Whom Does the Appraiser Communicate? The appraiser is to discuss the appraisal only with the DE Underwriter who is responsible for the quality of the appraisal report. Only the underwriter is allowed to request clarifications and discuss with the appraiser components of the appraisal that influence its quality. 5

6 6

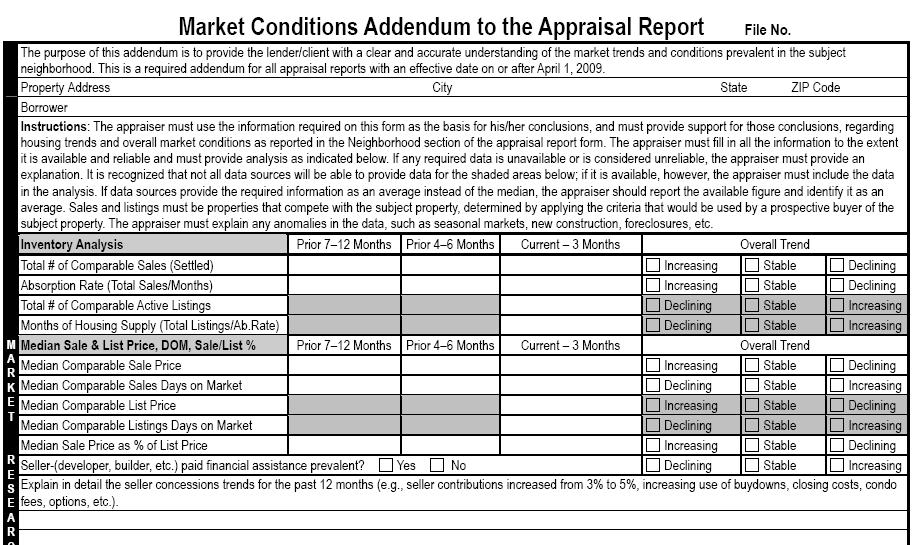

7 Appraisal Forms Form 1004 Uniform Residential Appraisal Report: Appraisal of a one-unit property (including individual unit in a PUD) Form 1004C Manufactured Home Appraisal Report: Appraisal of a manufactured home (including a manufactured home in a PUD or condominium project) Form 1073 Individual Condominium Unit Appraisal Report Form 1025 Small Residential Income Property Appraisal Report: Appraisal of a two-unit to four-unit property Market Conditions Addendum, Form 1004MC FNMA 1004D, Appraisal Update and/or Completion Form Form HUD Compliance Inspection Report: completion report for all one-unit to four-unit appraisal reports 7

8 Uniform Residential Appraisal Subject Section FHA Case #

9 Uniform Residential Appraisal Report Contract Section 9

10 Uniform Residential Appraisal Report Subject Section 10

11 Uniform Residential Appraisal Report Neighborhood 11

12 Uniform Residential Appraisal Report Site 12

13 Observing the Site FHA requires the appraiser to disclose if any property is subject to hazards that endanger the physical improvements, affect livability, marketability or health and safety of occupants 13

14 Site Hazards & Nuisances Subsidence Active or planned drill sites Above ground stationary storage tanks High voltage transmission lines/towers Grading and drainage Airport Noise and Hazards Runway Clear Zones/Accident Potential Zones ML

15 Individual Water Supply and Sewage Systems The Lender is required to insure the well and septic meet HUD and state and local jurisdiction requirements. The underwriter, not the appraiser, is required to determine feasibility of connecting improvements to public water and/or septic system. Call for inspection of readily observable deficiencies of well or septic systems 15

16 Residential Appraisal Report Improvements Units Number of Stories Property Type Design Year Built Effective Age 16

17 Accessory Units 17

18 Foundation/Basement/Crawl Space Basement Crawl Space Basement Area Basement Finish 18

19 Interior Materials Condition Appraiser is to state what they saw and describe when necessary. What is readily observable? What upgrades did he/she see? 19

20 Interior 20

21 Uniform Residential Appraisal Report Attic The appraiser must enter a minimum head and shoulders and be able to inspect entire area. An attic must have adequate ventilation and be free from defects. Homes with attic access sealed must be opened and inspected. 21

22 Mechanical Systems All utilities should be on at the time of appraisal. 22

23 Uniform Residential Appraisal Improvements 23

24 Property Condition Requirements Determine the overall quality and condition of property. Identify items that require immediate repair (health & safety, structural soundness). Identify items where maintenance has been deferred, which may not require immediate repair. 24

25 Property Condition Requirements Typical property conditions requiring further inspection and/or repair by qualified individuals reflected on the Conditional Commitment, HUD B: Infestation evidence of termites Inoperative or inadequate plumbing, heating or electrical systems Structural failure in framing members Leaking or worn-out roofs Cracked masonry or foundation damage Drainage problems/standing water against foundation/structural Hazardous material on the site 25

26 Property Condition Requirements FHA does not require automatic inspections for the following items and/or conditions in existing properties unless mandated by State or local jurisdiction, customary in the area or lender required: Well (individual water system) Septic Termite Flat and/or unobservable roof 26

27 Uniform Residential Appraisal Report Sales Comparison Approach Comparable Listings The number of comparable properties currently offered for sale, including those under contract, within the subject neighborhood together with the price range. Comparable Sales The number of comparable sales that occurred within the 12-month period preceding the effective date of the appraisal, and within the subject neighborhood, together with the price range. 27

28 Uniform Residential Appraisal Report Sales Comparison Approach 28

29 Uniform Residential Appraisal Report Sales Comparison Approach Golf Course -25, $ $ 2400 > 20% 29

30 Uniform Residential Appraisal Report Sales Comparison Approach 3-car attach 2 car attach car attach car attach % 15% 115, ,000 25% 30

31 Uniform Residential Appraisal Report Sales Comparison Approach Standard Rule 1-5 of the Uniform Standards of Professional Appraisal Practice (USPAP), appraisers are required to analyze any prior sales of a subject property in the previous three years for one to four family residential properties. 31

32 Uniform Appraisal Report Reconciliation Handbook , Appendix D)( The three approaches to value: comparison, cost and income are reconciled with a brief description of the validity of each approach with respect to the subject property appraisal. 32

33 Uniform Residential Appraisal Cost Approach The cost approach is required for: Manufactured Housing (New Construction) Unique properties/properties with specialized improvements Lender s request The name of the cost service and reference page numbers of cost tables or factors required; Reviewer must be able to replicate, and; Remaining economic life line must be completed for every FHA appraisal including condominiums. 33

34 Uniform Residential Appraisal Report Income Approach The Income Approach is not required for FHA appraisals completed on the Uniform Residential Appraisal Report, Fannie Mae Form

35 Required Exhibits: Sketch 35

Be original photographs: MLS photos are not to be used as primary photo")

36 Required Exhibits: Photographs Photographs should: Show front and rear at opposite angles to show all sides of subject property and all improvements Show street scene Include a single photo of each comparable Show the grade of the vacant lot; proposed construction Be taken by appraiser (no people in photos) Be original photographs: MLS photos are not to be used as primary photo 36

37 Common Deficiencies - Photographs Photos reflecting silhouettes or Black Blobs are not acceptable. Imaged photos & documents must also be clear FHA - Serving the American Homebuyer Since

38 Required Exhibits: Location Map Maps Local street map showing location subject & each comparable sale Show proposed roadways and street names 38

39 39

40 Appraisal Practices in a Declining Market Underwriter Responsibilities Review Comments in the Neighborhood Section to determine if the information is adequately supported by the data on the 1004MC. If not, further obtain support for the subject s value through requiring additional sales data from the appraiser and/or an online resource or a review appraisal. 40

41 90 Day Flipping Rule Suspended for Forward Mortgages Cases with a sale date on or after February 1, 2010 that had a prior sale within 90 days may now be processed for mortgage endorsement. 41

42 When is a second appraisal required? Resale date of property is between 1 and 90 days and Resale price is 20% percent or more over the price paid by the seller: Increase must be supported by: full appraisal by an independent FHA roster appraiser or adequate documentation of repair/rehabilition/renovation property inspection Resale date of property is between 91 and 180 days and Resale price is 100% percent or more over the price paid by the seller: 2nd appraisal required 42

43 Appraisal Portability 43

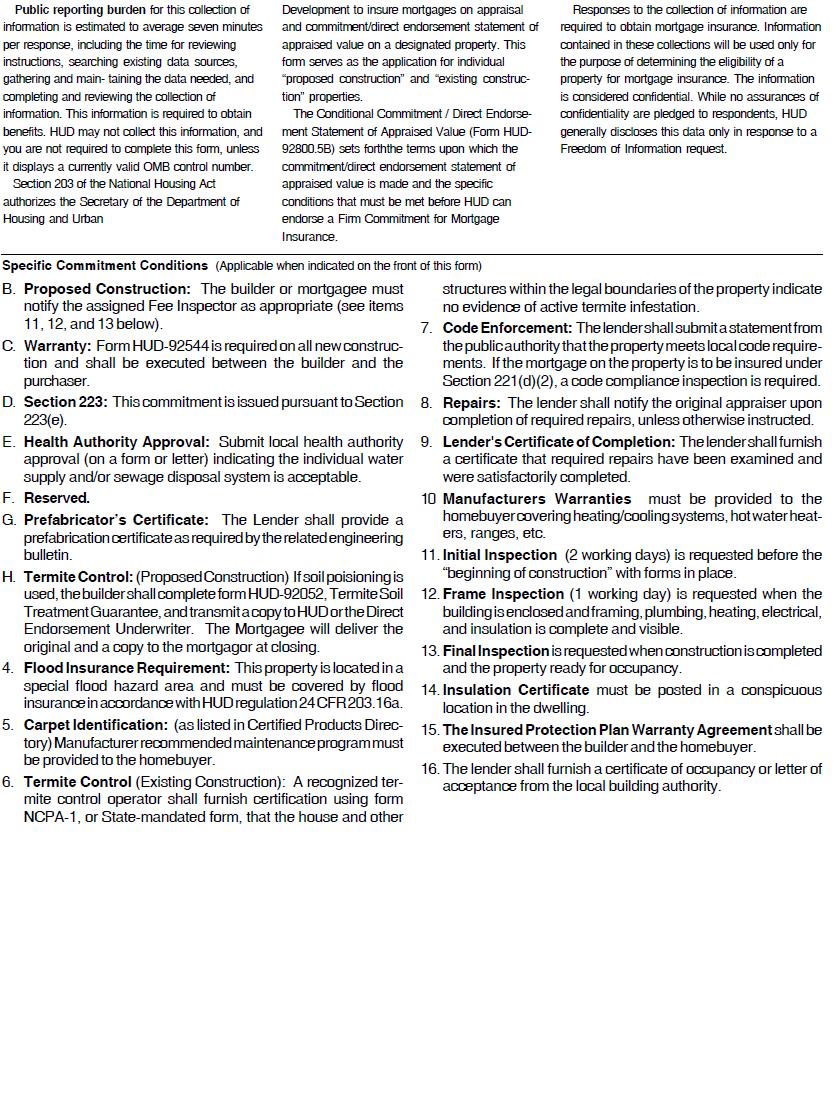

44 Appraisal Validity Without Update: 150 days 120 days plus 30 day extension With Update: 240 days 120 days plus 120 days (update report validity) 44

45 FNMA 1004D 45

46 Conditional Commitment B C A D E F H G 46

47 47

48 The Direct Endorsement Underwriter/HUD Reviewer Analysis of Appraisal Report (HUD ) is used to modify value or for comments. 48

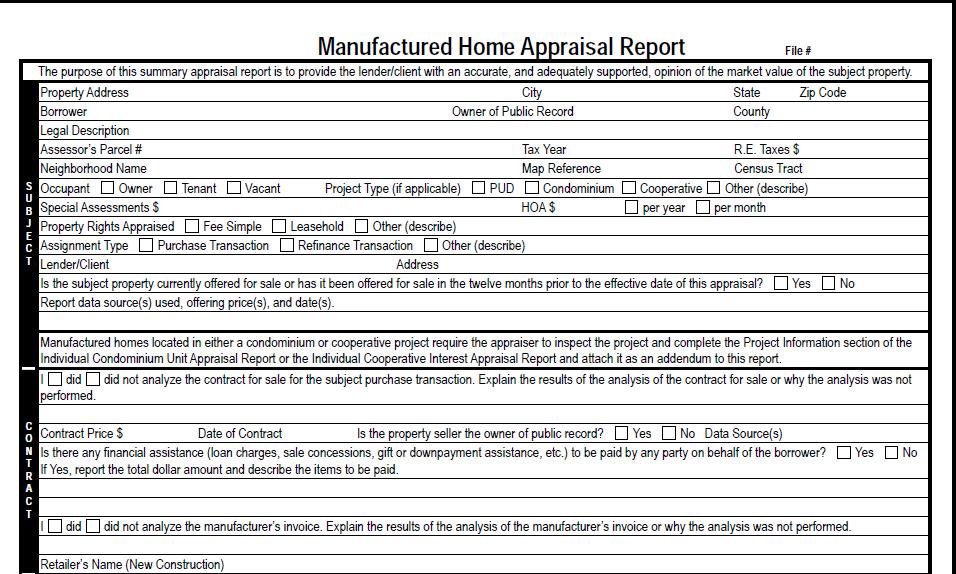

49 Construction Procedures for Single Family The Code of Federal Regulations (CFR) governs when an FHA loan may exceed a 90% Loan to Value predicated by the stage of construction the day the subject property is appraised. 49

50 New Construction 50

51 New Construction 51

52 Construction Exhibits for Appraisal Proposed or Under Construction less than 90% complete Builder s Certification of Plans, Specifications and Site Appraiser to comment on any discrepancies existing between what he/she observes at the site and what was certified to by the builder (HOC Ref Guide 1-8C) Lenders must resolve any noted discrepancies Complete set of Plans and Specifications Description of Materials Appraise subject to completion per plans and specifications and a final inspection by a fee inspector or local authority. 52

53 Appraisal Construction Exhibits Under Construction 90% or more complete Builder s Certification of Plans, Specifications and Site Appraiser notes any repairs and/or alterations required Appraisal is completed subject to the following repairs or alterations and a final inspection by a fee inspector or local authority, i.e. certificate of occupancy. 53

54 A B C 54

55 Appraisal Serving as Final Inspection The appraiser is required to: Take additional photographs of each diagonally opposite front and rear corner of the house to record adequate grading and drainage of the site Must comment in the appraisal report on the acceptance of the grading and drainage Can the Appraisal serve as a final inspection on manufactured housing? X 55

56 56

57 Manufactured Home Appraisal Report 1004C 57

58 Factory Built Homes Manufactured Homes Are constructed to comply with the Federal Manufactured Home Construction & Safety Standards. Modular A.K.A. Factory-Built, are constructed to comply with the local State codes and the Uniform Building Code (UBC) or International Residential Code (IRC) Mobile Homes Constructed prior to June 15, 1976, the effective date of the Federal HUD Code (uninsurable) 58

59 Modular? Manufactured? Site Built? You can no longer tell sitting at the curb. 59

60 60

61 HUD Certification Label, Red Tag HUD Certification Label must be affixed to the taillight end of each transportable section 61

62 DATA PLATE HUD Certification Label Number Serial Number 62

63 Missing HUD Label? Obtain the label and/or serial number from data plate or chassis. Website for IBTS: Freedom of Information Act 63

64 Foundations & Additions or Modifications 64

65 Selection Of Comparables At least two of the comparable sales must be manufactured 65

66 Manufactured Home: Cost Approach 66

67 MORTGAGEE LETTER SUBJECT: Manufactured Housing Policy Guidance Property and Underwriting Eligibility 67

68 Condo or PUD? Condominium Any mortgage covering a one-family unit in a project coupled with an undivided interest in the common areas and facilities which serve the project. May include dwelling units in detached, semi-detached, row garden-type, low or high rise structures. * Note: Remaining Economic Life is to be entered in the Reconciliation section of the Form 1073 as a statement similar to that contained in the Cost Approach section of the other three FHA approved forms, i.e., Estimated Remaining Economic Life Years. PUD (Planned Unit Development) The development contains common areas and facilities owned by a homeowners association which all homeowners must belong and pay lien-supported assessments. FHA - Serving the American Homebuyer Since

69 This form is designed to report an appraisal of a unit in a condominium project based on an interior and exterior inspection of the subject property. 69

70 Condominiums are set forth in the Code of Federal Regulations FHA Approved Condo Project Condominium Approval Process Single Family Housing Mortgagee Letter

71 FHA Connection Condominiums 71

or an acceptable cash flow and operating income statement for investment property (including a two-four unit property in which")

72 Small Residential Income Property Appraisal Form, FNMA 1025 This report form is designed to report an appraisal of a 2-4 unit property. Required exhibits include an Operating Income Statement (Form #216) or an acceptable cash flow and operating income statement for investment property (including a two-four unit property in which the borrower will occupy one unit as a primary residence). 72

73 Handbooks (6/99) Valuation Analysis REV 2 (12/91) Architectural Processing & Inspections REV 1 (3/91) Requirements for existing 1-4 family units (7/94) Appendix K, MPS Proposed construction 1-4 family 73

74 Mortgagee Letters Adoption of the Appraisal Update &/or Completion Report Second Appraisal Reporting Requirements 09-46b Condominium Approval Process for Single Family Housing Appraisal Validity Periods Appraisal Portability Appraiser Independence Condominium Approval Process Single Family Housing Manufactured Housing Policy Guidance Property and Underwriting Eligibility Adoption of Market Conditions Addendum (1004MC) New Construction - Architectural Exhibits Requirements Property Flipping Prohibition Amendment FHA Repair and Inspection Requirements Seller Concessions and Verification of Sales 74

75 Thank you! 75

76 Disclosure The purpose of this presentation is an overview of the subject matter with summation and explanation of recent changes in FHA policy. It introduces and explains, rather than supplants, official policy issued in Handbooks and Mortgagee Letters. If you find a discrepancy between the presentation and Handbooks, Mortgagee Letters, etc., the official policies prevail. Please note the information provided in this training is subject to change. Please consult HUD online Handbooks at asp?address= and Mortgagee Letters through ee/index.cfm for the most recent updates and current policy. 76

Appraisal Engagement Instructions

Appraisal Engagement Instructions OVERVIEW The appraisal report must be prepared by a state licensed or certified appraiser and must comply with the Appraiser Independence Requirements (AIR), Uniform Standards

Appraisal Engagement Instructions OVERVIEW The appraisal report must be prepared by a state licensed or certified appraiser and must comply with the Appraiser Independence Requirements (AIR), Uniform Standards

What issues regarding FHA lending have been raise throughout this chapter and which ones place great responsibility on the appraiser?

The FHA & VA Appraiser: Thriving and Surviving (7 hour CE) This course will provide you with an understanding of the historical and present needs for FHA and VA programs. It focuses on the most current

The FHA & VA Appraiser: Thriving and Surviving (7 hour CE) This course will provide you with an understanding of the historical and present needs for FHA and VA programs. It focuses on the most current

MORTGAGEE LETTER ML-48. FHA Repair and Inspection Requirements for existing properties and revisions to FHA Appraisal Protocol

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT WASHINGTON, DC 20410-8000 ASSISTANT SECRETARY FOR HOUSING- FEDERAL HOUSING COMMISSIONER December 19, 2005 MORTGAGEE LETTER 2005- ML-48 Deleted: 6 TO: ALL

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT WASHINGTON, DC 20410-8000 ASSISTANT SECRETARY FOR HOUSING- FEDERAL HOUSING COMMISSIONER December 19, 2005 MORTGAGEE LETTER 2005- ML-48 Deleted: 6 TO: ALL

March 23, 2009 MORTGAGEE LETTER

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT WASHINGTON, DC 20410-8000 ASSISTANT SECRETARY FOR HOUSING- FEDERAL HOUSING COMMISSIONER March 23, 2009 MORTGAGEE LETTER 2009-09 TO: SUBJECT: ALL APPROVED

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT WASHINGTON, DC 20410-8000 ASSISTANT SECRETARY FOR HOUSING- FEDERAL HOUSING COMMISSIONER March 23, 2009 MORTGAGEE LETTER 2009-09 TO: SUBJECT: ALL APPROVED

SIRVA Mortgage Order Instructions

SIRVA Mortgage Order Instructions Appraiser Trainees: This client does not permit Trainees to sign the appraisal report, however USPAP requirements apply when significant assistance has been provided by

SIRVA Mortgage Order Instructions Appraiser Trainees: This client does not permit Trainees to sign the appraisal report, however USPAP requirements apply when significant assistance has been provided by

MORTGAGEE LETTER ML-468

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT WASHINGTON, DC 20410-8000 ASSISTANT SECRETARY FOR HOUSING- FEDERAL HOUSING COMMISSIONER December 19, 2005 MORTGAGEE LETTER 2005- ML-468 TO: ALL APPROVED

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT WASHINGTON, DC 20410-8000 ASSISTANT SECRETARY FOR HOUSING- FEDERAL HOUSING COMMISSIONER December 19, 2005 MORTGAGEE LETTER 2005- ML-468 TO: ALL APPROVED

APPENDIX A: VALUATION OF REAL ESTATE OWNED PROPERTIES A-1 REAL ESTATE OWNED (REO)

") APPENDIX A: VALUATION OF REAL ESTATE OWNED PROPERTIES 4150.2 A-1 REAL ESTATE OWNED (REO) FHA s Real Estate Owned (REO) properties are a result of paying a claim to a lending institution and the lender

APPENDIX A: VALUATION OF REAL ESTATE OWNED PROPERTIES 4150.2 A-1 REAL ESTATE OWNED (REO) FHA s Real Estate Owned (REO) properties are a result of paying a claim to a lending institution and the lender

Appraisal Review Reminders

Use the following list of reminders as a tool when underwriting the appraisal report. For complete information on appraisal requirements, refer to the Freddie Mac Seller/Servicer Guide (Guide) Chapter

Use the following list of reminders as a tool when underwriting the appraisal report. For complete information on appraisal requirements, refer to the Freddie Mac Seller/Servicer Guide (Guide) Chapter

Appraisal Review Reminders

Use the following list of reminders as a tool when underwriting the appraisal report. For complete information on appraisal requirements, refer to the Freddie Mac Seller/Servicer Guide (Guide) Chapter

Use the following list of reminders as a tool when underwriting the appraisal report. For complete information on appraisal requirements, refer to the Freddie Mac Seller/Servicer Guide (Guide) Chapter

Chapter 5 Fee Appraiser Responsibilities

Chapter 5 Fee Appraiser Responsibilities The fee appraiser is responsible for all aspects of the appraisal process. Important: Certain key appraisal functions may not be delegated to anyone else. Failure

Chapter 5 Fee Appraiser Responsibilities The fee appraiser is responsible for all aspects of the appraisal process. Important: Certain key appraisal functions may not be delegated to anyone else. Failure

Evaluating Your Appraisal

Evaluating Your Appraisal April 28, 2011 Presented by: Brady W. Meadows Mortgage Compliance Advisors Instructions Because of the large number of registrants, the lines will be muted. To ask a question,

Evaluating Your Appraisal April 28, 2011 Presented by: Brady W. Meadows Mortgage Compliance Advisors Instructions Because of the large number of registrants, the lines will be muted. To ask a question,

APPRAISAL REQUIREMENTS FOR SUNTENDER VALUATIONS, INC. Updated 03/26/2018

APPRAISAL REQUIREMENTS FOR SUNTENDER VALUATIONS, INC. Updated 03/26/2018 STOP Call Suntender Valuations if subject is a refinance transaction however it has been listed for sale in the past 3 months, unless

APPRAISAL REQUIREMENTS FOR SUNTENDER VALUATIONS, INC. Updated 03/26/2018 STOP Call Suntender Valuations if subject is a refinance transaction however it has been listed for sale in the past 3 months, unless

FHA Handbook, Appendix D (January 2006) - PDF Page 1

- PDF Page 1") APPENDIX D: VALUATION PROTOCOL FHA Handbook, Appendix D (January 2006) - PDF Page 1 The appraisal process is the lender s tool for determining if a property meets the minimum requirements and eligibility

APPENDIX D: VALUATION PROTOCOL FHA Handbook, Appendix D (January 2006) - PDF Page 1 The appraisal process is the lender s tool for determining if a property meets the minimum requirements and eligibility

Appraisal Review: Analyzing the 1004

Appraisal Review: Analyzing the 1004 1 LIVE ONLINE PARTICIPANT GUIDE Version: 8.12 Table of Contents The Purpose of the Appraisal... 3 Define Market Value... 3 Scenario 1 (John Johnson report) - 1004 Uniform

Appraisal Review: Analyzing the 1004 1 LIVE ONLINE PARTICIPANT GUIDE Version: 8.12 Table of Contents The Purpose of the Appraisal... 3 Define Market Value... 3 Scenario 1 (John Johnson report) - 1004 Uniform

Chapter 8 Qualifying Property

The 3 "Cs" of Lending Capacity to Pay does the borrower make enough money to repay loan? lenders use qualifying ratios Creditworthiness [Character] is the borrower likely to repay loan on time? lenders

The 3 "Cs" of Lending Capacity to Pay does the borrower make enough money to repay loan? lenders use qualifying ratios Creditworthiness [Character] is the borrower likely to repay loan on time? lenders

Manufactured Home Requirements

Manufactured Home Requirements All end agency (FHA/FNMA/VA/USDA) guidelines must always be met. This is provided as guidance, but if the end agency requirements are more restrictive, those must be followed.

Manufactured Home Requirements All end agency (FHA/FNMA/VA/USDA) guidelines must always be met. This is provided as guidance, but if the end agency requirements are more restrictive, those must be followed.

UNIFORM APPRAISAL DATASET (UAD) FHA SPOTLIGHT - SELECTION AND VERIFICATION OF COMPARABLE SALES

FHA SPOTLIGHT - SELECTION AND VERIFICATION OF COMPARABLE SALES") Spring 2011 Issue 3 FHA APPRAISER In This Issue: Welcome to the third issue of the Federal Housing Administration Appraiser Roster Newsletter. We hope you will find it informative. Uniform Appraisal Dataset

Spring 2011 Issue 3 FHA APPRAISER In This Issue: Welcome to the third issue of the Federal Housing Administration Appraiser Roster Newsletter. We hope you will find it informative. Uniform Appraisal Dataset

The ATA Board of Directors concurred that this information be shared with not only ATA members, but all of the Appraisers in Texas.

General Announcement 11 19 2013 Subject: FHA Seminars in Texas Points of Misunderstanding On September 12, 2013, several ATA members contacted the ATA about contradictory statements which has caused some

General Announcement 11 19 2013 Subject: FHA Seminars in Texas Points of Misunderstanding On September 12, 2013, several ATA members contacted the ATA about contradictory statements which has caused some

All audio for this webinar is through your computer there is no separate call-in number

All audio for this webinar is through your computer there is no separate call-in number Please ensure that you are able to receive sound through your computer and that your speakers are un-muted If you

All audio for this webinar is through your computer there is no separate call-in number Please ensure that you are able to receive sound through your computer and that your speakers are un-muted If you

Manufactured Home Requirements

Manufactured Home Requirements All end agency (FHA/FNMA/VA/USDA) guidelines must always be met. This is provided as guidance, but if the end agency requirements are more restrictive, those must be followed.

Manufactured Home Requirements All end agency (FHA/FNMA/VA/USDA) guidelines must always be met. This is provided as guidance, but if the end agency requirements are more restrictive, those must be followed.

FHA -203K And Renovation Loans

FHA -203K And Renovation Loans What is a 203K FHA Loan or a Renovation Loan? Both loan types enable homebuyers and homeowners to finance both the purchase (or refinancing) of a house and the cost of its

FHA -203K And Renovation Loans What is a 203K FHA Loan or a Renovation Loan? Both loan types enable homebuyers and homeowners to finance both the purchase (or refinancing) of a house and the cost of its

ii. Minimum Property Requirements and Minimum Property Standards

Underwriting the Property The Mortgagee must underwrite the completed appraisal report to determine if the Property provides sufficient collateral for the FHA-insured Mortgage. The appraisal and Property

Underwriting the Property The Mortgagee must underwrite the completed appraisal report to determine if the Property provides sufficient collateral for the FHA-insured Mortgage. The appraisal and Property

SECTION 5 ELIGIBLE RESIDENCE

5.01 Qualifying Residences Qualifying Residences must be located within the State of North Dakota. The Residence must be a fully completed, one- to four-unit Residence including townhouses, condominiums,

5.01 Qualifying Residences Qualifying Residences must be located within the State of North Dakota. The Residence must be a fully completed, one- to four-unit Residence including townhouses, condominiums,

FHA Reference Materials for This Seminar... 1 Primary Audience for This Seminar... 1 Not Yet Approved for FHA Appraisal Assignments?...

Table of Contents Overview... vii Seminar Schedule... xi Section 1 Introduction FHA Reference Materials for This Seminar... 1 Primary Audience for This Seminar... 1 Not Yet Approved for FHA Appraisal Assignments?...

Table of Contents Overview... vii Seminar Schedule... xi Section 1 Introduction FHA Reference Materials for This Seminar... 1 Primary Audience for This Seminar... 1 Not Yet Approved for FHA Appraisal Assignments?...

Announcement March 24, 2005

Announcement 05-02 March 24, 2005 Amends these Guides: Selling Final Appraisal Report Forms Part XI: Property and Appraisal Analysis Guidelines In Lender Announcement 04-07 dated November 8, 2004, we released

Announcement 05-02 March 24, 2005 Amends these Guides: Selling Final Appraisal Report Forms Part XI: Property and Appraisal Analysis Guidelines In Lender Announcement 04-07 dated November 8, 2004, we released

Selling Part VII - Property and Appraisal Analysis

Selling Part VII - Property and Appraisal Analysis This Part--Property and Appraisal Analysis--details our general requirements for analyzing the property appraisal aspects of conventional mortgages secured

Selling Part VII - Property and Appraisal Analysis This Part--Property and Appraisal Analysis--details our general requirements for analyzing the property appraisal aspects of conventional mortgages secured

REV General Proposed Additions and Alterations Compliance with Codes 1-1

TABLE OF CONTENTS Paragraph Page REQUIREMENTS FOR EXISTING HOUSING - ONE TO FOUR FAMILY LIVING UNITS Chapter 1 - APPLICATION 1-1 General 1-1 1-2 Proposed Additions and Alterations 1-1 1-3 Compliance with

TABLE OF CONTENTS Paragraph Page REQUIREMENTS FOR EXISTING HOUSING - ONE TO FOUR FAMILY LIVING UNITS Chapter 1 - APPLICATION 1-1 General 1-1 1-2 Proposed Additions and Alterations 1-1 1-3 Compliance with

THE FUNDAMENTALS OF MANUFACTURED LENDING

THE FUNDAMENTALS OF MANUFACTURED LENDING Last Revised: 06/07/17 DISCLAIMER These materials are intended for AFR internal use and client training procedures only. This is neither legal advice nor a substitute

THE FUNDAMENTALS OF MANUFACTURED LENDING Last Revised: 06/07/17 DISCLAIMER These materials are intended for AFR internal use and client training procedures only. This is neither legal advice nor a substitute

Paramount Residential Mortgage Group (PRMG) HUD REPAIR ESCROWS UNDERWRITING AND APPRAISAL REQUIREMENTS

HUD REPAIR ESCROWS UNDERWRITING AND APPRAISAL REQUIREMENTS") Paramount Residential Mortgage Group (PRMG) HUD REPAIR ESCROWS UNDERWRITING AND APPRAISAL REQUIREMENTS PURPOSE This is an outline of specific requirements for HUD repair escrows. Follow the published FHA

Paramount Residential Mortgage Group (PRMG) HUD REPAIR ESCROWS UNDERWRITING AND APPRAISAL REQUIREMENTS PURPOSE This is an outline of specific requirements for HUD repair escrows. Follow the published FHA

2. Is the information in the contract section complete and accurate? Yes No Not Applicable If Yes, provide a brief summary.

The purpose of this appraisal field review report is to provide the lender/client with an opinion on the accuracy of the appraisal report under review. Property Address City State Zip Code Borrower Owner

The purpose of this appraisal field review report is to provide the lender/client with an opinion on the accuracy of the appraisal report under review. Property Address City State Zip Code Borrower Owner

MANUFACTURED HOME GUIDELINES

Table of Contents 1. Manufactured Housing Overview... 3 2. Loan Eligibility and Product Codes... 3 3. Eligible Mortgages... 3 4. Ineligible Mortgages... 3 5. Manufactured Home Standards... 4 6. Definition

Table of Contents 1. Manufactured Housing Overview... 3 2. Loan Eligibility and Product Codes... 3 3. Eligible Mortgages... 3 4. Ineligible Mortgages... 3 5. Manufactured Home Standards... 4 6. Definition

MANUFACTURED HOME GUIDELINES

Table of Contents 1. Loan Eligibility..... 2 2. Eligible Mortgages... 2 3. Ineligible Mortgages... 2 4. Manufactured Home Standards... 2 5. Definition of Common Terms... 3 6. Property Eligibility... 4

Table of Contents 1. Loan Eligibility..... 2 2. Eligible Mortgages... 2 3. Ineligible Mortgages... 2 4. Manufactured Home Standards... 2 5. Definition of Common Terms... 3 6. Property Eligibility... 4

APPRAISAL OF LOCATED AT:

APPRAISAL OF LOCATED AT: 5905 S County Road K South Range, WI 54874 February 18, 2015 In accordance with your request, I have appraised the real property at: 5905 S County Road K South Range, WI 54874

APPRAISAL OF LOCATED AT: 5905 S County Road K South Range, WI 54874 February 18, 2015 In accordance with your request, I have appraised the real property at: 5905 S County Road K South Range, WI 54874

Appraisal and Property Related Frequently Asked Questions (FAQs) Updated September 2014

Updated September 2014") Appraisal and Property Related Frequently Asked Questions (FAQs) Updated September 2014 This FAQ document provides responses to common questions related to Fannie Mae s property eligibility and appraisal

Appraisal and Property Related Frequently Asked Questions (FAQs) Updated September 2014 This FAQ document provides responses to common questions related to Fannie Mae s property eligibility and appraisal

50 Most Common Appraisal Review Deficiencies Webinar 9:00 AM Mountain Time

50 Most Common Appraisal Review Deficiencies Webinar 9:00 AM Mountain Time All audio for this webinar is through your computer there is no separate call-in number Please ensure that you are able to receive

50 Most Common Appraisal Review Deficiencies Webinar 9:00 AM Mountain Time All audio for this webinar is through your computer there is no separate call-in number Please ensure that you are able to receive

APPRAISAL OF REAL PROPERTY

Home Appraisals, Inc. (866) 533-7173 APPRAISAL OF REAL PROPERTY File # LOCATED AT Field Review Form Sample FOR OPINION OF VALUE 35, AS OF 11/1/7 TABLE OF CONTENTS One-Unit Field Review... 1 General Text

Home Appraisals, Inc. (866) 533-7173 APPRAISAL OF REAL PROPERTY File # LOCATED AT Field Review Form Sample FOR OPINION OF VALUE 35, AS OF 11/1/7 TABLE OF CONTENTS One-Unit Field Review... 1 General Text

FHA Single Family Housing Policy Handbook TABLE OF CONTENTS

Table of Contents 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 FHA Single Family Housing Policy Handbook TABLE OF CONTENTS IV. APPRAISER AND

Table of Contents 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 FHA Single Family Housing Policy Handbook TABLE OF CONTENTS IV. APPRAISER AND

FHA Office of Single Family Housing. Appraisals Module 3A

Appraisals Module 3A Single Family Housing Policy Handbook 4000.1 Title II Insured Housing Program Forward Mortgages Origina@on through Post- Closing/Endorsement Gary E. Eisenbraun Branch Chief Appraisal/Technical

Appraisals Module 3A Single Family Housing Policy Handbook 4000.1 Title II Insured Housing Program Forward Mortgages Origina@on through Post- Closing/Endorsement Gary E. Eisenbraun Branch Chief Appraisal/Technical

Uniform Residential Appraisal Report (URAR) Model Appraisal

Model Appraisal") Basic Appraisal Procedures Residential Applications & Model Appraisals 15-13 Uniform Residential Appraisal Report (URAR) Model Appraisal On the following pages are examples of a completed Fannie Mae/Freddie

Basic Appraisal Procedures Residential Applications & Model Appraisals 15-13 Uniform Residential Appraisal Report (URAR) Model Appraisal On the following pages are examples of a completed Fannie Mae/Freddie

APPRAISED PROPERTY VALUE: FACT OR FICTION

APPRAISED PROPERTY VALUE: FACT OR FICTION What every real estate agent should know about the appraisal process. RHONDA IVEY-LENTINI GRI,ABR,SRS,SRES, E-PRO,GREEN,MRP,SFR,HAFA,RENE DYNAMIC DIRECTIONS, INC.

APPRAISED PROPERTY VALUE: FACT OR FICTION What every real estate agent should know about the appraisal process. RHONDA IVEY-LENTINI GRI,ABR,SRS,SRES, E-PRO,GREEN,MRP,SFR,HAFA,RENE DYNAMIC DIRECTIONS, INC.

CENTER FOR PROFESSIONAL EDUCATION 9590 West 14 th Avenue Lakewood, CO (720)

") CENTER FOR PROFESSIONAL EDUCATION 9590 West 14 th Avenue Lakewood, CO 80215 (720) 889-0797 Approved and Regulated by Division of Private Occupational Schools, Department of Higher Education, State of Colorado

CENTER FOR PROFESSIONAL EDUCATION 9590 West 14 th Avenue Lakewood, CO 80215 (720) 889-0797 Approved and Regulated by Division of Private Occupational Schools, Department of Higher Education, State of Colorado

Appraisal Stream Restricted Use Residential Appraisal Report

Appraisal Stream Restricted Use Residential Appraisal Report File No. 769kemplin This report is limited to the sole and exclusive use of the client. The appraiser's opinions and conclusions set forth in

Appraisal Stream Restricted Use Residential Appraisal Report File No. 769kemplin This report is limited to the sole and exclusive use of the client. The appraiser's opinions and conclusions set forth in

Demonstration Appraisal Report Utilizing a Form Report

Demonstration Appraisal Report Utilizing a Form Report National Association of Independent Fee Appraisers 330 North Wabash Avenue, Suite 2000 Chicago, IL 60611 Phone: (312) 321-6830 Fax: (312) 673-6652

Demonstration Appraisal Report Utilizing a Form Report National Association of Independent Fee Appraisers 330 North Wabash Avenue, Suite 2000 Chicago, IL 60611 Phone: (312) 321-6830 Fax: (312) 673-6652

10454 South Green Bay Avenue Chicago, IL Client and Order Detail. Subject Property Information

Client and Order Detail Client: Address: 10454 South Green Bay Avenue Client Loan Number: C/S/Z: Order Number: 0290016663 County: Cook Inspection Type: BPO-Interior BPO Agent: Lopez, Leo Mortgagor's Name:

Client and Order Detail Client: Address: 10454 South Green Bay Avenue Client Loan Number: C/S/Z: Order Number: 0290016663 County: Cook Inspection Type: BPO-Interior BPO Agent: Lopez, Leo Mortgagor's Name:

203K Standard Renovation Loan

203K Standard Renovation Loan RI Mortgage Broker Licene # 20082309LB MA Mortgage Broker License # MB3915 FL Mortgage Broker License # MBR475 PA Mortgage Broker License # 60246 Atlantic Mortgage & Finance

203K Standard Renovation Loan RI Mortgage Broker Licene # 20082309LB MA Mortgage Broker License # MB3915 FL Mortgage Broker License # MBR475 PA Mortgage Broker License # 60246 Atlantic Mortgage & Finance

Table of Contents F H A/VA M ANUF ACTURED HOME GUID E L I N E S

Table of Contents 1. Table of Contents... 1 2. FHA/VA Loan Eligibility... 3 3. FHA/VA FICO Score... 3 4. FHA/VA Eligible Mortgages... 3 5. FHA/VA Ineligible Mortgages... 4 6. FHA/VA Eligible Property Types...

Table of Contents 1. Table of Contents... 1 2. FHA/VA Loan Eligibility... 3 3. FHA/VA FICO Score... 3 4. FHA/VA Eligible Mortgages... 3 5. FHA/VA Ineligible Mortgages... 4 6. FHA/VA Eligible Property Types...

To all Appraisers: Brief Overview:

To all Appraisers: As the appraisal industry continues to change, the demand for alternative valuation solutions grows. That is why is excited to announce the addition of a new product - the Desktop Appraisal

To all Appraisers: As the appraisal industry continues to change, the demand for alternative valuation solutions grows. That is why is excited to announce the addition of a new product - the Desktop Appraisal

Overall Trend Section Example Seller Concessions Foreclosure Sales and Summary/Analysis of Data... 13

Appraisal and Property-Related Frequently Asked Questions (FAQs) This FAQ document provides responses to common questions related to Fannie Mae s property eligibility and appraisal policies. Following

Appraisal and Property-Related Frequently Asked Questions (FAQs) This FAQ document provides responses to common questions related to Fannie Mae s property eligibility and appraisal policies. Following

Land, Agricultural Improvements, CAFO, Rural Residence, Farm

*--FSA Appraisal Guidelines Land, Agricultural Improvements, CAFO, Rural Residence, Farm The following information elements and content descriptions are provided as guidelines to assist lenders and appraisers

*--FSA Appraisal Guidelines Land, Agricultural Improvements, CAFO, Rural Residence, Farm The following information elements and content descriptions are provided as guidelines to assist lenders and appraisers

What else are FHA appraisers looking for?

What else are FHA appraisers looking for? By: Oscar Castillo Broker Associate (858) 775-1057 Residential Brokerage San Diego, California email: Oscar@OscarSellsHomes.com If you plan to use a Federal Housing

What else are FHA appraisers looking for? By: Oscar Castillo Broker Associate (858) 775-1057 Residential Brokerage San Diego, California email: Oscar@OscarSellsHomes.com If you plan to use a Federal Housing

Unpermitted Additions and Garage Conversions Job Aid 8/14/17

Unpermitted Additions and Garage Conversions Job Aid 8/14/17 Issue Zoning Requirements Unpermitted Addition and Garage Conversion Additional living area added to the primary dwelling by addition or conversion

Unpermitted Additions and Garage Conversions Job Aid 8/14/17 Issue Zoning Requirements Unpermitted Addition and Garage Conversion Additional living area added to the primary dwelling by addition or conversion

Manufactured Home Program Guide FHA, VA and USDA

Manufactured Home Program Guide FHA, VA and USDA Non-Delegated Lending April 18, 2016 Manufactured Home Program Guide...1 Definition...3 Overview...3 Manufactured Homes Eligible States...3 Property Eligibility...3

Manufactured Home Program Guide FHA, VA and USDA Non-Delegated Lending April 18, 2016 Manufactured Home Program Guide...1 Definition...3 Overview...3 Manufactured Homes Eligible States...3 Property Eligibility...3

RESERVED FOR FUTURE USE RESERVED FOR FUTURE USE

B. Title II Insured Housing Programs Reverse Mortgages RESERVED FOR FUTURE USE This section is reserved for future use, and until such time, FHA-approved Mortgagees must continue to comply with all applicable

B. Title II Insured Housing Programs Reverse Mortgages RESERVED FOR FUTURE USE This section is reserved for future use, and until such time, FHA-approved Mortgagees must continue to comply with all applicable

Fannie Mae Single Family/2007 Selling Guide/Part XI: Property and Appraisal Guidelines/Part XI: Property and Appraisal Guidelines

Fannie Mae Single Family/2007 Selling Guide/Part XI: Property and Appraisal Guidelines/Part XI: Property and Appraisal Guidelines Part XI: Property and Appraisal Guidelines Copyright, 2001-2007, Fannie

Fannie Mae Single Family/2007 Selling Guide/Part XI: Property and Appraisal Guidelines/Part XI: Property and Appraisal Guidelines Part XI: Property and Appraisal Guidelines Copyright, 2001-2007, Fannie

Manufactured Home Program Guide FHA, VA and USDA

Manufactured Home Program Guide FHA, VA and USDA Non-Delegated Lending December 14, 2015 Manufactured Home Program Guide...1 Definition...3 Overview...3 Manufactured Homes Eligible States...3 Property

Manufactured Home Program Guide FHA, VA and USDA Non-Delegated Lending December 14, 2015 Manufactured Home Program Guide...1 Definition...3 Overview...3 Manufactured Homes Eligible States...3 Property

Groundwork Appraisal Survey Procedure Data Collection Report Requirements February 2017

Groundwork Appraisal Survey Procedure Data Collection Report Requirements February 2017 Accurate / Groundwork wo are they?? Accurate / Groundwork is an Ohio based company Groundwork vision is to provide

Groundwork Appraisal Survey Procedure Data Collection Report Requirements February 2017 Accurate / Groundwork wo are they?? Accurate / Groundwork is an Ohio based company Groundwork vision is to provide

Exterior Only Inspection Residential Appraisal Report File #

SUBJECT Summary Appraisal Report Brian J. Davis & Associates Exterior Only Inspection Residential Appraisal Report File # Page #3 The purpose of this summary appraisal report is to provide the lender/client

SUBJECT Summary Appraisal Report Brian J. Davis & Associates Exterior Only Inspection Residential Appraisal Report File # Page #3 The purpose of this summary appraisal report is to provide the lender/client

Uniform Residential Appraisal Report File #

D.S. Murphy & Associates FHA/VA Case No. SUBJECT The purpose of this summary appraisal report is to provide the lender/client with an accurate, and adequately supported, opinion of the market value of

D.S. Murphy & Associates FHA/VA Case No. SUBJECT The purpose of this summary appraisal report is to provide the lender/client with an accurate, and adequately supported, opinion of the market value of

Fannie Mae Selling Guide (04/12/2002) Part XI - Property and Appraisal Guidelines

Part XI - Property and Appraisal Guidelines") Fannie Mae Selling Guide (04/12/2002) Part XI - Property and Appraisal Guidelines This Part-Property and Appraisal Guidelines-details our general requirements for analyzing the property appraisal aspects

Fannie Mae Selling Guide (04/12/2002) Part XI - Property and Appraisal Guidelines This Part-Property and Appraisal Guidelines-details our general requirements for analyzing the property appraisal aspects

4 PROPERTY REQUIREMENTS

4 PROPERTY REQUIREMENTS IN GENERAL Only Single-Family Residences located in the state of Washington may be financed under the Program. QUALIFYING SINGLE-FAMILY RESIDENCES Single-family detached, attached,

4 PROPERTY REQUIREMENTS IN GENERAL Only Single-Family Residences located in the state of Washington may be financed under the Program. QUALIFYING SINGLE-FAMILY RESIDENCES Single-family detached, attached,

Section Leasehold Estate Guidelines

Section 1.10 - In This Section This section contains the following topics: Overview... 2 General... 2 Related Bulletins... 3 Identifying a Leasehold Estate... 4 Occupancy/Property Types... 5 Eligible Occupancy/

Section 1.10 - In This Section This section contains the following topics: Overview... 2 General... 2 Related Bulletins... 3 Identifying a Leasehold Estate... 4 Occupancy/Property Types... 5 Eligible Occupancy/

Conditional Commitment Direct Endorsement Statement of Appraised Value

Conditional Commitment Direct Endorsement Statement of Appraised Value General Commitment Conditions U.S. Department of Housing and Urban Development Office of Housing Federal Housing Commissioner 13390:LN_AppNum

Conditional Commitment Direct Endorsement Statement of Appraised Value General Commitment Conditions U.S. Department of Housing and Urban Development Office of Housing Federal Housing Commissioner 13390:LN_AppNum

Be it enacted by the People of the State of Illinois,

AN ACT concerning property. Be it enacted by the People of the State of Illinois, represented in the General Assembly: Section 5. The Residential Real Property Disclosure Act is amended by changing Section

AN ACT concerning property. Be it enacted by the People of the State of Illinois, represented in the General Assembly: Section 5. The Residential Real Property Disclosure Act is amended by changing Section

BPO Best Practices Guide

BPO Best Practices Guide A Step by Step Guide for Completing BPO Reports Version: 1.0.0 Published: 03/01/2011 Global DMS, 1555 Bustard Road, Suite 300, Lansdale, PA 19446 2014, All Rights Reserved. Table

BPO Best Practices Guide A Step by Step Guide for Completing BPO Reports Version: 1.0.0 Published: 03/01/2011 Global DMS, 1555 Bustard Road, Suite 300, Lansdale, PA 19446 2014, All Rights Reserved. Table

VA MATRIX. Last Updated: June Property of Docutech, LLC Page 1 Version

VA MATRIX Legal Disclaimer: This table was compiled for informational and reference purposes only. It does not constitute, nor should it be used as a substitute for, legal advice. No warranty, either expressed

VA MATRIX Legal Disclaimer: This table was compiled for informational and reference purposes only. It does not constitute, nor should it be used as a substitute for, legal advice. No warranty, either expressed

RESTRICTED APPRAISAL REPORT

Restricted Use Appraisal Report Thomas J. Schulte & Associates Page #1 RESTRICTED APPRAISAL REPORT SUBJECT ASSIGNMENT Property City: Zip Code: County: Legal Description: Assessor's Parcel #: Tax Year:

Restricted Use Appraisal Report Thomas J. Schulte & Associates Page #1 RESTRICTED APPRAISAL REPORT SUBJECT ASSIGNMENT Property City: Zip Code: County: Legal Description: Assessor's Parcel #: Tax Year:

A GUIDE TO HOUSING ARCHITECTURE IN SOUTH CENTRAL WISCONSIN

A GUIDE TO HOUSING ARCHITECTURE IN SOUTH CENTRAL WISCONSIN The purpose of this guide is to provide REALTORS with a common frame of reference in identifying housing architecture. In compiling the guide,

A GUIDE TO HOUSING ARCHITECTURE IN SOUTH CENTRAL WISCONSIN The purpose of this guide is to provide REALTORS with a common frame of reference in identifying housing architecture. In compiling the guide,

Individual Cooperative Interest Appraisal Report

PURPOSE Individual Cooperative Interest Appraisal Report The purpose of this appraisal report is to provide the client with a credible opinion of the defined value of the subject property, given the intended

PURPOSE Individual Cooperative Interest Appraisal Report The purpose of this appraisal report is to provide the client with a credible opinion of the defined value of the subject property, given the intended

This chapter describes Fannie Mae s project standards, policies, and requirements.

Chapter 2, Project Standards Chapter B4-2, Project Standards Project Standards Click to see prior version of topic Introduction This chapter describes Fannie Mae s project standards, policies, and requirements.

Chapter 2, Project Standards Chapter B4-2, Project Standards Project Standards Click to see prior version of topic Introduction This chapter describes Fannie Mae s project standards, policies, and requirements.

FHA Single Family Housing Policy Handbook Table of Contents

FHA Single Family Housing Policy Handbook Table of Contents b. Disasters and 203(h) Mortgage Insurance for Disaster Victims... 384 c. Energy Efficient Mortgages... 387 d. Refinances... 393 e. Refinance

FHA Single Family Housing Policy Handbook Table of Contents b. Disasters and 203(h) Mortgage Insurance for Disaster Victims... 384 c. Energy Efficient Mortgages... 387 d. Refinances... 393 e. Refinance

June 12, 2009 MORTGAGEE LETTER

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT WASHINGTON, DC 20410-8000 ASSISTANT SECRETARY FOR HOUSING- FEDERAL HOUSING COMMISSIONER June 12, 2009 MORTGAGEE LETTER 2009-19 TO: ALL APPROVED MORTGAGEES

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT WASHINGTON, DC 20410-8000 ASSISTANT SECRETARY FOR HOUSING- FEDERAL HOUSING COMMISSIONER June 12, 2009 MORTGAGEE LETTER 2009-19 TO: ALL APPROVED MORTGAGEES

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT WASHINGTON, DC

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT WASHINGTON, DC 20410-8000 ASSISTANT SECRETARY FOR HOUSING- FEDERAL HOUSING COMMISSIONER November 6, 2009 MORTGAGEE LETTER 2009-46 B TO: SUBJECT: ALL APPROVED

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT WASHINGTON, DC 20410-8000 ASSISTANT SECRETARY FOR HOUSING- FEDERAL HOUSING COMMISSIONER November 6, 2009 MORTGAGEE LETTER 2009-46 B TO: SUBJECT: ALL APPROVED

Uniform Appraisal Dataset (UAD) Frequently Asked Questions

Frequently Asked Questions") Uniform Appraisal Dataset (UAD) Frequently Asked Questions July 13, 2014 Updated for formatting May 15, 2017 The following provides answers to questions frequently asked about Fannie Mae s and Freddie

Uniform Appraisal Dataset (UAD) Frequently Asked Questions July 13, 2014 Updated for formatting May 15, 2017 The following provides answers to questions frequently asked about Fannie Mae s and Freddie

Condo - PUD Project Review Manual

Table of Contents Condo - PUD Project Review Manual Section 1: PRMG Project Approval Section 2: Limited/Streamlined Condo Project Review Section 3: CPM Review Section 4: Lender Full Condo Review Section

Table of Contents Condo - PUD Project Review Manual Section 1: PRMG Project Approval Section 2: Limited/Streamlined Condo Project Review Section 3: CPM Review Section 4: Lender Full Condo Review Section

Small Residential Income Property Appraisal Report File #

SUBJECT Summary Appraisal Report Brian J. Davis & Associates Small Residential Income Property Appraisal Report File # Page #4 The purpose of this summary appraisal report is to provide the lender/client

SUBJECT Summary Appraisal Report Brian J. Davis & Associates Small Residential Income Property Appraisal Report File # Page #4 The purpose of this summary appraisal report is to provide the lender/client

Continental Real Estate Services, Inc. ACTIVE TO SOLD ADJUSTMENT File No. Case No. Borrower Property Address City County State Zip Code

ACTIVE TO SOLD ADJUSTMENT Property Generally, when an appraiser appraises a unit in a cooperative project, he or she should use sales of cooperative units as comparables. However, the appraiser may use

ACTIVE TO SOLD ADJUSTMENT Property Generally, when an appraiser appraises a unit in a cooperative project, he or she should use sales of cooperative units as comparables. However, the appraiser may use

Exam Emphasis: Approximately 15 questions

Exam Emphasis: Approximately 5 questions Agency Relationships - or WB forms.. The listing broker is the seller s. 2. A licensee writes an offer for a buyer on the licensee s listing. The buyer is the licensee

Exam Emphasis: Approximately 5 questions Agency Relationships - or WB forms.. The listing broker is the seller s. 2. A licensee writes an offer for a buyer on the licensee s listing. The buyer is the licensee

Guidance for Lenders and Appraisers April 2009

Guidance for Lenders and Appraisers April 2009 Fannie Mae views lenders as our partners in ensuring the continued viability of the residential lending market and the continued availability of affordable

Guidance for Lenders and Appraisers April 2009 Fannie Mae views lenders as our partners in ensuring the continued viability of the residential lending market and the continued availability of affordable

3-2 ORDERING THE APPRAISAL AND OBTAINING A CASE NUMBER. To order an appraisal and receive a case number, a lender should do the following:

CHAPTER 3. PROPERTY ANALYSIS 3-1 PURPOSE. This chapter explains the procedures for the lender to follow in submitting the property for valuation analysis. The procedures for the local HUD office to follow

CHAPTER 3. PROPERTY ANALYSIS 3-1 PURPOSE. This chapter explains the procedures for the lender to follow in submitting the property for valuation analysis. The procedures for the local HUD office to follow

173 Technology Drive, Irvine, California 92618

173 Technology Drive, Irvine, California 92618 This engagement letter serves as a contract between the vendor listed and SWBC Lending Solutions and can ONLY be completed by the appraiser listed. The appraiser

173 Technology Drive, Irvine, California 92618 This engagement letter serves as a contract between the vendor listed and SWBC Lending Solutions and can ONLY be completed by the appraiser listed. The appraiser

Freddie Mac Condominium Unit Mortgages

For all mortgages secured by a Condominium Unit in a Condominium Project, the Seller must perform an underwriting review of the Condominium Project to ensure the mortgage and the project meet the requirements

For all mortgages secured by a Condominium Unit in a Condominium Project, the Seller must perform an underwriting review of the Condominium Project to ensure the mortgage and the project meet the requirements

SECURITYNATIONAL MORTGAGE COMPANY

SECURITYNATIONAL MORTGAGE COMPANY INFORMATION ON FNMA S LOAN QUALITY INITIATIVE OVERVIEW ON UMDP STANDARDIZED MORTGAGE DATA AND FILE FORMAT STANDARDS SecurityNational Mortgage Company Internal use only

SECURITYNATIONAL MORTGAGE COMPANY INFORMATION ON FNMA S LOAN QUALITY INITIATIVE OVERVIEW ON UMDP STANDARDIZED MORTGAGE DATA AND FILE FORMAT STANDARDS SecurityNational Mortgage Company Internal use only

A GUIDE TO HOUSING ARCHITECTURE IN SOUTH CENTRAL WISCONSIN

A GUIDE TO HOUSING ARCHITECTURE IN SOUTH CENTRAL WISCONSIN The purpose of this guide is to provide REALTORS with a common frame of reference in identifying housing architecture. In compiling the guide,

A GUIDE TO HOUSING ARCHITECTURE IN SOUTH CENTRAL WISCONSIN The purpose of this guide is to provide REALTORS with a common frame of reference in identifying housing architecture. In compiling the guide,

Pre-Listing Activities. Listing Appointment Presentation

The True Value of a Realtor: 184 Tasks Surveys show that many homeowners and homebuyers are not aware of the true value of a Realtor. Realtors perform the following 184 tasks, and while the list may differ

The True Value of a Realtor: 184 Tasks Surveys show that many homeowners and homebuyers are not aware of the true value of a Realtor. Realtors perform the following 184 tasks, and while the list may differ

FROM: Russell T. Davis (Signed by Tom Hannah) for Administrator Housing and Community Facilities Programs

for Administrator Housing and Community Facilities Programs") RD AN No. 4303 (1980-D) August 13, 2007 TO: All State Directors Rural Development ATTENTION: Rural Housing Program Directors, Guaranteed Rural Housing Specialists, Rural Development Managers, and Community

RD AN No. 4303 (1980-D) August 13, 2007 TO: All State Directors Rural Development ATTENTION: Rural Housing Program Directors, Guaranteed Rural Housing Specialists, Rural Development Managers, and Community

UNIFORM APPRAISAL DATASET

[Pick the date] [UNIFORM APPRAISAL DATASET] This document will provide Realtors knowledge about the new Fannie Mae and Freddy Mac appraisal requirements. Providing information discussed in this document

[Pick the date] [UNIFORM APPRAISAL DATASET] This document will provide Realtors knowledge about the new Fannie Mae and Freddy Mac appraisal requirements. Providing information discussed in this document

Agency Guideline Revisions Note: SunTrust Mortgage specific overlays are underlined.

Accessory Units Correspondent Section 1.07 Appraisal Guidelines & Correspondent Section.01 Agency Loan Programs- Guideline Standard Agency Agency Plus Home Possible Mortgage Section 1.07 Appraisal Guidelines

Accessory Units Correspondent Section 1.07 Appraisal Guidelines & Correspondent Section.01 Agency Loan Programs- Guideline Standard Agency Agency Plus Home Possible Mortgage Section 1.07 Appraisal Guidelines

The Real Estate Transaction in 180 Steps What Your REALTOR Does for You

REALTOR ASSOCIATION OF PIONEER VALLEY, INC. The Western New England Center for Real Estate Services 221 Industry Avenue Springfield, MA 01104 413-785-1328 phone 877-854-6978 toll-free 413-731-7125 fax

REALTOR ASSOCIATION OF PIONEER VALLEY, INC. The Western New England Center for Real Estate Services 221 Industry Avenue Springfield, MA 01104 413-785-1328 phone 877-854-6978 toll-free 413-731-7125 fax

WHAT YOUR REALTOR DOES FOR YOU IN 181 STEPS

WHAT YOUR REALTOR DOES FOR YOU IN 181 STEPS Surveys show that many homeowners and homebuyers are not aware of the true value a REALTOR provides during the course of a real estate transaction. The list

WHAT YOUR REALTOR DOES FOR YOU IN 181 STEPS Surveys show that many homeowners and homebuyers are not aware of the true value a REALTOR provides during the course of a real estate transaction. The list

Section Condominium and PUD Approval Requirements

Section 1.06 - Condominium and PUD Approval Requirements In This Section This section contains the following topics. Overview... 2 Related Bulletins... 3 Agency... 4 General Information on Condominium

Section 1.06 - Condominium and PUD Approval Requirements In This Section This section contains the following topics. Overview... 2 Related Bulletins... 3 Agency... 4 General Information on Condominium

STATE OF SOUTH CAROLINA RESIDENTIAL PROPERTY CONDITION DISCLOSURE STATEMENT

STATE OF SOUTH CAROLINA RESIDENTIAL PROPERTY CONDITION DISCLOSURE STATEMENT The South Carolina Code of Laws (Title 27, Chapter 50, Article 1) requires that an owner of residential real property (single

STATE OF SOUTH CAROLINA RESIDENTIAL PROPERTY CONDITION DISCLOSURE STATEMENT The South Carolina Code of Laws (Title 27, Chapter 50, Article 1) requires that an owner of residential real property (single

Freddie Mac Condominium Unit Mortgages

For all mortgages secured by a Unit in a Project, Sellers must meet the requirements of Freddie Mac Single-Family Seller/Servicer Guide (Guide) Chapter 5701, Special for s, and the Seller s other Purchase

For all mortgages secured by a Unit in a Project, Sellers must meet the requirements of Freddie Mac Single-Family Seller/Servicer Guide (Guide) Chapter 5701, Special for s, and the Seller s other Purchase

NADA MANUFACTURED HOUSING COST CD-ROM FANNIE MAE 1004C FREDDIE MAC 70B

USING THE NADA MANUFACTURED HOUSING COST CD-ROM WITH THE FANNIE MAE 1004C FREDDIE MAC 70B NADA Appraisal Guides Manufactured Housing Division PO Box 7800, Costa Mesa, CA 92628 800.966.6232 714.556.8715

USING THE NADA MANUFACTURED HOUSING COST CD-ROM WITH THE FANNIE MAE 1004C FREDDIE MAC 70B NADA Appraisal Guides Manufactured Housing Division PO Box 7800, Costa Mesa, CA 92628 800.966.6232 714.556.8715

Single Family Housing Policy Handbook: FHA Connection 203k Calculator and Other System Enhancements

Office of Single Family Program Development Single Family Housing Policy Handbook: FHA Connection 203k Calculator and Other System Enhancements April 28, 2016 Last Updated: 4/27/16 Presented by: Kevin

Office of Single Family Program Development Single Family Housing Policy Handbook: FHA Connection 203k Calculator and Other System Enhancements April 28, 2016 Last Updated: 4/27/16 Presented by: Kevin

Freddie Mac Condominium Unit Mortgages

For all mortgages secured by a Condominium Unit in a Condominium Project, you must meet the requirements of Freddie Mac Single-Family Seller/Servicer Guide (Guide) Chapter 5701, Special for Condominiums,

For all mortgages secured by a Condominium Unit in a Condominium Project, you must meet the requirements of Freddie Mac Single-Family Seller/Servicer Guide (Guide) Chapter 5701, Special for Condominiums,

GAAR Harness the Power of Technology to Create the BEST Appraisal Reviews Possible

GAAR Harness the Power of Technology to Create the BEST Appraisal Reviews Possible Presented by FNC March 21, 2012 INTRODUCTION General Information: Conference Web Page Audio & Supporting Documents Submit

GAAR Harness the Power of Technology to Create the BEST Appraisal Reviews Possible Presented by FNC March 21, 2012 INTRODUCTION General Information: Conference Web Page Audio & Supporting Documents Submit

4-Point Inspection Personal Lines (Edition 9/2012 revised)

") (Edition 9/2012 revised) INSURED/APPLICANT NAME John Doe APPLICATION / POLICY # 1-1 ADDRESS INSPECTED: ACTUAL YEAR BUILT: 123 Main St, Miami, FL 33138 1938 DATE INSPECTED: 2/12/2014 Minimum Photo Requirement:

(Edition 9/2012 revised) INSURED/APPLICANT NAME John Doe APPLICATION / POLICY # 1-1 ADDRESS INSPECTED: ACTUAL YEAR BUILT: 123 Main St, Miami, FL 33138 1938 DATE INSPECTED: 2/12/2014 Minimum Photo Requirement:

A. Proposed principal(s) must file form HUD-2530, Previous Participation Certificate; and

must file form HUD-2530, Previous Participation Certificate; and") SECTION 3. DETERMINATIVE CRITERIA FOR REVIEW OF TPAs The following are criteria employed by HUD to evaluate Full Review and certain Modified Review proposals: 13-10. Requirement that a Proposed Owner/Managing

SECTION 3. DETERMINATIVE CRITERIA FOR REVIEW OF TPAs The following are criteria employed by HUD to evaluate Full Review and certain Modified Review proposals: 13-10. Requirement that a Proposed Owner/Managing

Table of Contents. Glossary 4. Step 1: Prepare Your Home for Sale 6. Step 2: Market and Show Your Home 8. Step 3: Negotiate Offers 10

Selling a Home As frequently as the rules and markets change, selling a home can be a complicated process whether you use a real estate agent to help you or not. This Guidebook shows a practical process

Selling a Home As frequently as the rules and markets change, selling a home can be a complicated process whether you use a real estate agent to help you or not. This Guidebook shows a practical process

NADA MANUFACTURED HOUSING COST GUIDE FANNIE MAE 1004C FREDDIE MAC 70B

USING THE NADA MANUFACTURED HOUSING COST GUIDE WITH THE FANNIE MAE 1004C FREDDIE MAC 70B NADA Appraisal Guides Manufactured Housing Division PO Box 7800, Costa Mesa, CA 92628 800.966.6232 714.556.8715

USING THE NADA MANUFACTURED HOUSING COST GUIDE WITH THE FANNIE MAE 1004C FREDDIE MAC 70B NADA Appraisal Guides Manufactured Housing Division PO Box 7800, Costa Mesa, CA 92628 800.966.6232 714.556.8715