Property Assessment Seminar

|

|

|

- Charles Porter

- 6 years ago

- Views:

Transcription

1 1 Property Assessment Seminar Bloomfield Township Property Appeals Process Understanding the assessment change notice and preparing for the March Board of Review. The Seminar will also include a question & answer session with Bloomfield Township Assessing Department. Thursday, February 26 th 6:30PM 8:00PM Bloomfield Township Public Library Community Road Seminar Location Bloomfield Township Library 1099 Lone Pine Road Southeast corner of Lone Pine Road and Telegraph Road

2 2 AGENDA Property Appeals Process Definitions Assessing Contacts Bloomfield Township 2015 Value Overview Proposal A Assessment Change Notice How Assessments are formulated Modified Cost Approach 2 Year Study Land Values Building Values / E.C.F. Appealing your assessment Board of Review Research Appeal Outcomes Veterans Updated Exemption Questions & Answers

3 3 Property Appeals Process March Board of Review March Board of Review What is the March Board of Review? The March Board of Review is a body with members appointed in each municipality to review the assessment roll received from the Assessor to ascertain it is complete, accurate, uniform and valid. They then conduct public hearings in March to hear appeals from property owners. Should I Appeal to the Board of Review? Each year, prior to the March meetings of the local board of review, assessment change notices are mailed. These informational notices include State Equalized Value, Taxable Value, the percent of exemption as a Principal Residence or Qualified Agricultural Property, and whether or not an a Transfer of Ownership has occurred. If you believe the Assessed Value is more than half the value of your property, you may appeal the Assessed and /or Taxable Values at the March Board of Review. You can obtain information about the specific meeting dates and schedule an appearance with the Board of Review by contacting your local assessing office. The Board has no control over millage rates or property taxes. Other reasons to appeal to the Board of Review would include: CLASSIFICATION: Indicates the use of your property. There are six classifications, Agricultural, Commercial, Developmental, Industrial, Residential and Timber Cutover. STATUS: Certain properties are tax-exempt. EQUITY: All properties within the jurisdiction are to be assessed at the same ratio; 50% of TCV. HARDSHIP: Poverty stricken property owners can request tax relief from the Board of Review through a hardship. Household financial documentation will be required. Am I Required to Attend the March Board of Review for a Commercial/Industrial Real Property? No. As of 2007 Commercial and Industrial Real properties no longer have to petition to the March Board of Review. These appeals can be made directly to the Michigan Tax Tribunal on or before May 31 st. Am I Required to Attend the March Board of Review for Personal Property? No. Personal Property can be appealed directly to the Michigan Tax Tribunal provided a Personal Property Statement has been filed before the commencement of the March Board of Review. If the statement has not been filed an appearance at the March Board of Review is required. Michigan law indicates that Personal Property Statements are due February 20 th. The appeals to the Michigan Tax Tribunal must be made by May 31 st. Any property owner or their designated agent may file an appeal regarding the assessment of a property within the Board s jurisdiction. By law, non-resident property owners can appeal by letter. The Township will allow letter appeals by residents as well. Most commonly the property owners appeal in person. You will need to schedule an appointment if you or your agent is to appeal in person. The Board of Review meetings are open to the public in compliance with the Open Meetings Act. How to Prepare for the Board of Review? The taxpayer must provide evidence showing the assessment placed upon the property is incorrect. The Board of Review needs good reason to alter an assessment. It is imperative to be able to answer the questions. What do you think the property is worth? and What are you basing your opinion on? All assessments are to be based on the sales of similar properties. You may hire a professional appraiser, or you can look at sales in your neighborhood and compare them to your home. Per state law, the sale price of a property cannot be the sole determining factor of the assessment of that property. Neither the Assessor nor the Board of Review can raise or lower a property assessment based solely on its sale price. Mortgage appraisals also may not show TCV. When do I Receive Notification of the Decision of the March Board of Review? Every person who protests before the Board shall be notified in writing no later than the first Monday in June of the Board s action on the protest. The decision of the Board is binding for the current assessment year only. This notice must include information concerning the right to appeal to the Michigan Tax Tribunal, the time limits for appealing, and the tribunal s address. Can I Appeal the March Board of Review Decision? Yes. Assessments reviewed by the Board of Review can be appealed to the Michigan Tax Tribunal. The appeal deadline for residential and agricultural properties is July 31 st of that year. Hardships What is a Hardship? Section 211.7u of the Michigan General Property Tax Act defines the poverty or Hardship Exemption as a method to provide relief for those who, in the judgment of the Board of Review, are unable to fully contribute to the annual property tax burden of their principal residence due to their financial status. How do I Apply for a Hardship? The hardship waiver must be filed and approved by your local Board of Review on a yearly basis. Contact your local assessing office to an application.

4 4 Definitions Assessed Value (AV) Generally the same as state equalized value unless an equalization factor other than 50% has been applied by either the county in which the property is located or the State. Your property s assessment change notice will indicate your property s state equalized and assessed values and the amounts those values have increased over the previous tax year s state equalization and assessed values. Entire Tribunal The formal division of the Tribunal. Hearings are held in Lansing before a Tribunal Member. Principal Residence Exemption (PRE) Given to the property that is the primary residence of the property owner upon the filing of a principal residence exemption affidavit. Small Claims The informal division of the Tribunal. Hearings are held telephonically or in-person in the county where the property is located or an adjoining county but within 100 miles of the property. State Equalized Value (SEV) One-half ½) of your property s true cash value. State Equalized Value in Contention The difference between what the petitioner and the respondent believe to be the property s state equalized value for each tax year at issue. Taxable Value (TV) Is not the same as the property s true cash value. It is the value used to calculate your property taxes. A property s taxable value can only increase annually by the rate of inflation or 5%, whichever is less, unless there is an addition to the property (i.e. physical improvement or omitted property) or the property s ownership transferred during a previous tax year. See MCL d. Your property s assessment change notice will indicate your property s taxable and the amount the taxable value has increased over the previous tax year s taxable value. A property's taxable value can also decrease if there is a physical loss to the property. See MCL d. Taxable Value Contention The value that the petitioner believes it should have been for each tax year at issue. Taxable Value in Contention The difference between what the petitioner and the respondent believe to be the property s taxable value for each tax year at issue. True Cash Value The fair market value or the usual selling price of property. For a more detailed definition see MCL Uncapping of the Taxable Value When a transfer of property ownership occurred during a previous tax year, the taxable value of that property is uncapped and becomes the same as the state equalized value of the property. More Property Assessment Terminology:

5 THE GENERAL PROPERTY TAX ACT (EXCERPT) Act 206 of True cash value defined; considerations in determining value; indicating exclusions from true cash value on assessment roll; subsection (2) applicable only to residential property; repairs considered normal maintenance; exclusions from real estate sales data; present economic income defined; applicability of subsection (4); nonprofit cooperate housing corporation defined; value of transferred property; purchase price defined; additional definitions; standard too defined. Sec. 27. (1) As used in this act, true cash value means the usual selling price at the place where the property to which the term is applied is at the time of assessment, being the price that could be obtained for the property at private sale, and not at auction sale except as otherwise provided in this section, or at forced sale. The usual selling price may include sales at public auction held by a nongovernmental agency or person if those sales have become a common method of acquisition in the jurisdiction for the class of property being valued. The usual selling price does not include sales at public action if the sale is part of a liquidation of the seller s assets in a bankruptcy proceeding or if the seller is unable to use common marketing techniques to obtain the usual selling price for the property. 5

6 6 ASSESSING CONTACTS Phone: (248) Staff: William D. Griffin, Assessor (248) Darrin Kraatz, Deputy Assessor (248) Sharon Beslock, Equalization Coordinator (248) James Allen, Appraiser (248) Warsha Kulkarni, Appraiser (248) Jeffrey Edwards, Appraiser (248) Kathy Bono, Appraiser (248)

7 7 Township Average Residential Change 15.0% 13.0% P e r c e n t 10.0% 5.0% 0.0% 3.0% 2.06% 4.00% 10.0% C h a n g e -5.0% -10.0% -15.0% -5.0% -10.0% -16.0% -6.0% -20.0% Year

8 8 PROPOSAL A On March 15, 1994, Michigan voters approved the constitutional amendment known as Proposal A. Prior to Proposal A property tax calculations were based on State Equalized Value (SEV). Proposal A established Taxable Value (TV) as the basis for the calculation of property taxes. Increases in Taxable Value (TV) are limited to the percent of change in the rate of inflation or 5%, whichever is less, as long as there were no losses or additions to the property. The limit on TV does not apply to a property in the year following a transfer of ownership (sale).

9 9 IRM 2015 Inflation Rate Multiplier State Tax Commission BULLETIN NO. 13 OF 2014 INFLATION RATE OCTOBER 13, 2014

10 10 IRM Inflation Rate Multiplier % % % % % % % % % % % % % % % Taxable Value Calculations are derived by using IRM/CPI percentages. This has been mandated since the introduction of proposal A in IRM/CPI is calculated by the US Department of Labor % % % % % %

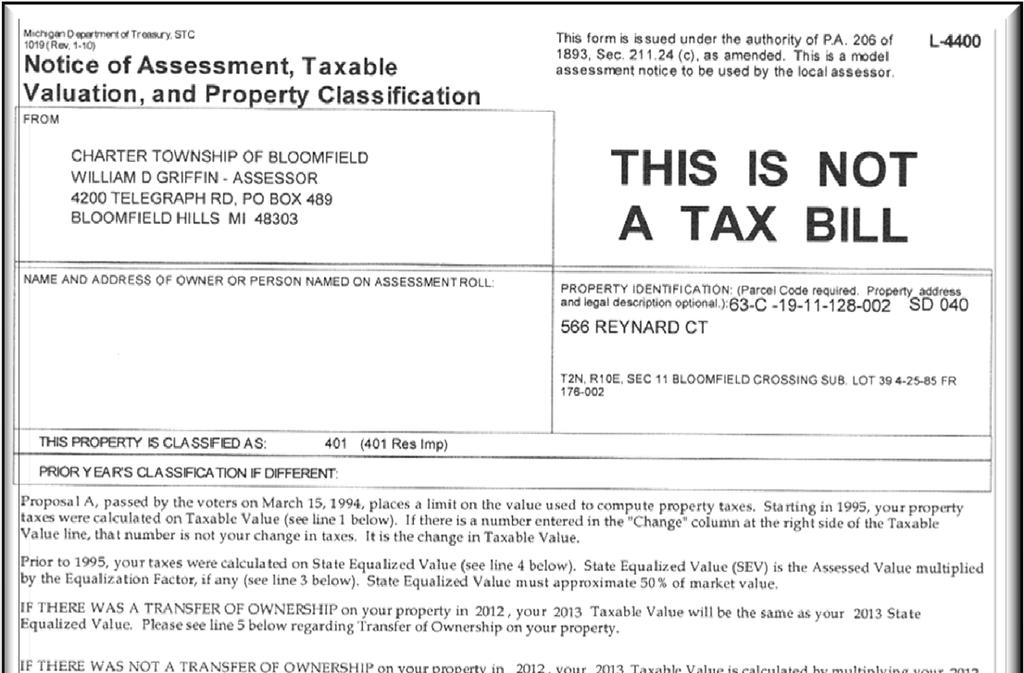

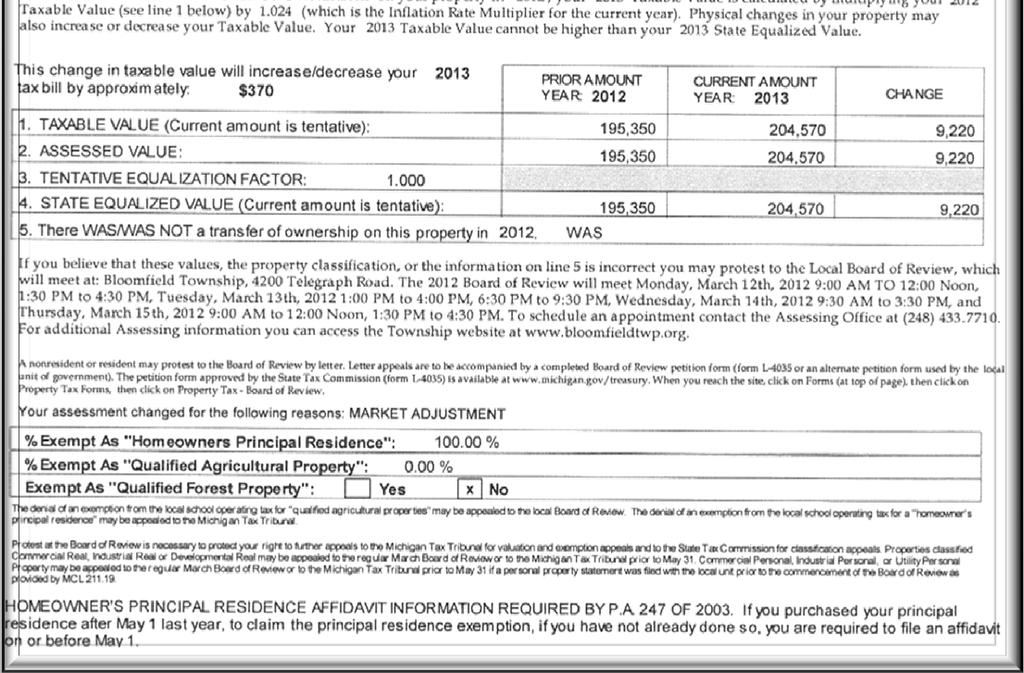

11 ASSESSMENT CHANGE NOTICE

12 12? What are my options after receiving the change of Assessment Notice? 1.Review Property Record Card 2.Contact the Assessor 3.Make Appointment for MBOR

13 Residential Record Cards 13

14 14 Important Items to Review on the Property Record Card Land Size Square Footage of Building (exterior Measurements) Class of Building (A,B,C,D) Garage Bathrooms Basement Finish Built-in Appliances Year Built Fireplaces Out-Buildings, Pools, Patios, Etc. This is just a sample of facts to verify and review with your Assessor

15 15 How Assessments are Formulated Step 1 Cost Approach

16 16 How Assessments are Formulated Look for Sales within this Timeframe. 2 Year Study (used in increasing markets) Look for properties like your own (subject) neighborhood Establishes 2015 Taxable Value for 2015 July and December levies. Sales Study Timeframes are determined by the State Tax Commission

17 17 Methods of Adjusting Assessments Land Value X Land Adjustment 2015 Land Value + Building Replacement Value X *ECF 2015 Building Value = 2015 True Cash Value *E.C.F. = Economic Conditions Factor by Neighborhood

18 Sales Study Against 2014 Values

19 19 E.C.F E.C.F E.C.F

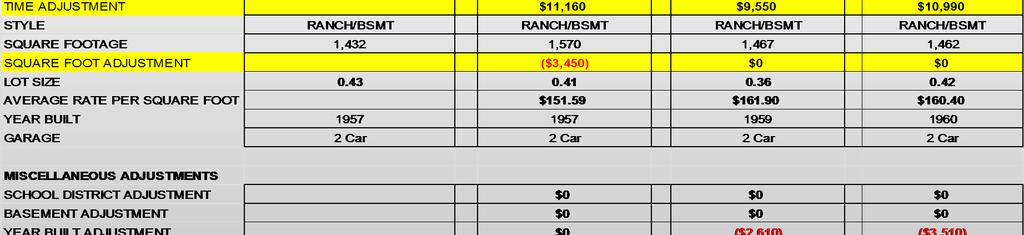

20 Sales Study Against 2014 Values Parcel Number Address Sale Date Sale Type Nghbd Sale Price 2014 Assessed Ratio Value Middlebury Ln 6/29/ Valid Sale Westchester Village $ 177,400 94, Wadsworth Ln 1/6/ Valid Sale Westchester Village $ 158,000 96, W. Maple Rd 6/14/ Valid Sale Westchester Village $ 295, , Dalebrook Ln 11/5/ Valid Sale Westchester Village $ 249, , Berkshire Dr 4/22/ Valid Sale Westchester Village $ 180, , Westbourne Ct 4/25/ Valid Sale Westchester Village $ 270, , Middlebury Ln 7/28/ Valid Sale Westchester Village $ 435, , Farmingdale Dr 8/31/ Valid Sale Westchester Village $ 185,000 91, Middlebury Ln 1/14/ Valid Sale Westchester Village $ 175,000 80, Farmingdale Dr 4/29/ Valid Sale Westchester Village $ 249,000 99, Heathfield Rd 6/23/ Valid Sale Westchester Village $ 200, , E. Breckenridge Ln 8/3/ Valid Sale Westchester Village $ 320, , E. Bradford Dr 12/21/ Valid Sale Westchester Village $ 360, , Target Ration 49.0% to 50.0%/48.74 = +2.52% $ 3,076,000 1,499, Sales in selected neighborhood suggests all property values in Westchester Village should receive an average increase in value of 2.52% for 2015

21 Sales Study Creating 2015 Values 21 Parcel Number Address Sale Date Sale Type Nghbd Sale Price 2013 Assessed Ratio Value Middlebury Ln 6/29/ Valid Sale Westchester Village $ 177,400 96, Wadsworth Ln 1/6/ Valid Sale Westchester Village $ 158,000 98, W. Maple Rd 6/14/ Valid Sale Westchester Village $ 295, , Dalebrook Ln 11/5/ Valid Sale Westchester Village $ 249, , Berkshire Dr 4/22/ Valid Sale Westchester Village $ 180, , Westbourne Ct 4/25/ Valid Sale Westchester Village $ 270, , Middlebury Ln 7/28/ Valid Sale Westchester Village $ 435, , Farmingdale Dr 8/31/ Valid Sale Westchester Village $ 185,000 93, Middlebury Ln 1/14/ Valid Sale Westchester Village $ 175,000 82, Farmingdale Dr 4/29/ Valid Sale Westchester Village $ 249, , Heathfield Rd 6/23/ Valid Sale Westchester Village $ 200, , E. Breckenridge Ln 8/3/ Valid Sale Westchester Village $ 320, , E. Bradford Dr 12/21/ Valid Sale Westchester Village $ 360, , $ 3,253,400 1,633,

22 22 How Assessments Are NOT FORMULATED How Assessments Are NOT Formulated Parcel Number Sale Date Sale Type Nghbd Sale Price 2014 Assessed Ratio 2015 Assessed % Change Value Value /29/ Valid Sale Westchester Village $ 177,400 94, ,700 (0.0610) /6/ Valid Sale Westchester Village $ 158,000 96, ,000 (0.1805) /14/ Valid Sale Westchester Village $ 295, , , /5/ Valid Sale Westchester Village $ 249, , ,500 (0.0306) /22/ Valid Sale Westchester Village $ 180, , ,000 (0.1608) /25/ Valid Sale Westchester Village $ 270, , , /28/ Valid Sale Westchester Village $ 435, , , /31/ Valid Sale Westchester Village $ 185,000 91, , /14/ Valid Sale Westchester Village $ 175,000 80, , /29/ Valid Sale Westchester Village $ 249,000 99, , /23/ Valid Sale Westchester Village $ 200, , ,000 (0.0797) /3/ Valid Sale Westchester Village $ 320, , ,000 (0.0176) /21/ Valid Sale Westchester Village $ 360, , ,000 (0.0334) $ 3,253,400 1,593, ,626, Assessors are responsible for valuing ALL properties in the neighborhood, not just the sold properties.

23 23 Boards of Review Meets 3 times a year. March, July & December. Valuation Appeals can only be heard in March. July and December Boards are for Clerical corrections and Administrative changes. Many communities address poverty appeals in July and December. Reasons: 1) Tax returns are filed in April. 2) Less hectic schedule allows more time for boards to review poverty applications.

24 24 Boards of Review Who can be a member of a Board of Review? Three, six, or nine electors of the Township shall be appointed by the Township to serve as the Board of Review. If 6 or 9 are appointed, they are divided into Boards of 3 individuals for the purpose of hearing and deciding. The size, composition, and manner of appointment of the Board of Review of a Township may be prescribed by Township Charter or Ordinance and a City may be prescribed by City Charter. Do Board of Review Members have to be property owners? At least 2/3 of the members shall be property taxpayers of the Township.

25 25 How to Prepare for the Board of Review? The taxpayer must provide evidence showing the assessment placed upon the property is incorrect. The Board of Review needs good reason to alter an assessment. It is imperative to be able to answer the questions, What do you think the property is worth? and What are you basing your opinion on? All assessments are to be based on the sales of similar properties. You may hire a professional appraiser, or you can look at sales in your neighborhood and compare them to your home. Per state law, the sale price of a property cannot be the sole determining factor of the assessment of that property. Neither the Assessor nor the Board of Review can raise or lower a property assessment based solely on its sale price. Mortgage appraisals also may not show True Cash Value. State Equalized Value = True Cash Value X 50%

26 26 Where to find sales data? Bloomfield Township Website Bloomfield Township Assessor s Office Realtors MLS Access Oakland Register of Deeds Websites (Sales must be verified)

27 27

28 Township Website 28

29 29 Click on Property and Land Search General Property Information Building Information Assessing Comparable Search Results

30 ~ Example ~ Sales Comparable Approach 30

31 31 Final Preparation for MBOR Validate all data. Make the presentation concise. Time with BOR may be limited, get straight to the point. More Data isn t always better.

32 32 Poverty What is a Poverty? Section 211.7u of the Michigan General Property Tax Act defines the poverty or Poverty Exemption as a method to provide relief for those who, in the judgment of the Board of Review, are unable to fully contribute to the annual property tax burden of their principal residence due to their financial status.

33 33 Poverty How do I apply for a Poverty? The poverty waiver must be filed and approved by your local Board of Review on a yearly basis. Contact the assessing office for an application. (July Boards for some communities) Poverty Guidelines are established by the Township. The guidelines include an asset test and income test.

34 G u i d e l i n e s HARDSHIP/POVERTY EXEMPTION 34 Page 1/Guidelines

35 35 G u i d e l i n e s Hardship/Poverty Exemption Page2/Guidelines

36 36 P o v e r t y A p p l i c a t i o n

37 Disabled Veterans Exemption Real Property used and owned as a homestead by a disabled veteran who was discharged from the armed forces of the United States under honorable conditions or his or her unremarried surviving spouse. Permanently or totally disabled as a result of military service and entitled to veterans benefits at the 100% rate. Receives pecuniary assistance due to disability for specially adapted housing. Rated as individually unemployable. Veteran must file annually the affidavit of Disabled Veterans Exemption and summary of benefits letter from the Department of Veterans Affairs. 37

38 38 The Outcomes of the MBOR Letters will be mailed to property owners after the closing of March Board of Review. Statutory Law: These letters are to be delivered to the property owners no later than June 3 rd. (first Monday in June) - No Change - Lowering of Assessment - Lowering of Taxable Value - Raising of Assessment The letter mailed to property will contain instructions on appealing to the Michigan Tax Tribunal.

39 39 MTT for Home Owners -Small Claims- What is the Michigan Tax Tribunal? Quasi-Judicial agency to preside over valuation disputes. How does the Tribunal Work? Informal hearing with administrative law judge. You must appeal to the MBR to appeal to the Tax Tribunal. Where do I file my appeal? Michigan Tax Tribunal P.O. Box Lansing, MI Ph: (517) Fax: (517) Website: general questions: taxtrib@michigan.gov When do I File? Appeals must be filed to the Tribunal by July 31 st (residential properties). How do I file? By writing a letter to the Tribunal. What are the Fees? None for primary residences.

40 Questions 40

The Department s Role

CITY ASSESSOR The Department s Role on the h Ci City s T Team August 21, 2013 Who we are... Micheal Lohmeier City Assessor (2012) (Commercial Appraiser 1998-2005, Assr. 2010-12) 12) Administration and

CITY ASSESSOR The Department s Role on the h Ci City s T Team August 21, 2013 Who we are... Micheal Lohmeier City Assessor (2012) (Commercial Appraiser 1998-2005, Assr. 2010-12) 12) Administration and

Allegan County Equalization Department

Allegan County Equalization Department 2011 Department Report Equalization Report Recap 2010 2011 projects January 1- December 31, 2010 Blaine R. McLeod Director of Equalization 1 Message from the Director

Allegan County Equalization Department 2011 Department Report Equalization Report Recap 2010 2011 projects January 1- December 31, 2010 Blaine R. McLeod Director of Equalization 1 Message from the Director

UNDERSTANDING PROPERTY TAXES IN COLORADO

UNDERSTANDING PROPERTY TAXES IN COLORADO This brochure was created to provide general information on the Colorado property tax system. For more specific information on any one of these topics, please visit

UNDERSTANDING PROPERTY TAXES IN COLORADO This brochure was created to provide general information on the Colorado property tax system. For more specific information on any one of these topics, please visit

ASSESSMENT AND TAXATION

ABSTRACT A brief synopsis of the assessment, appeal and taxation process as implemented by the Code of Iowa and Administrative Rules. ASSESSMENT AND TAXATION Iowa State Association of Assessors General

ABSTRACT A brief synopsis of the assessment, appeal and taxation process as implemented by the Code of Iowa and Administrative Rules. ASSESSMENT AND TAXATION Iowa State Association of Assessors General

How to Contest Your Assessment

How to Contest Your Assessment STATE OF NEW YORK Eliot Spitzer, Governor Donald C. DeWitt, Executive Director New York State Office of Real Property Services 16 Sheridan Avenue Albany, New York 12210-2714

How to Contest Your Assessment STATE OF NEW YORK Eliot Spitzer, Governor Donald C. DeWitt, Executive Director New York State Office of Real Property Services 16 Sheridan Avenue Albany, New York 12210-2714

Board of Appeal and Equalization Handbook

Board of Appeal and Equalization Handbook This handbook was created to satisfy the training requirements of Minnesota Statutes, sections 274.014 and 274.135 Updated January 2018 Table of Contents Introduction...

Board of Appeal and Equalization Handbook This handbook was created to satisfy the training requirements of Minnesota Statutes, sections 274.014 and 274.135 Updated January 2018 Table of Contents Introduction...

Reappraisal Important Property Tax Information

Reappraisal 2013 Important Property Tax Information Spartanburg County Assessor PO Box 5762 Spartanburg, SC 29304 Telephone: (864)596-2544 Fax: (864)596-2940 Fax: (864)596-2223 www.spartanburgcounty.org

Reappraisal 2013 Important Property Tax Information Spartanburg County Assessor PO Box 5762 Spartanburg, SC 29304 Telephone: (864)596-2544 Fax: (864)596-2940 Fax: (864)596-2223 www.spartanburgcounty.org

QUESTIONS? CALL THE ASSESSOR S OFFICE

2018 GRIEVANCE PACKET PLEASE NOTE: The Assessor s Office will make five (5) copies of the RP 524 complaint form and suppor ng documenta on for the Board of Assessment Review members if received on or before

2018 GRIEVANCE PACKET PLEASE NOTE: The Assessor s Office will make five (5) copies of the RP 524 complaint form and suppor ng documenta on for the Board of Assessment Review members if received on or before

What is a Small Claims Assessment Review (SCAR)?

?") Small Claims and Assessment Review What is a Small Claims Assessment Review (SCAR)? The Small Claims Assessment Review is a procedure that provides property owners with an opportunity to challenge the

Small Claims and Assessment Review What is a Small Claims Assessment Review (SCAR)? The Small Claims Assessment Review is a procedure that provides property owners with an opportunity to challenge the

INFORMATION ON 2017 PROPERTY TAX ASSESSMENTS AND APPEALS IN ORLEANS PARISH Property Tax Assessment & Appeal Information

INFORMATION ON 2017 PROPERTY TAX ASSESSMENTS AND APPEALS IN ORLEANS PARISH 2018 Property Tax Assessment & Appeal Information July 15 th August 15 th Assessor opens tax lists to public for inspection. Informal

INFORMATION ON 2017 PROPERTY TAX ASSESSMENTS AND APPEALS IN ORLEANS PARISH 2018 Property Tax Assessment & Appeal Information July 15 th August 15 th Assessor opens tax lists to public for inspection. Informal

IMPORTANT ANNOUNCEMENT: Our website is changing! Please click here for details.

IMPORTANT ANNOUNCEMENT: Our website is changing! Please click here for details. Home Search Downloads Exemptions Agriculture Maps Tangible Links Contact Home Frequently Asked Questions (FAQ) Frequently

IMPORTANT ANNOUNCEMENT: Our website is changing! Please click here for details. Home Search Downloads Exemptions Agriculture Maps Tangible Links Contact Home Frequently Asked Questions (FAQ) Frequently

A. Inflation Rate Used in the 2017 Capped Value Formula.

5102 (Rev. 04-15) RICK SNYDER GOVERNOR STATE OF MICHIGAN DEPARTMENT OF TREASURY LANSING NICK A. KHOURI STATE TREASURER TO: FROM: Assessors Equalization Directors State Tax Commission (STC) BULLETIN NO.

5102 (Rev. 04-15) RICK SNYDER GOVERNOR STATE OF MICHIGAN DEPARTMENT OF TREASURY LANSING NICK A. KHOURI STATE TREASURER TO: FROM: Assessors Equalization Directors State Tax Commission (STC) BULLETIN NO.

Past & Present Adjustments & Parcel Count Section... 13

Assessment 2017 Report This report includes specific information regarding the 2017 assessment as well as general information about both the appeals and assessment processes. Contents Introduction... 3

Assessment 2017 Report This report includes specific information regarding the 2017 assessment as well as general information about both the appeals and assessment processes. Contents Introduction... 3

Special Plainview City Council Meeting Board of Appeals and Equalization Meeting AGENDA Tuesday, April 16, 2019, at 6:00 P.M.

Special Plainview City Council Meeting Board of Appeals and Equalization Meeting AGENDA Tuesday, April 16, 2019, at 6:00 P.M. Special meetings are meetings held at a time or place that is different from

Special Plainview City Council Meeting Board of Appeals and Equalization Meeting AGENDA Tuesday, April 16, 2019, at 6:00 P.M. Special meetings are meetings held at a time or place that is different from

Introduction. Bruce Munneke, S.A.M.A. Washington County Assessor. 3 P a g e

Assessment 2016 Report This report includes specific information regarding the 2016 assessment as well as general information about both the appeals and assessment processes. Contents Introduction... 3

Assessment 2016 Report This report includes specific information regarding the 2016 assessment as well as general information about both the appeals and assessment processes. Contents Introduction... 3

Date: March 2018 TOWN OF WATERFORD Department of Assessment

Date: March 2018 TOWN OF WATERFORD 1. Overview: The purpose of this workshop is to explain the Assessment Disclosure Notice, how assessments are derived and how to challenge your assessment if you do not

Date: March 2018 TOWN OF WATERFORD 1. Overview: The purpose of this workshop is to explain the Assessment Disclosure Notice, how assessments are derived and how to challenge your assessment if you do not

ASSESSORS ANSWER FREQUENTLY ASKED QUESTIONS ABOUT REAL PROPERTY Assessors Office, 37 Main Street

A. THE ASSESSMENT PROCESS: ASSESSORS ANSWER FREQUENTLY ASKED QUESTIONS ABOUT REAL PROPERTY Assessors Office, 37 Main Street What is mass appraisal? Assessors must value all real and personal property in

A. THE ASSESSMENT PROCESS: ASSESSORS ANSWER FREQUENTLY ASKED QUESTIONS ABOUT REAL PROPERTY Assessors Office, 37 Main Street What is mass appraisal? Assessors must value all real and personal property in

What To Do If You Disagree With Your Assessment

What To Do If You Disagree With Your Assessment STATE OF NEW YORK David A. Paterson, Governor Lee Kyriacou, Executive Director New York State Office of Real Property Services 16 Sheridan Avenue Albany,

What To Do If You Disagree With Your Assessment STATE OF NEW YORK David A. Paterson, Governor Lee Kyriacou, Executive Director New York State Office of Real Property Services 16 Sheridan Avenue Albany,

PIATT COUNTY BOARD OF REVIEW RULES & PROCEDURES 2013

PIATT COUNTY BOARD OF REVIEW RULES & PROCEDURES 2013 1. SUGGESTION. It is strongly recommended that the tax payer discuss his or her assessment with their township assessor prior to filing a complaint

PIATT COUNTY BOARD OF REVIEW RULES & PROCEDURES 2013 1. SUGGESTION. It is strongly recommended that the tax payer discuss his or her assessment with their township assessor prior to filing a complaint

Assessing Reform Proposal Summary

Assessing Reform Proposal Summary Specify minimum quality standards that every assessing district must meet, on their own, in cooperation with other local units, or through the county. Local units could

Assessing Reform Proposal Summary Specify minimum quality standards that every assessing district must meet, on their own, in cooperation with other local units, or through the county. Local units could

Filing a property assessment complaint and preparing for your hearing. Alberta Municipal Affairs

Filing a property assessment complaint and preparing for your hearing Alberta Municipal Affairs Alberta s Municipal Government Act, the 2018 Matters Relating to Assessment Complaints Regulation, and the

Filing a property assessment complaint and preparing for your hearing Alberta Municipal Affairs Alberta s Municipal Government Act, the 2018 Matters Relating to Assessment Complaints Regulation, and the

Equalization. Equalization. Statutory Duties. Statutory Authority

Equalization Citizens Board of Commissioners Administrator /Controller Statutory Duties Advise and assist the Board of Commissioners in equalizing property tax assessments on a county-wide basis. File

Equalization Citizens Board of Commissioners Administrator /Controller Statutory Duties Advise and assist the Board of Commissioners in equalizing property tax assessments on a county-wide basis. File

Athens County Auditor, Jill Thompson provides homeowners answers to the most commonly asked questions about the countywide 2014 reappraisal

Contact: Jill Thompson Athens County Auditor Phone 740.592.3223 Fax 740.594.3270 15 S. Court Street, Room 330 Athens, Ohio 45701 www.athenscountyauditor.org Jill Thompson Athens County Auditor Property

Contact: Jill Thompson Athens County Auditor Phone 740.592.3223 Fax 740.594.3270 15 S. Court Street, Room 330 Athens, Ohio 45701 www.athenscountyauditor.org Jill Thompson Athens County Auditor Property

Request for Proposals For Assessor. Charter Township of Augusta Washtenaw County

Request for Proposals For Assessor (Michigan Certified Assessing Officer) Charter Township of Augusta Washtenaw County Charter Township of Augusta 8021 Talladay Road Whittaker, MI 48190 Phone 734-461-6117

Request for Proposals For Assessor (Michigan Certified Assessing Officer) Charter Township of Augusta Washtenaw County Charter Township of Augusta 8021 Talladay Road Whittaker, MI 48190 Phone 734-461-6117

Ottawa CountyEqualization Department

2016 Annual Report Ottawa CountyEqualization Department This report does not take the place of the "Equalization Report", statutorily required to be presented to the County Board of Commissioners for adoption

2016 Annual Report Ottawa CountyEqualization Department This report does not take the place of the "Equalization Report", statutorily required to be presented to the County Board of Commissioners for adoption

PROPERTY REASSESSMENT AND TAXATION. State Tax Commission Jefferson City, Missouri

PROPERTY REASSESSMENT AND TAXATION State Tax Commission Jefferson City, Missouri Revised January, 2017 INTRODUCTION Some aspects of the property tax system are confusing to many taxpayers. It is important

PROPERTY REASSESSMENT AND TAXATION State Tax Commission Jefferson City, Missouri Revised January, 2017 INTRODUCTION Some aspects of the property tax system are confusing to many taxpayers. It is important

Ottawa County Equalization Department

2017 Annual Report Ottawa County Equalization Department This report does not take the place of the "Equalization Report", statutorily required to be presented to the County Board of Commissioners for

2017 Annual Report Ottawa County Equalization Department This report does not take the place of the "Equalization Report", statutorily required to be presented to the County Board of Commissioners for

COMPLAINT ON REAL PROPERTY ASSESSMENT GUIDANCE (UNINCORPORATED TOWN OF GREENBURGH AND ALL VILLAGES) (Residential 1, 2, or 3 family homes)

(Residential 1, 2, or 3 family homes)") COMPLAINT ON REAL PROPERTY ASSESSMENT GUIDANCE (UNINCORPORATED TOWN OF GREENBURGH AND ALL VILLAGES) (Residential 1, 2, or 3 family homes) Although the assessment staff is very knowledgeable to answer your

COMPLAINT ON REAL PROPERTY ASSESSMENT GUIDANCE (UNINCORPORATED TOWN OF GREENBURGH AND ALL VILLAGES) (Residential 1, 2, or 3 family homes) Although the assessment staff is very knowledgeable to answer your

(35 ILCS 200/15-175) Sec General homestead exemption. (a) Except as provided in Sections and , homestead property is entitled

Sec General homestead exemption. (a) Except as provided in Sections and , homestead property is entitled") (35 ILCS 200/15-175) Sec. 15-175. General homestead exemption. (a) Except as provided in Sections 15-176 and 15-177, homestead property is entitled to an annual homestead exemption limited, except as described

(35 ILCS 200/15-175) Sec. 15-175. General homestead exemption. (a) Except as provided in Sections 15-176 and 15-177, homestead property is entitled to an annual homestead exemption limited, except as described

BOARD OF REVIEW SCRIPT

BOARD OF REVIEW SCRIPT CLERK'S SCRIPT: 1. Clerk introduces the case by stating the following information: a. Tax Key # b. Property address c. Property Owner d. Mailing address if different. e. Class of

BOARD OF REVIEW SCRIPT CLERK'S SCRIPT: 1. Clerk introduces the case by stating the following information: a. Tax Key # b. Property address c. Property Owner d. Mailing address if different. e. Class of

2014 Property Tax Base Projections

2014 Property Tax Base Projections SALES OCTOBER 1, 2012 - SEPTEMBER 30, 2013 2014 Ratios/Change Rev Dates Change based on: Preliminary as of 11/7/13 49.50% RESIDENTIAL RATIOS RESIDENTIAL CHANGES Addison

2014 Property Tax Base Projections SALES OCTOBER 1, 2012 - SEPTEMBER 30, 2013 2014 Ratios/Change Rev Dates Change based on: Preliminary as of 11/7/13 49.50% RESIDENTIAL RATIOS RESIDENTIAL CHANGES Addison

APPEAL PROCESS GUIDE FOR THE PROPERTY OWNER

2018 APPEAL PROCESS GUIDE FOR THE PROPERTY OWNER IMPORTANT DATES TO KNOW 2018 APPEAL PROCESS TIME FRAME March 1 - assessment notices must be mailed March 15 - last day to file for owner-occupied status

2018 APPEAL PROCESS GUIDE FOR THE PROPERTY OWNER IMPORTANT DATES TO KNOW 2018 APPEAL PROCESS TIME FRAME March 1 - assessment notices must be mailed March 15 - last day to file for owner-occupied status

F L O R I D A H O U S E O F R E P R E S E N T A T I V E S

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 House Joint Resolution A joint resolution proposing an amendment to Section 6 of Article VII and the creation of a new section in Article

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 House Joint Resolution A joint resolution proposing an amendment to Section 6 of Article VII and the creation of a new section in Article

Pickens County Reassessment Program. Utilizing CAMA GIS MLS SQL

1 Pickens County 2019 Reassessment Program Utilizing CAMA GIS MLS SQL Pickens County Reassessment History 1980 Countywide Reappraisal 1990 Countywide Reappraisal 1999 Countywide Reappraisal 2004 Countywide

1 Pickens County 2019 Reassessment Program Utilizing CAMA GIS MLS SQL Pickens County Reassessment History 1980 Countywide Reappraisal 1990 Countywide Reappraisal 1999 Countywide Reappraisal 2004 Countywide

GENERAL ASSESSMENT DEFINITIONS

21st Century Appraisals, Inc. GENERAL ASSESSMENT DEFINITIONS Ad Valorem tax. A tax levied in proportion to the value of the thing(s) being taxed. Exclusive of exemptions, use-value assessment laws, and

21st Century Appraisals, Inc. GENERAL ASSESSMENT DEFINITIONS Ad Valorem tax. A tax levied in proportion to the value of the thing(s) being taxed. Exclusive of exemptions, use-value assessment laws, and

YOUR GUIDE TO THE REASSESSMENT PROGRAM

YOUR GUIDE TO THE REASSESSMENT PROGRAM Why Reassess? Reassessment is required by law. Act 208, as passed by the General Assembly in 1975, provides that all real property will be valued at its current market

YOUR GUIDE TO THE REASSESSMENT PROGRAM Why Reassess? Reassessment is required by law. Act 208, as passed by the General Assembly in 1975, provides that all real property will be valued at its current market

FREQUENTLY ASKED QUESTIONS

FREQUENTLY ASKED QUESTIONS GENERAL How can I change my mailing address? Can you change my mailing address by phone? You may either call the District at (409) 840-9944 or 727-4611 in order to change your

FREQUENTLY ASKED QUESTIONS GENERAL How can I change my mailing address? Can you change my mailing address by phone? You may either call the District at (409) 840-9944 or 727-4611 in order to change your

MCLENNAN COUNTY APPRAISAL DISTRICT PROPERTY VALUATION WORKSHOP

MCLENNAN COUNTY APPRAISAL DISTRICT PROPERTY VALUATION WORKSHOP WORKSHOP OBJECTIVES To understand: Property Tax System The valuation process What is Market Value Market Trends Time frame for protesting

MCLENNAN COUNTY APPRAISAL DISTRICT PROPERTY VALUATION WORKSHOP WORKSHOP OBJECTIVES To understand: Property Tax System The valuation process What is Market Value Market Trends Time frame for protesting

Jim Webb, Deputy Chief Appraiser, Appraisal Operations Kelly Lintner, Director of Appraisal Residential and Land

Jim Webb, Deputy Chief Appraiser, Appraisal Operations Kelly Lintner, Director of Appraisal Residential and Land What s a Taxpayer to do? Informal and Formal Administrative Appeals (PROTESTS) Judicial

Jim Webb, Deputy Chief Appraiser, Appraisal Operations Kelly Lintner, Director of Appraisal Residential and Land What s a Taxpayer to do? Informal and Formal Administrative Appeals (PROTESTS) Judicial

A GUIDE TO THE PROPERTY VALUATION APPEAL PROCESS - EQUALIZATION APPEALS*

A GUIDE TO THE PROPERTY VALUATION APPEAL PROCESS - EQUALIZATION APPEALS* LAND AND BUILIDNGS USED FOR RESIDENTIAL AND COMMERICAL PURPOSES (*IN COUNTIES WITHOUT HEARING OFFICER/PANELS) (Rev. 08/2016) Kansas

A GUIDE TO THE PROPERTY VALUATION APPEAL PROCESS - EQUALIZATION APPEALS* LAND AND BUILIDNGS USED FOR RESIDENTIAL AND COMMERICAL PURPOSES (*IN COUNTIES WITHOUT HEARING OFFICER/PANELS) (Rev. 08/2016) Kansas

MOTLEY COUNTY APPRAISAL DISTRICT

MOTLEY COUNTY APPRAISAL DISTRICT Jim Finley RPA, RTA Chief Appraiser PO Box 249-104 E California Floydada, Texas 79235 806-983-5256 phone, 806-983-6230 fax floydcad@sbcglobal.net LOCAL PROPERTY TAXATION

MOTLEY COUNTY APPRAISAL DISTRICT Jim Finley RPA, RTA Chief Appraiser PO Box 249-104 E California Floydada, Texas 79235 806-983-5256 phone, 806-983-6230 fax floydcad@sbcglobal.net LOCAL PROPERTY TAXATION

State Tax Commission. Guide to Basic Assessing

State Tax Commission Guide to Basic Assessing March 2013 Chapter 1 History of Property Tax, Local Government Finance and Property Taxation Local governments receive revenue from a variety of sources including

State Tax Commission Guide to Basic Assessing March 2013 Chapter 1 History of Property Tax, Local Government Finance and Property Taxation Local governments receive revenue from a variety of sources including

UNDERSTANDING YOUR ASSESSMENT

UNDERSTANDING YOUR ASSESSMENT An informational booklet explaining property assessments and procedures. Provided by the Town of York Assessor s Office This booklet will attempt to explain the Assessment

UNDERSTANDING YOUR ASSESSMENT An informational booklet explaining property assessments and procedures. Provided by the Town of York Assessor s Office This booklet will attempt to explain the Assessment

Assessor Ken Yazel. Ad Valorem Property Taxes In Tulsa County, OK. Prepared by the Tulsa County Assessor s Office

Assessor Ken Yazel Ad Valorem Property Taxes In Tulsa County, OK Prepared by the Tulsa County Assessor s Office Tulsa County Assessor s Office Our Commitment Ken Yazel, Assessor The Tulsa County Assessor

Assessor Ken Yazel Ad Valorem Property Taxes In Tulsa County, OK Prepared by the Tulsa County Assessor s Office Tulsa County Assessor s Office Our Commitment Ken Yazel, Assessor The Tulsa County Assessor

UNDERSTANDING PROPERTY ASSESSMENT APPEALS A GUIDE TO REGULAR ASSESSMENT APPEALS UNDER TRUE MARKET VALUE AND COMMON LEVEL RANGE STANDARDS

UNDERSTANDING PROPERTY ASSESSMENT APPEALS A GUIDE TO REGULAR ASSESSMENT APPEALS UNDER TRUE MARKET VALUE AND COMMON LEVEL RANGE STANDARDS This information was developed to assist property owners in preparing

UNDERSTANDING PROPERTY ASSESSMENT APPEALS A GUIDE TO REGULAR ASSESSMENT APPEALS UNDER TRUE MARKET VALUE AND COMMON LEVEL RANGE STANDARDS This information was developed to assist property owners in preparing

Citrus County Property Appraiser TRIM Frequently Asked Questions

Citrus County Property Appraiser TRIM Frequently Asked Questions updated 8-13-2018 1 1 WHAT IS A TRIM NOTICE? TRIM stands for TRuth In Millage. This notice allows you to compare last year s assessed value

Citrus County Property Appraiser TRIM Frequently Asked Questions updated 8-13-2018 1 1 WHAT IS A TRIM NOTICE? TRIM stands for TRuth In Millage. This notice allows you to compare last year s assessed value

Throckmorton Central Appraisal District 144 N Minter Ave PO Box 788 Throckmorton, TX

Throckmorton Central Appraisal District 144 N Minter Ave PO Box 788 Throckmorton, TX 76483 940-849-5691 1 THIS PAGE IS INTENTIONALLY LEFT BLANK 2 EXECUTIVE SUMMARY Throckmorton Central Appraisal District

Throckmorton Central Appraisal District 144 N Minter Ave PO Box 788 Throckmorton, TX 76483 940-849-5691 1 THIS PAGE IS INTENTIONALLY LEFT BLANK 2 EXECUTIVE SUMMARY Throckmorton Central Appraisal District

Equalization Department

Equalization Department Citizens Board of Commissioners Administrator /Controller Equalization Director Statutory Authority Michigan Compiled Law 211.34 (3) The County Board of Commissioners of a county

Equalization Department Citizens Board of Commissioners Administrator /Controller Equalization Director Statutory Authority Michigan Compiled Law 211.34 (3) The County Board of Commissioners of a county

Franklin County Appraisal District 2016 Annual Report

Franklin County Appraisal District 2016 Annual Report The Franklin County Appraisal District is a political subdivision of the state. The Constitution of the State of Texas, the Texas Property Tax Code,

Franklin County Appraisal District 2016 Annual Report The Franklin County Appraisal District is a political subdivision of the state. The Constitution of the State of Texas, the Texas Property Tax Code,

York County 2015 Reassessment Program. York County Assessor s Office 18 W. Liberty St York SC fax

York County 2015 Reassessment Program York County Assessor s Office 18 W. Liberty St York SC 29745 803-684-8526 803-628-3936 fax Re-Assessment The Reassessment Program Act 208: Act 208, as passed by the

York County 2015 Reassessment Program York County Assessor s Office 18 W. Liberty St York SC 29745 803-684-8526 803-628-3936 fax Re-Assessment The Reassessment Program Act 208: Act 208, as passed by the

Ad Valorem Tax Escambia County FL Explained

Ad Valorem Tax Escambia County FL Explained What properties must be appraised? REAL PROPERTY - the physical land and appurtenances affixed to the land, e.g., structures. The term "land","real estate","realty"

Ad Valorem Tax Escambia County FL Explained What properties must be appraised? REAL PROPERTY - the physical land and appurtenances affixed to the land, e.g., structures. The term "land","real estate","realty"

The Texas Constitution sets out five basic rules for property taxes in our state:

Why does the appraisal district look at values each year? The Texas Constitution sets out five basic rules for property taxes in our state: 1. Taxation must be equal and uniform. No single property or

Why does the appraisal district look at values each year? The Texas Constitution sets out five basic rules for property taxes in our state: 1. Taxation must be equal and uniform. No single property or

Property Tax and Real Estate Appraisal Services

Property Tax and Real Estate Appraisal Services Appraisers/Consultants Micheal R. Lohmeier, ASA, MAI Certified General Real Estate Appraiser Direct: 248.368.8873 E: MLohmeier@virchowkrause.com Micheal

Property Tax and Real Estate Appraisal Services Appraisers/Consultants Micheal R. Lohmeier, ASA, MAI Certified General Real Estate Appraiser Direct: 248.368.8873 E: MLohmeier@virchowkrause.com Micheal

PAYMENT UNDER PROTEST APPEAL GUIDE

PAYMENT UNDER PROTEST APPEAL GUIDE In Kansas you have two opportunities to appeal the value of your property. If you appeal at the time of paying taxes, it is called a Payment Under Protest. This guide

PAYMENT UNDER PROTEST APPEAL GUIDE In Kansas you have two opportunities to appeal the value of your property. If you appeal at the time of paying taxes, it is called a Payment Under Protest. This guide

Harris County Appraisal District

Harris County Appraisal District General Policy & Policies for Public Access 13013 Northwest Freeway P.O. Box 920975 Houston, TX 77292-0975 Telephone (713) 812-5800 Information Center (713) 957-7800 Board

Harris County Appraisal District General Policy & Policies for Public Access 13013 Northwest Freeway P.O. Box 920975 Houston, TX 77292-0975 Telephone (713) 812-5800 Information Center (713) 957-7800 Board

CALLAHAN COUNTY APPRAISAL DISTRICT 2017 ANNUAL APPRAISAL REPORT

CALLAHAN COUNTY APPRAISAL DISTRICT 2017 ANNUAL APPRAISAL REPORT Introduction The Callahan County Appraisal District is a political subdivision of the state. The Constitution of the State of Texas, the

CALLAHAN COUNTY APPRAISAL DISTRICT 2017 ANNUAL APPRAISAL REPORT Introduction The Callahan County Appraisal District is a political subdivision of the state. The Constitution of the State of Texas, the

2018 Annual Appraisal Report

2018 Annual Appraisal Report SUMMARY OF APPRAISAL ACTIVITIES, EXEMPTIONS, EQUALIZATION AND TAX RATES FOR 2018 TAX YEAR Wendy Grams, RPA, CTA, CCA CENTRAL APPRAISAL DISTRICT OF BANDERA COUNTY P. O. BOX

2018 Annual Appraisal Report SUMMARY OF APPRAISAL ACTIVITIES, EXEMPTIONS, EQUALIZATION AND TAX RATES FOR 2018 TAX YEAR Wendy Grams, RPA, CTA, CCA CENTRAL APPRAISAL DISTRICT OF BANDERA COUNTY P. O. BOX

Terrell County Appraisal District 2018 Annual Report

Terrell County Appraisal District 2018 Annual Report Introduction The Terrell County Appraisal District is a political subdivision of the State of Texas. The Texas Constitution, Texas Property Tax Code

Terrell County Appraisal District 2018 Annual Report Introduction The Terrell County Appraisal District is a political subdivision of the State of Texas. The Texas Constitution, Texas Property Tax Code

To: Property Appraisers, Taxing Authorities and Interested Parties From: James McAdams Date: June 5, 2012 Bulletin: PTO 12-04

Property Tax Oversight Bulletin: PTO 12-04 To: Property Appraisers, Taxing Authorities and Interested Parties From: James McAdams Date: Bulletin: PTO 12-04 FLORIDA DEPARTMENT OF REVENUE PROPERTY TAX INFORMATIONAL

Property Tax Oversight Bulletin: PTO 12-04 To: Property Appraisers, Taxing Authorities and Interested Parties From: James McAdams Date: Bulletin: PTO 12-04 FLORIDA DEPARTMENT OF REVENUE PROPERTY TAX INFORMATIONAL

Susan Combs Texas Comptroller of Public Accounts. Property Tax Basics. Texas Property Tax

2013 Susan Combs Texas Comptroller of Public Accounts Property Tax Basics Texas Property Tax This publication is intended to provide customer assistance to taxpayers. It does not address all aspects of

2013 Susan Combs Texas Comptroller of Public Accounts Property Tax Basics Texas Property Tax This publication is intended to provide customer assistance to taxpayers. It does not address all aspects of

Van Zandt County Appraisal District 2017 Annual Report

Van Zandt County Appraisal District 2017 Annual Report Introduction The Van Zandt County Appraisal District is a political subdivision of the state. The Constitution of the State of Texas, the Texas Property

Van Zandt County Appraisal District 2017 Annual Report Introduction The Van Zandt County Appraisal District is a political subdivision of the state. The Constitution of the State of Texas, the Texas Property

1. How can I change my mailing address? Can you change my mailing address by phone?

GENERAL FAQ s 1. How can I change my mailing address? Can you change my mailing address by phone? Please request address changes in writing indicating the new mailing address for your property and a daytime

GENERAL FAQ s 1. How can I change my mailing address? Can you change my mailing address by phone? Please request address changes in writing indicating the new mailing address for your property and a daytime

CITY OF MENOMINEE, MICHIGAN SPECIAL COUNCIL PROCEEDINGS OCTOBER 21, 2015

CITY OF MENOMINEE, MICHIGAN SPECIAL COUNCIL PROCEEDINGS OCTOBER 21, 2015 A special meeting of the Menominee City Council, City of Menominee, County of Menominee, State of Michigan, was held Wednesday,

CITY OF MENOMINEE, MICHIGAN SPECIAL COUNCIL PROCEEDINGS OCTOBER 21, 2015 A special meeting of the Menominee City Council, City of Menominee, County of Menominee, State of Michigan, was held Wednesday,

Gaines County Appraisal District 2016 Annual Report

Gaines County Appraisal District 2016 Annual Report Introduction The Gaines County Appraisal District is a political subdivision of the state, The Constitution of the State of Texas, the Texas Property

Gaines County Appraisal District 2016 Annual Report Introduction The Gaines County Appraisal District is a political subdivision of the state, The Constitution of the State of Texas, the Texas Property

2015 Annual Report. The appraisal district is governed by a Board of Directors whose primary responsibilities are to:

Refugio County Appraisal District Mailing Address: PO Box 156, Refugio, Texas 78377-0156 Physical Location: 420 North Alamo Street, Refugio, Texas 78377 Telephone Number: 361-526-5994 Website: www.refugiocad.org

Refugio County Appraisal District Mailing Address: PO Box 156, Refugio, Texas 78377-0156 Physical Location: 420 North Alamo Street, Refugio, Texas 78377 Telephone Number: 361-526-5994 Website: www.refugiocad.org

FREEDOM OF INFORMATION ACT POSTING

CHIEF COUNTY ASSESSING OFFICIAL KENDALL COUNTY ANDREW P. NICOLETTI 111 West Fox Street Rm. 303 Yorkville, Illinois 60560-1498 630-553-4146 FREEDOM OF INFORMATION ACT POSTING The purpose of the Freedom

CHIEF COUNTY ASSESSING OFFICIAL KENDALL COUNTY ANDREW P. NICOLETTI 111 West Fox Street Rm. 303 Yorkville, Illinois 60560-1498 630-553-4146 FREEDOM OF INFORMATION ACT POSTING The purpose of the Freedom

Property Tax Fairness and the Future of Further Reform

Property Tax Fairness and the Future of Further Reform Ryan Kamrowski, Director of Tax Equalization, Ward County Senator Dwight Cook, Mandan (Dist. 34) Donnell Preskey Hushka, Government Affairs Specialist,

Property Tax Fairness and the Future of Further Reform Ryan Kamrowski, Director of Tax Equalization, Ward County Senator Dwight Cook, Mandan (Dist. 34) Donnell Preskey Hushka, Government Affairs Specialist,

Van Zandt County Appraisal District 2015 Annual Report

Van Zandt County Appraisal District 2015 Annual Report Introduction The Van Zandt County Appraisal District is a political subdivision of the state. The Constitution of the State of Texas, the Texas Property

Van Zandt County Appraisal District 2015 Annual Report Introduction The Van Zandt County Appraisal District is a political subdivision of the state. The Constitution of the State of Texas, the Texas Property

FLORIDA CONSTITUTION

FLORIDA CONSTITUTION (Provisions related to ad valorem property taxes and exemptions) ARTICLE VII - FINANCE AND TAXATION SECTION 2. Taxes; rate.-- All ad valorem taxation shall be at a uniform rate within

FLORIDA CONSTITUTION (Provisions related to ad valorem property taxes and exemptions) ARTICLE VII - FINANCE AND TAXATION SECTION 2. Taxes; rate.-- All ad valorem taxation shall be at a uniform rate within

Additional senior homestead exemption.

02-1 02-1 F L O R I D A H O U S E O F R E P R E S E N T A T I V E S ENROLLED CS/HJR 169 2012 Legislature 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 House Joint Resolution

02-1 02-1 F L O R I D A H O U S E O F R E P R E S E N T A T I V E S ENROLLED CS/HJR 169 2012 Legislature 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 House Joint Resolution

Perry County. Appeal Procedures, Rules, and Regulations v.1.1

Perry County Appeal Procedures, Rules, and Regulations 2000 v.1.1 PERRY COUNTY BOARD OF ASSESSMENT APPEALS APPEAL PROCEDURES, RULES, AND REGULATIONS Property owners have the right, under Pennsylvania law,

Perry County Appeal Procedures, Rules, and Regulations 2000 v.1.1 PERRY COUNTY BOARD OF ASSESSMENT APPEALS APPEAL PROCEDURES, RULES, AND REGULATIONS Property owners have the right, under Pennsylvania law,

CHAPTER Committee Substitute for House Bill No. 7097

CHAPTER 2012-193 Committee Substitute for House Bill No. 7097 An act relating to the administration of property taxes; amending s. 192.001, F.S.; revising the definitions of the terms assessed value of

CHAPTER 2012-193 Committee Substitute for House Bill No. 7097 An act relating to the administration of property taxes; amending s. 192.001, F.S.; revising the definitions of the terms assessed value of

Jasper County Appraisal District 2016 Annual Report

Jasper County Appraisal District 2016 Annual Report Introduction The Jasper County Appraisal District is a political subdivision of the state. The Constitution of the State of Texas, the Texas Property

Jasper County Appraisal District 2016 Annual Report Introduction The Jasper County Appraisal District is a political subdivision of the state. The Constitution of the State of Texas, the Texas Property

Understanding Mississippi Property Taxes

Understanding Mississippi Property Taxes Property tax revenues are a vital component of the budgets of Mississippi s local governments. Property tax revenues allow these governments to provide important

Understanding Mississippi Property Taxes Property tax revenues are a vital component of the budgets of Mississippi s local governments. Property tax revenues allow these governments to provide important

MECOSTA COUNTY EQUALIZATION JANUARY 1 - DECEMBER 31, 2014 APRIL 16, 2015

APRIL 16, 2015 MECOSTA COUNTY EQUALIZATION JANUARY 1 - DECEMBER 31, 2014 SHILA KIANDER, MAAO 3 MECOSTA COUNTY EQUALIZATION DIRECTOR skiander@co.mecosta.mi.us Contents Message from the Director...2 Mecosta

APRIL 16, 2015 MECOSTA COUNTY EQUALIZATION JANUARY 1 - DECEMBER 31, 2014 SHILA KIANDER, MAAO 3 MECOSTA COUNTY EQUALIZATION DIRECTOR skiander@co.mecosta.mi.us Contents Message from the Director...2 Mecosta

Brazoria County Appraisal District

Brazoria County Appraisal District Annual Report 2017 Mission Statement Our mission as public servants is to demand excellence in the services provided to the taxpayers and taxing jurisdictions of Brazoria

Brazoria County Appraisal District Annual Report 2017 Mission Statement Our mission as public servants is to demand excellence in the services provided to the taxpayers and taxing jurisdictions of Brazoria

NOTICE GRAND TRAVERSE COUNTY BOARD OF COMMISSIONERS EQUALIZATION MEETING. Tuesday, April 15, 2:00 p.m.

NOTICE GRAND TRAVERSE COUNTY BOARD OF COMMISSIONERS EQUALIZATION MEETING Tuesday, April 15, 214 @ 2: p.m. Commission Chambers, Governmental Center, 4 Boardman Avenue Traverse City, Michigan 49684 The Board

NOTICE GRAND TRAVERSE COUNTY BOARD OF COMMISSIONERS EQUALIZATION MEETING Tuesday, April 15, 214 @ 2: p.m. Commission Chambers, Governmental Center, 4 Boardman Avenue Traverse City, Michigan 49684 The Board

2017 Annual Report. Fayette County Appraisal District P. O. Box 836 La Grange, TX 78945

2017 Annual Report Fayette County Appraisal District P. O. Box 836 La Grange, TX 78945 FCAD 2017 Annual Report 1 2017 ANNUAL REPORT FAYETTE COUNTY APPRAISAL DISTRICT INTRODUCTION The Fayette County Appraisal

2017 Annual Report Fayette County Appraisal District P. O. Box 836 La Grange, TX 78945 FCAD 2017 Annual Report 1 2017 ANNUAL REPORT FAYETTE COUNTY APPRAISAL DISTRICT INTRODUCTION The Fayette County Appraisal

Be It Enacted by the Legislature of the State of Florida:

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 A bill to be entitled An act relating to ad valorem taxation; amending s. 193.023, F.S.; revising authority of the property appraiser

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 A bill to be entitled An act relating to ad valorem taxation; amending s. 193.023, F.S.; revising authority of the property appraiser

HOW TO PREPARE FOR YOUR ASSESSMENT APPEAL HEARING

ASSESSMENT APPEALS BOARD COUNTY OF SANTA BARBARA HOW TO PREPARE FOR YOUR ASSESSMENT APPEAL HEARING An Information Guide For Santa Barbara County Property Owners and Authorized Agents Assessment Appeals

ASSESSMENT APPEALS BOARD COUNTY OF SANTA BARBARA HOW TO PREPARE FOR YOUR ASSESSMENT APPEAL HEARING An Information Guide For Santa Barbara County Property Owners and Authorized Agents Assessment Appeals

MEDIA RELEASE. For Immediate Release June 28, 2010: (408)

") County of Santa Clara Office of the County Assessor County Government Center, East Wing 70 West Hedding Street San Jose, California 95110-1770 1-408-299-5500 FAX 1-408-297-9526 E-Mail: david.ginsborg@asr.sccgov.org

County of Santa Clara Office of the County Assessor County Government Center, East Wing 70 West Hedding Street San Jose, California 95110-1770 1-408-299-5500 FAX 1-408-297-9526 E-Mail: david.ginsborg@asr.sccgov.org

INTRODUCTION MISSION OVERVIEW

INTRODUCTION The Austin County Appraisal District is a political subdivision of the State of Texas. The Constitution of the State of Texas, the Texas Property Tax Code, and the Rules of the Texas Comptroller

INTRODUCTION The Austin County Appraisal District is a political subdivision of the State of Texas. The Constitution of the State of Texas, the Texas Property Tax Code, and the Rules of the Texas Comptroller

Camp Central Appraisal District LEGAL AND ADMINISTRATIVE REQUIREMENTS

Camp Central Appraisal District LEGAL AND ADMINISTRATIVE REQUIREMENTS Counties are responsible for creating and establishing an Appraisal District. As a political subdivision of the state the major responsibility

Camp Central Appraisal District LEGAL AND ADMINISTRATIVE REQUIREMENTS Counties are responsible for creating and establishing an Appraisal District. As a political subdivision of the state the major responsibility

VAN ZANDT COUNTY APPRAISAL DISTRICT 2018 ANNUAL REPORT

VAN ZANDT COUNTY APPRAISAL DISTRICT 2018 ANNUAL REPORT INTRODUCTION The Van Zandt County Appraisal District is a political subdivision of the state. The Constitution of the State of Texas, the Texas Property

VAN ZANDT COUNTY APPRAISAL DISTRICT 2018 ANNUAL REPORT INTRODUCTION The Van Zandt County Appraisal District is a political subdivision of the state. The Constitution of the State of Texas, the Texas Property

STATE OF MICHIGAN COURT OF APPEALS

STATE OF MICHIGAN COURT OF APPEALS RYAN M. HUIZENGA, Petitioner-Appellant, UNPUBLISHED September 1, 2016 v No. 327682 Michigan Tax Tribunal CITY OF GRAND RAPIDS, LC No. 14-006527-TT Respondent-Appellee.

STATE OF MICHIGAN COURT OF APPEALS RYAN M. HUIZENGA, Petitioner-Appellant, UNPUBLISHED September 1, 2016 v No. 327682 Michigan Tax Tribunal CITY OF GRAND RAPIDS, LC No. 14-006527-TT Respondent-Appellee.

Residential Property Assessment Appeals

Residential Property Assessment Appeals How to appeal the assessed value of residential properties a guide for California property owners CALIFORNIA STATE BOARD OF EQUALIZATION BOARD MEMBER (Names updated

Residential Property Assessment Appeals How to appeal the assessed value of residential properties a guide for California property owners CALIFORNIA STATE BOARD OF EQUALIZATION BOARD MEMBER (Names updated

We look forward to working with you to build on our collaboration and enhance our partnership on behalf of all Minnesotans.

Date: February 27, 2017 To: County Assessors, Auditors, and Treasurers From: Cynthia Rowley, Director Property Tax Division Subject: Property Tax Services Report The Property Tax Division of the Minnesota

Date: February 27, 2017 To: County Assessors, Auditors, and Treasurers From: Cynthia Rowley, Director Property Tax Division Subject: Property Tax Services Report The Property Tax Division of the Minnesota

2016 Annual Report. Carmen Ottmer, Chief Appraiser AUSTIN COUNTY APPRAISAL DISTRICT 906 E. AMELIA ST., BELLVILLE, TEXAS 77418

2016 Annual Report Carmen Ottmer, Chief Appraiser AUSTIN COUNTY APPRAISAL DISTRICT 906 E. AMELIA ST., BELLVILLE, TEXAS 77418 INTRODUCTION The Austin County Appraisal District is a political subdivision

2016 Annual Report Carmen Ottmer, Chief Appraiser AUSTIN COUNTY APPRAISAL DISTRICT 906 E. AMELIA ST., BELLVILLE, TEXAS 77418 INTRODUCTION The Austin County Appraisal District is a political subdivision

Procedural steps. MONROE SUPREME & COUNTY COURT SCAR Program Procedures Room 545, Hall of Justice Rochester, New York CHECKLIST:

MONROE SUPREME & COUNTY COURT SCAR Program Procedures Room 545, Hall of Justice Rochester, New York 14614 585-371-3616 CHECKLIST: G G G G G G G Procedural steps General Information and filing requirements

MONROE SUPREME & COUNTY COURT SCAR Program Procedures Room 545, Hall of Justice Rochester, New York 14614 585-371-3616 CHECKLIST: G G G G G G G Procedural steps General Information and filing requirements

February 2014 Legal Calendar

1 Clerk Report list of county officers to the Secretary of State. 23-1306 1 Assessor Last date for owners, lessees and/or managers of any aircraft hangars or land upon which aircraft are parked to report

1 Clerk Report list of county officers to the Secretary of State. 23-1306 1 Assessor Last date for owners, lessees and/or managers of any aircraft hangars or land upon which aircraft are parked to report

FILING INSTRUCTIONS. A.) Read & complete PTAX-230 Form. B.) Read attached guidelines for detailed instructions. C.) To prove value, you may:

Read & complete PTAX-230 Form. B.) Read attached guidelines for detailed instructions. C.) To prove value, you may:") FILING INSTRUCTIONS A.) Read & complete PTAX-230 Form B.) Read attached guidelines for detailed instructions. C.) To prove value, you may: 1) submit an appraisal 2) submit equitable comparable properties

FILING INSTRUCTIONS A.) Read & complete PTAX-230 Form B.) Read attached guidelines for detailed instructions. C.) To prove value, you may: 1) submit an appraisal 2) submit equitable comparable properties

Central Appraisal District Colorado County

Central Appraisal District Colorado County APPRAISAL PROCESS 1. OVERVIEW A. Definition of Property Tax A tax that is measured by the value of property that a taxpayer owns. Property taxes are also called

Central Appraisal District Colorado County APPRAISAL PROCESS 1. OVERVIEW A. Definition of Property Tax A tax that is measured by the value of property that a taxpayer owns. Property taxes are also called

We hope the trends provide additional perspective on your county s work. We know it provided valuable insight on the work we do here at Revenue.

Date: March 6, 2018 To: County Assessors, Auditors, and Treasurers From: Jon Klockziem, Acting Director Subject: Property Tax Services Report The Property Tax Division of the is pleased to provide the

Date: March 6, 2018 To: County Assessors, Auditors, and Treasurers From: Jon Klockziem, Acting Director Subject: Property Tax Services Report The Property Tax Division of the is pleased to provide the

How to Petition for a Review of Your Property Taxes: County Board of Equalization

How to Petition for a Review of Your Property Taxes: County Board of Equalization Talk with the Assessor There are several reasons why you may want to petition for a review of your property taxes. Whatever

How to Petition for a Review of Your Property Taxes: County Board of Equalization Talk with the Assessor There are several reasons why you may want to petition for a review of your property taxes. Whatever

Steps For Resurfacing Your Street by HOA Online

Steps For Resurfacing Your Street by HOA Online Many of the residential streets in Bloomfield Township were developed about the same time in the 1950's through the 1970's which means most have exceeded

Steps For Resurfacing Your Street by HOA Online Many of the residential streets in Bloomfield Township were developed about the same time in the 1950's through the 1970's which means most have exceeded

Office of Legislative Services Background Report The Assessment of Real Property: Answers to Frequently Asked Questions

Office of Legislative Services Background Report The Assessment of Real Property: Answers to Frequently Asked Questions OLS Background Report No. 120 Prepared By: Local Government Date Prepared: New Jersey

Office of Legislative Services Background Report The Assessment of Real Property: Answers to Frequently Asked Questions OLS Background Report No. 120 Prepared By: Local Government Date Prepared: New Jersey

MAP. METHODS AND ASSISTANCE PROGRAM 2013 REPORT McLennan County Appraisal District. Susan Combs Texas Comptroller of Public Accounts

MAP METHODS AND ASSISTANCE PROGRAM 2013 REPORT McLennan County Appraisal District Susan Combs Texas Comptroller of Public Accounts January 22, 2014 Chief Appraiser County Appraisal District Board of Directors

MAP METHODS AND ASSISTANCE PROGRAM 2013 REPORT McLennan County Appraisal District Susan Combs Texas Comptroller of Public Accounts January 22, 2014 Chief Appraiser County Appraisal District Board of Directors

May 1, Wendy M. Grams, Central Appraisal District of Bandera County

May 1, 2018 Wendy M. Grams, Central Appraisal District of Bandera County 1 The Texas Constitution Article 8 Section 1 states: (a) Taxation shall be equal and uniform. (b) All real property and tangible

May 1, 2018 Wendy M. Grams, Central Appraisal District of Bandera County 1 The Texas Constitution Article 8 Section 1 states: (a) Taxation shall be equal and uniform. (b) All real property and tangible

ALACHUA COUNTY VALUE ADJUSTMENT BOARD. Process and Procedures 2007

ALACHUA COUNTY VALUE ADJUSTMENT BOARD Process and Procedures 2007 VALUE ADJUSTMENT BOARD County Commissioner Chair Lee Pinkoson School Board Member Vice Chair Wes Eubank County Commissioner Paula M. DeLaney

ALACHUA COUNTY VALUE ADJUSTMENT BOARD Process and Procedures 2007 VALUE ADJUSTMENT BOARD County Commissioner Chair Lee Pinkoson School Board Member Vice Chair Wes Eubank County Commissioner Paula M. DeLaney

Property Tax Overview. Budget, Finance, & Audit Committee January 3, 2017

Property Tax Overview Budget, Finance, & Audit Committee January 3, 2017 Briefing Outline Property tax base values Property tax rate Property tax exemptions Legislative Session 2 Overview Ad valorem taxes

Property Tax Overview Budget, Finance, & Audit Committee January 3, 2017 Briefing Outline Property tax base values Property tax rate Property tax exemptions Legislative Session 2 Overview Ad valorem taxes