Eligible Personal Property Exemptions for Assessors

|

|

|

- Bridget Hines

- 6 years ago

- Views:

Transcription

1 Eligible Personal Property Exemptions for Assessors Presented by Tim Schnelle, Manager of the Commercial/Industrial/Utilities Valuations Section, Assessment and Certification Division, Michigan Department of Treasury December 17, 2013

2 The purpose of today's presentation is to: Provide you with a basic understanding of the legislation as a whole. Provide you with detailed information relating to those portions of the legislation which will take effect for the 2014 assessment year. Alert you to several areas where you may be likely to encounter difficulties in implementing the enactments.

3 Contrary to the understanding of many taxpayers and assessors, the Acts do not provide for the complete exemption of business personal property. Instead, they provide for exemptions in two separate categories. The two categories of exemptions are: The Eligible Personal Property exemption (sometimes informally referred to as the (Small Taxpayer Exemption); and, Two Eligible Manufacturing Personal Property exemptions, one for new Eligible Manufacturing Personal Property and the other for previously existing Eligible Manufacturing Personal Property.

4 The Eligible Personal Property Exemption The exemption applies to personal property which is classified either as commercial personal property or as industrial personal property. The determination of whether the true cash value is less than $80,000 must be based on all commercial personal property and industrial personal property owned by, leased to, or in the possession of that owner or a related entity in that local assessing unit. It is possible for an owner that is assessed for less than $80,000 of true cash value of personal property to be ineligible for the Eligible Personal Property exemption.

5 The Eligible Personal Property Exemption (Cont d) The legislation provides that an affidavit claiming the exemption for Eligible Personal Property must be filed by February 10 th. In 2014 only, a taxpayer that has missed the February 10 th deadline may claim the exemption at the March Board of Review. The personal property statement will continue to be due on February 20.

6 The Eligible Personal Property Exemption (Cont d) The definition of Eligible Personal Property considers and includes indirect control situations when determining that the true cash value of the claimant s personal property is less than $80,000. The legislation defines control, controlled by, under common control with, and related entity, in an effort to prevent a taxpayer from gaining exemption by means of titling property in the names of related entities. The phrase "Related entity" means a person that, directly or indirectly, controls, is controlled by, or is under common control with the person claiming an exemption under this section.

7 The Eligible Personal Property Exemption (Cont d) The word "Person" means an individual, partnership, corporation, association, limited liability company, or any other legal entity. The exemption is not available to personal property which is leased or used by a person that directly or indirectly controls, is controlled by, or is under common control with the person that previously owned the property. This provision deals with sale and leaseback situations. The legislation authorizes an assessor to deny the exemption if the assessor believes that the property does not qualify.

8 The Eligible Personal Property Exemption (Cont d) The legislation authorizes an assessor to retroactively deny an exemption for the current year and the three previous years, and issue a corrected tax bill, plus interest and penalties, if he or she believes that the property was not eligible.

9 The Eligible Personal Property Exemption (Cont d) Entitlement to the exemption is determined by adding together the true cash value of the personal property which the taxpayer, or a related entity: Owns, Leases; or Possesses, in the entire assessment unit.

10 The Eligible Personal Property Exemption (Cont d) The exemption is granted to taxpayers who own or use a small amount of personal property in the local assessing unit, not to taxpayers who have small assessments because they are leasing or borrowing part of the personal property that they use to conduct their business. Therefore, the true cash value of the personal property which is owned, leased or possessed in the assessment unit, is added together to determine whether the taxpayer is entitled to the Small Taxpayer Exemption. Notice that only the property owned by the taxpayer is exempted. The personal property of lessors and other owners of personal property considered in determining the exemption for that taxpayer is not exempt unless they separately qualify for the exemption based on the property which they and related entities own, lease or possess in the local assessing unit.

11 The Eligible Personal Property Exemption (Cont d) To claim the exemption, the Taxpayer must file Form 5076, Affidavit of Owner of Eligible Personal Property Claiming Exemption from Collection of Taxes by February 10 th of the assessment year. The Taxpayer cannot receive, and the Assessor cannot grant, the Eligible Personal Property exemption unless the taxpayer fully completes and returns the Affidavit to the Assessor, so that it is actually received by the assessor by February 10 of the assessment year. The exception is 2014, when the March Board of Review can also grant the exemption. The Taxpayer must file the Affidavit every year to continue to receive the exemption.

12 The Eligible Personal Property Exemption (Cont d) If the Taxpayer files a fully completed Affidavit Form 5076 with the Assessor by February 10 th of the assessment year, the Taxpayer is excused from filing a personal property statement for that assessment year. For the 2014 assessment year only, if the Taxpayer fails to return the Affidavit by February 10 th, then the Taxpayer is permitted to petition the March Board of Review for the exemption. If the exemption is denied by the Assessor, then that denial may be appealed to the March, July or December Board of Review, and the Taxpayer may also appeal to the Michigan Tax Tribunal.

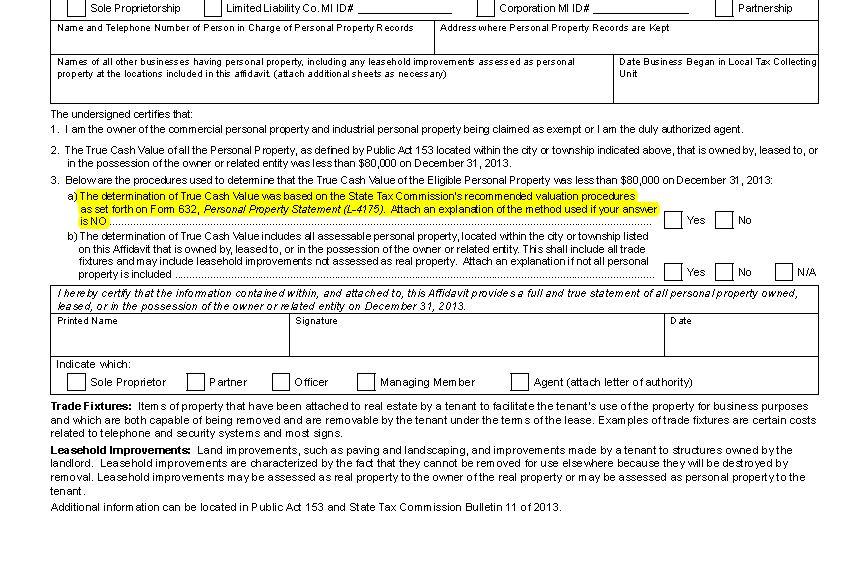

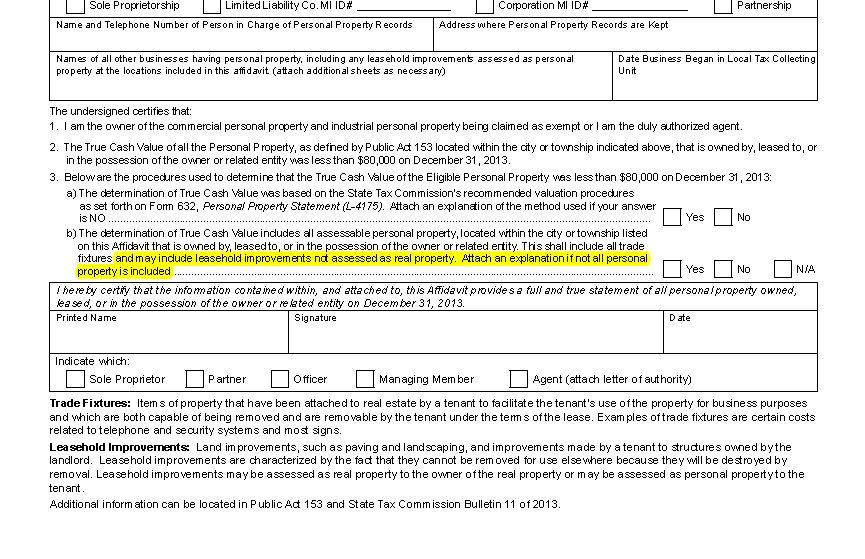

13 Areas of Particular Concern to Assessors & Taxpayers Trade Fixtures Trade Fixtures are items attached to real property by a tenant, which the tenant has the right to remove at the end of the lease term and which can be detached for use elsewhere without destroying the item in question. Under Michigan Law, if the lease is silent, the tenant has the right to remove such items. Most leases do not prevent the removal of trade fixtures. Trade fixtures do not become part of the real property and, instead, they remain personal property.

14 Areas of Particular Concern to Assessors & Taxpayers Trade Fixtures (Con d) MCL 211.8(k) specifically provides that trade fixtures are assessable as personal property. The true cash value of trade fixtures must be included in determining whether the tenant is eligible for the Small Taxpayer Exemption. A difficulty is that taxpayers frequently record trade fixture costs in the leasehold improvement section of their fixed asset accounting records, and then report them as leasehold improvements rather than as personal property.

15 Areas of Particular Concern to Assessors & Taxpayers Tenant installed leasehold improvements Tenant installed leasehold improvements are improvements to the land or structures of the landlord which have been made by the tenant. Leasehold Improvements are distinguished from trade fixtures by the fact that the leasehold improvements cannot be removed for use elsewhere without destroying them. During the tenancy of the lessee, leasehold improvements may be assessed to the tenant, as personal property, to the extent that the improvements add to the value of the real property and are not included in the assessment of the real property.

16 Areas of Particular Concern to Assessors & Taxpayers Tenant installed leasehold improvements (Con d) Leasehold improvements may be assessed as personal property pursuant to MCL 211.8(h) (unless the lease existed before 1984 and has not been substantially renegotiated since). In the alternative, leasehold improvements may be assessed to the real property interest of the landlord, based on the fact that they are really improvements to real property, not personal property at all.

17 Areas of Particular Concern to Assessors & Taxpayers Trade fixtures must be assessed as personal property to the tenant, and leasehold improvements may be assessed either as personal property to the tenant or as real property to the landlord. However, leasehold improvements are essentially real property in nature. Taxpayers generally have difficulty in distinguishing trade fixtures from leasehold improvements, particularly since they often book trade fixtures in their leasehold improvement asset accounts. This failure to discern the difference between trade fixtures and leasehold improvements may result in them mistakenly failing to consider the true cash value of trade fixtures when completing Affidavit Form 5076.

18 Areas of Particular Concern to Assessors & Taxpayers The methods used by taxpayers to calculate the true cash value Many taxpayers will not understand that they must add together the true cash values of all the personal property used in all of their business locations in the assessment unit, whether owned, leased or possessed by a related party or owned, leased or possessed by the taxpayer itself. Taxpayers have difficulty in calculating true cash value for the personal property they own and for the personal property owned by related entities. Taxpayers have particular difficulty in determining the true cash value of personal property which they or a related entity lease or possess.

19

20

21

22

23 Areas of Particular Difficulty Calculating True Cash Value Determining True Cash Value for Leased or Possessed Personal Property Distinguishing between Real Property and Personal Property Lack of rigorous application, or rigorous application, of the three part test by the Tax Tribunal. The identification of Trade Fixtures The Identification of Installation Costs for Machinery and Equipment. The handling of Leasehold Improvements. The handling of property which the Michigan Legislature or State Tax Commission has specifically indicated is personal property.

A. Inflation Rate Used in the 2017 Capped Value Formula.

5102 (Rev. 04-15) RICK SNYDER GOVERNOR STATE OF MICHIGAN DEPARTMENT OF TREASURY LANSING NICK A. KHOURI STATE TREASURER TO: FROM: Assessors Equalization Directors State Tax Commission (STC) BULLETIN NO.

5102 (Rev. 04-15) RICK SNYDER GOVERNOR STATE OF MICHIGAN DEPARTMENT OF TREASURY LANSING NICK A. KHOURI STATE TREASURER TO: FROM: Assessors Equalization Directors State Tax Commission (STC) BULLETIN NO.

Eligible Manufacturing Personal Property Tax Exemption Claim, Ad Valorem Personal Property

Michigan Department of Treasury 5278 (Rev. 08-16) Parcel Number 2017 Eligible Manufacturing Personal Property Tax Exemption Claim, Ad Valorem Personal Property Property (Combined Document) Issued under

Michigan Department of Treasury 5278 (Rev. 08-16) Parcel Number 2017 Eligible Manufacturing Personal Property Tax Exemption Claim, Ad Valorem Personal Property Property (Combined Document) Issued under

Principal Residence Exemption Review

Principal Residence Exemption Review Michigan Department of Treasury Property Services Division David A. Buick, Administrator Patrick G. Huber, Manager, Tax Exemption Section 1 The Basics 2 What is a Principal

Principal Residence Exemption Review Michigan Department of Treasury Property Services Division David A. Buick, Administrator Patrick G. Huber, Manager, Tax Exemption Section 1 The Basics 2 What is a Principal

Ì Î LEGISLATIVE ACTION... The Committee on Finance and Tax (Storms) recommended the following:

recommended the following:") Senate Comm: RCS 04/13/2010 LEGISLATIVE ACTION...... House The Committee on Finance and Tax (Storms) recommended the following: 1 2 3 4 5 6 7 8 9 10 11 12 Senate Amendment (with title amendment) Delete

Senate Comm: RCS 04/13/2010 LEGISLATIVE ACTION...... House The Committee on Finance and Tax (Storms) recommended the following: 1 2 3 4 5 6 7 8 9 10 11 12 Senate Amendment (with title amendment) Delete

Essential Services Assessment Annual Return

0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 Michigan Department of Treasury (0-), Page Essential Services Assessment Annual Return Issued under authority of the General Property Tax Act, Public Act of, and the State

0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 Michigan Department of Treasury (0-), Page Essential Services Assessment Annual Return Issued under authority of the General Property Tax Act, Public Act of, and the State

Charter Township of Lyon P.A. 198 Industrial Facilities Tax Exemption Tax Abatement Guidelines

1 Charter Township of Lyon P.A. 198 Industrial Facilities Tax Exemption Tax Abatement Guidelines A company that is in the planning phase of a major business attraction or expansion project that will include

1 Charter Township of Lyon P.A. 198 Industrial Facilities Tax Exemption Tax Abatement Guidelines A company that is in the planning phase of a major business attraction or expansion project that will include

Bulletin No. 4, January 24, 1997, Qualified Agricultural Property

Bulletin No. 4, January 24, 1997, Qualified Agricultural Property The following letterhead is reproduced for your information without the logo. STATE OF MICHIGAN John Engler, Governor DEPARTMENT OF TREASURY

Bulletin No. 4, January 24, 1997, Qualified Agricultural Property The following letterhead is reproduced for your information without the logo. STATE OF MICHIGAN John Engler, Governor DEPARTMENT OF TREASURY

COMMERCIAL REHABILITATION ACT Act 210 of The People of the State of Michigan enact:

COMMERCIAL REHABILITATION ACT Act 210 of 2005 AN ACT to provide for the establishment of commercial rehabilitation districts in certain local governmental units; to provide for the exemption from certain

COMMERCIAL REHABILITATION ACT Act 210 of 2005 AN ACT to provide for the establishment of commercial rehabilitation districts in certain local governmental units; to provide for the exemption from certain

City of Providence STATE OF RHODE ISLAND AND PROVIDENCE PLANTATIONS

City of Providence STATE OF RHODE ISLAND AND PROVIDENCE PLANTATIONS CHAPTER NO. AN ORDINANCE IN AMENDMENT OF ARTICLE X, SECTION 21-182 OF THE CODE OF ORDINANCES, ENTITLED PROPERTY TAX CLASSIFICATION Approved

City of Providence STATE OF RHODE ISLAND AND PROVIDENCE PLANTATIONS CHAPTER NO. AN ORDINANCE IN AMENDMENT OF ARTICLE X, SECTION 21-182 OF THE CODE OF ORDINANCES, ENTITLED PROPERTY TAX CLASSIFICATION Approved

How to file your Form 571-L Business Property Statement (BPS) For Small Business Owners

For Small Business Owners") How to file your Form 571-L Business Property Statement (BPS) For Small Business Owners What is a Form 571L Business Property Statement (BPS)? A property tax form that is required for declaring business

How to file your Form 571-L Business Property Statement (BPS) For Small Business Owners What is a Form 571L Business Property Statement (BPS)? A property tax form that is required for declaring business

REVISED ORDINANCE NO. 2 RESIDENTIAL LEASES

REVISED ORDINANCE NO. 2 RESIDENTIAL LEASES Section 1. Section 2. Section 3. Purpose and Authority. The purpose of this ordinance is to establish a system by which the members of the Saginaw Chippewa Indian

REVISED ORDINANCE NO. 2 RESIDENTIAL LEASES Section 1. Section 2. Section 3. Purpose and Authority. The purpose of this ordinance is to establish a system by which the members of the Saginaw Chippewa Indian

STATE TAX COMMISSION QUALIFIED AGRICULTURAL PROPERTY EXEMPTION GUIDELINES

STATE TAX COMMISSION QUALIFIED AGRICULTURAL PROPERTY EXEMPTION GUIDELINES Issued by the State Tax Commission August 2018 Table of Contents What is the Qualified Agricultural Exemption?... 2 How does Property

STATE TAX COMMISSION QUALIFIED AGRICULTURAL PROPERTY EXEMPTION GUIDELINES Issued by the State Tax Commission August 2018 Table of Contents What is the Qualified Agricultural Exemption?... 2 How does Property

An Overview of the Proposed Bonus Depreciation Regulations under Section 168(k)

") An Overview of the Proposed Bonus Depreciation Regulations under Section 168(k) August 21, 2018 Federal Bar Association 2018 (US) LLP All Rights Reserved. This communication is for general informational

An Overview of the Proposed Bonus Depreciation Regulations under Section 168(k) August 21, 2018 Federal Bar Association 2018 (US) LLP All Rights Reserved. This communication is for general informational

Accounting for Leases

Office: Business Services Procedure Contact: Director of Business Services Related Policy or Policies: Noted within procedure statement Revision History Revision Number: Change: Date: 001 Update content

Office: Business Services Procedure Contact: Director of Business Services Related Policy or Policies: Noted within procedure statement Revision History Revision Number: Change: Date: 001 Update content

C O N F I D E N T I A L

00320540000001 Bexar Appraisal District COMMON ACCT.# PID: RETURN COMPLETED RENDITION BY 1 APRIL 2018 NAME OF BUSINESS (DBA) AND LOCATION OF PROPERTY: IF OUT OF BUSINESS GIVE DATE (OPTIONAL) C O N F I

00320540000001 Bexar Appraisal District COMMON ACCT.# PID: RETURN COMPLETED RENDITION BY 1 APRIL 2018 NAME OF BUSINESS (DBA) AND LOCATION OF PROPERTY: IF OUT OF BUSINESS GIVE DATE (OPTIONAL) C O N F I

Guide to Personal Property Rendition

Guide to Personal Property Rendition If you own a business, you are required by law to report personal property that is used in that business to your county appraisal district. There are substantial penalties

Guide to Personal Property Rendition If you own a business, you are required by law to report personal property that is used in that business to your county appraisal district. There are substantial penalties

Assessing Reform Proposal Summary

Assessing Reform Proposal Summary Specify minimum quality standards that every assessing district must meet, on their own, in cooperation with other local units, or through the county. Local units could

Assessing Reform Proposal Summary Specify minimum quality standards that every assessing district must meet, on their own, in cooperation with other local units, or through the county. Local units could

OVERVIEW OF PROPERTY TAX DISASTER RELIEF PROVISIONS September 2015 Governor-Proclaimed State of Emergency

September 2015 Governor-Proclaimed State of Emergency Revenue and Taxation Code 1 Property Type Type of Relief Available Section 170 All property types New construction exclusion Section 69 All property

September 2015 Governor-Proclaimed State of Emergency Revenue and Taxation Code 1 Property Type Type of Relief Available Section 170 All property types New construction exclusion Section 69 All property

Business Personal Property

Business Personal Property Question: Are businesses required to list with local government? Answer: Yes, all businesses, whether maintaining an office or operating out of the home, must list using the

Business Personal Property Question: Are businesses required to list with local government? Answer: Yes, all businesses, whether maintaining an office or operating out of the home, must list using the

60-HR FL Real Estate Broker Post-Licensing Learning Objectives by Lesson

Lesson 1: Starting a Real Estate Office SECTION 1: BROKERAGE OFFICE ESSENTIALS Recall the characteristics of business entities that may register as a real estate brokerage and the rules involved to operate

Lesson 1: Starting a Real Estate Office SECTION 1: BROKERAGE OFFICE ESSENTIALS Recall the characteristics of business entities that may register as a real estate brokerage and the rules involved to operate

Lease Accounting: Gather your data now and understand tax implications. Tuesday, December 5, 2017

Lease Accounting: Gather your data now and understand tax implications Tuesday, December 5, 2017 Presenters Chris Stephenson Principal, Business Consulting & Technology chris.stephenson@us.gt.com Rebekah

Lease Accounting: Gather your data now and understand tax implications Tuesday, December 5, 2017 Presenters Chris Stephenson Principal, Business Consulting & Technology chris.stephenson@us.gt.com Rebekah

Adopt Local Law No. 3 of A Local Law for Landlord Rental and Property Owner Registration

Town of Cheektowaga Meeting: 10/23/18 07:00 PM 3301 Broadway Cheektowaga, NY 14227 ADOPTED RESOLUTION 2018-514 Sponsors: Councilmember Nowak, Supervisor Benczkowski Adopt Local Law No. 3 of 2018 - A Local

Town of Cheektowaga Meeting: 10/23/18 07:00 PM 3301 Broadway Cheektowaga, NY 14227 ADOPTED RESOLUTION 2018-514 Sponsors: Councilmember Nowak, Supervisor Benczkowski Adopt Local Law No. 3 of 2018 - A Local

Exposure Draft (ED) 64 Summary Leases

64 Summary Leases") AT A GLANCE January 2018 Exposure Draft (ED) 64 Summary Leases This summary provides an overview of Exposure Draft 64, Leases. Project objective: Development of ED 64: This ED proposes new requirements

AT A GLANCE January 2018 Exposure Draft (ED) 64 Summary Leases This summary provides an overview of Exposure Draft 64, Leases. Project objective: Development of ED 64: This ED proposes new requirements

Lease Accounting. Dr.T.P.Ghosh Professor, MDI, Gurgaon

Lease Accounting Dr.T.P.Ghosh Professor, MDI, Gurgaon Controversy Over Lease Classification and Accounting The basic concept of lease accounting is that some leases are merely rentals, whereas others are

Lease Accounting Dr.T.P.Ghosh Professor, MDI, Gurgaon Controversy Over Lease Classification and Accounting The basic concept of lease accounting is that some leases are merely rentals, whereas others are

STATE OF MICHIGAN COURT OF APPEALS

STATE OF MICHIGAN COURT OF APPEALS LAKE FOREST PARTNERS 2, INC., Petitioner-Appellant, FOR PUBLICATION June 6, 2006 9:05 a.m. v No. 257417 Tax Tribunal DEPARTMENT OF TREASURY, LC No. 00-292089 Respondent-Appellee.

STATE OF MICHIGAN COURT OF APPEALS LAKE FOREST PARTNERS 2, INC., Petitioner-Appellant, FOR PUBLICATION June 6, 2006 9:05 a.m. v No. 257417 Tax Tribunal DEPARTMENT OF TREASURY, LC No. 00-292089 Respondent-Appellee.

SENATE, No. 277 STATE OF NEW JERSEY. 218th LEGISLATURE PRE-FILED FOR INTRODUCTION IN THE 2018 SESSION

SENATE, No. STATE OF NEW JERSEY th LEGISLATURE PRE-FILED FOR INTRODUCTION IN THE 0 SESSION Sponsored by: Senator JAMES W. HOLZAPFEL District 0 (Ocean) Co-Sponsored by: Senator Pennacchio SYNOPSIS "Homestead

SENATE, No. STATE OF NEW JERSEY th LEGISLATURE PRE-FILED FOR INTRODUCTION IN THE 0 SESSION Sponsored by: Senator JAMES W. HOLZAPFEL District 0 (Ocean) Co-Sponsored by: Senator Pennacchio SYNOPSIS "Homestead

April 20, Assessors

53rd Legislature - 2nd Regular Session, 2018 April 20, 2018 Assessors Bill summaries and histories copyright 2018 Arizona Capitol Reports, L.L.C. Assessors Friday, Apr 20 2018 8:20 AM BILL NUMBER/ SHORT

53rd Legislature - 2nd Regular Session, 2018 April 20, 2018 Assessors Bill summaries and histories copyright 2018 Arizona Capitol Reports, L.L.C. Assessors Friday, Apr 20 2018 8:20 AM BILL NUMBER/ SHORT

Modern Real Estate Practice, 18 th Edition

Chapter 16 Leases LECTURE OUTLINE: I. Leasing Real Estate A. Definition lease 1. A contract between owner of real estate (lessor) and tenant (lessee) to transfer rights of exclusive possession and use

Chapter 16 Leases LECTURE OUTLINE: I. Leasing Real Estate A. Definition lease 1. A contract between owner of real estate (lessor) and tenant (lessee) to transfer rights of exclusive possession and use

DISCUSSION PAPER TAX IMPLICATIONS RELATED TO THE IMPLEMENTATION OF FRS 117: LEASES

The Malaysian Institute of Certified Public Accountants DISCUSSION PAPER TAX IMPLICATIONS RELATED TO THE IMPLEMENTATION OF FRS 117: LEASES Prepared by: Joint Tax Working Group on FRS Date of issue: 22

The Malaysian Institute of Certified Public Accountants DISCUSSION PAPER TAX IMPLICATIONS RELATED TO THE IMPLEMENTATION OF FRS 117: LEASES Prepared by: Joint Tax Working Group on FRS Date of issue: 22

2003 Tax Abatement Policy Guidelines & Criteria City of Shenandoah, Texas

2003 Tax Abatement Policy Guidelines & Criteria City of Shenandoah, Texas Adopted: May 27, 1993 Revised: May 28, 1997 Revised: March 26, 2003 Revised: May 14, 2003 PAGE -1- SECTION I: PREAMBLE This Tax

2003 Tax Abatement Policy Guidelines & Criteria City of Shenandoah, Texas Adopted: May 27, 1993 Revised: May 28, 1997 Revised: March 26, 2003 Revised: May 14, 2003 PAGE -1- SECTION I: PREAMBLE This Tax

Contact Us. Forms for these credits and exemptions are included with the descriptions. Ag Land Credit. Low-Rent Housing Exemption

1 of 12 12/5/2017 2:01 PM Contact Us Home» Iowa Tax / Fee Descriptions and Rates Forms for these credits and exemptions are included with the descriptions. Ag Land Credit Barn and One-Room School House

1 of 12 12/5/2017 2:01 PM Contact Us Home» Iowa Tax / Fee Descriptions and Rates Forms for these credits and exemptions are included with the descriptions. Ag Land Credit Barn and One-Room School House

Alienation of Income

Alienation of Income Marc Romaldi FTIA Kelly & Co. Lawyers Introduction Alienation of income Strategies in relation to: Leases and Licensing Improvements to property Current use of service trusts Assignments

Alienation of Income Marc Romaldi FTIA Kelly & Co. Lawyers Introduction Alienation of income Strategies in relation to: Leases and Licensing Improvements to property Current use of service trusts Assignments

RULES OF TENNESSEE STATE BOARD OF EQUALIZATION CHAPTER ASSESSMENT OF COMMERCIAL AND INDUSTRIAL TANGIBLE PERSONAL PROPERTY TABLE OF CONTENTS

RULES OF TENNESSEE STATE BOARD OF EQUALIZATION CHAPTER 0600 5 ASSESSMENT OF COMMERCIAL AND INDUSTRIAL TABLE OF CONTENTS 0600-5-.01 Definitions 0600-5-.02 Discovery 0600-5-.03 Control Records 0600-5-.04

RULES OF TENNESSEE STATE BOARD OF EQUALIZATION CHAPTER 0600 5 ASSESSMENT OF COMMERCIAL AND INDUSTRIAL TABLE OF CONTENTS 0600-5-.01 Definitions 0600-5-.02 Discovery 0600-5-.03 Control Records 0600-5-.04

Title Insurance & Leasehold Estates By: Yosi (Joe) Benlevi VP & Senior Underwriting Counsel

Benlevi VP & Senior Underwriting Counsel") By: Yosi (Joe) Benlevi VP & Senior Underwriting Counsel Title Insurance and Leasehold Estates a short history The 1975 leasehold policy Covers for increased cost of leasing an alternate space and limited

By: Yosi (Joe) Benlevi VP & Senior Underwriting Counsel Title Insurance and Leasehold Estates a short history The 1975 leasehold policy Covers for increased cost of leasing an alternate space and limited

Principles of Real Estate Chapter 17-Leases And Property Management

Principles of Real Estate Chapter 17-Leases And Property Management This chapter will explain the elements needed for a valid lease, the different rights ascribed to tenants and property owners, and the

Principles of Real Estate Chapter 17-Leases And Property Management This chapter will explain the elements needed for a valid lease, the different rights ascribed to tenants and property owners, and the

SALT Whitepapers. Definitions for Purposes of the Brownfield Credit

Business Strategists Certified Public Accountants Echelbarger, Himebaugh, Tamm & Co., P.C. SALT Whitepapers An eligible taxpayer may claim a credit against the Single Business Tax for a percentage of the

Business Strategists Certified Public Accountants Echelbarger, Himebaugh, Tamm & Co., P.C. SALT Whitepapers An eligible taxpayer may claim a credit against the Single Business Tax for a percentage of the

Business Personal Property Return (File this tax return between October 1 and December 31 with the above taxing official)

") ADV-40 6/07 County: Taxing Official: Mailing Address: Tax Year Telephone Number: Business Personal Property Return (File this tax return between October 1 and December 31 with the above taxing official)

ADV-40 6/07 County: Taxing Official: Mailing Address: Tax Year Telephone Number: Business Personal Property Return (File this tax return between October 1 and December 31 with the above taxing official)

CORPORATE REORGANIZATIONS- PART I SECTION 85 TRANSFERS - INCOME TAX CONSIDERATIONS

CORPORATE REORGANIZATIONS- PART I SECTION 85 TRANSFERS - INCOME TAX CONSIDERATIONS This issue of the Legal Business Report provides current information to the clients of Alpert Law Firm on various types

CORPORATE REORGANIZATIONS- PART I SECTION 85 TRANSFERS - INCOME TAX CONSIDERATIONS This issue of the Legal Business Report provides current information to the clients of Alpert Law Firm on various types

APPLICATION FOR EXEMPTION FROM PROPERTY TAXATION

62A023 (7-13) Commonwealth of Kentucky DEPARTMENT OF REVENUE APPLICATION FOR EXEMPTION FROM PROPERTY TAXATION Office of Property Valuation Phone: 502-564-8338 Fax: 502-564-8368 This application is to be

62A023 (7-13) Commonwealth of Kentucky DEPARTMENT OF REVENUE APPLICATION FOR EXEMPTION FROM PROPERTY TAXATION Office of Property Valuation Phone: 502-564-8338 Fax: 502-564-8368 This application is to be

4/10/2012. Long-Lived Assets and Depreciation. Overview of Long-lived Assets. Learning Objectives (LO) Learning Objectives (LO)

Learning Objectives (LO)") Learning Objectives (LO) CHAPTER Long-Lived Assets and Depreciation 8 After studying this chapter, you should be able to 1. Distinguish a company s expenses from expenditures that it should capitalize

Learning Objectives (LO) CHAPTER Long-Lived Assets and Depreciation 8 After studying this chapter, you should be able to 1. Distinguish a company s expenses from expenditures that it should capitalize

Leases (S.566) Manual Part

Manual Part") Leases (S.566) Manual Part 19-2-21 Document last reviewed May 2017 1 Leases (S.566) 21.1 A lease is a particular form of wasting asset which is subject to special rules. For Capital Gains Tax purposes,

Leases (S.566) Manual Part 19-2-21 Document last reviewed May 2017 1 Leases (S.566) 21.1 A lease is a particular form of wasting asset which is subject to special rules. For Capital Gains Tax purposes,

How to Petition for a Review of Your Property Taxes: County Board of Equalization

How to Petition for a Review of Your Property Taxes: County Board of Equalization Talk with the Assessor There are several reasons why you may want to petition for a review of your property taxes. Whatever

How to Petition for a Review of Your Property Taxes: County Board of Equalization Talk with the Assessor There are several reasons why you may want to petition for a review of your property taxes. Whatever

November 2017 Legal Calendar

1 Sheriff, Clerk of the District, Clerk, County Board Sheriff or such person in charge of the administration of the jail must file jail report with the clerk of the district court and the county clerk,

1 Sheriff, Clerk of the District, Clerk, County Board Sheriff or such person in charge of the administration of the jail must file jail report with the clerk of the district court and the county clerk,

Chapter 15 Leases 15-1

Chapter 15 Leases 1. Why Leasing sometimes makes more sense 2. The accounting issues in recording a lease transaction 3. The types of contractual provisions in lease 4. The lease classification: capital

Chapter 15 Leases 1. Why Leasing sometimes makes more sense 2. The accounting issues in recording a lease transaction 3. The types of contractual provisions in lease 4. The lease classification: capital

March 9, Assessors

53rd Legislature - 2nd Regular Session, 2018 March 9, 2018 Assessors Bill summaries and histories copyright 2018 Arizona Capitol Reports, L.L.C. Assessors Friday, Mar 9 2018 9:33 AM BILL NUMBER/ SHORT

53rd Legislature - 2nd Regular Session, 2018 March 9, 2018 Assessors Bill summaries and histories copyright 2018 Arizona Capitol Reports, L.L.C. Assessors Friday, Mar 9 2018 9:33 AM BILL NUMBER/ SHORT

Bexar Appraisal District COMMON ACCT.#

MAILING ADDRESS Bexar Appraisal District COMMON ACCT.# RETURN COMPLETED RENDITION BY 1 APRIL 2018 NAME OF BUSINESS (DBA) AND LOCATION OF PROPERTY: IF OUT OF BUSINESS, GIVE DATE C O N F I D E N T I A L

MAILING ADDRESS Bexar Appraisal District COMMON ACCT.# RETURN COMPLETED RENDITION BY 1 APRIL 2018 NAME OF BUSINESS (DBA) AND LOCATION OF PROPERTY: IF OUT OF BUSINESS, GIVE DATE C O N F I D E N T I A L

STATE OF WEST VIRGINIA

OF WEST VIRGINIA Office of County Assessor Commercial Business Property Return County Code: 20 District: Account No.: Business Code: (rev. 2017) THIS RETURN IS TO BE FILED AS SOON AS POSSIBLE AFTER JULY

OF WEST VIRGINIA Office of County Assessor Commercial Business Property Return County Code: 20 District: Account No.: Business Code: (rev. 2017) THIS RETURN IS TO BE FILED AS SOON AS POSSIBLE AFTER JULY

Frequently Asked Questions Rent Review, Rent Stabilization, and Limitations on Evictions (Ordinance 3148)

") Frequently Asked Questions Rent Review, Rent Stabilization, and Limitations on Evictions (Ordinance 3148) A. General Questions The FAQ has four sections. Please review the sections below: A. General Questions

Frequently Asked Questions Rent Review, Rent Stabilization, and Limitations on Evictions (Ordinance 3148) A. General Questions The FAQ has four sections. Please review the sections below: A. General Questions

ASSIGNMENT OF LEASES. Presented by Andrew Brown, Principal Brown & Associates, Commercial Lawyers. 8 March 2016

ASSIGNMENT OF LEASES Presented by Andrew Brown, Principal Brown & Associates, Commercial Lawyers 8 March 2016 CLE Papers 8 March 2016 CONTENTS Page No Scope of Paper 2 A. Preliminary matters 1. Be clear

ASSIGNMENT OF LEASES Presented by Andrew Brown, Principal Brown & Associates, Commercial Lawyers 8 March 2016 CLE Papers 8 March 2016 CONTENTS Page No Scope of Paper 2 A. Preliminary matters 1. Be clear

GST/HST New Residential Rental Property Rebate

GST/HST New Residential Rental Property Rebate Includes Forms GST524 and GST525 RC4231(E) Rev.06 Before you start What s new Effective July 1, 2006, under proposed legislation, the GST rate will be reduced

GST/HST New Residential Rental Property Rebate Includes Forms GST524 and GST525 RC4231(E) Rev.06 Before you start What s new Effective July 1, 2006, under proposed legislation, the GST rate will be reduced

New Developments in Real Estate Law. Tuesday, June 26, 2018

New Developments in Real Estate Law Tuesday, June 26, 2018 Bill 139 Land Use Planning Changes in Ontario Joel Farber Bill 139 April 3, 2018 New Law Building Better Communities and Conserving Watersheds

New Developments in Real Estate Law Tuesday, June 26, 2018 Bill 139 Land Use Planning Changes in Ontario Joel Farber Bill 139 April 3, 2018 New Law Building Better Communities and Conserving Watersheds

IMPORTANT ANNOUNCEMENT: Our website is changing! Please click here for details.

IMPORTANT ANNOUNCEMENT: Our website is changing! Please click here for details. Home Search Downloads Exemptions Agriculture Maps Tangible Links Contact Home Frequently Asked Questions (FAQ) Frequently

IMPORTANT ANNOUNCEMENT: Our website is changing! Please click here for details. Home Search Downloads Exemptions Agriculture Maps Tangible Links Contact Home Frequently Asked Questions (FAQ) Frequently

Be It Enacted by the Legislature of the State of Florida:

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 A bill to be entitled An act relating to ad valorem taxation; amending s. 193.023, F.S.; revising authority of the property appraiser

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 A bill to be entitled An act relating to ad valorem taxation; amending s. 193.023, F.S.; revising authority of the property appraiser

Travis Central Appraisal District (TCAD)

") Travis Central Appraisal District (TCAD) 2017 Business Personal Property Rendition General Information If original cost was provided on a previous years rendition, those costs are preprinted in Schedule

Travis Central Appraisal District (TCAD) 2017 Business Personal Property Rendition General Information If original cost was provided on a previous years rendition, those costs are preprinted in Schedule

TAX ABATEMENT GUIDELINES SUMMARY

TAX ABATEMENT GUIDELINES SUMMARY OBJECTIVES Primary job creation -- target industries. Amount abatement -- minimum to be competitive. Fair to taxing jurisdictions -- It is a local option. Fair to existing

TAX ABATEMENT GUIDELINES SUMMARY OBJECTIVES Primary job creation -- target industries. Amount abatement -- minimum to be competitive. Fair to taxing jurisdictions -- It is a local option. Fair to existing

APPLICATION FOR EXEMPTION FROM PROPERTY TAXATION FOR RELIGIOUS ORGANIZATIONS

62A023-R (12-07) Commonwealth of Kentucky DEPARTMENT OF REVENUE APPLICATION FOR EXEMPTION FROM PROPERTY TAXATION FOR RELIGIOUS ORGANIZATIONS This application is to be used by institutions of religion seeking

62A023-R (12-07) Commonwealth of Kentucky DEPARTMENT OF REVENUE APPLICATION FOR EXEMPTION FROM PROPERTY TAXATION FOR RELIGIOUS ORGANIZATIONS This application is to be used by institutions of religion seeking

APPLICATION FOR EXEMPTION PROPERTY TAXATION

STATE OF UTAH APPLICATION FOR EXEMPTION PROPERTY TAXATION TO THE SALT LAKE COUNTY BOARD OF EQUALIZATION: SALT LAKE COUNTY Application Is Hereby Made For Exemption From Ad-Valorem Property Tax Of The Following

STATE OF UTAH APPLICATION FOR EXEMPTION PROPERTY TAXATION TO THE SALT LAKE COUNTY BOARD OF EQUALIZATION: SALT LAKE COUNTY Application Is Hereby Made For Exemption From Ad-Valorem Property Tax Of The Following

4/4/2018. GASB's New Leases Standard

GASB's New Leases Standard April 4, 2018 1 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing this webinar in a group Complete group attendance form

GASB's New Leases Standard April 4, 2018 1 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing this webinar in a group Complete group attendance form

COUNTY OF YANCEY North Carolina INVESTMENT GRANT PROGRAM

Yancey Manager 110 Town Square, Room 11 Burnsville, NC 28714 828-682-3971 COUNTY OF YANCEY North Carolina INVESTMENT GRANT PROGRAM Instructions for form Y-1 GENERAL INFORMATION Form Y-1 is required to

Yancey Manager 110 Town Square, Room 11 Burnsville, NC 28714 828-682-3971 COUNTY OF YANCEY North Carolina INVESTMENT GRANT PROGRAM Instructions for form Y-1 GENERAL INFORMATION Form Y-1 is required to

How to Maximize this Unit

Unit 18 Leases How to Maximize this Unit Have your book open to the Unit Have your recorder (iphone voice command recommended or voice recorder on Android) ready to record, with proper title prepared.

Unit 18 Leases How to Maximize this Unit Have your book open to the Unit Have your recorder (iphone voice command recommended or voice recorder on Android) ready to record, with proper title prepared.

H.329. It is hereby enacted by the General Assembly of the State of Vermont: (a) Land which has been classified as agricultural land or managed forest

Land which has been classified as agricultural land or managed forest") 2013 Page 1 of 10 H.329 An act relating to use value appraisals It is hereby enacted by the General Assembly of the State of Vermont: Sec. 1. 32 V.S.A. 3757 is amended to read: 3757. LAND USE CHANGE TAX

2013 Page 1 of 10 H.329 An act relating to use value appraisals It is hereby enacted by the General Assembly of the State of Vermont: Sec. 1. 32 V.S.A. 3757 is amended to read: 3757. LAND USE CHANGE TAX

UNDERSTANDING PROPERTY TAXES IN COLORADO

UNDERSTANDING PROPERTY TAXES IN COLORADO This brochure was created to provide general information on the Colorado property tax system. For more specific information on any one of these topics, please visit

UNDERSTANDING PROPERTY TAXES IN COLORADO This brochure was created to provide general information on the Colorado property tax system. For more specific information on any one of these topics, please visit

Assessment Overview. Gallagher Amendment Interim Committee. July 13, 2018

Assessment Overview Gallagher Amendment Interim Committee July 13, 2018 Life s FAQs: Why is the sky blue? How does gravity work? Are we there yet? What happens in an Assessor s office.. how does property

Assessment Overview Gallagher Amendment Interim Committee July 13, 2018 Life s FAQs: Why is the sky blue? How does gravity work? Are we there yet? What happens in an Assessor s office.. how does property

ENROLLED HOUSE BILL No. 4975

Act No. 505 Public Acts of 2012 Approved by the Governor December 27, 2012 Filed with the Secretary of State December 28, 2012 EFFECTIVE DATE: April 1, 2014 Introduced by Rep. O Brien STATE OF MICHIGAN

Act No. 505 Public Acts of 2012 Approved by the Governor December 27, 2012 Filed with the Secretary of State December 28, 2012 EFFECTIVE DATE: April 1, 2014 Introduced by Rep. O Brien STATE OF MICHIGAN

The Basics of Municipal Leasing

The Basics of Municipal Leasing 38 th Annual AGLF Conference May 2, 2018 Chicago, Illinois David G. Roeder, SVP Texas Capital Bank, N.A. How do State & Local Governments Traditionally Raise Capital? 1.

The Basics of Municipal Leasing 38 th Annual AGLF Conference May 2, 2018 Chicago, Illinois David G. Roeder, SVP Texas Capital Bank, N.A. How do State & Local Governments Traditionally Raise Capital? 1.

CHAPTER Senate Bill No. 4-D

CHAPTER 2007-339 Senate Bill No. 4-D An act relating to ad valorem taxation; authorizing the Department of Revenue to adopt emergency rules; providing for application and renewal thereof; requiring the

CHAPTER 2007-339 Senate Bill No. 4-D An act relating to ad valorem taxation; authorizing the Department of Revenue to adopt emergency rules; providing for application and renewal thereof; requiring the

1. How can I change my mailing address? Can you change my mailing address by phone?

GENERAL FAQ s 1. How can I change my mailing address? Can you change my mailing address by phone? Please request address changes in writing indicating the new mailing address for your property and a daytime

GENERAL FAQ s 1. How can I change my mailing address? Can you change my mailing address by phone? Please request address changes in writing indicating the new mailing address for your property and a daytime

- CODE OF ORDINANCES Chapter 48 - PROPERTY MAINTENANCE ARTICLE III. ONE AND TWO UNIT DWELLING RENTAL PROPERTIES

Sec. 48-40. Definitions. Sec. 48-41. Registry of owners and premises. Sec. 48-42. Certificate of compliance required. Sec. 48-43. Issuance of certificate of compliance. Sec. 48-44. Right to examine certificate

Sec. 48-40. Definitions. Sec. 48-41. Registry of owners and premises. Sec. 48-42. Certificate of compliance required. Sec. 48-43. Issuance of certificate of compliance. Sec. 48-44. Right to examine certificate

2018 WIND GENERATION PROPERTY STATEMENT

BOE-571-W (P1) REV. 03 (06-17) RETURN THIS ORIGINAL FORM. COPIES WILL NOT BE ACCEPTED. OFFICIAL REQUIREMENT A report on this form is required by section 441(a) of the Revenue and Taxation Code (R&T). The

BOE-571-W (P1) REV. 03 (06-17) RETURN THIS ORIGINAL FORM. COPIES WILL NOT BE ACCEPTED. OFFICIAL REQUIREMENT A report on this form is required by section 441(a) of the Revenue and Taxation Code (R&T). The

State of Arizona Board of Equalization 100 N. 15 th Avenue Ste 130 Phoenix, Arizona (602) SUBSTANTIVE POLICY STATEMENT DIRECTORY

SUBSTANTIVE POLICY STATEMENT DIRECTORY") DIRECTORY # SBOE-04-001 - Board policy on what criteria must be met for a parcel to qualify as class four (rental residential) property under A.R.S. 42-12002(A)(1). Effective June 1, 2004 # SBOE-04-002

DIRECTORY # SBOE-04-001 - Board policy on what criteria must be met for a parcel to qualify as class four (rental residential) property under A.R.S. 42-12002(A)(1). Effective June 1, 2004 # SBOE-04-002

SANDS TOWNSHIP MARQUETTE COUNTY, MICHIGAN

SANDS TOWNSHIP MARQUETTE COUNTY, MICHIGAN ORDINANCE AUTHORIZING AND PERMITTING COMMERCIAL MARIHUANA FACILITIES Number 57 Adopted: December 12, 2017 At a regular meeting of the Township Board of Sands Township,

SANDS TOWNSHIP MARQUETTE COUNTY, MICHIGAN ORDINANCE AUTHORIZING AND PERMITTING COMMERCIAL MARIHUANA FACILITIES Number 57 Adopted: December 12, 2017 At a regular meeting of the Township Board of Sands Township,

Technical Line FASB final guidance

No. 2018-18 13 December 2018 Technical Line FASB final guidance How the new leases standard affects life sciences entities In this issue: Overview... 1 Key considerations... 2 Scope and scope exceptions...

No. 2018-18 13 December 2018 Technical Line FASB final guidance How the new leases standard affects life sciences entities In this issue: Overview... 1 Key considerations... 2 Scope and scope exceptions...

July 30, Marvin C. Jones, Esquire Jasper County Attorney Post Office Box 420 Ridgeland, South Carolina Dear Mr.

ALAN WILSON ATIORNEY GENERAL Marvin C. Jones, Esquire Jasper County Attorney Post Office Box 420 Ridgeland, South Carolina 29936 Dear Mr. Jones: Attorney General Alan Wilson has referred your letter of

ALAN WILSON ATIORNEY GENERAL Marvin C. Jones, Esquire Jasper County Attorney Post Office Box 420 Ridgeland, South Carolina 29936 Dear Mr. Jones: Attorney General Alan Wilson has referred your letter of

CLAIM FROM ASSIGNEE OF OWNER OF RECORD

COUNTY OF EL DORADO CLAIM FOR EXCESS PROCEEDS FROM THE SALE OF TAX DEFAULTED PROPERTY California Revenue and Taxation Code Section 4675 CLAIM FROM ASSIGNEE OF OWNER OF RECORD The undersigned Assignee of

COUNTY OF EL DORADO CLAIM FOR EXCESS PROCEEDS FROM THE SALE OF TAX DEFAULTED PROPERTY California Revenue and Taxation Code Section 4675 CLAIM FROM ASSIGNEE OF OWNER OF RECORD The undersigned Assignee of

INFORMATION ON 2017 PROPERTY TAX ASSESSMENTS AND APPEALS IN ORLEANS PARISH Property Tax Assessment & Appeal Information

INFORMATION ON 2017 PROPERTY TAX ASSESSMENTS AND APPEALS IN ORLEANS PARISH 2018 Property Tax Assessment & Appeal Information July 15 th August 15 th Assessor opens tax lists to public for inspection. Informal

INFORMATION ON 2017 PROPERTY TAX ASSESSMENTS AND APPEALS IN ORLEANS PARISH 2018 Property Tax Assessment & Appeal Information July 15 th August 15 th Assessor opens tax lists to public for inspection. Informal

Chicago Title

LEGISLATION AFFECTING REAL ESTATE TITLES 2015-2016 Chicago Title 1 NC General Assembly / Legislation http://www.ncga.state.nc.us/legislation/legislation.html 2 Landlord/Tenant in Foreclosure on Single-Family

LEGISLATION AFFECTING REAL ESTATE TITLES 2015-2016 Chicago Title 1 NC General Assembly / Legislation http://www.ncga.state.nc.us/legislation/legislation.html 2 Landlord/Tenant in Foreclosure on Single-Family

Assembly Bill No. 489 Committee on Growth and Infrastructure CHAPTER...

Assembly Bill No. 489 Committee on Growth and Infrastructure CHAPTER... AN ACT relating to the taxation of property; providing for the partial abatement of the ad valorem taxes imposed on property; directing

Assembly Bill No. 489 Committee on Growth and Infrastructure CHAPTER... AN ACT relating to the taxation of property; providing for the partial abatement of the ad valorem taxes imposed on property; directing

SENATE, No STATE OF NEW JERSEY. 208th LEGISLATURE INTRODUCED MAY 6, 1999

SENATE, No. STATE OF NEW JERSEY 0th LEGISLATURE INTRODUCED MAY, Sponsored by: Senator WALTER J. KAVANAUGH District (Morris and Somerset) SYNOPSIS Provides standards for retention of records of certain

SENATE, No. STATE OF NEW JERSEY 0th LEGISLATURE INTRODUCED MAY, Sponsored by: Senator WALTER J. KAVANAUGH District (Morris and Somerset) SYNOPSIS Provides standards for retention of records of certain

Third District Court of Appeal State of Florida, January Term, A.D. 2011

Third District Court of Appeal State of Florida, January Term, A.D. 2011 Opinion filed April 13, 2011. Not final until disposition of timely filed motion for rehearing. Nos. 3D10-979 and 3D09-1924 Lower

Third District Court of Appeal State of Florida, January Term, A.D. 2011 Opinion filed April 13, 2011. Not final until disposition of timely filed motion for rehearing. Nos. 3D10-979 and 3D09-1924 Lower

Glossary of Terms Greenville County Register of Deeds

Glossary of Terms Greenville County Register of Deeds Disclaimer: This glossary of terms was compiled by Greenville County solely as a public service. Greenville County does not warrant the accuracy of

Glossary of Terms Greenville County Register of Deeds Disclaimer: This glossary of terms was compiled by Greenville County solely as a public service. Greenville County does not warrant the accuracy of

Staff Analysis and Economic Impact Statement

Staff Analysis and Economic Impact Statement Measure: SR 13 REFERENCE: ACTION: Sponsor: Subject: Finance and Tax Committee Just Valuation of Property 1. FTC 2. TBRC Favorable Pre-meeting Date: March 13,

Staff Analysis and Economic Impact Statement Measure: SR 13 REFERENCE: ACTION: Sponsor: Subject: Finance and Tax Committee Just Valuation of Property 1. FTC 2. TBRC Favorable Pre-meeting Date: March 13,

(35 ILCS 200/15-175) Sec General homestead exemption. (a) Except as provided in Sections and , homestead property is entitled

Sec General homestead exemption. (a) Except as provided in Sections and , homestead property is entitled") (35 ILCS 200/15-175) Sec. 15-175. General homestead exemption. (a) Except as provided in Sections 15-176 and 15-177, homestead property is entitled to an annual homestead exemption limited, except as described

(35 ILCS 200/15-175) Sec. 15-175. General homestead exemption. (a) Except as provided in Sections 15-176 and 15-177, homestead property is entitled to an annual homestead exemption limited, except as described

Denton Central Appraisal District P O Box Denton, TX (940)

") Denton Central Appraisal District P O Box 50746 Denton, TX 76206-0746 (940) 349-3800 NEW HOMESTEAD EXEMPTION APPLICATION RULES Dear Property Owner: Please complete the following application for Residential

Denton Central Appraisal District P O Box 50746 Denton, TX 76206-0746 (940) 349-3800 NEW HOMESTEAD EXEMPTION APPLICATION RULES Dear Property Owner: Please complete the following application for Residential

LINEAL HEIR HOMESTEAD DENSITY EXEMPTION APPLICATION. Levy County, Florida

LINEAL HEIR HOMESTEAD DENSITY EXEMPTION APPLICATION Levy County, Florida Petition Number: HDE Fee: $125.00 Filing Date: TO THE LEVY COUNTY PLAT REVIEW COMMITTEE Application is hereby made to the Levy County

LINEAL HEIR HOMESTEAD DENSITY EXEMPTION APPLICATION Levy County, Florida Petition Number: HDE Fee: $125.00 Filing Date: TO THE LEVY COUNTY PLAT REVIEW COMMITTEE Application is hereby made to the Levy County

City of Long Beach Mills Act Program Pre-Application Workshop. Saturday, February 23, :00 am 12:00 pm Long Beach Gas & Oil Auditorium

City of Long Beach Mills Act Program Pre-Application Workshop Saturday, February 23, 2019 10:00 am 12:00 pm Long Beach Gas & Oil Auditorium Introduction Alejandro Plascencia Historic Preservation Planner

City of Long Beach Mills Act Program Pre-Application Workshop Saturday, February 23, 2019 10:00 am 12:00 pm Long Beach Gas & Oil Auditorium Introduction Alejandro Plascencia Historic Preservation Planner

LANDLORD AND TENANT RELATIONSHIPS Act 348 of 1972

LANDLORD AND TENANT RELATIONSHIPS Act 348 of 1972 AN ACT to regulate relationships between landlords and tenants relative to rental agreements for rental units; to regulate the payment, repayment, use

LANDLORD AND TENANT RELATIONSHIPS Act 348 of 1972 AN ACT to regulate relationships between landlords and tenants relative to rental agreements for rental units; to regulate the payment, repayment, use

2) All long-term leases should be capitalized in the accounts by the lessee.

All long-term leases should be capitalized in the accounts by the lessee.") Chapter 18 Leases 1) The principal attribute of finance leases is that the risks and rewards of asset ownership are deemed to remain with the lessor. LO: 18-02 List the criteria for classification of a

Chapter 18 Leases 1) The principal attribute of finance leases is that the risks and rewards of asset ownership are deemed to remain with the lessor. LO: 18-02 List the criteria for classification of a

HUU-AY-AHT FIRST NATIONS

HUU-AY-AHT FIRST NATIONS LAND ACT OFFICIAL CONSOLIDATION Current to March 12, 2015 The Huu-ay-aht Legislature enacts this law to provide a fair and effective system for the management, protection and disposition

HUU-AY-AHT FIRST NATIONS LAND ACT OFFICIAL CONSOLIDATION Current to March 12, 2015 The Huu-ay-aht Legislature enacts this law to provide a fair and effective system for the management, protection and disposition

IRS guidance on claiming a payment in lieu of investment tax credits for solar, fuel cells, wind, biomass, geothermal, and other facilities

JULY 14, 2009 IRS guidance on claiming a payment in lieu of investment tax credits for solar, fuel cells, wind, biomass, geothermal, and other facilities By Forrest David Milder and Michael J. Goldman

JULY 14, 2009 IRS guidance on claiming a payment in lieu of investment tax credits for solar, fuel cells, wind, biomass, geothermal, and other facilities By Forrest David Milder and Michael J. Goldman

MEMORANDUM. Executive Summary

To: New Jersey Law Revision Commission From: Susan G. Thatch Re: Bulk sale tax notification N.J.S. 54:50-38 Date: January 11, 2016 MEMORANDUM Executive Summary In November 2015, the Commission authorized

To: New Jersey Law Revision Commission From: Susan G. Thatch Re: Bulk sale tax notification N.J.S. 54:50-38 Date: January 11, 2016 MEMORANDUM Executive Summary In November 2015, the Commission authorized

ORDINANCE NO

ORDINANCE NO. 02-787 AN ORDINANCE OF THE CITY OF POMEROY, WASHINGTON, ADDING A NEW CHAPTER 14.28 TO THE POMEROY MUNICIPAL CODE; ADOPTING REGULATIONS PERTAINING TO HISTORIC PRESERVATION IN THE CITY OF POMEROY;

ORDINANCE NO. 02-787 AN ORDINANCE OF THE CITY OF POMEROY, WASHINGTON, ADDING A NEW CHAPTER 14.28 TO THE POMEROY MUNICIPAL CODE; ADOPTING REGULATIONS PERTAINING TO HISTORIC PRESERVATION IN THE CITY OF POMEROY;

CITY COUNCIL AGENDA REPORT

CITY COUNCIL AGENDA REPORT Subject: COUNCIL MOTION NABI BUILDING LEASE NEGOTIATIONS On July 13, 2015 Councillor Hughes provided notice in accordance with Section 23 of Procedure Bylaw 35/2009 that she

CITY COUNCIL AGENDA REPORT Subject: COUNCIL MOTION NABI BUILDING LEASE NEGOTIATIONS On July 13, 2015 Councillor Hughes provided notice in accordance with Section 23 of Procedure Bylaw 35/2009 that she

For the purpose of this Chapter, the following definitions shall apply unless the context clearly indicates or requires a different meaning:

CHAPTER 12 BUSINESS REGISTRATION Section 12.1. Purpose Section 12.2. Definitions Section 12.3. Construction of this Chapter Section 12.4. Requirement for Registration Section 12.5. Period of Registration;

CHAPTER 12 BUSINESS REGISTRATION Section 12.1. Purpose Section 12.2. Definitions Section 12.3. Construction of this Chapter Section 12.4. Requirement for Registration Section 12.5. Period of Registration;

Community Preservation Act Answers To Frequently Asked Questions

Community Preservation Act Answers To Frequently Asked Questions On September 14, 2000, former Governor Paul Cellucci and Lieutenant Governor Jane Swift signed the Community Preservation Act into law.

Community Preservation Act Answers To Frequently Asked Questions On September 14, 2000, former Governor Paul Cellucci and Lieutenant Governor Jane Swift signed the Community Preservation Act into law.

Central Appraisal District Colorado County

Central Appraisal District Colorado County APPRAISAL PROCESS 1. OVERVIEW A. Definition of Property Tax A tax that is measured by the value of property that a taxpayer owns. Property taxes are also called

Central Appraisal District Colorado County APPRAISAL PROCESS 1. OVERVIEW A. Definition of Property Tax A tax that is measured by the value of property that a taxpayer owns. Property taxes are also called

Real Estate 63-Hour Sales Associate Pre-Licensing Course. Topics Covered & Learning Objectives

Real Estate 63-Hour Sales Associate Pre-Licensing Course Topics Covered & Learning Objectives Lesson 1: Administrative Matters And Course Overview; The Real Estate Business Describe the various activities

Real Estate 63-Hour Sales Associate Pre-Licensing Course Topics Covered & Learning Objectives Lesson 1: Administrative Matters And Course Overview; The Real Estate Business Describe the various activities

Chapter 58 - HUMAN RELATIONS

ARTICLE I. - IN GENERAL ARTICLE II. - EQUAL HOUSING Chapter 58 - HUMAN RELATIONS Secs. 58-1 58-30. - Reserved. ARTICLE I. - IN GENERAL Secs. 58-1 58-30. - RESERVED. 491 Code of Ordinanances 2013, Rochelle,

ARTICLE I. - IN GENERAL ARTICLE II. - EQUAL HOUSING Chapter 58 - HUMAN RELATIONS Secs. 58-1 58-30. - Reserved. ARTICLE I. - IN GENERAL Secs. 58-1 58-30. - RESERVED. 491 Code of Ordinanances 2013, Rochelle,

TOWNSHIP OF HARTLAND ORDINANCE NO. 57-1, AN ORDINANCE AMENDING THE LAND DIVISION ORDINANCE

TOWNSHIP OF HARTLAND ORDINANCE NO. 57-1, AN ORDINANCE AMENDING THE LAND DIVISION ORDINANCE An ordinance to amend the Land Division Ordinance enacted pursuant to but not limited to the State Land Division

TOWNSHIP OF HARTLAND ORDINANCE NO. 57-1, AN ORDINANCE AMENDING THE LAND DIVISION ORDINANCE An ordinance to amend the Land Division Ordinance enacted pursuant to but not limited to the State Land Division

Analysing lessee financial statements and Non-GAAP performance measures

February 2019 IFRS Foundation The Essentials Issue No. 5 Analysing lessee financial statements and Non-GAAP performance measures Introduction Investors and company managers generally view free cash flow

February 2019 IFRS Foundation The Essentials Issue No. 5 Analysing lessee financial statements and Non-GAAP performance measures Introduction Investors and company managers generally view free cash flow

Tax and Business Incentive Program Ordinance

Tax and Business Incentive Program Ordinance BE IT RESOLVED: That the Tax and Business Incentive Program Ordinance approved by the East Haddam Town Meeting on June 30, 2010 be amended and restated in its

Tax and Business Incentive Program Ordinance BE IT RESOLVED: That the Tax and Business Incentive Program Ordinance approved by the East Haddam Town Meeting on June 30, 2010 be amended and restated in its