Examples of Quantitative Support Methods from Real World Appraisals

|

|

|

- Mildred Higgins

- 6 years ago

- Views:

Transcription

1 Examples of Quantitative Support Methods from Real World Appraisals Jeffrey A. Johnson, MAI Integra Realty Resources Minneapolis / St. Paul Tony Lesicka, MAI Central Bank 1

2 Overview of Presentation EXAMPLES OF TECHNIQUES AND METHODS EMPLOYED BY REAL WORLD APPRAISERS TO SOLVEUNIQUEAPPRAISALCHALLENGES USING QUANTITATIVE METHODS, TO SUPPORT THEIR OPINIONS; EXAMPLES CHOSEN ARE ALL FROM THE SALES COMPARISON APPROACH Review of Sales Comparison Approach SEARCH, FIND, & VERIFY RECENT SALES OF PROPERTIES SIMILAR ENOUGH TO THE SUBJECTPROPERTY TO BE CALLED AND ANALYZED AS COMPARABLES 2

3 Review of Sales Comparison Approach IF COMPARABLE IS AN EXACT TWIN OF SUBJECT STOP HERE; IF NOT, MAKE A COMPARATIVE ANALYSIS OF EACH COMPARABLE SALEPROPERTY AND SUBJECT PROPERTY Review of Sales Comparison Approach IF SUBJECT AND COMPARABLE DIFFER SIGNIFICANTLY IN A PARTICULAR FEATURE, THEN ONE MAKES AN ADJUSTMENT TO THE SALE PRICE OF THE COMPARABLE TO REFLECT THE FEATURES DIFFERING CONTRIBUTIONS TO VALUEFORTHECOMPANDTHESUBJECT 3

4 Review of Sales Comparison Approach INDICATION OF SUBJECT VALUE = SALE PRICE OF COMPARABLE CONTRIBUTING VALUE OF COMPARABLE FEATURE + CONTRIBUTING VALUE OF SUBJECT FEATURE [AN ADDITIVE MODEL] Review of Sales Comparison Approach INDICATION OF SUBJECT VALUE = ADJUSTMENT FACTOR X SALE PRICE OF COMPARABLE [A MULTIPLICATIVEMODEL] 4

5 Review of Sales Comparison Approach IN MULTIPLICATIVE MODEL THE ADJUSTMENT FACTOR IS THE RATIO OF THE VALUE CONTRIBUTION OF THE SUBJECT FEATURE DIVIDED BY THE VALUE CONTRIBUTION OF THE COMP S FEATURE; IN THE ADDITIVE MODEL, IT IS THE DIFFERENCE OF THE FEATURES VALUE CONTRIBUTION TO THE SUBJECT LESS THAT OF THE COMPARABLE, THAT DIFFERENCE IS ADDED TO THE SALE PRICE OF COMPARABLE Review of Sales Comparison Approach HOW DOES ONE COME UP WITH THESE ADJUSTMENT FACTORS? HOW DOES ONE SUPPORT THESE ADJUSTMENT FACTORS? THAT IS WHY WE ARE HERE! 5

6 #1: Office Finish Adjustment Industrial THE AMOUNT OF OFFICE FINISHED SPACE IN AN INDUSTRIAL BUILDING APPRAISAL IS A VARIABLE FOR WHICH WE COMMONLY SEE AN ADJUSTMENT MADE. SOME INDUSTRIAL BUILDINGS, SUCH AS A MANUFACTURING PLANT, MAY HAVE A RELATIVELY SMALL AMOUNT OF OFFICE SPACE. SOME INDUSTRIAL BUILDINGS, SUCH AS A FLEX OR OFFICE/SHOWROOM BUILDING, MAY EVEN HAVE A MAJORITY OF ITS SPACE FINISHED AS OFFICES. #1: Office Finish Adjustment Industrial WHEN A NEW INDUSTRIAL BUILDING IS BUILT IT GENERALLY COSTS MORE FOR A GREATER AMOUNT OF OFFICE FINISHED SPACE. THIS COST DIFFERENTIAL IS AN OFTEN USED RATIONAL AS THE BASIS FOR THE ADJUSTMENT THAT IS MADE AND THIS IS OUR FIRST EXAMPLE. 6

7 #1: Office Finish Adjustment Cost Basis #18R APPRAISAL PROBLEM: THE SUBJECT APPRAISAL ASSIGNMENT WAS TO ESTIMATE MARKET VALUE FOR AN EXISTING INDUSTRIAL OFFICE/WAREHOUSE PROPERTY. THE APPRAISAL WAS USED FOR REFINANCING PURPOSES. THE PROPERTY APPRAISED CONSISTED OF A 5.34 ACRE SITE IMPROVED WITH A 108,000 SQUARE FOOT OFFICE/WAREHOUSE INDUSTRIAL BUILDING THAT WAS BUILT IN 1968 WITH AN ADDITION IN #1: Office Finish Adjustment Cost Basis THE COMPARABLE SALES RANGED FROM 7.5% FINISHED OFFICE SPACE TO 40.0% FINISHED. THIS EXAMPLE SHOWS HOW ONE APPRAISER HAD ATTEMPTED TO QUANTIFY THIS OFFICE FINISH ADJUSTMENT BY RELATING HIS ESTIMATED ADJUSTMENT TO THE REPLACEMENT COSTS OF BUILDINGS WITH VARYING PERCENTAGES OF FINISH. 7

8 #1: Office Finish Adjustment Cost Basis THE DATE OF VALUATION WASMAY 23, THE APPRAISER USED SIX SALES IN HIS SALES COMPARISON ANALYSIS THAT RANGED FROM 50,372 SQUARE FEET TO 192,924 SQUARE FEET. A SIGNIFICANT DIFFERENCE BETWEEN THESE COMPARABLE SALES AND THE SUBJECT PROPERTY WERE THEIR VARYING LEVELS OF OFFICE FINISH. #1: Office Finish Adjustment Cost Basis This adjustment category reflects the differences in the percentage of finished office area between the subject and the comparables. Adjustments were applied to the comparables based on the differential of finished area between the comparables and the subject. Typically, office space rents for nearly double the rate of warehouse space. 8

9 #1: Office Finish Adjustment Cost Basis The subject property has a finished area of approximately 20% of net rentable building area. The comparables have finished area ranging from 7.5% to 40%. The table below summarizes the adjustments made to each sale based on the differences of finished area. 9

10 #1: Office Finish Adjustment Cost Basis THE APPRAISAL THEORY BEHIND THIS TECHNIQUE IS THAT MARKET VALUE IS RELATED TO REPLACEMENT COST. THAT IS, THE GREATER THE COST FOR BUILDINGS WITH GREATER PERCENTAGES OF OFFICE SPACE, THE GREATER THE MARKET VALUES OF THOSE BUILDINGS. IN THE ABOVE CHART THE APPRAISER FIRST ESTIMATES THE LIKELY COST PER SQUARE FOOT FOR THE SUBJECT BUILDING, GIVEN ITS 20% LEVEL OF OFFICE FINISH. #1: Office Finish Adjustment Cost Basis THE SAME REPLACEMENT COST IS ESTIMATED FOR SALE #1, FOR EXAMPLE, WHICH IS A BUILDING WITH ONLY 7.5% OFFICE FINISH. BY DIVIDING THE ESTIMATED REPLACEMENT COST OF THE SUBJECT BY THAT FOR SALE #1, WE SEE THAT SUCH A BUILDING AS THE SUBJECT WOULD HAVE A LIKELY COST OF ABOUT +9% GREATER; THUS, AN UPWARD ADJUSTMENT OF +9% IS REASONED TO ESTIMATE MARKET VALUE. 10

11 #1: Office Finish Adjustment Cost Basis THIS APPROACH IS VIEWED AS A GOOD TECHNIQUE OF ATTEMPTING TO MEASURE VALUE DIFFERENCES FOR PROPERTIES WITH VARYING DEGREES OF OFFICE FINISH. ONE SHOULD BE AWARE THAT THIS IS A LINEAR MODEL AND IT MAY NOT APPLY IF THERE IS A LARGE DEGREE OF DIFFERENCE IN THE SUBJECT AND COMPARABLE SALE BUILDINGS. THIS TECHNIQUE IS CONSIDERED TO BEST MEASURE SMALL DIFFERENCES. #1: Office Finish Adjustment Cost Basis IF, FOR EXAMPLE, A COMPARABLE SALE BUILDING HAD 80% OFFICE FINISH AND THE SUBJECT HAD 20%, ONE MIGHT WANT TO TEMPER THIS CALCULATED ADJUSTMENT FOR THE POSSIBLE FUNCTIONAL OBSOLESCENCE OF AN OVER-IMPROVEMENT OF TOO MUCH OFFICE FINISHED SPACE. FINALLY, SINCE THIS METHOD USES COST DIFFERENCES TO MEASURE MARKET VALUE DIFFERENCES, ONE MUST BE AWARE OF ANY FUNCTIONAL OR EXTERNAL OBSOLESCENCE ISSUES. 11

12 #1: Office Finish Adjustment Cost Basis FUNCTIONAL OBSOLESCENCE MIGHT BE THE OVER IMPROVEMENT ISSUE OF TOO MUCH OFFICE SPACE FOR WHICH THE MARKET WILL NOT REFLECT FULLY IN VALUE, AS DISCUSSED ABOVE. THE EXTERNAL OBSOLESCENCE MIGHT BE AN ECONOMICALLY DEPRESSED OR OVER BUILT MARKET FOR WHICH COST DOES NOT EQUAL VALUE. #2: Office Finish Adjustment Rent Basis #18S APPRAISAL PROBLEM: THE SUBJECT APPRAISAL ASSIGNMENT WAS TO ESTIMATE MARKET VALUE FOR AN EXISTING INDUSTRIAL OFFICE/WAREHOUSE PROPERTY. THE APPRAISAL WAS USED FOR REFINANCING PURPOSES. THE PROPERTY APPRAISED CONSISTED OF A 2.79 ACRE SITE IMPROVED WITH A 29,000 SQUARE FOOT OFFICE WAREHOUSE INDUSTRIAL BUILDING THAT WAS BUILT IN THE DATE OF VALUATION WAS MARCH 16,

13 #2: Office Finish Adjustment Rent Basis THE APPRAISER USED FIVE SALES IN HIS SALES COMPARISON ANALYSIS THAT RANGED FROM 24,408 SQUARE FEET TO 59,782 SQUARE FEET. A SIGNIFICANT DIFFERENCE BETWEEN THESE COMPARABLE SALES AND THE SUBJECT PROPERTY WERE THEIR VARYING LEVELS OF OFFICE FINISH. INDUSTRIAL BUILDINGS WILL GENERALLY SELL FOR GREATER PRICES, IF THEY HAVE A LARGER PERCENTAGE OF SPACE FINISHED FOR OFFICE USE. #2: Office Finish Adjustment Rent Basis THE COMPARABLE SALES RANGED FROM 7.0% FINISHED OFFICE SPACE TO 50.2% FINISHED. APPRAISERS OFTEN HAVE TO USE INDUSTRIAL SALES THAT HAVE DIFFERENT LEVELS OF OFFICE FINISH THAN THEIR SUBJECT PROPERTY AND THEN APPLY AN OFFICE FINISH ADJUSTMENT. THIS EXAMPLE SHOWS HOW ONE APPRAISER HAD ATTEMPTED TO QUANTIFY THIS OFFICE FINISH ADJUSTMENT BY RELATING HIS ESTIMATED ADJUSTMENT TO THE NET RENTAL RATES OF BUILDINGS WITH VARYING PERCENTAGES OF FINISH. 13

14 #2: Office Finish Adjustment Rent Basis This adjustment category reflects the differences in the percentage of finished office area between the subject and the comparables. Adjustments are applied to the comparables based on the differential of finished area between the comparables and the subject. Typically, in this market place office space rents for nearly double the rate of warehouse space. #2: Office Finish Adjustment Rent Basis The subject property has a finished area of approximately 16% of gross building area. The comparables have finished area ranging from 7% to 50%. The theory of this adjustment is that greater rental rates imply greater market value. In the table below, first the overall rental rate factor of the subject building is calculated to be 116% of the rental rate factor of just warehouse space. 14

15 #2: Office Finish Adjustment Rent Basis Then the same factor is calculated for each comparable sale property and the adjustment is calculated by dividing the subject factor by that of the comparable sale. The table below summarizes the adjustments made to each sale based on the differences of finished area. 15

16 #2: Office Finish Adjustment Rent Basis THE APPRAISER DOES NOT FULLY EXPLAIN HIS METHOD SO WE WILL PRESENT OUR EXPLANATION. IN THISPARTICULAR INDUSTRIAL MARKET IT IS COMMON FOR RENTAL RATES TO BE QUOTED ON PRICE PER SQUARE FOOT OF WAREHOUSE SPACE AND A DIFFERENT QUOTED RATE OF FINISHED OFFICE SPACE. THE RELATIONSHIP OF THESE TWO RENTAL RATES IS THAT USUALLY THE RATE FOR FINISHED OFFICE SPACE IN A BUILDING IS ABOUT DOUBLE THE WAREHOUSE RATE. THUS, THE APPRAISER REASONS THAT THE OVERALL SPACE RENTAL RATE FOR A BUILDING, LIKE THE SUBJECT, HAVING APPROXIMATELY 16% OF ITS AREA FINISHED AS OFFICE SPACE IS 1.16X #2: Office Finish Adjustment Rent Basis [CALCULATED AS: 0.16(2X) (X) = 1.16X, WHERE X REPRESENTS THE RENTAL RATE FOR WAREHOUSE SPACE]. SIMILARLY, THE OVERALL RENTAL RATE FOR A BUILDING LIKE SALE #1, WITH 35% SPACE FINISHED AS OFFICES, IS 1.35X. SO WHEN YOU CREATE AN ADJUSTMENT FACTOR BY DIVIDING THE RENTAL RATE OF THE SUBJECT (1.16X) BYTHERENTALRATEOF SALE #1 (1.35X) YOU GET A FACTOR OF 0.857, WHICH IS RESTATED AS A DOWNWARD ADJUSTMENT OF 14.3%. 16

17 #2: Office Finish Adjustment Rent Basis THIS METHOD WORKS BEST IF THERE IS NOT TOO MUCH DIFFERENCE IN LEVELS OF OFFICE FINISH. IF THERE IS A SUBSTANTIAL DIFFERENCE IN LEVELS OF OFFICE FINISH THE READER IS CAUTIONED THAT THIS CALCULATED ADJUSTMENT MIGHT NOT ACCURATELY REFLECT THE DIFFERENCE IN MARKET PRICES FOR THE SAME REASONING WE SET FORTH IN EXAMPLE #18R. #3: Unit Mix Adjustment Apartments A very common real estate property type is Apartments. Many apartment appraisals will have comparable sales that differ from the subject property in Unit Mix. How does one adjust for these differences? 17

18 #3: Unit Mix Adjustment Apartments Unit Mix is merely a categorical variable; not a measurement variable, neither discrete or continuous Is a 3 Bedroom unit worth 150% of a 2 Bedroom unit? Is it worth 300% of a 1 Bedroom unit? #3: Unit Mix Adjustment Apartments #18U APPRAISAL PROBLEM: THE SUBJECT APPRAISAL ASSIGNMENT WAS TO ESTIMATE THE CURRENT MARKET VALUE OF A 30 UNIT MARKET RATE APARTMENT PROPERTY. THE PROPERTY APPRAISED CONSISTED OF A 1.46 ACRE SITE IMPROVED WITH A 30 UNIT APARTMENT BUILDING BUILT IN IT WAS93% OCCUPIED AND CONSISTED OF 24 ONE BEDROOM UNITS AND 6 TWO BEDROOM UNITS. THE APPRAISAL WAS MADE FOR MORTGAGE FINANCING PURPOSES. THE DATE OF VALUATION WAS JUNE 23,

19 #3: Unit Mix Adjustment Apartments THE APPRAISER USED EIGHT SALES OF APARTMENT PROPERTIES IN HER SALES COMPARISON ANALYSIS. ONE DIFFERENCE BETWEEN THESE COMPARABLE SALES AND THE SUBJECT PROPERTY WAS THEIR UNIT MIX. THE SUBJECT PROPERTY HAD MOSTLY ONE BEDROOM UNITS; 80% (24 30 = 0.80) OF ITS TOTAL UNITS. THE COMPARABLE SALES VARIED IN THEIR UNIT MIX MAKEUPS. SALE #4 CONSISTED OF AN APARTMENT WHERE APPROXIMATELY 89% (40 45 = ) OF ITS UNITS WERE ONE BEDROOM UNITS. #3: Unit Mix Adjustment Apartments HOWEVER, SALE #7 CONSISTED OF AN APARTMENT WHERE 100% OF ITS UNITS WERE TWO BEDROOM UNITS. IT IS COMMON FOR APPRAISERS TO HAVE TO USE SALES OF APARTMENT PROPERTIES THAT VARY IN THEIR UNIT MIX FROM THE SUBJECT APARTMENT PROPERTY BEING APPRAISED. THIS EXAMPLE SHOWS HOW ONE APPRAISER HAD ATTEMPTED TO QUANTIFY THIS ADJUSTMENT FOR VARYING UNIT MIXES IN AN APPRAISAL OF AN APARTMENT PROPERTY. 19

20 #3: Unit Mix Adjustment Apartments This adjustment category accounts for the differences in unit mix of the subject and comparable properties recognizing that the more bedrooms a multifamily property contains, the higher potential rent it can generally achieve. The expectation is that a property with a greater percentage of two and three bedroom units should sell for a higher per unit price than a complex with a greater percentage of efficiencies and one bedroom units. We find in this market that efficiency units typically rent for about 85% of the rent that otherwise similar one bedroom units achieve. #3: Unit Mix Adjustment Apartments Two bedroom rents are generally about +25% higher than one bedroom units, and three bedroom rental rates are approximately 60% higher than one bedroom units. These observed rental differences are summarized as follows: Efficiency Units: One Bedroom Units: Two Bedroom Units: Three Bedroom Units: 85% of a one bedroom 100% of a one bedroom 125% of a one bedroom 160% of a one bedroom 20

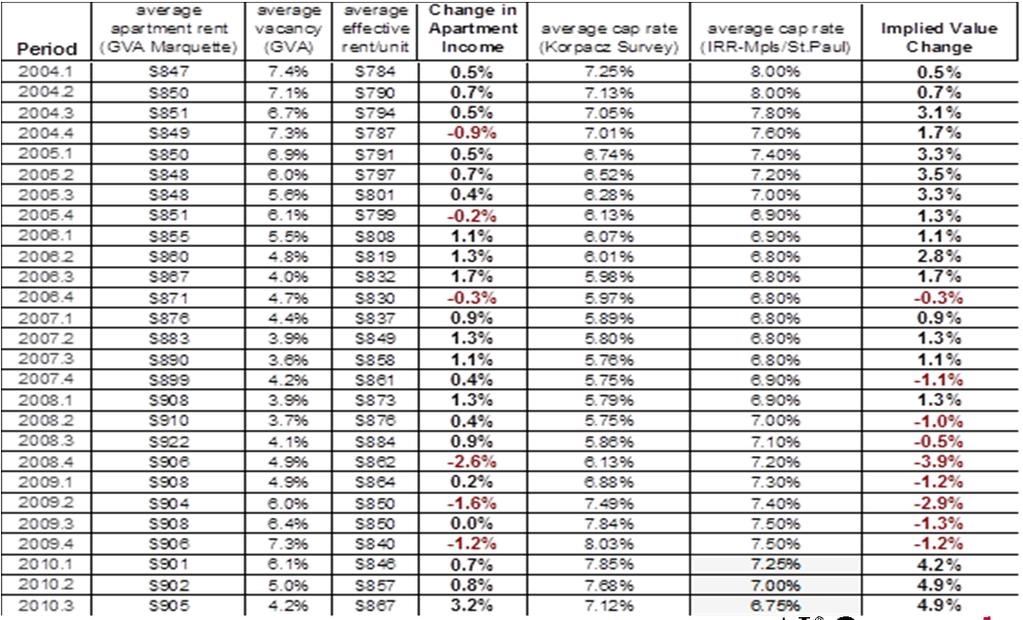

21 #3: Unit Mix Adjustment Apartments To initiate the adjustment process, the subject and comparable sales are converted to a one bedroomequivalency utilizing the preceding scale. To make this calculation, the total number of each unit type is multiplied by its corresponding rent percentage differential. Each of these figures is then added together and divided by the total number of dwelling units at the property. The result is a onebedroom equivalent factor for the subject and each comparable property. #3: Unit Mix Adjustment Apartments For example, the subject property, which consists of 24 one bedroom units and 6 two bedroom units, can be expressed on this one bedroom rentequivalent scale as being equivalent to an apartment with average units having rents of 1.05 times that of a typical one bedroom unit {e.g. [(0 x 0.85) + (24 x 1.00) + (6 x 1.25) + (0 x 1.60)] 30 = 1.05}. Then the relationship between the subject and each comparable one bedroom equivalency factor, if any, is the final adjustment factor, expressed as a percentage. 21

22 #3: Unit Mix Adjustment Apartments AUTHORS REVIEW COMMENTS: IN THIS APPRAISAL THAT WAS MADE FOR MORTGAGE FINANCING PURPOSES, THE APPRAISER USED A RENT BASED METHOD TO ASSIST IN HER EVALUATION OF HOW THE DIFFERING UNIT MIXES IMPACTED THE MARKET VALUE OF THIS PROPERTY. WE FINDTHATMOST ADJUSTMENTS THAT WE SEE FOR APARTMENT UNIT MIX ARE SUPPORTED ON A DIFFERENCE IN AVERAGE UNIT SQUARE FOOTAGES. WE OBSERVE THAT THIS METHOD IS BASED ON AN ECONOMIC SCALE FOR THE ADJUSTMENT. 22

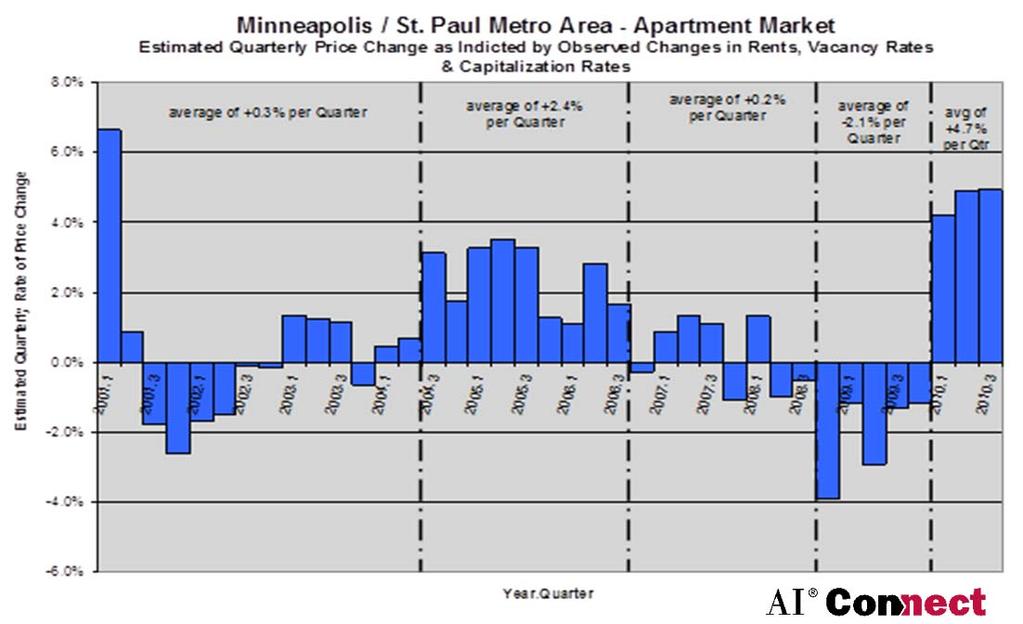

23 #4: Time/Market Conditions Adjustment Apartment Property #18M APPRAISAL PROBLEM: THE SUBJECT APPRAISAL ASSIGNMENT WAS TO ESTIMATE THE CURRENT AS IS MARKET VALUE, AND THE HYPOTHETICAL AS COMPLETED AND HYPOTHETICAL AS COMPLETED AND STABILIZED MARKET VALUES AS OF A CURRENT DATE (THE SAME AS THE EFFECTIVE DATE FOR THE AS IS VALUE) FOR AN EXISTING MARKET RATE APARTMENT PROPERTY LOCATED IN THE CITY OF MINNEAPOLIS. THE APPRAISAL WAS USED FOR REFINANCING PURPOSES. THE PROPERTY APPRAISED CONSISTED OF A 4.5 ACRE SITE IMPROVED WITH A 100 UNIT APARTMENT PROPERTY #4: Time/Market Conditions Adjustment Apartment Property THAT WAS BUILT IN THIS PROPERTY WAS IN THE MIDDLE OF A MAJOR REMODELING PROJECT WITH 52 UNITS COMPLETED AND 20 MORE UNITS IN THE PROCESS OF BEING REMODELED WITH THE REMAINDER OF THE 28 UNITS TO BE COMPLETED WITHIN SIX MONTHS. THE DATE OF VALUATION WAS DECEMBER 1, AT THAT POINT IN TIME THE LOCAL APARTMENT MARKET WAS THINLY TRADED. THERE WERE VERY FEW ARM S LENGTHSALES AVAILABLE FOR APPRAISERS TO USE IN THEIR SALES COMPARISON ANALYSIS. 23

24 #4: Time/Market Conditions Adjustment Apartment Property APPRAISERS WERE HAVING TO USE SOME OLDER SALES AND THEN APPLY A MARKET CONDITIONS ADJUSTMENT. THIS EXAMPLE SHOWS HOW ONE APPRAISER HAD ATTEMPTED TO QUANTIFY THIS CHANGING MARKET CONDITIONS ADJUSTMENT. There is no index for the local real estate market to show pricing movement through time for this particular multi family property sub market. However, since the local real estate market has become more dependent on the national financing market and also as many investors are seeking to acquire investments in a larger geographic area, many even on a national basis, we have reviewed a national property pricing index and present information on it in this section. 24

Center for Real Estate industry partner Real Capital Analytics, Inc. (RCA).")

25 The Moodys/REAL Commercial Property Index (CPPI) is a periodic same property round trip investment price change index of the United States commercial investment property market based on data from the Massachusetts Institute of Technology (MIT) Center for Real Estate industry partner Real Capital Analytics, Inc. (RCA). 25

26 An alternative way to analyze this data is to calculate the change from quarter to quarter. By dividing the current quarterly index by the prior quarterly index we obtain an indication of the quarterly rate of pricing change. Since many real estate investment market participants usually quote pricing rates of change on an annual percentage basis, 26

27 we find this quarterly rate of change analysis to be helpful and present the following graph showing the indicated quarterly rates of change through time for this national apartment market data. 27

28 To analyze our local apartment market for pricing movement we have assembled information on how average apartment rents have changed over time and also how average apartment vacancy rates have changed over time. The value of apartment properties is a function of not only the economic performance of the properties but also the capitalization rate that buyers are using to acquire properties. This chart also shows the average capitalization rate that is found in the Korpacz Real Estate Investor Survey, which is a quarterly publication of Price Waterhouse Coopers. We have used this information along with our estimate of typical expenses for metro area apartments to calculate an implied value change from quarter to quarter. 28

29 29

30 Additionally, we have tested the above theoretical pricing movement method by looking to the local apartment market and analyzing relevant recent apartment sales. To have groupings of more similar apartment properties we have looked only at sales of apartments of greater than 20 units and built after 1960 and located within the 11 county metro area. We have taken this sales data from a professional appraiser verified database of sale transactions. We find the following statistical data to also be of help in estimating rates of pricing change through time for the changing market conditions within our local apartment market. We have used the same time intervals identified in the above theoretical method and have grouped the apartment sales from our database of professional appraiser verified sales into groups based on the timing of the date each sale was closed. 30

31 The sales analyzed in this appraisal took place from May 2008 to March Based on our research and experience we conclude that for this evaluation of the subject property and for the comparable sales selected for this comparative analysis that the local apartment market was generally strengthening with prices appreciating during the period from the third quarter of 2004 through the third quarter of 2006 at a rate of about +10% per year; we will use a rate of +2.5% per quarter for that period. 31

32 We conclude that prices were generally stable during the period from the fourth quarter of 2006 through the third quarter of 2008 and we will use a rate of +0.0% per quarter for that period. However, beginning in the fourth quarter of 2008 through the fourth quarter of 2009 we are of the opinion that prices have been depreciating and we will use a rate of decline of 8% per year, or about 2.0% per quarter. We are of the opinion that beginning with the first quarter of 2010 through the current period that prices have stabilized and remained level at these reduced lower levels and we will use a rate of +0.0% per quarter for this most recent period. These conclusions of market condition rates of pricing changes will be applied to each of our comparable sales to express their transaction prices as of our date of evaluation. 32

33 Presenters Concluding Remarks Thanks for attending We are collecting examples like those shown in this presentation; if you have any to share please contact us at Questions and Comments 33

How to Read a Real Estate Appraisal Report

How to Read a Real Estate Appraisal Report Much of the private, corporate and public wealth of the world consists of real estate. The magnitude of this fundamental resource creates a need for informed

How to Read a Real Estate Appraisal Report Much of the private, corporate and public wealth of the world consists of real estate. The magnitude of this fundamental resource creates a need for informed

Typical Valuation Approaches and How to Deal With Them

Typical Valuation Approaches and How to Deal With Them January, 2018 Anthony F. DellaPelle, Esq., CRE Shareholder, McKirdy, Riskin, Olson & DellaPelle, P.C. Morristown, New Jersey Christian F. Torgrimson,

Typical Valuation Approaches and How to Deal With Them January, 2018 Anthony F. DellaPelle, Esq., CRE Shareholder, McKirdy, Riskin, Olson & DellaPelle, P.C. Morristown, New Jersey Christian F. Torgrimson,

GENERAL ASSESSMENT DEFINITIONS

21st Century Appraisals, Inc. GENERAL ASSESSMENT DEFINITIONS Ad Valorem tax. A tax levied in proportion to the value of the thing(s) being taxed. Exclusive of exemptions, use-value assessment laws, and

21st Century Appraisals, Inc. GENERAL ASSESSMENT DEFINITIONS Ad Valorem tax. A tax levied in proportion to the value of the thing(s) being taxed. Exclusive of exemptions, use-value assessment laws, and

Basic Appraisal Procedures

Hondros Learning Basic Appraisal Procedures Timed Outline Topic Area Reference(s) Learning Objectives The student will be able to identify and/or apply: Teaching Method Time Segment (Minutes) Day 1 Chapter

Hondros Learning Basic Appraisal Procedures Timed Outline Topic Area Reference(s) Learning Objectives The student will be able to identify and/or apply: Teaching Method Time Segment (Minutes) Day 1 Chapter

Published in Spring 1986 Issue The Real Estate Appraiser & Analyst Society of Real Estate Appraisers 1

(1) Published in Spring 1986 Issue The Real Estate Appraiser & Analyst Society of Real Estate Appraisers 1 Alternative Valuation Methods for Leasehold Properties By Tony Sevelka, AACI, SREA, MAI, CRE Introduction

(1) Published in Spring 1986 Issue The Real Estate Appraiser & Analyst Society of Real Estate Appraisers 1 Alternative Valuation Methods for Leasehold Properties By Tony Sevelka, AACI, SREA, MAI, CRE Introduction

The Cost of Property, Plant, Equipment

1 The Cost of Property, Plant, Equipment The cost of property, plant, and equipment includes the purchase price of the asset and all expenditures necessary to prepare the asset for its intended use. Land.

1 The Cost of Property, Plant, Equipment The cost of property, plant, and equipment includes the purchase price of the asset and all expenditures necessary to prepare the asset for its intended use. Land.

Index of Examples. Chapter 1 Letter of Transmittal Chapter 2 General Assumptions and Limiting Conditions... 19

Index of Examples Chapter 1 Letter of Transmittal... 1 Example 1A Detailed Letter of Transmittal... 2 Example 1B Detailed Letter of Transmittal with Risk Factors and Assumptions... 6 Example 1C Brief Letter

Index of Examples Chapter 1 Letter of Transmittal... 1 Example 1A Detailed Letter of Transmittal... 2 Example 1B Detailed Letter of Transmittal with Risk Factors and Assumptions... 6 Example 1C Brief Letter

Tangible Personal Property Summation Valuation Procedures

Property Tax Valuation Insights Tangible Personal Property Summation Valuation Procedures Robert F. Reilly, CPA For ad valorem property taxation purposes, industrial and commercial taxpayer tangible personal

Property Tax Valuation Insights Tangible Personal Property Summation Valuation Procedures Robert F. Reilly, CPA For ad valorem property taxation purposes, industrial and commercial taxpayer tangible personal

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence OVERVIEW OF RESIDENTIAL APPRAISAL PROCESS And Cost Valuation Report Introduction The

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence OVERVIEW OF RESIDENTIAL APPRAISAL PROCESS And Cost Valuation Report Introduction The

BUSI 330 Suggested Answers to Review and Discussion Questions: Lesson 10

BUSI 330 Suggested Answers to Review and Discussion Questions: Lesson 10 1. The client should give you a copy of their income and expense statements for the last 3 years showing their rental income by

BUSI 330 Suggested Answers to Review and Discussion Questions: Lesson 10 1. The client should give you a copy of their income and expense statements for the last 3 years showing their rental income by

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence OVERVIEW OF RESIDENTIAL APPRAISAL PROCESS And Cost Valuation Report Introduction The

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence OVERVIEW OF RESIDENTIAL APPRAISAL PROCESS And Cost Valuation Report Introduction The

2. The, and Act, also known as FIRREA, requires that states set standards for all appraisers.

CHAPTER 4 SHORT-ANSWER QUESTIONS 1. An appraisal is an or of value. 2. The, and Act, also known as FIRREA, requires that states set standards for all appraisers. 3. Value in real estate is the "present

CHAPTER 4 SHORT-ANSWER QUESTIONS 1. An appraisal is an or of value. 2. The, and Act, also known as FIRREA, requires that states set standards for all appraisers. 3. Value in real estate is the "present

Risk Management Insights

Risk Management Insights Appraisal Review Part II: Income Capitalization Approach George Mann, Managing Director and Chief Appraiser, Collateral Evaluation Services, Inc.and Nikki Griffith, MAI, CCIM,

Risk Management Insights Appraisal Review Part II: Income Capitalization Approach George Mann, Managing Director and Chief Appraiser, Collateral Evaluation Services, Inc.and Nikki Griffith, MAI, CCIM,

Math Relating to Real Property Appraisals

1. Sales Comparison Approach Math Relating to Real Property Appraisals A. If the comparable property is superior in a feature, you subtract value from the comparable. Example: Comp #l has a 1-car garage

1. Sales Comparison Approach Math Relating to Real Property Appraisals A. If the comparable property is superior in a feature, you subtract value from the comparable. Example: Comp #l has a 1-car garage

absorption rate ad valorem appraisal broker price opinion capital gain

absorption rate The estimated time required to sell or lease property within a designated area at its fair market value. ad valorem Real estate taxes imposed on property based on its assessed value. appraisal

absorption rate The estimated time required to sell or lease property within a designated area at its fair market value. ad valorem Real estate taxes imposed on property based on its assessed value. appraisal

Following is an example of an income and expense benchmark worksheet:

After analyzing income and expense information and establishing typical rents and expenses, apply benchmarks and base standards to the reappraisal area. Following is an example of an income and expense

After analyzing income and expense information and establishing typical rents and expenses, apply benchmarks and base standards to the reappraisal area. Following is an example of an income and expense

procedures Basic Appraisal F i n a l Examination #2 2 nd edition

F i n a l Examination #2 A n s w e r Key Page 82 1. When determining effective gross income from potential gross income, an appraiser considers a. debt service. b. depreciation. c. fixed expenses. d. vacancy

F i n a l Examination #2 A n s w e r Key Page 82 1. When determining effective gross income from potential gross income, an appraiser considers a. debt service. b. depreciation. c. fixed expenses. d. vacancy

California Real Estate License Exam Prep: Unlocking the DRE Salesperson and Broker Exam 4th Edition

California Real Estate License Exam Prep: Unlocking the DRE Salesperson and Broker Exam 4th Edition ANSWER SHEET INSTRUCTIONS: The exam consists of multiple choice questions. Multiple choice questions

California Real Estate License Exam Prep: Unlocking the DRE Salesperson and Broker Exam 4th Edition ANSWER SHEET INSTRUCTIONS: The exam consists of multiple choice questions. Multiple choice questions

Cycle Monitor Real Estate Market Cycles Third Quarter 2017 Analysis

Cycle Monitor Real Estate Market Cycles Third Quarter 2017 Analysis Real Estate Physical Market Cycle Analysis of Five Property Types in 54 Metropolitan Statistical Areas (MSAs). Income-producing real

Cycle Monitor Real Estate Market Cycles Third Quarter 2017 Analysis Real Estate Physical Market Cycle Analysis of Five Property Types in 54 Metropolitan Statistical Areas (MSAs). Income-producing real

Real Estate Appraisal

Market Value Chapter 17 Real Estate Appraisal This presentation includes materials from Ling and Archer, 4 th edition, Real Estate Principles The highest price a property will bring if: Payment is made

Market Value Chapter 17 Real Estate Appraisal This presentation includes materials from Ling and Archer, 4 th edition, Real Estate Principles The highest price a property will bring if: Payment is made

Residential Property Value Procedures: How to calculate a value

2500 Handley Ederville Road Fort Worth, TX 76118 (817) 284 3925 res@tad.org Residential Property Value Procedures: How to calculate a value Mass Appraisal: The Residential Department is responsible for

2500 Handley Ederville Road Fort Worth, TX 76118 (817) 284 3925 res@tad.org Residential Property Value Procedures: How to calculate a value Mass Appraisal: The Residential Department is responsible for

INDUSTRIAL MARKET REPORT. San Antonio. 4th Quarter Q4 Market Trends 2016 by Xceligent, Inc. All Rights Reserved

INDUSTRIAL MARKET REPORT San Antonio 4th Quarter 2015 Table of Contents/ Methodology of Tracked Set Xceligent is a leading provider of verified commercial real estate information which assists real estate

INDUSTRIAL MARKET REPORT San Antonio 4th Quarter 2015 Table of Contents/ Methodology of Tracked Set Xceligent is a leading provider of verified commercial real estate information which assists real estate

General Market Analysis and Highest & Best Use. Learning Objectives

General Market Analysis and Highest & Best Use Learning Objectives Module & Title Module 1 Real Estate Markets and Analysis Module 2 Types and Levels of Market Analysis Module 3 The Six-Step Process and

General Market Analysis and Highest & Best Use Learning Objectives Module & Title Module 1 Real Estate Markets and Analysis Module 2 Types and Levels of Market Analysis Module 3 The Six-Step Process and

VALUATION CONSIDERATIONS AND METHODS FOR A PATENT VALUATION ANALYSIS

Insights Autumn 2009 54 Intellectual Property Valuation Insights VALUATION CONSIDERATIONS AND METHODS FOR A PATENT VALUATION ANALYSIS C. Ryan Stewart In recent years, the value of patents and other intellectual

Insights Autumn 2009 54 Intellectual Property Valuation Insights VALUATION CONSIDERATIONS AND METHODS FOR A PATENT VALUATION ANALYSIS C. Ryan Stewart In recent years, the value of patents and other intellectual

Minneapolis St. Paul Residential Real Estate Index

University of St. Thomas Minneapolis St. Paul Residential Real Estate Index Welcome to the latest edition of the UST Minneapolis St. Paul Residential Real Estate Index. The University of St Thomas Residential

University of St. Thomas Minneapolis St. Paul Residential Real Estate Index Welcome to the latest edition of the UST Minneapolis St. Paul Residential Real Estate Index. The University of St Thomas Residential

A Demonstration Appraisal Report. Of a. Located at. Date of Appraisal. Prepared for. Prepared by

A Demonstration Appraisal Report Of a Located at Date of Appraisal Prepared for Prepared by International Association of Assessing Officers Professional Designation Subcommittee 314 West 10 th Street Kansas

A Demonstration Appraisal Report Of a Located at Date of Appraisal Prepared for Prepared by International Association of Assessing Officers Professional Designation Subcommittee 314 West 10 th Street Kansas

Minneapolis St. Paul Residential Real Estate Index

University of St. Thomas Minneapolis St. Paul Residential Real Estate Index Welcome to the latest edition of the UST Minneapolis St. Paul Residential Real Estate Index. The University of St Thomas Residential

University of St. Thomas Minneapolis St. Paul Residential Real Estate Index Welcome to the latest edition of the UST Minneapolis St. Paul Residential Real Estate Index. The University of St Thomas Residential

The Honorable Larry Hogan And The General Assembly of Maryland

2015 Ratio Report The Honorable Larry Hogan And The General Assembly of Maryland As required by Section 2-202 of the Tax-Property Article of the Annotated Code of Maryland, I am pleased to submit the Department

2015 Ratio Report The Honorable Larry Hogan And The General Assembly of Maryland As required by Section 2-202 of the Tax-Property Article of the Annotated Code of Maryland, I am pleased to submit the Department

April 12, The Honorable Martin O Malley And The General Assembly of Maryland

April 12, 2011 The Honorable Martin O Malley And The General Assembly of Maryland As required by Section 2-202 of the Tax-Property Article of the Annotated Code of Maryland, I am pleased to submit the

April 12, 2011 The Honorable Martin O Malley And The General Assembly of Maryland As required by Section 2-202 of the Tax-Property Article of the Annotated Code of Maryland, I am pleased to submit the

Economic Impact of Commercial Multi-Unit Residential Property Transactions in Toronto, Calgary and Vancouver,

Economic Impact of Commercial Multi-Unit Residential Property Transactions in Toronto, Calgary and Vancouver, 2006-2008 SEPTEMBER 2009 Economic Impact of Commercial Multi-Unit Residential Property Transactions

Economic Impact of Commercial Multi-Unit Residential Property Transactions in Toronto, Calgary and Vancouver, 2006-2008 SEPTEMBER 2009 Economic Impact of Commercial Multi-Unit Residential Property Transactions

The Impact of Using. Market-Value to Replacement-Cost. Ratios on Housing Insurance in Toledo Neighborhoods

The Impact of Using Market-Value to Replacement-Cost Ratios on Housing Insurance in Toledo Neighborhoods February 12, 1999 Urban Affairs Center The University of Toledo Toledo, OH 43606-3390 Prepared by

The Impact of Using Market-Value to Replacement-Cost Ratios on Housing Insurance in Toledo Neighborhoods February 12, 1999 Urban Affairs Center The University of Toledo Toledo, OH 43606-3390 Prepared by

Volume 35, Issue 1. Hedonic prices, capitalization rate and real estate appraisal

Volume 35, Issue 1 Hedonic prices, capitalization rate and real estate appraisal Gaetano Lisi epartment of Economics and Law, University of assino and Southern Lazio Abstract Studies on real estate economics

Volume 35, Issue 1 Hedonic prices, capitalization rate and real estate appraisal Gaetano Lisi epartment of Economics and Law, University of assino and Southern Lazio Abstract Studies on real estate economics

2011 ASSESSMENT RATIO REPORT

2011 Ratio Report SECTION I OVERVIEW 2011 ASSESSMENT RATIO REPORT The Department of Assessments and Taxation appraises real property for the purposes of property taxation. Properties are valued using

2011 Ratio Report SECTION I OVERVIEW 2011 ASSESSMENT RATIO REPORT The Department of Assessments and Taxation appraises real property for the purposes of property taxation. Properties are valued using

Industrial and Commercial Real Estate Appraisal Procedures

Property Valuation Thought Leadership Industrial and Commercial Real Estate Appraisal Procedures John C. Ramirez The application of the asset-based approach to business valuation often involves the appraisal

Property Valuation Thought Leadership Industrial and Commercial Real Estate Appraisal Procedures John C. Ramirez The application of the asset-based approach to business valuation often involves the appraisal

concepts and techniques

concepts and techniques S a m p l e Timed Outline Topic Area DAY 1 Reference(s) Learning Objective The student will learn Teaching Method Time Segment (Minutes) Chapter 1: Introduction to Sales Comparison

concepts and techniques S a m p l e Timed Outline Topic Area DAY 1 Reference(s) Learning Objective The student will learn Teaching Method Time Segment (Minutes) Chapter 1: Introduction to Sales Comparison

METHODOLOGY GUIDE VALUING MOTELS IN ONTARIO. Valuation Date: January 1, 2016

METHODOLOGY GUIDE VALUING MOTELS IN ONTARIO Valuation Date: January 1, 2016 AUGUST 2016 August 22, 2016 The Municipal Property Assessment Corporation (MPAC) is responsible for accurately assessing and

METHODOLOGY GUIDE VALUING MOTELS IN ONTARIO Valuation Date: January 1, 2016 AUGUST 2016 August 22, 2016 The Municipal Property Assessment Corporation (MPAC) is responsible for accurately assessing and

Assessment Principles. Three Accepted Approaches to Value Cost Approach Sales Comparison Approach Property Income (Rental) Approach

Approach") Assessment Principles Three Accepted Approaches to Value Cost Approach Sales Comparison Approach Property Income (Rental) Approach Overview of the Cost Approach Land Valuation Average selling prices for

Assessment Principles Three Accepted Approaches to Value Cost Approach Sales Comparison Approach Property Income (Rental) Approach Overview of the Cost Approach Land Valuation Average selling prices for

Grain Elevator. Market Value Assessment in Saskatchewan Handbook. Grain Elevator Valuation Guide

Market Value Assessment in Saskatchewan Handbook Grain Elevator Saskatchewan Assessment Management Agency 2012 This document is a derivative work based upon a handbook entitled the "Market Value and Mass

Market Value Assessment in Saskatchewan Handbook Grain Elevator Saskatchewan Assessment Management Agency 2012 This document is a derivative work based upon a handbook entitled the "Market Value and Mass

ASSESSMENT METHODOLOGY

2018 ASSESSMENT METHODOLOGY COST APPROACH A summary of the methods used by the City of Edmonton in determining the value of residential and non-residential properties valued using the cost approach in

2018 ASSESSMENT METHODOLOGY COST APPROACH A summary of the methods used by the City of Edmonton in determining the value of residential and non-residential properties valued using the cost approach in

Appraiser Qualifications Board

Appraiser Qualifications Board Course Analysis Course Name Provider Date of Approval Course Expiration Date This detailed breakdown of the subject content of this course is provided by the AQB as part

Appraiser Qualifications Board Course Analysis Course Name Provider Date of Approval Course Expiration Date This detailed breakdown of the subject content of this course is provided by the AQB as part

Edmonton Composite Assessment Review Board

Edmonton Composite Assessment Review Board Citation: CVG v The City of Edmonton, 2013 ECARB 01878 Assessment Roll Number: 10002533 Municipal Address: 10904 102 A venue NW Assessment Year: 2013 Assessment

Edmonton Composite Assessment Review Board Citation: CVG v The City of Edmonton, 2013 ECARB 01878 Assessment Roll Number: 10002533 Municipal Address: 10904 102 A venue NW Assessment Year: 2013 Assessment

NEW LONDON, NEW HAMPSHIRE 375 MAIN STREET NEW LONDON, NH

TOWN OF NEW LONDON, NEW HAMPSHIRE 375 MAIN STREET NEW LONDON, NH 03257 WWW.NL-NH.COM READING YOUR PROPERTY RECORD CARD Vision Appraisal Technology 1.) Property Location: The actual physical location of

TOWN OF NEW LONDON, NEW HAMPSHIRE 375 MAIN STREET NEW LONDON, NH 03257 WWW.NL-NH.COM READING YOUR PROPERTY RECORD CARD Vision Appraisal Technology 1.) Property Location: The actual physical location of

Economic and monetary developments

Box 4 House prices and the rent component of the HICP in the euro area According to the residential property price indicator, euro area house prices decreased by.% year on year in the first quarter of

Box 4 House prices and the rent component of the HICP in the euro area According to the residential property price indicator, euro area house prices decreased by.% year on year in the first quarter of

Special Report. Australia s Cheapest Suburbs with the Greatest Potential for Capital Growth. For more reports head to

Demand Supply Ratio Market Report Special Report Australia s Cheapest Suburbs with the Greatest Potential for Capital Growth Market: Australia Created by: hotspotcentral.com.au Contact: t: 1300 200 340

Demand Supply Ratio Market Report Special Report Australia s Cheapest Suburbs with the Greatest Potential for Capital Growth Market: Australia Created by: hotspotcentral.com.au Contact: t: 1300 200 340

Proving Depreciation

Institute for Professionals in Taxation 40 th Annual Property Tax Symposium Tucson, Arizona Proving Depreciation Presentation Concepts and Content: Kathy G. Spletter, ASA Stancil & Co. Irving, Texas kathy.spletter@stancilco.com

Institute for Professionals in Taxation 40 th Annual Property Tax Symposium Tucson, Arizona Proving Depreciation Presentation Concepts and Content: Kathy G. Spletter, ASA Stancil & Co. Irving, Texas kathy.spletter@stancilco.com

Cook County Assessor s Office: 2019 North Triad Assessment. Norwood Park Residential Assessment Narrative March 11, 2019

Cook County Assessor s Office: 2019 North Triad Assessment Norwood Park Residential Assessment Narrative March 11, 2019 1 Norwood Park Residential Properties Executive Summary This is the current CCAO

Cook County Assessor s Office: 2019 North Triad Assessment Norwood Park Residential Assessment Narrative March 11, 2019 1 Norwood Park Residential Properties Executive Summary This is the current CCAO

Chapter 35. The Appraiser's Sales Comparison Approach INTRODUCTION

Chapter 35 The Appraiser's Sales Comparison Approach INTRODUCTION The most commonly used appraisal technique is the sales comparison approach. The fundamental concept underlying this approach is that market

Chapter 35 The Appraiser's Sales Comparison Approach INTRODUCTION The most commonly used appraisal technique is the sales comparison approach. The fundamental concept underlying this approach is that market

ECONOMIC CURRENTS. Vol. 4, Issue 3. THE Introduction SOUTH FLORIDA ECONOMIC QUARTERLY

ECONOMIC CURRENTS THE Introduction SOUTH FLORIDA ECONOMIC QUARTERLY Vol. 4, Issue 3 Economic Currents provides an overview of the South Florida regional economy. The report presents current employment,

ECONOMIC CURRENTS THE Introduction SOUTH FLORIDA ECONOMIC QUARTERLY Vol. 4, Issue 3 Economic Currents provides an overview of the South Florida regional economy. The report presents current employment,

A Demonstration Appraisal Report. Of a. Located at. Date of Appraisal. Prepared for. Prepared by

A Demonstration Appraisal Report Of a Located at Date of Appraisal Prepared for Prepared by International Association of Assessing Officers Professional Designation Subcommittee 314 W. 10 th Street Kansas

A Demonstration Appraisal Report Of a Located at Date of Appraisal Prepared for Prepared by International Association of Assessing Officers Professional Designation Subcommittee 314 W. 10 th Street Kansas

Special Purpose Properties. Special Valuation Considerations

Special Purpose Properties Special Valuation Considerations 2017 Case Study in Ottawa: New Automobile Dealership Many brand-specific specialties Cost: $4,000,000 (including land and a developer fee) Sales

Special Purpose Properties Special Valuation Considerations 2017 Case Study in Ottawa: New Automobile Dealership Many brand-specific specialties Cost: $4,000,000 (including land and a developer fee) Sales

Minneapolis St. Paul Residential Real Estate Index

University of St. Thomas Minneapolis St. Paul Residential Real Estate Index Welcome to the latest edition of the UST Minneapolis St. Paul Residential Real Estate Index. The University of St Thomas Residential

University of St. Thomas Minneapolis St. Paul Residential Real Estate Index Welcome to the latest edition of the UST Minneapolis St. Paul Residential Real Estate Index. The University of St Thomas Residential

CALGARY ASSESSMENT REVIEW BOARD DECISION WITH REASONS

.. Psg,e 1 of9 CARB 1812/2011-P CALGARY ASSESSMENT REVIEW BOARD DECISION WITH REASONS In the matter of the complaint against the property assessment as provided by the Municipal Government Act, Chapter

.. Psg,e 1 of9 CARB 1812/2011-P CALGARY ASSESSMENT REVIEW BOARD DECISION WITH REASONS In the matter of the complaint against the property assessment as provided by the Municipal Government Act, Chapter

Initial sales ratio to determine the current overall level of value. Number of sales vacant and improved, by neighborhood.

Introduction The International Association of Assessing Officers (IAAO) defines the market approach: In its broadest use, it might denote any valuation procedure intended to produce an estimate of market

Introduction The International Association of Assessing Officers (IAAO) defines the market approach: In its broadest use, it might denote any valuation procedure intended to produce an estimate of market

WALLER COUNTY APPRAISAL DISTRICT MASS APPRAISAL REPORT APPRAISAL YEAR 2018

WALLER COUNTY APPRAISAL DISTRICT MASS APPRAISAL REPORT APPRAISAL YEAR 2018 ADDENDUM TO WCAD REAPPRAISAL PLAN FOR 2017 AND 2018 WALLER COUNTY APPRAISAL DISTRICT Uniform Standards of Professional Appraisal

WALLER COUNTY APPRAISAL DISTRICT MASS APPRAISAL REPORT APPRAISAL YEAR 2018 ADDENDUM TO WCAD REAPPRAISAL PLAN FOR 2017 AND 2018 WALLER COUNTY APPRAISAL DISTRICT Uniform Standards of Professional Appraisal

Contract-Related Intangible

Income Tax Insights Valuation of Contract-Related Intangible Assets Robert F. Reilly, CPA The valuation of contract-related intangible assets is often an issue in matters related to income tax, gift tax,

Income Tax Insights Valuation of Contract-Related Intangible Assets Robert F. Reilly, CPA The valuation of contract-related intangible assets is often an issue in matters related to income tax, gift tax,

Guide to Appraisal Reports

Guide to Appraisal Reports What is an appraisal? An appraisal is an independent valuation of real property prepared by a qualified Appraiser and fully documented in a report. Based on a series of appraisal

Guide to Appraisal Reports What is an appraisal? An appraisal is an independent valuation of real property prepared by a qualified Appraiser and fully documented in a report. Based on a series of appraisal

RESIDENTIAL MARKET ANALYSIS

RESIDENTIAL MARKET ANALYSIS CLANCY TERRY RMLS Student Fellow Master of Real Estate Development Candidate Oregon and national housing markets both demonstrated shifting trends in the first quarter of 2015

RESIDENTIAL MARKET ANALYSIS CLANCY TERRY RMLS Student Fellow Master of Real Estate Development Candidate Oregon and national housing markets both demonstrated shifting trends in the first quarter of 2015

Chapter 12 Changes Since This is just a brief and cursory comparison. More analysis will be done at a later date.

Chapter 12 Changes Since 1986 This approach to Fiscal Analysis was first done in 1986 for the City of Anoka. It was the first of its kind and was recognized by the National Science Foundation (NSF). Geographic

Chapter 12 Changes Since 1986 This approach to Fiscal Analysis was first done in 1986 for the City of Anoka. It was the first of its kind and was recognized by the National Science Foundation (NSF). Geographic

Kathy Coon, SRA Appraisal Review: CSI Style ( )

") Appraisal Review: CSI Style Southern California Chapter Appraisal Institute July 16, 2009 Kathy Coon, SRA Chief Appraiser/Director-Appraisal Appraisal Quality Control FNC, Inc. www.fncinc.com com When

Appraisal Review: CSI Style Southern California Chapter Appraisal Institute July 16, 2009 Kathy Coon, SRA Chief Appraiser/Director-Appraisal Appraisal Quality Control FNC, Inc. www.fncinc.com com When

Course Commerical/Industrial Modeling Concepts Learning Objectives

Course 312 - Commerical/Industrial Modeling Concepts Learning Objectives Course Description Course 312 presents a detailed study of the mass appraisal process as applied to income-producing property. Topics

Course 312 - Commerical/Industrial Modeling Concepts Learning Objectives Course Description Course 312 presents a detailed study of the mass appraisal process as applied to income-producing property. Topics

NCGS , ,

NCGS 105-283, 105-286, 105-317 Requires Counties to establish values based on current market conditions. Values should be at or near 100% of market value as of the reappraisal date. Counties MUST do a

NCGS 105-283, 105-286, 105-317 Requires Counties to establish values based on current market conditions. Values should be at or near 100% of market value as of the reappraisal date. Counties MUST do a

Frequently Asked Questions: Residential Property Price Index

CENTRAL BANK OF CYPRUS EUROSYSTEM Frequently Asked Questions: Residential Property Price Index 1. What is a Residential Property Price Index (RPPI)? An RPPI is an indicator which measures changes in the

CENTRAL BANK OF CYPRUS EUROSYSTEM Frequently Asked Questions: Residential Property Price Index 1. What is a Residential Property Price Index (RPPI)? An RPPI is an indicator which measures changes in the

Technical Description of the Freddie Mac House Price Index

Technical Description of the Freddie Mac House Price Index 1. Introduction Freddie Mac publishes the monthly index values of the Freddie Mac House Price Index (FMHPI SM ) each quarter. Index values are

Technical Description of the Freddie Mac House Price Index 1. Introduction Freddie Mac publishes the monthly index values of the Freddie Mac House Price Index (FMHPI SM ) each quarter. Index values are

Assessment-To-Sales Ratio Study for Division III Equalization Funding: 1999 Project Summary. State of Delaware Office of the Budget

Assessment-To-Sales Ratio Study for Division III Equalization Funding: 1999 Project Summary prepared for the State of Delaware Office of the Budget by Edward C. Ratledge Center for Applied Demography and

Assessment-To-Sales Ratio Study for Division III Equalization Funding: 1999 Project Summary prepared for the State of Delaware Office of the Budget by Edward C. Ratledge Center for Applied Demography and

Relationship of age and market value of office buildings in Tirana City

Relationship of age and market value of office buildings in Tirana City Phd. Elfrida SHEHU Polytechnic University of Tirana Civil Engineering Department of Civil Engineering Faculty Tirana, Albania elfridaal@yahoo.com

Relationship of age and market value of office buildings in Tirana City Phd. Elfrida SHEHU Polytechnic University of Tirana Civil Engineering Department of Civil Engineering Faculty Tirana, Albania elfridaal@yahoo.com

SELF-STORAGE REPORT VIEWPOINT 2017 / COMMERCIAL REAL ESTATE TRENDS. By: Steven J. Johnson, MAI, Senior Managing Director, IRR-Metro LA. irr.

SELF-STORAGE REPORT VIEWPOINT 2017 / COMMERCIAL REAL ESTATE TRENDS By: Steven J. Johnson, MAI, Senior Managing Director, IRR-Metro LA The Self Storage Story The self-storage sector has been enjoying solid

SELF-STORAGE REPORT VIEWPOINT 2017 / COMMERCIAL REAL ESTATE TRENDS By: Steven J. Johnson, MAI, Senior Managing Director, IRR-Metro LA The Self Storage Story The self-storage sector has been enjoying solid

RESEARCH BRIEF TURKISH HOUSING MARKET: PRICE BUBBLE SEPTEMBER 2014 SUMMARY. A Cushman & Wakefield Research Publication OVERVIEW

RESEARCH BRIEF TURKISH HOUSING MARKET: PRICE BUBBLE SEPTEMBER 2014 SUMMARY OVERVIEW Debates on the existence of a price bubble in the Turkish housing market have continued after numerous news releases

RESEARCH BRIEF TURKISH HOUSING MARKET: PRICE BUBBLE SEPTEMBER 2014 SUMMARY OVERVIEW Debates on the existence of a price bubble in the Turkish housing market have continued after numerous news releases

60-HR FL Real Estate Broker Post-Licensing Learning Objectives by Lesson

Lesson 1: Starting a Real Estate Office SECTION 1: BROKERAGE OFFICE ESSENTIALS Recall the characteristics of business entities that may register as a real estate brokerage and the rules involved to operate

Lesson 1: Starting a Real Estate Office SECTION 1: BROKERAGE OFFICE ESSENTIALS Recall the characteristics of business entities that may register as a real estate brokerage and the rules involved to operate

Edmonton Composite Assessment Review Board

Edmonton Composite Assessment Review Board Citation: CVG v The City of Edmonton, 2013 ECARB 01877 Assessment Roll Number: 9942678 Municipal Address: 10020 103 A venue NW Assessment Year: 2013 Assessment

Edmonton Composite Assessment Review Board Citation: CVG v The City of Edmonton, 2013 ECARB 01877 Assessment Roll Number: 9942678 Municipal Address: 10020 103 A venue NW Assessment Year: 2013 Assessment

Appendix 1: Gisborne District Quarterly Market Indicators Report April National Policy Statement on Urban Development Capacity

Appendix 1: Gisborne District Quarterly Market Indicators Report April 2018 National Policy Statement on Urban Development Capacity Quarterly Market Indicators Report April 2018 1 Executive Summary This

Appendix 1: Gisborne District Quarterly Market Indicators Report April 2018 National Policy Statement on Urban Development Capacity Quarterly Market Indicators Report April 2018 1 Executive Summary This

Chapter 7. Valuation Using the Sales Comparison and Cost Approaches. Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter 7 Valuation Using the Sales Comparison and Cost Approaches McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. Decision Making in Commercial Real Estate Centers

Chapter 7 Valuation Using the Sales Comparison and Cost Approaches McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. Decision Making in Commercial Real Estate Centers

CAAR Market Report 2010 First Quarter Published by the Charlottesville Area Association of REALTORS

CAAR Market Report 2010 First Quarter Published by the Charlottesville Area Association of REALTORS Where Are We Now? In the first quarter of 2010, the Charlottesville real estate market continued the

CAAR Market Report 2010 First Quarter Published by the Charlottesville Area Association of REALTORS Where Are We Now? In the first quarter of 2010, the Charlottesville real estate market continued the

I R V. where I = Annual Net Income, R= Capitalization Rate and V= Value

Income Approach to Valuation Capitalization (Cap Rates) the short version! Capitalization is the process of converting net income into a meaningful value that correlates net income to the value of the

Income Approach to Valuation Capitalization (Cap Rates) the short version! Capitalization is the process of converting net income into a meaningful value that correlates net income to the value of the

Mueller. Real Estate Market Cycle Monitor Second Quarter 2018 Analysis

Mueller Real Estate Market Cycle Monitor Second Quarter 2018 Analysis Real Estate Market Cycle analysis of 5 property types in 54 Metropolitan Statistical Areas (MSAs). Graphic Clarification! Point 11

Mueller Real Estate Market Cycle Monitor Second Quarter 2018 Analysis Real Estate Market Cycle analysis of 5 property types in 54 Metropolitan Statistical Areas (MSAs). Graphic Clarification! Point 11

The Local Impact of Home Building in Douglas County, Nevada. Income, Jobs, and Taxes generated. Prepared by the Housing Policy Department

The Local Impact of Home Building in Douglas County, Nevada Income, Jobs, and Taxes generated = Prepared by the Housing Policy Department May 2007 National Association of Home Builders 1201 15th Street,

The Local Impact of Home Building in Douglas County, Nevada Income, Jobs, and Taxes generated = Prepared by the Housing Policy Department May 2007 National Association of Home Builders 1201 15th Street,

MAAO Sales Ratio Committee 2013 Fall Conference Seminar

MAAO Sales Ratio Committee 2013 Fall Conference Seminar Presented By: Al Whitcomb Dakota County (Retired) John Keefe Chisago County Assessor Brent Reid City of Coon Rapids Michael Thompson Scott County

MAAO Sales Ratio Committee 2013 Fall Conference Seminar Presented By: Al Whitcomb Dakota County (Retired) John Keefe Chisago County Assessor Brent Reid City of Coon Rapids Michael Thompson Scott County

Purchase Price Allocations ASC 805 Business Combinations

Purchase Price Allocations Introduction Mergers, acquisitions, and other business transactions have numerous accounting and tax implications. Buyers generally identify and report the fair values of the

Purchase Price Allocations Introduction Mergers, acquisitions, and other business transactions have numerous accounting and tax implications. Buyers generally identify and report the fair values of the

Before the Minnesota Public Utilities Commission State of Minnesota. Docket No. E002/GR Exhibit (LMC-1) Property Taxes

Property Taxes") Direct Testimony and Schedules Leanna M. Chapman Before the Minnesota Public Utilities Commission State of Minnesota In the Matter of the Application of Northern States Power Company for Authority to Increase

Direct Testimony and Schedules Leanna M. Chapman Before the Minnesota Public Utilities Commission State of Minnesota In the Matter of the Application of Northern States Power Company for Authority to Increase

ADOPTED REGULATION OF THE COMMISSION OF APPRAISERS OF REAL ESTATE. LCB File No. R Effective August 26, 2008

ADOPTED REGULATION OF THE COMMISSION OF APPRAISERS OF REAL ESTATE LCB File No. R026-08 Effective August 26, 2008 EXPLANATION Matter in italics is new; matter in brackets [omitted material] is material

ADOPTED REGULATION OF THE COMMISSION OF APPRAISERS OF REAL ESTATE LCB File No. R026-08 Effective August 26, 2008 EXPLANATION Matter in italics is new; matter in brackets [omitted material] is material

IN THE OREGON TAX COURT MAGISTRATE DIVISION Property Tax ) ) ) ) ) ) ) ) ) ) ) )

) ) ) ) ) ) ) ) ) ) )") IN THE OREGON TAX COURT MAGISTRATE DIVISION Property Tax WATUMULL PROPERTIES CORP.; MICRO SYSTEMS ENGINEERING INC.; BIOTRONIK, INC.; and MICROSYSTEMS ENGINEERING, v. Plaintiffs, CLACKAMAS COUNTY ASSESSOR,

IN THE OREGON TAX COURT MAGISTRATE DIVISION Property Tax WATUMULL PROPERTIES CORP.; MICRO SYSTEMS ENGINEERING INC.; BIOTRONIK, INC.; and MICROSYSTEMS ENGINEERING, v. Plaintiffs, CLACKAMAS COUNTY ASSESSOR,

Sales Associate Course

Sales Associate Course Chapter Sixteen Appraisal 1 2 Appraiser Specific amount Impartial (non biased) Defendable Estimate (Opinion) of value Fee based on time and difficulty Must follow Uniform Standards

Sales Associate Course Chapter Sixteen Appraisal 1 2 Appraiser Specific amount Impartial (non biased) Defendable Estimate (Opinion) of value Fee based on time and difficulty Must follow Uniform Standards

UNDERSTANDING HOW USPAP APPLIES TO REAL PROPERTY APPRAISAL PRACTICE USPAP Matrix

UNDERSTANDING HOW USPAP APPLIES TO REAL PROPERTY APPRAISAL PRACTICE - 2014-2015 USPAP Matrix This matrix assumes an Appraisal Report Format under S. R. 2-2(a). *Last updated 9/11/14* GENERAL Violation

UNDERSTANDING HOW USPAP APPLIES TO REAL PROPERTY APPRAISAL PRACTICE - 2014-2015 USPAP Matrix This matrix assumes an Appraisal Report Format under S. R. 2-2(a). *Last updated 9/11/14* GENERAL Violation

RESOLUTION NO ( R)

") RESOLUTION NO. 2013-06- 088 ( R) A RESOLUTION OF THE CITY COUNCIL OF THE CITY OF McKINNEY, TEXAS, APPROVING THE LAND USE ASSUMPTIONS FOR THE 2012-2013 ROADWAY IMPACT FEE UPDATE WHEREAS, per Texas Local

RESOLUTION NO. 2013-06- 088 ( R) A RESOLUTION OF THE CITY COUNCIL OF THE CITY OF McKINNEY, TEXAS, APPROVING THE LAND USE ASSUMPTIONS FOR THE 2012-2013 ROADWAY IMPACT FEE UPDATE WHEREAS, per Texas Local

STATE OF FLORIDA DEPARTMENT OF BUSINESS AND PROFESSIONAL REGULATION DIVISION OF FLORIDA CONDOMINIUMS, TIMESHARES AND MOBILE HOMES

STATE OF FLORIDA DEPARTMENT OF BUSINESS AND PROFESSIONAL REGULATION DIVISION OF FLORIDA CONDOMINIUMS, TIMESHARES AND MOBILE HOMES IN RE: PETITION FOR ARBITRATION CONDO TERMINATION NORMA QUINONES and KRISTIE

STATE OF FLORIDA DEPARTMENT OF BUSINESS AND PROFESSIONAL REGULATION DIVISION OF FLORIDA CONDOMINIUMS, TIMESHARES AND MOBILE HOMES IN RE: PETITION FOR ARBITRATION CONDO TERMINATION NORMA QUINONES and KRISTIE

The Impact of Market Rate Vacancy Increases Eleven-Year Report

The Impact of Market Rate Vacancy Increases Eleven-Year Report January 1, 1999 - December 31, 2009 Santa Monica Rent Control Board April 2010 TABLE OF CONTENTS Summary 1 Vacancy Decontrol s Effects on

The Impact of Market Rate Vacancy Increases Eleven-Year Report January 1, 1999 - December 31, 2009 Santa Monica Rent Control Board April 2010 TABLE OF CONTENTS Summary 1 Vacancy Decontrol s Effects on

LESSON 4. Market Research and Subject Property Identification

LESSON 4 Market Research and Subject Property Identification Note: Selected readings can be found under "Online Readings" on your Course Resources webpage. ASSIGNED READING 1. UBC Real Estate Division.

LESSON 4 Market Research and Subject Property Identification Note: Selected readings can be found under "Online Readings" on your Course Resources webpage. ASSIGNED READING 1. UBC Real Estate Division.

7224 Nall Ave Prairie Village, KS 66208

Real Results - Income Package 10/20/2014 TABLE OF CONTENTS SUMMARY RISK Summary 3 RISC Index 4 Location 4 Population and Density 5 RISC Influences 5 House Value 6 Housing Profile 7 Crime 8 Public Schools

Real Results - Income Package 10/20/2014 TABLE OF CONTENTS SUMMARY RISK Summary 3 RISC Index 4 Location 4 Population and Density 5 RISC Influences 5 House Value 6 Housing Profile 7 Crime 8 Public Schools

CALGARY ASSESSMENT REVIEW BOARD DECISION WITH REASONS

Paae 1 of 6 ARB 08981201 0-P CALGARY ASSESSMENT REVIEW BOARD DECISION WITH REASONS In the matter of the complaint against the Property assessment as provided by the Municipal Government Act, Chapter M-26,

Paae 1 of 6 ARB 08981201 0-P CALGARY ASSESSMENT REVIEW BOARD DECISION WITH REASONS In the matter of the complaint against the Property assessment as provided by the Municipal Government Act, Chapter M-26,

Business Valuation More Art Than Science

Business Valuation More Art Than Science One of the more difficult aspects of business planning is business valuation. It is also one of the more important aspects. While owners of closely held businesses

Business Valuation More Art Than Science One of the more difficult aspects of business planning is business valuation. It is also one of the more important aspects. While owners of closely held businesses

Golf Course. Market Value Assessment in Saskatchewan Handbook. Golf Course Valuation Guide

Market Value Assessment in Saskatchewan Handbook Golf Course Saskatchewan Assessment Management Agency 2012 This document is a derivative work based upon a handbook entitled the "Market Value and Mass

Market Value Assessment in Saskatchewan Handbook Golf Course Saskatchewan Assessment Management Agency 2012 This document is a derivative work based upon a handbook entitled the "Market Value and Mass

Student Generation Rate and School Impact Fee Study Update

Student Generation Rate and School Impact Fee Study Update DRAFT REPORT October 3, 2017 Prepared for: 600 SE 3 rd Avenue Ft. Lauderdale, FL 33301 ph (754) 321-0000 Prepared by: 1000 N. Ashley Dr., #400

Student Generation Rate and School Impact Fee Study Update DRAFT REPORT October 3, 2017 Prepared for: 600 SE 3 rd Avenue Ft. Lauderdale, FL 33301 ph (754) 321-0000 Prepared by: 1000 N. Ashley Dr., #400

MODULE 7-A: APPRAISALS, BPOS AND USPAP

MODULE 7-A: APPRAISALS, BPOS AND USPAP LEARNING OBJECTIVES One of the most challenging aspects of the real estate business is the development of prices or values of the rights to real estate. Buyers and

MODULE 7-A: APPRAISALS, BPOS AND USPAP LEARNING OBJECTIVES One of the most challenging aspects of the real estate business is the development of prices or values of the rights to real estate. Buyers and

Special Report. Australia s Cheapest Suburbs with the Greatest Potential for Capital Growth. For more reports head to

Special Report Australia s Cheapest Suburbs with the Greatest Potential for Capital Growth Market: Australia Compilation date: May 2013 Created by: Redwerks Pty Ltd Contact: 1300 200 340 For more reports

Special Report Australia s Cheapest Suburbs with the Greatest Potential for Capital Growth Market: Australia Compilation date: May 2013 Created by: Redwerks Pty Ltd Contact: 1300 200 340 For more reports

250 CMR: BOARD OF REGISTRATION OF PROFESSIONAL ENGINEERS AND LAND SURVEYORS DRAFT FOR DISCUSSION PURPOSES ONLY

250 CMR 6.00: LAND SURVEYING PROCEDURES AND STANDARDS Section 6.01: Elements Common to All Survey Works 6.02: Survey Works of Lines Affecting Property Rights All land surveying work is considered work

250 CMR 6.00: LAND SURVEYING PROCEDURES AND STANDARDS Section 6.01: Elements Common to All Survey Works 6.02: Survey Works of Lines Affecting Property Rights All land surveying work is considered work

An Assessment of Recent Increases of House Prices in Austria through the Lens of Fundamentals

An Assessment of Recent Increases of House Prices in Austria 1 Introduction Martin Schneider Oesterreichische Nationalbank The housing sector is one of the most important sectors of an economy. Since residential

An Assessment of Recent Increases of House Prices in Austria 1 Introduction Martin Schneider Oesterreichische Nationalbank The housing sector is one of the most important sectors of an economy. Since residential

EXPLANATION OF MARKET MODELING IN THE CURRENT KANSAS CAMA SYSTEM

EXPLANATION OF MARKET MODELING IN THE CURRENT KANSAS CAMA SYSTEM I have been asked on numerous occasions to provide a lay man s explanation of the market modeling system of CAMA. I do not claim to be an

EXPLANATION OF MARKET MODELING IN THE CURRENT KANSAS CAMA SYSTEM I have been asked on numerous occasions to provide a lay man s explanation of the market modeling system of CAMA. I do not claim to be an

6. Review of Property Value Impacts at Rapid Transit Stations and Lines

6. Review of Property Value Impacts at Rapid Transit Stations and Lines 6.0 Review of Property Value Impacts at Rapid Transit Station April 3, 2001 RICHMOND/AIRPORT VANCOUVER RAPID TRANSIT PROJECT Technical

6. Review of Property Value Impacts at Rapid Transit Stations and Lines 6.0 Review of Property Value Impacts at Rapid Transit Station April 3, 2001 RICHMOND/AIRPORT VANCOUVER RAPID TRANSIT PROJECT Technical

Broker. Basic Business Appraisal. Chapter 9. Copyright Gold Coast Schools 1

Broker Chapter 9 Basic Business Appraisal 1 Learning Objectives Describe the characteristics of the legal entities a business appraiser may encounter List at least 5 reasons for a business appraisal List

Broker Chapter 9 Basic Business Appraisal 1 Learning Objectives Describe the characteristics of the legal entities a business appraiser may encounter List at least 5 reasons for a business appraisal List

WYOMING DEPARTMENT OF REVENUE CHAPTER 7 PROPERTY TAX VALUATION METHODOLOGY AND ASSESSMENT (DEPARTMENT ASSESSMENTS)

") CHAPTER 7 PROPERTY TAX VALUATION METHODOLOGY AND ASSESSMENT (DEPARTMENT ASSESSMENTS) Section 1. Authority. These Rules are promulgated under the authority of W.S. 39-11-102(b). Section 2. Purpose of Rules.

CHAPTER 7 PROPERTY TAX VALUATION METHODOLOGY AND ASSESSMENT (DEPARTMENT ASSESSMENTS) Section 1. Authority. These Rules are promulgated under the authority of W.S. 39-11-102(b). Section 2. Purpose of Rules.

Cap Rate Trends, Methodology and Analysis. Dane R. Anderson MAI, CCIM Appraisal & Litigation Services Director

Cap Rate Trends, Methodology and Analysis Dane R. Anderson MAI, CCIM Appraisal & Litigation Services Director 1 Quickly The Income Approach Basis of the Approach Present worth of future benefits Two Methods:

Cap Rate Trends, Methodology and Analysis Dane R. Anderson MAI, CCIM Appraisal & Litigation Services Director 1 Quickly The Income Approach Basis of the Approach Present worth of future benefits Two Methods: