Facilities PRESENTED BY: BELINDA RINKER, JD SENIOR ADVISOR, OFFICE OF HEAD START.

|

|

|

- Abigail Dennis

- 6 years ago

- Views:

Transcription

1 Facilities PRESENTED BY: BELINDA RINKER, JD SENIOR ADVISOR, OFFICE OF HEAD START Note: Play presentation as a PowerPoint slide show to activate hyperlinks.

2 Facilities Laws and Regulations The 2007 Head Start Act requires the establishment of uniform procedures for Head Start agencies to request approval to purchase facilities to be used to carry out Head Start programs. Sec. 644(f)(1). 45 CFR and prescribe the procedures for applying for Head Start grant funds to purchase, construct, or make major renovations to facilities in which to operate Head Start programs. 45 CFR and detail the measures which must be taken to protect the Federal interest in such facilities (including modular units) which are purchased, constructed or renovated with Head Start grant funds.

3 Organization of Facilities Regulations Subpart A General 45 CFR Subpart B Application Procedures 45 CFR Subpart C Protection of Federal Interest 45 CFR Subpart D Modular Units 45 CFR Subpart E Other Administrative Provisions 45 CFR Subpart F Construction and Major Renovation 45 CFR

4 Types of Facilities Activities Acquisition Purchase Outright (full purchase or down payment) Payments (mortgage principal and/or interest) Construction Renovation Major Renovation Minor Renovation (incidental alteration)

5 Facilities Project Process Pre-Award Planning costs approval Application Cost comparison Independent analysis Davis-Bacon Act assurance Special circumstances Modular units Leased property Third party property Mortgages Post-Award & Pre-Project Final working drawings and written specifications Certification of appropriateness and conformity Written estimate of project costs Procurement compliance Davis-Bacon Act in contracts Contract approval Changes in scope Material cost alteration File notice of Federal interest for major renovations, construction and ongoing purchases Casualty insurance for construction and renovation projects Post-Award & Ongoing Provide and maintain architectural or engineering inspection onsite Submit final inspection File notice of Federal interest for outright purchase Title insurance and casualty insurance for outright purchase Ongoing maintenance Audit of mortgage Submit document copies Maintain property records for three years after disposition

6 Definitions 45 CFR Facility Facility means a structure such as a building or modular unit appropriate for use by a Head Start grantee to carry out a Head Start program. Modular unit means a portable prefabricated structure made at another location and moved to a site for use by a Head Start grantee to carry out a Head Start program.

7 Definitions 45 CFR Purchase Purchase means to buy an existing facility, either outright or through a mortgage. Purchase also refers to an approved use of Head Start funds to continue paying the cost of purchasing facilities. Construction Construction means new buildings, and excludes renovations, alterations, additions, or work of any kind to existing buildings.

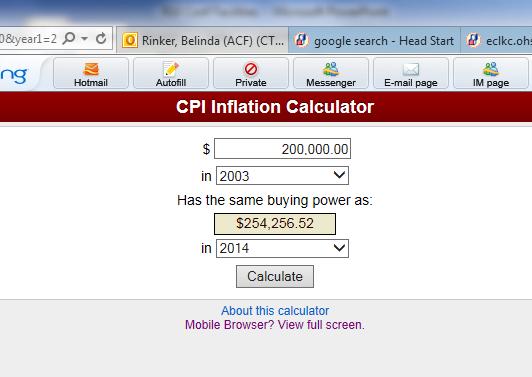

8 Definitions 45 CFR Major Renovation Major renovation means a structural change to the foundation, roof, floor, or exterior or load-bearing walls of a facility, or extension of an existing facility to increase its floor area. Major renovation also means extensive alteration of an existing facility, such as to significantly change its function and purpose, even if such renovation does not include any structural change to the facility. Major renovation also includes a renovation of any kind which has a cost exceeding the lesser of $200,000, adjusted annually to reflect the percentage change in the Consumer Price Index for All Urban Consumers (issued by the Bureau of Labor Statistics) beginning one year after June 2, 2003, or 25 percent of the total annual direct costs approved for the grantee by ACF for the budget period in which the application is made. Minor Renovation Incidental alterations and [minor] renovations mean improvements to facility which do not meet the definition of major renovation.

9

10 Davis-Bacon Act 45 CFR Construction and renovation projects and subcontracts financed with funds awarded under the Head Start program are subject to the Davis-Bacon Act and the Regulations of the Department of Labor. All contracts entered into by any Head Start program which are in excess of $2,000 and are for the construction, renovation or repair of buildings used by Head Start programs, are subject to the requirements of the Davis-Bacon Act. See ACYF-IM-HS All laborers and mechanics employed by contractors or subcontractors in the construction or renovation of affected Head Start facilities shall be paid wages at not less than those prevailing on similar construction in the locality, as determined by the Secretary of Labor.

11 Facilities Projects THE PRE-AWARD PHASE

12 Facilities Application (General) Applications to use Head Start funds (in whole or in part) for the purchase, construction and major renovation of facilities. Reasonable fees and costs associated with and necessary to the acquisition or major renovation of a facility (including reasonable and necessary fees and costs incurred to establish preliminary eligibility under and , or otherwise prior to the submission of an application under or acquisition of the facility) are payable with grant funds, and require prior, written approval of the responsible HHS official. 45 CFR A grantee which proposes to use grant funds to purchase a facility, to apply for funds to construct a facility, or to undertake major renovation of a facility, including facilities purchased for that purpose, must submit a written application to the responsible HHS official, detailed in 45 CFR (a) (q).

13 Facilities Application (Cost Comparison) Applications for the purchase, construction and major renovation of facilities must include a cost estimate. A grantee proposing to acquire or undertake a major renovation of a facility must submit a detailed estimate of the costs of the proposed activity and compare the costs of the proposed activity and provide any additional information requested by the responsible HHS official, detailed in 45 CFR (b)-(f). Responsible HHS official means the official who is authorized to make the grant of financial assistance to operate a Head Start program, or such official's designee, 45 CFR , the Regional Grants Manager or Grants Management Officer (GMO). The responsible HHS official may direct the grantee applying for funds to acquire or make major renovations to a facility to obtain an independent analysis of the cost comparison submitted by the grantee. 45 CFR

14 Pre-Award Summary Before using Head Start funds (wholly or partly) for any of the following facilities activities, a grantee must submit a written application and receive permission: Purchase a facility Initial purchase Ongoing purchase (mortgage) Purchase of a modular unit Construct a facility Make a major renovation To grantee owned property To third party owned property Approval of the facilities application generates many additional grantee restrictions and responsibilities.

15 45 CFR applies to all Head Start and Early Head Start grantees: The Federal government has an interest in all real property and equipment acquired or upon which major renovations have been undertaken with grant funds for use as a Head Start facility. Facilities acquired with grant funds may not be mortgaged or used as collateral, or sold or otherwise transferred to another party, without the written permission of the responsible HHS official. Use of the facility for other than the purpose for which the facility was funded, without the express written approval of the responsible HHS official, is prohibited. the grantee must record the Notice of Federal Interest in the appropriate official records for the jurisdiction where a facility is or will be located 45 CFR applies to institutions of higher education, hospitals, other nonprofit organizations and commercial organizations: Property trust relationship. Real property acquired or improved with Federal funds shall be held in trust by the recipients as trustee for the beneficiaries of the project or program under which the property was acquired or improved, and shall not be encumbered without the approval of the HHS awarding agency. Recipients shall record liens or other appropriate notices of record to indicate that real property has been acquired or constructed or, where applicable, improved with Federal funds, and that use and disposition conditions apply to the property. 45 CFR applies to state, local and tribal governments: Except as otherwise provided by Federal statutes, real property will be used for the originally authorized purposes as long as needed for that purposes, and the grantee or subgrantee shall not dispose of or encumber its title or other interests.

16 Facilities Projects THE POST-AWARD PHASE

17 Title to Facilities 45 CFR Title Held by Grantee Title to facilities acquired with Head Start grant funds vests with the grantee upon acquisition (purchase or construction). Subject to Restrictions Facilities acquired with Head Start grant funds are subject to the provisions of 45 CFR Part 1309, including applicable sections of 45 CFR Part 74 and 45 CFR Part 92.

18 Grantee Facilities Responsibilities 45 CFR , , and Before advertising or taking bids, submit required drawings, specifications and certification and cost estimate by engineer or architect. Follow procurement procedures in 45 CFR Part 74 and 45 CFR Part 92. Submit contracts, leases and mortgages (including subordination agreements) for approval. Maintain architect or engineer inspection onsite and submit upon completion. Comply with the Davis-Bacon Act.

19 Grantee Facilities Responsibilities Record (45 CFR ) or post (45 CFR ) notice of Federal interest. Special length of occupancy requirements and mandatory lease language. 45 CFR Facility on land not owned by the grantee. Major renovations to leased facilities. Make written request and receive written permission before mortgage, use as collateral, sale or transfer. 45 CFR Obtain permission and enter into a written agreement with required terms before subordination of the Federal interest. 45 CFR Include mortgages and encumbrance review in the annual audit. 45 CFR

20 Grantee Facilities Responsibilities (Cont d) Receive express written permission before using a facility for a purpose other than than that for which is was funded. 45 CFR Obtain title insurance with ACF named as loss payee. 45 CFR Obtain physical destruction insurance (may include flood insurance). 45 CFR Adequately maintain facilities. 45 CFR Submit timely certified copies of all required documents. 45 CFR

21 Grantee Facilities Responsibilities (Cont d) 45 CFR , Keep all facilities records for three years after end of ownership or occupancy (if leased). 45 CFR For modular units, meet the additional requirements of 45 CFR , Subpart D. Meet property disposal requirements of 45 CFR and 45 CFR Additional Resource: PI

22 Notice of Federal Interest When Applicable, Filing and Posting (45 CFR Part 1309) Acquire means to purchase or construct in whole or in part with Head Start grant funds through payments made in satisfaction of a mortgage agreement (both principal and interest), as a down payment, and for professional fees, closing costs and any other costs associated with the purchase or construction of the property that are usual and customary for the locality. 45 CFR The Federal government has an interest in all real property and equipment acquired or upon which major renovations have been undertaken with grant funds for use as a Head Start facility. 45 CFR (a). Except for certain modular units, the grantee must record the Notice of Federal Interest in the appropriate official records for the jurisdiction where a facility is or will be located immediately upon [45 CFR (d)(2)]: purchasing a facility or land on which a facility is to be constructed receiving permission to use funds to continue purchase of a facility commencing major renovation of a facility or construction of a facility Modular units which are purchased with grant funds and which are not permanently affixed to land, or which are affixed to land which is not owned by the grantee, must have [a Notice of Federal Interest] posted in a conspicuous place. 45 CFR (b).

23 Property Trust Relationship Grants Management Regulations (45 CFR and 45 CFR 92.31(b)) Property trust relationship Real property, equipment, intangible property and debt instruments that are acquired or improved with Federal funds shall be held in trust by the recipients as trustee for the beneficiaries of the project or program under which the property was acquired or improved, and shall not be encumbered without the approval of the HHS awarding agency. Recipients shall record liens or other appropriate notices of record to indicate that real property has been acquired or constructed or, where applicable, improved with Federal funds, and that use and disposition conditions apply to the property.

24 Facilities Projects COST ALLOCATION

25 Cost Allocation for Shared Facilities

26 Considerations for Allocation of Facilities Use floor plans, blueprints or measurements. Assign square footage to individual programs to the extent possible. Calculate percentages of shared use from assigned square footage. Apply percentages of shared use to square footage which can t be assigned to individual program (common areas). Make sure all space is accounted for. May need to factor in amount of time used to equitably apportion shared space.

27 Example: The Sunshine Center The Sunshine Center building floor plan shows it to be 10,000 square feet, used as follows: Head Start (HS) classrooms: 3,000 sq. ft Offices for EHS home visitors: 2,000 sq. ft Adult Basic Education (ABE) classrooms: 2,000 sq. ft Meeting room: 1,000 sq. ft Used 30 hours per week for ABE classes Used 10 hours per week for EHS meetings Not used by HS program Common areas: 2,000 sq. ft Stairways, halls, utilities, public restrooms used by all programs How would you allocate rent, maintenance, insurance and utilities for the Sunshine Center?

28 Sunshine Center Cost Allocation Plan Head Start Early Head Start Adult Basic Ed Classrooms 3,000 2,000 Offices 2,000 Meeting Room 30 hours ABE (75%) 10 hours EHS (25%) Subtotals: 3,000 2,250 2,750 Percentages: 3,000/8,000=38% 2,250/8,000=28% 2,750/8,000=34% Common Areas: 38% x 2,000=760 28% x 2,000=560 34% x 2,000=680 Entire Center: 3,760 2,810 3,430 Total: 10,000

29 Facilities Projects SPECIAL SITUATIONS

30 Mortgages and Loans Facilities acquired with grant funds may not be mortgaged or used as collateral, or sold or otherwise transferred to another party, without the written permission of the responsible HHS official, including refinancing of existing loans. 45 CFR (b). The terms of any proposed or existing loan(s) related to acquisition or major renovation of facility and the repayment plans (detailing balloon payments or other unconventional terms, if any), and information on all other sources of funding of the acquisition or major renovations, including any restrictions or conditions imposed by other funding sources. 45 CFR (g). If loan is paid in whole or in part, directly or indirectly, with grant funds, 45 CFR (d) requires the filing or posting of a Notice of Federal Interest. Any audit of a grantee, which has acquired or made major renovations to a facility with grant funds, shall include an audit of any mortgage or encumbrance on the facility. Reasonable and necessary fees for this audit and appraisal are payable with grant funds. 45 CFR Notice of default to ACF ACF right of intervention ACF right to substitute borrower If foreclosure occurs, Federal share must be paid to ACF

31 Lines of Credit Facilities acquired with grant funds may not be mortgaged or used as collateral, or sold or otherwise transferred to another party, without the written permission of the responsible HHS official. 45 CFR (b). Real property, equipment, intangible property and debt instruments that are acquired or improved with Federal funds shall be held in trust by the recipients as trustee for the beneficiaries of the project or program under which the property was acquired or improved, and shall not be encumbered without the approval of the HHS awarding agency. 45 CFR and 45 CFR 92.31(b). Lenders providing lines of credit often require a security agreement. A security agreement is a written agreement between a borrower and a lender, filed of record, that creates a lien on behalf of the lender in the property covered by the security agreement. Security agreements covering multiple types of property are sometimes referred to as blanket liens and may include: Real property Inventory Fixtures Equipment Vehicles Accounts receivable Deposit accounts.621, C-27: Interest on debt (or financing costs) to acquire, construct, or replace capital assets is allowable, subject to the conditions stated in this section C-27 Interest. All other interest costs, including interest on borrowed capital, temporary use of endowment funds, and use of the recipient s own funds, however represented, are unallowable. See new Omni Cost Principles, at:

32 Subordination Agreements The responsible HHS official may subordinate the Federal interest in such property to that of a lender which financed the acquisition or major renovation costs subject to the conditions set forth in paragraph (f) of this section. 45 CFR (a). Subordination of the Federal interest allows a lender to take precedence over HHS in receiving its money back in case the borrower (grantee) defaults on the mortgage. Mortgage provisions in (d) still apply: Notice of default to ACF ACF right of intervention ACF right to substitute borrower If foreclosure occurs, Federal share must be paid to ACF Head Start grantees which purchase facilities with respect to which the responsible HHS official has subordinated the Federal Interest to that of the lender must keep the lender informed of the current addresses and telephone numbers of the agencies to which the lender is obligated to give notice in the event of a default.

33 Depreciation and (not) Use Allowance.621, C-15. Depreciation is calculated using: Acquisition cost, excluding land, Federal contributions and amounts claimed to meet a matching requirement (nonfederal share). Period of useful service or useful life is to be established taking into account such factors as type of construction. Straight line depreciation is presumed to be the appropriate method. If the facility is shared, depreciation costs must be properly allocated. Charges for depreciation must be supported by adequate property records, and physical inventories must be taken at least once every two years to ensure that the assets exist and are usable, used, and needed. No depreciation may be allowed on any assets that have outlived their depreciable lives.

34 Sample Calculation of Depreciation Facts: Acquisition cost of the facility was $1,200,000 Useful life of the facility is 40 years Depreciation is straight line Head Start uses 80% of the building $200,000 of the cost was donated materials claimed as nonfederal match $400,000 of the cost was funded by an OHS facilities grant award What amount of annual depreciation can the grantee charge against its Head Start award? Step 1: $1,200,000 - $200,000 - $400,000 = $600,000 (removes match and Federal share) Step 2: $600, = $15,000 (applies useful life to adjusted acquisition cost to determine amount of unallocated annual depreciation) Step 3: $15,000 x 80% = $12,000 (allocates for use and benefit to Head Start)

35 Facility (including Modular Unit) Sited on or Major Renovations on Leased or Third Party Property Required by 45 CFR (l): A grantee applying for funding to make major renovations to a facility it does not own must include with its application written permission from the owner of the building projected to undergo major renovation and a copy of the lease or proposed lease for the facility. Required by 45 CFR (d)(1): A lease or other arrangement which protects the Federal interest in the facility and ensures the grantee's undisturbed use and possession of the facility. A land lease or other similar interest in the underlying land which is long enough to allow the Head Start program to receive the full value of those permanent grant-supported improvements. The lease or document evidencing another arrangement shall include provisions to protect the right of the grantee, or some other organization designated by ACF in the place of the grantee, to occupy the facility for the term of the lease or other arrangement. Such other terms required by the responsible HHS official. Filing of lease or affidavit as Notice of Federal Interest required by 45 CFR (d)(2)-(4): In the case of a facility now sited or to be constructed on land not owned by the grantee, the Notice of Federal Interest shall be the land lease or other document protecting the Federal interest. In the event that filing of a lease is prohibited by State law, the grantee shall file an affidavit signed by the representatives of the grantee and the Lessor stating that the lease includes terms which protect the right of the grantee, or some other organization designated by ACF in the place of the grantee, to occupy the facility for the term of the lease.

36 Valuation of Donated Property and Space (Do not apply fair rental value below to Related Party donations see next Slide) Third party in-kind contributions count towards satisfying a cost sharing or matching requirement only where, if the party receiving the contributions were to pay for them, the payments would be allowable costs. 45 CFR 74.23(a)(4) or 45 CFR 92.24(b)(7)(i). The value of donated land and buildings shall not exceed its fair market value at the time of donation to the recipient as established by an independent appraiser (e.g., certified real property appraiser or General Services Administration representative) and certified by a responsible official of the recipient. 45 CFR 74.23(h)(1) or 45 CFR 92.24(g). The value of donated space shall not exceed the fair rental value of comparable space as established by an independent appraisal of comparable space and facilities in a privately-owned building in the same locality. 45 CFR 74.23(h)(1) or 45 CFR 92.24(g). For reductions in fair rental value, intent to contribute must be demonstrated.

37 Donated Space from Related Parties Third party in-kind contributions count towards satisfying a cost sharing or matching requirement only where, if the party receiving the contributions were to pay for them, the payments would be allowable costs. 45 CFR 74.23(a)(4) or 45 CFR 92.24(b)(7)(i). Rental costs under "less-than-arm s-length" leases are allowable only up to the amount (as explained in paragraph (2)) that would be allowed had title to the property vested in the institution. For this purpose, a less-than-arm s-length lease is one under which one party to the lease agreement is able to control or substantially influence the actions of the other. Such leases include, but are not limited to those between (1) divisions of an institution; (2) non-federal entities under common control through common officers, directors, or members; and (3) an institution and a director, trustee, officer, or key employee of the institution or an immediate family member, either directly or through corporations, trusts, or similar arrangements in which they hold a controlling interest. For example, an institution may establish a separate corporation for the sole purpose of owning property and leasing it back to the institution. Omni Cost Principles,.621, C-15.

38 Sample Comparison for Unrelated and Related Parties Unrelated Party: A local private school allows Head Start to use 1,000 square feet of classroom and common space without charge. An independent appraisal by a certified appraiser sets the fair rental value of the space at $12 per square foot per year. 1,000 x $12 = $12,000 The grantee can claim $12,000 in nonfederal match. Related Party: A separate housing corporation with the same governing body members as the Head Start agency allows Head Start to use 1,000 square feet of classroom and common space without charge. The acquisition cost of the building was $200,000, the useful life is 40 years and 1,000 square feet is 20% of the total square footage in the building. $200, = $5,000 $5,000 x 20% = $1,000 The grantee can claim $1,000 in nonfederal match.

39 Capital Leases (Slide #1) Rental costs under leases which are required to be treated as capital leases under GAAP are allowable only up to the amount that would be allowed had the institution purchased the property on the date the lease agreement was executed. This amount would include expenses such as depreciation, maintenance, taxes, and insurance. The provisions of Financial Accounting Standards Board Statement 13, Accounting for Leases, shall be used to determine whether a lease is a capital lease. Ownership is transferred at the end of the lease term The lease contains a bargain purchase option The lease term is equal to 75 percent or more of the estimated economic life The present value of the minimum lease payments equals or exceeds 90 percent of the fair market value of the leased property

40 Capital Leases (Slide #2) Interest costs related to capital leases are allowable to the extent they meet the criteria in C-27 Interest. Interest on debt (or financing costs) to acquire, construct, or replace capital assets is allowable, subject to the conditions stated. Unallowable costs include amounts paid for profit, management fees, and taxes that would not have been incurred had the institution purchased the facility. The use of Head Start funds to pay all or part of capital lease payments is classified as an acquisition for purposes of application of 45 CFR Part An application meeting the requirements of 45 CFR and is required. The grantee must file a Notice of Federal Interest in accordance with 45 CFR

41 Modular Units Special regulations for modular units are found at 45 CFR Applications for purchase must include: A detailed site description. 45 CFR (a). A statement of procurement procedures used by the grantee. 45 CFR (a). Specifications for the proposed modular unit. 45 CFR (a). The grantee must have the modular unit inspected by a licensed engineer or architect within 15 calendar days of its installation or approval of a continuing purchase, and must submit to the responsible HHS official the engineer's or architect's inspection report within 30 calendar days of the inspection. 45 CFR Notice of Federal Interest must be posted in a conspicuous location on the modular unit. 45 CFR (b). Must also meet applicable regulations if modular unit is placed on leased property or property owned by a third party. See Slide 36. After 15 years, modular units can be disposed of without further responsibility for compensation to ACF. See ACF-IM-HS-12-08, Disposition of Older Modular Units.

42 Disposition of Facilities Real property must be used for the authorized purpose as long as it is needed. May use in other Federally sponsored programs with approval of the HHS awarding agency. If property is no longer needed, grantee must request disposition instructions: Grantee retains property and compensates the U. S. Treasury for the Federal share. Awarding agency directs transfer to another grantee and compensates for the grantee share. Property is sold and net proceeds are allocated between Federal share and grantee share. 45 CFR and 45 CFR

43 Sample Disposition Calculation Original Purchase Price: $2,000,000 $1,200,000 Down Payment $ 800,000 Purchase Mortgage $ 200,000 Mortgage Balance at Disposition $2,500,000 Facility Fair Market Appraised Value or Net Proceeds at Disposition Contribution Grantee OHS/ACF (Federal) Down Payment $200,000 Third party donation not claimed as nonfederal match Annual Mortgage Payments Made prior to disposition over 20 years $600,000 Principal paid by grantee from nonfederal funds Major Renovation Year 5 $300,000 Donated not federal source $1,000,000 One time funds $ 400,000 Interest charged to annual base grant Major Renovation Year 10 $500,000 One time funds Total: $3,000,000 $1,100,000 $1,900,000

44 Sample Disposition Calculation (No Subordination Agreement) Original Purchase Price: $2,000,000 $1,200,000 Down Payment $ 800,000 Purchase Mortgage (Federal Interest not subordinated) $ 200,000 Mortgage Balance at Disposition $2,500,000 Facility Fair Market Appraised Value at Disposition Contribution Grantee OHS/ACF (Federal) Total: $3,000,000 $1,100,000 $1,900,000 Step 1: Establish Grantee and Federal Shares as Percentages Grantee: $1,100,000 $3,000,000 = 37% Federal: $1,900,000 $3,000,000 = 63% Step 2: Apply Grantee and Federal Shares to Facility FMV or Net Proceeds Federal: 63% x $2,500,000 = $1,580,000 Grantee: 37 % x $2,500,000 = $ 920,000 Step 3: Lender paid from Grantee Share: $ 200,000 Final Grantee Share: $ 720,000

45 Sample Disposition Calculation (Subordination Agreement) Original Purchase Price: $2,000,000 $1,200,000 Down Payment $ 800,000 Purchase Mortgage (Federal Interest subordinated) $ 200,000 Mortgage Balance at Disposition $2,500,000 Facility Fair Market Appraised Value or Net Proceeds at Disposition Contribution Grantee OHS/ACF (Federal) Total: $3,000,000 $1,100,000 $1,900,000 Step 1: Establish Grantee and Federal Shares as Percentages Grantee: $1,100,000 $3,000,000 = 37% Federal: $1,900,000 $3,000,000 = 63% Step 2: Lender paid from Net Proceeds $2,500,000 - $200,000 = $2,200,000 Step 3: Apply Grantee and Federal Shares to remaining Net Proceeds Federal: 63% x $2,200,000 = $1,386,000 Grantee: 37 % x $2,200,000 = $ 814,000

46 Super Circular Disposition Language (Does not currently apply except to Part 92 pending implementation of regulations) Disposition. When real property is no longer needed for the originally authorized purpose, the recipient or subrecipient will request disposition instructions from the Federal awarding agency. The instructions will provide for one of the following alternatives: Retention of title. Retain title after compensating the Federal awarding agency. The amount paid to the Federal awarding agency will be computed by applying the Federal awarding agency's percentage of participation in the cost of the original purchase to the fair market value of the property. However, in those situations where a recipient or subrecipient is disposing of real property acquired or improved with award funds and acquiring replacement real property under the same program, the net proceeds from the disposition may be used as an offset to the cost of the replacement property. Sale of property. Sell the property and compensate the Federal awarding agency. The amount due to the Federal awarding agency will be calculated by applying the Federal awarding agency's percentage of participation in the cost of the original purchase (and cost of any improvements) to the proceeds of the sale after deduction of any actual and reasonable selling and fixing-up expenses. If the award is still active, the net proceeds from sale may be offset against the original cost of the property. When a recipient or subrecipient is directed to sell property, sales procedures shall be followed that provide for competition to the extent practicable and result in the highest possible return. Transfer of title. Transfer title to the Federal awarding agency or to a third party designated/approved by the Federal awarding agency. The recipient or subrecipient shall be entitled to be paid an amount calculated by applying the award or subaward recipient's percentage of participation in the purchase of the real property (and cost of any improvements) to the current fair market value of the property.

47 Facilities Tip Sheet #1 Facilities activities by Grantees: The facilities regulations apply to grantees, so facilities activities proposing that title be held by a delegate agency or mortgage payments be made on behalf of a delegate agency are not fundable. Construction: The term construction in the Head Start regulations is defined at a much higher dollar value than the term construction under the Davis-Bacon Act. Under the Head Start regulations, the term construction only applies to new facilities. Major Renovation: Note the three separate criteria for defining a major renovation. Be sure to use the CPI adjusted dollar threshold, if applicable. The term construction under the Davis-Bacon Act includes a major renovation as defined in the Head Start regulations.

48 Facilities Tip Sheet #2 Pre-Application Costs: Be sure to obtain prior written approval for initial pre-project costs such as blueprints, feasibility studies, surveys and similar expenses. Facilities Project Applications: An effective way to organize applications is to use a notebook with an alphabetic tab system aligned with the subsections of 45 CFR Under (q) applicants must submit such additional information as the responsible HHS official may require.

49 Facilities Tip Sheet #3 Independent Analysis: The responsible HHS official may require the applicant to obtain an independent analysis of the cost comparison submitted under or the statement under (f) [lack of alternative facilities], or both, if, in the judgment of the official, such an analysis is necessary to adequately review a proposal. The analysis shall be in writing and shall be made by a qualified, disinterested real estate professional in the community in which the property to be purchased or renovated is situated. 45 CFR

50 Questions and Comments

Capital Assets, Supplies, Equipment, and Intangible Property

Capital Assets, Supplies, Equipment, and Intangible Property 1 Uniform Guidance vs. OMB Circulars Prior to the Uniform Guidance, requirements governing cost Designed for DOL-ETA direct principles, administrative

Capital Assets, Supplies, Equipment, and Intangible Property 1 Uniform Guidance vs. OMB Circulars Prior to the Uniform Guidance, requirements governing cost Designed for DOL-ETA direct principles, administrative

CALIFORNIA STATE UNIVERSITY, BAKERSFIELD AUXILIARY FOR SPONSORED PROGRAMS ADMINISTRATION. Equipment Management Policy

CALIFORNIA STATE UNIVERSITY, BAKERSFIELD AUXILIARY FOR SPONSORED PROGRAMS ADMINISTRATION Equipment Management Policy I. Policy Objective It is the policy of the California State University Bakersfield

CALIFORNIA STATE UNIVERSITY, BAKERSFIELD AUXILIARY FOR SPONSORED PROGRAMS ADMINISTRATION Equipment Management Policy I. Policy Objective It is the policy of the California State University Bakersfield

FEDERAL INTEREST: THE GOVERNMENT S INTEREST IN PROPERTY ACQUIRED OR IMPROVED WITH FEDERAL FUNDS

FEDERAL INTEREST: THE GOVERNMENT S INTEREST IN PROPERTY ACQUIRED OR IMPROVED WITH FEDERAL FUNDS Edward (Ted) Waters, Esq. Scott Sheffler, Esq. August 4, 2016 1 AGENDA 1. Legal Concept of Federal Interest

FEDERAL INTEREST: THE GOVERNMENT S INTEREST IN PROPERTY ACQUIRED OR IMPROVED WITH FEDERAL FUNDS Edward (Ted) Waters, Esq. Scott Sheffler, Esq. August 4, 2016 1 AGENDA 1. Legal Concept of Federal Interest

Guidance for Habitat for Humanity Affiliates January 12, 2011

January 12, 2011 Community Planning and Development NSP Policy Alert! Guidance for Habitat for Humanity Affiliates January 12, 2011 Overview Habitat for Humanity utilizes a unique development model to

January 12, 2011 Community Planning and Development NSP Policy Alert! Guidance for Habitat for Humanity Affiliates January 12, 2011 Overview Habitat for Humanity utilizes a unique development model to

NoRTEC Policy Statement Property Purchasing, Inventory and Disposal

NoRTEC Policy Statement Property Purchasing, Inventory and Disposal Effective: November 10, 2016 Last Updated: November 10, 2016 PURPOSE This policy provides guidance and establishes the procedures for

NoRTEC Policy Statement Property Purchasing, Inventory and Disposal Effective: November 10, 2016 Last Updated: November 10, 2016 PURPOSE This policy provides guidance and establishes the procedures for

Federal Grants Manual Webinar Series: Property Management

Federal Grants Manual Webinar Series: Property Management June 24, 2015 The content and materials are not to be shared or distributed unless you have written permission from TASBO to do so. That includes:

Federal Grants Manual Webinar Series: Property Management June 24, 2015 The content and materials are not to be shared or distributed unless you have written permission from TASBO to do so. That includes:

UAS GM 12: Property Standards

Overview The UA Statewide Accounting Manual definition of capital expenditures is found in Revenue and Expenditure Account Codes, Section 5000, and for UA purposes, is defined as over $5,000 and having

Overview The UA Statewide Accounting Manual definition of capital expenditures is found in Revenue and Expenditure Account Codes, Section 5000, and for UA purposes, is defined as over $5,000 and having

Purchasing, Inventory and Disposal of Property

Policy Number: P-WIOA-PIDP-1.A Effective Date: April 11, 2017 Approved By: Nick Schultz, Executive Director Purchasing, Inventory and Disposal of Property PURPOSE This policy provides guidance and establishes

Policy Number: P-WIOA-PIDP-1.A Effective Date: April 11, 2017 Approved By: Nick Schultz, Executive Director Purchasing, Inventory and Disposal of Property PURPOSE This policy provides guidance and establishes

Policy Policy Title: LWDA-10 Property Management Policy

Policy Title: LWDA-10 Property Management Policy Policy 00-31 Purpose: This policy communicates methods used by Tennessee Department of Labor and Workforce Development (TDLWD) for the procurement of goods

Policy Title: LWDA-10 Property Management Policy Policy 00-31 Purpose: This policy communicates methods used by Tennessee Department of Labor and Workforce Development (TDLWD) for the procurement of goods

What is the Omni-Circular Final Guidance on the Uniform Administrative Requirements, Cost Principals and Audit Requirements for Federal Awards

What is the Omni-Circular Final Guidance on the Uniform Administrative Requirements, Cost Principals and Audit Requirements for Federal Awards What are the Goals? Streamline guidance Reduce administrative

What is the Omni-Circular Final Guidance on the Uniform Administrative Requirements, Cost Principals and Audit Requirements for Federal Awards What are the Goals? Streamline guidance Reduce administrative

Type of Costs, Obligations and Property Management Federal Programs

Type of Costs, Obligations and Property Management Federal Programs The Interlocal establishes and maintains board policies, administrative regulations, and administrative procedures on administration

Type of Costs, Obligations and Property Management Federal Programs The Interlocal establishes and maintains board policies, administrative regulations, and administrative procedures on administration

LOUISIANA HOUSING CORPORATION QUALIFIED CONTRACT PROCESSING GUIDELINES

LOUISIANA HOUSING CORPORATION QUALIFIED CONTRACT PROCESSING GUIDELINES The Louisiana Housing Corporation (the LHC ) is successor in interest to the Louisiana Housing Finance Agency (the LHFA ) and is now

LOUISIANA HOUSING CORPORATION QUALIFIED CONTRACT PROCESSING GUIDELINES The Louisiana Housing Corporation (the LHC ) is successor in interest to the Louisiana Housing Finance Agency (the LHFA ) and is now

Property Management Under Uniform Guidance (UG)

") Property Management Under Uniform Guidance (UG) Presented by: Gelman, Rosenberg & Freedman CPAs Jennifer Arminger, CPA, Partner Jim Larson, CPA, Partner and E-ISG Asset Intelligence Jackie Luo, CEO Property

Property Management Under Uniform Guidance (UG) Presented by: Gelman, Rosenberg & Freedman CPAs Jennifer Arminger, CPA, Partner Jim Larson, CPA, Partner and E-ISG Asset Intelligence Jackie Luo, CEO Property

SEATTLE UNIVERSITY. Disposal of Equipment Purchased with Sponsor Funds. Policy and Procedures Manual

SEATTLE UNIVERSITY Disposal of Equipment Purchased with Sponsor Funds Policy and Procedures Manual As of August 11, 2014 1 Table of Contents I. Policy Statement... 3 II. Determination of Ownership and

SEATTLE UNIVERSITY Disposal of Equipment Purchased with Sponsor Funds Policy and Procedures Manual As of August 11, 2014 1 Table of Contents I. Policy Statement... 3 II. Determination of Ownership and

will not unbalance the ratio of debt to equity.

paragraph 2-12-3. c.) and prime commercial paper. All these restrictions are designed to assure that debt proceeds (including Title VII funds disbursed from escrow), equity contributions and operating

paragraph 2-12-3. c.) and prime commercial paper. All these restrictions are designed to assure that debt proceeds (including Title VII funds disbursed from escrow), equity contributions and operating

EARLY LEARNING COALITION OF OSCEOLA COUNTY

Page of 1 of 9 POLICY STATEMENT The Coalition shall adhere to Federal and state laws, regulations, and rules requiring the implementation of proper controls related to the management, maintenance, reporting,

Page of 1 of 9 POLICY STATEMENT The Coalition shall adhere to Federal and state laws, regulations, and rules requiring the implementation of proper controls related to the management, maintenance, reporting,

Uniform Guidance: Cost Principles. Why This Session Is Needed. Lesson Overview & Module Objectives. Changes to many Cost Principles and

Uniform Guidance: Cost Principles Uniform Guidance: Cost Principles 1 Why This Session Is Needed Changes to many Cost Principles and Selected Items of Cost Impact of changes on current operations Required

Uniform Guidance: Cost Principles Uniform Guidance: Cost Principles 1 Why This Session Is Needed Changes to many Cost Principles and Selected Items of Cost Impact of changes on current operations Required

Purpose: Intended Audience: Introduction: Federal Regulation: 29 CFR Equipment.

Purpose: This technical assistance guide has been created to provide guidance in developing policy and procedures regarding inventory. Adherence to a comprehensive policy and procedures will ensure the

Purpose: This technical assistance guide has been created to provide guidance in developing policy and procedures regarding inventory. Adherence to a comprehensive policy and procedures will ensure the

LWDB PROCUREMENT / PROPERTY MANAGEMENT POLICY

NWPA WDB POLICY - 100 Rev. Level: C LWDB PROCUREMENT / PROPERTY MANAGEMENT POLICY The system of property and procurement management must have procedures to determine the actions of responsible parties

NWPA WDB POLICY - 100 Rev. Level: C LWDB PROCUREMENT / PROPERTY MANAGEMENT POLICY The system of property and procurement management must have procedures to determine the actions of responsible parties

CITY'S BONDS TO FINANCE HOUSING PROGRAMS ARE NOT PRIVATE ACTIVITY BONDS.

Private Letter Ruling 9203021, IRC Section 141 CITY'S BONDS TO FINANCE HOUSING PROGRAMS ARE NOT PRIVATE ACTIVITY BONDS. Date: October 21, 1991 Dear ***: This letter is our reply to your request for rulings

Private Letter Ruling 9203021, IRC Section 141 CITY'S BONDS TO FINANCE HOUSING PROGRAMS ARE NOT PRIVATE ACTIVITY BONDS. Date: October 21, 1991 Dear ***: This letter is our reply to your request for rulings

HOME Program Basic Facts

HOME Program Basic Facts WHAT IS HOME? HOME is short for "HOME Investment Partnership Program", which became law in 1990. HOME provides an annual formula-based federal grant to the City of San Diego for

HOME Program Basic Facts WHAT IS HOME? HOME is short for "HOME Investment Partnership Program", which became law in 1990. HOME provides an annual formula-based federal grant to the City of San Diego for

Acquisition IOWA 2015 CDBG MANAGEMENT GUIDE APPENDIX 2 PAGE: 79

Acquisition IOWA 2015 CDBG MANAGEMENT GUIDE APPENDIX 2 PAGE: 79 WHEN A PUBLIC AGENCY ACQUIRES YOUR PROPERTY Introduction U.S. Department of Housing And Urban Development Office of Community Planning and

Acquisition IOWA 2015 CDBG MANAGEMENT GUIDE APPENDIX 2 PAGE: 79 WHEN A PUBLIC AGENCY ACQUIRES YOUR PROPERTY Introduction U.S. Department of Housing And Urban Development Office of Community Planning and

Sec. 48 Investment Credit: Eligible property and special rules; Rehabilitation expenditures; Rehabilitation credit passthroughs

Private Letter Ruling 8943074 Sec. 48 Investment Credit: Eligible property and special rules; Rehabilitation expenditures; Rehabilitation credit passthroughs This is in response to a letter dated January

Private Letter Ruling 8943074 Sec. 48 Investment Credit: Eligible property and special rules; Rehabilitation expenditures; Rehabilitation credit passthroughs This is in response to a letter dated January

1 SB By Senators Hightower, Glover and Albritton. 4 RFD: County and Municipal Government. 5 First Read: 12-MAR-15.

1 SB220 2 168824-6 3 By Senators Hightower, Glover and Albritton 4 RFD: County and Municipal Government 5 First Read: 12-MAR-15 Page 0 1 SB220 2 3 4 ENROLLED, An Act, 5 To allow a county, municipality,

1 SB220 2 168824-6 3 By Senators Hightower, Glover and Albritton 4 RFD: County and Municipal Government 5 First Read: 12-MAR-15 Page 0 1 SB220 2 3 4 ENROLLED, An Act, 5 To allow a county, municipality,

The Substance of the Standard

The Substance of the Standard Mayer Hoffman McCann P.C. An Independent CPA Firm TM A publication of the Professional Standards Group April 2014 Accounting Election for Common Control Leasing Arrangements

The Substance of the Standard Mayer Hoffman McCann P.C. An Independent CPA Firm TM A publication of the Professional Standards Group April 2014 Accounting Election for Common Control Leasing Arrangements

OPERATIONS MANUAL CHAPTER 3 ACQUISITION AND PROPERTY MANAGEMENT

OPERATIONS MANUAL CHAPTER 3 ACQUISITION AND PROPERTY MANAGEMENT REVISED NOVEMBER 14, 2016 TABLE OF CONTENTS Sec 1. Scope and Applicability... 3 Sec 2. Purpose of Property Management... 3 Sec 3. Definitions...

OPERATIONS MANUAL CHAPTER 3 ACQUISITION AND PROPERTY MANAGEMENT REVISED NOVEMBER 14, 2016 TABLE OF CONTENTS Sec 1. Scope and Applicability... 3 Sec 2. Purpose of Property Management... 3 Sec 3. Definitions...

Common Interest Ownership Act Key Points

Common Interest Ownership Act Key Points Declaration A common interest community may be created only by recording a declaration executed in the same manner as a deed. In a cooperative, it is created by

Common Interest Ownership Act Key Points Declaration A common interest community may be created only by recording a declaration executed in the same manner as a deed. In a cooperative, it is created by

CHAPTER Committee Substitute for Committee Substitute for House Bill No. 229

CHAPTER 2013-240 Committee Substitute for Committee Substitute for House Bill No. 229 An act relating to land trusts; creating s. 689.073, F.S., and transferring, renumbering, and amending s. 689.071(4)

CHAPTER 2013-240 Committee Substitute for Committee Substitute for House Bill No. 229 An act relating to land trusts; creating s. 689.073, F.S., and transferring, renumbering, and amending s. 689.071(4)

LKAS 17 Sri Lanka Accounting Standard LKAS 17

Sri Lanka Accounting Standard LKAS 17 Leases CONTENTS SRI LANKA ACCOUNTING STANDARD LKAS 17 LEASES paragraphs OBJECTIVE 1 SCOPE 2 DEFINITIONS 4 CLASSIFICATION OF LEASES 7 LEASES IN THE FINANCIAL STATEMENTS

Sri Lanka Accounting Standard LKAS 17 Leases CONTENTS SRI LANKA ACCOUNTING STANDARD LKAS 17 LEASES paragraphs OBJECTIVE 1 SCOPE 2 DEFINITIONS 4 CLASSIFICATION OF LEASES 7 LEASES IN THE FINANCIAL STATEMENTS

International Accounting Standard 17 Leases. Objective. Scope. Definitions IAS 17

International Accounting Standard 17 Leases Objective 1 The objective of this Standard is to prescribe, for lessees and lessors, the appropriate accounting policies and disclosure to apply in relation

International Accounting Standard 17 Leases Objective 1 The objective of this Standard is to prescribe, for lessees and lessors, the appropriate accounting policies and disclosure to apply in relation

BILL H.3653: An Act Financing the Production and Preservation of Housing for Low and Moderate Income Residents

BILL H.3653: An Act Financing the Production and Preservation of Housing for Low and Moderate Income Residents SECTION 2 Authorizes capital spending amounts and provides line item language describing permitted

BILL H.3653: An Act Financing the Production and Preservation of Housing for Low and Moderate Income Residents SECTION 2 Authorizes capital spending amounts and provides line item language describing permitted

Transit Joint Development: A New Look at FTA s Guidelines

Transit Joint Development: A New Look at FTA s Guidelines New Partners for Smart Growth Conference February 9, 2008 Jayme L. Blakesley Attorney-Advisor Federal Transit Administration jayme.blakesley@dot.gov

Transit Joint Development: A New Look at FTA s Guidelines New Partners for Smart Growth Conference February 9, 2008 Jayme L. Blakesley Attorney-Advisor Federal Transit Administration jayme.blakesley@dot.gov

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 2015 S 2 SENATE BILL 554 Education/Higher Education Committee Substitute Adopted 6/24/16

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION S SENATE BILL Education/Higher Education Committee Substitute Adopted // Short Title: School Building Leases. (Public) Sponsors: Referred to: March 0, 1 0 1 A

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION S SENATE BILL Education/Higher Education Committee Substitute Adopted // Short Title: School Building Leases. (Public) Sponsors: Referred to: March 0, 1 0 1 A

CAPITAL ASSET POLICY

CAPITAL ASSET POLICY POLICY STATEMENT Morningside College, through each of its operating departments acquires and disposes of capital assets. Each department is responsible for following College procedures

CAPITAL ASSET POLICY POLICY STATEMENT Morningside College, through each of its operating departments acquires and disposes of capital assets. Each department is responsible for following College procedures

TRIBAL CODE CHAPTER 13 PROCUREMENT AND PROPERTY MANAGEMENT

TRIBAL CODE CHAPTER 13 PROCUREMENT AND PROPERTY MANAGEMENT CONTENTS: 13.101 Definitions. 13.102 Compliance. 13.103 Financial Reporting and Recordkeeping. 13.104 Maintenance of Property. 13.105 Disposition

TRIBAL CODE CHAPTER 13 PROCUREMENT AND PROPERTY MANAGEMENT CONTENTS: 13.101 Definitions. 13.102 Compliance. 13.103 Financial Reporting and Recordkeeping. 13.104 Maintenance of Property. 13.105 Disposition

DEPARTMENT OF HUMAN SERVICES SENIORS AND PEOPLE WITH DISABILITIES DIVISION OREGON ADMINISTRATIVE RULES CHAPTER 411

DEPARTMENT OF HUMAN SERVICES SENIORS AND PEOPLE WITH DISABILITIES DIVISION OREGON ADMINISTRATIVE RULES CHAPTER 411 DIVISION 310 DEVELOPMENTAL DISABILITIES COMMUNITY HOUSING 411-310-0010 Statement of Purpose

DEPARTMENT OF HUMAN SERVICES SENIORS AND PEOPLE WITH DISABILITIES DIVISION OREGON ADMINISTRATIVE RULES CHAPTER 411 DIVISION 310 DEVELOPMENTAL DISABILITIES COMMUNITY HOUSING 411-310-0010 Statement of Purpose

TANGIBLE CAPITAL ASSETS

Administrative Procedure 535 Background TANGIBLE CAPITAL ASSETS The Division will follow a prescribed procedure to record and manage the tangible capital assets (TCA) owned by the Division. The treatment

Administrative Procedure 535 Background TANGIBLE CAPITAL ASSETS The Division will follow a prescribed procedure to record and manage the tangible capital assets (TCA) owned by the Division. The treatment

EVERGREEN COURT SENIOR HOUSING ASSOCIATION / EVERGREEN COURT SENIOR APARTMENTS HUD PROJECT NO. 127 EE013

EVERGREEN COURT SENIOR HOUSING ASSOCIATION / EVERGREEN COURT SENIOR APARTMENTS HUD PROJECT NO. 127 EE013 Financial Statements and Single Audit Reports Table of Contents Independent Auditor s Report 1 2

EVERGREEN COURT SENIOR HOUSING ASSOCIATION / EVERGREEN COURT SENIOR APARTMENTS HUD PROJECT NO. 127 EE013 Financial Statements and Single Audit Reports Table of Contents Independent Auditor s Report 1 2

INDEX. of subrecipients, VIII -2 records, VI-1, 4, 13. OMB Circular A-122, VIII- 3 certification: I-28

INDEX A B Barney Frank Amendment, IV-7 accounts beneficiary characteristics (form), VI-1, 2, 19 escrow, II-2,4,7-11, 16,20 bidder s instructions, I-12 interest-bearing, II-7, 0 compliance notion, I-12

INDEX A B Barney Frank Amendment, IV-7 accounts beneficiary characteristics (form), VI-1, 2, 19 escrow, II-2,4,7-11, 16,20 bidder s instructions, I-12 interest-bearing, II-7, 0 compliance notion, I-12

TULSA DEVELOPMENT AUTHORITY (A Component Unit of the City of Tulsa, Oklahoma) FINANCIAL REPORTS June 30, 2018 and 2017

FINANCIAL REPORTS June 30, 2018 and 2017") FINANCIAL REPORTS June 30, 2018 and 2017 Index Page Independent Auditor s Report 1 Management s Discussion and Analysis 3 Basic Financial Statements: Statements of Net Position 9 Statements of Revenues,

FINANCIAL REPORTS June 30, 2018 and 2017 Index Page Independent Auditor s Report 1 Management s Discussion and Analysis 3 Basic Financial Statements: Statements of Net Position 9 Statements of Revenues,

1 H. 4702, 190th Gen. Ct (Mass. 2018). 2 H. 4297, 190th Gen. Ct (Mass. 2018).

. 2 H. 4297, 190th Gen. Ct (Mass. 2018).") Public Housing Provisions in the Economic Development Bill (H.4702), as Reported Out by House Committee on Bonding, Capital Expenditures & State Assets Prepared by Citizens Housing and Planning Association

Public Housing Provisions in the Economic Development Bill (H.4702), as Reported Out by House Committee on Bonding, Capital Expenditures & State Assets Prepared by Citizens Housing and Planning Association

MEADOW PARK SENIOR HOUSING ASSOCIATION / MEADOW PARK SENIOR APARTMENTS HUD PROJECT NO. 127 EE021. Financial Statements and Single Audit Reports

MEADOW PARK SENIOR HOUSING ASSOCIATION / MEADOW PARK SENIOR APARTMENTS HUD PROJECT NO. 127 EE021 Financial Statements and Single Audit Reports Table of Contents Independent Auditor s Report 1 2 Financial

MEADOW PARK SENIOR HOUSING ASSOCIATION / MEADOW PARK SENIOR APARTMENTS HUD PROJECT NO. 127 EE021 Financial Statements and Single Audit Reports Table of Contents Independent Auditor s Report 1 2 Financial

PART 1 - Rules and Regulations Governing the Building Homes Rhode Island Program

860-RICR-00-00-1 TITLE 860 Housing Resources Commission CHAPTER 00 N/A SUBCHAPTER 00 N/A PART 1 - Rules and Regulations Governing the Building Homes Rhode Island Program 1.1 Purpose A. The purpose of these

860-RICR-00-00-1 TITLE 860 Housing Resources Commission CHAPTER 00 N/A SUBCHAPTER 00 N/A PART 1 - Rules and Regulations Governing the Building Homes Rhode Island Program 1.1 Purpose A. The purpose of these

TEXAS GENERAL LAND OFFICE PROCUREMENT GUIDANCE FOR RECIPIENTS AND SUBRECIPIENTS UNDER 2 CFR PART 200 (UNIFORM RULES)

") TEXAS GENERAL LAND OFFICE COMMUNITY DEVELOPMENT & REVITALIZATION PROCUREMENT GUIDANCE FOR RECIPIENTS AND SUBRECIPIENTS UNDER 2 CFR PART 200 (UNIFORM RULES) This checklist will assist the Texas General

TEXAS GENERAL LAND OFFICE COMMUNITY DEVELOPMENT & REVITALIZATION PROCUREMENT GUIDANCE FOR RECIPIENTS AND SUBRECIPIENTS UNDER 2 CFR PART 200 (UNIFORM RULES) This checklist will assist the Texas General

All CDBG Grantees Issued: October 18, Subject: Management of Community Development Block Grant Assisted Real Property

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT WASHINGTON, DC 20410-7000 OFFICE OF COMMUNITY PLANNING AND DEVELOPMENT Special Attention of: NOTICE: CPD-17-09 All CDBG Grantees Issued: October 18, 2017

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT WASHINGTON, DC 20410-7000 OFFICE OF COMMUNITY PLANNING AND DEVELOPMENT Special Attention of: NOTICE: CPD-17-09 All CDBG Grantees Issued: October 18, 2017

ADMINISTRATION & FINANCE August 2010 FEDERAL PROPERTY MANAGEMENT STANDARDS

[ FEDERAL PROPERTY MANAGEMENT STANDARDS 3-0127 ADMINISTRATION & FINANCE August 2010 1.01 The Director of Budget Operations through the Associate Vice President for Administration and Finance is designated

[ FEDERAL PROPERTY MANAGEMENT STANDARDS 3-0127 ADMINISTRATION & FINANCE August 2010 1.01 The Director of Budget Operations through the Associate Vice President for Administration and Finance is designated

HABITAT FOR HUMANITY OF THE MIDDLE KEYS, INC. Financial Statements. December 31, (With Independent Auditors Report Thereon)

") Financial Statements (With Independent Auditors Report Thereon) TABLE OF CONTENTS PAGE Independent Auditors Report 1-2 Financial Statements for the year ended Statement of Financial Position 3 Statement

Financial Statements (With Independent Auditors Report Thereon) TABLE OF CONTENTS PAGE Independent Auditors Report 1-2 Financial Statements for the year ended Statement of Financial Position 3 Statement

CITY OF BOISE HOUSING AND COMMUNITY DEVELOPMENT DIVISION CDBG MONITORING FORM

CITY OF BOISE HOUSING AND COMMUNITY DEVELOPMENT DIVISION CDBG MONITORING FORM GENERAL INFORMATION Date of Monitoring Visit: / / Number of Monitoring Visit for the Fiscal Year: # Subrecipient Name: Subgrantee

CITY OF BOISE HOUSING AND COMMUNITY DEVELOPMENT DIVISION CDBG MONITORING FORM GENERAL INFORMATION Date of Monitoring Visit: / / Number of Monitoring Visit for the Fiscal Year: # Subrecipient Name: Subgrantee

FLORIDA HOUSING FINANCE CORPORATION Tax Credit Assistance Program Project Selection Process and Criteria

FLORIDA HOUSING FINANCE CORPORATION Tax Credit Assistance Program Project Selection Process and Criteria On February 17, 2009, President Obama signed the American Recovery and Reinvestment Act of 2009

FLORIDA HOUSING FINANCE CORPORATION Tax Credit Assistance Program Project Selection Process and Criteria On February 17, 2009, President Obama signed the American Recovery and Reinvestment Act of 2009

*Charter references: Power of city to impose and collect tax on transfer of real property, subpart A,

ARTICLE III. REALTY TRANSFER TAX* Page 1 of8 ARTICLE III. REAL TV TRANSFER TAX* *Charter references: Power of city to impose and collect tax on transfer of real property, subpart A, 3. Sec. 102-71. Definitions.

ARTICLE III. REALTY TRANSFER TAX* Page 1 of8 ARTICLE III. REAL TV TRANSFER TAX* *Charter references: Power of city to impose and collect tax on transfer of real property, subpart A, 3. Sec. 102-71. Definitions.

Oregon Statutes Relevant to Quiet Water Home Owners Association

Oregon Statutes Relevant to Quiet Water Home Owners Association 1 1 1 1 0 1 0 1 0 1 PLANNED COMMUNITIES (General Provisions).0 Definitions for ORS.0 to.. As used in ORS.0 to.: (1) Assessment means any

Oregon Statutes Relevant to Quiet Water Home Owners Association 1 1 1 1 0 1 0 1 0 1 PLANNED COMMUNITIES (General Provisions).0 Definitions for ORS.0 to.. As used in ORS.0 to.: (1) Assessment means any

17 CFR Ch. II ( Edition)

") 229.1110 trustee s removal, replacement or resignation, as well as how the expenses associated with changing from one trustee to another trustee will be paid. Instruction to Item 1109. If multiple trustees

229.1110 trustee s removal, replacement or resignation, as well as how the expenses associated with changing from one trustee to another trustee will be paid. Instruction to Item 1109. If multiple trustees

CHAPTER 4.0: PARTICIPANT EXERCISES

Training CDBG Subrecipients in Administrative Systems CHAPTER 4.0: PARTICIPANT EXERCISES 4.1 Overview The questions and answers provided here are reproduced from the subrecipient handbook Playing by the

Training CDBG Subrecipients in Administrative Systems CHAPTER 4.0: PARTICIPANT EXERCISES 4.1 Overview The questions and answers provided here are reproduced from the subrecipient handbook Playing by the

PROPERTY MANAGEMENT. These procedures apply to all tangible, non-consumable equipment meeting all the following criteria;

PURPOSE To provide procedures and guidance to ensure University property is properly recorded, maintained and safeguarded, and that appropriate tracking and disposal methods are followed in accordance

PURPOSE To provide procedures and guidance to ensure University property is properly recorded, maintained and safeguarded, and that appropriate tracking and disposal methods are followed in accordance

Swift Academies Assets & Disposal Policy

Swift Academies Assets & Disposal Policy Accepted by: Board of Trustees March 2018 Approving Body : Board of Trustees Committee : Finance & Resources Review Cycle: 3 years Last reviewed: March 2018 Date

Swift Academies Assets & Disposal Policy Accepted by: Board of Trustees March 2018 Approving Body : Board of Trustees Committee : Finance & Resources Review Cycle: 3 years Last reviewed: March 2018 Date

Fixed Asset Policy and Procedure Manual

UNIVERSITY OF OREGON Fixed Asset Policy and Procedure Manual Draft Rob Freytag, Brett Giles, Bob Swanson, Teri Rowe, Shereé Johnson, George Baiting, Jennifer Creighton Neiwert 4/22/2010 In compliance with

UNIVERSITY OF OREGON Fixed Asset Policy and Procedure Manual Draft Rob Freytag, Brett Giles, Bob Swanson, Teri Rowe, Shereé Johnson, George Baiting, Jennifer Creighton Neiwert 4/22/2010 In compliance with

Accounting for Leases

Office: Business Services Procedure Contact: Director of Business Services Related Policy or Policies: Noted within procedure statement Revision History Revision Number: Change: Date: 001 Update content

Office: Business Services Procedure Contact: Director of Business Services Related Policy or Policies: Noted within procedure statement Revision History Revision Number: Change: Date: 001 Update content

HABITAT FOR HUMANITY OF GREATER NEW HAVEN, INC. AND SUBSIDIARY Consolidated Financial Statements December 31, 2009

HABITAT FOR HUMANITY OF GREATER NEW HAVEN, INC. AND SUBSIDIARY Consolidated Financial Statements December 31, 2009 HABITAT FOR HUMANITY OF GREATER NEW HAVEN, INC. AND SUBSIDIARY CONSOLIDATED FINANCIAL

HABITAT FOR HUMANITY OF GREATER NEW HAVEN, INC. AND SUBSIDIARY Consolidated Financial Statements December 31, 2009 HABITAT FOR HUMANITY OF GREATER NEW HAVEN, INC. AND SUBSIDIARY CONSOLIDATED FINANCIAL

Community Housing Development Organization (CHDO) Manual. Policies Requirements for Certification Requirements for Recertification

Manual. Policies Requirements for Certification Requirements for Recertification") Community Housing Development Organization (CHDO) Manual Policies Requirements for Certification Requirements for Recertification Kentucky Housing Corporation 1231 Louisville Road Frankfort, KY 40601 (502)

Community Housing Development Organization (CHDO) Manual Policies Requirements for Certification Requirements for Recertification Kentucky Housing Corporation 1231 Louisville Road Frankfort, KY 40601 (502)

ROCKFORD AREA HABITAT FOR HUMANITY, INC. FINANCIAL STATEMENTS and INDEPENDENT AUDITOR S REPORT. For the years ended June 30, 2014 and 2013

FINANCIAL STATEMENTS and INDEPENDENT AUDITOR S REPORT For the years ended June 30, 2014 and 2013 TABLE OF CONTENTS Independent Auditor s Report 1 Statements of Financial Position 2 Statements of Activities

FINANCIAL STATEMENTS and INDEPENDENT AUDITOR S REPORT For the years ended June 30, 2014 and 2013 TABLE OF CONTENTS Independent Auditor s Report 1 Statements of Financial Position 2 Statements of Activities

APPENDIX 'N' PROGRESS PAYMENTS FOR LARGE BUSINESS CONCERNS

12 April 1999 APPENDIX 'N' PROGRESS PAYMENTS FOR LARGE BUSINESS CONCERNS Progress payments shall be made to the Seller when requested as work progresses, but not more frequently than monthly in amounts

12 April 1999 APPENDIX 'N' PROGRESS PAYMENTS FOR LARGE BUSINESS CONCERNS Progress payments shall be made to the Seller when requested as work progresses, but not more frequently than monthly in amounts

FLORIDA CONSTITUTION

FLORIDA CONSTITUTION (Provisions related to ad valorem property taxes and exemptions) ARTICLE VII - FINANCE AND TAXATION SECTION 2. Taxes; rate.-- All ad valorem taxation shall be at a uniform rate within

FLORIDA CONSTITUTION (Provisions related to ad valorem property taxes and exemptions) ARTICLE VII - FINANCE AND TAXATION SECTION 2. Taxes; rate.-- All ad valorem taxation shall be at a uniform rate within

State of Rhode Island. National Housing Trust Fund Allocation Plan. July 29, 2016

HTF Program: Method of Distribution State of Rhode Island National Housing Trust Fund Allocation Plan July 29, 2016 The Housing Trust Fund (HTF) is a new affordable housing production program that will

HTF Program: Method of Distribution State of Rhode Island National Housing Trust Fund Allocation Plan July 29, 2016 The Housing Trust Fund (HTF) is a new affordable housing production program that will

LIHPRHA, Pub. L. No , Title VI (1990), codified at 12 U.S.C et seq.

, codified at 12 U.S.C et seq.") LIHPRHA, Pub. L. No. 101-625, Title VI (1990), codified at 12 U.S.C. 4101 et seq. TITLE VI--PRESERVATION OF AFFORDABLE RENTAL HOUSING Subtitle A--Prepayment of Mortgages Insured Under National Housing

LIHPRHA, Pub. L. No. 101-625, Title VI (1990), codified at 12 U.S.C. 4101 et seq. TITLE VI--PRESERVATION OF AFFORDABLE RENTAL HOUSING Subtitle A--Prepayment of Mortgages Insured Under National Housing

EITF ABSTRACTS. [Nullified by FIN 46 and FIN 46(R) for entities within the scope of FIN 46 or FIN 46(R)]

![EITF ABSTRACTS. [Nullified by FIN 46 and FIN 46(R) for entities within the scope of FIN 46 or FIN 46(R)]](/thumbs/83/87695858.jpg "EITF ABSTRACTS. [Nullified by FIN 46 and FIN 46(R) for entities within the scope of FIN 46 or FIN 46(R)]") EITF ABSTRACTS Issue No. 90-15 Title: Impact of Nonsubstantive Lessors, Residual Value Guarantees, and Other Provisions in Leasing Transactions [Nullified by FIN 46 and FIN 46(R) for entities within the

EITF ABSTRACTS Issue No. 90-15 Title: Impact of Nonsubstantive Lessors, Residual Value Guarantees, and Other Provisions in Leasing Transactions [Nullified by FIN 46 and FIN 46(R) for entities within the

DATE: TO OWNER: Washington State Housing Finance Commission Low-Income Housing Tax Credit Program 1000 Second Avenue Suite 2700 Seattle WA

INDEPENDENT CERTIFIED PUBLIC ACCOUNTANT'S REPORT on CARRYOVER ALLOCATION BASIS PURSUANT TO IRS SECTION 42 (h)(1)(e)(ii) and AMERICAN RECOVERY AND REINVESTMENT ACT (ARRA) EXCHANGE PROGRAM 30% TEST PURSUANT

INDEPENDENT CERTIFIED PUBLIC ACCOUNTANT'S REPORT on CARRYOVER ALLOCATION BASIS PURSUANT TO IRS SECTION 42 (h)(1)(e)(ii) and AMERICAN RECOVERY AND REINVESTMENT ACT (ARRA) EXCHANGE PROGRAM 30% TEST PURSUANT

VIRGINIA HOUSING DEVELOPMENT AUTHORITY COST CERTIFICATION GUIDE FOR MORTGAGORS, CONTRACTORS AND CERTIFIED PUBLIC ACCOUNTANTS

VIRGINIA HOUSING DEVELOPMENT AUTHORITY COST CERTIFICATION GUIDE FOR MORTGAGORS, CONTRACTORS AND CERTIFIED PUBLIC ACCOUNTANTS February l, l98l (Amended September 1, 1984, September 1, 1992, December 1,

VIRGINIA HOUSING DEVELOPMENT AUTHORITY COST CERTIFICATION GUIDE FOR MORTGAGORS, CONTRACTORS AND CERTIFIED PUBLIC ACCOUNTANTS February l, l98l (Amended September 1, 1984, September 1, 1992, December 1,

ACCOUNTING FOR CAPITAL ASSETS. Presented by: Joel Knopp, CPA Shareholder

ACCOUNTING FOR CAPITAL ASSETS Presented by: Joel Knopp, CPA Shareholder Agenda Definition Reporting Capital Assets Questions from Implementation Guides Modified Approach Interest Capitalization Intangibles

ACCOUNTING FOR CAPITAL ASSETS Presented by: Joel Knopp, CPA Shareholder Agenda Definition Reporting Capital Assets Questions from Implementation Guides Modified Approach Interest Capitalization Intangibles

EN Official Journal of the European Union L 320/373

29.11.2008 EN Official Journal of the European Union L 320/373 INTERNATIONAL FINANCIAL REPORTING STANDARD 3 Business combinations OBJECTIVE 1 The objective of this IFRS is to specify the financial reporting

29.11.2008 EN Official Journal of the European Union L 320/373 INTERNATIONAL FINANCIAL REPORTING STANDARD 3 Business combinations OBJECTIVE 1 The objective of this IFRS is to specify the financial reporting

Section 1.16a Resale/Deed Restrictions Guidelines

Section 1.16a Resale/Deed Restrictions Guidelines In This Section This section contains the following topics: Overview... 2 Introduction... 2 Related Bulletins... 2 General... 2 Identification and Eligibility

Section 1.16a Resale/Deed Restrictions Guidelines In This Section This section contains the following topics: Overview... 2 Introduction... 2 Related Bulletins... 2 General... 2 Identification and Eligibility

Section by Section Summary of the 2013 HOME Final Rule

Section by Section Summary of the 2013 HOME Final Rule The Section by Section Summary of the 2013 HOME Final Rule summarizes all the changes made to the HOME regulations to help participating jurisdictions,

Section by Section Summary of the 2013 HOME Final Rule The Section by Section Summary of the 2013 HOME Final Rule summarizes all the changes made to the HOME regulations to help participating jurisdictions,

The United States Department of Transportation (USDOT) Standard Title VI/Non-Discrimination Assurances. DOT Order No A

Standard Title VI/Non-Discrimination Assurances. DOT Order No A") The United States Department of Transportation (USDOT) Standard Title VI/Non-Discrimination Assurances DOT Order No. 1050.2A The (Title of Subrecipient) (herein referred to as the Subrecipient ), HEREBY

The United States Department of Transportation (USDOT) Standard Title VI/Non-Discrimination Assurances DOT Order No. 1050.2A The (Title of Subrecipient) (herein referred to as the Subrecipient ), HEREBY

NEWTOWN SCHOOL FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER

NEWTOWN SCHOOL FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2016 School Address: Mein Street, Newtown, Wellington School Postal Address: Mein Street, Newtown, WELLINGTON, 6021 School Phone: 04 389

NEWTOWN SCHOOL FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2016 School Address: Mein Street, Newtown, Wellington School Postal Address: Mein Street, Newtown, WELLINGTON, 6021 School Phone: 04 389

Leases. (a) the lease transfers ownership of the asset to the lessee by the end of the lease term.

the lease transfers ownership of the asset to the lessee by the end of the lease term.") Leases 1.1. Classification of leases A lease is classified as a finance lease if it transfers substantially all the risks and rewards incidental to ownership. A lease is classified as an operating lease

Leases 1.1. Classification of leases A lease is classified as a finance lease if it transfers substantially all the risks and rewards incidental to ownership. A lease is classified as an operating lease

NSP DEVELOPER ARRESALE PROGRAM PROCEDURES

NSP DEVELOPER ARRESALE PROGRAM PROCEDURES HERA 2301(c)(3)(B) purchase and rehabilitate homes and residential properties that have been abandoned or foreclosed upon, in order to sell, rent, or redevelop

NSP DEVELOPER ARRESALE PROGRAM PROCEDURES HERA 2301(c)(3)(B) purchase and rehabilitate homes and residential properties that have been abandoned or foreclosed upon, in order to sell, rent, or redevelop

CHAPTER Senate Bill No. 4-D

CHAPTER 2007-339 Senate Bill No. 4-D An act relating to ad valorem taxation; authorizing the Department of Revenue to adopt emergency rules; providing for application and renewal thereof; requiring the

CHAPTER 2007-339 Senate Bill No. 4-D An act relating to ad valorem taxation; authorizing the Department of Revenue to adopt emergency rules; providing for application and renewal thereof; requiring the

CITY OF SEASIDE. Infrastructure and Fixed Asset Capitalization and Inventory Control Policy PURPOSE

PURPOSE The purpose of this policy is to ensure adequate control, appropriate use of, and proper reporting of the City s infrastructure assets and fixed assets. This policy and the related procedures are

PURPOSE The purpose of this policy is to ensure adequate control, appropriate use of, and proper reporting of the City s infrastructure assets and fixed assets. This policy and the related procedures are

Rental Housing Compliance for the NSP Development & Affordability Period May 17, 2011

U.S. Department of Housing and Urban Development Rental Housing Compliance for the NSP Development & Affordability Period May 17, 2011 Speakers and Format Speakers David Noguera, HUD Virginia Sardone,

U.S. Department of Housing and Urban Development Rental Housing Compliance for the NSP Development & Affordability Period May 17, 2011 Speakers and Format Speakers David Noguera, HUD Virginia Sardone,

The joint leases project change is coming

No. 2010-4 18 June 2010 Technical Line Technical guidance on standards and practice issues The joint leases project change is coming What you need to know The proposed changes to the accounting for leases

No. 2010-4 18 June 2010 Technical Line Technical guidance on standards and practice issues The joint leases project change is coming What you need to know The proposed changes to the accounting for leases

Sri Lanka Accounting Standard-LKAS 17. Leases

Sri Lanka Accounting Standard-LKAS 17 Leases -516- Sri Lanka Accounting Standard-LKAS 17 Leases Sri Lanka Accounting Standard LKAS 17 Leases is set out in paragraphs 1 69. All the paragraphs have equal

Sri Lanka Accounting Standard-LKAS 17 Leases -516- Sri Lanka Accounting Standard-LKAS 17 Leases Sri Lanka Accounting Standard LKAS 17 Leases is set out in paragraphs 1 69. All the paragraphs have equal

2. Our community wants to demolish some blighted properties. How can we meet a CDBG national objective with this activity?

ENTITLEMENT CDBG PROGRAM FAQs ON MEETING A NATIONAL OBJECTIVE WITH ACQUISITION, DEMOLITION, AND DISPOSITION 1. What are the basic principles to meet eligibility and national objective requirements? As

ENTITLEMENT CDBG PROGRAM FAQs ON MEETING A NATIONAL OBJECTIVE WITH ACQUISITION, DEMOLITION, AND DISPOSITION 1. What are the basic principles to meet eligibility and national objective requirements? As

Appendix C to Part 37-What is the Desired Coverage for Periodic Audits of For-Profit Participants to be Audited by IPAs?

Appendix C to Part 37-What is the Desired Coverage for Periodic Audits of For-Profit Participants to be Audited by IPAs? You may provide the following guidance to a for-profit participant and its IPA on

Appendix C to Part 37-What is the Desired Coverage for Periodic Audits of For-Profit Participants to be Audited by IPAs? You may provide the following guidance to a for-profit participant and its IPA on

FPP Committee Meeting Proposed COA Changes. June 8, 2018

FPP Committee Meeting Proposed COA Changes June 8, 2018 Agenda Visit various GASB Statements COA changes needed GASB #84 Fiduciary Activities Statement No. 84 Fiduciary Activities How many currently report

FPP Committee Meeting Proposed COA Changes June 8, 2018 Agenda Visit various GASB Statements COA changes needed GASB #84 Fiduciary Activities Statement No. 84 Fiduciary Activities How many currently report

Chapter 8 VALUATION OF AND INFORMATION ON PROPERTIES. Definitions

Chapter 8 VALUATION OF AND INFORMATION ON PROPERTIES Definitions 8.01 In this Chapter:- (1) carrying amount means, for an applicant, the amount at which an asset is recognised in the most recent audited

Chapter 8 VALUATION OF AND INFORMATION ON PROPERTIES Definitions 8.01 In this Chapter:- (1) carrying amount means, for an applicant, the amount at which an asset is recognised in the most recent audited

This Contract is entered into by the Regional Access Mobility Program of Montana, Inc. (the Grantee), and the City of Missoula, Montana, (the City).

, and the City of Missoula, Montana, (the City).") CFDA NO. 14.218 COMMUNITY DEVELOPMENT BLOCK GRANT CONTRACT CONTRACT #10-09 This Contract is entered into by the Regional Access Mobility Program of Montana, Inc. (the Grantee), and the City of Missoula,

CFDA NO. 14.218 COMMUNITY DEVELOPMENT BLOCK GRANT CONTRACT CONTRACT #10-09 This Contract is entered into by the Regional Access Mobility Program of Montana, Inc. (the Grantee), and the City of Missoula,

SSAP 14 STATEMENT OF STANDARD ACCOUNTING PRACTICE 14 LEASES

SSAP 14 STATEMENT OF STANDARD ACCOUNTING PRACTICE 14 LEASES (Issued October 1987; revised February 2000) The standards, which have been set in bold italic type, should be read in the context of the background

SSAP 14 STATEMENT OF STANDARD ACCOUNTING PRACTICE 14 LEASES (Issued October 1987; revised February 2000) The standards, which have been set in bold italic type, should be read in the context of the background

Real Estate Syndication Income 19,451 NOTE

Real Estate Syndication Income 19,451 Section 10,500 Statement of Position 92-1 Accounting for Real Estate Syndication Income February 6, 1992 NOTE Statements of Position of the Accounting Standards Division

Real Estate Syndication Income 19,451 Section 10,500 Statement of Position 92-1 Accounting for Real Estate Syndication Income February 6, 1992 NOTE Statements of Position of the Accounting Standards Division

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION SENATE DRS35055-LTz-20A* (2/14)

") S GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 0 SENATE DRS0-LTz-A* (/) D Short Title: Revise UCC Article on Bulk Transfers. Sponsors: Senator Hartsell. Referred to: (Public) A BILL TO BE ENTITLED AN ACT

S GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 0 SENATE DRS0-LTz-A* (/) D Short Title: Revise UCC Article on Bulk Transfers. Sponsors: Senator Hartsell. Referred to: (Public) A BILL TO BE ENTITLED AN ACT

Differences, Procurement and

U.S. Department of Housing and Urban Development Developers and Subrecipients: Differences, Procurement and Other Rules July 24, 2012 2:00 PM EDT Community Planning and Development Purpose of Webinar To

U.S. Department of Housing and Urban Development Developers and Subrecipients: Differences, Procurement and Other Rules July 24, 2012 2:00 PM EDT Community Planning and Development Purpose of Webinar To

LEON COUNTY, FLORIDA

LEON COUNTY, FLORIDA SHIP LOCAL HOUSING ASSISTANCE PLAN (LHAP) FISCAL YEARS COVERED 2014-2015, 2015-2016, 2016-2017 Technical Amendments: 12/19/16 1. Strategy: Housing Replacement 2. Strategy: Disaster

LEON COUNTY, FLORIDA SHIP LOCAL HOUSING ASSISTANCE PLAN (LHAP) FISCAL YEARS COVERED 2014-2015, 2015-2016, 2016-2017 Technical Amendments: 12/19/16 1. Strategy: Housing Replacement 2. Strategy: Disaster