LEASES & HOT TOPICS PRESENTED BY: JASON MYERS & BRYAN CALLAHAN

|

|

|

- Penelope Julianna Jefferson

- 6 years ago

- Views:

Transcription

1 LEASES & HOT TOPICS PRESENTED BY: JASON MYERS & BRYAN CALLAHAN

2 LEASES PROJECT Summary of Key Changes & Impact 2

3 KEY CHANGES Lessee (the contractor usually) Requires recognition of most leases on their balance sheets as lease liabilities with corresponding right-of-use (ROU) assets Recognize expenses on their income statements in a manner similar to today s accounting Requires impairment testing for new ROU assets 3

4 KEY CHANGES Lessor (the equipment company, landlord, etc.) Aligns certain classification criteria & accounting guidance with lessee guidance & with the revenue recognition model in Topic 606 Includes an assessment of collectability to support classification as a direct financing lease & de-recognize asset & record revenue for sales-type lease Eliminates today s real estate-specific provisions for all entities Leveraged lease accounting not permitted for new transactions or existing transactions modified after the effective date 4

5 EFFECTIVE DATES Effective January 1, 2019 (public entity), including interim periods within those years, for any of the following: 1. Public business entities 2. A not-for-profit entity that has issued, or is a conduit bond obligor for securities that are traded, listed, or quoted on an exchange or an over-the-counter market 3. An employee benefit plan that files financial statements with the SEC For all other entities, the amendments are effective for fiscal years beginning after December 15, 2019 (2020 calendar year end), & interim periods within fiscal years beginning after December 15, All entities may early adopt 5

6 DETERMINING WHETHER A LEASE EXISTS Under the standard, a contract is or contains a lease if it conveys the right to control the use of identified property, plant or equipment (an identified asset) for a period of time in exchange for consideration An entity is required to reassess whether a contract is or contains a lease only if the terms & conditions of the contract are changed 6

7 RIGHT TO CONTROL THE USE OF THE ASSET A lease contract conveys the right to control the use of the identified asset for a specified period of time. A customer controls an identified asset when the customer has both of the following: Customer has right to direct its use (e.g. the right to direct how & for what purpose the asset is used, including the right to change how & for what purpose the asset is used) Customer has right to obtain substantially all economic benefits from its use 7

8 MULTIPLE LEASE COMPONENTS Both lessees & lessors will be required to separate lease & nonlease (service) components of a contract, & allocate contract consideration to each component Lessees will perform allocation based on observable relative standalone price basis Lessors will allocate the transaction price to separate performance obligations aligned with guidance in the new revenue recognition standard Components include only those items or activities that transfer a good or service to the lessee Lessees are permitted to make accounting policy election (by class of underlying asset) to account for lease & non-lease components as single lease component 8

9 SUBCONTRACT VS. LEASE? GC building new 15 story apartment building Subcontract for tower crane & operator GC controls scheduling of lifts on tower crane 24 month estimated construction period 9

10 LESSEE CLASSIFICATION Classification of leases is based on criteria in International Accounting Standards (IAS) 17 (similar to existing U.S. GAAP regarding capital vs. operating lease) Classification will be determined in accordance with the principles in current lease requirements, but without the bright-line tests (e.g. by determining whether a lease is effectively an installment purchase by the lessee) Lease will be classified finance lease if it transfers substantially all risks & rewards incident to ownership (meets one of the 5 criteria on the next page) All other leases will be classified as operating leases by lessee Classification continues to contain no bright-line criteria, but contains one additional criterion regarding the specialized nature of the underlying asset 10

11 FINANCE LEASE CRITERIA (SALES-TYPE FOR LESSOR) 1. Ownership of asset transfers to lessee by end of lease term 2. Lessee has option to purchase asset at price which is expected to be sufficiently lower than FV at date option becomes exercisable such that it is reasonably certain option will be exercised 3. Lease term is for major part of the economic life of asset Lessees (& lessors) are afforded an exception to the lease classification test & do not need to consider this criterion for leases that commence at or near the end of the underlying asset s economic life (e.g. in the final 25% of an asset s economic life). 4. PV of minimum lease payments amounts to at least substantially all of fair value of leased asset 5. NEW: The underlying asset is of such a specialized nature that it is expected to have no alternative use to the lessor at the end of the lease term 11

12 LESSEE CLASSIFICATION Lessee is required to reassess lease classification throughout the lease term upon the occurrence of: A change in lease term A change in the lessee s assessment of whether it is reasonably certain to exercise an option to purchase the underlying asset Contract modification that is not accounted for as a separate lease 12

13 LESSEE ACCOUNTING INITIAL MEASUREMENT All leases result in a liability for its lease obligation & an asset representing a lessee s right to use the underlying asset for the lease term Amount initially recorded as an ROU asset & lease liability is computed the same regardless of whether the lease is classified as an operating lease or as a finance lease The recognition, measurement, & presentation of expenses & cash flows arising from a lease by a lessee have not significantly changed from previous GAAP. 13

14 INITIAL MEASUREMENT OF LESSEE ROU ASSET & LEASE LIABILITIES Begin by measuring lease liability & make adjustments to get to ROU asset Lease liability = present value of future lease payments, using the effective interest method to subsequently account for the lease liability ROU asset = Lease liability + Initial direct expenses* + Payments made at or before lease commencement - Lessor-provided incentives *Incremental costs of a lease that would not have been incurred if the lease had not been obtained 14

15 LESSEE MODEL SUBSEQUENT ACCOUNTING Annual expense recognition & subsequent amortization of ROU asset depends on lease classification & accounting approach: A change in lease term Front-loaded expense pattern similar to today s capital leases with interest & amortization recognized separately Interest determined on the lease liability in each period during the lease term as the amount that produces a constant periodic discount rate ROU asset generally amortized on a straight-line basis Operating lease approach: Straight-line expense recognition similar to today s operating leases ROU Asset: Reduced by the difference between the lease expense & the interest cost on the lease liability 15

16 COMPARISON OF LESSEE ACCOUNTING MODELS Finance Lease Operating Lease Balance Sheet Balance Sheet Right of Use (ROU) Asset* Right of Use (ROU) Asset** Lease Liability Lease Liability Income Statement Interest Expense (on lease liability) Amortization Expense (on ROU asset) Income Statement Lease/Rent Expense (straightline) Cash Flow Cash paid for principal payments (financing activities) & interest payments (operating activities) *Periodically reduced by straight-line amortization Cash Flow Cash paid for lease payments **Periodically reduced by the difference between straight-line lease expense & interest cost on lease liability, i.e., plug figure 16

17 LEASE EXAMPLE Three-year lease term at $25,000 per year rent Lessee s incremental borrowing rate of 6% 17

18 LESSEE EXAMPLE LEASE LIABILITY Begin by calculating lease liability (net present value of lease payments) Same for finance & operating lease In subsequent years, lease liability is reduced by discounted lease payments Analysis of Liability to Make Lease Payments Beginning Balance $ (66,825) Year 1 interest ($66,825 *.06) $ (4,010) Year 1 lease payment 25,000 Balance at end of year 1 (45,835) Year 2 interest ($45,835 *.06) (2,750) Year 2 lease payment 25,000 Balance at end of year 2 (23,585) Year 3 interest ($23,585 *.06) (1,415) Year 3 lease payment 25,000 Balance at end of year 3-18

19 LESSEE EXAMPLE ROU ASSET FINANCE LEASE Beginning ROU asset is measured same as lease liability (plus initial direct expenses & other adjustments, as applicable) In subsequent years, amortize ROU asset evenly over three-year lease term (66,825/3) Analysis of Right-of-Use Asset Beginning Balance $ 66,825 Year 1 amortization ($66,825/3) $ 22,275 Balance at end of year 1 44,550 Year 2 amortization ($66,825/3) 22,275 Balance at end of year 2 22,275 Year 3 amortization ($66,825/3) 22,275 Balance at end of year 3-19

20 LESSEE EXAMPLE ROU ASSET OPERATING LEASE Initial measurement same as finance lease ROU asset In subsequent years, reduce ROU asset by difference between straightline lease expense & interest cost of lease liability Analysis of Right-of-Use Asset Beginning Balance $ 66,825 Year 1 accretion of lease liability (interest) $ 4,010 Year 1 lease expense ($75,000/3) (25,000) Balance at end of year 1 45,835 Year 2 accretion of lease liability (interest) 2,750 Year 2 lease expense ($75,000/3) (25,000) Balance at end of year 2 23,585 Year 3 accretion of lease liability (interest) 1,415 Year 3 lease expense ($75,000/3) (25,000) Balance at end of year 3-20

21 LEASE TERM Lease term is the non-cancelable period in which the lessee has the right to use an underlying asset, plus optional periods for which, after considering all relevant factors that may give lessee economic incentive to renew or terminate, it is reasonably certain that the lessee will: exercise the renewal option, or not exercise the termination option, or in which the exercise of those options is controlled by the lessor. 21

22 LEASE TERM Lessees will be required to reassess the lease term or a lessee option to purchase the underlying asset if & when the following occurs: 1. Upon the occurrence of significant event or change in circumstances directly attributable to actions of lessee that affects whether the lessee is reasonably certain to exercise or not to exercise an option to extend or terminate the lease, or to purchase the underlying asset (e.g. lessee makes significant modifications or customizations to the underlying asset) 2. The lessee elects to exercise (or not exercise) an option to extend or terminate the lease even though it had previously determined it was not reasonably certain to do so, or the contract term obliges the lessee to do so 22

23 INCEPTION DATE VS. COMMENCEMENT DATE Lease commencement is the date a lessor makes an underlying asset available for use to a lessee, & is the date for classification, recognition, & measurement The determination of whether a contract is a lease or contains a lease is done at the inception date Lease classification, recognition, & measurement are determined at the lease commencement date 23

24 DISCOUNT RATE Lessee uses the rate charged by the lessor if readily determinable (not likely) If not, use their incremental borrowing rate at lease commencement Lessor uses rate it charges lessee to discount its lease-related assets Lessees not public business entities may make accounting policy election to use a risk-free rate for initial & subsequent measurement of lease liabilities 24

25 LEASE PAYMENTS Includes: 1. Fixed payments 2. Variable lease payments linked to index or rate (e.g. CPI) Includes in-substance fixed payments 3. Amounts probable of being owed under a residual value guarantee (for lessees); full amounts at which residual assets are guaranteed by a lessee or by a third party (for lessor) 4. Payments related to renewal, termination or purchase options that the lessee is reasonably certain to exercise (consistent with the lease term) 5. Fees paid by the lessee to the owners of a special-purpose entity for structuring the transaction. 25

26 LESSEE BALANCE SHEET PRESENTATION Assets Present finance lease ROU assets & operating lease ROU assets as separate line items on face of balance sheet, or disclose in notes which line items in balance sheet include finance lease ROU assets & operating lease ROU assets Finance lease ROU assets cannot be presented in the same line item as operating lease ROU assets Liabilities Same separate presentation requirements as ROU assets Current liabilities will include payments due in next 12 months *Look out for working capital impact 26

27 DISCLOSURES Disclosures are required by lessees & lessors to meet a disclosure objective, which would enable users of financial statements to assess amount, timing, & uncertainty of cash flows arising from leases Requires qualitative disclosures along with specific quantitative disclosures Intent is to require enough information to supplement the amounts recorded in the financial statements so that users can understand more about the nature of an entity s leasing activities Entities will consider level of detail necessary to satisfy disclosure objective Entities will provide transition disclosures 27

28 TRANSITION Entities will use modified retrospective approach (assets & liabilities measured at implementation date over remaining life of lease; specific guidance provided) Lessees - Transition method applies to all capital & operating leases Lessors - Applies to all sales-type, direct financing & operating leases (leveraged leases grandfathered, but otherwise phased out) Applies to all outstanding leases, not just new leases Specific transition guidance for sale & leaseback transactions, build-to-suit transactions, leveraged leases, & amounts previously recognized under business combinations guidance for leases 28

29 TRANSITION PRACTICAL EXPEDIENTS FASB tentatively decided entity can choose to elect set of three specifically defined practical expedients all three or none must be used 1. Lessee (or lessor) need not reassess whether any expired or existing contracts are or contain leases 2. Lessee (or lessor) need not reassess the lease classification for any expired or existing lease (capital leases will be classified as finance leases, & operating leases will classified as operating leases) 3. Lessee (or lessor) need not reassess initial direct costs for any existing lease May also elect another, separate, practical expedient to use hindsight in evaluating lessee options to extend or terminate a lease or to purchase the underlying asset 29

30 IMPACT ON ACCOUNTING & REPORTING Policies, Processes & Controls Inventory & assessment of all agreements/contracts Significantly amend accounting policies & procedures Applies to all outstanding leases, not just new leases Ongoing remeasurement requirements, e.g., index or rate changes, modification to contract terms, lessee s assessment of options to extend or terminate, or purchase underlying asset Increased disclosure requirements Definitions requiring management s judgment, e.g., definition of lease, lease term, terminology, e.g., insignificant, reasonably certain, substantially all, & book vs. tax differences Internal control changes with policy & process changes 30

31 31 HOT TOPICS

32 Success in Applying Analytics = Becoming an Insight-Driven Organization 32

33 Definition of Analytics: analysis methods designed to extract useful information for answering strategic questions... 33

34 DATA VOLUMES ARE INCREASING Source: 34

35 HARNESSING DATA Key Performance Indicators (KPIs) What is a Key Performance Indicator? A performance measurement used to evaluate project & organizational success Quantifiable measurements that reflect the critical success factors of an organization Used to monitor & modify staff activities & results Can be financial or non-financial Benefits of KPIs Align your organization to meet vital objectives Make better decisions 35

36 OPERATIONAL KPI EXAMPLES Cost codes approaching or over budget (actual & committed) Labor hours or cost exceeding budget Productivity below estimate Change requests overdue Defects found Safety incidents Rent roll Repairs & maintenance by division/property Name yours! 36

37 Can you impact growth & profitability with KPI s? Yes but it s not simple Is your Organization innovative & imaginative find what drives growth Or content as followers, even if you re fast Where can the improvement come from? Better planning & forecasting Margin by property & unit Repairs by property & unit Property by property comparison Set goals for growth Goal #1 increase working capital in the next quarter by $XXX,000 KPI current ratio, acid ratio, contract margin, revenue per day Goal #2 increase average margin on contract revenue by 2% in the next quarter KPI average margin by customer, average margin by contract, average margin on new bids Goal #3 reduce the average labor hours on rework by 10% in the next quarter KPI rework labor hours per dollar of contract revenue, rework dollars as a % of total contract costs 37

38 38 Emerging Technologies

39 Standard Analysis (Excel, Access) Tools Data Analytics (ACL, IDEA, Arbutus) Data Visualization (Tableau, Analysts Notebook) Artificial Intelligence (Machine Learning, Social Media, Sentiment)

40 Structured Data Analytics Unstructured Data Analytics Visual Analytics Relationship Mapping Techniques

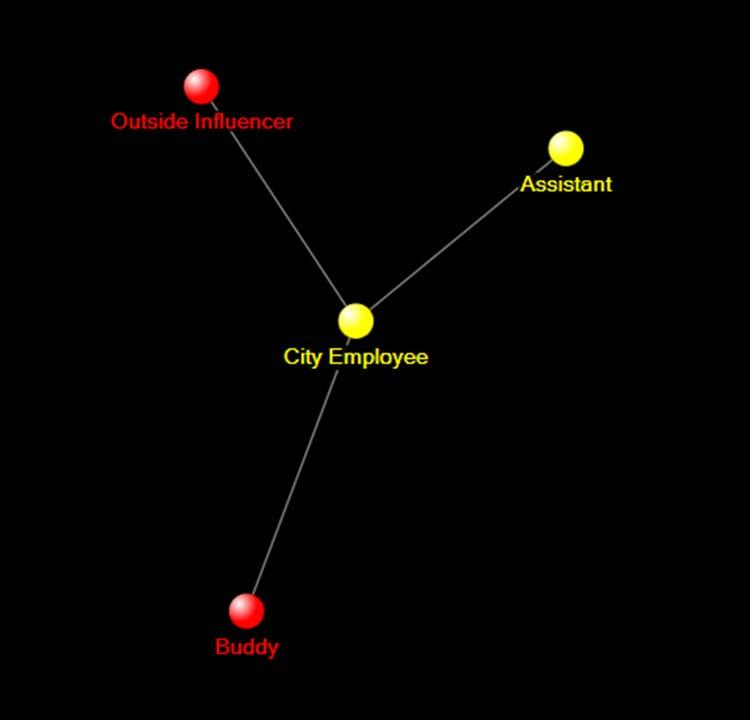

41 NEW & DEVELOPING TECHNOLOGIES Textual analytics Machine learning Supervised Unsupervised Advanced analytics Regression Predictive 41

42 Relationship Mapping Tone Detection Named Entity Extraction Textual Analytics Digital Forensics Predictive Coding Topic Mapping

43 DATA TYPES 43

44

45

46 DEGREE 46

47 BETWEENNESS CENTRALITY 47

48 TEXTUAL ANALYTICS AT WORK 48

49 TEXTUAL ANALYTICS AT WORK ES [9:50 AM]: cable? CV [9:50 AM]: yes, so that helps. i never submit for it though. lol ES [9:51 AM]: lol, you want my company credit card number? we could autobill it :) CV [9:52 AM]: :) it's ok. i'll do it eventually. i don't think any of us work here for the money lol ES [9:52 AM]: let me know. i'm burning that thing up 49

50 IT CAN EVEN CATCH From: MF 3/19/2010 To: ES Subject: I am happy and distraught. Happy for you, distraught for me :) Who will take care of me?? I will be adrift and unloved. Seriously, I hope that you are happy at Company A and you already know you can work for Ryan so it should be a smooth transition. I just want you to know how much I truly appreciated everything you have done for me and my team. You will be missed... 50

51 MANAGING YOUR REPUTATION How are you viewed in market? What are your customers saying? What can you do to control conversation? 51

52 EMOTIONS: TONE DETECTION & SENTIMENT 52

53 EMOTIONS: TONE DETECTION & SENTIMENT Anger Frustration Anxiety/Nervous Tension Vague/evasive Conspiratorial Sadness Intimacy Positive Negative 53

54 54

55 NEW MINDSET Communications & corporate assets are used to transact business Financial systems are used to transact business Transacting business = business transaction 55

56

57 Jason Myers, CPA // Partner //

Executive Summary. New leases standard Lessees

Executive Summary December 2018 The new leases standard focuses on increased transparency and comparability providing financial statement users with more information about an entity s leasing activities.

Executive Summary December 2018 The new leases standard focuses on increased transparency and comparability providing financial statement users with more information about an entity s leasing activities.

The New Lease Accounting Standard. Hunter Mink, CPA, CCIFP Brian Rosenberg, CPA, MBA

The New Lease Accounting Standard Hunter Mink, CPA, CCIFP Brian Rosenberg, CPA, MBA 1 Agenda Introduction Lease Identification and Classification Lessee Accounting Other Considerations Disclosures Impact

The New Lease Accounting Standard Hunter Mink, CPA, CCIFP Brian Rosenberg, CPA, MBA 1 Agenda Introduction Lease Identification and Classification Lessee Accounting Other Considerations Disclosures Impact

2018 Accounting & Auditing Update P R E S E N T E D B Y : D A N I E L L E Z I M M E R M A N & A N D R E A S A R T I N

2018 Accounting & Auditing Update P R E S E N T E D B Y : D A N I E L L E Z I M M E R M A N & A N D R E A S A R T I N AGENDA Leases FASB & GASB Revenue Recognition FASB 2 FASB ASU 2016-02, Leases (Topic

2018 Accounting & Auditing Update P R E S E N T E D B Y : D A N I E L L E Z I M M E R M A N & A N D R E A S A R T I N AGENDA Leases FASB & GASB Revenue Recognition FASB 2 FASB ASU 2016-02, Leases (Topic

Center for Plain English Accounting

Report April 18, 2018 Center for Plain English Accounting AICPA s National A&A Resource Center Debits and Credits Associated with New Lease Accounting Standard CPEA Lease Standard Implementation Series

Report April 18, 2018 Center for Plain English Accounting AICPA s National A&A Resource Center Debits and Credits Associated with New Lease Accounting Standard CPEA Lease Standard Implementation Series

Miles CPA Review: FAR Updates

Miles CPA Review: FAR - 2019 Updates Summary of updates: - FAR-4.4: s [ASC 842] effective fiscal years beginning after Dec 15, 2018 (for issuers) and effective fiscal years beginning after Dec 15, 2019

Miles CPA Review: FAR - 2019 Updates Summary of updates: - FAR-4.4: s [ASC 842] effective fiscal years beginning after Dec 15, 2018 (for issuers) and effective fiscal years beginning after Dec 15, 2019

Impact of lease accounting changes to corporate real estate

Impact of lease accounting changes to corporate real estate Overview In February 2016, the Financial Accounting Standards Board (FASB) issued its long-awaited revision to lease accounting Accounting Standards

Impact of lease accounting changes to corporate real estate Overview In February 2016, the Financial Accounting Standards Board (FASB) issued its long-awaited revision to lease accounting Accounting Standards

Leases: Overview of the new guidance

Leases: Overview of the new guidance Prepared by: Richard Stuart, Partner, National Professional Standards Group, RSM US LLP richard.stuart@rsmus.com, +1 203 905 5027 March 2, 2016 Introduction On February

Leases: Overview of the new guidance Prepared by: Richard Stuart, Partner, National Professional Standards Group, RSM US LLP richard.stuart@rsmus.com, +1 203 905 5027 March 2, 2016 Introduction On February

Implementing the New Lease Guidance

Implementing the New Lease Guidance October 22, 2018 2018 Crowe LLP 2018 Crowe LLP Agenda Background Scope Effective dates & transition requirements Lessee accounting model Lessor accounting model Specialized

Implementing the New Lease Guidance October 22, 2018 2018 Crowe LLP 2018 Crowe LLP Agenda Background Scope Effective dates & transition requirements Lessee accounting model Lessor accounting model Specialized

Technical Line FASB final guidance

No. 2016-09 14 April 2016 Technical Line FASB final guidance How the FASB s new leases standard will affect health care entities In this issue: Overview... 1 Key considerations... 3 Scope and scope exceptions...

No. 2016-09 14 April 2016 Technical Line FASB final guidance How the FASB s new leases standard will affect health care entities In this issue: Overview... 1 Key considerations... 3 Scope and scope exceptions...

New leases standard ASC 842 Lessee - operating leases. Itai Gotlieb, Partner, Professional Practice July 2017

ASC 842 Lessee - operating leases Itai Gotlieb, Partner, Professional Practice July 2017 Overview Under Accounting Standards Codification (ASC) 842, Leases, lessees recognize assets and liabilities for

ASC 842 Lessee - operating leases Itai Gotlieb, Partner, Professional Practice July 2017 Overview Under Accounting Standards Codification (ASC) 842, Leases, lessees recognize assets and liabilities for

Edison Electric Institute and American Gas Association New Lease Standard

Edison Electric Institute and American Gas Association New Lease Standard May 16, 2016 Disclaimer The information contained herein is of a general nature and is not intended to address the circumstances

Edison Electric Institute and American Gas Association New Lease Standard May 16, 2016 Disclaimer The information contained herein is of a general nature and is not intended to address the circumstances

Accounting and Auditing Update. Staci L. Brogan, CPA, Shareholder Patricia R. Giudici, CPA, Senior Manager Schneider Downs & Co. Inc.

Accounting and Auditing Update Staci L. Brogan, CPA, Shareholder Patricia R. Giudici, CPA, Senior Manager Schneider Downs & Co. Inc. Agenda Overview of the standard setting agenda Revenue recognition Lease

Accounting and Auditing Update Staci L. Brogan, CPA, Shareholder Patricia R. Giudici, CPA, Senior Manager Schneider Downs & Co. Inc. Agenda Overview of the standard setting agenda Revenue recognition Lease

Lease Accounting and Loan Covenants: What is the Impact?

Lease Accounting and Loan Covenants: What is the Impact? Monday June 26, 2017 9:15 AM 10:30 AM Presented by: Charlie Shannon Partner Moss Adams LLP 8750 N. Central Expressway, Suite 300 Dallas, TX 75231

Lease Accounting and Loan Covenants: What is the Impact? Monday June 26, 2017 9:15 AM 10:30 AM Presented by: Charlie Shannon Partner Moss Adams LLP 8750 N. Central Expressway, Suite 300 Dallas, TX 75231

IMPACTS OF NEW LEASE ACCOUNTING STANDARD WHAT DOES IT MEAN TO ME? Jessica Richter, CPA.CITP, CISA Jamie Becker June 11, 2018

IMPACTS OF NEW LEASE ACCOUNTING STANDARD WHAT DOES IT MEAN TO ME? Jessica Richter, CPA.CITP, CISA Jamie Becker June 11, 2018 3 AGENDA ASC 842 Leases, ASU 2016-02 What s new Comparison with today s rules

IMPACTS OF NEW LEASE ACCOUNTING STANDARD WHAT DOES IT MEAN TO ME? Jessica Richter, CPA.CITP, CISA Jamie Becker June 11, 2018 3 AGENDA ASC 842 Leases, ASU 2016-02 What s new Comparison with today s rules

Technical Line FASB final guidance

No. 2018-08 20 September 2018 Technical Line FASB final guidance How the new leases standard affects engineering and construction entities In this issue: Overview... 1 Key considerations... 2 Scope and

No. 2018-08 20 September 2018 Technical Line FASB final guidance How the new leases standard affects engineering and construction entities In this issue: Overview... 1 Key considerations... 2 Scope and

Lease & Finance Accountants Conference. September The Westin Charlotte Charlotte, NC

Lease & Finance Accountants Conference September 11-13 The Westin Charlotte Charlotte, NC H A N D O U T S Basic Principles of Lessors under ASC 842 Mamta Shori, Wells Fargo Equipment Finance Joe Sebik,

Lease & Finance Accountants Conference September 11-13 The Westin Charlotte Charlotte, NC H A N D O U T S Basic Principles of Lessors under ASC 842 Mamta Shori, Wells Fargo Equipment Finance Joe Sebik,

New Lease Accounting Standards: Love at First Sight or Heartbreak?

New Lease Accounting Standards: Love at First Sight or Heartbreak? February 14, 2019 To Receive CPE Credit Individuals Participate in entire webinar Answer polls when they are provided Groups Group leader

New Lease Accounting Standards: Love at First Sight or Heartbreak? February 14, 2019 To Receive CPE Credit Individuals Participate in entire webinar Answer polls when they are provided Groups Group leader

Lease Accounting and simplease Accounting Updates. Trevor Warren & Jason Reljac

Lease Accounting and simplease Accounting Updates Trevor Warren & Jason Reljac Today s Agenda Overview Scope and Definition of a Lease Lease Classification Lessee Accounting Financial Statement Impact

Lease Accounting and simplease Accounting Updates Trevor Warren & Jason Reljac Today s Agenda Overview Scope and Definition of a Lease Lease Classification Lessee Accounting Financial Statement Impact

IFRS Project Insights Leases

IFRS Project Insights Leases The IASB and FASB ( the Boards ) published a Discussion Paper (DP) setting out a proposed lessee accounting model in March 2009. The proposed accounting model has evolved since

IFRS Project Insights Leases The IASB and FASB ( the Boards ) published a Discussion Paper (DP) setting out a proposed lessee accounting model in March 2009. The proposed accounting model has evolved since

The new accounting standard for leases. 27 March 2017

The new accounting standard for leases 27 March 2017 Disclaimer Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity.

The new accounting standard for leases 27 March 2017 Disclaimer Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity.

Summary of IFRS Exposure Draft Leases

The International Accounting Standards Board (IASB) recently issued a revised exposure draft (ED) relating to leases. Once these proposals are finalized the new guidance will replace the IAS 17 Leases.

The International Accounting Standards Board (IASB) recently issued a revised exposure draft (ED) relating to leases. Once these proposals are finalized the new guidance will replace the IAS 17 Leases.

Lease Accounting Is Final Time to Prepare for Implementation

Copyright 2016 by the Construction Financial Management Association (CFMA). All rights reserved. This article first appeared in CFMA Building Profits (a member-only benefit) and is reprinted with permission.

Copyright 2016 by the Construction Financial Management Association (CFMA). All rights reserved. This article first appeared in CFMA Building Profits (a member-only benefit) and is reprinted with permission.

REAL ESTATE PERSPECTIVE ON NEW LEASE ACCOUNTING STANDARDS

VALUATION & ADVISORY REAL ESTATE PERSPECTIVE ON NEW LEASE ACCOUNTING STANDARDS BY JOHN CORBETT, MAI, ASA, FRICS AND MARC R. SHAPIRO, MAI, MRICS INTRODUCTION The Financial Accounting Standards Board (FASB)

VALUATION & ADVISORY REAL ESTATE PERSPECTIVE ON NEW LEASE ACCOUNTING STANDARDS BY JOHN CORBETT, MAI, ASA, FRICS AND MARC R. SHAPIRO, MAI, MRICS INTRODUCTION The Financial Accounting Standards Board (FASB)

Defining Issues May 2013, No

Defining Issues May 2013, No. 13-24 FASB and IASB Issue Revised Exposure Drafts on Lease Accounting The FASB and IASB (the Boards) recently issued revised joint exposure drafts (EDs) on proposed changes

Defining Issues May 2013, No. 13-24 FASB and IASB Issue Revised Exposure Drafts on Lease Accounting The FASB and IASB (the Boards) recently issued revised joint exposure drafts (EDs) on proposed changes

LEASES WHERE ARE WE? Steve Rathjen

LEASES WHERE ARE WE? Steve Rathjen 267 256-3110 srathjen@kpmg.com Agenda Project status Lease definition and classification Lessee accounting Lessor accounting Presentation, disclosures, and transition

LEASES WHERE ARE WE? Steve Rathjen 267 256-3110 srathjen@kpmg.com Agenda Project status Lease definition and classification Lessee accounting Lessor accounting Presentation, disclosures, and transition

Applying the new lease accounting standard

Applying the new lease accounting standard In February 26, the FASB issued Accounting Standards Update (ASU) No. 26-, Leases (codified as Accounting Standards Codification Topic (ASC) 842). ASC 842 introduces

Applying the new lease accounting standard In February 26, the FASB issued Accounting Standards Update (ASU) No. 26-, Leases (codified as Accounting Standards Codification Topic (ASC) 842). ASC 842 introduces

Brad Bonde, CPA Senior Manager, HC Services/Audit & Advisory

Brad Bonde, CPA Senior Manager, HC Services/Audit & Advisory Overview Background Improving Lease Accounting Scope Accounting Models Disclosures Effective Dates 2 Background Source - FASB 3 QUIZ What amount

Brad Bonde, CPA Senior Manager, HC Services/Audit & Advisory Overview Background Improving Lease Accounting Scope Accounting Models Disclosures Effective Dates 2 Background Source - FASB 3 QUIZ What amount

Accounting and Auditing. Norman Mosrie, CPA, FMFMA, CHFP James Sutherland, CPA

Accounting and Auditing Norman Mosrie, CPA, FMFMA, CHFP James Sutherland, CPA Leases (ASU 2016-02; Topic 842) A lease contract conveys the right to use an asset (the underlying asset) for a period of time

Accounting and Auditing Norman Mosrie, CPA, FMFMA, CHFP James Sutherland, CPA Leases (ASU 2016-02; Topic 842) A lease contract conveys the right to use an asset (the underlying asset) for a period of time

Defining Issues. FASB Completes Technical Redeliberations on Leases. October 2015, No Key Facts. Key Impacts

Defining Issues October 2015, No. 15-47 FASB Completes Technical Redeliberations on Leases The FASB met on October 7 to discuss comments received and related follow-up issues on the external review of

Defining Issues October 2015, No. 15-47 FASB Completes Technical Redeliberations on Leases The FASB met on October 7 to discuss comments received and related follow-up issues on the external review of

Lease Accounting Standard Update ASU Presented by: Nicholas Hoefel, CPA Manager, Audit Services Group

Lease Accounting Standard Update ASU 2016-02 Presented by: Nicholas Hoefel, CPA Manager, Audit Services Group 1 Overview Introduction Background and current environment Effective dates and transition Key

Lease Accounting Standard Update ASU 2016-02 Presented by: Nicholas Hoefel, CPA Manager, Audit Services Group 1 Overview Introduction Background and current environment Effective dates and transition Key

CPE regulations require online participants to take part in online questions

KPMG s CFO Financial Forum Webcast FASB/IASB Revised Lease Accounting Exposure Drafts A Detailed Look Part III: Lessor Accounting June 25, 2013 Administrative CPE regulations require online participants

KPMG s CFO Financial Forum Webcast FASB/IASB Revised Lease Accounting Exposure Drafts A Detailed Look Part III: Lessor Accounting June 25, 2013 Administrative CPE regulations require online participants

Measuring Lease Liabilities EQUIPMENT LEASING AND FINANCE ASSOCIATION

Measuring Lease Liabilities EQUIPMENT LEASING AND FINANCE ASSOCIATION Presenters Kerrie Cadugan, Executive Director, EY Barbara Galaini, Chief Accounting Officer of the Americas, Avolon The views expressed

Measuring Lease Liabilities EQUIPMENT LEASING AND FINANCE ASSOCIATION Presenters Kerrie Cadugan, Executive Director, EY Barbara Galaini, Chief Accounting Officer of the Americas, Avolon The views expressed

Something Borrowed, Something New Get Ready for the New Lease Accounting Standard

April 2016 Something Borrowed, Something New Get Ready for the New Lease Accounting Standard By Scott G. Lehman, CPA, and David E. Wentzel, CPA Audit / Tax / Advisory / Risk / Performance Smart decisions.

April 2016 Something Borrowed, Something New Get Ready for the New Lease Accounting Standard By Scott G. Lehman, CPA, and David E. Wentzel, CPA Audit / Tax / Advisory / Risk / Performance Smart decisions.

Leases ASU September 20, 2017

Leases ASU 2016-02 September 20, 2017 Meet the Speakers Tonisha Spratte, CPA Senior Accountant Cherry Bekaert tspratte@cbh.com Matthew Mars Senior Accountant Cherry Bekaert mmars@cbh.com Agenda What is

Leases ASU 2016-02 September 20, 2017 Meet the Speakers Tonisha Spratte, CPA Senior Accountant Cherry Bekaert tspratte@cbh.com Matthew Mars Senior Accountant Cherry Bekaert mmars@cbh.com Agenda What is

ASC 842: Leases. Presented by: Maxwell Locke & Ritter LLP June 15, Maxwell Locke & Ritter

ASC 842: Leases Presented by: Maxwell Locke & Ritter LLP June 15, 2018 The New Lease Standard FASB ASC 842, Leases Supersedes FASB ASC 840, Leases Effective for calendar year-end public companies in 2019;

ASC 842: Leases Presented by: Maxwell Locke & Ritter LLP June 15, 2018 The New Lease Standard FASB ASC 842, Leases Supersedes FASB ASC 840, Leases Effective for calendar year-end public companies in 2019;

Accounting Update. Anne Cloutier, CPA, FHFMA Principal March 27, 2015

Accounting Update Anne Cloutier, CPA, FHFMA Principal March 27, 2015 Current Accounting for Leases Capital leases - a lessee recognizes leased assets and liabilities on the balance sheet. Operating leases

Accounting Update Anne Cloutier, CPA, FHFMA Principal March 27, 2015 Current Accounting for Leases Capital leases - a lessee recognizes leased assets and liabilities on the balance sheet. Operating leases

IFRS 16 LEASES. Page 1 of 21

IFRS 16 LEASES OBJECTIVE The objective is to ensure that lessees and lessors provide relevant information in a manner that faithfully represents those transactions. This information gives a basis for users

IFRS 16 LEASES OBJECTIVE The objective is to ensure that lessees and lessors provide relevant information in a manner that faithfully represents those transactions. This information gives a basis for users

Deeper Dive Leases. Overview

Deeper Dive Leases Presented by: Shaun Johnson, CPA Dingus, Zarecor & Associates PLLC Overview Effective dates Big picture Objective, impact, and implementation Applicability and definition Initial recognition

Deeper Dive Leases Presented by: Shaun Johnson, CPA Dingus, Zarecor & Associates PLLC Overview Effective dates Big picture Objective, impact, and implementation Applicability and definition Initial recognition

Technical Line FASB final guidance

No. 2019-01 3 January 2019 Technical Line FASB final guidance How the new leases standard affects automotive entities In this issue: Overview... 1 Recent standard setting activity... 2 Key considerations...

No. 2019-01 3 January 2019 Technical Line FASB final guidance How the new leases standard affects automotive entities In this issue: Overview... 1 Recent standard setting activity... 2 Key considerations...

Is Your Operating Lease An Asset or Liability? It s Now Both

MFM Annual Conference Is Your Operating Lease An Asset or Liability? It s Now Both 23 May 2016-1:30 pm 2:20 pm Disclaimer These slides are for educational purposes only and are not intended, and should

MFM Annual Conference Is Your Operating Lease An Asset or Liability? It s Now Both 23 May 2016-1:30 pm 2:20 pm Disclaimer These slides are for educational purposes only and are not intended, and should

FASB/IASB Update Part II

American Accounting Association FASB/IASB Update Part II Tom Linsmeier FASB Member August 3, 2014 The views expressed in this presentation are those of the presenters. Official positions of the FASB/IASB

American Accounting Association FASB/IASB Update Part II Tom Linsmeier FASB Member August 3, 2014 The views expressed in this presentation are those of the presenters. Official positions of the FASB/IASB

Lease & Finance Accountants Conference. September The Westin Charlotte Charlotte, NC

Lease & Finance Accountants Conference September 11-13 The Westin Charlotte Charlotte, NC H A N D O U T S EQUIPMENT LEASING AND FINANCE ASSOCIATION Transitioning to the ASC 842 Guidance Lessee Requirements

Lease & Finance Accountants Conference September 11-13 The Westin Charlotte Charlotte, NC H A N D O U T S EQUIPMENT LEASING AND FINANCE ASSOCIATION Transitioning to the ASC 842 Guidance Lessee Requirements

47.1% of organizations concerned about their ability to implement

Leases: Not Just for the 1 Lease Standard - Statistics 10 year project In 2014, $3.0 trillion in off-balance sheet lease commitments 47.1% of organizations concerned about their ability to implement 2

Leases: Not Just for the 1 Lease Standard - Statistics 10 year project In 2014, $3.0 trillion in off-balance sheet lease commitments 47.1% of organizations concerned about their ability to implement 2

Lease Update. June 2017 Addison, Texas

Lease Update June 2017 Addison, Texas William Bill Schneider CPA, CGMA Bill is an Audit Director at AT&T. AT&T delivers advanced mobile services, next-generation TV, highspeed internet and smart solutions

Lease Update June 2017 Addison, Texas William Bill Schneider CPA, CGMA Bill is an Audit Director at AT&T. AT&T delivers advanced mobile services, next-generation TV, highspeed internet and smart solutions

Click to edit Master title style REVENUE RECOGNITION Understanding the New Revenue Recognition Standard ASC 606

Click to edit Master title style REVENUE RECOGNITION Understanding the New Revenue Recognition Standard ASC 606 9/7/2017 0 Agenda Overview of ASC 606 Review of the five-step process Accounting for contract

Click to edit Master title style REVENUE RECOGNITION Understanding the New Revenue Recognition Standard ASC 606 9/7/2017 0 Agenda Overview of ASC 606 Review of the five-step process Accounting for contract

Technical Line FASB final guidance

No. 2016-11 14 April 2016 Technical Line FASB final guidance How the FASB s new leases standard will affect real estate entities In this issue: Overview... 1 Key considerations... 2 Scope and scope exceptions...

No. 2016-11 14 April 2016 Technical Line FASB final guidance How the FASB s new leases standard will affect real estate entities In this issue: Overview... 1 Key considerations... 2 Scope and scope exceptions...

Lease accounting scope & impacts

Leasing Lease accounting scope & impacts Scope What s in? All industries, all entities Arrangements that meet the definition of a lease Embedded leases within other arrangements What s out? Leases of:

Leasing Lease accounting scope & impacts Scope What s in? All industries, all entities Arrangements that meet the definition of a lease Embedded leases within other arrangements What s out? Leases of:

IFRS 16 Leases supplement

IFRS 16 Leases supplement Guide to annual financial statements IFRS December 2017 kpmg.com/ifrs Contents About this supplement 1 About IFRS 16 3 The Group s lease portfolio 6 Part I Modified retrospective

IFRS 16 Leases supplement Guide to annual financial statements IFRS December 2017 kpmg.com/ifrs Contents About this supplement 1 About IFRS 16 3 The Group s lease portfolio 6 Part I Modified retrospective

Technical Line FASB final guidance

No. 2018-18 13 December 2018 Technical Line FASB final guidance How the new leases standard affects life sciences entities In this issue: Overview... 1 Key considerations... 2 Scope and scope exceptions...

No. 2018-18 13 December 2018 Technical Line FASB final guidance How the new leases standard affects life sciences entities In this issue: Overview... 1 Key considerations... 2 Scope and scope exceptions...

What private companies need to know about applying the new lease standard

What private companies need to know about applying the new lease standard In February 26, the FASB issued Accounting Standards Update (ASU) No. 26-, Leases (codified as Accounting Standards Codification

What private companies need to know about applying the new lease standard In February 26, the FASB issued Accounting Standards Update (ASU) No. 26-, Leases (codified as Accounting Standards Codification

Welcome to Webinar: Implementing FASB s Updated Lease Accounting Standard ASU (Topic 842)

") Welcome to Webinar: Implementing FASB s Updated Lease Accounting Standard ASU 2016-02 (Topic 842) Presented by: Gelman, Rosenberg & Freedman CPAs Please note: Use the Question panel to speak with the administrator

Welcome to Webinar: Implementing FASB s Updated Lease Accounting Standard ASU 2016-02 (Topic 842) Presented by: Gelman, Rosenberg & Freedman CPAs Please note: Use the Question panel to speak with the administrator

THE NEW LEASE ACCOUNTING STANDARD

THE NEW LEASE ACCOUNTING STANDARD May 30, 2018 BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited by guarantee, and forms part

THE NEW LEASE ACCOUNTING STANDARD May 30, 2018 BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited by guarantee, and forms part

Financial Computer Systems Inc. (203)

") Introduction to ASC 842 and EZLease Financial Computer Systems Inc. www.ezlease.net (203) 652-1375 The road to ASC 842 Begun in July 2006; joint project of FASB & IASB Primary purpose: Put lessee operating

Introduction to ASC 842 and EZLease Financial Computer Systems Inc. www.ezlease.net (203) 652-1375 The road to ASC 842 Begun in July 2006; joint project of FASB & IASB Primary purpose: Put lessee operating

Lease & Finance Accountants Conference. September The Westin Charlotte Charlotte, NC

Lease & Finance Accountants Conference September 11-13 The Westin Charlotte Charlotte, NC H A N D O U T S Lessor Accounting under ASC 842 EQUIPMENT LEASING AND FINANCE ASSOCIATION Presenters Rod Hurd Chief

Lease & Finance Accountants Conference September 11-13 The Westin Charlotte Charlotte, NC H A N D O U T S Lessor Accounting under ASC 842 EQUIPMENT LEASING AND FINANCE ASSOCIATION Presenters Rod Hurd Chief

Preparing for the new ASC 842 Leasing Standard Challenges and Solutions. August 24, 2017

Preparing for the new ASC 842 Leasing Standard Challenges and Solutions August 24, 2017 Learning objectives Define leasing implications related to recently revised FASB standard Differentiate between new

Preparing for the new ASC 842 Leasing Standard Challenges and Solutions August 24, 2017 Learning objectives Define leasing implications related to recently revised FASB standard Differentiate between new

MONITORDAILY SPECIAL REPORT. Lease Accounting Project Update as of May 25, 2011 Prepared by Bill Bosco, Leasing 101

MONITORDAILY SPECIAL REPORT Lease Accounting Project Update as of May 25, 2011 Prepared by Bill Bosco, Leasing 101 The high volume of comment letters (780+) and numerous outreach meetings had common criticisms

MONITORDAILY SPECIAL REPORT Lease Accounting Project Update as of May 25, 2011 Prepared by Bill Bosco, Leasing 101 The high volume of comment letters (780+) and numerous outreach meetings had common criticisms

Leases: A Comprehensive Update on the Joint Project

The Dbriefs Financial Reporting series presents: Leases: A Comprehensive Update on the Joint Project Bob Uhl, Deloitte & Touche LLP Trevor Farber, Deloitte & Touche LLP James Barker, Deloitte & Touche

The Dbriefs Financial Reporting series presents: Leases: A Comprehensive Update on the Joint Project Bob Uhl, Deloitte & Touche LLP Trevor Farber, Deloitte & Touche LLP James Barker, Deloitte & Touche

ASC Topic 842 Leases. September 25 &

ASC Topic 842 Leases September 25 & 26 2017 This presentation is intended solely for the information and use of the EEI and AGA and is not intended to be and should not be used by anyone other than these

ASC Topic 842 Leases September 25 & 26 2017 This presentation is intended solely for the information and use of the EEI and AGA and is not intended to be and should not be used by anyone other than these

New Developments Summary

July 10, 2018 NDS 2018-07 New Developments Summary Leases in transition New leasing standard provides detailed transition guidance Summary For most entities, one of the more complex aspects of implementing

July 10, 2018 NDS 2018-07 New Developments Summary Leases in transition New leasing standard provides detailed transition guidance Summary For most entities, one of the more complex aspects of implementing

Accounting and Auditing Update. Paul Lundy

Accounting and Auditing Update Paul Lundy Leases: Not Just for the Footnotes Anymore Significant Financial Statement Impact New lease standard generally requires all leases to be capitalized and recognized

Accounting and Auditing Update Paul Lundy Leases: Not Just for the Footnotes Anymore Significant Financial Statement Impact New lease standard generally requires all leases to be capitalized and recognized

Preparing for the new ASC 842 Leasing Standard Challenges and Solutions. August 24, 2017

Preparing for the new ASC 842 Leasing Standard Challenges and Solutions August 24, 2017 Learning objectives Define leasing implications related to recently revised FASB standard Differentiate between new

Preparing for the new ASC 842 Leasing Standard Challenges and Solutions August 24, 2017 Learning objectives Define leasing implications related to recently revised FASB standard Differentiate between new

No February Leases (Topic 842) An Amendment of the FASB Accounting Standards Codification

An Amendment of the FASB Accounting Standards Codification") No. 2016-02 February 2016 Leases (Topic 842) An Amendment of the FASB Accounting Standards Codification The FASB Accounting Standards Codification is the source of authoritative generally accepted accounting

No. 2016-02 February 2016 Leases (Topic 842) An Amendment of the FASB Accounting Standards Codification The FASB Accounting Standards Codification is the source of authoritative generally accepted accounting

Transition Requirements Under the New Lease Accounting Rules

Accounting Policy & Practice Report: News Archive 2017 December 12/28/2017 BNA Insights Transition Requirements Under the New Lease Accounting Rules By Jeffrey Ellis Jeffrey Ellis is a Senior Managing

Accounting Policy & Practice Report: News Archive 2017 December 12/28/2017 BNA Insights Transition Requirements Under the New Lease Accounting Rules By Jeffrey Ellis Jeffrey Ellis is a Senior Managing

IFRS 16 : Lease accounting

IFRS 16 : Lease accounting Effective for accounting periods beginning on or after 1 January 2019 December 2017 IFRS 16: Lease accounting The IASB published the new IFRS 16 lease standard, in order to avoid

IFRS 16 : Lease accounting Effective for accounting periods beginning on or after 1 January 2019 December 2017 IFRS 16: Lease accounting The IASB published the new IFRS 16 lease standard, in order to avoid

FSA Faculty Consortium Technical Accounting Update. Bob Uhl, partner, Deloitte & Touche LLP

FSA Faculty Consortium Technical Accounting Update Bob Uhl, partner, Deloitte & Touche LLP Deloitte University May 30, 2014 Acronyms Acronym ASC ASU ED FASB IASB IFRS U.S. GAAP Full Form Accounting Standards

FSA Faculty Consortium Technical Accounting Update Bob Uhl, partner, Deloitte & Touche LLP Deloitte University May 30, 2014 Acronyms Acronym ASC ASU ED FASB IASB IFRS U.S. GAAP Full Form Accounting Standards

Proposed New Accounting Standards For Leases

Relationships backed by performance. Proposed New Accounting Standards For Leases Doug Richardson Live Seminar 9:00am 10:30am June 21 2012 Overview and Background Leases serve a vital role in many entities

Relationships backed by performance. Proposed New Accounting Standards For Leases Doug Richardson Live Seminar 9:00am 10:30am June 21 2012 Overview and Background Leases serve a vital role in many entities

The Financial Accounting Standards Board

V A L U A T I O N How the New Leases Standard May Impact Business Valuations By Judith H. O Dell, CPA, CVA The Financial Accounting Standards Board issued the 485 page Leases Standard (Topic 842) in February,

V A L U A T I O N How the New Leases Standard May Impact Business Valuations By Judith H. O Dell, CPA, CVA The Financial Accounting Standards Board issued the 485 page Leases Standard (Topic 842) in February,

GASB 87 - Leases. South Carolina Association of CPAs Fall Fest November 16, 2018 Mauldin & Jenkins

November 16, 2018 Mauldin & Jenkins 800-277-0050 www.mjcpa.com GASB 87 - Leases Effective for periods beginning after December 15, 2019 - December 31, 2020 or June 30, 2021 or September 30, 2021 Amends

November 16, 2018 Mauldin & Jenkins 800-277-0050 www.mjcpa.com GASB 87 - Leases Effective for periods beginning after December 15, 2019 - December 31, 2020 or June 30, 2021 or September 30, 2021 Amends

Defining Issues. FASB and IASB Enter Home Stretch in Redeliberations on Lease Accounting but on Different Tracks. Key Facts. October 2014, No.

Defining Issues October 2014, No. 14-46 FASB and IASB Enter Home Stretch in Redeliberations on Lease Accounting but on Different Tracks At their July and October joint meetings, the FASB and the IASB (the

Defining Issues October 2014, No. 14-46 FASB and IASB Enter Home Stretch in Redeliberations on Lease Accounting but on Different Tracks At their July and October joint meetings, the FASB and the IASB (the

Headline Verdana Bold The evolutions of leases accounting under IFRS 16 Mariano Bruno, Carlo Laganà, Giuseppe Ambrosio, Deloitte & Touche S.p.A.

SHIPPING AND THE LAW 7^ Edition 25-26 October 2016 NAPLES Headline Verdana Bold The evolutions of leases accounting under IFRS 16 Mariano Bruno, Carlo Laganà, Giuseppe Ambrosio, Deloitte & Touche S.p.A.

SHIPPING AND THE LAW 7^ Edition 25-26 October 2016 NAPLES Headline Verdana Bold The evolutions of leases accounting under IFRS 16 Mariano Bruno, Carlo Laganà, Giuseppe Ambrosio, Deloitte & Touche S.p.A.

International Financial Reporting Standard 16 Leases. Objective. Scope. Recognition exemptions (paragraphs B3 B8) IFRS 16

IFRS 16") International Financial Reporting Standard 16 Leases Objective 1 This Standard sets out the principles for the recognition, measurement, presentation and disclosure of leases. The objective is to ensure

International Financial Reporting Standard 16 Leases Objective 1 This Standard sets out the principles for the recognition, measurement, presentation and disclosure of leases. The objective is to ensure

GASB 87: Leases. Hosted By: Ben Lindekugel, Executive Director Association of Washington Public Hospital Districts

GASB 87: Leases Hosted By: Ben Lindekugel, Executive Director Association of Washington Public Hospital Districts November 6, 2018 Presented By Tom Dingus, CPA, Partner Dingus, Zarecor & Associates PLLC

GASB 87: Leases Hosted By: Ben Lindekugel, Executive Director Association of Washington Public Hospital Districts November 6, 2018 Presented By Tom Dingus, CPA, Partner Dingus, Zarecor & Associates PLLC

HERE WE GO AGAIN. THE NEW LEASE STANDARD (ASC TOPIC 842) February Internal Audit, Risk, Business & Technology Consulting

February Internal Audit, Risk, Business & Technology Consulting") HERE WE GO AGAIN THE NEW LEASE STANDARD (ASC TOPIC 842) February 2018 Internal Audit, Risk, Business & Technology Consulting PRESENTERS Edna Lopez Protiviti Managing Director edna.lopez@protiviti.com Scott

HERE WE GO AGAIN THE NEW LEASE STANDARD (ASC TOPIC 842) February 2018 Internal Audit, Risk, Business & Technology Consulting PRESENTERS Edna Lopez Protiviti Managing Director edna.lopez@protiviti.com Scott

7/30/2018. Health Care. A CHC-Focused Plan for the New Lease Accounting Standard

Health Care A CHC-Focused Plan for the New Lease Accounting Standard July 31, 2018 1 TO RECEIVE CPE CREDIT Individuals Participate in entire webinar Answer polls when they are provided Groups Group leader

Health Care A CHC-Focused Plan for the New Lease Accounting Standard July 31, 2018 1 TO RECEIVE CPE CREDIT Individuals Participate in entire webinar Answer polls when they are provided Groups Group leader

The joint leases project change is coming

No. 2010-4 18 June 2010 Technical Line Technical guidance on standards and practice issues The joint leases project change is coming What you need to know The proposed changes to the accounting for leases

No. 2010-4 18 June 2010 Technical Line Technical guidance on standards and practice issues The joint leases project change is coming What you need to know The proposed changes to the accounting for leases

What Nonprofits Need to Know About the New Standards for Lease Accounting

The webcast will start at 1 p.m. Eastern Please note: Handout You can print or download the webcast handout at https://capincrouse.com/webcast-lease-accounting CPE CPE certificates will be emailed to you

The webcast will start at 1 p.m. Eastern Please note: Handout You can print or download the webcast handout at https://capincrouse.com/webcast-lease-accounting CPE CPE certificates will be emailed to you

GAAP Update SCHFMA 2016 Fall Institute

GAAP Update SCHFMA 2016 Fall Institute Ken Conner, CPA Shareholder Tiffany Brackett, CPA Senior Manager This material was used by Elliott Davis Decosimo during an oral presentation; it is not a complete

GAAP Update SCHFMA 2016 Fall Institute Ken Conner, CPA Shareholder Tiffany Brackett, CPA Senior Manager This material was used by Elliott Davis Decosimo during an oral presentation; it is not a complete

Technical Line FASB final guidance

No. 2018-15 6 December 2018 Technical Line FASB final guidance How the new leases standard affects consumer products and retail entities In this issue: Overview... 1 Recent standard-setting activity...

No. 2018-15 6 December 2018 Technical Line FASB final guidance How the new leases standard affects consumer products and retail entities In this issue: Overview... 1 Recent standard-setting activity...

NEW LEASE ACCOUNTING STANDARD

NEW LEASE ACCOUNTING STANDARD Accounting Standards Update (ASU) 2016-02, Leases & GASB 87, Leases LEASES Leases: Why a New Leases Standard? 1 IMPLEMENTATION TIMELINE January 2016 IASB issued IFRS 16, Leases

NEW LEASE ACCOUNTING STANDARD Accounting Standards Update (ASU) 2016-02, Leases & GASB 87, Leases LEASES Leases: Why a New Leases Standard? 1 IMPLEMENTATION TIMELINE January 2016 IASB issued IFRS 16, Leases

IFRS Update Guy Thomas, CPA, CA

IFRS Update Guy Thomas, CPA, CA D&Co IFRS update Agenda 3 new standards under IFRS IFRS 9 Financial Instruments IFRS 15 Revenue from Contracts with Customers IFRS 16 Leases Agenda Some narrow scope amendments

IFRS Update Guy Thomas, CPA, CA D&Co IFRS update Agenda 3 new standards under IFRS IFRS 9 Financial Instruments IFRS 15 Revenue from Contracts with Customers IFRS 16 Leases Agenda Some narrow scope amendments

GASBs Presented by: William Blend, CPA, CFE

GASBs 87-89 Presented by: William Blend, CPA, CFE Leases: Statement 87 Effective Date and General Implementation Effective for Florida fiscal year end 2021. Earlier application is encouraged. Leases should

GASBs 87-89 Presented by: William Blend, CPA, CFE Leases: Statement 87 Effective Date and General Implementation Effective for Florida fiscal year end 2021. Earlier application is encouraged. Leases should

Preview of the New Exposure Draft of the Lease Accounting Project Key elements and commentary

Preview of the New Exposure Draft of the Lease Accounting Project Key elements and commentary Prepared by Bill Bosco, Leasing 101 www.leasing-101.com The Financial Accounting Standards Board (FASB) and

Preview of the New Exposure Draft of the Lease Accounting Project Key elements and commentary Prepared by Bill Bosco, Leasing 101 www.leasing-101.com The Financial Accounting Standards Board (FASB) and

NEED TO KNOW. Leases A Project Update

NEED TO KNOW Leases A Project Update 2 LEASES - A PROJECT UPDATE TABLE OF CONTENTS Introduction 3 Existing guidance and the rationale for change 4 The IASB/FASB project to date 5 The main proposals 6 Definition

NEED TO KNOW Leases A Project Update 2 LEASES - A PROJECT UPDATE TABLE OF CONTENTS Introduction 3 Existing guidance and the rationale for change 4 The IASB/FASB project to date 5 The main proposals 6 Definition

RE: Proposed Accounting Standards Update, Leases (Topic 842): Targeted Improvements (File Reference No )

: Targeted Improvements (File Reference No )") KPMG LLP Telephone +1 212 758 9700 345 Park Avenue Fax +1 212 758 9819 New York, N.Y. 10154-0102 Internet www.us.kpmg.com 401 Merritt 7 PO Box 5116 Norwalk, CT 06856-5116 RE: Proposed Accounting Standards

KPMG LLP Telephone +1 212 758 9700 345 Park Avenue Fax +1 212 758 9819 New York, N.Y. 10154-0102 Internet www.us.kpmg.com 401 Merritt 7 PO Box 5116 Norwalk, CT 06856-5116 RE: Proposed Accounting Standards

In December 2003 the IASB issued a revised IAS 17 as part of its initial agenda of technical projects.

IFRS Standard 16 Leases In April 2001 the International Accounting Standards Board (IASB) adopted IAS 17 Leases, which had originally been issued by the International Accounting Standards Committee (IASC)

IFRS Standard 16 Leases In April 2001 the International Accounting Standards Board (IASB) adopted IAS 17 Leases, which had originally been issued by the International Accounting Standards Committee (IASC)

IFRS 16 Leases. PICPA IFRS: New Standards and Updates Dubai. 28 April 2017

IFRS 16 Leases PICPA IFRS: New Standards and Updates Dubai 28 April 2017 1 More transparent lease accounting IFRS 16 will bring most leases on-balance sheet from 2019. All companies that lease assets for

IFRS 16 Leases PICPA IFRS: New Standards and Updates Dubai 28 April 2017 1 More transparent lease accounting IFRS 16 will bring most leases on-balance sheet from 2019. All companies that lease assets for

Heads Up. FASB Draws a Bright Line Through Operating Leases Proposed ASU Revamps Lease. Accounting. The ED, released by the FASB as a proposed

August 17, 2010 Volume 17, Issue 27 Heads Up In This Issue: Background Effective Date In a Nutshell Scope Lessee Accounting Lessor Accounting Presentation and Disclosures Transition The ED, released by

August 17, 2010 Volume 17, Issue 27 Heads Up In This Issue: Background Effective Date In a Nutshell Scope Lessee Accounting Lessor Accounting Presentation and Disclosures Transition The ED, released by

Technical Line FASB final guidance

No. 2018-10 11 October 2018 Technical Line FASB final guidance How the new leases standard affects airlines In this issue: Overview... 1 Key considerations... 2 Scope and scope exceptions... 2 Definition

No. 2018-10 11 October 2018 Technical Line FASB final guidance How the new leases standard affects airlines In this issue: Overview... 1 Key considerations... 2 Scope and scope exceptions... 2 Definition

IFRS 16 Lease overview and EY s enabling toolkit

IFRS 16 Lease overview and EY s enabling toolkit Content Page Section I IFRS 16 overview 2 Appendix I EY Lease enabling technology suite 9 Appendix II EY Contacts 17 Page 1 IFRS 9 Classification and measurement

IFRS 16 Lease overview and EY s enabling toolkit Content Page Section I IFRS 16 overview 2 Appendix I EY Lease enabling technology suite 9 Appendix II EY Contacts 17 Page 1 IFRS 9 Classification and measurement

Leases Refashioned. The Bottom Line. Retail & Distribution Spotlight January In This Issue

Retail & Distribution Spotlight January 2017 In This Issue Background Key Issues Challenges Thinking Ahead Contacts Leases Refashioned The Bottom Line On February 25, 2016, the FASB issued its new leases

Retail & Distribution Spotlight January 2017 In This Issue Background Key Issues Challenges Thinking Ahead Contacts Leases Refashioned The Bottom Line On February 25, 2016, the FASB issued its new leases

IASB Staff Paper March 2011

IASB Staff Paper March 2011 Effect of board redeliberations on Exposure Draft Leases About this staff paper This staff paper indicates how the proposals in the Exposure Draft Leases would change as a result

IASB Staff Paper March 2011 Effect of board redeliberations on Exposure Draft Leases About this staff paper This staff paper indicates how the proposals in the Exposure Draft Leases would change as a result

On the Horizon: Leases and Fiduciary Responsibilities

On the Horizon: Leases and Fiduciary Responsibilities Dean Michael Mead, Research Manager Florida School Finance Officers Association November 11, 2015 The views expressed in this presentation are those

On the Horizon: Leases and Fiduciary Responsibilities Dean Michael Mead, Research Manager Florida School Finance Officers Association November 11, 2015 The views expressed in this presentation are those

FASB Leases Topic 842

FASB Leases Topic 842 Date of Entry: 9/13/2013 Respondent information Type of entity or individual: Service Provider Contact information: Organization: Name: Email address: Phone number: LeaseTeam, Inc.

FASB Leases Topic 842 Date of Entry: 9/13/2013 Respondent information Type of entity or individual: Service Provider Contact information: Organization: Name: Email address: Phone number: LeaseTeam, Inc.

Defining Issues. FASB and IASB Take Divergent Paths on Key Aspects of Lease Accounting. March 2014, No Key Facts

Defining Issues March 2014, No. 14-17 FASB and IASB Take Divergent Paths on Key Aspects of Lease Accounting At their March 18-19 meeting to redeliberate the proposals in their 2013 exposure drafts (EDs)

Defining Issues March 2014, No. 14-17 FASB and IASB Take Divergent Paths on Key Aspects of Lease Accounting At their March 18-19 meeting to redeliberate the proposals in their 2013 exposure drafts (EDs)

A Review of IFRS 16 Leases By Tan Liong Tong

A Review of IFRS 16 Leases By Tan Liong Tong In April 2016, the MASB issued MFRS 16 Leases that is identical to IFRS 16 Leases issued by the IASB in January 2016. The effective date of this new MFRS is

A Review of IFRS 16 Leases By Tan Liong Tong In April 2016, the MASB issued MFRS 16 Leases that is identical to IFRS 16 Leases issued by the IASB in January 2016. The effective date of this new MFRS is

Sri Lanka Accounting Standard - SLFRS 16. Leases

Sri Lanka Accounting Standard - SLFRS 16 Leases CONTENTS from paragraph SRI LANKA ACCOUNTING STANDARD - SLFRS 16 LEASES INTRODUCTION OBJECTIVE 1 SCOPE 3 RECOGNITION EXEMPTIONS 5 IDENTIFYING A LEASE 9 Separating

Sri Lanka Accounting Standard - SLFRS 16 Leases CONTENTS from paragraph SRI LANKA ACCOUNTING STANDARD - SLFRS 16 LEASES INTRODUCTION OBJECTIVE 1 SCOPE 3 RECOGNITION EXEMPTIONS 5 IDENTIFYING A LEASE 9 Separating

Chapter 15 Leases 15-1

Chapter 15 Leases 1. Why Leasing sometimes makes more sense 2. The accounting issues in recording a lease transaction 3. The types of contractual provisions in lease 4. The lease classification: capital

Chapter 15 Leases 1. Why Leasing sometimes makes more sense 2. The accounting issues in recording a lease transaction 3. The types of contractual provisions in lease 4. The lease classification: capital

Topic 842 Technical Corrections Summary of Comments Received

Contact(s) David Hoyer Co-Author Ext. 462 Andy Bologna Co-Author Ext. 356 Thomas Faineteau Co-Author Ext. 362 Chris Roberge Co-Author Ext. 274 Amy Park Co-Author Ext. 476 Shayne Kuhaneck Assistant Director

Contact(s) David Hoyer Co-Author Ext. 462 Andy Bologna Co-Author Ext. 356 Thomas Faineteau Co-Author Ext. 362 Chris Roberge Co-Author Ext. 274 Amy Park Co-Author Ext. 476 Shayne Kuhaneck Assistant Director

Defining Issues. FASB and IASB Continue Discussions on Lease Accounting. Key Facts. June 2014, No

Defining Issues June 2014, No. 14-29 FASB and IASB Continue Discussions on Lease Accounting During the second quarter of 2014, the FASB and IASB (the Boards) continued redeliberations on the proposals

Defining Issues June 2014, No. 14-29 FASB and IASB Continue Discussions on Lease Accounting During the second quarter of 2014, the FASB and IASB (the Boards) continued redeliberations on the proposals

New Zealand Equivalent to International Financial Reporting Standard 16 Leases (NZ IFRS 16)

") New Zealand Equivalent to International Financial Reporting Standard 16 Leases (NZ IFRS 16) Issued February 2016 This Standard was issued on 11 February 2016 by the New Zealand Accounting Standards Board

New Zealand Equivalent to International Financial Reporting Standard 16 Leases (NZ IFRS 16) Issued February 2016 This Standard was issued on 11 February 2016 by the New Zealand Accounting Standards Board