Brad Bonde, CPA Senior Manager, HC Services/Audit & Advisory

|

|

|

- Erick Johns

- 6 years ago

- Views:

Transcription

1 Brad Bonde, CPA Senior Manager, HC Services/Audit & Advisory

2 Overview Background Improving Lease Accounting Scope Accounting Models Disclosures Effective Dates 2

3 Background Source - FASB 3

4 QUIZ What amount of Off-Balance Sheet Operating Lease Commitments for SEC registrants were there in 2005? A. $1.25 MILLION B. $1.25 BILLION C. $1.25 TRILLION 4

5 ANSWER C TRILLION Source - FASB 5

6 Improving Lease Accounting How will the new lease standard improve lease accounting? Results in a more faithful representation of a lessee s rights and obligations arising from leases Results in fewer opportunities for organizations to structure leasing transactions to achieve a particular outcome on the balance sheet Improves understanding and comparability of lessee s financial statements Aligns lessor accounting and sale and leaseback transaction guidance more closely to comparable revenue guidance in the new revenue recognition standard Provides users of financial statements with additional information about lessors leasing activities and lessors exposure to credit and asset risk as a result of leasing Clarifies the definition of a lease to address practice issues within current GAAP and to align concept of control, as used within the definition, more closely with control principle used in revenue recognition and consolidations Source - FASB 6

7 Scope Who is affected? The new lease standard affects all companies or other organizations that lease assets such as real estate, airplanes, ships, and construction and manufacturing equipment. Source - FASB 7

8 New Guidance Under the new lease standard, all lessees will recognize assets and liabilities for leases with lease terms of more than 12 months. Companies will record an asset related to the right to use the leased asset and a liability related to the lease obligation. 8

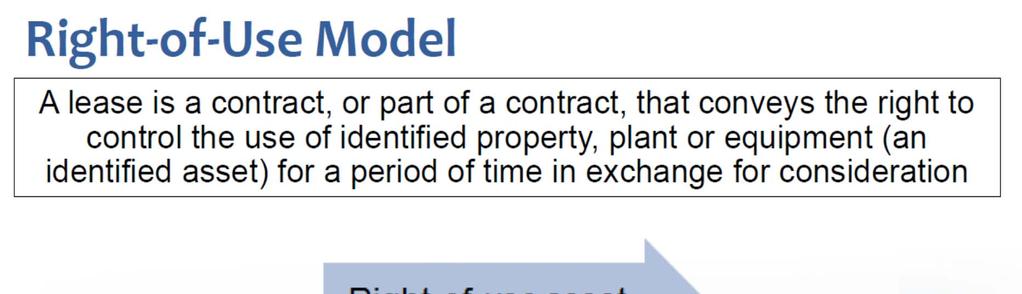

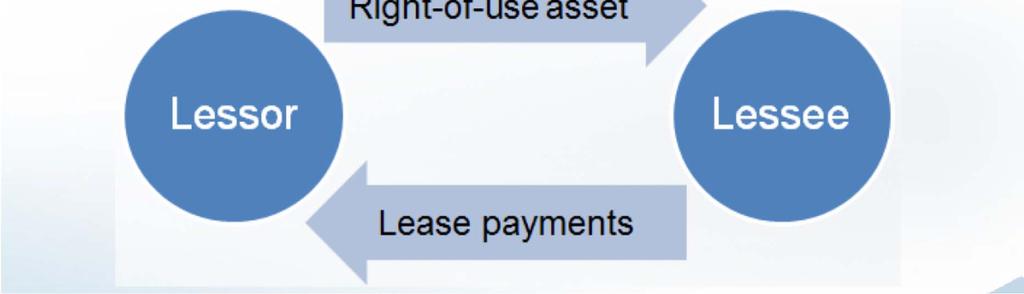

9 Right-of-Use Source - FASB 9

10 Scope Identifying a Lease Source - FASB 10

11 Accounting Models Source - FASB 11

12 Example Overview Sales Type Lease (from Lessor perspective) Customer contracts with Supplier to lease purification equipment over a five-year period and purchases disposable tablets and filters (disposables) used in operation of the equipment. The equipment has an estimated 5 year life, no residual value, and the standalone sales price is $150,000 (cost basis of $100,000). Contracted to sale disposables during the lease for $10 (cost basis of $5), which is not considered the standalone sales price of each disposable (est. at $12). Standalone price (A) Relative % (A /total) = (B) Payment (C) Allocated lease payment (B x C) Purification equipment $150, % $40,000 $28,600 Estimated disposables sold over contract term (1,000 per year for 5 years) 60, % 40,000 11,400 Total $210, % $40,000 12

13 How should Supplier account for this arrangement (commencement and first year) The equipment lease and sale of disposables are separate lease and nonlease components, respectively. The variable payments relate specifically to the nonlease component (sale of disposables) because the sale of disposables is not related to the usage of the leased purification equipment. In this example, we are assuming that Supplier allocates the variable payments to the lease and nonlease components. However, if a lessor believes that allocating the variable consideration entirely to the nonlease component is consistent with the allocation objective in ASC , then it should do so. 13

14 How should Supplier account for this arrangement (commencement and first year) Since the lease is a sales-type lease, Supplier would remove the asset from its balance sheet and record a receivable equal to the present value of the lease payments. The lease receivable is $142,857, calculated as ($150,000 total fixed payments + $50,000 estimate of variable consideration for disposables) ($150,000 selling price of equipment $210,000 combined selling price of equipment and disposables). For simplicity, discounting has been ignored in this example. 14

15 How should Supplier account for this arrangement (commencement of lease) Supplier would record the following journal entry at the beginning of the lease: Dr. Lease receivable $142,857 Dr. Cost of sales $100,000 Cr. Revenue $142,857 Cr. Inventory $100,000 15

16 How should Supplier account for this arrangement (first year) (carryforward from prior slide) Standalone price (A) Total $210, % $40,000 Supplier would record the following journal entries during the first year of the lease: Dr. Cash $40,000 Cr. Lease receivable $28,600 Cr. Sales revenue $11,400 Dr. Cost of sales $5,000 Relative % (A /total) = (B) Payment (C) Allocated lease payment (B x C) Purification equipment $150, % $40,000 $28,600 Estimated disposables sold over contract term (1,000 per year for 5 years) 60, % 40,000 11,400 Cr. Inventory $5,000 16

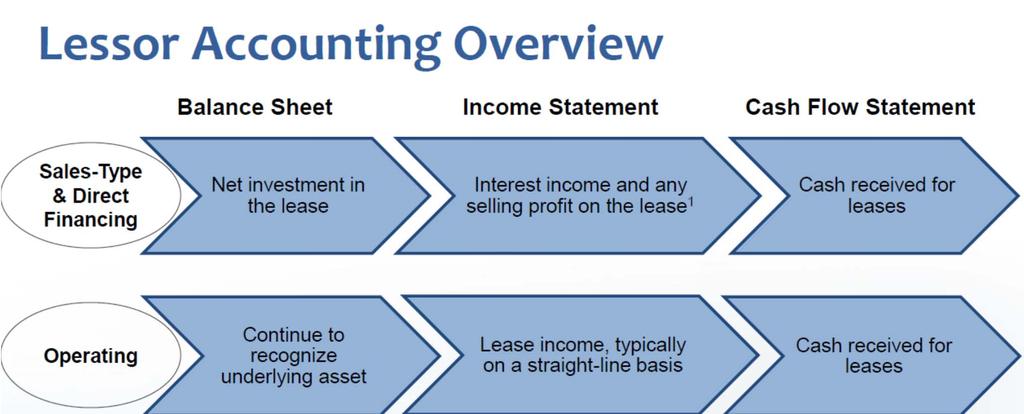

17 Accounting Models Source - FASB 17

18 Lessee Lease Classification Criteria Does the lease transfer ownership of the underlying asset to the lessee by the end of the lease term? Does the lease grant the lessee an option to purchase the underlying asset that the lessee is reasonably certain to exercise? Is the lease term for a major part of the remaining economic life of the underlying asset? Is the present value of the sum of the lease payments and any residual value guaranteed by the lessee, that is not otherwise included in the lease payments, substantially all of the fair value of the underlying asset? Is the underlying asset of such a specialized nature that it is expected to have no alternative use to the lessor at the end of the lease term? If YES to ANY, it is a Financing Lease If NO to ALL, it is an Operating Lease 18

19 Example Overview - Finance Lease (from lessee s perspective) Customer contracts with Supplier to lease purification equipment over a five-year period and purchases disposable tablets and filters (disposables) used in operation of the equipment. The equipment has an estimated 5 year life, no residual value, and the standalone sales price is $150,000 (cost basis of $100,000). Contracted to sale disposables during the lease for $10 (cost basis of $5), which is not considered the standalone sales price of each disposable (est. at $12). Standalone price (A) Relative % (A /total) = (B) Payment (C) Allocated lease payment (B x C) Purification equipment $150, % $40,000 $28,600 Estimated disposables sold over contract term (1,000 per year for 5 years) 60, % 40,000 11,400 Total $210, % $40,000 19

20 Example Overview - Finance Lease (from lessee s perspective) Additional Information: First annual payment of $30,000 is due at execution of the lease. Customer incurs $5,000 of initial direct costs, which are payable at execution. Customer calculates the initial lease liability at present value of the lease payments discounted using their incremental borrowing rate as the implicit rate is not readily available of $135,000. Initial measurement of lease liability $135,000 Initial direct costs 5,000 Initial measurement of rightof-use asset $140,000 20

21 How should Customer account for this arrangement Finance Lease (from lessee s perspective) Customer would record the following journal entry at the beginning of the finance lease: Dr. Right-of-use asset $135,000 Cr. Lease liability $135,000 Dr. Right-of-use asset $5,000 Cr. Accrued expense / cash $5,000 For each subsequent period, Customer would amortize the Right-of-use asset over the shorter of the lease term (5 years) or the useful life of the asset and recognize interest expense under the interest method (7%). Dr. Amortization expense $28,000 Cr. Right-of-use asset $28,000 Dr. Interest expense $9,400 Dr. Lease liability $20,600 Cr. Cash $30,000 21

22 Operating Lease Example Lessee Corp leases an automobile from Lessor Corp. The following table summarizes information about the lease and the leased asset: Source PwC Lease Accounting Guide 22

23 Operating Lease Example - Continued This lease is classified as an operating lease as none of the criteria for finance lease classification are met. The right-of-use asset and lease liability are $16,518. Source PwC Lease Accounting Guide 23

24 Operating Lease Example - Continued How would Lessee Corp measure the right-ofuse asset and lease liability over the lease term? Analysis: Lessee Corp is required to pay $500 per month for three years, so the total lease payments are $18,000 ($500 x 36 months). Lessee Corp would then calculate the straight-line lease expense to be recorded each period by dividing the total lease payments by the total number of periods. The monthly straight-line expense are equal as the lease does not contain any escalation provisions or other required or optional payments. Lessee Corp would calculate the amortization of the lease liability as shown on the table on the following page. This table is shown on an annual basis for simplicity; the schedule would be calculated on a monthly basis to reflect the frequency of the lease payments. Source PwC Lease Accounting Guide 24

25 Operating Lease Example - Continued Source PwC Lease Accounting Guide 25

26 Operating Lease Example - Continued The amortization of the right-of-use asset is calculated as the difference between the straight-line lease expense and the interest expense on the lease liability. The following table shows this calculation. This table is shown on an annual basis for simplicity; the schedule would be calculated on a monthly basis to reflect the frequency of the lease payments. Source PwC Lease Accounting Guide 26

27 Lessee Disclosures Source - FASB 27

28 Lessor Disclosures Source - FASB 28

29 Effective Dates New guidance is effective for fiscal years beginning after December 15, 2018 for the following: A public business entity A not-for-profit entity that has issued, or is a conduit bond obligor for, securities that are traded, listed or an over-the-counter market An employee benefit plan that files financial statements with the U.S. Securities and Exchange Commission (SEC) For all other organizations, the new guidance is effective for fiscal years beginning after December 15, Early application is permitted for all organizations. Source - FASB 29

30 Questions & Comments Brad Bonde Senior Manager, HC Services/Audit & Advisory

Miles CPA Review: FAR Updates

Miles CPA Review: FAR - 2019 Updates Summary of updates: - FAR-4.4: s [ASC 842] effective fiscal years beginning after Dec 15, 2018 (for issuers) and effective fiscal years beginning after Dec 15, 2019

Miles CPA Review: FAR - 2019 Updates Summary of updates: - FAR-4.4: s [ASC 842] effective fiscal years beginning after Dec 15, 2018 (for issuers) and effective fiscal years beginning after Dec 15, 2019

Deeper Dive Leases. Overview

Deeper Dive Leases Presented by: Shaun Johnson, CPA Dingus, Zarecor & Associates PLLC Overview Effective dates Big picture Objective, impact, and implementation Applicability and definition Initial recognition

Deeper Dive Leases Presented by: Shaun Johnson, CPA Dingus, Zarecor & Associates PLLC Overview Effective dates Big picture Objective, impact, and implementation Applicability and definition Initial recognition

Lease & Finance Accountants Conference. September The Westin Charlotte Charlotte, NC

Lease & Finance Accountants Conference September 11-13 The Westin Charlotte Charlotte, NC H A N D O U T S Lessor Accounting under ASC 842 EQUIPMENT LEASING AND FINANCE ASSOCIATION Presenters Rod Hurd Chief

Lease & Finance Accountants Conference September 11-13 The Westin Charlotte Charlotte, NC H A N D O U T S Lessor Accounting under ASC 842 EQUIPMENT LEASING AND FINANCE ASSOCIATION Presenters Rod Hurd Chief

Impact of lease accounting changes to corporate real estate

Impact of lease accounting changes to corporate real estate Overview In February 2016, the Financial Accounting Standards Board (FASB) issued its long-awaited revision to lease accounting Accounting Standards

Impact of lease accounting changes to corporate real estate Overview In February 2016, the Financial Accounting Standards Board (FASB) issued its long-awaited revision to lease accounting Accounting Standards

Technical Line FASB final guidance

No. 2016-09 14 April 2016 Technical Line FASB final guidance How the FASB s new leases standard will affect health care entities In this issue: Overview... 1 Key considerations... 3 Scope and scope exceptions...

No. 2016-09 14 April 2016 Technical Line FASB final guidance How the FASB s new leases standard will affect health care entities In this issue: Overview... 1 Key considerations... 3 Scope and scope exceptions...

Leases: Overview of the new guidance

Leases: Overview of the new guidance Prepared by: Richard Stuart, Partner, National Professional Standards Group, RSM US LLP richard.stuart@rsmus.com, +1 203 905 5027 March 2, 2016 Introduction On February

Leases: Overview of the new guidance Prepared by: Richard Stuart, Partner, National Professional Standards Group, RSM US LLP richard.stuart@rsmus.com, +1 203 905 5027 March 2, 2016 Introduction On February

Accounting and Auditing Update. Tennessee Chapter of hfma Spring Institute 2016 Presented by William C. Matheney FHFMA CPA and Meredith P.

Accounting and Auditing Update Tennessee Chapter of hfma Spring Institute 2016 Presented by William C. Matheney FHFMA CPA and Meredith P. Cate Today s Objectives Present an overview of pertinent recently

Accounting and Auditing Update Tennessee Chapter of hfma Spring Institute 2016 Presented by William C. Matheney FHFMA CPA and Meredith P. Cate Today s Objectives Present an overview of pertinent recently

The new accounting standard for leases. 27 March 2017

The new accounting standard for leases 27 March 2017 Disclaimer Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity.

The new accounting standard for leases 27 March 2017 Disclaimer Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity.

Technical Line FASB final guidance

No. 2019-01 3 January 2019 Technical Line FASB final guidance How the new leases standard affects automotive entities In this issue: Overview... 1 Recent standard setting activity... 2 Key considerations...

No. 2019-01 3 January 2019 Technical Line FASB final guidance How the new leases standard affects automotive entities In this issue: Overview... 1 Recent standard setting activity... 2 Key considerations...

The New Lease Accounting Standard. Hunter Mink, CPA, CCIFP Brian Rosenberg, CPA, MBA

The New Lease Accounting Standard Hunter Mink, CPA, CCIFP Brian Rosenberg, CPA, MBA 1 Agenda Introduction Lease Identification and Classification Lessee Accounting Other Considerations Disclosures Impact

The New Lease Accounting Standard Hunter Mink, CPA, CCIFP Brian Rosenberg, CPA, MBA 1 Agenda Introduction Lease Identification and Classification Lessee Accounting Other Considerations Disclosures Impact

Technical Line FASB final guidance

No. 2018-08 20 September 2018 Technical Line FASB final guidance How the new leases standard affects engineering and construction entities In this issue: Overview... 1 Key considerations... 2 Scope and

No. 2018-08 20 September 2018 Technical Line FASB final guidance How the new leases standard affects engineering and construction entities In this issue: Overview... 1 Key considerations... 2 Scope and

Accounting Update. Anne Cloutier, CPA, FHFMA Principal March 27, 2015

Accounting Update Anne Cloutier, CPA, FHFMA Principal March 27, 2015 Current Accounting for Leases Capital leases - a lessee recognizes leased assets and liabilities on the balance sheet. Operating leases

Accounting Update Anne Cloutier, CPA, FHFMA Principal March 27, 2015 Current Accounting for Leases Capital leases - a lessee recognizes leased assets and liabilities on the balance sheet. Operating leases

What Nonprofits Need to Know About the New Standards for Lease Accounting

The webcast will start at 1 p.m. Eastern Please note: Handout You can print or download the webcast handout at https://capincrouse.com/webcast-lease-accounting CPE CPE certificates will be emailed to you

The webcast will start at 1 p.m. Eastern Please note: Handout You can print or download the webcast handout at https://capincrouse.com/webcast-lease-accounting CPE CPE certificates will be emailed to you

Lease & Finance Accountants Conference. September The Westin Charlotte Charlotte, NC

Lease & Finance Accountants Conference September 11-13 The Westin Charlotte Charlotte, NC H A N D O U T S Basic Principles of Lessors under ASC 842 Mamta Shori, Wells Fargo Equipment Finance Joe Sebik,

Lease & Finance Accountants Conference September 11-13 The Westin Charlotte Charlotte, NC H A N D O U T S Basic Principles of Lessors under ASC 842 Mamta Shori, Wells Fargo Equipment Finance Joe Sebik,

Technical Line FASB final guidance

No. 2016-11 14 April 2016 Technical Line FASB final guidance How the FASB s new leases standard will affect real estate entities In this issue: Overview... 1 Key considerations... 2 Scope and scope exceptions...

No. 2016-11 14 April 2016 Technical Line FASB final guidance How the FASB s new leases standard will affect real estate entities In this issue: Overview... 1 Key considerations... 2 Scope and scope exceptions...

New leases standard ASC 842 Lessee - operating leases. Itai Gotlieb, Partner, Professional Practice July 2017

ASC 842 Lessee - operating leases Itai Gotlieb, Partner, Professional Practice July 2017 Overview Under Accounting Standards Codification (ASC) 842, Leases, lessees recognize assets and liabilities for

ASC 842 Lessee - operating leases Itai Gotlieb, Partner, Professional Practice July 2017 Overview Under Accounting Standards Codification (ASC) 842, Leases, lessees recognize assets and liabilities for

FASB/IASB Update Part II

American Accounting Association FASB/IASB Update Part II Tom Linsmeier FASB Member August 3, 2014 The views expressed in this presentation are those of the presenters. Official positions of the FASB/IASB

American Accounting Association FASB/IASB Update Part II Tom Linsmeier FASB Member August 3, 2014 The views expressed in this presentation are those of the presenters. Official positions of the FASB/IASB

Applying the new lease accounting standard

Applying the new lease accounting standard In February 26, the FASB issued Accounting Standards Update (ASU) No. 26-, Leases (codified as Accounting Standards Codification Topic (ASC) 842). ASC 842 introduces

Applying the new lease accounting standard In February 26, the FASB issued Accounting Standards Update (ASU) No. 26-, Leases (codified as Accounting Standards Codification Topic (ASC) 842). ASC 842 introduces

Welcome to Webinar: Implementing FASB s Updated Lease Accounting Standard ASU (Topic 842)

") Welcome to Webinar: Implementing FASB s Updated Lease Accounting Standard ASU 2016-02 (Topic 842) Presented by: Gelman, Rosenberg & Freedman CPAs Please note: Use the Question panel to speak with the administrator

Welcome to Webinar: Implementing FASB s Updated Lease Accounting Standard ASU 2016-02 (Topic 842) Presented by: Gelman, Rosenberg & Freedman CPAs Please note: Use the Question panel to speak with the administrator

Accounting and Auditing Update. Staci L. Brogan, CPA, Shareholder Patricia R. Giudici, CPA, Senior Manager Schneider Downs & Co. Inc.

Accounting and Auditing Update Staci L. Brogan, CPA, Shareholder Patricia R. Giudici, CPA, Senior Manager Schneider Downs & Co. Inc. Agenda Overview of the standard setting agenda Revenue recognition Lease

Accounting and Auditing Update Staci L. Brogan, CPA, Shareholder Patricia R. Giudici, CPA, Senior Manager Schneider Downs & Co. Inc. Agenda Overview of the standard setting agenda Revenue recognition Lease

Accounting and Auditing. Norman Mosrie, CPA, FMFMA, CHFP James Sutherland, CPA

Accounting and Auditing Norman Mosrie, CPA, FMFMA, CHFP James Sutherland, CPA Leases (ASU 2016-02; Topic 842) A lease contract conveys the right to use an asset (the underlying asset) for a period of time

Accounting and Auditing Norman Mosrie, CPA, FMFMA, CHFP James Sutherland, CPA Leases (ASU 2016-02; Topic 842) A lease contract conveys the right to use an asset (the underlying asset) for a period of time

REAL ESTATE PERSPECTIVE ON NEW LEASE ACCOUNTING STANDARDS

VALUATION & ADVISORY REAL ESTATE PERSPECTIVE ON NEW LEASE ACCOUNTING STANDARDS BY JOHN CORBETT, MAI, ASA, FRICS AND MARC R. SHAPIRO, MAI, MRICS INTRODUCTION The Financial Accounting Standards Board (FASB)

VALUATION & ADVISORY REAL ESTATE PERSPECTIVE ON NEW LEASE ACCOUNTING STANDARDS BY JOHN CORBETT, MAI, ASA, FRICS AND MARC R. SHAPIRO, MAI, MRICS INTRODUCTION The Financial Accounting Standards Board (FASB)

What private companies need to know about applying the new lease standard

What private companies need to know about applying the new lease standard In February 26, the FASB issued Accounting Standards Update (ASU) No. 26-, Leases (codified as Accounting Standards Codification

What private companies need to know about applying the new lease standard In February 26, the FASB issued Accounting Standards Update (ASU) No. 26-, Leases (codified as Accounting Standards Codification

7/30/2018. Health Care. A CHC-Focused Plan for the New Lease Accounting Standard

Health Care A CHC-Focused Plan for the New Lease Accounting Standard July 31, 2018 1 TO RECEIVE CPE CREDIT Individuals Participate in entire webinar Answer polls when they are provided Groups Group leader

Health Care A CHC-Focused Plan for the New Lease Accounting Standard July 31, 2018 1 TO RECEIVE CPE CREDIT Individuals Participate in entire webinar Answer polls when they are provided Groups Group leader

Measuring Lease Liabilities EQUIPMENT LEASING AND FINANCE ASSOCIATION

Measuring Lease Liabilities EQUIPMENT LEASING AND FINANCE ASSOCIATION Presenters Kerrie Cadugan, Executive Director, EY Barbara Galaini, Chief Accounting Officer of the Americas, Avolon The views expressed

Measuring Lease Liabilities EQUIPMENT LEASING AND FINANCE ASSOCIATION Presenters Kerrie Cadugan, Executive Director, EY Barbara Galaini, Chief Accounting Officer of the Americas, Avolon The views expressed

Summary of IFRS Exposure Draft Leases

The International Accounting Standards Board (IASB) recently issued a revised exposure draft (ED) relating to leases. Once these proposals are finalized the new guidance will replace the IAS 17 Leases.

The International Accounting Standards Board (IASB) recently issued a revised exposure draft (ED) relating to leases. Once these proposals are finalized the new guidance will replace the IAS 17 Leases.

Lease Accounting Standard Update ASU Presented by: Nicholas Hoefel, CPA Manager, Audit Services Group

Lease Accounting Standard Update ASU 2016-02 Presented by: Nicholas Hoefel, CPA Manager, Audit Services Group 1 Overview Introduction Background and current environment Effective dates and transition Key

Lease Accounting Standard Update ASU 2016-02 Presented by: Nicholas Hoefel, CPA Manager, Audit Services Group 1 Overview Introduction Background and current environment Effective dates and transition Key

Leases: A Comprehensive Update on the Joint Project

The Dbriefs Financial Reporting series presents: Leases: A Comprehensive Update on the Joint Project Bob Uhl, Deloitte & Touche LLP Trevor Farber, Deloitte & Touche LLP James Barker, Deloitte & Touche

The Dbriefs Financial Reporting series presents: Leases: A Comprehensive Update on the Joint Project Bob Uhl, Deloitte & Touche LLP Trevor Farber, Deloitte & Touche LLP James Barker, Deloitte & Touche

Technical Line FASB final guidance

No. 2018-18 13 December 2018 Technical Line FASB final guidance How the new leases standard affects life sciences entities In this issue: Overview... 1 Key considerations... 2 Scope and scope exceptions...

No. 2018-18 13 December 2018 Technical Line FASB final guidance How the new leases standard affects life sciences entities In this issue: Overview... 1 Key considerations... 2 Scope and scope exceptions...

IASB Staff Paper March 2011

IASB Staff Paper March 2011 Effect of board redeliberations on Exposure Draft Leases About this staff paper This staff paper indicates how the proposals in the Exposure Draft Leases would change as a result

IASB Staff Paper March 2011 Effect of board redeliberations on Exposure Draft Leases About this staff paper This staff paper indicates how the proposals in the Exposure Draft Leases would change as a result

Defining Issues May 2013, No

Defining Issues May 2013, No. 13-24 FASB and IASB Issue Revised Exposure Drafts on Lease Accounting The FASB and IASB (the Boards) recently issued revised joint exposure drafts (EDs) on proposed changes

Defining Issues May 2013, No. 13-24 FASB and IASB Issue Revised Exposure Drafts on Lease Accounting The FASB and IASB (the Boards) recently issued revised joint exposure drafts (EDs) on proposed changes

The joint leases project change is coming

No. 2010-4 18 June 2010 Technical Line Technical guidance on standards and practice issues The joint leases project change is coming What you need to know The proposed changes to the accounting for leases

No. 2010-4 18 June 2010 Technical Line Technical guidance on standards and practice issues The joint leases project change is coming What you need to know The proposed changes to the accounting for leases

Executive Summary. New leases standard Lessees

Executive Summary December 2018 The new leases standard focuses on increased transparency and comparability providing financial statement users with more information about an entity s leasing activities.

Executive Summary December 2018 The new leases standard focuses on increased transparency and comparability providing financial statement users with more information about an entity s leasing activities.

4/4/2018. GASB's New Leases Standard

GASB's New Leases Standard April 4, 2018 1 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing this webinar in a group Complete group attendance form

GASB's New Leases Standard April 4, 2018 1 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing this webinar in a group Complete group attendance form

Center for Plain English Accounting

Report April 18, 2018 Center for Plain English Accounting AICPA s National A&A Resource Center Debits and Credits Associated with New Lease Accounting Standard CPEA Lease Standard Implementation Series

Report April 18, 2018 Center for Plain English Accounting AICPA s National A&A Resource Center Debits and Credits Associated with New Lease Accounting Standard CPEA Lease Standard Implementation Series

Technical Line FASB final guidance

No. 2018-10 11 October 2018 Technical Line FASB final guidance How the new leases standard affects airlines In this issue: Overview... 1 Key considerations... 2 Scope and scope exceptions... 2 Definition

No. 2018-10 11 October 2018 Technical Line FASB final guidance How the new leases standard affects airlines In this issue: Overview... 1 Key considerations... 2 Scope and scope exceptions... 2 Definition

Lease Accounting and simplease Accounting Updates. Trevor Warren & Jason Reljac

Lease Accounting and simplease Accounting Updates Trevor Warren & Jason Reljac Today s Agenda Overview Scope and Definition of a Lease Lease Classification Lessee Accounting Financial Statement Impact

Lease Accounting and simplease Accounting Updates Trevor Warren & Jason Reljac Today s Agenda Overview Scope and Definition of a Lease Lease Classification Lessee Accounting Financial Statement Impact

The Financial Accounting Standards Board

V A L U A T I O N How the New Leases Standard May Impact Business Valuations By Judith H. O Dell, CPA, CVA The Financial Accounting Standards Board issued the 485 page Leases Standard (Topic 842) in February,

V A L U A T I O N How the New Leases Standard May Impact Business Valuations By Judith H. O Dell, CPA, CVA The Financial Accounting Standards Board issued the 485 page Leases Standard (Topic 842) in February,

New Lease Accounting Standards: Love at First Sight or Heartbreak?

New Lease Accounting Standards: Love at First Sight or Heartbreak? February 14, 2019 To Receive CPE Credit Individuals Participate in entire webinar Answer polls when they are provided Groups Group leader

New Lease Accounting Standards: Love at First Sight or Heartbreak? February 14, 2019 To Receive CPE Credit Individuals Participate in entire webinar Answer polls when they are provided Groups Group leader

Lease accounting scope & impacts

Leasing Lease accounting scope & impacts Scope What s in? All industries, all entities Arrangements that meet the definition of a lease Embedded leases within other arrangements What s out? Leases of:

Leasing Lease accounting scope & impacts Scope What s in? All industries, all entities Arrangements that meet the definition of a lease Embedded leases within other arrangements What s out? Leases of:

presentation for October 5, 2018

presentation for October 5, 2018 Proper Lease Analysis + Proper Technology = Successful Implementation Designed by Former Big 4 Auditors Built for Audit Efficiency Key Design Principles Ease of Use & Security

presentation for October 5, 2018 Proper Lease Analysis + Proper Technology = Successful Implementation Designed by Former Big 4 Auditors Built for Audit Efficiency Key Design Principles Ease of Use & Security

On the Horizon: Leases and Fiduciary Responsibilities

On the Horizon: Leases and Fiduciary Responsibilities Dean Michael Mead, Research Manager Florida School Finance Officers Association November 11, 2015 The views expressed in this presentation are those

On the Horizon: Leases and Fiduciary Responsibilities Dean Michael Mead, Research Manager Florida School Finance Officers Association November 11, 2015 The views expressed in this presentation are those

Click to edit Master title style REVENUE RECOGNITION Understanding the New Revenue Recognition Standard ASC 606

Click to edit Master title style REVENUE RECOGNITION Understanding the New Revenue Recognition Standard ASC 606 9/7/2017 0 Agenda Overview of ASC 606 Review of the five-step process Accounting for contract

Click to edit Master title style REVENUE RECOGNITION Understanding the New Revenue Recognition Standard ASC 606 9/7/2017 0 Agenda Overview of ASC 606 Review of the five-step process Accounting for contract

Is Your Operating Lease An Asset or Liability? It s Now Both

MFM Annual Conference Is Your Operating Lease An Asset or Liability? It s Now Both 23 May 2016-1:30 pm 2:20 pm Disclaimer These slides are for educational purposes only and are not intended, and should

MFM Annual Conference Is Your Operating Lease An Asset or Liability? It s Now Both 23 May 2016-1:30 pm 2:20 pm Disclaimer These slides are for educational purposes only and are not intended, and should

Proposed New Accounting Standards For Leases

Relationships backed by performance. Proposed New Accounting Standards For Leases Doug Richardson Live Seminar 9:00am 10:30am June 21 2012 Overview and Background Leases serve a vital role in many entities

Relationships backed by performance. Proposed New Accounting Standards For Leases Doug Richardson Live Seminar 9:00am 10:30am June 21 2012 Overview and Background Leases serve a vital role in many entities

2018 Accounting & Auditing Update P R E S E N T E D B Y : D A N I E L L E Z I M M E R M A N & A N D R E A S A R T I N

2018 Accounting & Auditing Update P R E S E N T E D B Y : D A N I E L L E Z I M M E R M A N & A N D R E A S A R T I N AGENDA Leases FASB & GASB Revenue Recognition FASB 2 FASB ASU 2016-02, Leases (Topic

2018 Accounting & Auditing Update P R E S E N T E D B Y : D A N I E L L E Z I M M E R M A N & A N D R E A S A R T I N AGENDA Leases FASB & GASB Revenue Recognition FASB 2 FASB ASU 2016-02, Leases (Topic

IFRS 16 LEASES. Page 1 of 21

IFRS 16 LEASES OBJECTIVE The objective is to ensure that lessees and lessors provide relevant information in a manner that faithfully represents those transactions. This information gives a basis for users

IFRS 16 LEASES OBJECTIVE The objective is to ensure that lessees and lessors provide relevant information in a manner that faithfully represents those transactions. This information gives a basis for users

Chapter 15 Leases 15-1

Chapter 15 Leases 1. Why Leasing sometimes makes more sense 2. The accounting issues in recording a lease transaction 3. The types of contractual provisions in lease 4. The lease classification: capital

Chapter 15 Leases 1. Why Leasing sometimes makes more sense 2. The accounting issues in recording a lease transaction 3. The types of contractual provisions in lease 4. The lease classification: capital

Technical Line FASB final guidance

No. 2018-15 6 December 2018 Technical Line FASB final guidance How the new leases standard affects consumer products and retail entities In this issue: Overview... 1 Recent standard-setting activity...

No. 2018-15 6 December 2018 Technical Line FASB final guidance How the new leases standard affects consumer products and retail entities In this issue: Overview... 1 Recent standard-setting activity...

IFRS 16: Leases; a New Era of Lease Accounting!

The journal is running a series of updates on IFRS, IAS, IFRIC and SIC. The updates mostly collected from different sources of IASB publication, seminars, workshop & IFRS website. This issue is based on

The journal is running a series of updates on IFRS, IAS, IFRIC and SIC. The updates mostly collected from different sources of IASB publication, seminars, workshop & IFRS website. This issue is based on

International Financial Reporting Standard 16 Leases. Objective. Scope. Recognition exemptions (paragraphs B3 B8) IFRS 16

IFRS 16") International Financial Reporting Standard 16 Leases Objective 1 This Standard sets out the principles for the recognition, measurement, presentation and disclosure of leases. The objective is to ensure

International Financial Reporting Standard 16 Leases Objective 1 This Standard sets out the principles for the recognition, measurement, presentation and disclosure of leases. The objective is to ensure

Defining Issues. FASB and IASB Enter Home Stretch in Redeliberations on Lease Accounting but on Different Tracks. Key Facts. October 2014, No.

Defining Issues October 2014, No. 14-46 FASB and IASB Enter Home Stretch in Redeliberations on Lease Accounting but on Different Tracks At their July and October joint meetings, the FASB and the IASB (the

Defining Issues October 2014, No. 14-46 FASB and IASB Enter Home Stretch in Redeliberations on Lease Accounting but on Different Tracks At their July and October joint meetings, the FASB and the IASB (the

GASB 87. OVERVIEW: Supersedes GASB s 13 and 62 (paragraphs ).

.") Leases OVERVIEW: Supersedes GASB s 13 and 62 (paragraphs 211-271). Will require significant changes from its current practice, particularly in the accounting for operating leases Effective for reporting

Leases OVERVIEW: Supersedes GASB s 13 and 62 (paragraphs 211-271). Will require significant changes from its current practice, particularly in the accounting for operating leases Effective for reporting

IFRS 16 : Lease accounting

IFRS 16 : Lease accounting Effective for accounting periods beginning on or after 1 January 2019 December 2017 IFRS 16: Lease accounting The IASB published the new IFRS 16 lease standard, in order to avoid

IFRS 16 : Lease accounting Effective for accounting periods beginning on or after 1 January 2019 December 2017 IFRS 16: Lease accounting The IASB published the new IFRS 16 lease standard, in order to avoid

Implementing the New Lease Guidance

Implementing the New Lease Guidance October 22, 2018 2018 Crowe LLP 2018 Crowe LLP Agenda Background Scope Effective dates & transition requirements Lessee accounting model Lessor accounting model Specialized

Implementing the New Lease Guidance October 22, 2018 2018 Crowe LLP 2018 Crowe LLP Agenda Background Scope Effective dates & transition requirements Lessee accounting model Lessor accounting model Specialized

Heads Up. FASB Draws a Bright Line Through Operating Leases Proposed ASU Revamps Lease. Accounting. The ED, released by the FASB as a proposed

August 17, 2010 Volume 17, Issue 27 Heads Up In This Issue: Background Effective Date In a Nutshell Scope Lessee Accounting Lessor Accounting Presentation and Disclosures Transition The ED, released by

August 17, 2010 Volume 17, Issue 27 Heads Up In This Issue: Background Effective Date In a Nutshell Scope Lessee Accounting Lessor Accounting Presentation and Disclosures Transition The ED, released by

ASC 842: Leases. Presented by: Maxwell Locke & Ritter LLP June 15, Maxwell Locke & Ritter

ASC 842: Leases Presented by: Maxwell Locke & Ritter LLP June 15, 2018 The New Lease Standard FASB ASC 842, Leases Supersedes FASB ASC 840, Leases Effective for calendar year-end public companies in 2019;

ASC 842: Leases Presented by: Maxwell Locke & Ritter LLP June 15, 2018 The New Lease Standard FASB ASC 842, Leases Supersedes FASB ASC 840, Leases Effective for calendar year-end public companies in 2019;

Lease Accounting Standard

Lease Accounting Standard AGA/EEI Spring Accounting Conference May 22, 2017 Lease Identification & Lease Classification Lease identification Identified asset Control over use Lease Asset is explicitly

Lease Accounting Standard AGA/EEI Spring Accounting Conference May 22, 2017 Lease Identification & Lease Classification Lease identification Identified asset Control over use Lease Asset is explicitly

Leases ASU September 20, 2017

Leases ASU 2016-02 September 20, 2017 Meet the Speakers Tonisha Spratte, CPA Senior Accountant Cherry Bekaert tspratte@cbh.com Matthew Mars Senior Accountant Cherry Bekaert mmars@cbh.com Agenda What is

Leases ASU 2016-02 September 20, 2017 Meet the Speakers Tonisha Spratte, CPA Senior Accountant Cherry Bekaert tspratte@cbh.com Matthew Mars Senior Accountant Cherry Bekaert mmars@cbh.com Agenda What is

The New Lease Accounting Standards

The New Lease Accounting Standards 4 CPE Hours d PDH Academy PO Box 449 Pewaukee, WI 53072 www.pdhacademy.com pdhacademy@gmail.com 888-564-9098 CONTINUING EDUCATION for Certified Public Accountants THE

The New Lease Accounting Standards 4 CPE Hours d PDH Academy PO Box 449 Pewaukee, WI 53072 www.pdhacademy.com pdhacademy@gmail.com 888-564-9098 CONTINUING EDUCATION for Certified Public Accountants THE

Defining Issues. FASB and IASB Take Divergent Paths on Key Aspects of Lease Accounting. March 2014, No Key Facts

Defining Issues March 2014, No. 14-17 FASB and IASB Take Divergent Paths on Key Aspects of Lease Accounting At their March 18-19 meeting to redeliberate the proposals in their 2013 exposure drafts (EDs)

Defining Issues March 2014, No. 14-17 FASB and IASB Take Divergent Paths on Key Aspects of Lease Accounting At their March 18-19 meeting to redeliberate the proposals in their 2013 exposure drafts (EDs)

Defining Issues. FASB Completes Technical Redeliberations on Leases. October 2015, No Key Facts. Key Impacts

Defining Issues October 2015, No. 15-47 FASB Completes Technical Redeliberations on Leases The FASB met on October 7 to discuss comments received and related follow-up issues on the external review of

Defining Issues October 2015, No. 15-47 FASB Completes Technical Redeliberations on Leases The FASB met on October 7 to discuss comments received and related follow-up issues on the external review of

Agenda. Monday, August 14, Section One The FASB s New Lease Accounting Standard. 8:30 Introduction to the new Lease Accounting Model Overview

Lease and Revenue Recognition Accounting Workshop Hosted by: Smith and Gesteland August 14 15, 2017 Madison Marriott West (This workshop qualifies for 16 hours of CPE) Monday, August 14, 2017 Agenda Section

Lease and Revenue Recognition Accounting Workshop Hosted by: Smith and Gesteland August 14 15, 2017 Madison Marriott West (This workshop qualifies for 16 hours of CPE) Monday, August 14, 2017 Agenda Section

Defining Issues. FASB and IASB Continue Discussions on Lease Accounting. Key Facts. June 2014, No

Defining Issues June 2014, No. 14-29 FASB and IASB Continue Discussions on Lease Accounting During the second quarter of 2014, the FASB and IASB (the Boards) continued redeliberations on the proposals

Defining Issues June 2014, No. 14-29 FASB and IASB Continue Discussions on Lease Accounting During the second quarter of 2014, the FASB and IASB (the Boards) continued redeliberations on the proposals

Preview of the New Exposure Draft of the Lease Accounting Project Key elements and commentary

Preview of the New Exposure Draft of the Lease Accounting Project Key elements and commentary Prepared by Bill Bosco, Leasing 101 www.leasing-101.com The Financial Accounting Standards Board (FASB) and

Preview of the New Exposure Draft of the Lease Accounting Project Key elements and commentary Prepared by Bill Bosco, Leasing 101 www.leasing-101.com The Financial Accounting Standards Board (FASB) and

In February 2016, FASB issued Accounting Standards. An Analysis of the New Sale and Leaseback Guidance. DEPARTMENTS I Accounting.

An Analysis of the New Sale and Leaseback Guidance By Josef Rashty In February 2016, FASB issued Accounting Standards Update (ASU) 2016-02, Leases (Topic 842). Topic 842 will supersede the existing lease

An Analysis of the New Sale and Leaseback Guidance By Josef Rashty In February 2016, FASB issued Accounting Standards Update (ASU) 2016-02, Leases (Topic 842). Topic 842 will supersede the existing lease

Leasing standard A comprehensive look at the new model and its impact

Leasing standard A comprehensive look at the new model and its impact No. US2016-02(supplement) December 14, 2016 What s inside: Overview... 1 Scope 2 Effective date and transition.. 2 Impact. 2 Embedded

Leasing standard A comprehensive look at the new model and its impact No. US2016-02(supplement) December 14, 2016 What s inside: Overview... 1 Scope 2 Effective date and transition.. 2 Impact. 2 Embedded

ASC 842 (Leases)

") ASC 842 (Leases) On February 25, 2016 the Financial Accounting Standards Board of the United States (FASB) issued substantial new guidance on the treatment of leases for both lessees and lessors. The FASB

ASC 842 (Leases) On February 25, 2016 the Financial Accounting Standards Board of the United States (FASB) issued substantial new guidance on the treatment of leases for both lessees and lessors. The FASB

Lease Accounting and Loan Covenants: What is the Impact?

Lease Accounting and Loan Covenants: What is the Impact? Monday June 26, 2017 9:15 AM 10:30 AM Presented by: Charlie Shannon Partner Moss Adams LLP 8750 N. Central Expressway, Suite 300 Dallas, TX 75231

Lease Accounting and Loan Covenants: What is the Impact? Monday June 26, 2017 9:15 AM 10:30 AM Presented by: Charlie Shannon Partner Moss Adams LLP 8750 N. Central Expressway, Suite 300 Dallas, TX 75231

Clay L. Pilgrim, CPA, CFE, CFF. What Financial Statement Preparers Need to Know About GASB s New Lease Accounting Proposal.

Clay L. Pilgrim, CPA, CFE, CFF What Financial Statement Preparers Need to Know About GASB s New Lease Accounting Proposal Today s Presenter Clay Pilgrim, CPA, CFE, CFF is a partner with Rushton & Company,

Clay L. Pilgrim, CPA, CFE, CFF What Financial Statement Preparers Need to Know About GASB s New Lease Accounting Proposal Today s Presenter Clay Pilgrim, CPA, CFE, CFF is a partner with Rushton & Company,

Topic 842 Technical Corrections Summary of Comments Received

Contact(s) David Hoyer Co-Author Ext. 462 Andy Bologna Co-Author Ext. 356 Thomas Faineteau Co-Author Ext. 362 Chris Roberge Co-Author Ext. 274 Amy Park Co-Author Ext. 476 Shayne Kuhaneck Assistant Director

Contact(s) David Hoyer Co-Author Ext. 462 Andy Bologna Co-Author Ext. 356 Thomas Faineteau Co-Author Ext. 362 Chris Roberge Co-Author Ext. 274 Amy Park Co-Author Ext. 476 Shayne Kuhaneck Assistant Director

Financial Computer Systems Inc. (203)

") Introduction to ASC 842 and EZLease Financial Computer Systems Inc. www.ezlease.net (203) 652-1375 The road to ASC 842 Begun in July 2006; joint project of FASB & IASB Primary purpose: Put lessee operating

Introduction to ASC 842 and EZLease Financial Computer Systems Inc. www.ezlease.net (203) 652-1375 The road to ASC 842 Begun in July 2006; joint project of FASB & IASB Primary purpose: Put lessee operating

Preparing for the new ASC 842 Leasing Standard Challenges and Solutions. August 24, 2017

Preparing for the new ASC 842 Leasing Standard Challenges and Solutions August 24, 2017 Learning objectives Define leasing implications related to recently revised FASB standard Differentiate between new

Preparing for the new ASC 842 Leasing Standard Challenges and Solutions August 24, 2017 Learning objectives Define leasing implications related to recently revised FASB standard Differentiate between new

Lease Accounting Is Final Time to Prepare for Implementation

Copyright 2016 by the Construction Financial Management Association (CFMA). All rights reserved. This article first appeared in CFMA Building Profits (a member-only benefit) and is reprinted with permission.

Copyright 2016 by the Construction Financial Management Association (CFMA). All rights reserved. This article first appeared in CFMA Building Profits (a member-only benefit) and is reprinted with permission.

No February Leases (Topic 842) An Amendment of the FASB Accounting Standards Codification

An Amendment of the FASB Accounting Standards Codification") No. 2016-02 February 2016 Leases (Topic 842) An Amendment of the FASB Accounting Standards Codification The FASB Accounting Standards Codification is the source of authoritative generally accepted accounting

No. 2016-02 February 2016 Leases (Topic 842) An Amendment of the FASB Accounting Standards Codification The FASB Accounting Standards Codification is the source of authoritative generally accepted accounting

Edison Electric Institute and American Gas Association New Lease Standard

Edison Electric Institute and American Gas Association New Lease Standard May 16, 2016 Disclaimer The information contained herein is of a general nature and is not intended to address the circumstances

Edison Electric Institute and American Gas Association New Lease Standard May 16, 2016 Disclaimer The information contained herein is of a general nature and is not intended to address the circumstances

New Developments Summary

July 10, 2018 NDS 2018-07 New Developments Summary Leases in transition New leasing standard provides detailed transition guidance Summary For most entities, one of the more complex aspects of implementing

July 10, 2018 NDS 2018-07 New Developments Summary Leases in transition New leasing standard provides detailed transition guidance Summary For most entities, one of the more complex aspects of implementing

Exposure Draft. Indian Accounting Standard (Ind AS) 116 Leases. (Last date for Comments: August 31, 2017)

116 Leases. (Last date for Comments: August 31, 2017)") ED/Ind AS/2017/06 Exposure Draft Indian Accounting Standard (Ind AS) 116 Leases (Last date for Comments: August 31, 2017) Issued by Accounting Standards Board The Institute of Chartered Accountants of

ED/Ind AS/2017/06 Exposure Draft Indian Accounting Standard (Ind AS) 116 Leases (Last date for Comments: August 31, 2017) Issued by Accounting Standards Board The Institute of Chartered Accountants of

A Review of IFRS 16 Leases By Tan Liong Tong

A Review of IFRS 16 Leases By Tan Liong Tong In April 2016, the MASB issued MFRS 16 Leases that is identical to IFRS 16 Leases issued by the IASB in January 2016. The effective date of this new MFRS is

A Review of IFRS 16 Leases By Tan Liong Tong In April 2016, the MASB issued MFRS 16 Leases that is identical to IFRS 16 Leases issued by the IASB in January 2016. The effective date of this new MFRS is

CONTACT(S) Danielle Zeyher Patrina Buchanan

Danielle Zeyher Patrina Buchanan") IASB Agenda ref 3B STAFF PAPER November 2013 FASB IASB Meeting Project Leases Paper topic Redeliberations Plan CONTACT(S) Danielle Zeyher dtzeyher@fasb.org +1 203 956 5265 Patrina Buchanan pbuchanan@ifrs.org

IASB Agenda ref 3B STAFF PAPER November 2013 FASB IASB Meeting Project Leases Paper topic Redeliberations Plan CONTACT(S) Danielle Zeyher dtzeyher@fasb.org +1 203 956 5265 Patrina Buchanan pbuchanan@ifrs.org

FASB and IASB Continue Making Decisions on Lease Accounting

Accounting Journal Entry FASB and IASB Continue Making Decisions on Lease Accounting March 28, 2011 At recent meetings, the FASB and IASB (the boards ) have continued to make progress on the leases project,

Accounting Journal Entry FASB and IASB Continue Making Decisions on Lease Accounting March 28, 2011 At recent meetings, the FASB and IASB (the boards ) have continued to make progress on the leases project,

Technical Line FASB final guidance

No. 2016-03 31 March 2016 Technical Line FASB final guidance A closer look at the new leases standard The new leases standard requires lessees to recognize most leases on their balance sheets. What you

No. 2016-03 31 March 2016 Technical Line FASB final guidance A closer look at the new leases standard The new leases standard requires lessees to recognize most leases on their balance sheets. What you

LEASES & HOT TOPICS PRESENTED BY: JASON MYERS & BRYAN CALLAHAN

LEASES & HOT TOPICS PRESENTED BY: JASON MYERS & BRYAN CALLAHAN LEASES PROJECT Summary of Key Changes & Impact 2 KEY CHANGES Lessee (the contractor usually) Requires recognition of most leases on their

LEASES & HOT TOPICS PRESENTED BY: JASON MYERS & BRYAN CALLAHAN LEASES PROJECT Summary of Key Changes & Impact 2 KEY CHANGES Lessee (the contractor usually) Requires recognition of most leases on their

Section 12 Accounting for Leases Accounting by the Lessor and Lessee

Section 12 Accounting for Leases Accounting by the Lessor and Lessee 15-1 A lease is an agreement in which the lessor conveys the right to use property, plant, or equipment, usually for a stated period

Section 12 Accounting for Leases Accounting by the Lessor and Lessee 15-1 A lease is an agreement in which the lessor conveys the right to use property, plant, or equipment, usually for a stated period

GASBs Presented by: William Blend, CPA, CFE

GASBs 87-89 Presented by: William Blend, CPA, CFE Leases: Statement 87 Effective Date and General Implementation Effective for Florida fiscal year end 2021. Earlier application is encouraged. Leases should

GASBs 87-89 Presented by: William Blend, CPA, CFE Leases: Statement 87 Effective Date and General Implementation Effective for Florida fiscal year end 2021. Earlier application is encouraged. Leases should

Lease Accounting - New Changes in US, International and Government Accounting Standards

Lease Accounting - New Changes in US, International and Government Accounting Standards Roberta J. Cable, Ph.D., CMA Patricia Healy, CPA, CMA Lubin School of Business Administration, Pace University, USA

Lease Accounting - New Changes in US, International and Government Accounting Standards Roberta J. Cable, Ph.D., CMA Patricia Healy, CPA, CMA Lubin School of Business Administration, Pace University, USA

GASB 87 - Leases. South Carolina Association of CPAs Fall Fest November 16, 2018 Mauldin & Jenkins

November 16, 2018 Mauldin & Jenkins 800-277-0050 www.mjcpa.com GASB 87 - Leases Effective for periods beginning after December 15, 2019 - December 31, 2020 or June 30, 2021 or September 30, 2021 Amends

November 16, 2018 Mauldin & Jenkins 800-277-0050 www.mjcpa.com GASB 87 - Leases Effective for periods beginning after December 15, 2019 - December 31, 2020 or June 30, 2021 or September 30, 2021 Amends

A New Lease on Life: The GASB s New Accounting for Leases

Tuesday, May 23, 2017 2:00 3:15PM A New Lease on Life: The GASB s New Accounting for Leases MODERATOR Frances Lee Deputy Chief Financial Officer San Francisco Public Utilities Commission SPEAKERS Stephen

Tuesday, May 23, 2017 2:00 3:15PM A New Lease on Life: The GASB s New Accounting for Leases MODERATOR Frances Lee Deputy Chief Financial Officer San Francisco Public Utilities Commission SPEAKERS Stephen

IMPACTS OF NEW LEASE ACCOUNTING STANDARD WHAT DOES IT MEAN TO ME? Jessica Richter, CPA.CITP, CISA Jamie Becker June 11, 2018

IMPACTS OF NEW LEASE ACCOUNTING STANDARD WHAT DOES IT MEAN TO ME? Jessica Richter, CPA.CITP, CISA Jamie Becker June 11, 2018 3 AGENDA ASC 842 Leases, ASU 2016-02 What s new Comparison with today s rules

IMPACTS OF NEW LEASE ACCOUNTING STANDARD WHAT DOES IT MEAN TO ME? Jessica Richter, CPA.CITP, CISA Jamie Becker June 11, 2018 3 AGENDA ASC 842 Leases, ASU 2016-02 What s new Comparison with today s rules

Accounting Standards Codification Topic 842

Accounting Standards Codification Topic 842 Leases RISK & TRANSACTION ADVISORY MBAFCPA.COM January 2018 Dear Clients and Other Friends, In February 2016, the Financial Accounting Standards Board (FASB)

Accounting Standards Codification Topic 842 Leases RISK & TRANSACTION ADVISORY MBAFCPA.COM January 2018 Dear Clients and Other Friends, In February 2016, the Financial Accounting Standards Board (FASB)

Accounting For Leases

C hapter 21 Accounting For Leases Intermediate Accounting 10th edition Nikolai Bazley Jones An electronic presentation by Norman Sunderman Angelo State University COPYRIGHT 2007 Thomson South-Western,

C hapter 21 Accounting For Leases Intermediate Accounting 10th edition Nikolai Bazley Jones An electronic presentation by Norman Sunderman Angelo State University COPYRIGHT 2007 Thomson South-Western,

IFRS Project Insights Leases

IFRS Project Insights Leases The IASB and FASB ( the Boards ) published a Discussion Paper (DP) setting out a proposed lessee accounting model in March 2009. The proposed accounting model has evolved since

IFRS Project Insights Leases The IASB and FASB ( the Boards ) published a Discussion Paper (DP) setting out a proposed lessee accounting model in March 2009. The proposed accounting model has evolved since

47.1% of organizations concerned about their ability to implement

Leases: Not Just for the 1 Lease Standard - Statistics 10 year project In 2014, $3.0 trillion in off-balance sheet lease commitments 47.1% of organizations concerned about their ability to implement 2

Leases: Not Just for the 1 Lease Standard - Statistics 10 year project In 2014, $3.0 trillion in off-balance sheet lease commitments 47.1% of organizations concerned about their ability to implement 2

Sri Lanka Accounting Standard - SLFRS 16. Leases

Sri Lanka Accounting Standard - SLFRS 16 Leases CONTENTS from paragraph SRI LANKA ACCOUNTING STANDARD - SLFRS 16 LEASES INTRODUCTION OBJECTIVE 1 SCOPE 3 RECOGNITION EXEMPTIONS 5 IDENTIFYING A LEASE 9 Separating

Sri Lanka Accounting Standard - SLFRS 16 Leases CONTENTS from paragraph SRI LANKA ACCOUNTING STANDARD - SLFRS 16 LEASES INTRODUCTION OBJECTIVE 1 SCOPE 3 RECOGNITION EXEMPTIONS 5 IDENTIFYING A LEASE 9 Separating

Lease Update. June 2017 Addison, Texas

Lease Update June 2017 Addison, Texas William Bill Schneider CPA, CGMA Bill is an Audit Director at AT&T. AT&T delivers advanced mobile services, next-generation TV, highspeed internet and smart solutions

Lease Update June 2017 Addison, Texas William Bill Schneider CPA, CGMA Bill is an Audit Director at AT&T. AT&T delivers advanced mobile services, next-generation TV, highspeed internet and smart solutions

Technical Line FASB final guidance

No. 2018-11 11 October 2018 Technical Line FASB final guidance How the new leases standard affects telecom and media and entertainment entities In this issue: Overview... 1 Key considerations... 2 Scope

No. 2018-11 11 October 2018 Technical Line FASB final guidance How the new leases standard affects telecom and media and entertainment entities In this issue: Overview... 1 Key considerations... 2 Scope

In December 2003 the IASB issued a revised IAS 17 as part of its initial agenda of technical projects.

IFRS Standard 16 Leases In April 2001 the International Accounting Standards Board (IASB) adopted IAS 17 Leases, which had originally been issued by the International Accounting Standards Committee (IASC)

IFRS Standard 16 Leases In April 2001 the International Accounting Standards Board (IASB) adopted IAS 17 Leases, which had originally been issued by the International Accounting Standards Committee (IASC)

THE NEW LEASE ACCOUNTING STANDARD

THE NEW LEASE ACCOUNTING STANDARD May 30, 2018 BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited by guarantee, and forms part

THE NEW LEASE ACCOUNTING STANDARD May 30, 2018 BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited by guarantee, and forms part

FASB Update. FASB Exempts Private Companies from Variable Interest Entity Guidance Affects: Private Companies

FASB Update New Guidance Raises the Threshold for Discontinued Operations On April 10, the FASB issued ASU 2014-08, Reporting Discontinued Operations and Disclosures of Disposals of Components of an Entity,

FASB Update New Guidance Raises the Threshold for Discontinued Operations On April 10, the FASB issued ASU 2014-08, Reporting Discontinued Operations and Disclosures of Disposals of Components of an Entity,

New Zealand Equivalent to International Financial Reporting Standard 16 Leases (NZ IFRS 16)

") New Zealand Equivalent to International Financial Reporting Standard 16 Leases (NZ IFRS 16) Issued February 2016 This Standard was issued on 11 February 2016 by the New Zealand Accounting Standards Board

New Zealand Equivalent to International Financial Reporting Standard 16 Leases (NZ IFRS 16) Issued February 2016 This Standard was issued on 11 February 2016 by the New Zealand Accounting Standards Board