Property Tax Guide for Wisconsin Manufactured and Mobile Home Owners

|

|

|

- Dortha Dalton

- 6 years ago

- Views:

Transcription

1 Property Tax Guide for Wisconsin Manufactured and Mobile Home Owners 2013 Wisconsin Department of Revenue Division of State & Local Finance Office of Assessment Practices P.O. Box 8971 Madison, WI Prop 075 (R. 12/12)

2 Property Tax Guide for Wisconsin Manufactured and Mobile Home Owners Preface The questions and answers in this booklet provide information about manufactured and mobile home property assessment and taxation in Wisconsin. The narrative provides general information and does not deal with legal details. Should you want additional information about your assessment, please contact your local assessor. Wisconsin Department of Revenue Office of Assessment Practices, M/S 6-97 P.O. Box 8971 Madison, WI Copies are available for download in Adobe Acrobat format at the following Internet address under Quick Links - Publications - Government - Property Tax heading:

3 Property Tax Guide for Wisconsin Manufactured and Mobile Home Owners Table of Contents Introduction... 1 What is General Property?... 1 What are the components of the general property tax?... 1 Who determines the assessed value of the taxable property?... 1 Assessment Process... 1 What is an assessment and what is its purpose?... 1 What is meant by assessment classification?... 2 How are assessments made for property classified as residential, commercial, manufacturing, productive forest, and other?... 2 How are assessments made for personal property?... 2 Who makes the assessment?... 2 Can the assessment on my property be raised even if the assessor has never been inside the Manufactured or mobile home?... 2 Will I be notified if there is a change in my assessment?... 3 How can I find out about my assessment?... 3 Can property be assessed higher or lower than market value?... 3 Manufactured and Mobile Home Assessments... 3 Overview... 3 What is a mobile home?... 4 What is a manufactured home?... 4 What are camping trailers and recreational mobile homes?... 4 Are mobile homes real or personal property?... 5 Are any mobile homes exempt from property tax?... 5 If a mobile home is on the owner s land and is connected to a well and septic tank and supported by cement blocks, can the assessor classify the mobile home as real estate?... 5 Does the fact that the wheels are attached to a mobile home make it exempt?... 6 How should the assessor measure a mobile home to determine if it qualifies for exemption?... 6 If the town charges a monthly municipal permit fee for a mobile home, is there a property tax in addition to the fee?... 7 Are recreational motor homes taxed as mobile homes?... 7 How can someone appeal the property assessment placed on a mobile home?... 7 Can the Board of Review exempt mobile homes?... 7 Are a dealer s vacant mobile homes displayed for sale on the sales lot taxable?... 8 Vacant units that have been repossessed by financial institutions Examples Recreational Mobile Home... 9

4 Property Tax Guide for Wisconsin Manufactured and Mobile Home Owners Table of Contents, cont. Overview of Manufactured and Mobile Home Property Taxes Wisconsin Act 68 Trespass and Revaluation Notice Definitions of Terms Flowchart of the Assessment Appeal Process Equalization District Offices... 17

5 What is General Property? Introduction General Property is defined by statute as including all taxable real and personal property except that which is taxed under special provisions, such as low-grade iron ore, utility, Forest Crop, Woodland Tax, and Managed Forest property. The terms real property, real estate, and land include the land and all buildings, improvements, fixtures, and rights and privileges connected with the land. The term personal property includes all goods, wares, merchandise, chattels, and effects of any nature or description having any marketable value and not included in the term real property. Under general property tax law all property as defined above is taxable unless expressly exempted by the legislature. Because Manufactured or Mobile Homes can be assessed either as Real Estate or Personal Property, subject to a monthly municipal permit fee, or exempt fundamental concepts of property taxation will be explained before focusing on Manufactured or Mobile Homes. What are the components of the general property tax? There are two basic components in any tax: the base and the rate. By multiplying the base times the rate, the amount of tax is determined. In the property tax, the base is the value of all taxable property in the district. The clerk calculates the rate after the governing body of the town, village, or city determines how much money must be raised from the property tax. In Wisconsin the town, village, or city treasurer collects property taxes not only for its own purposes, but also for the school, the county and the state. Who determines the assessed value of the taxable property? The assessor of each taxation district determines the assessed value of all taxable property, with the exception of manufacturing property. The Department of Revenue makes the annual assessment of all manufacturing property in the state. Assessment Process What is an assessment and what is its purpose? An assessment is the value placed upon your property by the assessor. This value determines what portion of the local property tax levy will be borne by your property. 1

6 What is meant by assessment classification? Wisconsin law requires the assessor to classify land on the basis of use. Sometimes this involves a judgment of the predominant use. Effective January 1, 2004 Wisconsin Act 33 renamed the swamp and waste class of property to undeveloped and created the agricultural forest class of property. The eight statutory classifications for real property are now: (1) residential (5) undeveloped (2) commercial, (5m) agricultural forest (3) manufacturing (6) productive forest land (4) agricultural (7) other Classification is important since it affects the assessed value of land classified as agricultural, undeveloped, and agricultural forest. How are assessments made for property classified as residential, commercial, manufacturing, productive forest, and other? Residential, commercial, manufacturing, productive forest land, and other should be assessed based on the amount that a typical purchaser would pay for the property under ordinary circumstances. Assessments should be uniform at the full value which could ordinarily be obtained therefore at private sale per sec , Wis. Stats. How are assessments made for personal property? Section 70.34, Wis. Stats. requires that All articles of personal property shall, as far as practicable, be valued by the assessor upon actual view at their true cash value. Numerous court decisions have held true cash value to have the same meaning as market value. Who makes the assessment? The assessor of manufacturing property is the Department of Revenue. For all other property (residential, agricultural, etc.) the assessor is appointed or elected at the local level. When the assessor has completed the assessments, the assessor s affidavit is signed and attached to the assessment roll as required by law. Both are then turned over to the Board of Review. Can the assessment on my property be raised even if the assessor has never been inside the manufactured or mobile home? An interior inspection will result in a better quality assessment and is the recommended practice. However, it is not always possible to do this. The law requires that property be valued from actual view or from the best information that can be practicably obtained. It is also important to remember that Wisconsin has an annual assessment. This means that each year s assessment is a new assessment. The assessor is not obligated to keep the same assessment year after year but rather has a duty to keep all property at market value. Therefore, the assessor may increase your assessment because of building permits or sales activity even though an actual inspection of the property has not been made. 2

7 Will I be notified if there is a change in my assessment? According to sec , Wis. Stats., whenever an assessor changes the total assessment of any real property or any improvements taxed as personal property under sec (1), Wis. Stats. by any amount, the owner must be notified. However, failure to receive a notice does not affect the validity of the changed assessment. The notice must be in writing and mailed at least 15 days prior to the Board of Review meeting (or meeting of the Board of Assessors if one exists). The notice contains the amount of the changed assessment and the time, date, and place of the local Board of Review (or Board of Assessors) meeting. The notice must include information notifying the owner of the procedures to be used to object to the assessment. The notice requirement does not apply to personal property assessed under Chapter 70. How can I find out about my assessment? Each property is described in books called assessment rolls that are open for examination at the office of the clerk or the assessor during regular office hours. In many districts each property is identified by a parcel number that also appears on your tax bill. Your name should also appear on the assessment roll opposite the legal description of your property. Properties other than your own may be viewed as well. Personal Property rolls are generally kept in alphabetical order by name of the owner. Can property be assessed higher or lower than market value? Wisconsin law recognizes the difficulties in maintaining annual market value assessments and therefore requires each municipality to assess all property within 10 percent of market value once every five years. If the municipality does not comply, the law requires the assessor to attend a Department of Revenue training session and after seven consecutive years of non-compliance requires the Department to order a state supervised assessment. Since 1992, Wisconsin law required each municipality to assess each major class of property within 10 percent of the corresponding equalized value of the same class once every five years. Requiring municipalities to assess at or near market value makes it easier for taxpayers to determine whether their assessments are equitable. Manufactured and Mobile Home Assessment Overview Wisconsin Statutes provide manufactured and mobile homes may be classified for assessment and taxation purposes as real or personal property, may be subject to a monthly municipal permit fee or may be exempt from monthly municipal permit fees and property tax. A March 2002 Wisconsin Supreme Court Case, Ahrens Etal vs. the Town of Fulton, case number , validated mobile home assessment practices while providing statutory 3

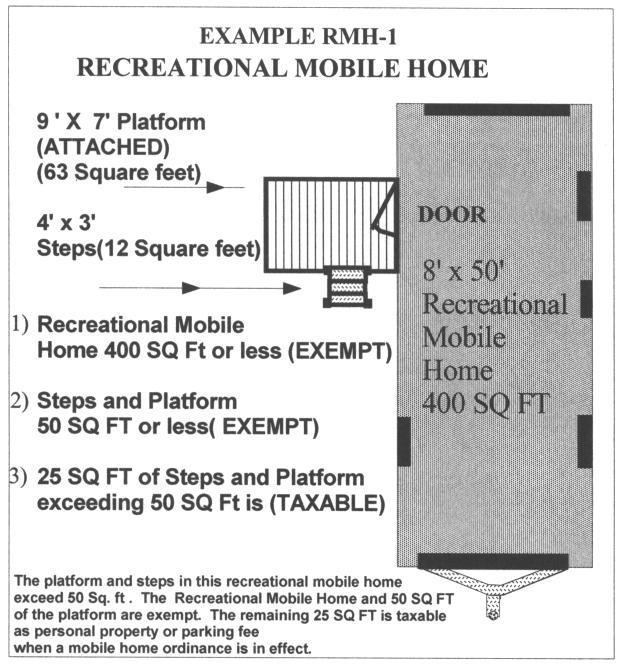

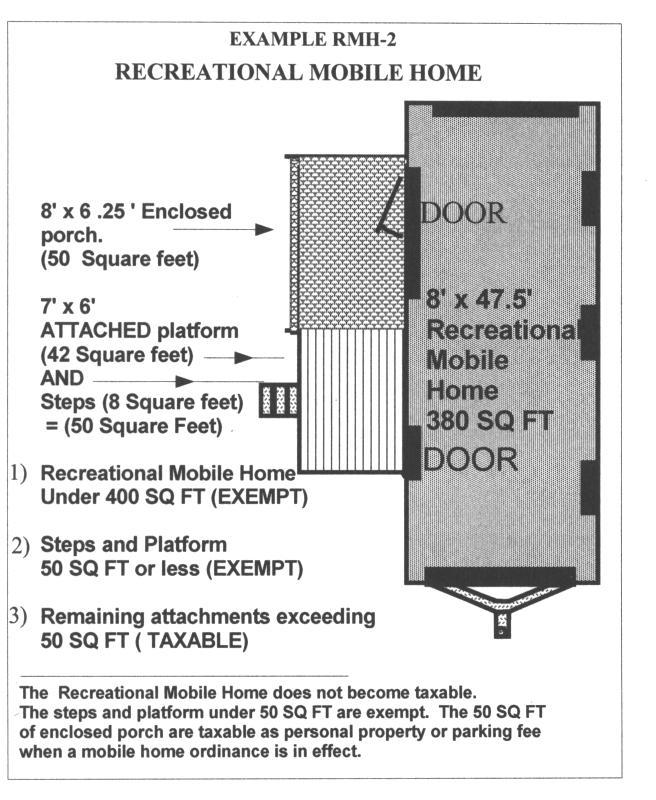

8 interpretation, including clarification of the phrase "set upon a foundation" in sec , Wis. Stats. The following is an overview of mobile home assessment in Wisconsin with excerpts from Ahrens Etal vs. Town of Fulton. What is a mobile home? For purposes of property taxation in Wisconsin, a mobile home is defined by sec , Wis. Stats. as: that which is, or was as originally constructed, designed to be transported by any motor vehicle upon a public highway and designed, equipped and used primarily for sleeping, eating and living quarters, or is intended to be so used; and has the meaning given in sec (10), Wis. Stats. and includes any additions, attachments, annexes, foundations and appurtenances. What is a manufactured home? For purposes of property taxation in Wisconsin, a manufactured home is defined by sec (2), Wis. Stats. as: A structure that is designed to be used as a dwelling with or without a permanent foundation and that is certified by the federal department of housing and urban development as complying with the standards established under 42 USC 5401 to 5425 and includes any additions, annexes, foundations and appurtenances. What are camping trailers and recreational mobile homes? Section (19)(a), Wis. Stats. defines camping trailers by reference to statutory vehicles sec (6m), Wis. Stats. as a vehicle with a collapsible or folding structure designed for human habitation and towed upon a highway by a motor vehicle. Effective January 1, 2007, Sec (1)(hm), Wis. Stats. states, Recreational mobile home means a mobile home prefabricated structure that is no larger than 400 square feet, or that is certified by the manufacturer as complying with the code promulgated by the American National Standards Institute as ANSI A119.5, and that is designed to be towed and used primarily as temporary living quarters for recreational, camping, travel, or seasonal purposes. Recreational mobile homes certified as complying with ANSI A are identified with a metal plate as shown on Exhibit M-1. Please see Examples RMH-1 and RMH-2 for more information. Section (19)(b), Wis. Stats. further states the exemption under this paragraph also applies to steps and a platform, not exceeding 50 square feet, that lead to a doorway of a recreational mobile home or a recreational vehicle, but does not apply to any other addition, attachment, deck, or patio. 4

, Wis. Stats.")

9 Exhibit M-1 Are mobile and manufactured homes real or personal property? A mobile and manufactured home can be classified as real or personal property. The conditions required for a mobile and manufactured home to be classified as an improvement to real property per sec (1), Wis. Stats. are: it is connected to utilities and, it is on a foundation upon land owned by the mobile and manufactured home owner. The conditions required for a mobile and manufactured home to be classified as personal property per sec (2), Wis. Stats. are: if someone other than the mobile and manufactured home owner owns the land upon which the mobile home is located or, if the mobile and manufactured home is not set upon a foundation or connected to utilities. Are any mobile and manufactured homes exempt from property tax? Some mobile and manufactured homes are exempt from property tax. Section (70.111(19), Wis. Stats. exempts camping trailers and certain recreational mobile homes from personal property taxation. If a mobile or manufactured home is on the owner s land and is connected to a well and septic tank and supported by cement blocks, can the assessor classify the mobile or manufactured home as real estate? If a mobile home or manufactured home is to be assessed as an improvement to real property, it must be set upon a foundation. Section (1), Wis. Stats. states that a mobile home or manufactured home is defined as set upon a foundation if it is off its wheels and is set upon some other support. The assessor has the authority to determine if the cement blocks supporting the trailer meet this definition of foundation. In Ahrens Etal vs. Town of Fulton, the Supreme Court held " a mobile home is 'set upon a foundation' when the home is resting for more than a temporary time, in whole or in part, on some other means of support than its wheels." 5

10 "In this case, the stipulated facts reveal that 19 of the 20 representative owners have 'some form of stabilizer under the unit, whether it be concrete blocks, cinder blocks or screw jacks ' The use of these support mechanisms effectively took some of the weight of the home off its wheels. The remaining mobile home did not have any stabilizers under it. This mobile home did, however, have additional structures that were caulked to the unit. The additional structures included a 385 square foot screened-in room and a 104 square foot porch. Both structures rest on footings." The Town argued that, when this addition is considered, the mobile home would not be completely supported by its wheels. The Supreme Court agreed with this interpretation. Does the fact that the wheels are attached to a mobile home or manufactured home make it exempt? No. Attached wheels are not the sole criterion for exemption. First, to be entitled to an exemption, the mobile home must be classified as personal property per sec (2), Wis. Stats. Secondly, the unit must meet the definition of a recreational mobile home found in the Statutes. How should the assessor measure a mobile home to determine if it qualifies for exemption? The total square footage (rounded to the nearest square foot) should be calculated using the outside length and width of the mobile, including the area of any additions and attachments. It is important that only additions and attachments that are clearly attached to the recreational mobile home be included in the calculation of total square footage. The Wisconsin Court of Appeals, affirmed by the Supreme Court, in Ahrens Etal vs. Town of Fulton, defined how the assessor should determine what is an addition and attachment. The court stated, It seems clear from the forgoing that any rooms, porches, decks and the like, that are attached in any way to the basic unit are included within the definition of a mobile home. The length and width of a mobile home or manufactured home should not include the excess measurements caused by the protrusion of corner caps and end caps as this could influence the exemption determination. Freestanding structures (appurtenances) should not be included in the mobile home or manufactured home area calculation. Garages, sheds, and other freestanding structures (if they are so affixed to the real estate so as to become a part of it) should be assessed as real estate if the mobile home owner owns the land or as personal property if the mobile or manufactured home owner does not own the land. Square footage disagreements should first be discussed with the assessor. If you believe the mobile home or manufactured home is exempt, you may file a claim of unlawful tax with the municipality per sec , Wis. Stats. If the municipality rejects the claim, a direct appeal may be made to the Circuit Court of the county in which the property is located. 6

11 If the town charges a monthly municipal permit fee for a mobile home, is there a property tax in addition to the fee? No. Section (7), Wis. Stats. exempts from property taxation every mobile home unit subject to a monthly parking municipal permit fee. Per sec )(3) (1)(j), Wis. Stats. a municipality may enact an ordinance to collect a mobile home or manufactured home parking monthly municipal permit fee from all units located within the municipality except for: mobile homes or manufactured homes that are improvements to real property as defined in sec (1), Wis. Stats., and recreational mobile homes and camping trailers per sec (19), Wis. Stats., and recreational mobile homes located in campgrounds licensed under sec , Wis. Stats., and mobile homes located on land where the principal residence home owner is located per sec (9), Wis. Stats. Are recreational motor homes taxed as mobile or manufactured homes? No. Section (5), Wis. Stats. exempts motor vehicles from property taxation. This statute exempts items such as Winnebago motor homes, Ford campers, and other motorized vehicles known as RV s. Licensed vehicles and trailers are not considered mobile homes or manufactured homes. How can someone appeal the property assessment placed on a mobile or manufactured home? The mobile home or manufactured home owner may appeal the valuation placed on the mobile and manufactured home by appearing before the local Board of Review and presenting sworn oral testimony as to its true and correct market value. This applies to a mobile home or manufactured home whether it is assessed as real estate, personal property, or subject to the monthly municipal permit fee. Can the Board of Review exempt mobile or manufactured homes? No. Disputes concerning exemption issues are not heard at the Board of Review. Property owners contesting exemption status may file a claim of unlawful tax with the municipality by January 31 of the year in which the tax is payable, sec , Wis. Stats. If the municipality rejects the claim, a direct appeal may be made to the Circuit Court of the county in which the property is located. 7

12 Are a dealer s vacant mobile or manufactured homes displayed for sale on the sales lot taxable? No. Vacant mobile or manufactured homes held for sale by a dealer are considered merchant s stock-in-trade and are exempt per sec (17), Wis. Stats. if the merchant is also the owner of the vacant mobile or manufactured home. Vacant mobile or manufactured homes held by the manufactured or mobile home community operator, that is not a dealer are taxable or subject to a monthly municipal permit fee. Vacant units that have been repossessed by a financial institution. Vacant units that have been repossessed by the financial institution are not subject to municipal parking fee as per sec (3)(c)9, Wis. Stats. The statute was created to read, "No monthly municipal permit fee may be imposed on a financial institution, as defined in sec (1)(b), Wis. Stats., that relates to a vacant unit that has been repossessed by the financial institution." 8

13 9

14 10

15 Overview of Manufactured and Mobile Home (Unit) Property Taxes Item Unit of any size including additions, on a foundation, connected to utilities, land owned by unit s owner. Unit of any size including additions either still on wheels, and/or not connected to utilities, and/or on land not owned by unit s owner. Recreational mobile home or vehicle no larger than 400 square feet used as temporary living quarters. Camping trailer designed to expand into a tent with built-in space for mattress and other fixtures Unit Per Yes Yes Yes No Subject to General Property Tax Yes, as real property Yes, as personal property unless subject to permit fee Exempt under (19)(b) to include steps and a platform, not exceeding 50 square feet leading to a doorway of a recreational mobile home, does not apply to any other addition, attachment, deck, or patio Exempt under (19)(b) Subject to Municipal Permit Fee No Yes, if located in municipality with permit fee No, by (3)(c) No, by (3)(c) Comments Meets definition in and real estate in (1). Meets definition in and personal property in (2). Subject to permit fee if in community; if subject to fee, exempt from personal property tax (7). Meets definition in (1)(hm); by size and use exempt from personal property tax under (19)(b); exempt from permit fee under (3)(c). Pop-up trailer meets definition of camping trailer in (6m) as trailer with collapsible or folding structure towed on the highway. 11

16 Item Camper body installed or mounted on pick-up truck. Twin-section units transported on wheels or dolly and assembled on site. Unit Per Yes Subject to General Property Tax Exempt under (19)(b) Subject to Municipal Permit Fee No, by (3)(c) Comments Meets definition of mobile home in ; if under 400 square feet, exempt from personal property tax under (19)(b). No Yes No Not a unit under Realty if located on land owned by unit s owner; otherwise, treated as personal property as a building on leased land. Buses or vans No Exempt under (5) Vacant unit held for sale by a dealer No Motor vehicle exempt from property tax under (5) No No No Considered merchant s stock under (17) 2009 Wisconsin Act 68 Trespass and Revaluation Notice The trespass law entitles the assessor to enter a property once during an assessment cycle unless the property owner authorizes additional visits. If the property owner denies the assessor access to the property, the assessor must maintain a list of denied entries. Sections and , Wis. Stats. pertain to the entry onto the property. Assessors and their staff should understand the conditions included in these statutes. The major conditions for entry are listed below: The reason for the entry must be to make an assessment on behalf of the state or a political subdivision. The entry must be on a weekday during daylight hours, or at another time as agreed upon with the property owner. The assessor s visit must not be more than one hour. The assessor must not open doors, enter through open doors, or look into windows of structures. If the property owner or occupant is not present, the assessor must leave a notice on the principal building providing the owner information on how to contact them. The assessor may not enter the premises if they have received a notice from the property owner or occupant denying them entry. The assessor must leave if the property owner or occupant asks them to leave. 12

17 2009 Wisconsin Act 68, which was signed November 12, 2009, addresses notification which must be published or posted prior to commencement of a revaluation by an assessor. The trespass bill states in part Before a city, village, or town assessor conducts a revaluation of property under this paragraph [Section 70.05(5)(b) Wis. Stats.], the city, village or town shall publish a notice on its municipal website that a revaluation will occur and the approximate dates of the property revaluation. The notice shall also describe the authority of an assessor, under Section , Wis. Stats. and Section , Wis. Stats., to enter land. If a municipality does not have a website, it shall post the required information in at least 3 public places within the city, village or town. (Emphasis added) It is recommended that you provide a link to the above noted statutory references so that persons visiting your website could click on those links and review the statutes. Model language regarding this notice is provided below. Sample Revaluation Notice A revaluation of property assessments in the (municipality) shall occur for the (year) assessment year. The approximate dates of the revaluation notices being sent to property owners is expected to be in (month/year). Please also notice that the Assessor has certain statutory authority to enter land as described in Sections and , Wisconsin Statutes. The ability to enter land is subject to several qualifications and limitations, as described within the foregoing statutes. Copies of the applicable statutes can be obtained at public depositories throughout the State of Wisconsin, and from the State of Wisconsin Legislative Reference Bureau website or a copy may be obtained from the municipal clerk upon payment of applicable copying charges. 13

18 Definition of Terms Arm s-length Sale A sale between two parties, neither of whom is related to or under abnormal pressure from the other. Assessed Value The dollar amount assigned to taxable real and personal property by the assessor for the purpose of taxation. Assessed value is estimated as of January 1 and will apply to the taxes levied at the end of that year. Assessed value is called a primary assessment because a levy is applied directly against it to determine the tax due. Accurate assessed values ensure fairness between properties within the taxing jurisdiction. (See Equalized value for fairness between municipalities). Assessment Level The relationship between the assessed value and the equalized value of non-manufacturing property minus corrections for prior year over or under charges within a municipality town, village or city. For example, if the assessed value of all the property subject to property tax in the municipality is $2,700,000 and the Equalized Value (with no prior year corrections) in the municipality is $3,000,000 then the assessment level is said to be 90% ($2,700,000 $3,000,000 =.90 or 90%). Assessment Ratio The relationship between the assessed value and the statutory valuation standard (fair market value for most property, use value for agricultural land, and 50% of full value for agricultural forest and undeveloped lands). For example, if the assessment of a parcel which sold for $150,000 (fair market value) was $140,000, the assessment ratio is said to be 93% (140,000 divided by 150,000). The difference in the assessment level and the assessment ratio is that the level typically refers to the taxation district; the ratio refers to the individual parcel. Assessment Ratio = Assessed Value Market Value = $140,000 $150,000 = 93% Equalized Value The estimated value of all taxable real and personal property in each taxation district, by class, as of January 1 and certified by the Department of Revenue on August 15 of each year. The value represents market value (most probable selling price), except for agricultural property, which is based on its use (ability to generate agricultural income) and agricultural forest and undeveloped lands, which are based on 50% of their full value. Full Value (1) The value reflected as fair market value when used in reference to the valuation of real property under sec (1), Wis. Stats. (This does not include agricultural property defined in sec (2)1, Wis. Stats). (2) The same as Equalized Value, however is often used when referring to the value of school and special districts. Levy The amount of property taxes imposed by a taxing unit. 14

19 Market Value The definition of market value is the most probable price which a property should bring in a competitive and open market under all conditions requisite to a fair sale, the buyer and seller each acting prudently and knowledgeably, and assuming the price is not affected by undue stimulus. Implicit in this definition is the consummation of a sale as of a specified date and the passing of title from seller to buyer under conditions whereby: 1. Buyer and seller are typically motivated; 2. Both parties are well informed or well advised, and acting in what they consider their own best interests; 3. A reasonable time is allowed for exposure in the open market; 4. Payment is made in terms of cash in U.S. dollars or in terms of financial arrangements comparable thereto; and 5. The price represents the normal consideration for the property sold unaffected by special or creative financing or sales concessions granted by anyone associated with the sale Reassessment This is the redoing of the existing assessment roll because of substantial inequities. All the property of the district is viewed, valued, and placed in the new assessment roll, which is then substituted for the original roll. Revaluation This is the determination of new values for an upcoming assessment year. The previous year s assessment roll is not affected. The term is often used in conjunction with sec , Wis. Stats. where expert help can be hired to work with the assessor in revaluing the district. Tax Rate The ratio of the property tax levy to the base. The tax rate is determined by dividing the amount of the tax levy by either the total assessed value or the Equalized Value of the tax district. It is often expressed in terms of dollars per thousand. It is synonymous with the term levy rate. Taxation District A city, village, or town. If a city or village lies in more than one county, that portion of the city or village which lies within each county. Taxing Jurisdiction The entity authorized by law to levy taxes on general property that is located within its boundaries (see sec (7), Wis. Stats.) In addition to towns, villages, and cities, this includes school districts, sewerage districts, and lake rehabilitation districts, for example. 15

20 Flowchart of the Assessment Appeal Process If you are not satisfied with your assessment, then consider the following assessment appeal process: Discuss your assessment with the Assessor Do you still wish to appeal? No Stop Yes Does your community have a Board of Assessors? Yes Appeal to the Board of Assessors No Appeal to the Board of Review Yes Continue Appeal? No Stop Continue Appeal? No Stop Yes Next avenue of appeal (2 options) #2 Department of Revenue s #1 Circuit Court s (13) Yes Continue Appeal? No Stop 16

21 Equalization District Offices District Supervisor Madison District Office (76) Jim Young MS PO Box 8909 Madison, WI Counties Columbia, Crawford, Dane, Dodge, Grant, Green, Green Lake, Iowa, Jefferson, Lafayette, Marquette, Richland, Rock, Sauk, Vernon Phone (608) FAX (608) Milwaukee District Office (77) Vacant Room North 6th St Milwaukee, WI Fond du Lac, Kenosha, Milwaukee, Ozaukee, Racine, Sheboygan, Walworth, Washington, Waukesha Phone (414) FAX (414) Eau Claire District (79) Diane Forrest 610 Gibson St Ste 7 Eau Claire, WI Phone (715) FAX (715) Wausau District Office (80) Albert Romportl 730 Third St Wausau, WI Barron, Bayfield, Buffalo, Burnett, Chippewa, Douglas, Dunn, Eau Claire, Jackson, La Crosse, Monroe, Pepin, Pierce, Polk, Rusk, St. Croix, Sawyer, Trempealeau, Washburn Adams, Ashland, Clark, Iron, Juneau, Langlade, Lincoln, Marathon, Oneida, Portage, Price, Taylor, Vilas, Wood Phone (715) FAX (715) Green Bay District Office (81) Mary Gawryleski Ste N Jefferson St Green Bay, WI Brown, Calumet, Door, Florence, Forest, Kewaunee, Manitowoc, Marinette, Menominee, Oconto, Outagamie, Shawano, Waupaca, Waushara, Winnebago Phone (920) FAX (920) Last updated December 18,

Record Year on Track for Wisconsin Housing Market

Date: 10/17/2016 For Release: Immediately For More Information Contact: Michael Theo, WRA President & CEO, 608-241-2047, mtheo@wra.org or David Clark, Economist, C3 Statistical Solutions and Professor

Date: 10/17/2016 For Release: Immediately For More Information Contact: Michael Theo, WRA President & CEO, 608-241-2047, mtheo@wra.org or David Clark, Economist, C3 Statistical Solutions and Professor

2018 Housing Market Remains Strong Despite Limited Inventories

Date: 1/21/19 For Release: Immediately For More Information Contact: Michael Theo, WRA President & CEO, 608-241-2047, mtheo@wra.org or David Clark, Economist, C3 Statistical Solutions and Professor of

Date: 1/21/19 For Release: Immediately For More Information Contact: Michael Theo, WRA President & CEO, 608-241-2047, mtheo@wra.org or David Clark, Economist, C3 Statistical Solutions and Professor of

Limited Supply of Homes for Sale Impacts Prices and Sales

Date: 2/20/17 For Release: Immediately For More Information Contact: Michael Theo, WRA President & CEO, 608-241-2047, mtheo@wra.org or David Clark, Economist, C3 Statistical Solutions and Professor of

Date: 2/20/17 For Release: Immediately For More Information Contact: Michael Theo, WRA President & CEO, 608-241-2047, mtheo@wra.org or David Clark, Economist, C3 Statistical Solutions and Professor of

January Home Sales Fall as Prices Continue to Rise

Date: 2/23/15 For Release: Immediately For More Information Contact: Michael Theo, WRA President & CEO, 608-241-2047, mtheo@wra.org or David Clark, Economist, C3 Statistical Solutions and Professor of

Date: 2/23/15 For Release: Immediately For More Information Contact: Michael Theo, WRA President & CEO, 608-241-2047, mtheo@wra.org or David Clark, Economist, C3 Statistical Solutions and Professor of

Wisconsin Housing Market Remains Hot in January

Date: 2/22/16 For Release: Immediately For More Information Contact: Michael Theo, WRA President & CEO, 608-241-2047, mtheo@wra.org or David Clark, Economist, C3 Statistical Solutions and Professor of

Date: 2/22/16 For Release: Immediately For More Information Contact: Michael Theo, WRA President & CEO, 608-241-2047, mtheo@wra.org or David Clark, Economist, C3 Statistical Solutions and Professor of

First Quarter Home Sales Decline as Prices Continue to Rise

Date: 4/22/19 For Release: Immediately For More Information Contact: Michael Theo, WRA President & CEO, 608-241-2047, mtheo@wra.org or David Clark, Economist, ECON Analytics, LLC and Professor of Economics,

Date: 4/22/19 For Release: Immediately For More Information Contact: Michael Theo, WRA President & CEO, 608-241-2047, mtheo@wra.org or David Clark, Economist, ECON Analytics, LLC and Professor of Economics,

HOME SALES RALLY IN THE FOURTH QUARTER TO KEEP WISCONSIN HOUSING MARKET STABLE

Date: 2/11/2010 For Release: Immediately For More Information Contact: David E. Clark, Economist C3 Statistical Solutions Inc. Office phone: 414-803-6537 or William Malkasian, President Wisconsin REALTORS

Date: 2/11/2010 For Release: Immediately For More Information Contact: David E. Clark, Economist C3 Statistical Solutions Inc. Office phone: 414-803-6537 or William Malkasian, President Wisconsin REALTORS

MARKET AREA UPDATE Report as of: 1Q 2Q 3Q 4Q

Year: 2012 Market Area (City, State): Madison/Dane County, Wisconsin Provided by (Company / Companies): Restaino & Associates, Realtors MARKET AREA UPDATE Report as of: 1Q 2Q 3Q 4Q What are the most significant

Year: 2012 Market Area (City, State): Madison/Dane County, Wisconsin Provided by (Company / Companies): Restaino & Associates, Realtors MARKET AREA UPDATE Report as of: 1Q 2Q 3Q 4Q What are the most significant

WISCONSIN HOUSING MARKETPLACE

WISCONSIN REALTORS ASSOCIATION WISCONSIN HOUSING MARKETPLACE Date: 2/16/06 For Release: Immediately For More Information Contact: David E. Clark, Economist C3 Statistical Solutions Inc. Office phone: 414-803-6537

WISCONSIN REALTORS ASSOCIATION WISCONSIN HOUSING MARKETPLACE Date: 2/16/06 For Release: Immediately For More Information Contact: David E. Clark, Economist C3 Statistical Solutions Inc. Office phone: 414-803-6537

WISCONSIN WEST NORTHEAST SOUTH CENTRAL SOUTHEAST

WISCONSIN The RE/MAX INTEGRA, Midwest s Springboard into Summer Housing Market Report analyzes the latest trends and economic conditions of the residential real estate market throughout Wisconsin. Individual

WISCONSIN The RE/MAX INTEGRA, Midwest s Springboard into Summer Housing Market Report analyzes the latest trends and economic conditions of the residential real estate market throughout Wisconsin. Individual

Wisconsin Agricultural. Land Prices. Ag Land Values up 4.0%

Wisconsin Agricultural 2012 Land Prices Drought conditions, strong commodity prices and low interest rates combined to fuel another increase in Wisconsin agricultural land prices in 2012. While the year

Wisconsin Agricultural 2012 Land Prices Drought conditions, strong commodity prices and low interest rates combined to fuel another increase in Wisconsin agricultural land prices in 2012. While the year

Municipal Treasurers. April 23, Wisconsin Department of Revenue

DOR Update Municipal Treasurers Waukesha April 23, 1 Presenters Scott Shields Director, Technical & Assessment Services Leah Foy Director, Local Government Services 2 Topics of Discussion General Division

DOR Update Municipal Treasurers Waukesha April 23, 1 Presenters Scott Shields Director, Technical & Assessment Services Leah Foy Director, Local Government Services 2 Topics of Discussion General Division

Working Lands Initiative WI TOWNS ASSOCIATION December 2010

Working Lands Initiative WI TOWNS ASSOCIATION December 2010 Certification of Plans and Ordinances 2011 Calumet* Brown Dane Dodge Jefferson Kenosha La Crosse Outagamie Ozaukee Racine Rock Walworth Waukesha

Working Lands Initiative WI TOWNS ASSOCIATION December 2010 Certification of Plans and Ordinances 2011 Calumet* Brown Dane Dodge Jefferson Kenosha La Crosse Outagamie Ozaukee Racine Rock Walworth Waukesha

Due by March 31, 2010

State of Wisconsin Department of Natural Resources dnr.wi.gov Annual Report under MS4 General Permit No. WI-S050075-1 Form 3400-195 (R 01/2010) Page 1 Due by March 31, 2010 This form is for the purpose

State of Wisconsin Department of Natural Resources dnr.wi.gov Annual Report under MS4 General Permit No. WI-S050075-1 Form 3400-195 (R 01/2010) Page 1 Due by March 31, 2010 This form is for the purpose

PROPERTY REASSESSMENT AND TAXATION. State Tax Commission Jefferson City, Missouri

PROPERTY REASSESSMENT AND TAXATION State Tax Commission Jefferson City, Missouri Revised January, 2017 INTRODUCTION Some aspects of the property tax system are confusing to many taxpayers. It is important

PROPERTY REASSESSMENT AND TAXATION State Tax Commission Jefferson City, Missouri Revised January, 2017 INTRODUCTION Some aspects of the property tax system are confusing to many taxpayers. It is important

ASSESSMENT AND TAXATION

ABSTRACT A brief synopsis of the assessment, appeal and taxation process as implemented by the Code of Iowa and Administrative Rules. ASSESSMENT AND TAXATION Iowa State Association of Assessors General

ABSTRACT A brief synopsis of the assessment, appeal and taxation process as implemented by the Code of Iowa and Administrative Rules. ASSESSMENT AND TAXATION Iowa State Association of Assessors General

Board of Appeal and Equalization Handbook

Board of Appeal and Equalization Handbook This handbook was created to satisfy the training requirements of Minnesota Statutes, sections 274.014 and 274.135 Updated January 2018 Table of Contents Introduction...

Board of Appeal and Equalization Handbook This handbook was created to satisfy the training requirements of Minnesota Statutes, sections 274.014 and 274.135 Updated January 2018 Table of Contents Introduction...

Housing Solutions for People with Disabilities

Housing Solutions for People with Disabilities Movin Out, in partnership with people with disabilities and their allies, creates and sustains community-integrated, safe, affordable housing solutions. Movin

Housing Solutions for People with Disabilities Movin Out, in partnership with people with disabilities and their allies, creates and sustains community-integrated, safe, affordable housing solutions. Movin

WATERFRONT LOCAL IMPROVEMENT DISTRICT OVERVIEW. November 2017

WATERFRONT LOCAL IMPROVEMENT DISTRICT OVERVIEW November 2017 LOCAL IMPROVEMENT DISTRICT Funding tool by which property owners financially contribute to a project that will increase the value of their property

WATERFRONT LOCAL IMPROVEMENT DISTRICT OVERVIEW November 2017 LOCAL IMPROVEMENT DISTRICT Funding tool by which property owners financially contribute to a project that will increase the value of their property

THE OFFICE OF COUNTY ASSESSOR

CHAPTER 5 THE OFFICE OF COUNTY ASSESSOR The office of county assessor is primarily responsible for determining equitable values on both real and personal property for property tax purposes (63-207). However,

CHAPTER 5 THE OFFICE OF COUNTY ASSESSOR The office of county assessor is primarily responsible for determining equitable values on both real and personal property for property tax purposes (63-207). However,

York County 2015 Reassessment Program. York County Assessor s Office 18 W. Liberty St York SC fax

York County 2015 Reassessment Program York County Assessor s Office 18 W. Liberty St York SC 29745 803-684-8526 803-628-3936 fax Re-Assessment The Reassessment Program Act 208: Act 208, as passed by the

York County 2015 Reassessment Program York County Assessor s Office 18 W. Liberty St York SC 29745 803-684-8526 803-628-3936 fax Re-Assessment The Reassessment Program Act 208: Act 208, as passed by the

JEFFERSON COUNTY, WEST VIRGINIA EMERGENCY AMBULANCE SERVICE FEE ORDINANCE. Table of Contents

JEFFERSON COUNTY, WEST VIRGINIA EMERGENCY AMBULANCE SERVICE FEE ORDINANCE Table of Contents SECTION 1 LEGISLATIVE AUTHORITY... 1 SECTION 2 PURPOSE... 1 SECTION 3 DEFINITIONS... 1 SECTION 4 RATES... 3 Residential

JEFFERSON COUNTY, WEST VIRGINIA EMERGENCY AMBULANCE SERVICE FEE ORDINANCE Table of Contents SECTION 1 LEGISLATIVE AUTHORITY... 1 SECTION 2 PURPOSE... 1 SECTION 3 DEFINITIONS... 1 SECTION 4 RATES... 3 Residential

Past & Present Adjustments & Parcel Count Section... 13

Assessment 2017 Report This report includes specific information regarding the 2017 assessment as well as general information about both the appeals and assessment processes. Contents Introduction... 3

Assessment 2017 Report This report includes specific information regarding the 2017 assessment as well as general information about both the appeals and assessment processes. Contents Introduction... 3

Introduction. Bruce Munneke, S.A.M.A. Washington County Assessor. 3 P a g e

Assessment 2016 Report This report includes specific information regarding the 2016 assessment as well as general information about both the appeals and assessment processes. Contents Introduction... 3

Assessment 2016 Report This report includes specific information regarding the 2016 assessment as well as general information about both the appeals and assessment processes. Contents Introduction... 3

Multi-Family Methodology Analysis

Multi-Family Methodology 2018 Analysis Assessment Department February, 2018 2018 Multi-Family Assessment Methodology Property assessments in the City of Medicine Hat reflect the fee simple market value

Multi-Family Methodology 2018 Analysis Assessment Department February, 2018 2018 Multi-Family Assessment Methodology Property assessments in the City of Medicine Hat reflect the fee simple market value

Assembly Bill No. 489 Committee on Growth and Infrastructure CHAPTER...

Assembly Bill No. 489 Committee on Growth and Infrastructure CHAPTER... AN ACT relating to the taxation of property; providing for the partial abatement of the ad valorem taxes imposed on property; directing

Assembly Bill No. 489 Committee on Growth and Infrastructure CHAPTER... AN ACT relating to the taxation of property; providing for the partial abatement of the ad valorem taxes imposed on property; directing

[Code of Federal Regulations] [Title 12, Volume 5] [Revised as of January 1, 2004] From the U.S. Government Printing Office via GPO Access

![[Code of Federal Regulations] [Title 12, Volume 5] [Revised as of January 1, 2004] From the U.S. Government Printing Office via GPO Access](/thumbs/80/82487200.jpg "[Code of Federal Regulations] [Title 12, Volume 5] [Revised as of January 1, 2004] From the U.S. Government Printing Office via GPO Access") [Code of Federal Regulations] [Title 12, Volume 5] [Revised as of January 1, 2004] From the U.S. Government Printing Office via GPO Access TITLE 12--BANKS AND BANKING CHAPTER V--OFFICE OF THRIFT SUPERVISION,

[Code of Federal Regulations] [Title 12, Volume 5] [Revised as of January 1, 2004] From the U.S. Government Printing Office via GPO Access TITLE 12--BANKS AND BANKING CHAPTER V--OFFICE OF THRIFT SUPERVISION,

MANUFACTURED HOUSING GENERAL ISSUES, CLASSIFICATION & VALUATION VAAO 58 TH EDUCATION SEMINAR JOINT SESSION JULY 19, :00 AM 12:00 NOON

MANUFACTURED HOUSING GENERAL ISSUES, CLASSIFICATION & VALUATION VAAO 58 TH EDUCATION SEMINAR JOINT SESSION JULY 19, 2013 9:00 AM 12:00 NOON Panel Members Hon. Ellen Murphy Commissioner of the Revenue Frederick

MANUFACTURED HOUSING GENERAL ISSUES, CLASSIFICATION & VALUATION VAAO 58 TH EDUCATION SEMINAR JOINT SESSION JULY 19, 2013 9:00 AM 12:00 NOON Panel Members Hon. Ellen Murphy Commissioner of the Revenue Frederick

V2 Attribute Schema Version 2 Statewide Parcel Map Database Project August 31, 2016

http:/ /www.sco.wisc.edu/parcels/data/assets/v2/v2_wisconsin_statewide_parcels_schema_documentation.pdf V2 Attribute Schema Version 2 Statewide Parcel Map Database Project August 31, 2016 Contents About

http:/ /www.sco.wisc.edu/parcels/data/assets/v2/v2_wisconsin_statewide_parcels_schema_documentation.pdf V2 Attribute Schema Version 2 Statewide Parcel Map Database Project August 31, 2016 Contents About

Village of Scarsdale

Village of Scarsdale VILLAGE HALL / 1001 POST ROAD / SCARSDALE, NY 10583 914.722.1110 / WWW.SCARSDALE.COM Village Wide Revaluation Frequently Asked Questions Q1. How was the land value for each parcel

Village of Scarsdale VILLAGE HALL / 1001 POST ROAD / SCARSDALE, NY 10583 914.722.1110 / WWW.SCARSDALE.COM Village Wide Revaluation Frequently Asked Questions Q1. How was the land value for each parcel

BOARD OF REVIEW SCRIPT

BOARD OF REVIEW SCRIPT CLERK'S SCRIPT: 1. Clerk introduces the case by stating the following information: a. Tax Key # b. Property address c. Property Owner d. Mailing address if different. e. Class of

BOARD OF REVIEW SCRIPT CLERK'S SCRIPT: 1. Clerk introduces the case by stating the following information: a. Tax Key # b. Property address c. Property Owner d. Mailing address if different. e. Class of

Office of Legislative Services Background Report The Assessment of Real Property: Answers to Frequently Asked Questions

Office of Legislative Services Background Report The Assessment of Real Property: Answers to Frequently Asked Questions OLS Background Report No. 120 Prepared By: Local Government Date Prepared: New Jersey

Office of Legislative Services Background Report The Assessment of Real Property: Answers to Frequently Asked Questions OLS Background Report No. 120 Prepared By: Local Government Date Prepared: New Jersey

YOUR GUIDE TO THE REASSESSMENT PROGRAM

YOUR GUIDE TO THE REASSESSMENT PROGRAM Why Reassess? Reassessment is required by law. Act 208, as passed by the General Assembly in 1975, provides that all real property will be valued at its current market

YOUR GUIDE TO THE REASSESSMENT PROGRAM Why Reassess? Reassessment is required by law. Act 208, as passed by the General Assembly in 1975, provides that all real property will be valued at its current market

Mobile Home Titles for the Real Property Lawyer. This, not that

Mobile Home Titles for the Real Property Lawyer Chicago Title CPE Seminar October 2017 This, not that Mobile Home NOT Mobile Home 1 This, not that Mobile Home GS 143 145(7): >8 in width or >40 in length

Mobile Home Titles for the Real Property Lawyer Chicago Title CPE Seminar October 2017 This, not that Mobile Home NOT Mobile Home 1 This, not that Mobile Home GS 143 145(7): >8 in width or >40 in length

Special Plainview City Council Meeting Board of Appeals and Equalization Meeting AGENDA Tuesday, April 16, 2019, at 6:00 P.M.

Special Plainview City Council Meeting Board of Appeals and Equalization Meeting AGENDA Tuesday, April 16, 2019, at 6:00 P.M. Special meetings are meetings held at a time or place that is different from

Special Plainview City Council Meeting Board of Appeals and Equalization Meeting AGENDA Tuesday, April 16, 2019, at 6:00 P.M. Special meetings are meetings held at a time or place that is different from

Guidelines for the Snowmobile Program. A financial assistance program Administered by the Wisconsin Department of Natural Resources

Guidelines for the Snowmobile Program A financial assistance program Administered by the Wisconsin Department of Natural Resources PUB-CA-002 2006 TABLE OF CONTENTS Introduction...1 DNR Contacts...1 Where

Guidelines for the Snowmobile Program A financial assistance program Administered by the Wisconsin Department of Natural Resources PUB-CA-002 2006 TABLE OF CONTENTS Introduction...1 DNR Contacts...1 Where

To: Property Appraisers, Taxing Authorities and Interested Parties From: James McAdams Date: June 5, 2012 Bulletin: PTO 12-04

Property Tax Oversight Bulletin: PTO 12-04 To: Property Appraisers, Taxing Authorities and Interested Parties From: James McAdams Date: Bulletin: PTO 12-04 FLORIDA DEPARTMENT OF REVENUE PROPERTY TAX INFORMATIONAL

Property Tax Oversight Bulletin: PTO 12-04 To: Property Appraisers, Taxing Authorities and Interested Parties From: James McAdams Date: Bulletin: PTO 12-04 FLORIDA DEPARTMENT OF REVENUE PROPERTY TAX INFORMATIONAL

LOCAL IMPROVEMENT DISTRICT APPRAISER PRESENTATION. November 2017

LOCAL IMPROVEMENT DISTRICT APPRAISER PRESENTATION November 2017 SPECIAL BENEFIT STUDY WHY? A special benefit study is a tool consistently used with LID projects. Municipality retains an expert consultant

LOCAL IMPROVEMENT DISTRICT APPRAISER PRESENTATION November 2017 SPECIAL BENEFIT STUDY WHY? A special benefit study is a tool consistently used with LID projects. Municipality retains an expert consultant

Make checks payable to Columbia County Treasurer. We do not issue refunds. Credit Cards accepted.

Columbia County Camping Application Planning & Zoning Department Pursuant to Columbia County Ordinance 16-130-050(D)(5)(i) Phone: (608) 742-9660 Fax: (608) 742-9817 www.co.columbia.wi.us 112 E. Edgewater

Columbia County Camping Application Planning & Zoning Department Pursuant to Columbia County Ordinance 16-130-050(D)(5)(i) Phone: (608) 742-9660 Fax: (608) 742-9817 www.co.columbia.wi.us 112 E. Edgewater

S18A0430. CLAYTON COUNTY BOARD OF TAX ASSESSORS v. ALDEASA ATLANTA JOINT VENTURE.

In the Supreme Court of Georgia Decided: June 18, 2018 S18A0430. CLAYTON COUNTY BOARD OF TAX ASSESSORS v. ALDEASA ATLANTA JOINT VENTURE. BENHAM, Justice. This case presents the issue of whether the contract

In the Supreme Court of Georgia Decided: June 18, 2018 S18A0430. CLAYTON COUNTY BOARD OF TAX ASSESSORS v. ALDEASA ATLANTA JOINT VENTURE. BENHAM, Justice. This case presents the issue of whether the contract

CITY OF OWATONNA ASSESSMENT REPORT. Steele County Assessor s Department. William G. Effertz, SAMA Steele County Assessor

2017 CITY OF OWATONNA ASSESSMENT REPORT Steele County Assessor s Department William G. Effertz, SAMA Steele County Assessor Tyler Diersen, AMA, Assistant County Assessor April 11, 2017 2017 Assessment

2017 CITY OF OWATONNA ASSESSMENT REPORT Steele County Assessor s Department William G. Effertz, SAMA Steele County Assessor Tyler Diersen, AMA, Assistant County Assessor April 11, 2017 2017 Assessment

2018 Seminar Series. Mobile Home Titles for the Real Property Lawyer

2018 Seminar Series Mobile Home Titles for the Real Property Lawyer James W. Williams, III Title Counsel Attorneys Title 720 N. Third Street, Suite 202 Wilmington, NC 28401 (910) 343-1096 Jay.Williams@AttorneysTitle.com

2018 Seminar Series Mobile Home Titles for the Real Property Lawyer James W. Williams, III Title Counsel Attorneys Title 720 N. Third Street, Suite 202 Wilmington, NC 28401 (910) 343-1096 Jay.Williams@AttorneysTitle.com

APPEAL PROCESS GUIDE FOR THE PROPERTY OWNER

2018 APPEAL PROCESS GUIDE FOR THE PROPERTY OWNER IMPORTANT DATES TO KNOW 2018 APPEAL PROCESS TIME FRAME March 1 - assessment notices must be mailed March 15 - last day to file for owner-occupied status

2018 APPEAL PROCESS GUIDE FOR THE PROPERTY OWNER IMPORTANT DATES TO KNOW 2018 APPEAL PROCESS TIME FRAME March 1 - assessment notices must be mailed March 15 - last day to file for owner-occupied status

2015 Polk County Assessor s Office. Ankeny Economic Development Corp. October 15, 2015

2015 Polk County Assessor s Office Ankeny Economic Development Corp. October 15, 2015 2015 Rollback Commercial - 90% Industrial - 90% Multiresidential 86.25% Residential 55.1976% (Projected) How is the

2015 Polk County Assessor s Office Ankeny Economic Development Corp. October 15, 2015 2015 Rollback Commercial - 90% Industrial - 90% Multiresidential 86.25% Residential 55.1976% (Projected) How is the

Chapter 3 FINANCE, TAXATION, AND PUBLIC RECORDS

Chapter 3 FINANCE, TAXATION, AND PUBLIC RECORDS 3.01 Preparation of Tax Roll and Receipts 3.02 Fiscal Year 3.03 Allowance of Claims 3.04 Budget 3.05 Village Borrowing 3.06 Monthly Reports of Receipts 3.07

Chapter 3 FINANCE, TAXATION, AND PUBLIC RECORDS 3.01 Preparation of Tax Roll and Receipts 3.02 Fiscal Year 3.03 Allowance of Claims 3.04 Budget 3.05 Village Borrowing 3.06 Monthly Reports of Receipts 3.07

County and Tribal Coordinators:

and Tribal s: Area Covered Contact Position Title E-mail Phone Adams Co. Reesa Evans Lake revans@co.adams.wi.us 608-339-4275 Barron Co. Bayfield Co. Burnett Co. Dale Hanson Stefania Strzalkowska Dave Ferris

and Tribal s: Area Covered Contact Position Title E-mail Phone Adams Co. Reesa Evans Lake revans@co.adams.wi.us 608-339-4275 Barron Co. Bayfield Co. Burnett Co. Dale Hanson Stefania Strzalkowska Dave Ferris

IMPORTANT ANNOUNCEMENT: Our website is changing! Please click here for details.

IMPORTANT ANNOUNCEMENT: Our website is changing! Please click here for details. Home Search Downloads Exemptions Agriculture Maps Tangible Links Contact Home Frequently Asked Questions (FAQ) Frequently

IMPORTANT ANNOUNCEMENT: Our website is changing! Please click here for details. Home Search Downloads Exemptions Agriculture Maps Tangible Links Contact Home Frequently Asked Questions (FAQ) Frequently

Office of Legislative Services Background Report The Revaluation of Real Property: Answers to Frequently Asked Questions About the Revaluation Process

Office of Legislative Services Background Report The Revaluation of Real Property: Answers to Frequently Asked Questions About the Revaluation Process OLS Background Report No. 119 Prepared By: Local Government

Office of Legislative Services Background Report The Revaluation of Real Property: Answers to Frequently Asked Questions About the Revaluation Process OLS Background Report No. 119 Prepared By: Local Government

ARLINGTON COUNTY CODE. Chapter 20 REAL ESTATE ASSESSMENT. Article I. In General

ARLINGTON COUNTY CODE Chapter 20 Article I. In General 20-1. Department of Real Estate Assessments Established. 20-2. Board of Equalization of Real Estate Assessments Established; Powers; Compensation.

ARLINGTON COUNTY CODE Chapter 20 Article I. In General 20-1. Department of Real Estate Assessments Established. 20-2. Board of Equalization of Real Estate Assessments Established; Powers; Compensation.

4-1 TITLE 6 MOBILE HOME AND RECREATIONAL VEHICLE PARKS 4-3

4-1 TITLE 6 MOBILE HOME AND RECREATIONAL VEHICLE PARKS 4-3 Chapter 4 RECREATIONAL VEHICLE PARKS Sec. 4-1: Sec. 4-2: Sec. 4-3: Sec. 4-4: Sec. 4-5: Sec. 4-6: Sec. 4-7: Sec. 4-8: Sec. 4-9: Sec. 4-10: Sec.

4-1 TITLE 6 MOBILE HOME AND RECREATIONAL VEHICLE PARKS 4-3 Chapter 4 RECREATIONAL VEHICLE PARKS Sec. 4-1: Sec. 4-2: Sec. 4-3: Sec. 4-4: Sec. 4-5: Sec. 4-6: Sec. 4-7: Sec. 4-8: Sec. 4-9: Sec. 4-10: Sec.

Reappraisal Important Property Tax Information

Reappraisal 2013 Important Property Tax Information Spartanburg County Assessor PO Box 5762 Spartanburg, SC 29304 Telephone: (864)596-2544 Fax: (864)596-2940 Fax: (864)596-2223 www.spartanburgcounty.org

Reappraisal 2013 Important Property Tax Information Spartanburg County Assessor PO Box 5762 Spartanburg, SC 29304 Telephone: (864)596-2544 Fax: (864)596-2940 Fax: (864)596-2223 www.spartanburgcounty.org

Understanding Mississippi Property Taxes

Understanding Mississippi Property Taxes Property tax revenues are a vital component of the budgets of Mississippi s local governments. Property tax revenues allow these governments to provide important

Understanding Mississippi Property Taxes Property tax revenues are a vital component of the budgets of Mississippi s local governments. Property tax revenues allow these governments to provide important

Open Space Taxation Act

Open Space Taxation Act WASHINGTON STATE DEPARTMENT OF REVENUE JUNE 2007 The information and instructions in this brochure are to be used when applying for assessment on the basis of current use under

Open Space Taxation Act WASHINGTON STATE DEPARTMENT OF REVENUE JUNE 2007 The information and instructions in this brochure are to be used when applying for assessment on the basis of current use under

SEASONAL CAMPING AT CORPS PROJECTS

SEASONAL CAMPING AT CORPS PROJECTS The entity(ies) responsible for operating outgranted campgrounds are referred to as "Lessee(s)" and are defined as those campgrounds operating under park and recreation

SEASONAL CAMPING AT CORPS PROJECTS The entity(ies) responsible for operating outgranted campgrounds are referred to as "Lessee(s)" and are defined as those campgrounds operating under park and recreation

DEMO ITEM SUBJECT COMPARABLE SOLD # 1 COMPARABLE SOLD # 2 COMPARABLE SOLD # 3

Residential Broker Price Opinion FHA CASE #: ASSIGNED LLB: PROPERTY ADDRESS: I. GENERAL MARKET CONDITIONS II. Current market condition: Depressed Slow Stable Improving Excellent Employment conditions:

Residential Broker Price Opinion FHA CASE #: ASSIGNED LLB: PROPERTY ADDRESS: I. GENERAL MARKET CONDITIONS II. Current market condition: Depressed Slow Stable Improving Excellent Employment conditions:

As Introduced. 132nd General Assembly Regular Session H. B. No

132nd General Assembly Regular Session H. B. No. 368 2017-2018 Representative Lepore-Hagan Cosponsors: Representatives Holmes, Ingram, O'Brien, Reece, Sheehy A B I L L To amend sections 1343.01, 3781.10,

132nd General Assembly Regular Session H. B. No. 368 2017-2018 Representative Lepore-Hagan Cosponsors: Representatives Holmes, Ingram, O'Brien, Reece, Sheehy A B I L L To amend sections 1343.01, 3781.10,

UNDERSTANDING PROPERTY TAXES IN COLORADO

UNDERSTANDING PROPERTY TAXES IN COLORADO This brochure was created to provide general information on the Colorado property tax system. For more specific information on any one of these topics, please visit

UNDERSTANDING PROPERTY TAXES IN COLORADO This brochure was created to provide general information on the Colorado property tax system. For more specific information on any one of these topics, please visit

a. It is in the public interest that the Legislature address the difficult questions raised in litigation over the tax status of manufactured homes ;

Page 1 of 3 54:4-1.3. Legislative findings and determinations The Legislature finds and determines that: a. It is in the public interest that the Legislature address the difficult questions raised in litigation

Page 1 of 3 54:4-1.3. Legislative findings and determinations The Legislature finds and determines that: a. It is in the public interest that the Legislature address the difficult questions raised in litigation

Monthly Statistical Reports INDEX

1 Monthly Statistical Reports INDEX 1. Index Page 2. Monthly Statistical Narrative 4. Month and YTD Sold & Active Single Family Listings 5. Monthly Sales by Price Range and Bedrooms 6. Single Family Sold

1 Monthly Statistical Reports INDEX 1. Index Page 2. Monthly Statistical Narrative 4. Month and YTD Sold & Active Single Family Listings 5. Monthly Sales by Price Range and Bedrooms 6. Single Family Sold

Separating Intangible Value in Valuation of Billboards & Other Property

Separating Intangible Value in Valuation of Billboards & Other Property Clark R. Calhoun Partner Alston & Bird LLP Los Angeles, CA Clark.Calhoun@Alston.com Joe Torzewski Direction, Valuation Stout Advisory

Separating Intangible Value in Valuation of Billboards & Other Property Clark R. Calhoun Partner Alston & Bird LLP Los Angeles, CA Clark.Calhoun@Alston.com Joe Torzewski Direction, Valuation Stout Advisory

The Texas Constitution sets out five basic rules for property taxes in our state:

Why does the appraisal district look at values each year? The Texas Constitution sets out five basic rules for property taxes in our state: 1. Taxation must be equal and uniform. No single property or

Why does the appraisal district look at values each year? The Texas Constitution sets out five basic rules for property taxes in our state: 1. Taxation must be equal and uniform. No single property or

2018 Annual Appraisal Report

2018 Annual Appraisal Report SUMMARY OF APPRAISAL ACTIVITIES, EXEMPTIONS, EQUALIZATION AND TAX RATES FOR 2018 TAX YEAR Wendy Grams, RPA, CTA, CCA CENTRAL APPRAISAL DISTRICT OF BANDERA COUNTY P. O. BOX

2018 Annual Appraisal Report SUMMARY OF APPRAISAL ACTIVITIES, EXEMPTIONS, EQUALIZATION AND TAX RATES FOR 2018 TAX YEAR Wendy Grams, RPA, CTA, CCA CENTRAL APPRAISAL DISTRICT OF BANDERA COUNTY P. O. BOX

SPECIAL ISSUES AFFECTING MUNICIPALITIES IN REAL ESTATE

SPECIAL ISSUES AFFECTING MUNICIPALITIES IN REAL ESTATE 1 Opportunity Zones Program Issues when buying/selling real property Fees & Costs in Condemnation Dark Property Theory 2 1 Purpose: Designed to promote

SPECIAL ISSUES AFFECTING MUNICIPALITIES IN REAL ESTATE 1 Opportunity Zones Program Issues when buying/selling real property Fees & Costs in Condemnation Dark Property Theory 2 1 Purpose: Designed to promote

HOW TO PREPARE FOR YOUR ASSESSMENT APPEAL HEARING

ASSESSMENT APPEALS BOARD COUNTY OF SANTA BARBARA HOW TO PREPARE FOR YOUR ASSESSMENT APPEAL HEARING An Information Guide For Santa Barbara County Property Owners and Authorized Agents Assessment Appeals

ASSESSMENT APPEALS BOARD COUNTY OF SANTA BARBARA HOW TO PREPARE FOR YOUR ASSESSMENT APPEAL HEARING An Information Guide For Santa Barbara County Property Owners and Authorized Agents Assessment Appeals

COMPLAINT ON REAL PROPERTY ASSESSMENT FOR 20. BEFORE THE BOARD OF ASSESSMENT REVIEW FOR (city, town village or county) PART ONE: GENERAL INFORMATION

PART ONE: GENERAL INFORMATION") NEW YORK STATE DEPARTMENT OF TAXATION & FINANCE OFFICE OF REAL PROPERTY TAX SERVICES RP-524 (3/09) COMPLAINT ON REAL PROPERTY ASSESSMENT FOR 20 BEFORE THE BOARD OF ASSESSMENT REVIEW FOR (city, town village

NEW YORK STATE DEPARTMENT OF TAXATION & FINANCE OFFICE OF REAL PROPERTY TAX SERVICES RP-524 (3/09) COMPLAINT ON REAL PROPERTY ASSESSMENT FOR 20 BEFORE THE BOARD OF ASSESSMENT REVIEW FOR (city, town village

We look forward to working with you to build on our collaboration and enhance our partnership on behalf of all Minnesotans.

Date: February 27, 2017 To: County Assessors, Auditors, and Treasurers From: Cynthia Rowley, Director Property Tax Division Subject: Property Tax Services Report The Property Tax Division of the Minnesota

Date: February 27, 2017 To: County Assessors, Auditors, and Treasurers From: Cynthia Rowley, Director Property Tax Division Subject: Property Tax Services Report The Property Tax Division of the Minnesota

Source: Reg. Y, 55 FR 27771, July 5, 1990, unless otherwise noted.

Subpart G Appraisal Standards for Federally Related Transactions Source: Reg. Y, 55 FR 27771, July 5, 1990, unless otherwise noted. 225.61 Authority, purpose, and scope. (a) Authority. This subpart is

Subpart G Appraisal Standards for Federally Related Transactions Source: Reg. Y, 55 FR 27771, July 5, 1990, unless otherwise noted. 225.61 Authority, purpose, and scope. (a) Authority. This subpart is

GENERAL ASSESSMENT DEFINITIONS

21st Century Appraisals, Inc. GENERAL ASSESSMENT DEFINITIONS Ad Valorem tax. A tax levied in proportion to the value of the thing(s) being taxed. Exclusive of exemptions, use-value assessment laws, and

21st Century Appraisals, Inc. GENERAL ASSESSMENT DEFINITIONS Ad Valorem tax. A tax levied in proportion to the value of the thing(s) being taxed. Exclusive of exemptions, use-value assessment laws, and

METHODOLOGY GUIDE VALUING MOTELS IN ONTARIO. Valuation Date: January 1, 2016

METHODOLOGY GUIDE VALUING MOTELS IN ONTARIO Valuation Date: January 1, 2016 AUGUST 2016 August 22, 2016 The Municipal Property Assessment Corporation (MPAC) is responsible for accurately assessing and

METHODOLOGY GUIDE VALUING MOTELS IN ONTARIO Valuation Date: January 1, 2016 AUGUST 2016 August 22, 2016 The Municipal Property Assessment Corporation (MPAC) is responsible for accurately assessing and

IC Chapter 7. Real Property Transactions

IC 8-23-7 Chapter 7. Real Property Transactions IC 8-23-7-0.1 Application of certain amendments to chapter Sec. 0.1. The amendments made to section 19 of this chapter by P.L.133-2007 apply only to public

IC 8-23-7 Chapter 7. Real Property Transactions IC 8-23-7-0.1 Application of certain amendments to chapter Sec. 0.1. The amendments made to section 19 of this chapter by P.L.133-2007 apply only to public

QUESTIONS? CALL THE ASSESSOR S OFFICE

2018 GRIEVANCE PACKET PLEASE NOTE: The Assessor s Office will make five (5) copies of the RP 524 complaint form and suppor ng documenta on for the Board of Assessment Review members if received on or before

2018 GRIEVANCE PACKET PLEASE NOTE: The Assessor s Office will make five (5) copies of the RP 524 complaint form and suppor ng documenta on for the Board of Assessment Review members if received on or before

ASSESSORS ANSWER FREQUENTLY ASKED QUESTIONS ABOUT REAL PROPERTY Assessors Office, 37 Main Street

A. THE ASSESSMENT PROCESS: ASSESSORS ANSWER FREQUENTLY ASKED QUESTIONS ABOUT REAL PROPERTY Assessors Office, 37 Main Street What is mass appraisal? Assessors must value all real and personal property in

A. THE ASSESSMENT PROCESS: ASSESSORS ANSWER FREQUENTLY ASKED QUESTIONS ABOUT REAL PROPERTY Assessors Office, 37 Main Street What is mass appraisal? Assessors must value all real and personal property in

Appendix C SUMMARY OF LAND USE-RELATED EXTRATERRITORIAL AUTHORITIES

#235120-2 NMA/RMB 3/13/17 Appendix C SUMMARY OF LAND USE-RELATED EXTRATERRITORIAL AUTHORITIES Introduction Cities and villages in Wisconsin have several types of extraterritorial authority that may affect

#235120-2 NMA/RMB 3/13/17 Appendix C SUMMARY OF LAND USE-RELATED EXTRATERRITORIAL AUTHORITIES Introduction Cities and villages in Wisconsin have several types of extraterritorial authority that may affect

CHAPTER Senate Bill No. 4-D

CHAPTER 2007-339 Senate Bill No. 4-D An act relating to ad valorem taxation; authorizing the Department of Revenue to adopt emergency rules; providing for application and renewal thereof; requiring the

CHAPTER 2007-339 Senate Bill No. 4-D An act relating to ad valorem taxation; authorizing the Department of Revenue to adopt emergency rules; providing for application and renewal thereof; requiring the

Report and Recommendations of the Chelsea City Study Committee

Report and Recommendations of the Chelsea City Study Committee To the Honorable The Village President and Trustees The Village of Chelsea, Michigan Preamble By resolution dated June 9 1992 the Chelsea

Report and Recommendations of the Chelsea City Study Committee To the Honorable The Village President and Trustees The Village of Chelsea, Michigan Preamble By resolution dated June 9 1992 the Chelsea

BROCHURE # 37 OPEN SPACE

BROCHURE # 37 OPEN SPACE The information and instructions in this publication are to be used when applying for assessment on the basis of current use under the open space laws, chapter 84.34 RCW and chapter

BROCHURE # 37 OPEN SPACE The information and instructions in this publication are to be used when applying for assessment on the basis of current use under the open space laws, chapter 84.34 RCW and chapter

COMMERCIAL REHABILITATION ACT Act 210 of The People of the State of Michigan enact:

COMMERCIAL REHABILITATION ACT Act 210 of 2005 AN ACT to provide for the establishment of commercial rehabilitation districts in certain local governmental units; to provide for the exemption from certain

COMMERCIAL REHABILITATION ACT Act 210 of 2005 AN ACT to provide for the establishment of commercial rehabilitation districts in certain local governmental units; to provide for the exemption from certain

Copyright, 1999, 2002, 2004, Freddie Mac. All Rights Reserved.

Page 1 of 13 Engineering Requirements/Chapter 12: Appraiser and Appraisal Requirements/12.1: General requirements 12.1: General requirements For all multifamily purchase programs and products, the Seller/Servicer

Page 1 of 13 Engineering Requirements/Chapter 12: Appraiser and Appraisal Requirements/12.1: General requirements 12.1: General requirements For all multifamily purchase programs and products, the Seller/Servicer

Final Report Taxpayer Complaint. Teller County

Final Report 2013 Taxpayer Complaint Teller County February 12, 2014 Submitted by: Laura Forbes, Administrative Resources 2013 Taxpayer Complaint Teller County Page 1 Complaint filed: Teller County Property

Final Report 2013 Taxpayer Complaint Teller County February 12, 2014 Submitted by: Laura Forbes, Administrative Resources 2013 Taxpayer Complaint Teller County Page 1 Complaint filed: Teller County Property

STATE OF WEST VIRGINIA

OF WEST VIRGINIA Office of County Assessor Commercial Business Property Return County Code: 20 District: Account No.: Business Code: (rev. 2017) THIS RETURN IS TO BE FILED AS SOON AS POSSIBLE AFTER JULY

OF WEST VIRGINIA Office of County Assessor Commercial Business Property Return County Code: 20 District: Account No.: Business Code: (rev. 2017) THIS RETURN IS TO BE FILED AS SOON AS POSSIBLE AFTER JULY

THE CORPORATION OF THE TOWNSHIP OF MUSKOKA LAKES BY-LAW NUMBER

THE CORPORATION OF THE TOWNSHIP OF MUSKOKA LAKES BY-LAW NUMBER 2014-107 A By-Law of the Corporation of the Township of Muskoka Lakes with respect to Development Charges. WHEREAS the Township of Muskoka

THE CORPORATION OF THE TOWNSHIP OF MUSKOKA LAKES BY-LAW NUMBER 2014-107 A By-Law of the Corporation of the Township of Muskoka Lakes with respect to Development Charges. WHEREAS the Township of Muskoka

Assessment Overview. Gallagher Amendment Interim Committee. July 13, 2018

Assessment Overview Gallagher Amendment Interim Committee July 13, 2018 Life s FAQs: Why is the sky blue? How does gravity work? Are we there yet? What happens in an Assessor s office.. how does property

Assessment Overview Gallagher Amendment Interim Committee July 13, 2018 Life s FAQs: Why is the sky blue? How does gravity work? Are we there yet? What happens in an Assessor s office.. how does property

Ferry County Ordinance #89-04 BINDING SITE PLAN ORDINANCE

Ferry County Ordinance #89-04 BINDING SITE PLAN ORDINANCE AN ORDINANCE providing for an alternate method of subdividing property for the purpose of allowing tracts of land having more than one residence

Ferry County Ordinance #89-04 BINDING SITE PLAN ORDINANCE AN ORDINANCE providing for an alternate method of subdividing property for the purpose of allowing tracts of land having more than one residence

MAINE REVENUE SERVICES PROPERTY TAX DIVISION PROPERTY TAX BULLETIN NO. 19

MAINE REVENUE SERVICES PROPERTY TAX DIVISION PROPERTY TAX BULLETIN NO. 19 MAINE TREE GROWTH TAX LAW REFERENCE: 36 M.R.S.A. 571-584-A. Issued May 2013; Replaces September, 2012 FOR RECENT CHANGES TO THE

MAINE REVENUE SERVICES PROPERTY TAX DIVISION PROPERTY TAX BULLETIN NO. 19 MAINE TREE GROWTH TAX LAW REFERENCE: 36 M.R.S.A. 571-584-A. Issued May 2013; Replaces September, 2012 FOR RECENT CHANGES TO THE

How to Contest Your Assessment

How to Contest Your Assessment STATE OF NEW YORK Eliot Spitzer, Governor Donald C. DeWitt, Executive Director New York State Office of Real Property Services 16 Sheridan Avenue Albany, New York 12210-2714

How to Contest Your Assessment STATE OF NEW YORK Eliot Spitzer, Governor Donald C. DeWitt, Executive Director New York State Office of Real Property Services 16 Sheridan Avenue Albany, New York 12210-2714

CHAPTER House Bill No. 963

CHAPTER 2000-401 House Bill No. 963 An act relating to Manatee County; merging the Anna Maria Fire Control District and Westside Fire Control District to create a new district; creating and establishing

CHAPTER 2000-401 House Bill No. 963 An act relating to Manatee County; merging the Anna Maria Fire Control District and Westside Fire Control District to create a new district; creating and establishing

UNDERSTANDING PROPERTY ASSESSMENT APPEALS A GUIDE TO REGULAR ASSESSMENT APPEALS UNDER TRUE MARKET VALUE AND COMMON LEVEL RANGE STANDARDS

UNDERSTANDING PROPERTY ASSESSMENT APPEALS A GUIDE TO REGULAR ASSESSMENT APPEALS UNDER TRUE MARKET VALUE AND COMMON LEVEL RANGE STANDARDS This information was developed to assist property owners in preparing

UNDERSTANDING PROPERTY ASSESSMENT APPEALS A GUIDE TO REGULAR ASSESSMENT APPEALS UNDER TRUE MARKET VALUE AND COMMON LEVEL RANGE STANDARDS This information was developed to assist property owners in preparing

PAYMENT UNDER PROTEST APPEAL GUIDE

PAYMENT UNDER PROTEST APPEAL GUIDE In Kansas you have two opportunities to appeal the value of your property. If you appeal at the time of paying taxes, it is called a Payment Under Protest. This guide

PAYMENT UNDER PROTEST APPEAL GUIDE In Kansas you have two opportunities to appeal the value of your property. If you appeal at the time of paying taxes, it is called a Payment Under Protest. This guide

Athens County Auditor, Jill Thompson provides homeowners answers to the most commonly asked questions about the countywide 2014 reappraisal

Contact: Jill Thompson Athens County Auditor Phone 740.592.3223 Fax 740.594.3270 15 S. Court Street, Room 330 Athens, Ohio 45701 www.athenscountyauditor.org Jill Thompson Athens County Auditor Property

Contact: Jill Thompson Athens County Auditor Phone 740.592.3223 Fax 740.594.3270 15 S. Court Street, Room 330 Athens, Ohio 45701 www.athenscountyauditor.org Jill Thompson Athens County Auditor Property

IN THE DISTRICT COURT OF APPEAL OF THE STATE OF FLORIDA FIFTH DISTRICT JULY TERM v. CASE NO. 5D

IN THE DISTRICT COURT OF APPEAL OF THE STATE OF FLORIDA FIFTH DISTRICT JULY TERM 2003 RON SCHULTZ, as Property Appraiser of Citrus County, et al., Appellants, v. CASE NO. 5D02-2406 TIME WARNER ENTERTAINMENT

IN THE DISTRICT COURT OF APPEAL OF THE STATE OF FLORIDA FIFTH DISTRICT JULY TERM 2003 RON SCHULTZ, as Property Appraiser of Citrus County, et al., Appellants, v. CASE NO. 5D02-2406 TIME WARNER ENTERTAINMENT

IN THE OREGON TAX COURT MAGISTRATE DIVISION Property Tax ) ) ) ) ) ) ) ) )

) ) ) ) ) ) ) )") IN THE OREGON TAX COURT MAGISTRATE DIVISION Property Tax DON CHAMBERS, Plaintiff, v. LINCOLN COUNTY ASSESSOR, Defendant. TC-MD 070161C DECISION 1 Plaintiff appeals the value of his mobile home, identified

IN THE OREGON TAX COURT MAGISTRATE DIVISION Property Tax DON CHAMBERS, Plaintiff, v. LINCOLN COUNTY ASSESSOR, Defendant. TC-MD 070161C DECISION 1 Plaintiff appeals the value of his mobile home, identified

Title 17 MOBILE HOMES AND RECREATIONAL VEHICLES

17.04 General Provisions Title 17 MOBILE HOMES AND RECREATIONAL VEHICLES 17.04.010 General provisions 17.04.020 Application 17.04.030 Interpretation 17.04.040 Mobile homes and recreational vehicles--location

17.04 General Provisions Title 17 MOBILE HOMES AND RECREATIONAL VEHICLES 17.04.010 General provisions 17.04.020 Application 17.04.030 Interpretation 17.04.040 Mobile homes and recreational vehicles--location

ZONING PERMIT MOBILE HOME (ZPMH) SUBMITTAL CHECKLIST

SUBMITTAL CHECKLIST") ZONING PERMIT MOBILE HOME (ZPMH) SUBMITTAL CHECKLIST (A PRINCIPLE DWELLING UNIT, TEMPORARY USE DURING CONSTRUCTION OF RESIDENCE, TEMPORARY STORAGE (UNLESS OTHERWISE SPECIFIED), TEMPORARY ACCESSORY FARM

ZONING PERMIT MOBILE HOME (ZPMH) SUBMITTAL CHECKLIST (A PRINCIPLE DWELLING UNIT, TEMPORARY USE DURING CONSTRUCTION OF RESIDENCE, TEMPORARY STORAGE (UNLESS OTHERWISE SPECIFIED), TEMPORARY ACCESSORY FARM

How to Build a Defensible Record

ASSESSMENT LITIGATION: How to Build a Defensible Record 2017 LWM Assessor Institute, Lake Lawn Resort, Delevan Presented by Amy Seibel & Shannon Krause What type of valuation year? Revaluation Year Maintenance

ASSESSMENT LITIGATION: How to Build a Defensible Record 2017 LWM Assessor Institute, Lake Lawn Resort, Delevan Presented by Amy Seibel & Shannon Krause What type of valuation year? Revaluation Year Maintenance

How to Petition for a Review of Your Property Taxes: County Board of Equalization