Klickitat County Assessor's Office Mass Appraisal Report

|

|

|

- Emily McKenzie

- 6 years ago

- Views:

Transcription

1 Klickitat County Assessor's Office Mass Appraisal Report Appraisal Date: January 1, 2012 for 2013 Property Taxes Report Date: Aug 14, 2012 Prepared For: Darlene R. Johnson, Klickitat County Assessor By: Karen Reisenauer, Supervisor Assessor

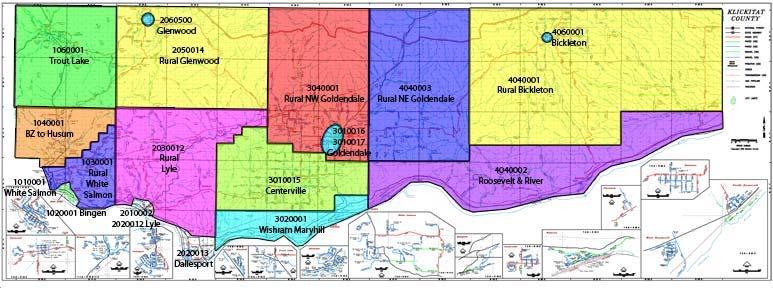

2 Preliminary Summary of Value Change: This mass appraisal report is a post revaluation report card on the performance of the valuation model(s) used. It is not a fully self contained appraisal report but rather a summary of the performance of the model used in the mass appraisal process for Klickitat County. All real property parcels and personal property parcels were valued for this report. This is a preliminary summary report as of Aug 14, This does not include any New Construction values. These values are subject to change only from Board of Equalization ordered changes and manifest error changes. Preliminary Summary of Real Property Value Change* January 1, ,887,918,134 January 1, ,916,168,266 Value Change 28,250,132 Percent Change 1.5% Preliminary Summary of Real Property Value Change by Neighborhood* Nbrhd Description Parcels Difference White Salmon Urban ,481, ,709, % Area 1 Commercial ,358,130 94,172, % Bingen ,309,500 34,963, % Rural White Salmon, Snowden ,776, ,689, % Husum to BZ Corner ,522, ,483, % BZ Corner to Trout Lake ,275, ,872, % Lyle I ,502,950 43,644, % Area 2 Commercial 98 20,580,960 21,513, % Lyle II ,913,600 19,225, % Dallesport Murdock ,580, ,412, % Appleton, Klickitat, and Surrounding ,029, ,940, % Rural Glenwood ,205,174 55,888, % Glenwood, Klickitat Urban ,688,880 16,408, % Area 3 Commercial ,192,290 54,775, % Centerville and Surrounding ,629,666 68,539, % Goldendale Urban I ,969, ,114, % Goldendale Urban II 45 6,228,700 6,239, % Wishram and River Communities ,157,990 25,576, % N NW Goldendale Rural ,034, ,312, % Area 4 Commercial 75 26,827,130 27,045, % Bickleton Rural and Surrounding ,885,470 61,864, % Roosevelt and River Communities ,958,500 26,734, % NE Goldendale Rural ,311, ,957, % Bickleton Urban 108 3,497,250 4,083, % Klickitat County ,887,918,134 1,916,168, % *The Summary of Value Change reflect the aggregate change in value for residential parcels. Personal Property Listings, and New Construction will have their assessed value notices sent in September and certified September 15. All data in this Summary Table is from pre-certification Residential Report dated August 14, The values in this report may change.

3 Preliminary Summary of Personal Property Value Change* January 1, ,211,873,980 January 1, ,202,645,730 Value Change -9,228,250 Percent Change -0.76% *The Preliminary Summary of Personal Property Value Change reflects the aggregate change in value for personal property accounts, which include real property located on leased land such as wind turbines, and personal property accounts of businesses located in Klickitat County. All data in this Summary Table is from pre-certification Residential Report dated August 14, The values in this report may change. Client and Intended Users: This residential mass appraisal report was prepared for the Klickitat County Assessor as per the client's instructions. The intended users include the Assessor (Client), the Klickitat County Board of Equalization, the Washington State Board of Tax Appeals and the Washington State Department of Revenue. No other users are intended or implied. Client Instructions to Appraisers: Appraise all properties in each Residential Appraisal Management Region by the date specified in the approved Department of Revenue Klickitat County revaluation plan. The appraisals are to be compliant with Washington State Law (RCW), Washington State Administrative Code (WAC), Washington State Department of Revenue (DOR) guidelines, and International Association of Assessing Officers (IAAO) standard on ratio studies, July 2007 edition and the Uniform Standards of Professional Appraisal Standards (USPAP) Standard 6: Mass Appraisal, Development and Reporting. The appraisals are to be performed using industry standards mass appraisal techniques. Physical inspections must comply with the revaluation plan approved by the Washington State Department of Revenue November 5, Physical inspections will at a minimum be a curbside visit and review of the property characteristics. An effort should be made to inspect and review all qualified sales that occurred in the year prior to the assessment date. A written mass appraisal report that is compliant with USPAP Standard 6 must be completed. The intended use of the appraisals and subsequent report is the administration of ad valorem property appraisals. Use of This Report The use of this report, its analysis and conclusions, is limited to the administration of appraisals for property tax purposes in accordance with Washington State law and administrative code. The information and conclusions contained in this report cannot be relied upon for any other purpose. This document is not intended to be a self contained documentation of the mass appraisal but to summarize the methods and data used and to guide the reader to other documents or files which were relied upon to perform the mass appraisal. These other documents may include the following: Individual Property Records - Contained in Assessor's Property System Database / ProVal Real Estate Sales File Part of Assessor's Property System Database / ProVal Land Sales and Model Calibration Spreadsheets

4 Residential Cost Tables Contained in Assessor's Property System Database / ProVal Residential Depreciation Tables Contained in the Assessor's Property System Database / ProVal Revised Code of Washington (RCW) - Title 84 Washington Administrative Code (WAC) WAC 458 Uniform Standards of Professional Appraisal Practice (USPAP) published by the Appraisal Standards Board of the Appraisal Foundation Klickitat County Revaluation plan as approved by the Washington State Department of Revenue Mass Appraisal Report data extracts and sales files Measuring Real Property Appraisal Performance in Washington's Property Tax System Office of Program Research, Washington House of Representatives (Accessed at Property Assessment Valuation published by the International Association of Assessing Officers, 3 rd Edition, Property Appraisal and Assessment Administration by the International Association of Assessing Officers, Mass Appraisal of Real Property by the International Association of Assessing Officers, IAAO Mass Appraisal Report Template Snohomish County Mass Appraisal Report Effective Date of the Appraisal: January 1, 2012 The appraisal date for properties other than new construction is January 1 st as required by Washington State legislative requirements. The appraisal date for new construction is July 31 st as required by Washington State legislative requirements. RCW Assessment date Average inventory basis may be used Public inspection of listing, documents, and records. All real property in this state subject to taxation shall be listed and assessed every year, with reference to its value on the first day of January of the year in which it is assessed. The appraisal date for new construction, that is those properties that were issued a building permit or should have been issued a building permit, is July 31st. RCW New construction building permits When property placed on assessment rolls. The county assessor is authorized to place any property that is increased in value due to construction or alteration for which a building permit was issued, or should have been issued, under chapter 19.27, 19.27A, or RCW or other laws providing for building permits on the assessment rolls for the purposes of tax levy up to August 31st of each year. The assessed valuation of the property shall be considered as of July 31st of that year. Type and Definition of Value: Market Value for Assessment Purposes Market Value: The basis of all assessments is the true and fair market value of property. True and fair market value (Spokane etc. R. Company v. Spokane County, 75 Wash. 72 (1913); Mason County Overtaxed, Inc. v. Mason County, 62d (1963); AGO 57-58, No. 2, 1/8/57; AGO 65-66, No /31/65... or amount of money a buyer is willing but not obligated to buy would pay for it to a seller willing but not obligated to sell. In arriving at a determination of such value, the assessing officer can consider only those factors that can within reason be said to affect the price in negotiations between a

5 willing purchaser and willing seller, and he must consider all of such factors (AGO No. 65, 12/31/65). WAC (1) True and fair value -- Defined. All property must be valued and assessed at one hundred percent of true and fair value unless otherwise provided by law. "True and fair value" means market value and is the amount of money a buyer of property willing but not obligated to buy would pay a seller of property willing but not obligated to sell, taking into consideration all uses to which the property is adapted and might in reason be applied. (2) True and fair value--criteria. In determining true and fair value, the assessor may use the sales (market data) approach, the cost approach, or the income approach, or a combination of the three approaches to value. The provisions of (b) and (c) of this subsection, the cost and income approaches, respectively, shall be the dominant factors considered in determining true and fair value in cases of property of a complex nature, or property being used under terms of a franchise granted by a public agency, or property being operated as a public utility, or property not having a record of sale within five years and not having a significant number of sales of comparable property in the general area. When the cost or income approach is used, the assessor shall provide the property owner, upon request, with the factors used in arriving at the value determined, subject to any lawful restrictions on the disclosure of confidential or privileged tax information. Assumptions, Limiting Conditions, and Jurisdictional Exceptions: The properties were assumed to be free of any and all liens and encumbrances. Each property has also been appraised as though under responsible ownership and competent management. Surveys of the assessed properties have not been provided. We have relied upon tax maps and other materials in the course of estimating physical dimensions and the acreage associated with assessed properties. We assume the utilization of the land and any improvements is located within the boundaries of the property described. It is assumed that there are no adverse easements or encroachments for any parcel that have not already been addressed in the mass appraisal, unless otherwise noted in the property system database. In the preparation of the mass appraisal, interior inspections have/have not been made of the parcels of property included in this report. All inspections are made from the exterior only. It is assumed that the condition of the interior of each property is similar to its exterior condition, unless the assessor has received additional information from qualified sources giving more specific detail about the interior condition. Property inspection dates will have ranged in time from both before and after the appraisal date. It is assumed that there has been no material change in condition from the latest property inspection, unless otherwise noted on individual property records retained in the assessor s office. We assume that there are no hidden or unapparent conditions associated with the properties, subsoil, or structures, which would render the properties (land and/or improvements) more or less valuable, unless otherwise noted in the property system database. It is assumed that the properties and/or the landowners are in full compliance with all applicable federal, state, and local environmental regulations and laws, unless otherwise noted in the property system database.

6 It is assumed that all applicable zoning and use regulations have been complied with, unless otherwise noted in the property system database. It is assumed that all required licenses, certificates of occupancy, consents, or other instruments of legislative or administrative authority from any private, local, state, or national government entity have been obtained for any use on which the value opinions contained within this report are based. We have not been provided a hazardous condition s report, nor are we qualified to detect hazardous materials. Therefore, evidence of hazardous materials, which may or may not be present on a property, was not observed. As a result, the final opinion of value is predicated upon the assumption that there is no such material on any of the properties that might result in a loss, or change in value. It is assumed that there are no hazardous materials affecting the value of the property, unless specifically identified in the property system database. Information, estimates, and opinions furnished to the appraisers and incorporated into the analysis and final report were obtained from sources assumed to be reliable, and a reasonable effort has been made to verify such information. However, no warranty is given for the reliability of this information. The Americans with Disabilities Act (ADA) became effective January 26, We have not made compliance surveys nor conducted a specific analysis of any property to determine if it conforms to the various detailed requirements identified in the ADA. It is possible that such a survey might identify nonconformity with one or more ADA requirements, which could lead to a negative impact on the value of the property(s). Because such a survey has not been requested and is beyond the scope of this appraisal assignment, we did not take into consideration adherence or non-adherence to ADA in the valuation of the properties addressed in this report. Possession of this report does not carry with it the right of reproduction and disclosure of this report is governed by the rules and regulations of the State of Washington, and is subject to jurisdictional exception and the laws of the State of Washington. Fiscal constraints may impact data completeness and accuracy, valuation methods and valuation accuracy. The Assessor s records are assumed to be correct for the properties appraised. Sales utilized are assumed to be arm s-length market transactions; fiscal constraints limit the Assessor s ability to verify the transactions beyond initial sales screening. Secondary screening is limited to the mailing of sales questionnaires and/or inspection of 'outlier' sales. The subject property is assumed to be buildable unless otherwise noted in the property system database. It is assumed that the property is unaffected by sensitive or critical areas regulations (federal, state or local) unless otherwise noted in the property system database. Maps, aerials, and drawings may be included to assist the intended user in visualizing the property; however, no responsibility is assumed as to their exactness. The value conclusions contained in this report apply to the subject parcels only and are valid only for assessment purposes. No attempt has been made to relate the conclusions in this report to any other revaluation, past, present or future. It is assumed that 'exposure time' for the properties appraised are typical for their market area. It is assumed that the legal descriptions stored in the Assessor's property system database for the properties appraised are correct. No survey or search of title of the properties has been made for this report and no responsibility for legal matters is assumed.

7 Rental rates, when employed, were calculated in accord with generally accepted appraisal industry standards. The Klickitat County Assessor's office does not employ a sales database that captures property characteristics at the time of sale. Staffing resources preclude the level of sales review required to support this activity. Not employing a static sales database may bias the mass appraisal results when there are few sales with which to calibrate the market model. Exterior inspections were made of all properties in the physical inspection areas per the revaluation plan approved by the Washington State Department of Revenue dated Nov 5, 2009 and as required by RCW This inspection plan provides that all taxable real property is physically inspected one every four years. For the January 1, 2012 valuations, area 1 received physical inspections. Most properties received a visual inspection and some properties received 'walk around' inspections or interior inspections. Time constraints and fiscal constraints set by statue limit the ability of the Assessor s office to complete a more complete inspection of all parcels, however we make every effort to do on site and interior inspections for home owners who request an inspection. RCW Each county assessor shall cause taxable real property to be physically inspected and valued at least once every six years in accordance with RCW , and in accordance with a plan filed with and approved by the Department of Revenue. Jurisdictional Exception The mass appraisal must be completed within the time constraints set by statute and with the work force and financial resources available. Where these constraints limit the scope of work performed for the mass appraisal, limiting the ability to fully comply with USPAP Standards 6, the Jurisdictional Exception as provided for in Standard 6 is invoked.

8 Property Rights Appraised: Property Rights Appraised Fee Simple Fee Simple Title: Fee simple title indicates ownership that is absolute and subject to no limitation other than eminent domain, police power, escheat and taxation. (International Association of Assessing Officers, Glossary for Property Appraisal and Assessment, (Chicago. IAAO 1997). Scope of Work: Inspection of Property The modeling process relies on the physical inspections performed by the Klickitat County Inspection Team members and the data contained in the Assessor's Computer Added Mass Appraisal (CAMA) property system database (ProVal). CAMA models have the advantage of explicitly controlling for the effects of all variables tested in the model neighborhood, lot size, building size, construction grade, year built, and all other features for which variables were included in the model. All known land sales were investigated and site visits performed to verify the physical characteristics of the parcel unless precluded from doing so due to lack of access or lack of time that coincided with an extreme weather condition such as snow or flooding in which case aerial photographs and Parcel Analyst maps were utilized. Sales Source The Klickitat County Assessor's office utilizes sales obtained from Real Estate Excise Tax Affidavits filed with the Klickitat County Treasurer's Office. Sales Review Sales are assumed to be arm's length transactions based on initial screening in the sales verification process utilizing standards published by the Washington State Department of Revenue (see appendix for more information on this process). The mass appraisal must be completed within the time constraints set by statute and with the work force and financial resources available. These constraints limit the amount of sales review that can occur. Sales located in the scheduled physical inspection review area receive at a minimum an external inspection. Identification of Properties All residential parcels located within the boundaries of Klickitat County were valued. Each parcel is identified by a 14 digit parcel number. The first two digits represent the Township, the second two digits represent the Range, the next two digits represent the Section, the next four digits represent the Plat Number, and the next four represent a parcel number for administrative purposes. To help further stratify residential parcels, the County is broken into four inspection areas based on the approved plan. Each inspection area is divided into neighborhoods, which represent geographical areas that share important locational characteristics. As part of our effort in improve the statistical quality of our neighborhoods, the number of neighborhoods has decreased from 65 neighborhoods to a total of 20 residential neighborhoods, 5 commercial neighborhoods, and 2 neighborhoods with wind farm parcels. Inspection Area 1 had 18 neighborhoods and now has

9 approximately 5 neighborhoods; Inspection Area 2 had 21 neighborhoods and now has approximately 6 neighborhoods, Inspection Area 3 had 12 neighborhoods and now has approximately 5 neighborhoods, and Area 4 had 11 neighborhoods and now has 4 neighborhoods. Residential appraisal neighborhoods are identified with a seven (7) digit number. The first character of the neighborhood codes identifies the area in which inspection cycle the property is located but some neighborhoods now cross inspection areas. The complete neighborhood breakdowns are included in the appendix. Included in the appendix is a list of the House Types used to provide for coding of improvement house styles further stratified by the square footage. Highest and Best Use: This mass appraisal relies on the determinations of Highest and Best Use made by the Assessor's appraisal staff as part of Physical Inspection and/or Sales Review. RCW All property shall be valued at one hundred percent of its true and fair value in money and assessed on the same basis unless specifically provided otherwise by law. (1) The appraisal shall be consistent with the comprehensive land use plan, development regulations under chapter 36.70A RCW, zoning and any other governmental policies or practices in effect at the time of the appraisal that affect the use of property as well as physical and environmental influences. An assessment may not be determined by a method that assumes a land usage or highest and best use not permitted, for that property being appraised, under existing zoning or land use planning ordinances or statutes or other government restrictions. WAC (3) True and fair value -- Highest and best use. Unless specifically provided otherwise by statute, all property shall be valued on the basis of its highest and best use for assessment purposes. Highest and best use is the most profitable, likely use to which a property can be put. It is the use which will yield the highest return on the owner's investment. Any reasonable use to which the property may be put may be taken into consideration and if it is peculiarly adapted to some particular use, that fact may be taken into consideration. Uses that are within the realm of possibility, but not reasonably probable of occurrence, shall not be considered in valuing property at its highest and best use. Current Use Properties The market values of parcels enrolled in a 'current use farm and agriculture' or 'current use timber' category are set according to highest and best use. The taxable assessed value of current use timber lands and designated forest lands are set by statue by the Department of Revenue each year. The taxable assessed value of parcels enrolled in the Open Space Current Use Farm and Agriculture land should be set are set according to RCW and WAC, not on Highest and Best Use. These parcels current use value is set by considering the earning or productive capacity of comparable lands from crops grown most typically in the area average over not less than give year, capitalized at the rate set by the Department of Revenue each year. (RCW WAC ) Typically the net cash rental- which represents the leases of farm and agricultural land paid on an annual basis is divided by the 2012 capitalization rate of 7.06% to determine its current use value. Based on requirements from the Department of Revenue s audits of Klickitat County s Current Use Program in 2004, 2009 and 2011, we have changed the method of valuing current use farm and agriculture lands to follow statute. This year represents the first year that Klickitat County has had an Open Space Advisory

10 Board since 2001 as a method in assisting the Assessor s office in implementing assessment guidelines for current use values for farm and agriculture parcels. The advisory committee does not give advice regarding the valuation of specific parcels however; they supply the Assessor with advice on typical crops, land quality, leases and expenses. This information assists the Assessor in determining the appropriate current use values (RCW ). In a random selection of agriculture lands, we found that many current use values haven t change since 2001 and the 2004 audit by the Department of Revenue found some accounts have had the same value since The 2011 Open Space Advisory Board recommended rental rates to the Assessor at their May 3, 2012 meeting. All of Open Space Advisory Board meetings are open to the public and all minutes of the meetings are available online. The complete lease rates and subsequent rental rates are available online and in the separate Mass Appraisal Report of Current Use. In addition, the Department of Revenue required that all current use farm and agriculture lands less than 20 acres, current use timber, current use farm and agriculture conservation, current use open space and designated forest lands home sites to be assessed at true and fair market value. Prior values for these home sites were at a lower integral home site value only allowed by statute for parcels 20 acres or more in the farm and agricultural land classification. In addition, prior Board of County Commissioners resolution was unclear on the value of the home site of those enrolled in the current use open space land. Now the home site value is clearly at true and fair market value while the land is valued at 50% of the true and fair market value. These parcels have been recoded to reflect the true and fair market values resulting in a significant change in assessed value for these parcels. Preliminary Testing Results: WAC The Washington state Constitution requires that all taxes be uniform upon the same class of property within the territorial limits of the authority levying the tax. In order to comply with this constitutional mandate and ensure that all taxes are uniform, all real property must be valued in a manner consistent with this principle of uniformity. Also, to comply with statutory and case law, the county assessor must value all taxable real property in the county on a regular, systematic, and continuous basis. Klickitat County now values all taxable real property in the county annually. To help determine if the property tax is distributed fairly for local governments and taxing districts, IAAO recommends using ratio studies to measure mass appraisal performance. The Ratio studies measure two primary aspects of mass appraisal accuracy level and uniformity. In a ratio study, market values are represented by qualified individual market transactions or sales prices. The ratios used in a ratio study are formed by dividing appraised values made for tax purposes by actual sales prices. For example, a property appraised for tax purposes at $80,000 and sold for $100,000 has a ratio of.80 or 80 percent. This measures the Level of Assessments and the Assessor is required by statue to value at 1.00 or 100% percent of market value. Level of Assessment relates to the overall or average relationship between assessed values and market values Uniformity of Assessments relates to the consistency or equity of individual assessments. Uniformity measures the extent to which properties are assessed uniformly or at the same percentage of market value. Good uniformity is associated with equitable assessments. Poor uniformity implies inequitable assessments. To measure the uniformity or the fair equitable treatment of individual properties additional statistical analysis is conducted on the ratios. The most common measure is the coefficient of dispersion (COD), which provides a measure of appraisal uniformity independent of the level of

11 appraisal. IAAO recommends a COD for single family residential homes of 20.0 or less. Complete IAAO Ratio Study Performance Standards are included in the appendix of this report. Preliminary to the initiation of the 2012 revaluation, ratio studies were conducted to measure the relationship of current assessed values to 2011 sales prices and to determine examine the uniformity of assessments in Klickitat County. The Pre-Revaluation analysis showed that the past January 1, 2010 assessed values would be not accurate and reliable if used for the assessed values for January 1, To perform the Pre-revaluation analysis, the pre appraisal ratio is calculated by dividing the 2010 certified value by the 2010 sales price and performing additional statistically analysis using our Computed Aided Mass Appraisal System, ProVal. Neighborhood Description Median Ratio Post Revaluation Ratio Study Arith. Mean Weighted Mean Coefficient of Dispersion Price Related Differential White Salmon Urban Area 1 Commercial Bingen Rural White Salmon, Snowden Husum to BZ Corner BZ Corner to Trout Lake Lyle I Area 2 Commercial n/a n/a n/a n/a n/a Lyle II Dallesport Murdock Appleton, Klickitat, and Surrounding Rural Glenwood Glenwood, Klickitat Urban Area 3 Commercial Centerville and Surrounding Goldendale Urban I Goldendale Urban II Wishram and River Communities N NW Goldendale Rural Area 4 Commercial n/a n/a n/a n/a n/a Bickleton Rural and Surrounding Roosevelt and River Communities NE Goldendale Rural Bickleton Urban Model Specification Klickitat County uses a "mass appraisal" process to appraise the more than 19,000 real properties each year. "Mass appraisal" is the processes of valuing large numbers of properties as of a given date, using standard methods, employing common data and allowing for statistical testing. Standard procedures are used to collect property data, analyze data, apply the results of the analysis and report the results. Klickitat County uses a Sales Adjusted Cost Approach to assessment value where the base model is specified by using a Computer Aided Mass Appraisal System called ProVal which is owned by the parent company Thompson and Reuter. The ProVal cost model is a derivative of the Marshall & Swift valuation service cost approach. This approach is often referred by ProVal as a Market Calibrated Stratified Cost Approach. This computer program applies market derived land

12 rates by neighborhood and property type. Computer programs apply building costs and depreciation factors calibrated to local market conditions using sales data, by neighborhood, building style, grade of construction, and building condition. This approach uses both the cost approach to value and the comparable sales approach to value. The income approach is not applicable to the appraisal of land, single family residences or manufactured homes and therefore the income approach was not considered in determining assessed value. The income approach is applicable in the use of commercial real property valuation. Data Requirements The data management system is the heart of the mass appraisal system. Property characteristics data are used in the analysis and valuation system to conduct research and to generate values. Some property characteristics that IAAO considers factors that influence the valuation of land were not in the current property records store in the ProVal system. Major factors that influence the valuation of land are location, soil and subsoil conditions, climate, utilities, size, shape, topography, appearance, proximity to supporting facilities, drainage and in Klickitat County views. Our staff has spent a considerable amount of time adding in the size, topography and view codes for parcels. We discovered over 3,500 parcels without any size data in their property records. It appears that the prior administration lumped parcels into size ranges and gave them lump sum values based on appraiser knowledge. We have improved this method of valuation by entering the size for the majority of parcels and letting the sales of other parcels set the values of parcels in the Proval System giving consideration to size. We intend to continue to work toward fully recording and verifying all the characteristics in our database that influence value as the time constraints set by statute and the limited work force and financial resources available allow. The appraisal staff relies on a number of tools to collect and verify property characteristics including: Physical Inspection of Properties Maps including but not limited to: o Aerials o Topographic Maps, o Wetland and Stream Maps o Easement Maps o Utility Maps o Zoning Maps o Comprehensive Plan Maps o UGA Maps o Any map that conveys property characteristic data Blueprints Multiple Listing Service Real Estate Flyers & Brochures Real Estate Web Sites NADA Mobile Home Values Property characteristics data is maintained annually from the various maps, through sales review and property re-inspections per the approved revaluation plan. Property characteristics may also be verified and updated in the course of re-inspection of a property in the course of perfecting the Assessor's answer to an appeal or in response to a value review initiated by a taxpayer.

13 Data is captured in ProVal. Sales review notes are contained in the analysis spreadsheets and in the Assessor's Property System Database ProVal. Model Chosen Sales Adjusted Cost Approach for all residential properties Cost Approach for outbuildings and miscellaneous structures. Value Model Calibration Model calibration is conducted using ratio studies. The standards applied are those published by the IAAO, July The level of appraisal is set by RCW. In 2011, preliminary initial ratio studies indicated a need to recalibrate the valuation model(s). The following steps were employed: 1. Recalibration of the base Single Family Residential improvement model 2. Update of the land value model / land tables 3. Recalibration of the whole property value model. Land When sufficient land sales exist, the land calibration is based wholly on land sales. When there are insufficient land sales, land values are abstracted from improved property sales. Land sales were inspected and their property characteristics verified. The sales were entered on a spreadsheet and stratified by land type, size and other property characteristics. A preliminary land table was developed and ratio study performed to determine how effective the land model is in predicting the sales prices. The number and type of land sales available were insufficient to construct the entire land model so a combination of land sales and residuals were used. Single Family Residences, Manufactured Homes Initial ratio analysis indicated the need to recalibrate the base Single Family Residential value model. The initial calibration of the base single family residential model was based upon the sales of homes. The cost model was adjusted until the ratio studies produced acceptable performance statistics for both level of appraisal (ratio) and uniformity (see tables later in this document). Base cost model adjustments include adjusting the base rate cost tables and setting the base house type model. The performance of the base cost model was evaluated on a neighborhood by neighborhood basis; house type by house type; and by year built and specific location and the base cost model refined until it produces acceptable performance statistics. Refinements to the base cost model were made using house type factor models (applied universally by neighborhood by house style), the application of improvement modifiers (AKA Market Modifiers or Relative Desirability Factors (RDF)), lump sum or percentage land factors and modifications to depreciation tables. Refer to the model performance summary analysis tables for details.

14 RCW The term real property shall also include a mobile home which has substantially lost its identity as a mobile unit by virtue of its being permanently fixed in location upon land owned or leased by the owner of the mobile home and placed on a permanent foundation (posts or blocks) with fixed pipe connections with sewer, water, or other utilities: PROVIDED, That a mobile home located on land leased by the owner of the mobile home shall be subject to the personal property provisions of chapter RCW and RCW Manufactured Homes In Parks and on Leased Land The value of manufactured homes in parks and on leased land may be significantly different than the value of manufactured homes on land owned by the owner. The manufactured home on leased land does not have the ability to be sold as a package unit. This limits the marketability of the manufactured home and does not allow for the application of improvement modifiers that may increase the value of the mobile home based on desirability of location. In addition, they do not meet the requirements of RCW to qualify as real property (the treasurer does not have the ability to charge personal property taxes against the real property they are located on). These mobile homes are not exempt from personal property taxation. The Assessor s office has used the Sales Adjusted Cost Approach for Manufactured Homes in parks and on leased land to determine their market value. Initial ratio analysis indicated the need to recalibrate the Manufactured Home value model. The analysis was performed county wide and the final model was applied to all manufactured homes located in parks and on leased land. Final Testing and Reconciliation: Final value determinations were based on a careful analysis of the quantity and quality of data available to each estimation approach as well as validation through the performance statistics produced at the conclusion of each of the approaches used and the final testing validation. The Post Revaluation Ratio Study results all show that the changes made meet all of the standards set by the IAAO. Public Disclosure: Disclosure to the taxpaying public of values of individual properties should be administered through normal jurisdictional processes. The value in this report may change as a result of processes following that disclosure. Certification of Appraisal The appraisers are accredited by the State of Washington, Department of Revenue. By signing this report, the Appraiser certifies that he or she has the appropriate knowledge and experience to complete this Assessor's Report of the Mass Appraisal, with professional assistance if required and disclosed. To the best of the Appraisers knowledge and belief, all statements and information in this report are true and correct, and the Appraiser has not knowingly withheld any significant information The reported analyses, opinions and conclusions are limited only by the reported assumptions and limiting conditions, and is the appraisers personal, impartial and unbiased professional analysis, opinions and conclusions.

15 The appraisers have no bias with respect to any property that is the subject of this report or to the parties involved with this assignment. The appraisers engagement in this assignment was not contingent upon developing or reporting predetermined results. The appraisers compensation for completing this assignment is not contingent upon the reporting of a predetermined value or direction in value that favors the cause of the client, the amount of the value opinion, the attainment of a stipulated result, or the occurrence of a subsequent event directly related to the intended use of this appraisal. The appraisers analyses, opinions, and conclusions were developed and this report has been prepared, in conformity with the Uniform Standards of Professional Appraisal Practice (USPAP). Inspections were performed by members of the Klickitat County Assessor's Office in accordance with the revaluation plan approved by the Washington State Department of Revenue, November 5, Assessor's Office mass appraisal is a team effort. Significant participants and tasks are listed below: Property Inspections and Data Collection Karen Reisenauer, Supervisor Assessor Adam DeHart, Appraiser Dan McCabe, Appraiser Darlene Johnson, Assessor Model Specification: Thompson Reuter ProVal implementation of Marshall & Swift cost approach. ProVal is a licensed re-distributor of the Marshall & Swift cost data. Klickitat County is a licensed user of the Marshall & Swift cost data. Model Calibration / Analysis and Statistics: Karen Reisenauer, Supervisor Assessor Darlene Johnson, Assessor Signature: Date:

16 Appendix Mass Appraisal Reports Sales: Sales meeting the following criteria are included in the ratio analysis: Sales within the Date Range of:...01/01/ /31/2010 (Although not required, when available we considered sales up to 3/30/2011 to improve number and quality of sales) Sales Qualification Code:...V (valid sale) 'Short Sales' and 'REO Sales' which meet the DOR ration study standards are included as 'Q' sales. Auction sales are not. In a letter dated June 30, 2009, the Department of Revenue instructed the Klickitat County Assessor to assume Short Sales and Bank Sales were qualified sales, unless the appraiser could determine they were invalid due to another reason, i.e. Family Sale, Divorce, etc. Based on Washington State Department of Revenue Ratio Procedures Manual April 1997, the following sales were excluded from the ratio analysis: Outliers - Sales ratios (certified value divided by sales price) below 0.25 or greater than Sales that are less than $1,000. Sales with a DOR ratio study invalid code (any sales whose qualification code is not 'V'). Sales that are not transferred by either a Warranty Deed or Real Estate Contract, with the exception of manufactured homes where the deed type is generally other than a Warranty Deed. Additional sales excluded: Sales involving multiple parcels Sales where the prior year's appraised value did not include an improvement value by the sales price included improvements i.e. new construction that has not yet been appraised for the current assessment year. Sales where the improvements were appraised at less than 100% as of July 31st of the prior assessment year but the sales price was for a 100% complete home. A sale that included an appraised improvement value and the improvement was subsequently torn down or moved and the current appraised value does not include any improvement value. A sale on a parcel that did not exist for the prior assessment year but exists for the current assessment year (new plats, short plats, condominiums, etc). These parcels are excluded from the ratio report as their inclusion would distort the before and after ratio. Sales, which meet the DOR ratio study standard, but which investigation reveals to be nonmarket transactions. These sales are denoted as such in the appraisal spreadsheets and in the ProVal database sales file, field 'transaction type' as 'NM' (not market).

17 Definitions Mass Appraisal Report From Property Assessment Valuation, International Association of Assessing Officers, Measures of Appraisal Level Definitions for Ratio Study Terms Median Ratio- the median is the midpoint, or middle ratio, when the ratios are arrayed in order of magnitude. The median divides the ratios into two equal groups; therefore extreme ratios have little effect. IAAO standard is 0.90 to Arithmetic Mean- the mean is the average ratio. It is found by summing the ratios and then dividing by the number of ratios. When the sample has been properly obtained and the data have been carefully screened and processed, the mean provides a valid measure of appraisal level. IAAO standard is 0.90 to Weighted Mean-the weighted mean is an aggregate ratio determined by summing the appraised values for the entire sample, summing the sales prices for the entire sample and divided the total of the appraised values by the total of the sales prices. It is a measure of central tendency. IAAO standard is 0.90 to Geometric Mean- a measure of central tendency computed by multiplying the values of all of the observations by one another and then taking the result to an exponent equal to one divided by the number of observations. The geometric mean is particularly appropriate when typical rate of change is being calculated such as an inflation rate or a cost index. Coefficient of Dispersion (COD)-is the most used measure of uniformity ratio studies. The COD is based on average absolute deviations but expresses it as a percentage. Thus the COD provides a measure of appraisal uniformity independent of the level of appraisal and permits direction comparisons among property groups. IAAO standard for Older, Heterogeneous Areas is 15.0 or less, Rural Residential and Seasonal is 20.0 or less. Standard Deviation is a measure of dispersion. It is computed by subtracting the mean from each ratio, squaring the resulting differences, summing the squared differences, dividing by the number of ratios less 1 to obtain the variance of ratios, and computer the square root to obtain the standard deviation. Coefficient of Variation (COV) expresses the standard deviation as a percentage making comparison of appraisal levels between groups easier. Priced Related Differential (PRD) is a statistics for measuring assessment regressivity or progressivity. Appraisals are considered regressive if high-value properties are under-appraised relative to low-value property and progressive if high-value property are relatively over-appraised. It is calculated by dividing the mean by the weighted mean. A PRD greater than 1.00 suggests that high-value parcels are under-appraised, thus pulling the weighted mean below the mean. On the other, if PRD is less than 1.00, high-value parcels are relatively over appraised, pulling the weighted mean above the mean.

18 Confidence Level is the required degree of confidence in a statistical test or confidence interval; commonly, 90, 95 or 99 percent. A 95 percent confidence interval would mean, for example, that one can be 95 percent confident that the population measure (such as the median or mean appraisal ratio) falls in the indicated range. Computer Aided Mass Appraisal (CAMA)- is a system of appraiser property, usually only certain types of real property, that incorporates computer-supported statistical analysis such as multiple regression analysis and adaptive estimation procedure to assist the appraiser in estimating value. International Association of Assessing Officers (IAAO) is an international leader in the mass appraisal and ad valorem taxation community. Its members have been valuing property of all types for more than 75 years by using proven valuation techniques that are taught and endorsed by IAAO. Klickitat County Neighborhoods A neighborhood comprises complementary land uses in which all properties are similarly influence by the factors affecting property value. We anticipate a significant change in the boundaries of neighborhoods in the next few years as we work to improve the boundaries of neighborhoods for the purpose of analysis. Larger neighborhoods will improve the number of sales used for analysis and improve the quality of analysis. Neighborhood Description Parcels White Salmon Area 1 Commercial Bingen Rural White Salmon, Snowden Husum to BZ Corner BZ Corner to Troutlake Area 2 Commercial Government Area 2 Commercial Lyle Residential Lyle Residential II Dallesport Murdock Appleton, Klickitat, Wahkiacus Glenwood and surrounding range Glenwood Klickitat Residential Area 3 Commercial Area 3 Wind Towers Centerville and surrounding Goldendale Residential Goldendale Residential II Wishram and River Communities N NW Goldendale Rural Area 4 Commercial NE Goldendale Rural Bickleton and surrounding Roosevelt and River Area 4 Wind Towers Bickleton Urban 108

19

20 Klickitat County House Types House Type Number Description Detailed Description 11 Small Bungalow 0 Bsmt Pre 1940's homes 12 Bungalow Bsmt without a basement 13 Bungalow Bsmt 14 Bungalow Bsmt 15 Bungalow Bsmt 16 Large Bungalow Bsmt 17 Small Bungalow Pre 1940's homes 18 Bungalow with a basement 19 Bungalow Bungalow Bungalow Large Bungalow Small Vintage Multi Story 0 Bsmt Pre 1940's multi- 24 Vintage Multi Story Bsmt story homes without 25 Vintage Multi Story Bsmt a basement 26 Vintage Multi Story Bsmt 27 Vintage Multi Story Bsmt 28 Large Vintage Multi Story Bsmt 29 Small Vintage Multi Story Pre 1940's multi- 30 Vintage Multi Story story homes with 31 Vintage Multi Story a basement 32 Vintage Multi Story Vintage Multi Story Vintage Multi Story Large Historic Grand 0 Bsmt High End Vintage 36 Large Historic Grand pre-1940's 36 Cabin 38 Pole Building with Living 39 Contemporary Architectural Custom Home 40 A-Frame 41 Small Square Foot Ranch 0 Bsmt Ranch new 42 Ranch Bsmt without a basement 43 Ranch Bsmt 44 Ranch Bsmt 45 Ranch Bsmt 46 Large Ranch Bsmt 47 Small Square Foot Ranch w/bsmt Ranch new 48 Ranch with a basement 49 Ranch Ranch Ranch Large Ranch 2300+

RAINS COUNTY APPRAISAL DISTRICT

RAINS COUNTY APPRAISAL DISTRICT 2017 MASS APPRAISAL SUMMARY REPORT mass appraisal report 2017 uspap_appr_report RAINS COUNTY APPRAISAL DISTRICT 2017 MASS APPRAISAL SUMMARY REPORT Identification of Subject:

RAINS COUNTY APPRAISAL DISTRICT 2017 MASS APPRAISAL SUMMARY REPORT mass appraisal report 2017 uspap_appr_report RAINS COUNTY APPRAISAL DISTRICT 2017 MASS APPRAISAL SUMMARY REPORT Identification of Subject:

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence OVERVIEW OF RESIDENTIAL APPRAISAL PROCESS And Cost Valuation Report Introduction The

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence OVERVIEW OF RESIDENTIAL APPRAISAL PROCESS And Cost Valuation Report Introduction The

DIRECTIVE # This Directive Supersedes Directive # and #92-003

Division Of Property Valuation Docking State Office Building 915 SW Harrison St., Room 400N Topeka, KS 66612-1588 Nick Jordan, Secretary David N. Harper, Director phone: 785-296-2365 fax: 785-296-2320

Division Of Property Valuation Docking State Office Building 915 SW Harrison St., Room 400N Topeka, KS 66612-1588 Nick Jordan, Secretary David N. Harper, Director phone: 785-296-2365 fax: 785-296-2320

2011 ASSESSMENT RATIO REPORT

2011 Ratio Report SECTION I OVERVIEW 2011 ASSESSMENT RATIO REPORT The Department of Assessments and Taxation appraises real property for the purposes of property taxation. Properties are valued using

2011 Ratio Report SECTION I OVERVIEW 2011 ASSESSMENT RATIO REPORT The Department of Assessments and Taxation appraises real property for the purposes of property taxation. Properties are valued using

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence OVERVIEW OF RESIDENTIAL APPRAISAL PROCESS And Cost Valuation Report Introduction The

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence OVERVIEW OF RESIDENTIAL APPRAISAL PROCESS And Cost Valuation Report Introduction The

Residential Revaluation Report

Residential Revaluation Report 2013 Mass Appraisal of Mobile Homes In Courts for 2014 Property Taxes Prepared For Steven J. Drew Thurston County Assessor TABLE of CONTENTS page. CERTIFICATE OF APPRAISAL...

Residential Revaluation Report 2013 Mass Appraisal of Mobile Homes In Courts for 2014 Property Taxes Prepared For Steven J. Drew Thurston County Assessor TABLE of CONTENTS page. CERTIFICATE OF APPRAISAL...

LLANO CENTRAL APPRAISAL DISTRICT REAPPRAISAL PLAN FOR TAX YEARS 2017 & 2018 AS ADOPTED BY THE BOARD OF DIRECTORS

LLANO CENTRAL APPRAISAL DISTRICT REAPPRAISAL PLAN FOR TAX YEARS 2017 & 2018 AS ADOPTED BY THE BOARD OF DIRECTORS TABLE OF CONTENTS ITEM PAGE Executive Summary 5 Revaluation Decision (Statutory or Administrative)

LLANO CENTRAL APPRAISAL DISTRICT REAPPRAISAL PLAN FOR TAX YEARS 2017 & 2018 AS ADOPTED BY THE BOARD OF DIRECTORS TABLE OF CONTENTS ITEM PAGE Executive Summary 5 Revaluation Decision (Statutory or Administrative)

The Honorable Larry Hogan And The General Assembly of Maryland

2015 Ratio Report The Honorable Larry Hogan And The General Assembly of Maryland As required by Section 2-202 of the Tax-Property Article of the Annotated Code of Maryland, I am pleased to submit the Department

2015 Ratio Report The Honorable Larry Hogan And The General Assembly of Maryland As required by Section 2-202 of the Tax-Property Article of the Annotated Code of Maryland, I am pleased to submit the Department

April 12, The Honorable Martin O Malley And The General Assembly of Maryland

April 12, 2011 The Honorable Martin O Malley And The General Assembly of Maryland As required by Section 2-202 of the Tax-Property Article of the Annotated Code of Maryland, I am pleased to submit the

April 12, 2011 The Honorable Martin O Malley And The General Assembly of Maryland As required by Section 2-202 of the Tax-Property Article of the Annotated Code of Maryland, I am pleased to submit the

Residential Revaluation Report

Residential Revaluation Report 2012 Mass Appraisal of Region 5 for 2013 Property Taxes Prepared For Steven J. Drew Thurston County Assessor TABLE OF CONTENTS Page No. CERTIFICATE OF APPRAISAL... 3 APPRAISAL

Residential Revaluation Report 2012 Mass Appraisal of Region 5 for 2013 Property Taxes Prepared For Steven J. Drew Thurston County Assessor TABLE OF CONTENTS Page No. CERTIFICATE OF APPRAISAL... 3 APPRAISAL

GENERAL ASSESSMENT DEFINITIONS

21st Century Appraisals, Inc. GENERAL ASSESSMENT DEFINITIONS Ad Valorem tax. A tax levied in proportion to the value of the thing(s) being taxed. Exclusive of exemptions, use-value assessment laws, and

21st Century Appraisals, Inc. GENERAL ASSESSMENT DEFINITIONS Ad Valorem tax. A tax levied in proportion to the value of the thing(s) being taxed. Exclusive of exemptions, use-value assessment laws, and

Past & Present Adjustments & Parcel Count Section... 13

Assessment 2017 Report This report includes specific information regarding the 2017 assessment as well as general information about both the appeals and assessment processes. Contents Introduction... 3

Assessment 2017 Report This report includes specific information regarding the 2017 assessment as well as general information about both the appeals and assessment processes. Contents Introduction... 3

Introduction. Bruce Munneke, S.A.M.A. Washington County Assessor. 3 P a g e

Assessment 2016 Report This report includes specific information regarding the 2016 assessment as well as general information about both the appeals and assessment processes. Contents Introduction... 3

Assessment 2016 Report This report includes specific information regarding the 2016 assessment as well as general information about both the appeals and assessment processes. Contents Introduction... 3

Table of Contents 2015 Commercial Revaluation Report

Table of Contents 05 Commercial Revaluation Report 05 Commercial & Industrial Valuation Summary Introduction Uniform Standards Approaches to Value Land Valuation Land to Building Ratios Parking to Building

Table of Contents 05 Commercial Revaluation Report 05 Commercial & Industrial Valuation Summary Introduction Uniform Standards Approaches to Value Land Valuation Land to Building Ratios Parking to Building

How to Read a Real Estate Appraisal Report

How to Read a Real Estate Appraisal Report Much of the private, corporate and public wealth of the world consists of real estate. The magnitude of this fundamental resource creates a need for informed

How to Read a Real Estate Appraisal Report Much of the private, corporate and public wealth of the world consists of real estate. The magnitude of this fundamental resource creates a need for informed

Swisher County Appraisal District 2017 Mass Appraisal Report

Swisher County Appraisal District 2017 Mass Appraisal Report Prepared Pursuant to Standard 6 of the Uniform Standards of Professional Appraisal Practice 1 TABLE OF CONTENTS Introduction 3 Listing of Taxing

Swisher County Appraisal District 2017 Mass Appraisal Report Prepared Pursuant to Standard 6 of the Uniform Standards of Professional Appraisal Practice 1 TABLE OF CONTENTS Introduction 3 Listing of Taxing

WALLER COUNTY APPRAISAL DISTRICT MASS APPRAISAL REPORT APPRAISAL YEAR 2018

WALLER COUNTY APPRAISAL DISTRICT MASS APPRAISAL REPORT APPRAISAL YEAR 2018 ADDENDUM TO WCAD REAPPRAISAL PLAN FOR 2017 AND 2018 WALLER COUNTY APPRAISAL DISTRICT Uniform Standards of Professional Appraisal

WALLER COUNTY APPRAISAL DISTRICT MASS APPRAISAL REPORT APPRAISAL YEAR 2018 ADDENDUM TO WCAD REAPPRAISAL PLAN FOR 2017 AND 2018 WALLER COUNTY APPRAISAL DISTRICT Uniform Standards of Professional Appraisal

Anatomy Of An Appraisal

Anatomy Of An Appraisal Leslie A. Fields The most important thing to know about an appraisal report is how to review and critique it. Leslie A. Fields a partner with the Law Firm of Faegre & Benson LLP,

Anatomy Of An Appraisal Leslie A. Fields The most important thing to know about an appraisal report is how to review and critique it. Leslie A. Fields a partner with the Law Firm of Faegre & Benson LLP,

A Demonstration Appraisal Report. Of a. Located at. Date of Appraisal. Prepared for. Prepared by

A Demonstration Appraisal Report Of a Located at Date of Appraisal Prepared for Prepared by International Association of Assessing Officers Professional Designation Subcommittee 314 West 10 th Street Kansas

A Demonstration Appraisal Report Of a Located at Date of Appraisal Prepared for Prepared by International Association of Assessing Officers Professional Designation Subcommittee 314 West 10 th Street Kansas

Rockwall CAD. Basics of. Appraising Property. For. Property Taxation

Rockwall CAD Basics of Appraising Property For Property Taxation ROCKWALL CENTRAL APPRAISAL DISTRICT 841 Justin Rd. Rockwall, Texas 75087 972-771-2034 Fax 972-771-6871 Introduction Rockwall Central Appraisal

Rockwall CAD Basics of Appraising Property For Property Taxation ROCKWALL CENTRAL APPRAISAL DISTRICT 841 Justin Rd. Rockwall, Texas 75087 972-771-2034 Fax 972-771-6871 Introduction Rockwall Central Appraisal

A Demonstration Appraisal Report. Of a. Located at. Date of Appraisal. Prepared for. Prepared by

A Demonstration Appraisal Report Of a Located at Date of Appraisal Prepared for Prepared by International Association of Assessing Officers Professional Designation Subcommittee 314 W. 10 th Street Kansas

A Demonstration Appraisal Report Of a Located at Date of Appraisal Prepared for Prepared by International Association of Assessing Officers Professional Designation Subcommittee 314 W. 10 th Street Kansas

RESTRICTED APPRAISAL REPORT

Restricted Use Appraisal Report Thomas J. Schulte & Associates Page #1 RESTRICTED APPRAISAL REPORT SUBJECT ASSIGNMENT Property City: Zip Code: County: Legal Description: Assessor's Parcel #: Tax Year:

Restricted Use Appraisal Report Thomas J. Schulte & Associates Page #1 RESTRICTED APPRAISAL REPORT SUBJECT ASSIGNMENT Property City: Zip Code: County: Legal Description: Assessor's Parcel #: Tax Year:

Table of Contents 2013 Commercial Revaluation Report

Table of Contents Commercial Revaluation Report 1. Commercial & Industrial Valuation Summary Introduction Uniform Standards Approaches to Value Land Valuation Land to Building Ratios Parking to Building

Table of Contents Commercial Revaluation Report 1. Commercial & Industrial Valuation Summary Introduction Uniform Standards Approaches to Value Land Valuation Land to Building Ratios Parking to Building

Table of Contents 2017 Commercial Revaluation Report

Table of Contents 07 Commercial Revaluation Report 07 Commercial & Industrial Valuation Summary Introduction Uniform Standards Approaches to Value Land Valuation Land to Building Ratios Parking to Building

Table of Contents 07 Commercial Revaluation Report 07 Commercial & Industrial Valuation Summary Introduction Uniform Standards Approaches to Value Land Valuation Land to Building Ratios Parking to Building

City of Nashua, NH 2018 Revaluation Informational Meeting

City of Nashua, NH 2018 Revaluation Informational Meeting Legal Requirements Constitutional Duty of the City: [Art.] 6. [Valuation and Taxation.] The public charges of government, or any part thereof,

City of Nashua, NH 2018 Revaluation Informational Meeting Legal Requirements Constitutional Duty of the City: [Art.] 6. [Valuation and Taxation.] The public charges of government, or any part thereof,

Assessment Year 2016 Assessment Valuations / Mass Appraisal Summary Report

Assessment Year 2016 Assessment Valuations / Mass Appraisal Summary Report Overview Following up on last year s work, additional work was done cleaning up the sales data. The land valuation model was further

Assessment Year 2016 Assessment Valuations / Mass Appraisal Summary Report Overview Following up on last year s work, additional work was done cleaning up the sales data. The land valuation model was further

Appraisal Stream Restricted Use Residential Appraisal Report

Appraisal Stream Restricted Use Residential Appraisal Report File No. 769kemplin This report is limited to the sole and exclusive use of the client. The appraiser's opinions and conclusions set forth in

Appraisal Stream Restricted Use Residential Appraisal Report File No. 769kemplin This report is limited to the sole and exclusive use of the client. The appraiser's opinions and conclusions set forth in

Midland Central Appraisal District BIENNIAL REAPPRAISAL PLAN

BIENNIAL REAPPRAISAL PLAN FOR THE TAX YEARS 2015 AND 2016 BY THE MIDLAND CENTRAL APPRAISAL DISTRICT BOARD OF DIRECTORS September 10, 2014 TABLE OF CONTENTS ITEM PAGE Executive Summary... 4 General Overview

BIENNIAL REAPPRAISAL PLAN FOR THE TAX YEARS 2015 AND 2016 BY THE MIDLAND CENTRAL APPRAISAL DISTRICT BOARD OF DIRECTORS September 10, 2014 TABLE OF CONTENTS ITEM PAGE Executive Summary... 4 General Overview

RevuPro Appraisal Review

RevuPro Appraisal Review Getting It Right ELLIOTT introduces its flagship review product RevuPro, as an independent appraisal review service. Q. What is it and what does it do? A. RevuPro is a fast, economical

RevuPro Appraisal Review Getting It Right ELLIOTT introduces its flagship review product RevuPro, as an independent appraisal review service. Q. What is it and what does it do? A. RevuPro is a fast, economical

YOUNG COUNTY APPRAISAL DISTRICT

YOUNG COUNTY APPRAISAL DISTRICT 2017 - ANNUAL APPRAISAL REPORT AS OF 10/6/2017 1 2 TABLE OF CONTENTS ITEM PAGE Introduction 4 Purpose of Report...4 Taxing Entities, Rates & Exemptions 5 Property Types

YOUNG COUNTY APPRAISAL DISTRICT 2017 - ANNUAL APPRAISAL REPORT AS OF 10/6/2017 1 2 TABLE OF CONTENTS ITEM PAGE Introduction 4 Purpose of Report...4 Taxing Entities, Rates & Exemptions 5 Property Types

Table of Contents. Chapter 1: Introduction (Mobile Technology Evolution) 1

1") Chapter 1: Introduction (Mobile Technology Evolution) 1 I. WHY APPRAISAL IS IMPORTANT (p. 3) II. DEFINITION OF APPRAISAL (p. 4) A. Opinion (p. 4) B. Value (p. 5) C. Appraisal Art or Science? (p. 5) D.

Chapter 1: Introduction (Mobile Technology Evolution) 1 I. WHY APPRAISAL IS IMPORTANT (p. 3) II. DEFINITION OF APPRAISAL (p. 4) A. Opinion (p. 4) B. Value (p. 5) C. Appraisal Art or Science? (p. 5) D.

MAAO Sales Ratio Committee 2013 Fall Conference Seminar

MAAO Sales Ratio Committee 2013 Fall Conference Seminar Presented By: Al Whitcomb Dakota County (Retired) John Keefe Chisago County Assessor Brent Reid City of Coon Rapids Michael Thompson Scott County

MAAO Sales Ratio Committee 2013 Fall Conference Seminar Presented By: Al Whitcomb Dakota County (Retired) John Keefe Chisago County Assessor Brent Reid City of Coon Rapids Michael Thompson Scott County

To all Appraisers: Brief Overview:

To all Appraisers: As the appraisal industry continues to change, the demand for alternative valuation solutions grows. That is why is excited to announce the addition of a new product - the Desktop Appraisal

To all Appraisers: As the appraisal industry continues to change, the demand for alternative valuation solutions grows. That is why is excited to announce the addition of a new product - the Desktop Appraisal

YOUNG CENTRAL APPRAISAL DISTRICT

YOUNG CENTRAL APPRAISAL DISTRICT 2018 - MASS APPRAISAL REPORT AS OF 8/07/2018 1 2 2018 - MASS APPRAISAL REPORT INTRODUCTION: The Young Central Appraisal District has prepared and published this report

YOUNG CENTRAL APPRAISAL DISTRICT 2018 - MASS APPRAISAL REPORT AS OF 8/07/2018 1 2 2018 - MASS APPRAISAL REPORT INTRODUCTION: The Young Central Appraisal District has prepared and published this report

Residential Revaluation Report

Residential Revaluation Report 2010 Mass Appraisal of Region 8 for 2011 Property Taxes Prepared For Patricia Costello Thurston County Assessor TABLE OF CONTENTS Page No. CERTIFICATE OF APPRAISAL...3 APPRAISAL

Residential Revaluation Report 2010 Mass Appraisal of Region 8 for 2011 Property Taxes Prepared For Patricia Costello Thurston County Assessor TABLE OF CONTENTS Page No. CERTIFICATE OF APPRAISAL...3 APPRAISAL

ASSESSMENT METHODOLOGY

2019 ASSESSMENT METHODOLOGY COMMERCIAL RETAIL AND OFFICE CONDOMINIUMS A summary of the methods used by the City of Edmonton in determining the value of commercial retail and office condominium properties

2019 ASSESSMENT METHODOLOGY COMMERCIAL RETAIL AND OFFICE CONDOMINIUMS A summary of the methods used by the City of Edmonton in determining the value of commercial retail and office condominium properties

Dear Brazos County Citizens and Property Owners,

2017 Annual Report Dear Brazos County Citizens and Property Owners, It is my pleasure to present the 2017 Annual Report of the Brazos Central Appraisal District. The annual report provides general information

2017 Annual Report Dear Brazos County Citizens and Property Owners, It is my pleasure to present the 2017 Annual Report of the Brazos Central Appraisal District. The annual report provides general information

2. Is the information in the contract section complete and accurate? Yes No Not Applicable If Yes, provide a brief summary.

The purpose of this appraisal field review report is to provide the lender/client with an opinion on the accuracy of the appraisal report under review. Property Address City State Zip Code Borrower Owner

The purpose of this appraisal field review report is to provide the lender/client with an opinion on the accuracy of the appraisal report under review. Property Address City State Zip Code Borrower Owner

EvaluePro Real Estate Restricted Appraisal Report

EvaluePro Real Estate Restricted Appraisal Report EvaluePro Highlights Property Street: 1000 Main Street City: Anytown State: NC Zip: 12345 Property Owner: Mr. & Mrs. Property Owner Estimated Market Value:

EvaluePro Real Estate Restricted Appraisal Report EvaluePro Highlights Property Street: 1000 Main Street City: Anytown State: NC Zip: 12345 Property Owner: Mr. & Mrs. Property Owner Estimated Market Value:

Course Mass Appraisal Practices and Procedures

Course 331 - Mass Appraisal Practices and Procedures Course Description This course is designed to build on the subject matter covered in Course 300 Fundamentals of Mass Appraisal and prepare the student

Course 331 - Mass Appraisal Practices and Procedures Course Description This course is designed to build on the subject matter covered in Course 300 Fundamentals of Mass Appraisal and prepare the student

METHODOLOGY GUIDE VALUING LANDS IN TRANSITION IN ONTARIO. Valuation Date: January 1, 2016

METHODOLOGY GUIDE VALUING LANDS IN TRANSITION IN ONTARIO Valuation Date: January 1, 2016 August 2017 August 22, 2017 The Municipal Property Assessment Corporation (MPAC) is responsible for accurately assessing

METHODOLOGY GUIDE VALUING LANDS IN TRANSITION IN ONTARIO Valuation Date: January 1, 2016 August 2017 August 22, 2017 The Municipal Property Assessment Corporation (MPAC) is responsible for accurately assessing

GOVERNANCE OF ASSESSOR

GOVERNANCE OF ASSESSOR State of NH Constitution NH State Statutes (RSA) State Supreme Court Case Law NH Assessing Standard Board Rules NH Department of Revenue Rules Professional Code of Conduct (USPAP)

GOVERNANCE OF ASSESSOR State of NH Constitution NH State Statutes (RSA) State Supreme Court Case Law NH Assessing Standard Board Rules NH Department of Revenue Rules Professional Code of Conduct (USPAP)

City of Norwalk Revaluation Project

City of Norwalk 2018 Revaluation Project Presenter: Paul Miller Supervisor: Salim Serdah Appraisers: James Steiner, John Valente, Steve Beccio, Rich Nicolosi, and Gynt Grube. Why Revaluation? It s important

City of Norwalk 2018 Revaluation Project Presenter: Paul Miller Supervisor: Salim Serdah Appraisers: James Steiner, John Valente, Steve Beccio, Rich Nicolosi, and Gynt Grube. Why Revaluation? It s important

Residential and Commercial Revaluation Annual Report

Residential and Commercial Revaluation 2015 Annual Report MOUNT VERNON REVALUATION CYCLE 6 Skagit County Assessor s Office Mount Vernon, Washington Dear Property Owner: The Assessor s office staff has

Residential and Commercial Revaluation 2015 Annual Report MOUNT VERNON REVALUATION CYCLE 6 Skagit County Assessor s Office Mount Vernon, Washington Dear Property Owner: The Assessor s office staff has

procedures Basic Appraisal F i n a l Examination #2 2 nd edition

F i n a l Examination #2 A n s w e r Key Page 82 1. When determining effective gross income from potential gross income, an appraiser considers a. debt service. b. depreciation. c. fixed expenses. d. vacancy

F i n a l Examination #2 A n s w e r Key Page 82 1. When determining effective gross income from potential gross income, an appraiser considers a. debt service. b. depreciation. c. fixed expenses. d. vacancy

Washington Department of Revenue Property Tax Division. Valid Sales Study Kitsap County 2015 Sales for 2016 Ratio Year.

P. O. Box 47471 Olympia, WA 98504-7471. Washington Department of Revenue Property Tax Division Valid Sales Study Kitsap County 2015 Sales for 2016 Ratio Year Sales from May 1, 2014 through April 30, 2015

P. O. Box 47471 Olympia, WA 98504-7471. Washington Department of Revenue Property Tax Division Valid Sales Study Kitsap County 2015 Sales for 2016 Ratio Year Sales from May 1, 2014 through April 30, 2015

concepts and techniques

concepts and techniques S a m p l e Timed Outline Topic Area DAY 1 Reference(s) Learning Objective The student will learn Teaching Method Time Segment (Minutes) Chapter 1: Introduction to Sales Comparison

concepts and techniques S a m p l e Timed Outline Topic Area DAY 1 Reference(s) Learning Objective The student will learn Teaching Method Time Segment (Minutes) Chapter 1: Introduction to Sales Comparison

Tangible Personal Property Summation Valuation Procedures

Property Tax Valuation Insights Tangible Personal Property Summation Valuation Procedures Robert F. Reilly, CPA For ad valorem property taxation purposes, industrial and commercial taxpayer tangible personal

Property Tax Valuation Insights Tangible Personal Property Summation Valuation Procedures Robert F. Reilly, CPA For ad valorem property taxation purposes, industrial and commercial taxpayer tangible personal

COMAL APPRAISAL DISTRICT ANNUAL APPRAISAL REPORT

COMAL APPRAISAL DISTRICT 2017 ANNUAL APPRAISAL REPORT TABLE OF CONTENTS Introduction..2 Mission Statement... 2 Purpose of Report...2 Entities Served..2 Legislative Changes.3 Property Types.3 Appraisal

COMAL APPRAISAL DISTRICT 2017 ANNUAL APPRAISAL REPORT TABLE OF CONTENTS Introduction..2 Mission Statement... 2 Purpose of Report...2 Entities Served..2 Legislative Changes.3 Property Types.3 Appraisal

Board of Appeal and Equalization Handbook

Board of Appeal and Equalization Handbook This handbook was created to satisfy the training requirements of Minnesota Statutes, sections 274.014 and 274.135 Updated January 2018 Table of Contents Introduction...

Board of Appeal and Equalization Handbook This handbook was created to satisfy the training requirements of Minnesota Statutes, sections 274.014 and 274.135 Updated January 2018 Table of Contents Introduction...

COMAL APPRAISAL DISTRICT ANNUAL APPRAISAL REPORT

COMAL APPRAISAL DISTRICT 2016 ANNUAL APPRAISAL REPORT TABLE OF CONTENTS Introduction..2 Mission Statement... 2 Purpose of Report...2 Entities Served..2 Legislative Changes.3 Property Types.3 Appraisal

COMAL APPRAISAL DISTRICT 2016 ANNUAL APPRAISAL REPORT TABLE OF CONTENTS Introduction..2 Mission Statement... 2 Purpose of Report...2 Entities Served..2 Legislative Changes.3 Property Types.3 Appraisal

CITY OF OWATONNA ASSESSMENT REPORT. Steele County Assessor s Department. William G. Effertz, SAMA Steele County Assessor

2017 CITY OF OWATONNA ASSESSMENT REPORT Steele County Assessor s Department William G. Effertz, SAMA Steele County Assessor Tyler Diersen, AMA, Assistant County Assessor April 11, 2017 2017 Assessment

2017 CITY OF OWATONNA ASSESSMENT REPORT Steele County Assessor s Department William G. Effertz, SAMA Steele County Assessor Tyler Diersen, AMA, Assistant County Assessor April 11, 2017 2017 Assessment

ASSESSORS ANSWER FREQUENTLY ASKED QUESTIONS ABOUT REAL PROPERTY Assessors Office, 37 Main Street

A. THE ASSESSMENT PROCESS: ASSESSORS ANSWER FREQUENTLY ASKED QUESTIONS ABOUT REAL PROPERTY Assessors Office, 37 Main Street What is mass appraisal? Assessors must value all real and personal property in

A. THE ASSESSMENT PROCESS: ASSESSORS ANSWER FREQUENTLY ASKED QUESTIONS ABOUT REAL PROPERTY Assessors Office, 37 Main Street What is mass appraisal? Assessors must value all real and personal property in

Town of Fairfield 2015 Revaluation Informational Meeting

www.vgsi.com Town of Fairfield 2015 Revaluation Informational Meeting Fairfield Revaluation Cycle Ct. Law states revaluations take place every 5 years Fairfield s last Revaluation was in 2010 All property

www.vgsi.com Town of Fairfield 2015 Revaluation Informational Meeting Fairfield Revaluation Cycle Ct. Law states revaluations take place every 5 years Fairfield s last Revaluation was in 2010 All property

Equity from the Assessor s Perspective

Institute of Municipal Assessors 55th Annual Conference Equity from the Assessor s Perspective Andy Anstett Legislation & Policy Support Services MPAC June 7th, 2011 Key Aspects of Equity Test Defining

Institute of Municipal Assessors 55th Annual Conference Equity from the Assessor s Perspective Andy Anstett Legislation & Policy Support Services MPAC June 7th, 2011 Key Aspects of Equity Test Defining

ASSESSMENT METHODOLOGY

2018 ASSESSMENT METHODOLOGY COST APPROACH A summary of the methods used by the City of Edmonton in determining the value of residential and non-residential properties valued using the cost approach in

2018 ASSESSMENT METHODOLOGY COST APPROACH A summary of the methods used by the City of Edmonton in determining the value of residential and non-residential properties valued using the cost approach in

2016 MASS APPRAISAL REPORT

THROCKMORTON CENTRAL APPRAISAL DISTRICT 2016 MASS APPRAISAL REPORT WEBSITE HOMEPAGE http://www.throckmortoncad.org 2016 MASS APPRAISAL REPORT PG 1 ORGANIZATION http://www.throckmortoncad.org/organization

THROCKMORTON CENTRAL APPRAISAL DISTRICT 2016 MASS APPRAISAL REPORT WEBSITE HOMEPAGE http://www.throckmortoncad.org 2016 MASS APPRAISAL REPORT PG 1 ORGANIZATION http://www.throckmortoncad.org/organization

Tax Implications Of The Intellectual Property Valuation Process

Tax Implications Of The Intellectual Property Valuation Process Robert F. Reilly Robert F. Reilly is a managing director of Willamette Management Associates. He is a Certified Public Accountant, Accredited

Tax Implications Of The Intellectual Property Valuation Process Robert F. Reilly Robert F. Reilly is a managing director of Willamette Management Associates. He is a Certified Public Accountant, Accredited

Land, Agricultural Improvements, CAFO, Rural Residence, Farm

*--FSA Appraisal Guidelines Land, Agricultural Improvements, CAFO, Rural Residence, Farm The following information elements and content descriptions are provided as guidelines to assist lenders and appraisers

*--FSA Appraisal Guidelines Land, Agricultural Improvements, CAFO, Rural Residence, Farm The following information elements and content descriptions are provided as guidelines to assist lenders and appraisers

Fundamentals of Real Estate APPRAISAL. 10th Edition. William L. Ventolo, Jr. Martha R. Williams, JD

A Fundamentals of Real Estate APPRAISAL 10th Edition William L. Ventolo, Jr. Martha R. Williams, JD Dennis S. Tosh, PhD William B. Rayburn, PhD, MAI, CFA Consulting Editors Dearb rri Real Estate Education

A Fundamentals of Real Estate APPRAISAL 10th Edition William L. Ventolo, Jr. Martha R. Williams, JD Dennis S. Tosh, PhD William B. Rayburn, PhD, MAI, CFA Consulting Editors Dearb rri Real Estate Education

2016 Mass Appraisal Report Archer County Appraisal District

2016 Mass Appraisal Report Archer County Appraisal District Archer County Appraisal District 112 East Walnut St P.O. Box 1141 Archer City, Texas 76351 (940) 574-2172 Kimbra York, RPA,RTA Chief Appraiser

2016 Mass Appraisal Report Archer County Appraisal District Archer County Appraisal District 112 East Walnut St P.O. Box 1141 Archer City, Texas 76351 (940) 574-2172 Kimbra York, RPA,RTA Chief Appraiser

Individual Cooperative Interest Appraisal Report

PURPOSE Individual Cooperative Interest Appraisal Report The purpose of this appraisal report is to provide the client with a credible opinion of the defined value of the subject property, given the intended

PURPOSE Individual Cooperative Interest Appraisal Report The purpose of this appraisal report is to provide the client with a credible opinion of the defined value of the subject property, given the intended

Lee Central Appraisal District

Lee Central Appraisal District 2015 Mass Appraisal Report 1 INTRODUCTION Scope of Responsibility The Lee Central Appraisal District has prepared and published this report to provide citizens and taxpayers

Lee Central Appraisal District 2015 Mass Appraisal Report 1 INTRODUCTION Scope of Responsibility The Lee Central Appraisal District has prepared and published this report to provide citizens and taxpayers

Understanding Mississippi Property Taxes

Understanding Mississippi Property Taxes Property tax revenues are a vital component of the budgets of Mississippi s local governments. Property tax revenues allow these governments to provide important