Uniform Standards of Professional Appraisal Practice Business Valuation 7 Hour Course

|

|

|

- Rudolf Rodgers

- 6 years ago

- Views:

Transcription

1 Uniform Standards of Professional Appraisal Practice Business Valuation 7 Hour Course Carla G Glass, FASA Jay E Fishman, FASA

2 Introduction USPAP Introduction Definitions Preamble Rules Standards 9 and 10 Standard 3 Changes to Edition Summary Outline

3 Recognition We would like to thank the following individuals for their contribution in preparing this course Lisa Cruikshank, CMA, CFM, ASA Nicholas R. Mears Additionally, we will reference the website of The Appraisal Foundation which is

4 Learning Objectives Upon completion, the participant will be able to: Understand the purpose and flow of USPAP Have a working knowledge of the various definitions and how they interrelate Understand how the five Rules apply to your practice

5 Learning Objectives Upon completion, the participant will be able to (cont d): Apply Standards 9 and 10 for business and intangible asset appraisal Apply Standard 3 for appraisal review Be aware of the major differences in the other Standards Demonstrate an understanding of the changes made to the Edition of USPAP

6 USPAP Introduction

7 Purpose of USPAP Promote and maintain a high level of public trust in appraisal practice by establishing requirements for appraisers.

8 Why Need USPAP Savings & Loan Debacle (earlier RE crash) Appraisers believed deeply involved in causes of crash Needed to restore and maintain public trust Ongoing effect of valuations on economic conditions

9 Need for USPAP Providing credible appraisal services Service performed by ethical and competent individuals Professional services that create public trust

10 Need for USPAP Initially addressed by 9 North American appraisal professional organizations Ad Hoc committee created standards leading to USPAP Then 8 U.S. organizations formed The Appraisal Foundation

11 Need for USPAP Framework for comparison Reference source Reason for public trust Basis for enforcement

12 Legal Authority Financial Institution Reform Recovery & Enforcement Act (FIRREA) Established Appraisal Subcommittee (ASC) within Federal Financial Institutions Examination Council (FFIEC) Title XI of FIRREA Oversee The Appraisal Foundation Oversee State Boards (Real Property)

13 FFIEC Appraisal Subcommittee (ASC) ASC monitors the ASB, AQB, APB. Grants are made to the ASB and AQB per Title XI. State Appraisal Programs (55) The Appraisal Foundation (Board of Trustees) Appraisal Standards Board (ASB) Appraiser Qualifications Board (AQB) Appraisal Practices Board (APB) The Appraisal Foundation Advisory Council (TAFAC) Industry Advisory Council (IAC) International Valuation Council (IVC)

14 FFIEC The Council is a formal interagency body empowered to prescribe uniform principles, standards, and report forms for the federal examination of financial institutions by four regulatory agencies: Governors of the Federal Reserve System (FRB) Federal Deposit Insurance Corporation (FDIC) National Credit Union Administration (NCUA) Office of the Comptroller of the Currency (OCC)

15 Appraisal Subcommittee (ASC) In 1989, Title XI of FIRREA established the ASC within FFEIC. ASC has the authority from Title XI to monitor the activities of The Appraisal Foundation (TAF). This includes the activities of the ASB, AQB, & APB.

16 The Appraisal Foundation (TAF) A private non-profit corporation established in 1987 authorized by Congress (Title XI of FIRREA) with the responsibility of establishing, improving and promoting minimum uniform appraisal standards and appraiser qualification criteria [for real property]. Directed by a Board of Trustees. Appoints members and provides financial support to, and oversight of, the three independent boards of TAF

17 The Appraisal Foundation (TAF) Three Independent Boards: Appraiser Qualifications Board (AQB) Appraisal Standards Board (ASB) Appraisal Practices Board (APB)

18 AQB Establishes the qualification criteria for state licensing, certification and recertification of real property appraisers. FIRREA mandates that all state certified real property appraisers must meet minimum education, experience and examination criteria as promulgated by the AQB. Has voluntary criteria for personal property appraisers. Business valuators not currently addressed.

19 ASB sets forth the rules for developing an appraisal and reporting its results. ASB Develops and promotes the use of the Uniform Standards of Professional Appraisal Practice (USPAP). FIRREA requires real estate appraisals in conjunction with most federally-related transactions be in accordance with USPAP.

20 ASB Why/how USPAP changes ASB is a publicly-accountable board All proposed changes must be exposed to the public for comment Changes come about as the result of public comment Each member of the ASB reads each comment Best comments contain well-explained opinions with focus on public good No comment source takes priority over others focus is on rationale of comment

21 APB TAF s newest board having started in July Issues voluntary guidance on recognized methods and techniques. Not under the authority of the ASC and the guidance issued is strictly voluntary mostly RE. Has a standing SME group addressing valuation for financial reporting. One Valuation Advisory issued dealing with Contributory Asset Charges.

22 USPAP

23 USPAP 1. DEFINITIONS 2. PREAMBLE 3. RULES Ethics Record Keeping Competency Scope of Work Jurisdictional Exception 4. Standards Statements on Appraisal Standards page U-viii

24 Standards 1 and 2: Real Property Appraisal Standard 3: Appraisal Review Standards 4 and 5: RP Appraisal Consulting - Retired for Edition Standard 6: Mass Appraisal Standards 7 and 8: Personal Property Appraisal Standards 9 and 10: Business Valuation USPAP

25 USPAP Statements on Appraisal Standards are specifically for the purposes of clarification, interpretation, explanation, or elaboration of USPAP. Statements have the full weight of a Standards Rule and can be adopted by the ASB only after exposure and comment.

26 USPAP Comments: are an integral part of USPAP and have the same weight as the component they address. These extensions of the Definitions, Rules, and Standard Rules provide interpretation and establish the context and conditions for application. page U-1, line 16 for example

27 Other Communications Advisory Opinions: a form of guidance issued by the ASB to illustrate the applicability of USPAP in specific situations and to offer advice from the ASB for the resolution of appraisal issues and problems. They do not establish new standards or interpret existing standards. They are not part of USPAP. (see divider) Frequently Asked Questions: a form of guidance issued by the ASB to respond to questions raised by appraisers, enforcement officials, and other to illustrate the applicability of USPAP in specific situations and to offer advice from the ASB for the resolutions of appraisal issues. They are not part of USPAP. (see divider)

28 The Appraisal Process USPAP addresses the steps in the appraisal process. Divided into Development Reporting

29 The Appraisal Process Four Steps: Identify appraisal problem to be solved Determine the scope of work Perform research and analysis Report

30

31 Identify Appraisal Problem to be Solved (these are assignment elements): Client and other intended users Intended Use Type & Definition of Value (Standard & Premise) Effective Date Relevant characteristics of subject property Assignment conditions The Appraisal Process

32 Determine the Scope of Work: Which research & analysis to perform Dependent on prior identifications Especially Intended Users Intended Use Standard and Premise of value The Appraisal Process

33 The Appraisal Process Research Subject Market Analysis Approaches Methods Techniques/Procedures Reconciliation

34 Report: Written or oral If written Appraisal Report Restricted Appraisal Report The Appraisal Process

35 USPAP Definitions

36 Learning Objectives Upon completion, the participant will be able to: Have a working knowledge of the various definitions and how they interrelate

37 Overview: Definitions Terms with special definitions within USPAP, to be applied in the context of the USPAP document. May be different from their common usage. They are essential to understanding USPAP page U-1

38 Definitions Appraisal : (noun) the act or process of developing an opinion of value; an opinion of value. (adjective) of or pertaining to appraising and related function such as appraisal practice or appraisal review services Appraisal Review: the act or process of developing and communicating an opinion about the quality of another appraiser s work that was performed as part of an appraisal or appraisal review assignment

39 Definitions Assignment: 1) An agreement between an appraiser and a client to provide a valuation service 2) the valuation service that is provided as a consequence of such an agreement. Assignment Results: an appraiser s opinion or conclusions developed specific to an assignment.

40 Assumption: that which is taken to be true. Definitions Extraordinary Assumption: an assumption, directly related to a specific assignment, as of the effective date of the assignment results, which if found to be false, could alter the appraiser s opinions or conclusions. Hypothetical Condition: a condition, directly related to a specific assignment, which is contrary to what is known by the appraiser to exist on the effective date of the assignment results, but is used for the purpose of the analysis.

41 Definitions - Application Application: An appraiser is hired to do a valuation for divorce purposes. The client indicates that all of the income is not reported. A forensic accountant has provided a report that indicates that there is a shortfall of reported revenue of $300,000 per year. What type of assignment condition could the appraiser use?

42 Definitions Application Application: A client is constructing an office building and has a real property appraisal that indicates the as is value and the as fully occupied value. The client has asked you to perform two appraisals, each with a current effective date, but using the two different values in the two appraisals. What type of assignment condition would this indicate?

43 Definitions Client: the party or parties who engage by employment or contract an appraiser in a specific assignment. Intended User: the client and any other party as identified, by name or type, as users of the appraisal or appraisal review report by the appraiser on the basis of communication with the client at the time of the assignment.

44 Definitions Intended Use: the use or uses of an appraiser s reported appraisal or appraisal review assignment opinions and conclusions, as identified by the appraiser on the basis of communication with the client at the time of the assignment.

45 Definitions Credible: worthy of belief. Comment: Credible assignment results require support, by relevant evidence and logic, to the degree necessary for the intended use.

46 Definitions Confidential information: information that is either: identified by the client as confidential when providing it to an appraiser and that is not available from any other source; or classified as confidential or private by applicable law or regulation. Assignment results are not an example of confidential information, but instead must be treated as confidential (ETHICS RULE).

47 Definitions Appraiser: one who is expected to perform valuation services competently and in a manner that is independent, impartial, and objective. Appraiser s Peers: other appraisers who have expertise and competency in a similar type of assignment

48 Definitions Report: any communication, written or oral, of an appraisal or appraisal review that is transmitted to the client upon completion of the assignment. Scope of Work: the type and extent of research and analyses in an appraisal or appraisal review assignment.

49 Definitions Real Estate: an identified parcel or tract of land, including improvements, if any. Real Property: the interests, benefits, and rights inherent in the ownership of real estate. Personal Property: identifiable tangible objects that are considered by the general public as being personal for example, furnishings, artwork, antiques, gems and jewelry, collectibles, machinery and equipment; all tangible property that is not classified as real estate.

50 Business Enterprise: an entity pursuing an economic activity. Definitions Business Equity: the interests, benefits, and rights inherent in the ownership of a business enterprise or a part thereof in any form (including, but not necessarily limited to, capital stock, partnership interests, cooperatives, sole proprietorships, options, and warrants).

51 Definitions Intangible Property (Intangible Assets): nonphysical assets, including but not limited to franchises, trademarks, patents, copyrights, goodwill, equities, securities, and contracts as distinguished from physical assets such as facilities and equipment.

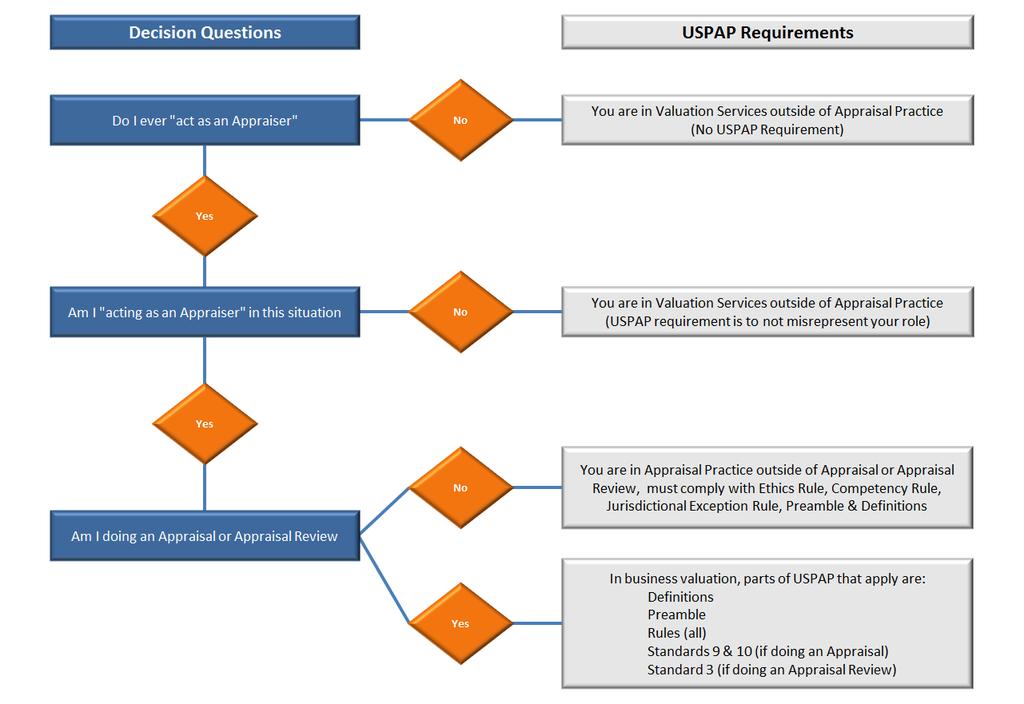

52 Preamble

53 Preamble The purpose of USPAP is to promote and maintain a high level of public trust in appraisal practice by establishing requirements for appraisers. Appraisers must develop and communicate their analyses, opinions, and conclusions to intended users in a manner that is meaningful and not misleading. page U-5

54 Preamble In order to comply with USPAP an appraiser must act competently and in a manner that is independent, impartial and objective. USPAP is for both appraisers and users of appraisal services. Appraiser s responsibility is to protect the overall public trust.

55 Preamble USPAP does not establish who or which assignments must comply. An appraiser must comply with USPAP when either the service or the appraiser is required by law, regulation, or agreement with a client or intended user.

56 USPAP American Society of Appraisers (ASA) The General Preamble to the American Society of Appraisers Business Valuation Standards indicates that: The American Society of Appraisers, in its Principles of Appraisal Practice and Code of Ethics, and The Appraisal Foundation, in its Uniform Standards of Professional Appraisal Practice (USPAP), have established authoritative principles and a code of professional ethics.

57 USPAP ASA Administrative Rule IV: Professional Standards and Ethics of the ASA s Administrative Rules, Section 1: Professional Standards and Ethics: states that the entire membership of the society individually and collectively shall observe USPAP as promulgated by the Appraisal Foundation, unless they practice in Canada or solely outside of North America.

58 USPAP ASA Section 8.6 Appraisers Responsibility to Communicate Each Analysis, Opinion and Conclusion in a Manner that is not Misleading of ASA s Principles of Appraisal Practice and Code of Ethics indicates that the appraiser should state in each report: I hereby certify that, to the best of my knowledge, the statements of fact contained in this report are true and correct, and this report has been prepared in conformity with the Uniform Standards of Professional Appraisal Practice of the Appraisal Foundation and the Principles of Appraisal Practice and Code of Ethics of the American Society of Appraisers

59 DEFINITIONS When Does USPAP Apply Valuation Service: services pertaining to aspects of property value. Comment: Valuation services pertain to all aspects of property value and include services performed by appraisers and others Appraisal Practice: valuation services performed by an individual acting as an appraiser, including but not limited to appraisal and appraisal review.

60 When Does USPAP Apply Appraisal : (noun) the act or process of developing an opinion of value; an opinion of value. (adjective) of or pertaining to appraising and related function such as appraisal practice or appraisal review services Appraisal Review: the act or process of developing and communicating an opinion about the quality of another appraiser s work that was performed as part of an appraisal or appraisal review assignment

61 When Does USPAP Apply Valuation Services are services pertaining to aspects of property value. Appraisal Practice is a subset of valuation services. Appraisal Practice is defined as valuation services provided by an appraiser. Only appraisers may offer services that are considered appraisal practice. Appraisal and Appraisal Review are subsets of Appraisal Practice.

62 When Does USPAP Apply

63 USPAP applies to all Appraisal Practice Appraisal and Appraisal Review Have Standards and Standards Rules that apply Also, all Rules apply Appraisal Practice outside of Appraisal and Appraisal Review Three Rules apply Ethics Competency Jurisdictional Exception When Does USPAP Apply

64 Appraisal Practice: When Does USPAP Apply Comment: Appraisal practice is provided only by appraisers, while valuation services are provided by a variety of professionals and others. The terms appraisal and appraisal review are intentionally generic and are not mutually exclusive. For example, an opinion of value may be required as part of an appraisal review assignment. The use of other nomenclature for an appraisal or appraisal review assignment (e.g., analysis, counseling, evaluation, study, submission, or valuation) does not exempt an appraiser from adherence to USPAP.

65 Appraisal Practice outside of Appraisal and Appraisal Review Appraiser acting as an appraiser One who is expected to perform valuation services competently and in a manner that is independent, impartial, and objective. Examples: Teaching an appraisal class When Does USPAP Apply Providing a service related to appraisal that does not provide any opinion of value such as collecting transaction data in an industry

66 An expectation that an individual is acting as an appraiser indicates an obligation to comply with USPAP in order to: Maintain public trust Adhere to the definition of Appraiser When Does USPAP Apply Meet expectations of client when working with someone considered to be an Appraiser

67 When Does USPAP Apply Valuation Service outside of Appraisal Practice Might be done by someone who sometimes works as an appraiser or someone who never does. Provided by person NOT acting as an appraiser in the particular project. When acting as an appraiser, cannot be advocate of client or client s position. When someone who sometimes acts as an appraiser performs an assignment requiring advocacy, that person must clarify that they are performing a Valuation Service outside of Appraisal Practice not acting as an appraiser

68 Valuation Service outside of Appraisal Practice Only one USPAP requirement when someone who sometimes acts as an appraiser performs Valuation Service outside of Appraisal Practice Must not misrepresent his/her role when providing valuation services that are outside of appraisal practice Examples: Litigation consulting as an advocate When Does USPAP Apply Attorney or CPA (who does not represent him/herself as an appraiser) providing a value opinion

69 When Does USPAP Apply Advisory Opinion 21 USPAP Compliance page A-64 (typo on page A-68)

70

71 When Does USPAP Apply - Application Application: I am retained by an attorney to provide suggestions regarding ways to challenge an opposing expert s report. In another situation, I am retained by an attorney to provide an appraisal of a business owned by a woman in the midst of divorce. What does USPAP say about these two situations?

72 The Rules

73 Learning Objectives Upon completion, the participant will be able to: Understand how the Five Rules apply to your practice Ethics Recordkeeping Competency Scope of Work Jurisdictional Exception

74 Ethics Rule applicable to Appraisal Practice Competency Rule applicable to Appraisal Practice Record Keeping Rule only applicable to Appraisal & Appraisal Review Scope of Work Rule only applicable to Appraisal & Appraisal Review Jurisdictional Exception Rule applicable to Appraisal Practice Rules

75 Rules Ethics Rule & Competency Rule Can be seen as two sides of overall requirements Competency Rule know what to do Ethics Rule do it Scope of Work Rule Standards can be seen as extension of this rule

76 Ethics Rule

77 Rules ETHICS RULE: An appraiser must promote and preserve the public trust inherent in appraisal practice by observing the highest standards of professional ethics. An appraiser must perform assignments with impartiality, objectivity, and independence, and without accommodation of personal interest. page U-7

78 Rules ETHICS RULE Conduct: Must not perform an assignment with bias; Must not advocate the cause or interest of any party or issue; Must not accept an assignment that includes predetermined opinions and conclusions; Must not misrepresent his/her role when providing valuation services that are outside of appraisal practice;

79 Rules ETHICS RULE Conduct: Must not communicate assignment results with the intent to be misleading or to defraud; Must not use or communicate a report that is known by the appraiser to be misleading and fraudulent; Must not knowingly permit an employee or other person to communicate a misleading or fraudulent report;

80 Rules ETHICS RULE Conduct: Must not use or rely on unsupported conclusions relating to race, color, religion, national origin, gender, marital status, familial status, age, receipt of public assistance income, handicap or an unsupported conclusion that the homogeneity of such characteristics is necessary to maximize value; Must not engage in criminal conduct; Must not violate the Record Keeping Rule; Must not perform an assignment in a grossly negligent manner.

81 ETHICS RULE Conduct: Rules If known prior to accepting an assignment, and/or if discovered any time during the assignment, an appraiser must disclose to the client, and in each subsequent report certification: Any current or prospective interest in the subject property or the parties involved; and Any services regarding the subject property performed by the appraiser within a three year period immediately preceding acceptance of the assignment as an appraiser or in any other capacity.

82 Rules - Application Application: I do lots of valuations for divorce cases and seem to generally have the business owner as a client. I usually reflect assumptions that derive a lower value than I otherwise would because I know the court is likely to split the difference and, therefore, end up with a reasonable conclusion. Is this in violation of USPAP?

83 ETHICS RULE Management: Rules An appraiser must disclose that he or she paid a fee or commission, or gave a thing of value in connection with the procurement of an assignment. Comment: The disclosure must appear in the certification and in any transmittal letter in which conclusions are stated; however, disclosure of the amount paid is not required. In groups or organizations engaged in appraisal practice, intracompany payments for business development do not require disclosure.

84 ETHICS RULE Management: An appraiser must not accept an assignment, or have a compensation arrangement for an assignment, that is contingent on any of the following: 1. The reporting of a predetermined result; 2. A direction in assignment results that favors the cause of the client; 3. The amount of a value opinion; 4. The attainment of a stipulated result; Rules 5. The occurrence of a subsequent event directly related to the appraiser s opinion and specific to the assignment s purpose.

85 ETHICS RULE Management: Must not advertise for or solicit assignments in a manner that is false, misleading or exaggerated; Must affix, or authorize the use of, his/her signature to certify recognition and acceptance of USPAP responsibilities in an appraisal or appraisal review assignment; An appraiser must not affix the signature of another appraiser without his/her consent. Rules

86 Rules - Application Application: I am aware of a firm that advertises they can settle a divorce case within 10% of their appraised value. Does this violate USPAP?

87 ETHICS RULE Confidentiality: Rules An appraiser must protect the confidential nature of the appraiser-client relationship; An appraiser must act in good faith with regard to the legitimate interests of the client in using confidential information and communicating assignment results; An appraiser must be aware of, and comply with, all confidentiality and privacy laws and regulations applicable to an assignment.

88 Rules ETHICS RULE Confidentiality: An appraiser must not disclose: (1) confidential information; or (2) assignment results to anyone other than: 1. The client; 2. Persons specifically authorized by the client; 3. State appraiser regulatory agencies; 4. Third parties as may be authorized by due process of law; 5. A duly authorized professional peer review committee (except if it would violate applicable law or regulation).

89 Rules - Application Application: I was contacted by an attorney on behalf of her client to perform an appraisal of limited partner interests. My client is the current owner of the limited partner interests. When I m nearing completion, the attorney calls and asks me where the value is coming in. What does USPAP say about this?

90 Record Keeping Rule

91 Rules RECORD KEEPING RULE An appraiser must prepare a workfile for each appraisal or appraisal review assignment. A workfile must be in existence prior to issuance of any report. A written summary of an oral report must be added to the workfile within a reasonable time after issuance of the oral report. page U-10

92 RECORD KEEPING RULE The workfile must include: 1. The name of the client and the identity, by name or type, of any intended users; 2. True copies of any written reports documented on any type of media; 3. Summaries of all oral reports or testimony, or a transcript of testimony including the appraiser s signed and dated certification; 4. All other data, information or documentation to support the appraiser s opinion and show compliance with USPAP. 5. If Restricted Appraisal Report, workfile must be sufficient to produce an Appraisal Report. Rules

93 Rules RECORD KEEPING RULE Retention Five Years Two Years Custody Have File Arrange Custody of File

94 Competency Rule

95 COMPETENCY RULE An Appraiser must: 1.Be competent to perform the assignment; 2.Acquire the necessary competency to perform the assignment; or 3.Decline or withdraw from the assignment. Rules In all cases, the appraiser must perform competently when completing the assignment. page U-11

96 COMPETENCY RULE Being Competent Requires: 1.The ability to properly identify the problem to be addressed; and 2.The knowledge and experience to complete the assignment competently; and 3.Recognition of, and compliance with, laws and regulations that apply to the appraiser in the assignment. Rules

97 Rules COMPETENCY RULE Acquiring Competency If an appraiser determines that he or she is not competent prior to accepting an assignment, the appraiser must: 1. Disclose the lack of knowledge and/or experience to the client before accepting the assignment; 2. Take all the steps necessary or appropriate to complete the assignment competently; and 3. Describe, in the report, the lack of knowledge and/or experience and the steps taken to complete the assignment competently.

98 Rules COMPETENCY RULE Acquiring Competency Comment: Competency can be acquired in various ways, including but not limited to, personal study by the appraiser, association with an appraiser reasonably believed to have the necessary knowledge and/or experience, or retention of others who possess the necessary knowledge and/or experience.

99 COMPETENCY RULE If, during an assignment, an appraiser realizes his/her lack of the required knowledge and experience to complete the assignment competently, the appraiser must: 1. notify the client; and 2. take all steps necessary or appropriate to complete the assignment competently; and 3. describe, in the report, the lack of knowledge and/or experience and the steps taken to complete the assignment competently. Rules

100 Rules COMPETENCY RULE Lack of Competency If the assignment cannot be completed competently, the appraiser must decline or withdraw from the assignment.

101 Rules - Application Application: An appraiser typically performs valuations for financial reporting purposes. That appraiser is asked to perform an assignment of a limited partner interest in a partnership for estate planning purposes. What are the appraiser s responsibilities?

102 Scope of Work Rule

103 Rules SCOPE OF WORK RULE Applies to development only not reporting page U-13

104 SCOPE OF WORK RULE For each appraisal and appraisal review assignment, an appraiser must: 1. Identify the problem to be solved; 2. Determine and perform the scope of work necessary to develop credible assignment results; and 3. Disclose the scope of work in the report. Rules

105 Rules SCOPE OF WORK RULE An appraiser must properly identify the problem to be solved in order to determine the appropriate scope of work. The appraiser must be prepared to demonstrate that the scope of work is sufficient to produce credible assignment results.

106 SCOPE OF WORK RULE Scope of work includes, but is not limited to: The extent to which property is identified The type and extent of data researched The type and extent of analyses applied to arrive at opinions or conclusions Rules

107 SCOPE OF WORK RULE Rules Appraisers have broad flexibility and significant responsibility in determining the appropriate scope of work for an appraisal or appraisal review assignment. Credible assignment results require support by relevant evidence and logic. The credibility of assignment results is always measured in the context of the intended use.

108 Rules SCOPE OF WORK RULE Problem Identification An appraiser must gather and analyze information about those assignment elements that are necessary to properly identify the appraisal or appraisal review problem to be solved.

109

110 SCOPE OF WORK RULE Problem Identification Appraisal Assignment Elements: client and any other intended users; intended use of the appraiser s opinions and conclusions; type and definition of value; effective date of the appraiser s opinions and conclusions; subject of the assignment and its relevant characteristics; and assignment conditions. Rules

111 Rules SCOPE OF WORK RULE Problem Identification Similar information needed for Appraisal Review. Communication with the client is needed. However, identification of relevant characteristics is a judgment made by the appraiser that requires competency in that type of assignment

112 Rules SCOPE OF WORK RULE Assignment Conditions include: 1.Assumptions 2.Extraordinary assumptions 3.Hypothetical Conditions 4.Laws and regulations 5.Jurisdictional Exceptions 6.Other Conditions

113 SCOPE OF WORK RULE Scope of Work Acceptability Rules Must include research and analysis that are necessary to develop credible assignment results. Whether meets requirements is based on: The expectations of parties who are regularly intended users for similar assignments; and What an appraiser s peers actions would be in performing the same or similar assignment.

114 SCOPE OF WORK RULE Work Acceptability Might change during assignment Rules Appraiser must be prepared to support the decision to exclude any investigation, information, method, or technique that would appear relevant to the client, another intended user, or the appraiser s peers.

115 SCOPE OF WORK RULE Work Acceptability Must not allow limits on the scope of work to extent that assignment results are not credible; No bias due to client s objectives or the intended use; Appraiser may need to withdraw from the assignment. Rules

116 SCOPE OF WORK RULE Disclosure Obligations Rules The report must contain sufficient information to allow intended users to understand the scope of work performed. Comment: proper disclosure is required because clients and other intended users rely on the assignment results. Sufficient information includes disclosure of research and analyses performed and might also include research and analysis not performed.

117 Rules SCOPE OF WORK RULE Advisory Opinion 28 Scope of Work Decision, Performance, and Disclosure Advisory Opinion 29 An Acceptable Scope of Work

118 Rules SCOPE OF WORK RULE Calculations Under SSVS-1* SSVS-1 discusses an Engagement to Estimate Value which includes both a Valuation Engagement and a Calculation Engagement all terms defined in SSVS-1. Engagement to Estimate Value is similar to Appraisal in USPAP. *SSVS-1 is the Statement on Standards for Valuation Services No. 1 issued by the American Institute of Certified Public Accountants

119 Rules - Calculations Appraisal : (noun) the act or process of developing an opinion of value; an opinion of value. (adjective) of or pertaining to appraising and related function such as appraisal practice or appraisal review services. Appraisal Practice: valuation services performed by an individual acting as an appraiser including, but not limited to appraisal and appraisal review.

120 Appraisal Practice: Rules - Calculation Comment: Appraisal practice is provided only by appraisers, while valuation services are provided by a variety of professionals and others. The terms appraisal and appraisal review are intentionally generic and are not mutually exclusive. For example, an opinion of value may be required as part of an appraisal review assignment. The use of other nomenclature for an appraisal or appraisal review assignment (e.g., analysis, counseling, evaluation, study, submission, or valuation) does not exempt an appraiser from adherence to USPAP.

121 SCOPE OF WORK RULE Calculations Under SSVS-1 Rules SSVS-1 States: This Statement is not applicable to mechanical computations that do not rise to the level of an engagement to estimate value; that is when the member does not apply valuation approaches and methods and does not use professional judgment.

122 SCOPE OF WORK RULE Calculations Under SSVS-1 Rules Based on a detailed reading of USPAP and SSVS-1, a Calculation under SSVS-1 is an Appraisal with a lesser Scope of Work under USPAP. When performing an SSVS-1 Calculation, USPAP would have some additional requirements.

123 Rules - Application Application: In a divorce setting, an appraiser is asked to provide an estimate of value for settlement discussion purposes only. The attorney has asked that the procedures be kept to a minimum to reach some reasonable value indication. How would USPAP be applied in this situation? Application: Settlement does not happen and another appraiser is retained as an expert witness to perform an appraisal for the litigation. Does this assignment have the same scope of work? What would expectations be for the conclusion relative to the conclusion reached above?

124 Jurisdictional Exception Rule

125 Rules JURISDICTIONAL EXCEPTION If any applicable law or regulation precludes compliance with any part of USPAP, only that part of USPAP becomes void for that assignment. page U-15

126 JURISDICTIONAL EXCEPTION In an assignment involving a jurisdictional exception an appraiser must: 1.Identify the law or regulation that precludes compliance with USPAP; 2.Comply with that law or regulation; 3.Clearly and conspicuously disclose in the report the part of USPAP that is voided by that law or regulation; 4.Cite in the report the law or regulation requiring this exception to USPAP compliance. Rules

127 Standard 9

128 Learning Objectives Upon completion, the participant will be able to: Apply Standard 9 for Business Appraisal, Development page U-60

129 Business Appraisal, Development In developing an appraisal of an interest in a business enterprise or intangible asset, an appraiser must Identify the problem to be solved Standard 9 Determine the scope of work necessary to solve the problem Correctly complete the research and analyses necessary to produce a credible appraisal. page U-60

130 Business Appraisal, Development Appraiser must Standard 9 Know and correctly use appropriate approaches, methods, techniques Not commit substantial error of omission or commission that significantly affects an appraisal Nor render appraisal services in a careless or negligent manner.

131 Business Appraisal, Development Must (see subsequent slide on each) Identify the assignment elements Determine whether orderly liquidation analysis is appropriate Collect and analyze all information necessary for credible assignment results Reconcile Standard 9

132

133 Business Appraisal, Development Assignment Elements Client & other intended users (see FAQ 123, page F-57) Intended use Standard and premise of value Effective date Standard 9 Characteristics of subject property that are relevant to the standard of value and intended use (see subsequent slide) Extraordinary assumptions and hypothetical conditions (see subsequent slide) From these, determine the appropriate scope of work

134 Business Appraisal, Development Characteristics of subject property The subject business enterprise or intangible asset The interest in the business enterprise, equity, asset, or liability to be valued Buy-sell, option agreements, restrictions, similar features that might influence value (legal terms) Elements of control Extent to which marketable and/or liquid Standard 9

135 Business Appraisal, Development Standard 9 Assignment conditions Extraordinary assumptions Hypothetical conditions

136 Business Appraisal, Development Orderly liquidation If interest has ability to cause liquidation Investigate possibility that liquidation is higher value Standard 9 Appraisal of real property and personal property might be appropriate

137

138 Business Appraisal, Development Collect and analyze all information necessary for credible assignment results Approaches Key factors (see next slide) Analyze specific applicable legal terms Elements of control and marketability Standard 9

139 Business Appraisal, Development Key factors Nature and history of subject Financial and economic conditions affecting subject, its industry, the general economy Past results, current operations, future prospects Past sales of capital stock or other ownership interest in subject Past sales of capital stock or other ownership interest in similar entities Prices, terms, and conditions affecting past sales Economic benefit of tangible and intangible assets Standard 9

140 Business Appraisal, Development Reconcile Quality and quantity of data available and analyzed Standard 9 Applicability and relevance of the approaches, methods and procedures used to arrive at the value conclusion

141 Standard 9 - Application Application: I was recently asked to perform an appraisal of 100% and a minority interest in the equity of a business and the client indicated it was for general management planning purposes. What USPAP concerns might I have?

142 Standard 9 - Application Application: I am valuing a minority interest in the equity of a company. There have been prior transactions in the shares of this company, and there is a buy-sell agreement in place. Does USPAP require that I analyze these factors and reflect them in my final conclusion?

143 Standard 10

144 Learning Objectives Upon completion, the participant will be able to: Apply Standard 10 for Business Appraisal, Reporting

145

146 Business Appraisal, Reporting In reporting the results of an appraisal of an interest in a business enterprise or intangible asset, an appraiser must communicate each analysis, opinion, and conclusion in a manner that is not misleading Addresses content and level of information (substantive content) Does not dictate form, format, style. Standard 10 page U-64

147 Business Appraisal, Reporting Report must Standard 10 Clearly and accurately set for the appraisal in a manner that will not be misleading Contain sufficient information to enable the intended user(s) to understand the report Clearly and accurately disclose all assumptions, extraordinary assumptions, hypothetical conditions, and limiting conditions used in the assignment

148 Business Appraisal, Reporting Report must Be prepared in accordance with one of two options Prominently state which option is used Appraisal Report Restricted Appraisal Report Standard 10

149 Business Appraisal, Reporting Determining which option is appropriate Depends on intended use and intended users If more than one intended user, must use Appraisal Report Can use another label in addition to USPAP ones (but not in place of) Minimum of report type must be met Standard 10 A party receiving a copy does not automatically become an intended user

150 Business Appraisal, Reporting Appraisal Report must (cont d next slide) Standard 10 State identity of client and other intended users State intended use Summarize identification of subject and interest appraised State existence of elements of control and basis of view State extent of marketability/liquidity and basis of view State standard and definition of value and premise State effective date and date of report

151 Business Appraisal, Reporting Appraisal Report must (continued) Summarize scope of work used Summarize information analyzed, procedures followed, and reasoning that supports the analyses, opinions, and conclusions; Explain exclusion of market, asset-based, or income approach State, clearly and conspicuously, Any extraordinary assumptions or hypothetical conditions and That their use might have affected assignment results Include a signed certification Standard 10

152 Business Appraisal, Reporting Restricted Appraisal Report must (cont d next slide) State identity of client and prominent use restriction with warning State intended use State identification of subject and interest appraised State existence of elements of control and basis of view State extent of marketability/liquidity and basis of view State standard of value and site source and premise State effective date and date of report Standard 10

153 Business Appraisal, Reporting Restricted Appraisal Report must (continued) State scope of work used State procedures followed, state the value opinion(s) and conclusion(s) reached, and reference the workfile; Explain exclusion of market, asset-based, or income approach State, clearly and conspicuously, Any extraordinary assumptions or hypothetical conditions and That their use might have affected assignment results Include a signed certification Standard 10

154 Business Appraisal, Reporting Certification (Cont d next slide) Indicates compliance with USPAP requirements Must include statements similar to those listed Standard 10 Appraiser who signs any part of report must sign a certification Anyone who signs certification accepts full responsibility for all elements of the certification, for the assignment results, and for the contents of the report. Are allowances for inclusion of different certifications for each of three disciplines represented in USPAP (real property, personal property, businesses) but no other division

155 Business Appraisal, Reporting Certification (continued) Relying on work done by appraisers or others who do not sign a certification (see FAQ 256, page F-120) Need reasonable basis for relying on their work Standard 10 Need reasonable basis for believing they are competent Must have no reason to doubt that the work of those individuals is credible Name the individuals providing significant business or intangible asset appraisal assistance and not signing the certification (are additional disclosure requirements)

156 Business Appraisal, Reporting Oral reports To extent both possible and appropriate, an oral report must address the substantive matters necessary for an Appraisal Report Workfile must have Signed, dated certification Standard 10 Sufficient information to produce an Appraisal Report

157 Standards 9 & 10 Advisory Opinion 11 Content of the Appraisal Report Options of Standards Rules 2-2, 8-2, and 10-2 (pg A-22) Advisory Opinion 12 Use of the Appraisal Report Options of Standards Rules 2-2, 8-2, and 10-2 (pg A-27) Statement 9 Identification of Intended Use and Intended Users (pg U-83) Advisory Opinion 3 Update of a Prior Appraisal (pg A-7)

158 Standards 9 & 10 - Application Application: An appraiser is asked to complete a valuation of an interest in a business for estate tax reporting purposes. The potential client is asking that the appraiser complete appropriate analyses and provide just exhibits and no narrative report. Could the appraiser complete this assignment in compliance with USPAP?

159 Standards 9 & 10 - Application Application: I am working on a valuation for estate tax reporting purposes with an attorney as my client. When I m nearing completion of the narrative report, the attorney asks that I discuss the value conclusion with him before sending the narrative report. When the attorney hears the conclusion, he asks that I stop work on the engagement and send a bill for the work to date. Can I do this and comply with USPAP?

160 Standard 3

161 Learning Objectives Upon completion, the participant will be able to: Apply Standard 3 for Appraisal Review

162 Appraisal Review, Development In developing an appraisal review assignment, an appraiser acting as a review must Identify the problem to be solved Standard 3 Determine the scope of work necessary to solve the problem Correctly complete the research and analyses necessary to produce a credible appraisal review. page U-28

163 Appraisal Review, Development Appraiser must Standard 3 Know and correctly use appropriate approaches, methods, techniques Not commit substantial error of omission or commission that significantly affects an appraisal review Not render appraisal review services in a careless or negligent manner.

164 Appraisal Review, Development Must (see subsequent slide on each) Identify the assignment elements Develop an opinion as to whether the report is appropriate and not misleading within the context of the requirements applicable to the work Develop the reasons for any disagreement Standard 3 Take additional steps if the scope of work includes the reviewer developing his/her own opinion of value or review opinion

165 Appraisal Review, Development Assignment Elements Client & other intended users Intended use Purpose and whether includes reviewer s own opinion of value or review opinion Work under review and its relevant characteristics (see subsequent slide) Effective date Standard 3 Extraordinary assumptions and hypothetical conditions From these, determine the appropriate scope of work

166 Appraisal Review, Development Identify the characteristics of the work under review that are relevant to the intended use and purpose of the appraisal review Ownership interest in the property that is the subject of the work under review Date of the work under review and its effective date Standard 3 Appraiser(s) who completed the work under review, unless identity withheld by client The physical, legal, and economic characteristics of the property, properties, property type(s), or market area in the work under review

167 Appraisal Review, Development Perform steps necessary for credible assignment results Within the context of requirements applicable to that work, and According to the scope of work Standard 3

168 Appraisal Review, Development Potential steps, including reasons for any disagreement Is analysis appropriate Are opinions and conclusions credible Is report appropriate and not misleading Standard 3 Own opinion of value or review opinion (see next slide)

169 Standard 3 Appraisal Review, Development When providing own opinion of value or review opinion Comply with Standards applicable Whether agreeing or disagreeing with value Scope of work might be same as or different from work under review Effective date might be same as or different from work under review Can accept parts of work under review by extraordinary assumption Those parts not deemed credible must be replaced

170 Appraisal Review, Reporting In reporting the results of an appraisal review assignment an appraiser acting as a reviewer must communicate each analysis, opinion, and conclusion in a manner that is not misleading Addresses content and level of information (substantive content) Does not dictate form, format, style. Standard 3

171 Appraisal Review, Reporting Report must Standard 3 Clearly and accurately set for the appraisal review in a manner that will not be misleading Contain sufficient information to enable the intended user(s) to understand the report Clearly and accurately disclose all assumptions, extraordinary assumptions, and hypothetical conditions used in the assignment

172 Standard 3 Appraisal Review, Reporting Review Report must (cont d next slide) State identity of client and other intended users State intended use State purpose State information sufficient to identify Work under review and ownership interest in property that is subject Date of work under review Effective date Appraiser(s) who completed work under review State effective date of review and date of review report

173 Appraisal Review, Reporting Review Report must (continued) State scope of work used State, clearly and conspicuously, Any extraordinary assumptions or hypothetical conditions and That their use might have affected assignment results State reviewer s opinion and conclusions and reasons for disagreement Include a signed certification Standard 3 Additional items if includes reviewer s own opinion of value (see next slide)

174 Appraisal Review, Reporting If reviewer developed own opinion of value or review opinion, report must State which information, analyses, opinions, and conclusions in the work under review were accepted as credible and used Summarize any additional information relied on and the reasoning for the reviewer s opinion related to the work under review State, clearly and conspicuously, Any extraordinary assumptions or hypothetical conditions and That their use might have affected assignment results Standard 3

175 Appraisal Review, Reporting If reviewer developed own opinion of value or review opinion Data and analysis provided by the reviewer to support a different opinion or conclusion must match, at a minimum, except for certification requirements, the reporting requirements for Appraisal Report under Standard 10 Appraisal Review Report under Standard 3 Standard 3

176 Appraisal Review, Reporting Oral reports To extent both possible and appropriate, an oral Appraisal Review Report must address the substantive matters above Workfile must have Signed, dated certification Standard 3 Sufficient information to produce a written Appraisal Review Report

First Exposure Draft of proposed changes for the edition of the Uniform Standards of Professional Appraisal Practice

TO: FROM: RE: All Interested Parties J. Carl Schultz, Jr., Chair Appraisal Standards Board First Exposure Draft of proposed changes for the 2014-15 edition of the Uniform Standards of Professional Appraisal

TO: FROM: RE: All Interested Parties J. Carl Schultz, Jr., Chair Appraisal Standards Board First Exposure Draft of proposed changes for the 2014-15 edition of the Uniform Standards of Professional Appraisal

619 STANDARD 2: REAL PROPERTY APPRAISAL, REPORTING

619 STANDARD 2: REAL PROPERTY APPRAISAL, REPORTING 620 In reporting the results of a real property appraisal, an appraiser must communicate each analysis, 621 opinion, and conclusion in a manner that is

619 STANDARD 2: REAL PROPERTY APPRAISAL, REPORTING 620 In reporting the results of a real property appraisal, an appraiser must communicate each analysis, 621 opinion, and conclusion in a manner that is

Second Exposure Draft of Proposed Changes for the Edition of the Uniform Standards of Professional Appraisal Practice

TO: FROM: RE: All Interested Parties Margaret Hambleton, Chair Appraisal Standards Board Second Exposure Draft of Proposed Changes for the 2018-19 Edition of the Uniform Standards of Professional Appraisal

TO: FROM: RE: All Interested Parties Margaret Hambleton, Chair Appraisal Standards Board Second Exposure Draft of Proposed Changes for the 2018-19 Edition of the Uniform Standards of Professional Appraisal

First Exposure Draft of proposed changes for the edition of the Uniform Standards of Professional Appraisal Practice

TO: FROM: RE: All Interested Parties Sandra Guilfoil, Chair Appraisal Standards Board First Exposure Draft of proposed changes for the 2012-13 edition of the Uniform Standards of Professional Appraisal

TO: FROM: RE: All Interested Parties Sandra Guilfoil, Chair Appraisal Standards Board First Exposure Draft of proposed changes for the 2012-13 edition of the Uniform Standards of Professional Appraisal

For clarification, the Statements and Advisory Opinions have been labeled as to their applicability to the various appraisal disciplines.

Forward The Appraisal Standards Board (ASB) of The Appraisal Foundation develops, publishes, interprets, and amends the Uniform Standards of Professional Appraisal Practice (USPAP) on behalf of appraisers

Forward The Appraisal Standards Board (ASB) of The Appraisal Foundation develops, publishes, interprets, and amends the Uniform Standards of Professional Appraisal Practice (USPAP) on behalf of appraisers

Exposure Draft of Proposed Changes to ADVISORY OPINION 21 (AO-21), USPAP Compliance

, USPAP Compliance") TO: FROM: RE: All Interested Parties Barry J. Shea, Chair Appraisal Standards Board Exposure Draft of Proposed Changes to ADVISORY OPINION 21 (AO-21), USPAP Compliance DATE: February 22, 2013 The goal

TO: FROM: RE: All Interested Parties Barry J. Shea, Chair Appraisal Standards Board Exposure Draft of Proposed Changes to ADVISORY OPINION 21 (AO-21), USPAP Compliance DATE: February 22, 2013 The goal

Real Estate Appraisal Professional Standards

Real Estate Appraisal Professional Standards Summary This proposal is to amend the Florida Administrative Code (FAC) to allow a Certified Residential Appraiser or a Certified General Appraiser to use standards

Real Estate Appraisal Professional Standards Summary This proposal is to amend the Florida Administrative Code (FAC) to allow a Certified Residential Appraiser or a Certified General Appraiser to use standards

Second Exposure Draft of proposed changes for the edition of the Uniform Standards of Professional Appraisal Practice

TO: FROM: RE: All Interested Parties Barry J. Shea, Chair Appraisal Standards Board Second Exposure Draft of proposed changes for the 2016-17 edition of the Uniform Standards of Professional Appraisal

TO: FROM: RE: All Interested Parties Barry J. Shea, Chair Appraisal Standards Board Second Exposure Draft of proposed changes for the 2016-17 edition of the Uniform Standards of Professional Appraisal

Page 1 of 5 STANDARD 3: APPRAISAL REVIEW, DEVELOPMENT AND REPORTING In performing an appraisal review, an appraiser acting as a reviewer must develop and report a credible opinion as to the quality of

Page 1 of 5 STANDARD 3: APPRAISAL REVIEW, DEVELOPMENT AND REPORTING In performing an appraisal review, an appraiser acting as a reviewer must develop and report a credible opinion as to the quality of

UNIFORM STANDARDS OF PROFESSIONAL APPRAISAL PRACTICE and ADVISORY OPINIONS 2006 EDITION

e UNIFORM STANDARDS OF PROFESSIONAL APPRAISAL PRACTICE and ADVISORY OPINIONS 2006 EDITION Published in the United States of America. All rights reserved. No parts of this publication may be reproduced,

e UNIFORM STANDARDS OF PROFESSIONAL APPRAISAL PRACTICE and ADVISORY OPINIONS 2006 EDITION Published in the United States of America. All rights reserved. No parts of this publication may be reproduced,

SUBJECT: Unacceptable Assignment Conditions in Real Property Appraisal Assignments

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 ADVISORY OPINION 19 (AO-19) This communication by the Appraisal Standards Board (ASB) does not establish new standards

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 ADVISORY OPINION 19 (AO-19) This communication by the Appraisal Standards Board (ASB) does not establish new standards

UNDERSTANDING HOW USPAP APPLIES TO REAL PROPERTY APPRAISAL PRACTICE USPAP Matrix

UNDERSTANDING HOW USPAP APPLIES TO REAL PROPERTY APPRAISAL PRACTICE - 2014-2015 USPAP Matrix This matrix assumes an Appraisal Report Format under S. R. 2-2(a). *Last updated 9/11/14* GENERAL Violation

UNDERSTANDING HOW USPAP APPLIES TO REAL PROPERTY APPRAISAL PRACTICE - 2014-2015 USPAP Matrix This matrix assumes an Appraisal Report Format under S. R. 2-2(a). *Last updated 9/11/14* GENERAL Violation

Second Exposure Draft of proposed changes for the edition of the Uniform Standards of Professional Appraisal Practice

TO: FROM: RE: All Interested Parties Sandra Guilfoil, Chair Appraisal Standards Board Second Exposure Draft of proposed changes for the 2012-13 edition of the Uniform Standards of Professional Appraisal

TO: FROM: RE: All Interested Parties Sandra Guilfoil, Chair Appraisal Standards Board Second Exposure Draft of proposed changes for the 2012-13 edition of the Uniform Standards of Professional Appraisal

UNIFORM STANDARDS OF PROFESSIONAL APPRAISAL PRACTICE Effective January 1, 2016 through December 31, 2017

2016-2017 EDITION 2016-2017 UNIFORM STANDARDS OF PROFESSIONAL APPRAISAL PRACTICE Effective January 1, 2016 through December 31, 2017 PLUS Guidance from the Appraisal Standards Board + USPAP ADVISORY OPINIONS

2016-2017 EDITION 2016-2017 UNIFORM STANDARDS OF PROFESSIONAL APPRAISAL PRACTICE Effective January 1, 2016 through December 31, 2017 PLUS Guidance from the Appraisal Standards Board + USPAP ADVISORY OPINIONS

USPAP Q&A USPAP Q&A Issue Date: December 19, 2017

USPAP Q&A 2018-19 USPAP Q&A Issue Date: December 19, 2017 The Appraisal Standards Board (ASB) of The Appraisal Foundation develops, interprets, and amends the Uniform Standards of Professional Appraisal

USPAP Q&A 2018-19 USPAP Q&A Issue Date: December 19, 2017 The Appraisal Standards Board (ASB) of The Appraisal Foundation develops, interprets, and amends the Uniform Standards of Professional Appraisal

Anatomy Of An Appraisal

Anatomy Of An Appraisal Leslie A. Fields The most important thing to know about an appraisal report is how to review and critique it. Leslie A. Fields a partner with the Law Firm of Faegre & Benson LLP,

Anatomy Of An Appraisal Leslie A. Fields The most important thing to know about an appraisal report is how to review and critique it. Leslie A. Fields a partner with the Law Firm of Faegre & Benson LLP,

EDITION 7-HOUR RESIDENTIAL APPRAISAL REVIEW AND UNIFORM STANDARDS OF PROFESSIONAL APPRAISAL PRACTICE (USPAP) COMPLIANCE COURSE

COMPLIANCE COURSE") 2016-17 EDITION 7-HOUR RESIDENTIAL APPRAISAL REVIEW AND UNIFORM STANDARDS OF PROFESSIONAL APPRAISAL PRACTICE (USPAP) COMPLIANCE COURSE Residential Appraisal Review and Uniform Standards of Professional

2016-17 EDITION 7-HOUR RESIDENTIAL APPRAISAL REVIEW AND UNIFORM STANDARDS OF PROFESSIONAL APPRAISAL PRACTICE (USPAP) COMPLIANCE COURSE Residential Appraisal Review and Uniform Standards of Professional

UNIFORM STANDARDS OF PROFESSIONAL APPRAISAL PRACTICE

UNIFORM STANDARDS OF PROFESSIONAL APPRAISAL PRACTICE 2010-2011 EDITION 2 PLUS Guidance from the Appraisal Standards Board + USPAP ADVISORY OPINIONS + USPAP FREQUENTLY ASKED QUESTIONS (FAQ) Effective January

UNIFORM STANDARDS OF PROFESSIONAL APPRAISAL PRACTICE 2010-2011 EDITION 2 PLUS Guidance from the Appraisal Standards Board + USPAP ADVISORY OPINIONS + USPAP FREQUENTLY ASKED QUESTIONS (FAQ) Effective January

Residential Evaluation Report (RER) April, 2016

April, 2016") Residential Evaluation Report (RER) ensuring compliance with the Interagency Guidelines (IAG) and USPAP April, 2016 Definitions RER shall mean a Residential Evaluation Report and is deemed to be a restricted

Residential Evaluation Report (RER) ensuring compliance with the Interagency Guidelines (IAG) and USPAP April, 2016 Definitions RER shall mean a Residential Evaluation Report and is deemed to be a restricted

Yellow highlighting emphases added by A.L. Appraisal Co.

1 2 3 4 5 6 7 8 9 10 11 (AO-11) This communication by the Appraisal Standards Board (ASB) does not establish new standards or interpret existing standards. Advisory Opinions are issued to illustrate the

1 2 3 4 5 6 7 8 9 10 11 (AO-11) This communication by the Appraisal Standards Board (ASB) does not establish new standards or interpret existing standards. Advisory Opinions are issued to illustrate the

Guide Note 15 Assumptions and Hypothetical Conditions

Guide Note 15 Assumptions and Hypothetical Conditions Introduction Appraisal and review opinions are often premised on certain stated conditions. These include assumptions (general, and special or extraordinary)

Guide Note 15 Assumptions and Hypothetical Conditions Introduction Appraisal and review opinions are often premised on certain stated conditions. These include assumptions (general, and special or extraordinary)

RESTRICTED APPRAISAL REPORT

Restricted Use Appraisal Report Thomas J. Schulte & Associates Page #1 RESTRICTED APPRAISAL REPORT SUBJECT ASSIGNMENT Property City: Zip Code: County: Legal Description: Assessor's Parcel #: Tax Year:

Restricted Use Appraisal Report Thomas J. Schulte & Associates Page #1 RESTRICTED APPRAISAL REPORT SUBJECT ASSIGNMENT Property City: Zip Code: County: Legal Description: Assessor's Parcel #: Tax Year:

Guide Note 6 Consideration of Hazardous Substances in the Appraisal Process

Guide Note 6 Consideration of Hazardous Substances in the Appraisal Process Introduction The consideration of environmental conditions along with social, economic, and governmental conditions is fundamental

Guide Note 6 Consideration of Hazardous Substances in the Appraisal Process Introduction The consideration of environmental conditions along with social, economic, and governmental conditions is fundamental

Significance of USPAP

Page 1 of 10 USPAP and the Personal Property Appraiser by David J. Maloney, Jr., AOA CM and William M. Novotny, ISA AM, GCA Originally published in the Journal of Advanced Appraisal Studies All professions,

Page 1 of 10 USPAP and the Personal Property Appraiser by David J. Maloney, Jr., AOA CM and William M. Novotny, ISA AM, GCA Originally published in the Journal of Advanced Appraisal Studies All professions,

USPAP Q&A USPAP Q&A Issue Date: June 10, 2011

USPAP Q&A 2011 USPAP Q&A Issue Date: June 10, 2011 The Appraisal Standards Board (ASB) of The Appraisal Foundation develops, interprets, and amends the Uniform Standards of Professional Appraisal Practice

USPAP Q&A 2011 USPAP Q&A Issue Date: June 10, 2011 The Appraisal Standards Board (ASB) of The Appraisal Foundation develops, interprets, and amends the Uniform Standards of Professional Appraisal Practice

VALUATION REPORTING REVISED Introduction. 3.0 Definitions. 2.0 Scope INTERNATIONAL VALUATION STANDARDS 3

4.4 INTERNATIONAL VALUATION STANDARDS 3 REVISED 2007 1.0 Introduction 1.1 The critical importance of a Valuation Report, the final step in the valuation process, lies in communicating the value conclusion

4.4 INTERNATIONAL VALUATION STANDARDS 3 REVISED 2007 1.0 Introduction 1.1 The critical importance of a Valuation Report, the final step in the valuation process, lies in communicating the value conclusion

Office of the Comptroller of the Currency Federal Deposit Insurance Corporation Federal Reserve Board Office of Thrift Supervision

Office of the Comptroller of the Currency Federal Deposit Insurance Corporation Federal Reserve Board Office of Thrift Supervision Purpose Interagency Appraisal and Evaluation Guidelines October 27, 1994

Office of the Comptroller of the Currency Federal Deposit Insurance Corporation Federal Reserve Board Office of Thrift Supervision Purpose Interagency Appraisal and Evaluation Guidelines October 27, 1994

What/Who Determines that an Appraiser is Qualified in our Program?

What/Who Determines that an Appraiser is Qualified in our Program? Mike Jones, SR/WA, Maryland Certified General Appraiser Realty Specialist, FHWA Office of Real Estate Services Is it becoming tougher

What/Who Determines that an Appraiser is Qualified in our Program? Mike Jones, SR/WA, Maryland Certified General Appraiser Realty Specialist, FHWA Office of Real Estate Services Is it becoming tougher

MODULE 7-A: APPRAISALS, BPOS AND USPAP

MODULE 7-A: APPRAISALS, BPOS AND USPAP LEARNING OBJECTIVES One of the most challenging aspects of the real estate business is the development of prices or values of the rights to real estate. Buyers and

MODULE 7-A: APPRAISALS, BPOS AND USPAP LEARNING OBJECTIVES One of the most challenging aspects of the real estate business is the development of prices or values of the rights to real estate. Buyers and

APPRAISAL STANDARDS BOARD SUMMARY OF ACTIONS RELATED TO PROPOSED CHANGES. June 8, 2007

APPRAISAL STANDARDS BOARD SUMMARY OF ACTIONS RELATED TO PROPOSED CHANGES Background On, the Appraisal Standards Board (ASB) approved and adopted modifications to the 2006 edition of the Uniform Standards

APPRAISAL STANDARDS BOARD SUMMARY OF ACTIONS RELATED TO PROPOSED CHANGES Background On, the Appraisal Standards Board (ASB) approved and adopted modifications to the 2006 edition of the Uniform Standards

ASA MTS CANDIDATE REPORT REVIEW CHECKLIST INSTRUCTIONS (Effective as of January 01, 2018) Basic Report Requirements and General Report Quality

Basic Report Requirements and General Report Quality") ASA MTS CANDIDATE REPORT REVIEW CHECKLIST INSTRUCTIONS (Effective as of January 01, 2018) Basic Report Requirements and General Report Quality This checklist was designed to be a useful resource tool by

ASA MTS CANDIDATE REPORT REVIEW CHECKLIST INSTRUCTIONS (Effective as of January 01, 2018) Basic Report Requirements and General Report Quality This checklist was designed to be a useful resource tool by

Assessor s offices may observe rules or policy items that

Understanding the Scope of Work Rule and Advisory Opinion 32 Kenneth L. Joyner, RES, AAS The statements made or opinions expressed by authors in Fair & Equitable do not necessarily represent a policy position

Understanding the Scope of Work Rule and Advisory Opinion 32 Kenneth L. Joyner, RES, AAS The statements made or opinions expressed by authors in Fair & Equitable do not necessarily represent a policy position

How to Read a Real Estate Appraisal Report

How to Read a Real Estate Appraisal Report Much of the private, corporate and public wealth of the world consists of real estate. The magnitude of this fundamental resource creates a need for informed

How to Read a Real Estate Appraisal Report Much of the private, corporate and public wealth of the world consists of real estate. The magnitude of this fundamental resource creates a need for informed

AICPA Valuation Services VS Section Statements on Standards for Valuation Services VS Section 100 Valuation of a Business, Business Ownership

AICPA Valuation Services VS Section Statements on Standards for Valuation Services VS Section 100 Valuation of a Business, Business Ownership Interest, Security, or Intangible Asset Calculation Engagements

AICPA Valuation Services VS Section Statements on Standards for Valuation Services VS Section 100 Valuation of a Business, Business Ownership Interest, Security, or Intangible Asset Calculation Engagements

2. Is the information in the contract section complete and accurate? Yes No Not Applicable If Yes, provide a brief summary.

The purpose of this appraisal field review report is to provide the lender/client with an opinion on the accuracy of the appraisal report under review. Property Address City State Zip Code Borrower Owner

The purpose of this appraisal field review report is to provide the lender/client with an opinion on the accuracy of the appraisal report under review. Property Address City State Zip Code Borrower Owner

Common Errors and Issues in Review

Common Errors and Issues in Review February 1, 2018 Copyright 2018 Appraisal Institute. All rights reserved. Printed in the United States of America. No part of this publication may be reproduced, stored

Common Errors and Issues in Review February 1, 2018 Copyright 2018 Appraisal Institute. All rights reserved. Printed in the United States of America. No part of this publication may be reproduced, stored

,J. 1 ~t

,J. 1 ~t An Update on the Activities of The Appraisal Foundation

An Update on the Activities of Prepared for the Great Lakes Chapter of the Appraisal Institute David S. Bunton, President February 12, 2015 An overview of the Foundation, followed by updates on: The Appraiser

An Update on the Activities of Prepared for the Great Lakes Chapter of the Appraisal Institute David S. Bunton, President February 12, 2015 An overview of the Foundation, followed by updates on: The Appraiser

SUBJECT: Interagency Appraisal and Evaluation Guidelines

BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM WASHINGTON, D. C. 20551 DIVISION OF BANKING SUPERVISION AND REGULATION TO THE OFFICER IN CHARGE OF SUPERVISION AT EACH FEDERAL RESERVE BANK SUBJECT: Interagency

BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM WASHINGTON, D. C. 20551 DIVISION OF BANKING SUPERVISION AND REGULATION TO THE OFFICER IN CHARGE OF SUPERVISION AT EACH FEDERAL RESERVE BANK SUBJECT: Interagency

SUBJECT: The Appraisal of Real Property That May Be Impacted by Environmental Contamination

1 ADVISORY OPINION 9 (AO-9) 1 2 3 4 This communication by the Appraisal Standards Board (ASB) does not establish new standards or interpret existing standards. Advisory Opinions are issued to illustrate

1 ADVISORY OPINION 9 (AO-9) 1 2 3 4 This communication by the Appraisal Standards Board (ASB) does not establish new standards or interpret existing standards. Advisory Opinions are issued to illustrate

This packet of information for the Rules Workshop contains the following information:

GENERAL SESSION: Rules Workshop Rule 61J1-9.001 Standards of Appraisal Practice This packet of information for the Rules Workshop contains the following information: Date Item Page Florida Statutes 2015

GENERAL SESSION: Rules Workshop Rule 61J1-9.001 Standards of Appraisal Practice This packet of information for the Rules Workshop contains the following information: Date Item Page Florida Statutes 2015

Code of Professional Ethics and Explanatory Comments

Code of Professional Ethics and Explanatory Comments Effective May 10, 2018 Copyright 2018 Appraisal Institute. All rights reserved. Printed in the United States of America. No part of this publication

Code of Professional Ethics and Explanatory Comments Effective May 10, 2018 Copyright 2018 Appraisal Institute. All rights reserved. Printed in the United States of America. No part of this publication

Tax Implications Of The Intellectual Property Valuation Process

Tax Implications Of The Intellectual Property Valuation Process Robert F. Reilly Robert F. Reilly is a managing director of Willamette Management Associates. He is a Certified Public Accountant, Accredited

Tax Implications Of The Intellectual Property Valuation Process Robert F. Reilly Robert F. Reilly is a managing director of Willamette Management Associates. He is a Certified Public Accountant, Accredited

ILLINOIS HOUSING DEVELOPMENT AUTHORITY APPRAISAL SCOPE AND GUIDELINES December 2015

ILLINOIS HOUSING DEVELOPMENT AUTHORITY APPRAISAL SCOPE AND GUIDELINES December 2015 As part of the Common Application for Multifamily Financing, the Illinois Housing Development Authority (IHDA) requires

ILLINOIS HOUSING DEVELOPMENT AUTHORITY APPRAISAL SCOPE AND GUIDELINES December 2015 As part of the Common Application for Multifamily Financing, the Illinois Housing Development Authority (IHDA) requires

DEALING WITH APPRAISERS AND OTHER EXPERTS:

DEALING WITH APPRAISERS AND OTHER EXPERTS: Challenges In Professionalism, Ethics and Related Issues Charles N. Pursley, Jr., Esquire Pursley Lowery Meeks LLP 260 Peachtree Street, Suite 2000 Atlanta, Georgia

DEALING WITH APPRAISERS AND OTHER EXPERTS: Challenges In Professionalism, Ethics and Related Issues Charles N. Pursley, Jr., Esquire Pursley Lowery Meeks LLP 260 Peachtree Street, Suite 2000 Atlanta, Georgia

Appraisal Review & Advisory Opinion 20 Controversy. Presenter: Lisa Kimbro, MAI, AI-GRS

Appraisal Review & Advisory Opinion 20 Controversy Presenter: Lisa Kimbro, MAI, AI-GRS Practicing appraisers know USPAP, and appraisers that complete review work know USPAP s Standard 3. But what about

Appraisal Review & Advisory Opinion 20 Controversy Presenter: Lisa Kimbro, MAI, AI-GRS Practicing appraisers know USPAP, and appraisers that complete review work know USPAP s Standard 3. But what about

Interagency. Appraisal and Evaluation. Guidelines

Interagency Appraisal and Evaluation Guidelines (December 2, 2010) Interagency Appraisal and Evaluation Guidelines Table of Contents I. Purpose..............................................................

Interagency Appraisal and Evaluation Guidelines (December 2, 2010) Interagency Appraisal and Evaluation Guidelines Table of Contents I. Purpose..............................................................

Appraisal Review for Appraiser Regulators

Appraisal Review for Appraiser Regulators Amy C. McClellan, SRA, MBA Stephen S. Wagner, MAI, SRA, AI GRS October 14, 2017 Presentation Highlights How appraisal regulators can use appraisal reviews Types

Appraisal Review for Appraiser Regulators Amy C. McClellan, SRA, MBA Stephen S. Wagner, MAI, SRA, AI GRS October 14, 2017 Presentation Highlights How appraisal regulators can use appraisal reviews Types

Guide Note 16 Arbitration 1

Guide Note 16 Arbitration 1 Introduction Real estate valuation professionals ( Valuer or Valuers ) are often retained to provide services in arbitration matters 2 either as arbitrators or expert witnesses

Guide Note 16 Arbitration 1 Introduction Real estate valuation professionals ( Valuer or Valuers ) are often retained to provide services in arbitration matters 2 either as arbitrators or expert witnesses

Appraisal Stream Restricted Use Residential Appraisal Report

Appraisal Stream Restricted Use Residential Appraisal Report File No. 769kemplin This report is limited to the sole and exclusive use of the client. The appraiser's opinions and conclusions set forth in

Appraisal Stream Restricted Use Residential Appraisal Report File No. 769kemplin This report is limited to the sole and exclusive use of the client. The appraiser's opinions and conclusions set forth in

All Interested Parties. Rick Baumgardner, Chair Appraisal Practices Board. Date: September 9, Background

TO: FROM: RE: All Interested Parties Rick Baumgardner, Chair Appraisal Practices Board Concept Paper Valuation Issues in Separating Tangible and Intangible Assets Date: September 9, 2013 Background Those

TO: FROM: RE: All Interested Parties Rick Baumgardner, Chair Appraisal Practices Board Concept Paper Valuation Issues in Separating Tangible and Intangible Assets Date: September 9, 2013 Background Those

CRN Presentation Review

CRN Presentation Review Collateral Risk Network June 18, 2013 Scott Sparks VP, Consumer Chief Real Estate Appraiser Fifth Third Bank Greg Stephens SVP, Appraisal Operations and Compliance Metro-West Appraisal

CRN Presentation Review Collateral Risk Network June 18, 2013 Scott Sparks VP, Consumer Chief Real Estate Appraiser Fifth Third Bank Greg Stephens SVP, Appraisal Operations and Compliance Metro-West Appraisal

Module Seven. Student Learning Objectives. After completing this module you should be able to

Module Seven Appraisal Student Learning Objectives After completing this module you should be able to describe the history of, and regulatory process governing, appraisal practice; recite the application

Module Seven Appraisal Student Learning Objectives After completing this module you should be able to describe the history of, and regulatory process governing, appraisal practice; recite the application

CANADIAN UNIFORM STANDARDS OF PROFESSIONAL APPRAISAL PRACTICE

CANADIAN UNIFORM STANDARDS OF PROFESSIONAL APPRAISAL PRACTICE Appraisal Institute of Canada 403 ~ 200 Catherine Street Ottawa, Ontario K2P 2K9 TABLE OF CONTENTS 1 INTRODUCTION... 1 2 DEFINITIONS... 3 3

CANADIAN UNIFORM STANDARDS OF PROFESSIONAL APPRAISAL PRACTICE Appraisal Institute of Canada 403 ~ 200 Catherine Street Ottawa, Ontario K2P 2K9 TABLE OF CONTENTS 1 INTRODUCTION... 1 2 DEFINITIONS... 3 3

Appraisal Review Update: Trends and Best Practices for Lenders and Appraisers

Appraisal Review Update: Trends and Best Practices for Lenders and Appraisers Presenters: Eric Schwartz, MAI, SRA, AI-GRS Rob Moorman, MAI, SRA, AI-GRS AI Connect July 2016 Charlotte, N.C. 1 2 Meet the

Appraisal Review Update: Trends and Best Practices for Lenders and Appraisers Presenters: Eric Schwartz, MAI, SRA, AI-GRS Rob Moorman, MAI, SRA, AI-GRS AI Connect July 2016 Charlotte, N.C. 1 2 Meet the

Paragraph s 8, 9, and 10 from NACVA. Letter of October 27, 2016

Paragraph s 8, 9, and 10 from NACVA Letter of October 27, 2016 Re: Comments Regarding Proposed Treasury Regulation (REG. 163113-02) (to be used also as an Outline of Topics to be Discussed at the Public

Paragraph s 8, 9, and 10 from NACVA Letter of October 27, 2016 Re: Comments Regarding Proposed Treasury Regulation (REG. 163113-02) (to be used also as an Outline of Topics to be Discussed at the Public

January 29, Florida Real Estate Appraisal Board 400 West Robinson Street, N801 Orlando, FL 32801

Francois K. Gregoire, IFA RAA Gregoire & Gregoire, Inc. Realtor - Appraiser 6285 25th Avenue North St. Petersburg, FL 33710 727-344-3393 francois@tampabay.rr.com January 29, 2018 Florida Real Estate Appraisal

Francois K. Gregoire, IFA RAA Gregoire & Gregoire, Inc. Realtor - Appraiser 6285 25th Avenue North St. Petersburg, FL 33710 727-344-3393 francois@tampabay.rr.com January 29, 2018 Florida Real Estate Appraisal

International Valuation Standards Update