Valuation Report. MRP Investments Ltd. Amerikaweg 18 in Assen, The Netherlands File number: 11738

|

|

|

- Cameron Hodges

- 6 years ago

- Views:

Transcription

1 Valuation Report MRP Investments Ltd. Amerikaweg 18 in Assen, The Netherlands File number: 11738

2 Amerikaweg 18 in Assen, The Netherlands Contents 1 Preliminary Notes... 1 Valuation Instruction... 1 Definition of value... 1 Purpose of valuation... 1 Type of valuation... 2 Date of Valuation... 2 Instruction letter... 2 Inspection... 2 JLL Valuation Advisory... 2 Requirements regarding the valuer s independence... 2 Sources of Information Physical Considerations... 4 Letting details... 4 Brief property description... 4 State of repair... 4 Accommodation... 4 Location and accessibility... 5 Sustainability Legal Considerations... 6 Land registry... 6 Real rights... 6 Town planning Market Considerations... 7 General... 7 Supply... 8 Completions and future developments... 9 Take-up... 9 Rental level Investment market general update on dynamics per sector Office investments Valuation Valuation method Marketability SWOT-analysis Comparables Comments Special assumptions Back testing General Principles Market Value Appendices Appendix 1 General Principles Appendix 2 Land Registry Appendix 3 Location Plan Appendix 4 Photograph(s) Appendix 5 Zoning Plan Appendix 6 Valuation Printout Appendix 7 Track Record

3 Amerikaweg 18 in Assen, The Netherlands 1 Preliminary Notes On 17 January 2017 MRP Investments Ltd. assigned JLL per by Mr. A. Fishman to perform a valuation of the four properties from the DW01 Portfolio situated at Spoorsingel in Heerlen, Cartograaf 3 in Duiven, and Amerikaweg 18 in Assen - The Netherlands, as at 31 December 2016 for the purpose of estimating the fair value of the subject property in compliance with IFRS 13. In this report you will find the specifics and grounds on which we base our valuation for the property in Assen. Enclosed you will find the accompanying calculation. We hereby consent to the inclusion and attachment of the valuation report of Amerikaweg 18 in Assen, dated 14 February 2017 with 31 December 2016 as the valuation date, which was prepared for the Company and which may be attached to its 2016 annual financial statements and/or any reports which, pursuant to the laws and regulations of the state of Israel, may be filed with respect to thereof. We hereby empower the authorized representatives of the Company to report the valuation report to the Israeli Securities Authority and Tel Aviv Stock Exchange. Valuation Instruction JLL, Valuation Advisory, with offices in Amsterdam on the Strawinskylaan 3103, declares, to have surveyed and valued the freehold interest of a parcel of land with an office building, situated at Amerikaweg 18 in Assen The Netherlands Definition of value Market value: Market rent: The estimated amount for which an asset or liability should exchange on the valuation date between a willing buyer and a willing seller in an arm's-length transaction after proper marketing and where the parties had each acted knowledgeably, prudently and without compulsion. The estimated amount for which an interest in real property should be leased on the valuation date between a willing lessor and willing lessee on appropriate lease terms in an arm s length transaction, after proper marketing and where the parties had each acted knowledgeably, prudently and without compulsion. The above stated definition of market value is in accordance with the International Financial Reporting Standards, the International Valuation Standards and the Standards of the Royal Institution of Chartered Surveyors. The valuation was requested to support the value of the four assets in the DW01 Portfolio which is listed on the Tel-Aviv Stock Exchange. This valuation is in compliance with IFRS 13 and the International Valuation Standards (IVS). Purpose of valuation We understand that the valuation is required for accounting purposes. The client holds the property as an investment. 1 File number: 11738

4 Amerikaweg 18 in Assen, The Netherlands Type of valuation The instruction involves a re-valuation. Date of Valuation We have adopted 31 December 2016 as the valuation date. Instruction letter This valuation is carried out in accordance with the fee proposal. The depth of work is maintained as set out in the fee proposal. Inspection The property was inspected by D.P.A. Diemel MSc MSRE and mw. C. Rampersad MSc RT on 25 January JLL Valuation Advisory All our valuations are based on internationally acknowledged guidelines and comply with local rules and legislation. Our employees have a high degree of specialization. JLL is recognized as Firm Regulated by RICS. Highly experienced, ISO-certified valuation team One central Amsterdam-based team One team one vision: consequent and consistent Regional approach, good local market knowledge Valuations in accordance with the RICS guidelines and the International Valuation Standards Valuations in accordance with the recommendations of NRVT Vast experience with IPD/ROZ and IPD/aeDex valuations Valuations across the Netherlands and support with European assignments 3,500 valuations per annum with a total value of 45 billion Working according to the four eyes principle High degree of accuracy and reliability Thorough analysis of the available data Intensive contact and consultation with the client Clear time planning Handling with agreements and deadlines in the right way Transparent calculations and reports Stringent requirements on ethical aspects Chinese Walls The properties are valued by Daan Diemel, who has experienced a specialized real estate education at the Amsterdam School of Real Estate (ASRE). Daan is involved by the Valuation Team for 10 years and is experienced in the valuations for all types of real estate. Second valuer is Chaya Rampersad, she has a master in Accountancy and Control and is registered in the Dutch Register for Commercial Real Estate. She is involved in all types of valuations for JLL for almost 3 years. Daan Diemel and Chaya Rampersad valued similar portfolios and single assets for national- and international clients. A track record is attached in Appendix 7. Requirements regarding the valuer s independence Both the IVS code of ethics and the JLL code of ethics contain conditions on how professionals must conduct themselves when having financial interests in clients. It is forbidden (hidden interests and the code of conduct) for JLL employees to have financial interests in property related companies or businesses or to invest directly in property. JLL is not financial dependent on carrying out this specific valuation instruction. Both JLL VA s annual turnover and the total income earned from other JLL services provided to a single client, including any client s related businesses entities, are less than 25% of total turnover. 2 File number: 11738

5 Amerikaweg 18 in Assen, The Netherlands The fee which JLL VA receives for this valuation work is not dependent on the value(s) reported in the valuations. The valuer does not, by carrying out the instruction, envisage any threat to independence or objectivity and concludes that no additional measures are needed to be able to accept the instruction. JLL adopts Chinese Walls which prevent information being exchanged between departments within the organization. Sources of Information In preparing this valuation report, we have relied on the following information: Information Requested from Provided Y (examined) / /N Details Measurement certificates (NEN 2580) MRP Investments Ltd. Y No comments Architectural scaled drawings MRP Investments Ltd. N Recent rent roll MRP Investments Ltd. N Lease agreements MRP Investments Ltd. Y Triple net lease Allonges, addenda and side letters MRP Investments Ltd. Y No comments Title deeds MRP Investments Ltd. N Ground lease (terms and conditions) MRP Investments Ltd. n/a Freehold Cadastral plan and Land Registry extract Land Registry Y No comments Zoning plan ( bestemmingsplan ) ruimtelijkeplannen.nl Y No comments Overview of technical building installations MRP Investments Ltd. N Overview of property charges, such as property tax, water rates and sewage charges MRP Investments Ltd. Maintenance forecast MRP Investments Ltd. N Overview of historical building costs MRP Investments Ltd. N Fire insurance report MRP Investments Ltd. N Environmental impact report (soil pollution / hazardous substances) MRP Investments Ltd. Energy label certificate MRP Investments Ltd. N Other relevant information: MRP Investments Ltd. N We assume that all information obtained from or on behalf of the client is correct and complete. The valuer has as far as possible considered the plausibility of the information provided. Should it appear (or a strong suspicions arise) that the information provided is not complete and/or incorrect, that will be commented on in this report. This also applies where the valuer has adopted information other than that in the information provided. N N 3 File number: 11738

6 Amerikaweg 18 in Assen, The Netherlands 2 Physical Considerations Letting details Based on the lease agreement and the addendum provided by MRP Investments Ltd. we understand that the property was as at the valuation date rented under the following terms and conditions: Tenant: Pharmaceutical Research Associates Group B.V. Rent Passing: 432,917 Start Date: 17 July 2015 Expiration Date: 16 July 2035 Option Period: n x 1 year Indexation: Every year according the CPI Index Further Details: Triple net lease, which means that the tenant bears all operating expenses. The management costs remain with the landlord. Brief property description Year of construction: 2015 Renovation (year): n/a Description renovation: n/a State of repair good Number of floors three floors Foundation concrete foundation Main bearing structure concrete structure Floors concrete floors covered with linoleum Roof flat roof covered with synthetic roof covering and gravel Walls two coloured brickwork walls Frames aluminium window frames fitted with double glazing Systems mechanical ventilation and air-conditioning Number of parking spaces 96 Parking ratio (per m² BVO) 1:30 State of repair At the time of our inspection the general state of repair could be described as good as the property is recently built. Accommodation The total lettable floor area amounts to 2,674 sq m, as contained in the measurement certificate conform NEN 2580, dated 12 March For a breakdown of the lettable floor areas and other details we refer to our valuation printout. 4 File number: 11738

7 Amerikaweg 18 in Assen, The Netherlands Location and accessibility Assen is the capital of the province Drenthe in the North-East of the country. Assen is surrounded by the cities Groningen at approximately 30 kms distance, Hoogeveen at approximately 45 kms distance and Drachten at 60 kms distance. Assen is located at approximately 65 kms away from the German border. Assen has three main business parks where small to medium industry is located. The subject property is located on the Peelerpark Business estate which is located 4 kms to the North of the city centre and is located alongside the A28 motorway towards Groningen. Major occupiers on the estate and close to the property include ANBW, Nederlandse Gasunie and several car showrooms. The accessibility is good by private transport as the property is located alongside the motorway with sufficient parking spaces. There is a bus stop at 10 minutes walking distance from the subject property, which connects with the train station Assen. Sustainability The client has no information available concerning the energy label or other sustainability matters for the property. We have assumed that the property is sufficient sustainable as the property is recently built. 5 File number: 11738

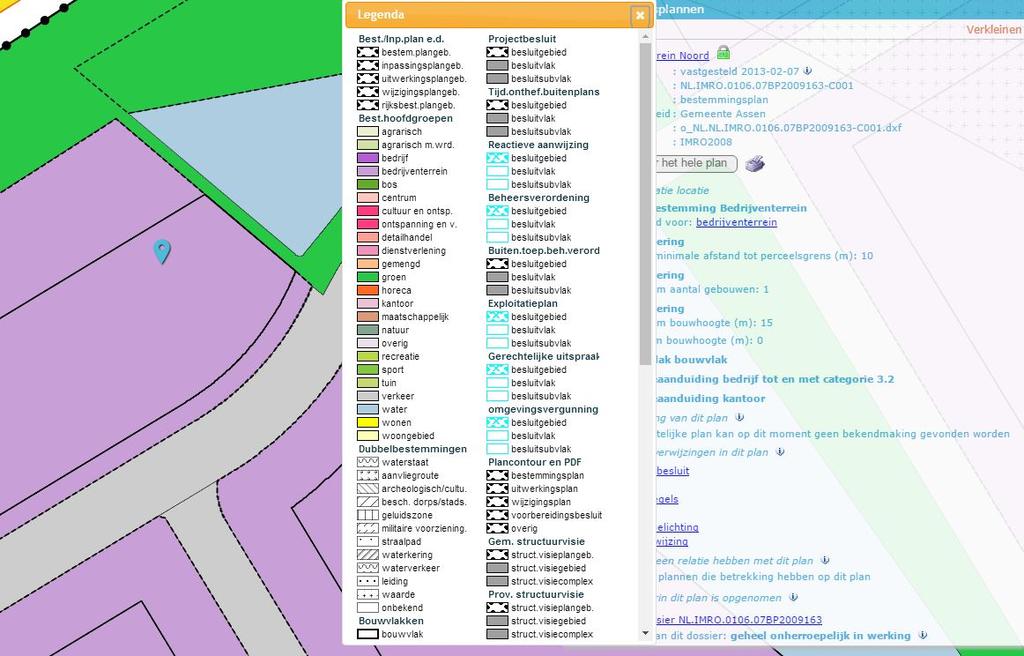

8 Amerikaweg 18 in Assen, The Netherlands 3 Legal Considerations Land registry The local Land Registry ("Kadaster en Openbare Registers") informed us that on 24 January 2017 the property was registered as follows: Municipality: Assen Section: Y Number 738 Estimated area: 68 a 90 ca (6,890 sq m) Description: Business (office) parking We understand from the local Land Registry that on 24 January 2017 the freehold was owned by Assen Office B.V., with its registered offices in s-gravenhage. Real rights National monument: Pre-emption law ( Wet Voorkeursrecht gemeenten ): Restrictions: Recordings in land registry extract: Not applicable. Not applicable. No restrictions recorded in the land registry extract. No comments recorded in the land registry extract. Other special rights: For the purposes of this valuation the valuer has not carried out a detailed investigation on title. Based on the valuer s professional assessment there is no reasonable reason to assume that there are any rights or impediments in the relevant deed(s) which effect the value reported. In determining the market value the valuer has assumed that there are no rights or impediments which effect the value reported. Town planning We understand from the municipality of Assen, that the property falls within the zoning plan ( Bestemmingsplan ) Bedrijventerrein- Noord. The Municipal Council approved the plan on 7 February The zoning plan allocates the property for Business estate ( Bedrijventerrein ) purposes with office use. This includes amongst others business uses, office use, roads, parking and other. The property is subject to a maximum height of 15 m. The maximum site coverage ( bebouwingspercentage ) is unknown. We understand that the current use conforms with the provisions of the zoning plan. 6 File number: 11738

9 Amerikaweg 18 in Assen, The Netherlands 4 Market Considerations General The office stock in the Netherlands grew strongly since 1990 with 71%. This was due to the flourishing economy in the 1990s, which boosted office employment to grow at a faster pace. Increasing demand and decreasing supply resulted in a scarcity of office space. New developments were initiated and were specifically focused on satellite-cities within the Randstad conurbation. This growth continued until the time of the dot-com bubble. GDP growth, together with the rise of the IT sector, led to a strong demand for office space. IT companies often leased twice as much office space than they actually needed for growth purposes. After the burst of the dotcom bubble this extra space was not taken into use. As a result of the historical development the Dutch market is rather densely structured compared to other European markets, while it is also widely spread across the country. Given its history of decentralization many large and small municipalities have their own or multiple office parks. Nevertheless, the Randstad conurbation (including the major 4 cities) has a total office stock of 31 million sq m and ranks among the largest office markets of Europe. Moreover, when combining the four largest cities (G4) because of the close proximity in which these are located, an office market of 16.3 million sq m appears, comparable in size to Berlin and Madrid. The Dutch office market is late in the European property cycle, which means that it follows the trends of the UK and Germany with a time delay of 1-3 years. Therefore the Dutch office leasing market is recovering from the crisis since the beginning of 2015 and the investment market one or two years earlier. Also within the Dutch markets some cities are gaining momentum over other cities. The Randstad conurbation is recovering quite well, especially in Amsterdam, while more peripheral located office districts are still coping with low take-up dynamics. Figure 1: Map of the Netherlands Map of the Netherlands which shows the five largest cities Source: JLL (2017) 7 File number: 11738

10 Amerikaweg 18 in Assen, The Netherlands The four main office markets in the Netherlands combined, which are all located in the Randstad, are accountable for 30% of all office stock within this region. These four cities are Amsterdam (6,140,000 sq m), The Hague (4,060,000 sq m), Rotterdam (3,430,000 sq m) and Utrecht (2,470,000 sq m). Over the last few years, the reconversion of office buildings into hotels, residential and to a lesser extent retail increased heavily. Approximately 2,200,000 sq m of office stock was demolished or converted into other functions during the period The Randstad holds two main ports: the Port of Rotterdam, which is the largest Seaport in Europe with an annual throughput of 440 million tonnes 1 and Amsterdam Schiphol Airport, which is world s second largest airport in terms of connectivity and Europe s third airport in terms of passengers. The airport is located within 10 minutes driving distance of Amsterdam and approximately 30 to 45 minutes from cities as Utrecht, The Hague and Rotterdam. Furthermore, the Randstad has a dense railway network and various motorways with both national and international connections. Examples of motorways that secure international connectivity are A1, A2, A4, A7, A12, A15, A16 and A20. Concerning its railway network, most intercity connections terminate in one of the key cities in the Randstad. Larger cities have multiple railway stations which also provide subway and/or tram connectivity. Supply Due to the vast recovery of the occupier and investment market, the Dutch office market no longer holds its nickname as the graveyard of Europe. In the pre-crisis years ( ) supply volume amounted to 5,000,000 sq m and 4,700,000 sq m respectively. During this period the economy boost was strongly driven by the IT-sector. When the IT-bubble burst and the economy declined, the developments which were already under construction remained vacant. Therefore the supply increased strongly during 2010 to stand at 7,300,000 sq m. The following years supply increased further to stand at Q at 7,600,000 sq m. In 2016 the economy and the office market showed a further recovery on the office occupier market. Combined with the continuing transformation dynamics, supply volume dropped over 2016 with 14% to stand at 6,500,000 sq m. Supply volume in the largest five cities of the Netherlands currently amounts to 2,200,000 sq m, which corresponds to approximately one-third (32%) of the total supply in the Netherlands. Especially the larger cities witnessed a drop in vacancy during Supply is mainly concentrated in the office markets of Amsterdam and Rotterdam with approximately 560,000 sq m and 570,000 sq m respectively. Although demand for grade A office space has increasing, supply in this segment has become relatively scarce. Approximately 19% of the current supply, consists of A-grade office space, 64% is rated as B-grade office space and 17% is rated as C-grade office space. Figure 2: Development of supply and take-up Q4 Supply Take-up '000 sq m 8,000 '000 sq m 2,500 7,000 6,000 2,000 5,000 4,000 3,000 1,500 1,000 2,000 1, Q Supply - Netherlands Five-year average ( ) Take-up - The Netherlands Five-year average ( ) 1 portofrotterdam.com (2015) 8 File number: 11738

11 Amerikaweg 18 in Assen, The Netherlands Completions and future developments As mentioned above, the development activity increased strongly during the upcoming IT-sector in Those office buildings were completed during 2008 and the activity remained high. Due to new regulations such as the ladder voor duurzame ontwikkeling and Kantoren Convenant possibilities for new built offices were restrained. New built office schemes are only allowed under strict conditions, within certain growth -area s and a 70% pre-let threshold. This resulted in a lower development pipeline. In 2013 approximately 531,000 sq m of office space was completed in the Netherlands. The largest completion refers to the De Rotterdam office building (60,000 sq m) in sub location Rotterdam Kop van Zuid, a partially pre-let development. In 2014 approximately 458,000 sq m of office space was completed in the Netherlands. The largest completion refers to the city hall of Utrecht (66,750 sq m) in sub location Utrecht Centre. Figure 3: Development activity Netherlands Supply 800, , , , , , , , Source: JLL (2017) During 2015 approximately 427,900 sq m of office stock was delivered to the Dutch office market. Largest completions refer to the renovation of the ASR headquarter in Utrecht Rijnsweerd and the newly built International Criminal Court. In 2016 a total of 275,000 sq m of office space was delivered to the market. Largest completions refer to the new built office building First (40,000 sq m) at Rotterdam Centre and the completion of the refurbishment of the Atrium complex. Other completed office buildings at the Zuidas are the new Stibbe and Akzo Nobel HQ at the Beethovenlaan. The Dutch office market has a firm pipeline of approximately 1.250,000 sq m until This includes new office schemes, as well as thorough renovations. Most of the developments are located in Amsterdam (464,000 sq m) Utrecht 277,000 sq m) and The Hague (105,000 sq m). The Dutch office market has a non-firm pipeline of approximately 8.3 million sq m which exists for the long term, and focuses primarily (65%) on Randstad. However, these plans are uncertain and have no known start or completion date. Take-up During the financial crisis the Dutch economy and the office market has witnessed turbulent years. Demand for office space has decreased due to consolidating companies and cost reductions. The IT-bubble burst has had a significant impact on the office market. In 2012 the office market has reached its bottom and has developed in a positive way since then. The five year average annual take-up volume over the period amounted to approx million sq. In 2015 and 2016 take-up volume surpassed this level at 1.24 million sq and 1.28 million sq m respectively. This indicates upcoming market conditions. Especially the larger cities benefit from recovering market conditions. Approx. 72% of the take-up volume found place in the Randstad conurbation. Amsterdam witnessed record high demand amounting to almost 400,000 sq m, followed by Utrecht (100,000 sq m), Rotterdam (76,000 sq m) and The Hague (51,000 sq m). 9 File number: 11738

12 Amerikaweg 18 in Assen, The Netherlands Rental level Currently prime rent is achieved in Amsterdam Zuidas. Due to the scarcity of available grade A office space and recovering market conditions, prime rents increased over 2016 in Amsterdam. During the second quarter of 2016, prime rent increased to 350 per sq m per annum. In the third quarter the prime rent remained stable and in the fourth quarter, the prime rent increased to 370 per sq m per annum, and is expected to increase within the next year. Prime rent is applicable to the Zuidas. In several high-end solitaire office buildings rents of above 400 per sq m per annum have been reported. The prime rent in the Netherlands was achieved in the WTC building in sub location Schiphol Centre and has remained stable since 2009.The prime rent in Schiphol remained stable over the last few years, amounting to 365 per sq m per annum. Prime rent for The Hague decreased due to low take-up dynamics from 195 per sq m per annum to the current level of 185 per sq m per annum. In Utrecht, office prime rent is achieved in sub location Centre and has increased during 2016 to stand at 220 per sq m per annum. In Eindhoven, prime rent for office space remained stable at 175 per sq m per annum. The prime rent in Eindhoven is only applicable to the Kennedy Tower. The prime rent in Rotterdam amounts to 210 per sq m per annum. Some office buildings like De Rotterdam (Kop van Zuidas) and First (Centre) have higher asking rents. However incentives are still high and therefore the prime rent is expected to remain stable for the coming period. Prime rents in Rotterdam are applicable to the central station area and sub location Rotterdam Kop van Zuid. Investment market general update on dynamics per sector Dutch investment volumes have been quite volatile over the last decade. A new all-time record was achieved in 2007 when approximately 11.5 billion of investments transactions in commercial real estate were registered. Offices were accountable for 61% of the total investment volume then. A variety of portfolio transactions contributed strongly (approx. 20%) to the total investment volume. Due to the financial crisis, which started in 2008, the investment volume in the Dutch property started to decrease to 9.2 billion in After several subdued years, where investment volumes fluctuated around 5 billion per annum, the investment market showed a slight recovery in 2013 a 21% increase compared to The recovery of the Dutch investment market in 2013 was driven by the entry of international investors new to the Dutch market. Anglo- American investors in particular entered the Dutch market because of attractive market conditions and pricing. They either focused on large-scale portfolio transactions within the office and logistic sectors in order to acquire a platform in the market, or they bought singleasset hotels to add to their existing portfolio. This trend accelerated in 2014 and 2015 with 2015 investment volume surpasses historic peak volumes. New sources of capital entered the Dutch real estate investment market in recent years. Among others Asian investors made their first direct investment in Dutch real estate. Supported by new sources of capital, but also Dutch institutional capital, the total investment volume in the Netherlands amounted to approximately 11.6 billion in 2015, a new record s investment volume has come to 12.8 billion, which has set a new record high. Increased investment activity was driven by low interest rates and compared to other European countries relative attractive pricing. In addition, occupier markets start to recover as well. The recovery of investment volumes was predominantly driven offices and residential. Office investment activity generally accounts for, on average, 40% of total investment activity ( ). In 2014, office investment volume doubled and amounted to 3.9 billion. Due to the low interest rate environment and the expected recovery of the Dutch economy, foreign real estate investors entered the market or expanded their presence. In 2015, total office investments amounted to 3.84 billion, a figure which increased to its highest level since 2008 in 2016 with over 4.5 of office investments registered in File number: 11738

13 Amerikaweg 18 in Assen, The Netherlands Compared to a decade ago, when office investment activity was widely spread throughout the Netherlands, current activity ( ) is more focused on four biggest cities (G4). Since 2006 office investments in the G4 were accountable for 45% of total investment activity, 28% is related to nationwide portfolio deals and the rest related to locations outside the G4. Figure 4: Dutch investment volumes per sector ( Q4) Dutch investment volume per sector ( Q3) 14 in billion '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 YtD Office Industrial Retail Residential Hotel Mixed Other Source: JLL (2017) Retail investments Total retail investment volume in 2015 amounted to approximately 2.7 billion, an increase of 68% compared to the total retail investment volume of Retail investments in 2016 came to 1.9 million, down 28% y-o-y. Industrial investments The investment volume in 2015 amounted to approximately 1.5 million. In 2016 a total of approximately 1.4 million was invested in the retail warehouse sector, down 3% compared to Residential investments The total investment volume in the residential market amounted approximately 2.8 billion in In 2016 the residential investment volume stands at 3.2 million, up 15% to Confidence in the housing market is high due to a positive GDP-growth forecast and a continuing housing shortage and growing demand. 11 File number: 11738

14 Amerikaweg 18 in Assen, The Netherlands Office investments After several years of an office investment volume of approximately 1.5 billion a year, office investment activity doubled during 2014 and amounted to 3.9 billion. Due to the low interest rate and the forecasted recovery of the Dutch economy, especially foreign real investors entered the market or expanded their presence. In 2015 the total office investments amounted to 3.84 billion. As stated before, where 2014 was marked by large portfolio transactions, during 2015 mostly single-asset deals occurred. In 2015 the total office investments amounted to 3.84 billion. In 2016 the office investment volumed summed up above to 5.4 billion. The investment activity was the highest in Amsterdam and Rotterdam, 2.6 billion and 1.2 billion respectively.two large single asset deals occurred in Rotterdam: De Rotterdam ( 352 million) to Amundi and the new development First Rotterdam ( 133 million) to Union. In The Hague the office building De Monarch was also purchased by Amundi. Largest deal in Amsterdam refers to the Noma House at the Zuidas. CBRE GI purchased the yet to be built office building from development group SAX Vastgoed, Maarsen Groep and Beheer Brouwershoff. Also Syntrus Achmea sold two assets in Hoofddorp; Zuidtoren at Beukenhorst South, sold to Syntrus Achmea Real Estate & Finance, and the South Point Complex, sold to The Royal Properties Group (SebaldInvest). Largest portfolio deal refers to the sale of the Castor portfolio. The Asian investor/bank Anbang purchased the portfolio from Blackstone for 498 million. The second largest transaction was the Maxima Portfolio which was sold by Credit Suisse for 372 million to MCAP Global Finance. Another large portfolio transaction refers to the Zenith portfolio, comprising 182 million (20 offices). Figure 5: Office investment volume Q4 Office investment volume 8 in billion '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 Office YtD Source: JLL (2017) Due to increasing lack of prime product and increasing demand, prime yields sharpened over 2016 with 20 to 50 base points. In the second quarter of 2015 prime net initial yields in the Netherlands (Amsterdam) sharpened and amounted to a yield of 5.00%. In the fourth quarter of 2015 the prime yields sharpened further to 4.75% and tightened further to 4.25% in the fourth quarter of In other major office cities the net initial yields are 75 to 110 base points higher. Figure 6 shows the tightening trend on the office yields in all major Dutch cities. 12 File number: 11738

15 Amerikaweg 18 in Assen, The Netherlands Figure 6: Prime net initial yield development Q4 Yield 7.0% 6.5% 6.0% 5.5% 5.0% 4.5% Amsterdam Rotterdam Utrecht The Hague Eindhoven 4.0% Q4 Source: JLL (2017) 13 File number: 11738

16 Amerikaweg 18 in Assen, The Netherlands 5 Valuation Valuation method We have applied two valuation methods: the Capitalisation Approach and the DCF-method. For the result of these valuation methods we refer to the calculation Clarification of the Capitalisation Approach The Hardcore / Topslice method (HCT-method) is based on the capitalisation of the core income at full occupancy. Hardcore income is defined as the most secure income. When a property is over-rented, the (lower) rental value is used as core income. When a property is under-rented, the (lower) rent passing is used as core income. The core income (net of annual outgoings) is capitalised using a net yield. Adjustments for over-rent (topslice) and under-rent (reversion), if applicable, are made thereafter. For a topslice, the over-rent is discounted using a discount rate reflecting our view of the security of that income. In case of under-rent the difference between reversion and hardcore is capitalised using a net yield that is higher than the net yield on hardcore, as it has a different risk profile. These calculations are made for each tenant separately, in order to fully reflect the respective income risks. Finally several deductions are applied. In case of vacancy the estimated loss of rent, the re-letting costs, the cost of any incentives and repairs are deducted from the value. For all tenants the chance of vacancy at the end of the existing lease is assessed. Deductions are made for potential loss of rent, re-letting costs, incentives and repairs reflecting the chance of vacancy actually occurring. Any additional corrections made, such as corrections for ground lease interest, rent free periods, VAT-loss, annuities or overdue capital expenditures are deducted as a capital sum from the gross value DCF (Discounted Cash Flow) Approach We have built up a 15 year cash flow scenario. Cash flows for the relevant year are calculated as follows: The rental income at full occupancy (total cash flow) is first reduced by the annual outgoings, incurred by the landlord. Annual rents are inflated with reference to our estimate of the possible long term average for indexation, until a rent review is possible. At the expiry of the initial lease term we have estimated the probability of the tenant(s) vacating. This percentage is applied to calculate the weighted rent loss, letting and marketing fees, which are deducted from the cash flow. For the tenant renews scenario we have considered whether it is likely that the rent will be increased (or reduced if appropriate) to our ERV or whether the increase (or reduction if appropriate) will be limited to a certain percentage of the difference between the current rent and the ERV. The valuation model enables market rents to be inflated at a uniform rate until the third review (assuming that takes place 10 years after the first review) when an alternative rate can be applied. Finally non-operating costs such as incentives and repairs are calculated and deducted from the cash flow where appropriate. This results in a total net cash flow. Our growth assumptions are specified for rental income, rental value and outgoings in detail in the IRR -calculations sheet. Additional corrections are made, if appropriate, such as corrections for ground lease interests, rent free periods, VAT-loss, annuities or overdue capital expenditures. The present value of these are usually reflected in year 1 of the cash flow and specified in our calculation as additional costs. 14 File number: 11738

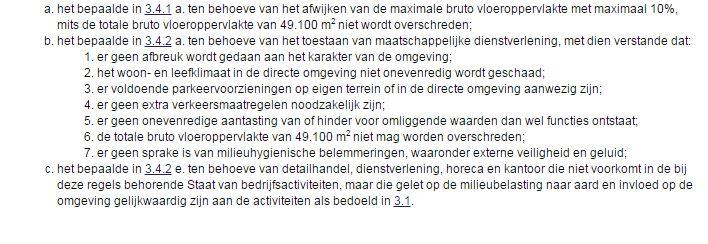

17 Amerikaweg 18 in Assen, The Netherlands An exit value and a gross yield at year 15 are shown on the IRR calculation sheet. The exit value is calculated based on the future income, starting in year 16. The exit value takes into account all the elements that are used for the cash flow for the first fifteen years. It is based on a fictitious cash flow for a further eighty-four years assuming no further growth. Using the discount rate that was applied to the cash flow for the first fifteen years, the result is the exit value. The resulting capitalisation rate is calculated from that value and our market rent inflated to year 16 with our assumed rates of market rental growth. By discounting the Cash Flows for years 1 to 15 and the exit value at the end of year 16 back to the valuation date, with the discount rate the gross value, as at the valuation date, is produced. The net value is calculated by deducting purchaser s costs for the property. The reported values are the rounded average from the two valuation methods. Marketability Lettability rating: Given the quality of the building, we have assessed the lettability as good, however the property is located on a secondary office location. In the immediate neighbourhood are a few available comparable properties on the market. In the valuation we expect a vacancy period of 12 months by lease expiry and 12 month s rent free to achieve a 5 year letting on market terms Saleability rating: The saleability of the freehold interest is good because of the long triple net lease. We expect that a sale could be achieved in 6 to 9 months. Given the characteristics of the property and the activity in the property market the most likely purchasers for this property will be (international) institutional investors and (local) investors. SWOT-analysis Fully occupied Single-tenant Strengths Good parking facilities Close to motorway Secondary location Weaknesses Opportunities Low vacancy rate in the area Overrented Threats 15 File number: 11738

18 Amerikaweg 18 in Assen, The Netherlands Comparables Rental references Property Tenant LFA Date /m 2 /Y Remarks Assen, Overcingellaan 13 Nidos Vluchtelingenhulp 337 Q Better location, inferior quality Assen, Nijlandstraat 151 Bierens en van Boven 620 Q Better location, inferior quality Assen, Dr. Nassaulaan 5 Ries ICT 165 Q Better location, inferior quality Hoogeveen, Elbe 2A TT Travel 378 Q Similar location, inferior quality Leeuwarden, Tesselschadestraat 29 Stichting Thuiszorg Het Friese Land Q Better location, inferior quality The comparables above are located in Assen, Hoogeveen and Leeuwarden. The first comparable is located in the centre close to the train station with good parking facilities. The quality is inferior to the subject property. The second comparable is also located in the centre along the ring road of Assen close to the train station with good parking facilities. The quality is inferior to the subject property. The third comparable is located in a luxurious area in the centre however the accessibility and quality are inferior to the subject property. The property in Hoogeveen is located on a business estate alongside the motorway A28 like the subject property and the A37 towards Emmen. The accessibility of this comparable is better but the building quality is inferior. The office at the Tesselschadestraat in Leeuwarden is located at Business Park Leeuwarden close to the train station and the city centre. We estimate the market rent for the subject property at 125 per sq m because this is a newly built property with good parking facilities, long lease term and view location from the motorway A Sale references Property Date LFA WALT Purchase price GIY Comments Assen, Amerikaweg 2 Q ,689 0, % Assen, Amerikaweg 16 Q ,609 1, % Located on the same estate, inferior letting situation and quality Located on the same estate, inferior letting situation and quality Assen, Mien Ruysweg 1 Q ,344 unknown 17,050, % Superior location, built to suit Amsterdam, Koivistokade 54 Q ,904 6, % Leiden, Zernikedreef 16 Q ,265 9, % Leiden, Zernikedreef 8 Q ,154 19, % Superior location, inferior because of the groundlease situation Superior location, inferior letting situation Superior location, superior letting situation The subject property is a built to suit property with a long remaining lease term of approx. 19 years. The comparables in Leiden are also offices with a long remaining lease term. However there is more competing space in the area of Leiden than in Assen. The property at the Zernikedreef 8 is a single tenant office and the property at the Zernikedreef 16 is a multi-tenant office. The comparable at the Mien Ruysweg 1 is located between the ringroad of and the motorway A28 in the western part of Assen. This property is also a built-tosuit property. The location is inferior to the subject property because this is not a primary office location in Assen. The comparables at the Amerikaweg are located at the same business estate as the subject property. Because of the inferior building quality and the unfavourable letting situation, the GIY s are higher. The property in Amsterdam is a fully occupied property. The Randstad area is superior to secondary office locations. Because of the ground lease situation, the subject property is better in terms of lease situation and because of the freehold. The subject property is newly built and has a better building quality compared to the above mentioned properties. The comparables in Assen are inferior because of the lease situation and the building quality. The property in Amsterdam is an inferior comparable because of the ground lease situation and the properties in Leiden are comparable in terms of a long Walt and the location on a business estate close to a motorway. We valued the property on a GIY on rental price of 7,28%. 16 File number: 11738

19 Amerikaweg 18 in Assen, The Netherlands Comments We are aware that the property has been sold at 30 December 2015 for a price of 5,650,000 The agreed fee between the client and JLL was fixed in advance The capitalization rates were derived from the market evidence The number of parking spaces increased from 75 to 96 spaces since last valuation, this amount is verified during the site visit The gross value is rounded Special assumptions The scope of the instruction as contained in the proposal has not been changed. During the site visit, the tenant informed us about the possibility to extend their space. At the valuation date, the process of building permissions were still going on. Therefore, we valued the subject property as is, based on the current situation. Back testing A valuation was also carried out for this property as at 5 February Other than changes to the annual outgoings and annual indexation of the rent, no significant changes have been made in this valuation compared to the previous valuation. The total market rent slightly increased because of the extra parking spaces compared to the previous valuation. The previous valuation was based on transfer costs of 1.00% as under the VAT regime. We note that the building was a new development in 2015 which has been, at the valuation date, in use for more than 6 months. Therefore, transfer tax would be payable on disposal today. In this valuation a 6% transfer tax is applicable. This is the main reason for the decreased net market value. The net market value decreased with 1.82% compared to the previous valuation. General Principles Our general principles can be found in appendix 1. These general principles apply to this valuation, unless specifically mentioned otherwise in this report. 17 File number: 11738

20 Amerikaweg 18 in Assen, The Netherlands Market Value We are of the opinion that the Market Value of the property, subject to the conditions contained in the report, was in the order of: Market value (gross) 6,370,000 (Six million three hundred seventy thousand Euros gross) Market value (net) 5,950,000 (Five million nine hundred fifty thousand Euros net) This value is reported on 16 March D.P.A. Diemel MSc MSRE Ms. C. Rampersad MSc RT Registered Valuer Registered with the NRVT under number RT File number: 11738

21 Amerikaweg 18 in Assen, The Netherlands APPENDIX 1 GENERAL PRINCIPLES File number: 11738

22 General Principles The valuation is subject to the general principles mentioned in this chapter, unless specifically stated otherwise. Carrying out the instruction Jones Lang LaSalle B.V., Valuation Advisory, has completed the valuation in accordance with the RICS Valuation - Professional Standards January 2014 (The Red Book) and the International Valuation Standards. Used data Information provided For the purposes of this valuation, we have assumed that all information provided by the client or third parties is correct. Furthermore we have assumed that there are no special conditions or circumstances which have not been included in that information, which could influence the valuation. Measurement For the purposes of this valuation, we have used the measurements provided by or on behalf of the client. Reporting date We have assumed that there are no material changes in circumstances between the date of inspection and the valuation date or vice versa or between the valuation date and the reporting date or vice versa. Letting details Where properties are valued with the benefit of lettings, it is assumed, that the tenants are capable of meeting their financial obligations under the lease and that there are no arrears of rent or undisclosed breaches of covenant. Property particulars Constructional and technical state Although in undertaking our inspection we believe that we have formed a fair and reliable opinion of the general state of repair of the premises, you will appreciate that we have only been able to concern ourselves with their condition insofar as it is likely to affect our valuation and insofar as we have been able to gain access to the various parts of the property. We have assumed the property to be free from structural and technical deficiencies.

23 If our valuation includes a property or a part of a property that has not been completed at the date of inspection, we have assumed that this property or part of a property has been or will be completed free from structural and technical deficiencies. If you wish for certainty regarding the constructional and technical state of the property, we advise you to consult an expert. Deleterious materials and pollution We do not normally carry out investigations on site to ascertain whether any buildings were constructed or altered using deleterious materials or techniques (including, by way of example, high aluminium cement concrete, wood wool as permanent shuttering, calcium chloride or asbestos). Unless we are otherwise informed, our valuation is on the basis that no such materials or techniques have been used. Jones Lang LaSalle B.V. accepts no responsibility in the event of chemical waste being located underground or indeed for the presence of other dangerous materials, foundation rests, explosives or other obstacles which may hamper the normal use of the building(s) or may react in an aggressive manner with materials used in the construction of the building(s). If there are any uncertainties with respect of the above, we would recommend that an investigation be undertaken, and, if any such material is found to be present in the construction, or any possible adverse ground condition is determined, we would wish the opportunity to reconsider our opinion. Sustainability In the event we are provided with an energy label certificate, EPC (energieprestatiecoëfficiënt) or a BREEAM, LEED or other similar certificate, we will reflect the general influence of sustainability issues in our valuation. Should you require an understanding on the sustainability of the building we advise you to consult an expert. Special conditions or restrictions For the purposes of the valuation we have not investigated the title deeds or the general or specific conditions in the ground lease or other restrictions or rights of third parties. We have assumed that these do not include any unusual or onerous covenants, outgoings, encumbrances or restrictions such as wayleaves and easements, or restrictions regarding use or transfer. Furthermore we assume the property is free of any mortgages or other charges that may be secured thereon. Specific advantages owner-occupiers In this valuation we have ignored possible specific advantages for certain owner/occupiers.

24 Legislation Regulations In carrying out this valuation we have assumed that, as at the valuation date, the property and the existing and future use of the property comply with all governmental rules and regulations. General and local regulations We have made informal enquiries by the Local Planning Authorities concerned, regarding planning consents, zoning, and Local Authority and highway schemes. We have assumed that the replies that we have received are correct. We have in all cases assumed that the uses to which the land and buildings are put are established uses for planning purposes and that all necessary town planning consents and byelaw approvals have been obtained, and that all other relevant statutory regulations have been complied with. If you want to be certain and gain details about the written regulations, we advise you to contact your legal advisor. Fiscal legislation For the purposes of this valuation we have taken no account of the effect of the changes to the VAT (BTW) legislation, nor in the changes to the provisions on property transfer and registration charges nor, of the introduction of legal measures intended to close loopholes in property tax legislation. In the event that VAT (BTW) is not paid, we have taken this into consideration when calculating the annual outgoings and possible renovation costs. If you require certainty on the possible considerable effects of changes in legislation on the value of the property, we advise you to contact your tax advisor. Revisions to landlord and tenant legislation In the valuation we have assumed that, when a lease expires, possible changes or improvements by the tenant do not influence the value of the property. Future changes in legislation In carrying out this valuation we have not anticipated any future changes in legislation. Material Previous involvement Jones Lang LaSalle B.V. confirms that the instruction has been carried out without any material previous involvement, other than for the current client.

25 Use and liability Report for exclusive use of client This report is exclusively intended for the client and may not be used in any form by third parties, be it in publications, circulars or articles intended for third parties, without the prior written approval of Jones Lang LaSalle B.V. Use for other purposes This valuation is intended for use by you or your organization for the purposes referred to in the report. We accept no liability for use of the report for any other purposes. Liability to third parties No responsibility is accepted by Jones Lang LaSalle B.V., to any third party for either the whole or any part of this report. Declaration Professional experience The Valuer has the knowledge, skills and understanding to undertake the valuation competently. Complaint handling procedure Jones Lang LaSalle B.V. has accounted for the eventuality that a client is dissatisfied with our performance. To this end we have adopted a Complaints Handling Procedure (the Procedure ) which accords with the guidelines provided by the RICS. A copy of the Procedure is available to you at your request. RICS standards Compliance with the RICS standards may be subject to monitoring under the institution s conduct and disciplinary regulations.

26 Amerikaweg 18 in Assen, The Netherlands APPENDIX 2 LAND REGISTRY File number: 11738

27 Kadastraal bericht object pagina 1 van 1 Kadaster Dienst voor het kadaster en de openbare registers in Nederland Gegevens over de rechtstoestand van kadastrale objecten, met uitzondering van de gegevens inzake hypotheken en beslagen Betreft: ASSEN Y Amerikaweg TK ASSEN 11:31:41 Uw referentie: CRA Toestandsdatum: Kadastraal object Kadastrale aanduiding: ASSEN Y 738 Grootte: 68 a 90 ca Coördinaten: Omschrijving kadastraal object: BEDRIJVIGHEID (KANTOOR) PARKEREN Locatie: Amerikaweg TK ASSEN Koopsom: Jaar: 2015 Ontstaan op: Ontstaan uit: ASSEN Y 726 ASSEN Y 724 Aantekening kadastraal object LOCATIEGEGEVENS ONTLEEND AAN BASISREGISTRATIES ADRESSEN EN GEBOUWEN Ontleend aan: ATG d.d Publiekrechtelijke beperkingen Er zijn geen beperkingen bekend in de Landelijke Voorziening WKPB en de Basisregistratie Kadaster. Gerechtigde EIGENDOM Assen Office B.V. Lange Voorhout EA 'S-GRAVENHAGE Zetel: 'S-GRAVENHAGE KvK-nummer: (Bron: Handelsregister) Voor de meest actuele naam, zetel en adres, raadpleeg het KvK-nummer. Recht ontleend aan: HYP /100 d.d Eerst genoemde object in ASSEN Y 738 brondocument: Aantekening recht DOORHALING KOOPOVEREENKOMST BW EN WVG Betrokken persoon: Volker Wessels Bouw & Vastgoedontwikkeling B.V. Reggesingel BA RIJSSEN Zetel: RIJSSEN KvK-nummer: (Bron: Handelsregister) Voor de meest actuele naam, zetel en adres, raadpleeg het KvK-nummer. Ontleend aan: HYP /69 d.d Einde overzicht De Dienst voor het kadaster en de openbare registers behoudt ten aanzien van de kadastrale gegevens zich het recht voor als bedoeld in artikel 2 lid 1 juncto artikel 6 lid 3 van de Databankenwet.

28 Uittreksel Kadastrale Kaart Uw referentie: CRA 725 Amerikaweg Afrikaweg Amerikaweg m 10 m 50 m Deze kaart is noordgericht Perceelnummer Huisnummer Vastgestelde kadastrale grens Voorlopige kadastrale grens Administratieve kadastrale grens Bebouwing Overige topografie Voor een eensluidend uittreksel, Apeldoorn, 24 januari 2017 De bewaarder van het kadaster en de openbare registers Schaal 1:1000 Kadastrale gemeente Sectie Perceel ASSEN Y 738 Aan dit uittreksel kunnen geen betrouwbare maten worden ontleend. De Dienst voor het kadaster en de openbare registers behoudt zich de intellectuele eigendomsrechten voor, waaronder het auteursrecht en het databankenrecht.

29 Amerikaweg 18 in Assen, The Netherlands APPENDIX 3 LOCATION PLAN File number: 11738

30 Amerikaweg 18 in Assen, The Netherlands File number: 11738

31 Amerikaweg 18 in Assen, The Netherlands APPENDIX 4 PHOTOGRAPH(S) File number: 11738

32 Amerikaweg 18 in Assen, The Netherlands File number: 11738

33 Amerikaweg 18 in Assen, The Netherlands File number: 11738

34 Amerikaweg 18 in Assen, The Netherlands APPENDIX 5 ZONING PLAN File number: 11738

35

36

37

38

39

40

41 Amerikaweg 18 in Assen, The Netherlands APPENDIX 6 VALUATION PRINTOUT File number: 11738

(incl.")

42 file prepared for Independent Committee property Office address Amerikaweg 18 inspection date city Assen - The Netherlands valuation date SUMMARY key figures property type Office main tenant PRA Group B.V. lettable floor area m² parking spaces 96 site area m² year of construction / refurbishment 2015 energy performance label unknown tenure freehold inflation 1,50% outgoings 10,74% 14 /m² theoretical gross rental income p.a. 162 /m² actual rental income p.a. 162 /m² market rent p.a. 133 /m² over-/underrented based on occupied areas 21,7% weighted average lease term (WALT) (incl. vacancy) 18,5 years vacancy rate 0,00% property rating (1 = negative, 5 = positive) cashflow valuation results building ground lease correction n.a. building quality 5 excellent building quality other additional corrections parking facilities 4 sufficient parking facilities WALT 4 long remaining lease term - hardcore/topslice-method property condition 4 good state of repair yield on hardcore 6,00% gross value HCT-method location net value HCT-method macro location 2 moderate macro location micro location 3 average micro location discounted cashflow-method lettability 3 average lettability IRR (internal rate of return) 6,45% investment market 3 average property market gross CF net CF gross value DCF-method marketability 3 average marketability net value DCF-method general comments SWOT analyses market value building strenghts weaknesses net initial yields (net income / gross value) fully occupied single-tenant net yield on RP 6,20% multiplier on RP 16,13 good parking facilities secondary location net yield on MR 4,99% multi plier on MR 20,04 close to motorway gross initial yields (gross income / rounded net value) gross yield on RP 7,28% multiplier on RP 13,74 gross yield on MR 5,98% mulitplier on MR 16,72 other opportunities threats low vacancy overrented gross market value /m² possibilities for extension undesirable location purchaser's costs 7,00% net market value /m² rounding net market value (rounded) file name: 11738b01 print date: page 1 of 6 Jones Lang LaSalle BV Valuation Advisory - taxversion ac

43 Independent Committee file property Office address Amerikaweg 18 city Assen valuation date TENANT DETAILS tenant unit rent passing VAT expiration m² m² m² m² # euro/m² euro/m² euro/m² euro/m² euro/# market rent years RP/MR (RP) Y/N date (MR) until euro office laboratory parking office laboratory parking euro exp. % 1 PRA Group B.V. A Y ,54 22% total ,54 22% occupied 100% ,54 22% vacancy 0% file name: 11738b01 print date: page 2 of 6 Jones Lang LaSalle BV Valuation Advisory - taxversion ac

44 Independent Committee file property Office address Amerikaweg 18 city Assen valuation date rent passing (RP) market rent (MR) management repairs insurance taxes ozb taxes waterschap sewerage others OUTGOINGS actual euro % of MR appl. Y/N estimated euro estimated as % of MR applicable outgoings as % of MR outgoings euro management - 0,00% N ,25% 1,25% repairs - 0,00% N ,00% 5,00% insurance - 0,00% N ,81% 0,81% taxes ozb - 0,00% N ,29% 3,29% taxes waterschap - 0,00% N ,33% 0,33% sewerage - 0,00% N 187 0,05% 0,05% 187 ground rent - 0,00% N - 0,00% 0,00% - others - 0,00% N - 0,00% 0,00% - others - 0,00% N - 0,00% 0,00% - total - 0,00% ,74% 10,74% file name: 11738b01 print date: page 3 of 6 Jones Lang LaSalle BV Valuation Advisory - taxversion ac

45 Independent Committee file property Office address Amerikaweg 18 city Assen valuation date ADDITIONAL CORRECTIONS ground lease correction ground lease correction applicable: Y/N N date of fictitious future pay-off (of ground rent) n.a. valuation date n.a. period until fictitious future pay-off n.a. years ground rent paid off: Y/N current annual ground rent n.a. n.a. NPV annual ground rent until fictitious future pay-off n.a. period ground rent paid off n.a. years actual (historical) pay-off premium n.a. per m² gross floor area n.a. annual growth land value current land value per m² gross floor area land value at date of fictitious future pay-off depreciation factor discount rate reserved for future pay-off n.a. n.a. n.a. n.a. n.a. n.a. n.a. for valuation purposes ground lease correction n.a. euro 0 additional corrections NPV VAT-loss for remaining lease periods, for tenants who do not pay VAT on rent 0 Triple net correction additional corrections euro total additional corrections income (+), outgoings (-) euro file name: 11738b01 print date: page 4 of 6 Jones Lang LaSalle BV Valuation Advisory - taxversion ac

46 Independent Committee standard variables total gross value file outgoings 10,74% total net value property letting fee + marketing 16,00% rounding Office management 1,25% total net value (rounded) address on RP on MR Amerikaweg 18 yield on topslice 7,00% net yield 6,20% 4,99% city yield on reversion NY+ 1,00% gross yield (net value) 7,28% 5,98% Assen discount rate corrections 7,00% multiplier 13,74 16,72 valuation date inflation 1,50% total m² HCT-METHOD purchasing costs 7,00% net value/m² (incl. pp) (hardcore - topslice method) tenant unit years until rent passing (RP) market rent (MR) NY on hardcore hardcore RP / MR appl. % on NPV topslice / initial void void 1st exp. appl. % on NPV void refurbishment and incentives / m² NPV costs NPV letting fee NPV additional value gross expiration capitalized TS/RV reversion void initial and initial 1st exp. at initial and and corrections 1st exp. 1st exp. 0 mnth 12 mnth 1st exp. marketing euro euro euro euro months months euro euro/m² euro/m² euro 16,0% euro euro 1 PRA Group B.V. A 18, ,00% % % total 18, file name: 11738b01 print date: page 5 of 6 Jones Lang LaSalle BV Valuation Advisory - taxversion ac

47 DCF 15 yrs escalation resultaat v.o.n Independent Committee standard variables outgoings euro HCT DCF file valuation date management 1,3% net value (k.k.) property inflation (IPD) 1,50% repairs 5,0% IRR 6,45% 6,45% Office MR growth 1&2 1,00% insurance 0,8% net yield on RP 6,20% 6,20% address MR growth 3&4 1,30% taxes ozb 3,3% gross yield on RP 7,28% 7,27% Amerikaweg 18 outgoings yr ,74% taxes watersc 0,3% multiplier 13,74 13,75 IRR-CALCULATIONS year 1-10 IRR-CALCULATIONS year 1-15 city outgoings yr ,27% sewerage 0,1% 187 total m² net value end year net value end year Assen growth on outg. 1,75% others 0,0% 0 result net value (incl. pp)/m² market rent market rent letting + marketing 16,00% total 10,7% gross yield on MR 7,3% gross yield on MR 9,2% appl. MR: income period: income period: tenant RP MR yrs until 1st 2nd 3rd 4th expiration rev rev rev rev 1 PRA Group B.V. A ,54 50% n.v.t. n.v.t. n.v.t total cashflow , outgoings potential void period months void % 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% loss of income marketing letting fee refurbishment and incentives in euro/m² refurbishment and incentives in euro/m² FV additional costs additional costs FV total (repairs) total net cashflow file name: 11738b01 print date: page 6 of 6 Jones Lang LaSalle BV Valuation Advisory - taxversion ac

48 Amerikaweg 18 in Assen, The Netherlands APPENDIX 7 TRACK RECORD File number: 11738

49 Track record Education Daan has a Masters degree in Real Estate from the Amsterdam School of Real Estate Sector Specialism(s) Client Service and offices, industrial, retail and residential valuations Daan Diemel MSc MSRE Associate Director Experience Daan is part of the Dutch Valuation team of JLL since 2006 and is responsible for portfolio acquisitions. He conducts valuations for major national and international real estate clients. Daan has experience in valuations of all types of properties. Regular valuation work includes the portfolios of CBRE Global Investors, Altera, NSI, Syntrus Achmea Real Estate & Finance, Deutsche Bank, ABN AMRO, and ING Bank. References Offices Retail - and parking 6

50 Track record Education Chaya has a Masters degree in Control from the University of Amsterdam and is a registered valuer in the Dutch register (NRVT) Sector Specialism(s) Office, industrial, retail, healthcare and residential valuations Chaya Rampersad MSc RT Junior Valuer Experience Chaya is part of the Dutch Valuation team of JLL since She conducts valuations for major national and international real estate clients. Chaya has experience in offices, retail, industrial and residential valuations. Regular valuation work includes portfolios of Altera, Syntrus Achmea Real Estate & Finance, NS Stations, Deutsche Bank, ABN AMRO, ING Bank and Geneba. References Offices Retail - and parking 6

51 JLL Daan Diemel Associate Director Valuation Advisory Strawinskylaan ZX Amsterdam Postbus AE Amsterdam +31 (0) JLL Chaya Rampersad Junior Valuer Valuation Advisory Strawinskylaan ZX Amsterdam Postbus AE Amsterdam +31 (0) JLL Nabila Zejli Team Assistant Valuation Advisory Strawinskylaan ZX Amsterdam Postbus AE Amsterdam +31 (0) COPYRIGHT JONES LANG LASALLE IP, INC This publication is the sole property of Jones Lang LaSalle IP, Inc. and must not be copied, reproduced or transmitted in any form or by any means, either in whole or in part, without the prior written consent of Jones Lang LaSalle IP, Inc. The information contained in this publication has been obtained from sources generally regarded to be reliable. However, no representation is made, or warranty given, in respect of the accuracy of this information. We would like to be informed of any inaccuracies so that we may correct them. Jones Lang LaSalle does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication.

52 Valuation Report MRP Investments Ltd. Cartograaf 3 in Duiven, The Netherlands File number: 11739

53 Cartograaf 3 in Duiven, The Netherlands Contents 1 Preliminary Notes... 1 Valuation Instruction... 1 Definition of value... 1 Purpose of valuation... 1 Type of valuation... 2 Date of Valuation... 2 Instruction letter... 2 Inspection... 2 JLL Valuation Advisory... 2 Requirements regarding the valuer s Independence... 2 Sources of Information Physical Considerations... 4 Letting details... 4 Brief property description... 4 State of repair... 4 Accommodation... 4 Location and accessibility... 5 Sustainability Legal Considerations... 6 Land registry... 6 Real rights... 6 Town planning Market Considerations... 7 General... 7 Retail indicators... 7 Supply... 8 Take up... 9 Rental level Investment market Valuation Valuation method Marketability SWOT-analysis Comparables Comments Special assumptions Back testing General Principles Market Value Appendices Appendix 1 General Principles Appendix 2 Land Registry Appendix 3 Location Plan Appendix 4 Photograph(s) Appendix 5 Zoning Plan Appendix 6 Valuation Printout Appendix 7 Track Record

54 Cartograaf 3 in Duiven, The Netherlands 1 Preliminary Notes On 17 January 2017 MRP Investments Ltd. assigned JLL per by Mr. A. Fishman to perform a valuation of the four properties from the DW01 Portfolio situated at Spoorsingel in Heerlen, Cartograaf 3 in Duiven, and Amerikaweg 18 in Assen - The Netherlands, as at 31 December 2016 for the purpose of estimating the fair value of the subject property in compliance with IFRS 13. In this report you will find the specifics and grounds on which we base our valuation for the property in Duiven. Enclosed you will find the accompanying calculation. We hereby consent to the inclusion and attachment of the valuation report of Cartograaf 3 in Duiven, dated 14 February 2017 with 31 December 2016 as the valuation date, which was prepared for the Company and which may be attached to its 2016 annual financial statements and/or any reports which, pursuant to the laws and regulations of the state of Israel, may be filed with respect to thereof. We hereby empower the authorized representatives of the Company to report the valuation report to the Israeli Securities Authority and Tel Aviv Stock Exchange. Valuation Instruction JLL, Valuation Advisory, with offices in Amsterdam on the Strawinskylaan 3103, declares, to have surveyed and valued the freehold interest of a parcel of land with a retail warehouse, situated at Cartograaf 3 in Duiven The Netherlands Definition of value Market value: Market rent: The estimated amount for which an asset or liability should exchange on the valuation date between a willing buyer and a willing seller in an arm's-length transaction after proper marketing and where the parties had each acted knowledgeably, prudently and without compulsion. The estimated amount for which an interest in real property should be leased on the valuation date between a willing lessor and willing lessee on appropriate lease terms in an arm s length transaction, after proper marketing and where the parties had each acted knowledgeably, prudently and without compulsion. The above stated definition of market value is in accordance with the International Financial Reporting Standards, the International Valuation Standards and the Standards of the Royal Institution of Chartered Surveyors. The valuation was requested to support the value of the four assets in the DW01 Portfolio which is listed on the Tel-Aviv Stock Exchange. This valuation is in compliance with IFRS 13 and the International Valuation Standards (IVS). Purpose of valuation We understand that the valuation is required for accounting purposes. The client holds the property as an investment. 1 File number: 11739

55 Cartograaf 3 in Duiven, The Netherlands Type of valuation The instruction involves a re-valuation. Date of Valuation We have adopted 31 December 2016 as the valuation date. Instruction letter This valuation is carried out in accordance with the fee proposal. The depth of work is maintained as set out in the fee proposal. Inspection The property was inspected by D.P.A. Diemel MSc MSRE and mw. C. Rampersad MSc RT on 25 January JLL Valuation Advisory All our valuations are based on internationally acknowledged guidelines and comply with local rules and legislation. Our employees have a high degree of specialization. JLL is recognized as Firm Regulated by RICS. Highly experienced, ISO-certified valuation team One central Amsterdam-based team One team one vision: consequent and consistent Regional approach, good local market knowledge Valuations in accordance with the RICS guidelines and the International Valuation Standards Valuations in accordance with the recommendations of NRVT Vast experience with IPD/ROZ and IPD/aeDex valuations Valuations across the Netherlands and support with European assignments 3,500 valuations per annum with a total value of 45 billion Working according to the four eyes principle High degree of accuracy and reliability Thorough analysis of the available data Intensive contact and consultation with the client Clear time planning Handling with agreements and deadlines in the right way Transparent calculations and reports Stringent requirements on ethical aspects Chinese Walls The properties are valued by Daan Diemel, who has experienced a specialized real estate education at the Amsterdam School of Real Estate (ASRE). Daan is involved by the Valuation Team for 10 years and is experienced in the valuations for all types of real estate. Second valuer is Chaya Rampersad, she has a master in Accountancy and Control and is registered in the Dutch Register for Commercial Real Estate. She is involved in all types of valuations for JLL for almost 3 years. Daan Diemel and Chaya Rampersad valued similar portfolios and single assets for national- and international clients. A track record is attached in Appendix 7. Requirements regarding the valuer s Independence Both the IVS code of ethics and the JLL code of ethics contain conditions on how professionals must conduct themselves when having financial interests in clients. It is forbidden (hidden interests and the code of conduct) for JLL employees to have financial interests in property related companies or businesses or to invest directly in property. 2 File number: 11739

56 Cartograaf 3 in Duiven, The Netherlands JLL is not financial dependent on carrying out this specific valuation instruction. Both JLL VA s annual turnover and the total income earned from other JLL services provided to a single client, including any client s related businesses entities, are less than 25% of total turnover. The fee which JLL VA receives for this valuation work is not dependent on the value(s) reported in the valuations. The valuer does not, by carrying out the instruction, envisage any threat to independence or objectivity and concludes that no additional measures are needed to be able to accept the instruction. JLL adopts Chinese Walls which prevent information being exchanged between departments within the organization. Sources of Information In preparing this valuation report, we have relied on the following information: Information Measurement certificates (NEN 2580) or RICS measurement code of practice Requested from MRP Investments Ltd. Architectural scaled drawings MRP Investments Ltd. N Recent rent roll MRP Investments Ltd. N Provided Y (examined) / /N Y Details No comments Lease agreements MRP Investments Ltd. Y No comments Allonges, addenda and side letters MRP Investments Ltd. n/a Title deeds MRP Investments Ltd. N Ground lease (terms and conditions) MRP Investments Ltd. n/a Freehold Cadastral plan and Land Registry extract Land Registry Y No comments Zoning plan ( bestemmingsplan ) ruimtelijkeplannen.nl Y No comments Overview of technical building installations MRP Investments Ltd. N Overview of property charges, such as property tax, water rates and sewage charges MRP Investments Ltd. Maintenance forecast MRP Investments Ltd. N Overview of historical building costs MRP Investments Ltd. N Fire insurance report MRP Investments Ltd. N Environmental impact report (soil pollution / hazardous substances) MRP Investments Ltd. Energy label certificate MRP Investments Ltd. N Other relevant information: MRP Investments Ltd. N We assume that all information obtained from or on behalf of the client is correct and complete. The valuer has as far as possible considered the plausibility of the information provided. Should it appear (or a strong suspicions arise) that the information provided is not complete and/or incorrect, that will be commented on in this report. This also applies where the valuer has adopted information other than that in the information provided. N N 3 File number: 11739

57 Cartograaf 3 in Duiven, The Netherlands 2 Physical Considerations Letting details Based on the lease agreement provided by MRP Investments Ltd. we understand that the property was as at the valuation date rented under the following terms and conditions: Tenant: Mediamarkt Saturn Holding Nederland B.V. Rent Passing: 608,923 Start Date: 30 October 2014 Expiration Date: 30 October 2024 Option Period: 5 years Indexation: Every year according the CPI index Further Details: Standard Dutch ROZ contract. The tenant has the right to sublet the space. Brief property description Year of construction: 2015 Renovation (year): n/a Description renovation: n/a State of repair good Number of floors two floors Foundation steel foundation Main bearing structure steel structure Floors carpet floors Roof flat roof with parking on top Walls aluminium panel facades with company branding on it Frames aluminium window frames fitted with double glazing Systems sprinkler system Number of parking spaces 160 roof parking spaces and 30 on-site parking spaces Parking ratio (per m² BVO) 1:27 State of repair At the time of our inspection the general state of repair could be described as good as the property is recently built in Accommodation The total lettable floor area amounts to 4,719 sq m, as contained in the measurement certificate conform NEN, dated 12 November For a breakdown of the lettable floor areas and other details we refer to our valuation printout. 4 File number: 11739

58 Cartograaf 3 in Duiven, The Netherlands Location and accessibility Duiven is a small city located in the East of the country in the province Gelderland. Duiven is located at approximately 10 kms distance from Arnhem and approximately 30 kms distance from Nijmegen. Duiven is located alongside the A12 motorway towards Utrecht. There are three main business estates in Duiven. The subject property is located at the mixed use business estate Centerpoort-Nieuwgraaf. Occupiers of this estate include: Ikea, Praxis, Makro and Leenbakker. The accessibility by private transport is good via the A12 motorway. There are sufficient parking spaces available on the rooftop and on-site. The property is also accessible by public transport. The closest bus stop is located at 5 minutes walking distance. The bus stop connects to the train station Westervoort, which is located at approx. 2,5 kms distance. Sustainability The client has no information available concerning the energy label or other sustainability matters for the property. We have assumed that the property is sufficient sustainable as the property is recently built. 5 File number: 11739

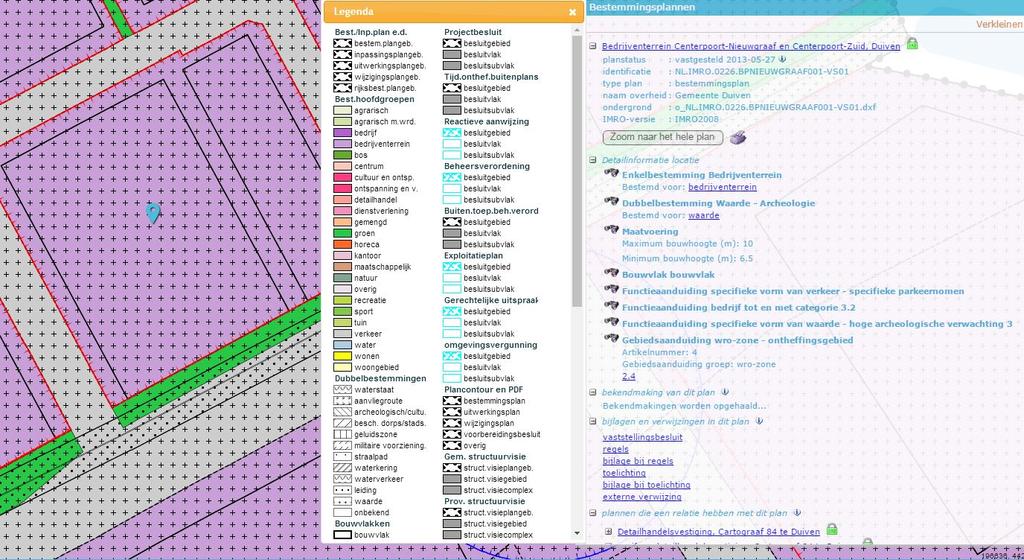

59 Cartograaf 3 in Duiven, The Netherlands 3 Legal Considerations Land registry The local Land Registry ("Kadaster en Openbare Registers") informed us that on 24 January 2017 the property was registered as follows: Municipality: Duiven Section: F Number 2022 Estimated area: 51 a (5,100 sq m) Description: Business (office) parking We understand from the local Land Registry that on 24 January 2017 the freehold was owned by Duiven Retail B.V. The parcels F 2150 and F 2151 are located at Cartograaf behind the property and have a collective common ownership. Real rights National monument: Pre-emption law ( Wet Voorkeursrecht gemeenten ): Restrictions: Recordings in land registry extract: Not applicable. Not applicable. No restrictions recorded in the land registry extract. No comments recorded in the land registry extract. Other special rights: For the purposes of this valuation the valuer has not carried out a detailed investigation on title. Based on the valuer s professional assessment there is no reasonable reason to assume that there are any rights or impediments in the relevant deed(s) which effect the value reported. In determining the market value the valuer has assumed that there are no rights or impediments which effect the value reported. Town planning We understand from the municipality of Duiven, that the property falls within the zoning plan ( Bestemmingsplan ) Bedrijventerrein Centerpoort-Nieuwgraaf en Centerpoort-Zuid, Duiven. The Municipal Council approved the plan on 27 May The zoning plan allocates the property for Business ( Bedrijventerrein ) purposes. This includes business and retail uses. The property is subject to a maximum height of 10 m and a maximum site coverage ( bebouwingspercentage ) of 100%. We understand that the current use conforms with the provisions of the zoning plan. 6 File number: 11739

60 Cartograaf 3 in Duiven, The Netherlands 4 Market Considerations General The total current retail stock in the Netherlands amounts to approximately 31.1 million sq m, distributed over 235,600 retail selling points (reference date January 2017). Table 1: Occupier market Q4 Occupier market Historical Present Forecast Unit 2013 Q Q Q Q4 2016/2017 Total stock sq m, in millions Daily sq m, in milllions Non-Daily sq m, in millions Source: JLL (2017). Retail indicators The consumer s confidence in the first quarter of 2016 amount to 1 and increased in the second and third quarter to 5. The consumer s confidence increased even further and by the end of 2016 consumers confidence amounted 10. As a result of the shrinking Dutch economy and the increasing unemployment rate, people tend to spend less money. But numbers show that consumers are starting to have more confidence in the Dutch market again. Retail sales have slightly increased in the first quarter of 2016 to 1.8% and fluctuated during In December 2016 retail sales amounted to 7%, a large increase compared to the beginning of Research shows an increase in consumers confidence and willingness to pay, however this doesn t necessarily lead to more consumption. Willingness to pay increased in Where it amounted in January 2015 at -5, this increased to -2 in April. In the third and fourth quarter of 2015 willingness to pay fluctuated slightly from -1 in August to -2 in December. Willingness to pay has increased slightly and amounted -1 medio July Currently the willingness to pay indicator amounts to 3. In addition to falling turnover levels, the Dutch retail market is structurally impacted by the strong growth of online sales. Online sales rose from 12.7 billion in 2013 up to 13.7 billion in 2014 (thuiswinkel.org), which is a growth of almost 8%. Current online retail sales amounts to approximately billion. To maintain an acceptable profit margin, retailers are focused on optimization and consolidation of their store portfolio, including disposal of underperforming stores, renegotiation of rents and right-sizing units. Although limited, new store acquisitions are focused on the right size unit, in the best location, at the best price. Not surprisingly, the Dutch retail market witnessed a polarization between prime retail locations, which mainly consist of the inner-city shopping areas of the 10 largest cities, and the secondary/tertiary retail locations. In particular small and medium-sized municipalities witnessed a decline in footfall and level of purchases. 7 File number: 11739