INCOME APPROACH. Direct Cap! Yield Cap! Rate Relationships

|

|

|

- Leona Darlene Russell

- 6 years ago

- Views:

Transcription

1 INCOME APPROACH Direct Cap! Yield Cap! Rate Relationships

2 Chapter 46 Operating Statements & Reconstruction Overview The following are financial statements for income properties. " statement " Balance sheet " Cash flow statement " Rent roll " Capital expenditure plan " Projected budgets In addition, an appraiser could benefit from " Leases " Environmental & structural reports " Plans & specifications " Cost information " Current & past contracts on the property " Any listing information " HUD statements from any sales of the property " Title policies Financial statements are a way to keep score in a business. They also serve as the starting point for many financial and management decisions. In addition, financing is easier when financial statements are healthy. Bankers look at the following statements when considering an applicant for a loan. Effective managers periodically look at the statements of a firm to adjust to market conditions. Financial statements should also be compared to industry averages. Often managers of companies find that there income statement looks healthy, their balance sheet looks acceptable, but they never seem to have enough cash to pay bills as they come due. Cash flow is often a problem when the average length of time to collect receivables is longer than average time of payables. Cash flow can be improved by extending payables and/or by shortening average collections. Cash flow is particularly a problem during expansion. Especially when employees are paid by salary or on a draw basis. Additionally, growing firms must pay for additional lease space, equipment, other capital expenditures and training. However, it is generally a long time before a new employee is productive with his/her first billings. Working capital is money needed in a firm to pay bills as they come due. Although working capital is used to pay short-term debt, it is a long-tern investment. For example, if a new firm has 60 days of bills that total $30,000 and no collections. The amount of $30,000 is needed to start the business. Once money comes in, a portion of the owner's salary or profit can be used to payoff the debt created by the gap. Otherwise, a continual 2"

3 line of credit to pay bills may be established and the firm pays interest on the debt. As the firm expands additional working capital is needed. A large firm may have as much as $100,000 in working capital that is engaged either through debt or equity. The working capital may be recovered through closing the firm, a sale of the firm, or some by contraction. The analysis of the effect of expansion or contraction begins with the following financial statements. The owner who submits financial statements should be careful to insure accurate reporting of their financial position. It is important to be accurate in your projection of statements to a financial institution because it is a federal crime to submit false documents when making application for a loan. The income statement and cash flow statements may be derived based upon historical income and expenses from the firm or as a pro-forma statement. A pro-forma statement is a projected statement for a defined period of time. In setting profitability goals the manager should develop a pro-forma statement and periodically. Balance Sheet A balance sheet is the summary of assets, liabilities, and net worth as of a given point in time. The assets and liabilities are usually divided into current and long-term. Current assets and liabilities are either paid or collected within one year of the balance sheet date. Net worth is simply the difference between assets and liabilities. Net worth is overstated for liquidity if transaction costs to sell assets are not considered. Assets can come from borrowing, ownership contributions, and from retained earnings. These are also defined as borrowed capital, contributed capital and earned capital. Assets are both tangible and intangible resources available to a business. Liabilities are financial obligations of a business. Liabilities include notes payable, accounts payable, unpaid taxes, etc. 3"

4 Balance Sheet Business Personal Assets: $ Assets: $ 1. Cash on hand $ 1. Cash on hand $ 2. Cash in bank $ 2. Cash in bank $ 3. US government securities $ 3. US government securities $ 4. Other marketable securities $ 4. Other marketable securities $ 5. Notes receivable $ 5. Notes receivable $ 6. Accounts receivable $ 6. Accounts receivable $ 7. Other liquid asset $ 7. Other liquid asset $ 8. Other liquid asset $ 8. Other liquid asset $ TOTAL CURRENT ASSETS $ TOTAL CURRENT ASSETS $ 9. Real estate owned $ 9. Real estate owned $ 10. Mortgages owned $ 10. Mortgages owned $ 11. Contracts owned $ 11. Contracts owned $ 12. Notes & accounts receivable $ 12. Notes & accounts receivable $ doubtful doubtful 13. Notes - Friends/family $ 13. Notes - Friends/family $ 14. Other securities $ 14. Other securities $ 15. Furniture, fixtures & equipment $ 15. Furniture, fixtures & equipment $ 16. Automobiles $ 16. Automobiles $ 17. Other asset $ 17. Motorcycles, boats, recreational, $ etc. 18. Other asset $ 18. Other asset $ 19. Other asset $ 19. Other asset $ 20. Other asset $ 20. Other asset $ TOTAL LONG-TERM ASSETS $ TOTAL LONG-TERM ASSETS $ TOTAL ASSETS $ TOTAL ASSETS $ Liabilities: $ Liabilities: $ 1. Notes due banks $ 1. Notes due banks $ 2. Notes due relatives/friends $ 2. Notes due relatives/friends $ 3. Notes due others $ 3. Notes due others $ 4. Accounts & bills payable $ 4. Accounts & bills payable $ 5. Unpaid federal income taxes $ 5. Unpaid federal income taxes $ 6. Unpaid state & local taxes $ 6. Unpaid state & local taxes $ 7. Interest & other payments due $ 7. Interest & other payments due $ 8. Any other past dues $ 8. Any other past dues $ 9. Other short-term liability $ 9. Other short-term liability $ 10. Other short-term liability $ 10. Other short-term liability $ 11. Notes due on real estate $ 11. Notes due on real estate $ 12. Credit card balances $ 12. Credit card balances $ 13. Contingent debt $ 13. Contingent debt $ 14. Other liabilities $ 14. Other liabilities $ 15. Other liabilities $ 15. Other liabilities $ 16. Other liabilities $ 16. Other liabilities $ TOTAL LIABILITIES $ TOTAL LIABILITIES $ NET WORTH $ NET WORTH $ (Assets minus liabilities) (Assets minus liabilities) 4"

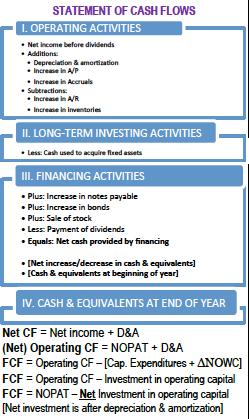

5 Statement An income statement is the summary of revenues and expenses over a specified time period. The balance sheet is a summary of assets and liabilities at a specified time, but the income statement is a summary of money in and out over a beginning and ending time period, usually one year. The income statement may also include non-cash transactions such as depreciation write-off. Revenues minus expenses indicate profit or loss. A proforma income statement is a projected statement of revenues and expenses. INCOME-STATEMENT 2015 REVENUES Rental+and+other+property+revenues $11,160,000 Other+income $200,000 Total&Revenues $11,360,000 OPERATING-EXPENSES Fixed&Expenes Property+taxes $1,300,000 Insurance $250,000 Total&Fixed&Expenses $1,550,000 Variable&expenes Management $568,000 Cleaning $400,000 Utilities $450,000 Salaries+&+wages $465,000 Services $110,000 Security $200,000 General+and+administrative $425,000 Repairs,+maintenance+and+supplies $650,000 Total&Variable&Expenses $3,268,000 Total&Operating&Expenses $4,818,000 NET-OPERATING-INCOME $6,542,000 Cash Flow Statement A cash flow statement shows sources and uses of cash. The source of cash may be other than from income, such as a loan. The use of cash is actual cash out and would not include non-cash transactions, such as depreciation write-off. The beginning and ending cash flow balance must agree with the cash flow balance stated on the balance sheet. Also, the net income from the income statement is the beginning figure for cash flows from operating activity used on business cash flow statements. While the income statement may recognize an expense based upon accrual, the cash flow statement recognizes uses of cash when paid out. 5"

6 6"

7 The appraiser must know the basics of financial statements to reconstruct an operating statement that would be used as the basis of the income approach. The income used could be any of the following. 1. The past year s performance. 2. The current rent roll and expenses annualized. 3. A projection of the next year s income. 4. A stabilized projection of the next year s income. 5. A projection of the next year s income after an assumed renovation or repair of the property. 7"

8 6. A projection based upon normalizing rent and/or expenses based upon the appraiser s estimate of what competent management would consider reasonable. 7. An income projection with or without reserves, tenant improvements & leasing commissions. The appraiser should project the income statement based upon the market. (However, some markets lack a consistent way to develop a projected income statement.) Many market participants buy properties based upon the year before performance and not on a projected income statement. This does not violate the theory of anticipation. The anticipation is built into the capitalization rate instead of the income. One market participant remarked I m not paying them for my expertise. I expect to increase the net income, but am paying for the property based upon what they were able to do. Many appraisal courses teach to use a projected income statement for the subject. Then the appraiser is instructed to force that upon their sales information. It would be preferable to see if there is a consistent way the market projects the income statement, then do the same for the subject. For example, if the sales show a consistent capitalization rate based upon projected income that does not include reserves, leasing commissions and tenant improvements, then do the same with the subject. If there is a more consistent capitalization rate with the reserves, leasing commissions and tenant improvements above the line, then put those categories into the calculation of net operating income. The point is to derive this from the market. A number of services providing yield and capitalization rates were surveyed. Some respondents put tenant improvements and leasing commissions above the line and some include the expenses below the line. Above the line means the categories are included as an expense line before net operating income is calculated. Below the line means the expenditures for tenant improvements and leasing commissions are not used in the calculation of net operating income. 8"

9 Chapter 47 Projecting Cash Flows & Reversion Overview Appraisers must project cash flows and reversions based upon the market. The appraiser should never guess what the future cash flows will be. Instead, the appraiser s role is to use today s expectations of future cash flows in the models used by the appraiser. The following are terms used to describe different types of income. Cash flows are developed vertically from potential gross income to net operating income (or pre-tax or after-tax cash flow) or horizontally over time. Cash flow development is necessary as a part of direct capitalization as well as yield capitalization. An appraiser often begins the development of the net operating income from actual history of the subject property. The actual income from the subject can be studied when 9"

10 developing fee simple income. However, the income cannot be used except as a comparable or a leased fee analysis will result. Developing Year One Cash Flow An appraiser must develop income projections based upon the assignment conditions given the appraiser. The following are a minimum instruction set that an appraiser must be given by the client before proceeding. 1. The value definition 2. The interest to be appraised 3. The date of value 4. The property. This is not only the legal description or description of the property but also the tangible and intangible property the appraisal would or would not include. The appraiser must understand the relationship between fee simple and leased fee interests. The fee simple interest is the valuation of property usually assuming competent management and therefore market rent and market occupancy. The leased fee interest is the owner s interest in leased property. The appraiser may use the leases in place as a rent comparable for fee simple valuations, but must not process the leases in place when conducting a fee simple valuation. The following illustrates the relationship between the fee simple and lease fee interests, depending upon the market and contract rents. In a rising markets, office an retail usually lag and the leased fee values are usually lower than the fees simple values. This is reversed in a soft market. In a stable market the values can be the same. When fee simple value is equal to leased fee value the numbers may be the same, but the concepts are not. When the tenant(s) are paying market rent the leased fee value is equal to the fee simple value. There is a leasehold estate (the tenant s interest in leased property) but the value of the leasehold estate in that example would be zero. However, there could be a negative or positive value in the following year if the tenant is paying above or below market rent. 10

11 Developing cash flows from comparable properties or from the subject should be consistent with the application of the rate. The following are potential ways to develop net operating income, yet neither is a correct way. The appraiser must be consistent in the development with the rate derived from the market. In fact, it is reasonable to develop a rate from the market consistent with market actions and then develop the income stream for the subject that is consistent with the rates given. For example, a tight range of capitalization rates may be derived from sales using historical (one-year) before incomes and from incomes that do not include an allowance for replacements. If such rates are developed they should be applied to the subject income both historically derived and without replacements in the income stream used to capitalize to value. This would seem to violate the principal of anticipation. This principal states that the investor purchases based upon expectations in the future. This is always true. However, if the increase, decrease or stable income is not reflected in the income projected it is embedded in the rate. The capitalization rate derived on historical incomes has the expectations built into it. Furthermore, investors know they have to replace worn out or functionally deficient items. The allowance is either reflected in the income stream or in the rate. The typical investor omits an allowance. However, many lenders require the use of an expressed allowance for replacements either per unit, as a percentage of some income (EGI), per square foot, etc. The following are potential ways income can be developed. # Anticipated income for the next year (always appropriate for cash flow modeling, but not necessarily for direct capitalization.) # Historical income for the year preceding (used when the market buyer s base purchases on what the previous owner accomplished and not what the buyer expects to have in performance.) # Current income annualized. # With and without reserves. 11

12 # With and without repairs and other curables. # Actual occupancy or stabilized or some other occupancy. # ETC., ETC., ETC. So what is the bottom line? You must be consistent with the derivation of income and match it to the kind of rate used. An appraiser often has to take out inappropriate expenses. The expenses are not necessarily inappropriate to the investor, but the appraiser is attempting to come to a generic income that applies regardless of particular management style, tax bracket, ownership entity, debt arrangements, or other expense related not to the property, but to the particular investor. For example, a business trip to Hawaii for a convention may be a legitimate and even prudent deduction for the investor, but an appraiser may adjust the statement by taking this expense out and thus increasing Io. Capital expenditures are smoothed out by taking capital expenditures out of expenses but reflecting a smoothedout outlay of capital expenses by expressing them in an allowance of replacements. (Of course this assumes the allowance is not already expressed in the overall rate being used to process the income stream. The overall rate can express the allowance when the income stream in the comparables is on the top of the fraction and the bottom of the fraction is value or price. The income would be overstated by leaving out the allowance. Therefore, the overall rate developed would be too high to use on a comparable property where an allowance for replacements is taken out of the income. The following is an example. Example: A comparable property identical to the subject in all respects sold for $600,000 and has the following income statement. PGI $100,000 Vacancy (5,000) EGI $95,000 Operating expenses (30,000) Replacements (5000) Io $60,000 The overall rate for the property is 60,000/600,000 or 10% with an allowance for replacements included in the income stream. The overall capitalization rate for the property is 65,000/600,000 or % without an allowance for replacement included in the income stream. If the subject has the identical income and the appraiser uses the $60,000 and the % overall capitalization rate, the appraiser would double-count the allowance for replacements. The value would indicate $60,000/ = $553,850 (R). It should be noted the difference between the two overall capitalization rates is or.833%. The percentage times the value $600,000 x.833% = $5,000. The loading of the rate for the allowance can easily be seen with this example. It also shows why the allowance should not be double-counted. The following is a partial list of inappropriate expenses. # Depreciation # taxes (Credits may be allowed below the line if related to the property) # Tax abatements (The present value may be added back) # Debt service (Principal & interest) # Entity expenses (Corporation, partnership trust, etc.) # Capital expenses (Except as reflect in allowance for replacements) 12

13 # Travel expenses (Some related directly to the property could be alright) # Business expenses (Related to the business and not the real estate) # Excessive expenses (These would be the correct category, but are not within market guidelines) The following are ways to estimate allowance for replacements. # Per unit (# units x $per unit for replacements) # Per square foot (square foot x $ PSF for replacements) # As a percentage of effective or potential gross income ( x % set aside for replacements) # By dividing the cost of a replacement item by the useful life (straight-line, this assumes the increase in the cost of the item is offset by money that can be earned from investing the funds) # By multiplying the cost of a replacement item by the sinking fund factor for the useful life of the item (This assumes either (1) the money could be set aside growing interest, (2) the cost of the item used is the anticipated cost in the future and this gives credit to the cash set aside, (3) the typical investor does not set aside money for replacements, but borrows when it is time to replace. Therefore, the sinking fund rate is the difference between the opportunity cost and the borrow rate.) 13

14 The following are statement ratios developed from operating statements. # NIR (net income ratio) Io/EGI, or 1 OER # OER (operating expense ratio) Expenses/EGI, or 1 NIR # Break even ratio (BER) (Expenses + Debt service) / PGI # Debt service coverage ratio (DCR or DSCR) Io/Debt service Statement Ratios Example: A property sold for $600,000 and has the following income statement. PGI $100,000 Vacancy (5,000) EGI $95,000 Operating expenses (30,000) Replacements (5000) Io $60,000 Debt service (40,000) PTCF $20,000 Net income ratio = 60,000/95,000 or 65,000/95,000 =.632, (63.2%), or.684 (68.4%) Operating expense ratio = 35,000/95,000 or 30,000/95,000 =.368 (36.8%), or.316 (31.6%) Break even ratio = (35, ,000)/100,000 = 75% occupancy Debt coverage ratio = 60,000/40,000 = 1.50 Developing Cash Flows Over Time changes The appraiser often uses a discounted cash flow to value property interests. The cash flow analysis begins with year one income. The appraiser then trends the income based upon the following. changes over time because of the following reasons. # Inflation or deflation this is the price change due to the overall change of prices in the economy. The basic economics model Money supply x velocity = price x GDP explains inflation/deflation. Money is the money supply in a closed area or system, velocity is the turnover of money that is somewhat constant, price is the money paid for goods and GDP is gross domestic product or the sum of all goods and services in an economy. If velocity is a constant and money supply is increased 5%, then the right side of the equation (in the mid to long-term) has to change. If GDP grows at 2%, then the prices have to increase 3%. The formula is affected by the globalization of the economy and although basic, is difficult to measure. # Relative price changes Even if money supply increases and is allocated over prices at 5%, the allocation is not 5% to all goods and services. Supply and demand forces for the good or service relative to the demand and supply forces for all goods and services determines the allocation of price. # could change because of contract terms set in a lease. # could change based upon the relative bargaining position of tenant and landlord. The particular location may be essential for the business of the tenant. The location may be marginal for the business of the particular tenant. # could change based upon the rate of depreciation of improvements. 14

15 # could change because the tenant is improving the property. The landlord may not look for increases if the tenant improves the property during the tenancy. Value changes The appraiser often derives a future value (reversion) as a component of a discounted cash flow. A reversion is a future value. That is why the term the present value of the reversion is used. If the property is a sell-out type property such as a subdivision, condominium project, time-share, etc. the hoped for reversion by a developer/investor is $0. If the property is a retail center, office building, residential property, or industrial, commercial property the reversion is hoped to be some future value, even if just land value. The following are types of reversions (note all are future values) # Property sale price less costs of sale # Equity property reversion less remaining loan balance # Mortgage the loan balance as of the date of sale # Land the value of the land at the date of sale. Because land is often a negative carry (the expenses exceed the rental income), the land must outpace inflation to produce a good return. The bottom line is the land has to have a change of highest and best use or the ultimate highest and best use must come about. # Building the value of the building as of the date of sale. The reversion to the building is affected by the following. o Depreciation on the building, e.g. 2%/year o Inflation in building costs, e.g. 4%/year o Increasing rate of return required to the building (in general the older the building, the higher the rate of return. o Changes in tax laws 15

16 Chapter 48 Stabilizing Cash Flows Overview There are numerous reasons to stabilize cash flows. The following is a partial list of those reasons. 1. The property is below market or stabilized occupancy because the market is soft. 2. The property is below market or stabilized occupancy because it is new. 3. The property is below market or stabilized occupancy because it has poor management. 4. The property is below market or stabilized occupancy because there happened to be a significant move-out of a major tenant or many tenants. 5. The property is below market or stabilized occupancy because it is being renovated. 6. Leases are not at market for some reason. 7. Leases have a structure that must be normalized to properly compare to another structure. An example of this is when a comparable has increases built into the lease but the subject is being analyzed for long-term and level leases. The income must be stabilized to properly compare to the subject structure. An example of an income stabilizing factor is a K-factor. The K-factor gives equivalent level income for an income stream that changes constant ratio. It is not a present value factor, but instead is used to smooth out streams that change constant ratio. Example: An income stream starts at $10,000 and increases 4%/year for 5 years and the yield rate is 10%. What is the equivalent level income and what is the K-factor? 1.04 Enter Enter Enter 10,000 g CFj X g CFj X g CFj X g CFj X g CFj 10 I f NPV [40,759] 5 N solve PMT [10,752.13] K-factor: 10,752 Enter 10,000 [ ] Note: Before calculators, one would look up this factor in tables. The present value of $10,752 discounted at 10% for 5 years is the same present value as the income stream that begins at $10,000, grows 4% compounded over the 5 years and is discounted at 10%. As can be seen, the K-factor is NOT a present value factor, but is a factor to provide level income equivalents to income streams that change constant ratio. The following demonstrates an equivalent level income stream for an income pattern that is irregular. As long as the present value can be determined of any income flow, the equivalent level income is simply solving for payment (PMT) once the present value (PV or NPV) is solved. Use an 11% yield rate 16

17 Year 1 Year 2 Year 3 Year 4 Year 5 $10,000 $11,000 $12,400 $13,800 $15,000 10,000 g CFj 11,000 g CFj 12,400 g CFj 13,800 g CFj 15,000 g CFj 11 i f NPV [44,996] 5 N PMT [12,175] Note: The step 5 N is not necessary for this particular calculation. However, if the Nj key is used, it would be necessary to add this step. If the 5 N were not used, it would be necessary to hit PMT twice. It is easier and safer to always add the step. Also note that the 12,175/10,000 = is a factor that would be a level equivalent factor but it is NOT a K-factor. The K-factor is just for constant changing income streams. 17

18 Chapter 49 Direct Capitalization Overview Direct capitalization is the use of a multiplier or capitalization rate to process an income to value. In direct capitalization, the yield rate is not specified. Also, the change in income and value is not explicitly set forth. For residential valuation the formula is as follows Monthly rent x GMRM = Value The GMRM is the gross monthly rent multiplier and is found by taking a sale price of a property that has sold and dividing it by the rent that it was achieving at the time of sale. An appraiser should be careful to assess if the 18

19 Chapter 50 Direct Capitalization - Commercial Overview SUMMARY OF METHODS OF DEVELOPING OVERALL CAPITALIZATION RATES Direct Capitalization Formulas " " " "! R o = Io / Sale Price! R o = M x R M + E x R E! R o = NIR / EGIM! R o = DCR x R M x M! R o = 1 / NIM! R o = B x R B + L x R L! V o = EGI x EGIM! V o = PGI x PGIM! V o = NIBT/(R o + ETR) 1. Ro = Io Sale price 19

20 The most important consideration when using capitalization rates derived from sales in the market is to apply them the same way you derive them. There is no correct way to derive capitalization rates from sales. However, there is only one way to apply them, consistently with how they are derived. For example, given a sale, you can derive a capitalization rate with and without reserves in expenses, stabilized or nonstabilized occupancy, on last year's income, current income annualized, projected income, one year later historical income, etc. Over 100 cap rates can be derived from one sale, none of them correct, nor wrong. Capitalization rates must be derived after adjusting sales for financing differences (as of the date of sale), but capitalization rates are indications of motivation only as of the date of sale, and cannot be adjusted for time. You can analyze older capitalization rates based upon changes in the capital market structures, but do not try to adjust them (especially for price and rental increases). A property sold for $100,000 with Io of $10,000. What is the indicated capitalization rate 4 years later if the income and value both increased 5% per year/compounded, and the property recently sold? Answer: INCOME: $10,000 X = $12,155 VALUE: $100,000 X = $121,551 Ro = $10,000 / 100,000 = 10% Ro = $12,155 / 121,551 = 10% 20

21 THE CAPITALIZATION RATE DOES NOT CHANGE WHEN THE Io & VALUE GO UP AT THE SAME RATE (THIS IS TRUE REGARDLESS OF THE EXPENSE RATIO) 2. Ro = NIR EGIM, or Ro = NIR PGIM The NIR must be developed on EGI in the first formula (Io EGI), and PGI in the second formula (Io PGI). What is the Ro if the NIR is 45% and the EGIM is 7? Answer: Ro =.45 / 7 = 6.43% What is the Ro if the NIR on EGI is 55%, vacancy is 5% and the PGIM is 6? Answer: EGIM = 6 /.95 = 6.32 & Ro =.55 /.0632 = 8.7% 3. Ro = DCR x M x Rm What is the Ro if the DCR requirement is 1.20, the loan to value ratio is 70% and the mortgage constant is 12%? Answer: Ro = 1.20 X.70 X.12 = 10.08% 4. Ro = (Rm x M) + (Re x E) What is the Ro if the loan to value ratio is 75%, Re = 8%, and Rm = 11%? Answer: Ro = (.75 X.11) + (.25 X.08) = 10.25% 21

22 5. Ro = (RL x L) + (RB x B) What is the Ro if the land to value ratio is 35%, R L = 10%, and R B = 14%? Answer: Ro = (.35 X.10) + (.65 X.14) = 12.6% What is the R L if the land to value ratio is 35%, R0 = 12%, and R B = 12.5%? Answer:.65 X.125 = X R L = [ =.03875] /.35 = 11.07% OR [.12 - (.65 X.125)] /.35 = 11.07% 6. Vo = NIBT (Ro + ETR), where NIBT = net income before property taxes, and ETR = effective tax rate. What is the value if NIBT = $50,000, the Ro from the market is 10% and the effective tax rate is 3% of value? Answer: $50,000 / ( ) = $384, Residual techniques 22

23 The following is a format that is used to solve for residual problems. The BLT denotes building, land & total. The MET is mortgage, equity & total. IRV is interest, rate & value. 84 Residual Techniques B/M L/E T I R V B/M L/E T! V B = $300,000! R B = 12%! R L = 10%! Io = $100,000 I R V 36,000 12% 300,000 64,000 10% 640,000 $100, , Recognition & set-up Given: a. Io b. 2 rates or ways to calculate c. part of a whole value 23

24 d. but, not the ratios so that the capitalization rates are not capable of being blended. 2. Land & building 3. Mortgage & equity 4. Present value of income & present value of reversion What is given to solve for the following residuals? Answers: a. Land - Building value, R L & R B, Io b. Building - Land value, R L & R B, Io c. Mortgage - Down payment (equity), R M & R E, Io d. Equity - Mortgage amount value, R M & R E, Io e. - Present value of the reversion, R I & R N, Io f. Reversion - Present value of the income, R I & R N, Io 8. Multipliers 1. Potential gross income multiplier (PGIM): Sale price all the potential income 2. Potential gross rent multiplier (PGRM): Sale price rental income only 3. Effective gross income multiplier (EGIM): Sale price effective gross income 4. Net income multiplier (NIM): Sale price net operating income From Sales Ro = Io Sale price Procedure: Analyze sales for income and price or value. The comparable sales income statement may be "reconstructed" to be consistent with the subject's net income. Generally, expenses that are not included in the calculation of net income are debt service (interest & principal), income taxes, capital expenses (but the allowance for reserves has capital items), entity expenses (such as corporate or partnership fees), often leasing commissions are omitted, and other inappropriate or excessive expenses. Divide net income by the sale price or value. The resulting capitalization rate is then applied to the subject income stream to process value for the subject property. Example: The net income from a sale is $100,000 and the property sold for $1,000,000. The capitalization rate is $100,000 $1,000,000 = 10%. However, given the same sale a total of 256 capitalization rates have been calculated with very little information. The capitalization rate calculations are shown following. Which is the "correct" rate? Note that the 256 possible capitalization rates could be increased in number by analyzing changing expenses, given probabilities that new management can change the expense structures (by tax appeal, etc.) and by analyzing different property rights. Given all the possibilities, over 1,000 capitalization rates could be calculated. The 256 capitalization rates should suffice to prove the point that... Rule number one when using direct capitalization is to be consistent with the derivation (from sales) and application (to the subject) of the rate!!! The capitalization rates in the example range from 5.4% to 14.6%, yet all are "correct." The derivation and application of rates, at first glance, seems relatively straight-forward. Use of direct capitalization is often preferable in courtroom settings to yield capitalization because it is easier to explain to a jury. However, in practice, if used correctly the selection and application is actually complex. For example, suppose the comparables are retail centers, like the subject. However, the best comparable has leases that are relatively level for three years followed by increases and indicates a capitalization rate of 13%. The subject is identical in all other respects except the lease is level for ten years. Given a 24

25 rising market the capitalization rate should be greater for the subject than 13%, and less than 13% if a declining market. The longer the income is expected to be level over a holding period, the closer the capitalization rate is to the yield rate. The yield rate is the rate of return over the entire period of ownership, while the capitalization rate is only an expression of a one year return. The relationship in a very simple model (we will look at later) is R = Y - o x SFF, where o is the overall change in value, and the model assumes income will remain level over the holding period. Given a long expected level income o x SFF becomes smaller and the R is approximately equal to Y. In nontechnical terms the capitalization rate is near the yield rate when expected income and value change is small. The more the value and income are expected to change, the larger the spread between the capitalization and yield rate. Multipliers such as effective gross income and potential gross income multipliers are also application of direct capitalization. In fact, the overall capitalization rate is the reciprocal of a net income multiplier, and an effective gross income multiplier is the net income multiplier times the net income ratio (which is 1 minus the operating expense ratio). We will also later look at this relationship expressed in the formula: R = NIR EGIM. There is obviously a relationship between the EGIM, Ro, OER, and Yo. The Ro should be consistent with the risk in a property, the higher the risk relative to other sales, generally the higher the capitalization rate. Summary of Market Information Needed: 1. Net operating income = Potential gross income - vacancy & collection loss - operating expenses 2. Sale price or adjusted sale price (adjusted for cash equivalency, personal property or business value included, property rights, etc.) 25

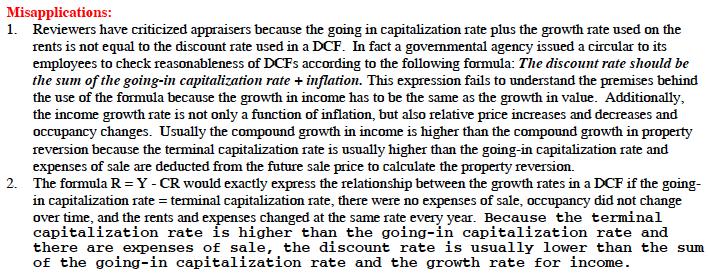

26 Misapplications: 1. Using the income from sales based upon historical data, and applying the rate to a subject income stream based upon projected data. [There is not a right or wrong way to derive or apply capitalization rates, just consistent or inconsistent. See if there is a consistent pattern from the sales on historical, current income annualized, projected or some other income, and derive the subject income based upon the way capitalization rates are consistently derived from sales. Do not think you have to always use projected income for the subject.] 2. Using an allowance for reserves to calculate subject net operating income, but not in the sales. Therefore, the capitalization rates in the sales include the allowance for reserves in the capitalization rates, and are too high when applying to a subject income stream derived with an allowance for reserves in the expenses.[the subject income will be lower than the comparables, all other items being equal, because an allowance for reserve is a deduction from income. Using a capitalization rate that includes the allowance for reserves results in double counting the deduction when the rate is applied to an income stream that already has an allowance deducted. The difference between a capitalization rate from a sale with and without reserves is equal to the basis point difference of the allowance as a dollar amount divided by the sale price. For example, Io with an allowance is equal to $10,000 and $12,000 without an allowance. The property sold for $100,000. The capitalization rate is 10% on income with the allowance deducted, and 12% without. It is not a coincidence that the difference between the capitalization rates of 2% is also the percent of allowance of reserves to value.] 3. Using "inferred" or "projected" income (made up). Often all capitalization rates from sales in a report are based on appraiser made up income that justifies the rate used on the subject. This is not market derived value and fails to result in a value that meets the definition of "market value." 4. Deriving capitalization rates before tenant improvements and leasing commissions and applying the rate to income after tenant improvements and leasing commissions. 5. Using Yo, or another yield rate, as a capitalization rate. Ro is a one year relationship of income to value, but Yo is the return "on" investment over the life of the investment.[some appraisers compare capital market rates to derive a capitalization rate. This is an erroneous comparison of yield to capitalization rates.] 26

27 IMPORTANT: All other methods in direct capitalization (such as band of investment & DCR analysis to derive Ro) are not generally preferred methods to primarily derive capitalization rates. If you have the inputs needed to derive the capitalization rate, you already have income divided by value, and do not need the alternative formulas. The alternative equations are useful (1) to adjust market-derived rates to better apply to the subject and (2) for tests of reasonableness. Furthermore, they are useful for adjusting previously market derived capitalization rates when time has lapsed since the derivation of the rates from sales, and subsequently no or little sales information is available. The following are 256 capitalization rates from one, the same sale. The rates range from 5.4% to 14.6%, depending upon which income and which price or value was used. Therefore, the income and price or value used to develop the Ro must be consistent with the income developed for the subject and the value or price that is being measured. 27

28 256$Capitalization$Rates$From$One$Sale$ Which$Ro$is$the$Correct$Rate?$ Sale Price $1,000,000 Cash Equivalent $920,000 TIs & Commissions Curables $100,000 $20,000 per year If tax appeal successful: NOI-stablized: With reserves W/O reserves With reserves W/O reserves Historical $100,000 $115,000 $104,000 $119,000 Current annualized $105,000 $120,000 $109,000 $124,000 Projected income $110,000 $125,000 $114,000 $129,000 Actual in 1 YR $115,000 $130,000 $119,000 $134,000 If tax appeal successful: NOI-actual occ: With reserves W/O reserves With reserves W/O reserves Historical $80,000 $95,000 $84,000 $99,000 Current annualized $85,000 $100,000 $89,000 $104,000 Projected income $90,000 $105,000 $94,000 $109,000 Actual in 1 YR $95,000 $110,000 $99,000 $114,000 Lose tax appeal: Win tax appeal: Cash Equiv Not Cash Equiv Cash Equiv Not Cash Equiv Historical Before TIs With Curables With reserves 9.80% 9.09% 10.20% 9.45% Stabilized W/O reserves 11.27% 10.45% 11.67% 10.82% W/O Curables With reserves 10.87% 10.00% 11.30% 10.40% W/O reserves 12.50% 11.50% 12.93% 11.90% After TIs With Curables With reserves 7.84% 7.27% 8.24% 7.64% W/O reserves 9.31% 8.64% 9.71% 9.00% W/O Curables With reserves 8.70% 8.00% 9.13% 8.40% W/O reserves 10.33% 9.50% 10.76% 9.90% Cash Equiv Not Cash Equiv Cash Equiv Not Cash Equiv Historical Before TIs With Curables With reserves 7.84% 7.27% 8.24% 7.64% Actual W/O reserves 9.31% 8.64% 9.71% 9.00% W/O Curables With reserves 8.70% 8.00% 9.13% 8.40% W/O reserves 10.33% 9.50% 10.76% 9.90% After TIs With Curables With reserves 5.88% 5.45% 6.27% 5.82% W/O reserves 7.35% 6.82% 7.75% 7.18% W/O Curables With reserves 6.52% 6.00% 6.96% 6.40% W/O reserves 8.15% 7.50% 8.59% 7.90% Cash Equiv Not Cash Equiv Cash Equiv Not Cash Equiv Current Before TIs With Curables With reserves 10.29% 9.55% 10.69% 9.91% Stabilized W/O reserves 11.76% 10.91% 12.16% 11.27% W/O Curables With reserves 11.41% 10.50% 11.85% 10.90% W/O reserves 13.04% 12.00% 13.48% 12.40% After TIs With Curables With reserves 8.33% 7.73% 8.73% 8.09% W/O reserves 9.80% 9.09% 10.20% 9.45% W/O Curables With reserves 9.24% 8.50% 9.67% 8.90% W/O reserves 10.87% 10.00% 11.30% 10.40% $ 28

29 256$Capitalization$Rates$From$One$Sale$ Which$Ro$is$the$Correct$Rate?$ $ Lose tax appeal: Win tax appeal: Cash Equiv Not Cash Equiv Cash Equiv Not Cash Equiv Current Before TIs With Curables With reserves 8.33% 7.73% 8.73% 8.09% Actual W/O reserves 9.80% 9.09% 10.20% 9.45% W/O Curables With reserves 9.24% 8.50% 9.67% 8.90% W/O reserves 10.87% 10.00% 11.30% 10.40% After TIs With Curables With reserves 6.37% 5.91% 6.76% 6.27% W/O reserves 7.84% 7.27% 8.24% 7.64% W/O Curables With reserves 7.07% 6.50% 7.50% 6.90% W/O reserves 8.70% 8.00% 9.13% 8.40% Cash Equiv Not Cash Equiv Cash Equiv Not Cash Equiv Projected Before TIs With Curables With reserves 10.78% 10.00% 11.18% 10.36% Stabilized W/O reserves 12.25% 11.36% 12.65% 11.73% W/O Curables With reserves 11.96% 11.00% 12.39% 11.40% W/O reserves 13.59% 12.50% 14.02% 12.90% After TIs With Curables With reserves 8.82% 8.18% 9.22% 8.55% W/O reserves 10.29% 9.55% 10.69% 9.91% W/O Curables With reserves 9.78% 9.00% 10.22% 9.40% W/O reserves 11.41% 10.50% 11.85% 10.90% Cash Equiv Not Cash Equiv Cash Equiv Not Cash Equiv Projected Before TIs With Curables With reserves 8.82% 8.18% 9.22% 8.55% Actual W/O reserves 10.29% 9.55% 10.69% 9.91% W/O Curables With reserves 9.78% 9.00% 10.22% 9.40% W/O reserves 11.41% 10.50% 11.85% 10.90% After TIs With Curables With reserves 6.86% 6.36% 7.25% 6.73% W/O reserves 8.33% 7.73% 8.73% 8.09% W/O Curables With reserves 7.61% 7.00% 8.04% 7.40% W/O reserves 9.24% 8.50% 9.67% 8.90% Cash Equiv Not Cash Equiv Cash Equiv Not Cash Equiv Actual 1 Year later Before TIs With Curables With reserves 11.27% 10.45% 11.67% 10.82% Stabilized W/O reserves 12.75% 11.82% 13.14% 12.18% W/O Curables With reserves 12.50% 11.50% 12.93% 11.90% W/O reserves 14.13% 13.00% 14.57% 13.40% After TIs With Curables With reserves 9.31% 8.64% 9.71% 9.00% W/O reserves 10.78% 10.00% 11.18% 10.36% W/O Curables With reserves 10.33% 9.50% 10.76% 9.90% W/O reserves 11.96% 11.00% 12.39% 11.40% Cash Equiv Not Cash Equiv Cash Equiv Not Cash Equiv Actual 1 Year later Before TIs With Curables With reserves 9.31% 8.64% 9.71% 9.00% Actual W/O reserves 10.78% 10.00% 11.18% 10.36% This is the income W/O Curables With reserves 10.33% 9.50% 10.76% 9.90% that is historically W/O reserves 11.96% 11.00% 12.39% 11.40% achieved after 1 year After TIs With Curables With reserves 7.35% 6.82% 7.75% 7.18% ownership of the W/O reserves 8.82% 8.18% 9.22% 8.55% property. W/O Curables With reserves 8.15% 7.50% 8.59% 7.90% W/O reserves 9.78% 9.00% 10.22% 9.40% $ 29

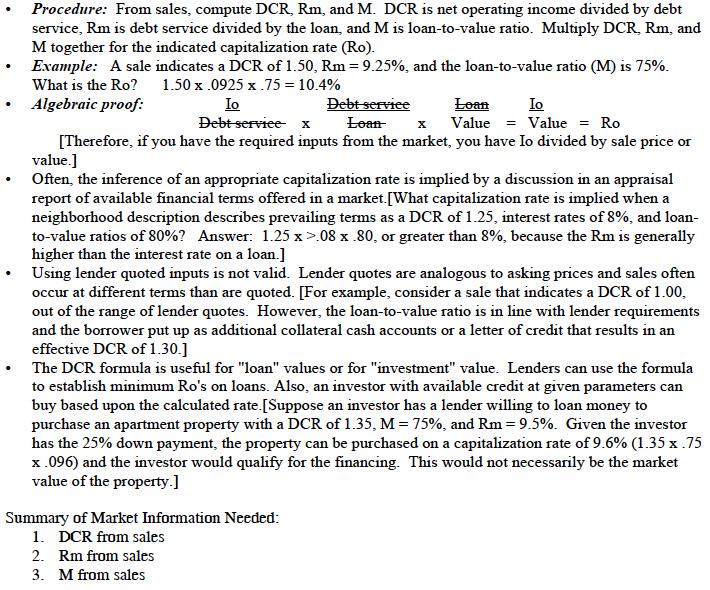

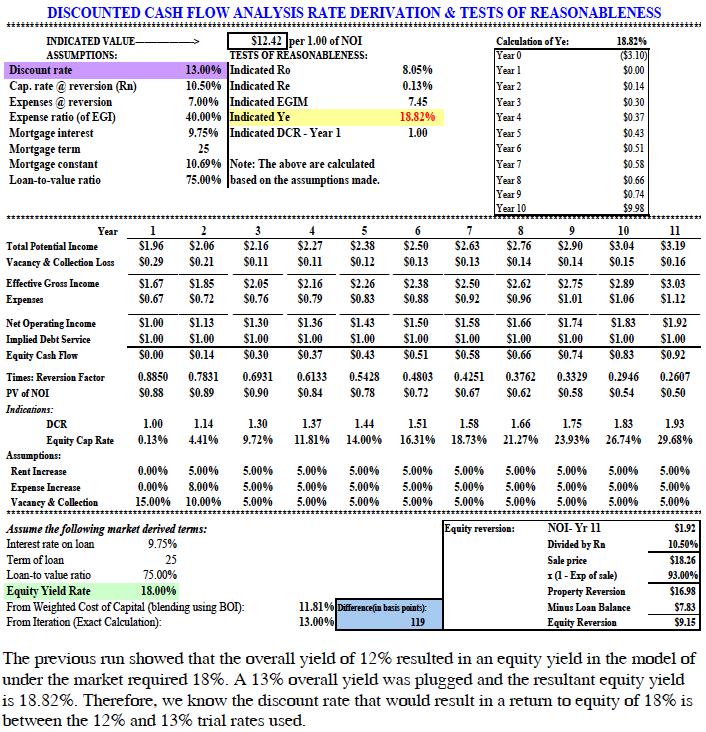

30 From$DCR$ $ Ro$=$DCR$x$Rm$x$M$ " 30

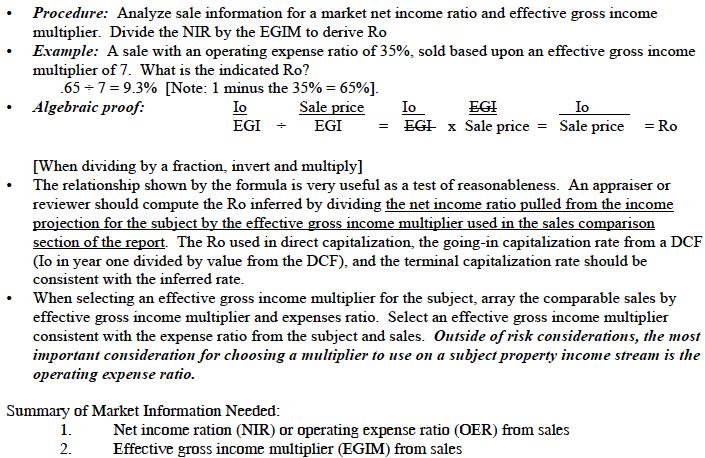

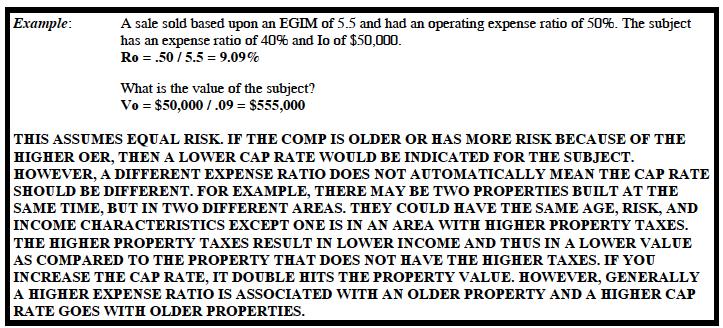

31 " $ $ From$EGIM$ $ Ro$=$NIR$ $EGIM" " 31

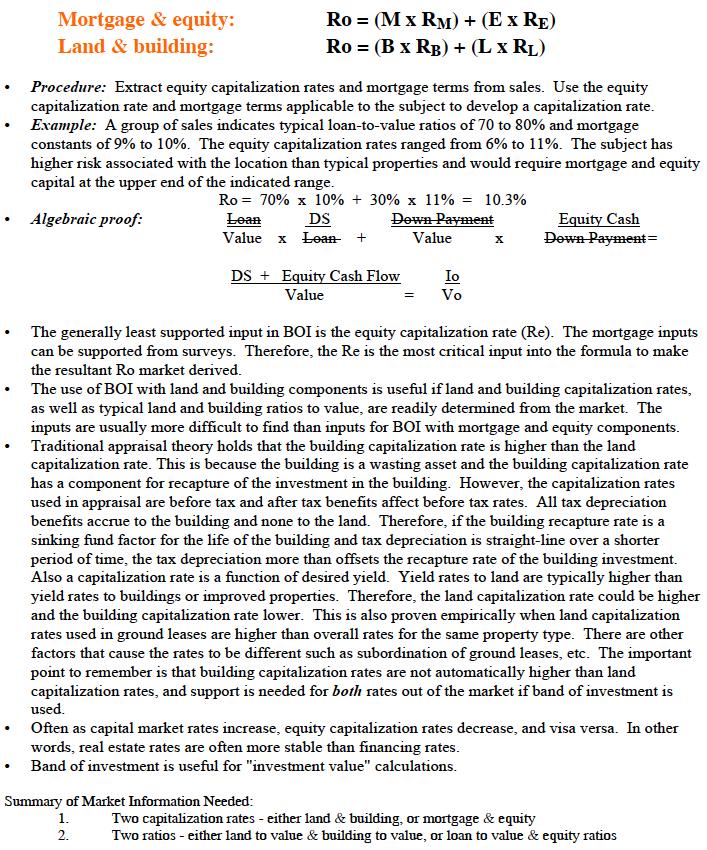

32 " " " $ From$Band$of$Investment$(BOI)$ $ $ $ " " 32

33 33

34 " " 34

35 Chapter 51 Yield Capitalization Overview The "" 35

36 $Models" " " " $ " Models Level Models! Perpetuity: R = Y! Inwood: R = Y + 1/s Y! Hoskold: R = Y + 1/s reinvestment rate Unlevel Models! Constant ratio change: " K-factor x Ann.Factor x I 1 " [1-(1+x) n /(1+i) n ]/(i-x) x I 1! Straight-line change: Vo= (d + hn)af - h(n - af)/i (d = I 1 ; h = $inc.change; af = annuity factor; i = yield rate)! Unlevel income: DCF " 36

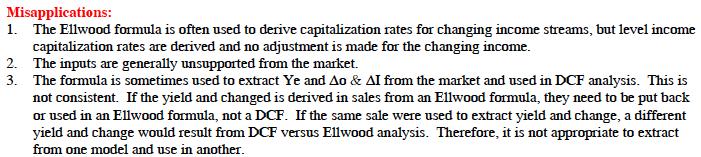

37 " Property$Models$ Yield Capitalization Formulas Property Models! R o = Y o - 1/s n! R o = Y o - CR! R o = Y o - 1/n Other Property Models! Ellwood: R o = Y E - MC - 1/s n (C = (Y E + P 1/s n - Rm)! Discounted Cash Flow " " 37

38 Investment Model Decision Tree Combining & Property Models If the income is level: Use R = Y - 1/s n! If only income or no value in reversion, then Δ = -1 (This means you will add the 1/s n to Y)! If reinvestment is at a different rate than Y, then calculate the 1/s lower rate (Hoskold premise)! If the income is in perpetuity or there is no change in value then Δ = 0! Otherwise, compute the 1/s Y (Inwood premise)! If the income is unlevel, calculate equivalent level income & use the above formula If the income is unlevel: " & straight-line change in value with related change in income! R = Y - 1/n " & constant ratio change in income & value! R = Y - CR " & given Ye & mortgage terms (Ellwood)! R = Y - MC - 1/s n " otherwise, use a DCF " " " 38

39 39

40 40

41 41

42 42

43 43

44 44

45 45

46 46

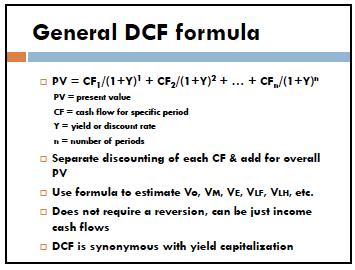

47 Discounted Cash Flow 47

48 48

49 49

50 Chapter 52 Leverage Overview Leverage is the use of borrowed funds to purchase property. The idea is that the control of property can take place with less than 100% of the purchase price by the buyer. The effect of leverage can be positive, neutral or negative. However, the anticipation is almost always a higher return to equity. This is because borrowing money to purchase property always increases risk in ownership. The equity position requires a higher return because of the financial risk taken. 113 Leverage Combining & Property Models Leverage Leverage Cash Flows Yield Rates Positive Re>Ro>Rm Ye>Yo>Ym Negative Re<Ro<Rm Ye<Yo<Ym Neutral Re=Ro=Rm Ye=Yo=Ym Considerations! Yield rates are the better measure of overall leverage because they represent the entire return on investment over the holding period! With positive leverage Re goes up as M increases! With negative leverage Re goes down as M increases! Focus on the mortgage rate:! If it is the highest that is bad, & bad is negative (leverage)! If it is the lowest that is good & good is positive (leverage). Leverage can be measured by the following ways. # In the cash flows This measure is conducted by comparing capitalization rates in either a sale or from investor expectations. The three rates looked at are the Re (capitalization rate to equity, or PTCF/Down payment), Rm (mortgage capitalization rate, constant, or debt service/loan, or interest rate + sinking fund factor), and the Ro (overall capitalization rate, or Io/SP). The Ro is always between the two other rates or all three have to be equal. If the equity rate, Re, is the highest of the three, there is positive leverage. This expected because the mortgage is always paid first, and any residual income goes to the equity. In fact, the equity investor can decrease. The measure based upon cash flows in never as good as as measuring leverage based upon yield. This is 50

51 because the yield rates include the first year returns, but the capitalization rates are just the first year return in an investment. Loosely put, the yield rates are a time weighted average of all capitalization rates, including the first year. Note also that if all rates are equal, there is still leverage, there is just no affect of the leverage. Note further, that if all rates are equal, the mortgage holder is in a favorable position relative to equity because the equity position is always with higher risk. # In the yield rates The affect of leverage is best measured by comparing the yield rates between equity, Ye, mortgage, Ym, and property Yo. The Yo is always between the Ye and Ym or they are all equal. Even if equal there is leverage, there is just no affect to the leverage. The same property can have negative leverage in the cash flows and positive leverage in the yield rates. This is common because of expectations of rising income and/or value. The leverage affect is outlined following. " Leverage Cash flows Yield rates Positive leverage Rm<Ro<Re Ym<Yo<Ye Negative leverage Rm>Ro>Re Ym>Yo>Ye No affect Rm=Ro=Re Ym=Yo=Ye Leverage" Residual$ to$the$ Debt$$ Paid"First" Equity" Re" Debt" Rm" Io$ Ro$ Equity is in the residual position and there is always an expectation of a greater return in the yield rates. However, because debt service is level and equity gets all increases, the leverage could be negative or neutral by measuring leverage based upon capitalization rates. $ " 51

52 Chapter 53 Weighted Average Cost of Capital Overview The 52

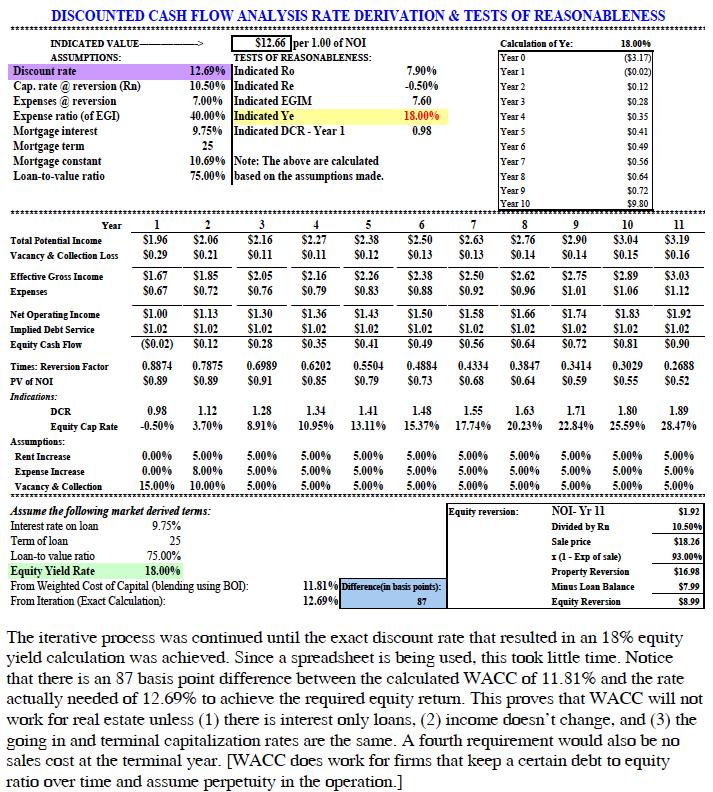

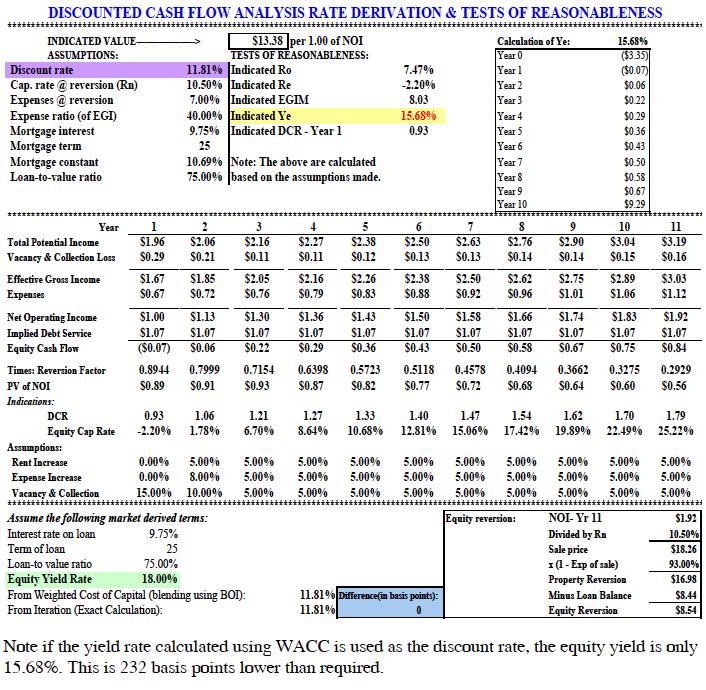

53 Weighted Average Cost of Capital (WACC)! Loan-to-value ratio x interest rate + Equity ratio x equity yield rate = Overall yield rate! This formula is in all basic financial text books, but is used for getting a hurdle or yield rate for businesses.! It works for business that keep the equity & debt ratios constant over time.! It doesn t work for real estate because the ratios change! It works only when loan & equity ratios remain constant over time! Businesses have an optimal debt & equity mix. Therefore, the managers keep the loan & equity ratios the same year to year by floating new debt! The following affects the loan & equity ratios in the life of a real estate (or other) investment! Changing income! Changing value! Pay down of the loan! Therefore, the weighted cost of capital in a rising market understates the discount rate by weighting in too much of the interest rate on a loan and not enough of the equity yield rate.! However, if the market for a certain type or area of real estate keeps the loan & equity ratios constant through refinancing, then the method could express overall yields for this type of product or area. 53

54 54

55 55

56 56

57 57

58 58

59 59

Risk Management Insights

Risk Management Insights Appraisal Review Part II: Income Capitalization Approach George Mann, Managing Director and Chief Appraiser, Collateral Evaluation Services, Inc.and Nikki Griffith, MAI, CCIM,

Risk Management Insights Appraisal Review Part II: Income Capitalization Approach George Mann, Managing Director and Chief Appraiser, Collateral Evaluation Services, Inc.and Nikki Griffith, MAI, CCIM,

PREPARING FOR THE MINNESOTA INCOME PROPERTY CASE STUDY EXAM WORKSHOP

PREPARING FOR THE MINNESOTA INCOME PROPERTY CASE STUDY EXAM WORKSHOP Date: September 18, 2018 Location: Country Inn & Suites Chanhassen, MN Instructor: Bob Wilson, CAE, ASA Revised October, 2017 PREPARING

PREPARING FOR THE MINNESOTA INCOME PROPERTY CASE STUDY EXAM WORKSHOP Date: September 18, 2018 Location: Country Inn & Suites Chanhassen, MN Instructor: Bob Wilson, CAE, ASA Revised October, 2017 PREPARING

Retail Acquisition Example

Property Information Retail Acquisition Example Project Assumptions Acquisition Assumptions Property Name Retail Acquisition Example Project Type Acquisition Location Austin, TX Acquisition Cost $1,800,000

Property Information Retail Acquisition Example Project Assumptions Acquisition Assumptions Property Name Retail Acquisition Example Project Type Acquisition Location Austin, TX Acquisition Cost $1,800,000

concepts and techniques

concepts and techniques S a m p l e Timed Outline Topic Area DAY 1 Reference(s) Learning Objective The student will learn Teaching Method Time Segment (Minutes) Chapter 1: Introduction to Sales Comparison

concepts and techniques S a m p l e Timed Outline Topic Area DAY 1 Reference(s) Learning Objective The student will learn Teaching Method Time Segment (Minutes) Chapter 1: Introduction to Sales Comparison

BUSI 330 Suggested Answers to Review and Discussion Questions: Lesson 10

BUSI 330 Suggested Answers to Review and Discussion Questions: Lesson 10 1. The client should give you a copy of their income and expense statements for the last 3 years showing their rental income by

BUSI 330 Suggested Answers to Review and Discussion Questions: Lesson 10 1. The client should give you a copy of their income and expense statements for the last 3 years showing their rental income by

Real Estate & REIT Modeling: Quiz Questions Module 1 Accounting, Overview & Key Metrics

Real Estate & REIT Modeling: Quiz Questions Module 1 Accounting, Overview & Key Metrics 1. How are REITs different from normal companies? a. Unlike normal companies, REITs are not required to pay income

Real Estate & REIT Modeling: Quiz Questions Module 1 Accounting, Overview & Key Metrics 1. How are REITs different from normal companies? a. Unlike normal companies, REITs are not required to pay income

Chapter 18. Investors have different required yields Different risk assessment Different opportunity cost of equity

Decision Making in Real Estate Centers Around Valuation Chapter 18 Investment Decisions: Ratios We examined the concept of market value in Chapters 7 & 8 As noted, professional RE appraisers are often

Decision Making in Real Estate Centers Around Valuation Chapter 18 Investment Decisions: Ratios We examined the concept of market value in Chapters 7 & 8 As noted, professional RE appraisers are often

Course Income Approach To Value. Course Description

Course 102 - Income Approach To Value Course Description The Income Approach to Valuation is designed to provide the students with an understanding and working knowledge of the procedures and techniques

Course 102 - Income Approach To Value Course Description The Income Approach to Valuation is designed to provide the students with an understanding and working knowledge of the procedures and techniques

2. The, and Act, also known as FIRREA, requires that states set standards for all appraisers.

CHAPTER 4 SHORT-ANSWER QUESTIONS 1. An appraisal is an or of value. 2. The, and Act, also known as FIRREA, requires that states set standards for all appraisers. 3. Value in real estate is the "present

CHAPTER 4 SHORT-ANSWER QUESTIONS 1. An appraisal is an or of value. 2. The, and Act, also known as FIRREA, requires that states set standards for all appraisers. 3. Value in real estate is the "present

Cost Segregation Instructor Teaching Schedule (3-Hour)

") Time Topic Pages Student Objectives 8:30-8:35 Course introduction Page 2 What is cost segregation? Objective of cost segregation: to increase cash flow Benefit of cost segregation Learning objectives Page

Time Topic Pages Student Objectives 8:30-8:35 Course introduction Page 2 What is cost segregation? Objective of cost segregation: to increase cash flow Benefit of cost segregation Learning objectives Page

Following is an example of an income and expense benchmark worksheet:

After analyzing income and expense information and establishing typical rents and expenses, apply benchmarks and base standards to the reappraisal area. Following is an example of an income and expense

After analyzing income and expense information and establishing typical rents and expenses, apply benchmarks and base standards to the reappraisal area. Following is an example of an income and expense

BUSI 331: Real Estate Investment Analysis and Advanced Income Appraisal

BUSI 331: Real Estate Investment Analysis and Advanced Income Appraisal PURPOSE AND SCOPE The Real Estate Investment Analysis and Advanced Income Appraisal course BUSI 331 is intended to build upon the

BUSI 331: Real Estate Investment Analysis and Advanced Income Appraisal PURPOSE AND SCOPE The Real Estate Investment Analysis and Advanced Income Appraisal course BUSI 331 is intended to build upon the

Cap Rate Trends, Methodology and Analysis. Dane R. Anderson MAI, CCIM Appraisal & Litigation Services Director

Cap Rate Trends, Methodology and Analysis Dane R. Anderson MAI, CCIM Appraisal & Litigation Services Director 1 Quickly The Income Approach Basis of the Approach Present worth of future benefits Two Methods:

Cap Rate Trends, Methodology and Analysis Dane R. Anderson MAI, CCIM Appraisal & Litigation Services Director 1 Quickly The Income Approach Basis of the Approach Present worth of future benefits Two Methods:

REAL ESTATE INVESTMENTS

REAL ESTATE INVESTMENTS PROBLEM SET 2 1. PROBLEM The leases for space in an office building provide for limitations or stops on the lessor s liability for real estate taxes and operating expenses. Each

REAL ESTATE INVESTMENTS PROBLEM SET 2 1. PROBLEM The leases for space in an office building provide for limitations or stops on the lessor s liability for real estate taxes and operating expenses. Each

Sales Associate Course

Sales Associate Course Chapter Seventeen Real Estate Investments and Business Opportunity Brokerage 1 Investment Analysis Most important consideration: Economic soundness Land use controls Zoning Deed

Sales Associate Course Chapter Seventeen Real Estate Investments and Business Opportunity Brokerage 1 Investment Analysis Most important consideration: Economic soundness Land use controls Zoning Deed

Chapter 8. How much would you pay today for... The Income Approach to Appraisal

How much would you pay today for... Chapter 8 One hundred dollars paid with certainty each year for five years, starting one year from now. Why would you pay less than $500 Valuation Using the Income Approach

How much would you pay today for... Chapter 8 One hundred dollars paid with certainty each year for five years, starting one year from now. Why would you pay less than $500 Valuation Using the Income Approach

Advanced M&A and Merger Models Quiz Questions

Advanced M&A and Merger Models Quiz Questions Transaction Assumptions and Sources & Uses Purchase Price Allocation & Balance Sheet Combination Combining the Income Statement Revenue, Expense, and CapEx

Advanced M&A and Merger Models Quiz Questions Transaction Assumptions and Sources & Uses Purchase Price Allocation & Balance Sheet Combination Combining the Income Statement Revenue, Expense, and CapEx

Project Economics: The Value of Leasing. Russell Banham, Savills

ICSC European Retail Property School Project Economics: The Value of Leasing Russell Banham, Savills (Investment, Development & Asset Management) Introduction Who I am Russell Banham Over 30 years of experience

ICSC European Retail Property School Project Economics: The Value of Leasing Russell Banham, Savills (Investment, Development & Asset Management) Introduction Who I am Russell Banham Over 30 years of experience

Real Estate Appraisal

Market Value Chapter 17 Real Estate Appraisal This presentation includes materials from Ling and Archer, 4 th edition, Real Estate Principles The highest price a property will bring if: Payment is made

Market Value Chapter 17 Real Estate Appraisal This presentation includes materials from Ling and Archer, 4 th edition, Real Estate Principles The highest price a property will bring if: Payment is made

$450,000 $63,425 $39, % PURCHASE PRICE NET OPERATING INCOME ANNUAL CASH FLOW CAP RATE

Executive Summary Key Property Metrics $450,000 $63,425 $39,143 14.1% PURCHASE PRICE NET OPERATING INCOME ANNUAL CASH FLOW CAP RATE $70,000 $60,000 $50,000 $40,000 $30,000 Annual Cash Flow Repairs, 8%

Executive Summary Key Property Metrics $450,000 $63,425 $39,143 14.1% PURCHASE PRICE NET OPERATING INCOME ANNUAL CASH FLOW CAP RATE $70,000 $60,000 $50,000 $40,000 $30,000 Annual Cash Flow Repairs, 8%

Chapter 1 Economics of Net Leases and Sale-Leasebacks

Chapter 1 Economics of Net Leases and Sale-Leasebacks 1:1 What Is a Net Lease? 1:2 Types of Net Leases 1:2.1 Bond Lease 1:2.2 Absolute Net Lease 1:2.3 Triple Net Lease 1:2.4 Double Net Lease 1:2.5 The

Chapter 1 Economics of Net Leases and Sale-Leasebacks 1:1 What Is a Net Lease? 1:2 Types of Net Leases 1:2.1 Bond Lease 1:2.2 Absolute Net Lease 1:2.3 Triple Net Lease 1:2.4 Double Net Lease 1:2.5 The

California Real Estate License Exam Prep: Unlocking the DRE Salesperson and Broker Exam 4th Edition

California Real Estate License Exam Prep: Unlocking the DRE Salesperson and Broker Exam 4th Edition ANSWER SHEET INSTRUCTIONS: The exam consists of multiple choice questions. Multiple choice questions

California Real Estate License Exam Prep: Unlocking the DRE Salesperson and Broker Exam 4th Edition ANSWER SHEET INSTRUCTIONS: The exam consists of multiple choice questions. Multiple choice questions

Chapter 8. How much would you pay today for... The Income Approach to Appraisal

How much would you pay today for... Chapter 8 One hundred dollars paid with certainty each year for five years, starting one year from now. Why would you pay less than $500 Valuation Using the Income Approach

How much would you pay today for... Chapter 8 One hundred dollars paid with certainty each year for five years, starting one year from now. Why would you pay less than $500 Valuation Using the Income Approach

PROBLEM SOLVING IN RESIDENTIAL REAL ESTATE APPRAISING

PROBLEM SOLVING IN RESIDENTIAL REAL ESTATE APPRAISING Copyright 2000 by LEE & GRANT COMPANY, Atlanta, Georgia. All rights reserved, including the right to reproduce this book or portions of this book in

PROBLEM SOLVING IN RESIDENTIAL REAL ESTATE APPRAISING Copyright 2000 by LEE & GRANT COMPANY, Atlanta, Georgia. All rights reserved, including the right to reproduce this book or portions of this book in

Broker. Basic Business Appraisal. Chapter 9. Copyright Gold Coast Schools 1

Broker Chapter 9 Basic Business Appraisal 1 Learning Objectives Describe the characteristics of the legal entities a business appraiser may encounter List at least 5 reasons for a business appraisal List

Broker Chapter 9 Basic Business Appraisal 1 Learning Objectives Describe the characteristics of the legal entities a business appraiser may encounter List at least 5 reasons for a business appraisal List

Chapter 8. The Income Approach to Appraisal. Two Approaches to Income Valuation. How Does DCF Differ from Direct Cap? Rationale:

The Income Approach to Appraisal Chapter 8 Valuation Using the Income Approach Rationale: Value of a property is the present value of its anticipated income. Often called income capitalization Capitalize:

The Income Approach to Appraisal Chapter 8 Valuation Using the Income Approach Rationale: Value of a property is the present value of its anticipated income. Often called income capitalization Capitalize:

Broker. Investment Real Estate. Chapter 15. Copyright Gold Coast Schools 1

Broker Chapter 15 Investment Real Estate Copyright Gold Coast Schools 1 Learning Objectives Matching an investor with the right property Evaluating the sites and improvements of income properties Determining

Broker Chapter 15 Investment Real Estate Copyright Gold Coast Schools 1 Learning Objectives Matching an investor with the right property Evaluating the sites and improvements of income properties Determining

THE APPRAISAL OF REAL ESTATE 3 RD CANADIAN EDITION BUSI 330

THE APPRAISAL OF REAL ESTATE 3 RD CANADIAN EDITION BUSI 330 REVIEW NOTES by CHUCK DUNN CHAPTER 20 Copyright 2010 by the Real Estate Division and Chuck Dunn. All rights reserved CHAPTER 20 - THE INCOME

THE APPRAISAL OF REAL ESTATE 3 RD CANADIAN EDITION BUSI 330 REVIEW NOTES by CHUCK DUNN CHAPTER 20 Copyright 2010 by the Real Estate Division and Chuck Dunn. All rights reserved CHAPTER 20 - THE INCOME

MPEEM The New and Improved Residual Technique of Reserve Valuation

MPEEM The New and Improved Residual Technique of Reserve Valuation Prepared by Alan K. Stagg, PG, CMA Stagg Resource Consultants, Inc. Cross Lanes, West Virginia ABSTRACT The residual technique of reserve

MPEEM The New and Improved Residual Technique of Reserve Valuation Prepared by Alan K. Stagg, PG, CMA Stagg Resource Consultants, Inc. Cross Lanes, West Virginia ABSTRACT The residual technique of reserve

Business Valuation More Art Than Science

Business Valuation More Art Than Science One of the more difficult aspects of business planning is business valuation. It is also one of the more important aspects. While owners of closely held businesses

Business Valuation More Art Than Science One of the more difficult aspects of business planning is business valuation. It is also one of the more important aspects. While owners of closely held businesses

GENERAL ASSESSMENT DEFINITIONS

21st Century Appraisals, Inc. GENERAL ASSESSMENT DEFINITIONS Ad Valorem tax. A tax levied in proportion to the value of the thing(s) being taxed. Exclusive of exemptions, use-value assessment laws, and

21st Century Appraisals, Inc. GENERAL ASSESSMENT DEFINITIONS Ad Valorem tax. A tax levied in proportion to the value of the thing(s) being taxed. Exclusive of exemptions, use-value assessment laws, and

How to Read a Real Estate Appraisal Report

How to Read a Real Estate Appraisal Report Much of the private, corporate and public wealth of the world consists of real estate. The magnitude of this fundamental resource creates a need for informed

How to Read a Real Estate Appraisal Report Much of the private, corporate and public wealth of the world consists of real estate. The magnitude of this fundamental resource creates a need for informed

SOLUTIONS Learning Goal 19

S1 Learning Goal 19 Multiple Choice 1. b 2. a 3. c 4. b However, the double-declining-balance method calculates the depreciation expense on the full asset cost until the final year of use. 5. d Total appraised

S1 Learning Goal 19 Multiple Choice 1. b 2. a 3. c 4. b However, the double-declining-balance method calculates the depreciation expense on the full asset cost until the final year of use. 5. d Total appraised

Raising Your Commercial IQ

Raising Your Commercial IQ Real Estate Investment & Lease Analysis January 2013 0 P age Neil Osborne M.B.A. DL. (604) 988-5518 nosborne@investitsoftware.com Investit Software Inc. Toll free 877-878-1828

Raising Your Commercial IQ Real Estate Investment & Lease Analysis January 2013 0 P age Neil Osborne M.B.A. DL. (604) 988-5518 nosborne@investitsoftware.com Investit Software Inc. Toll free 877-878-1828

Published in Spring 1986 Issue The Real Estate Appraiser & Analyst Society of Real Estate Appraisers 1

(1) Published in Spring 1986 Issue The Real Estate Appraiser & Analyst Society of Real Estate Appraisers 1 Alternative Valuation Methods for Leasehold Properties By Tony Sevelka, AACI, SREA, MAI, CRE Introduction

(1) Published in Spring 1986 Issue The Real Estate Appraiser & Analyst Society of Real Estate Appraisers 1 Alternative Valuation Methods for Leasehold Properties By Tony Sevelka, AACI, SREA, MAI, CRE Introduction

INSTITUTE FOR PROFESSIONALS IN TAXATION REAL PROPERTY TAX SCHOOL REVIEW AND INTRODUCTION

INSTITUTE FOR PROFESSIONALS IN TAXATION REAL PROPERTY TAX SCHOOL REVIEW AND INTRODUCTION This section is an overview of the major topics covered by IPT s Property Tax School which are directly relevant

INSTITUTE FOR PROFESSIONALS IN TAXATION REAL PROPERTY TAX SCHOOL REVIEW AND INTRODUCTION This section is an overview of the major topics covered by IPT s Property Tax School which are directly relevant

Definitions. CPI is a lease in which base rent is adjusted based on changes in a consumer price index.

Annualized Rental Income is rental revenue under our leases on Operating Properties on a straight-line basis, which includes the effect of rent escalations and any tenant concessions, such as free rent,

Annualized Rental Income is rental revenue under our leases on Operating Properties on a straight-line basis, which includes the effect of rent escalations and any tenant concessions, such as free rent,

Tenant: Law Firm 4 NAICS: Primary Industry: Offices of lawyers

Tenant: Law Firm 4 NAICS: 541110 Primary Industry: Offices of lawyers Date: 05.25.17 Table of Contents Law Firm 4 132 Main Street TABLE OF CONTENTS TIL Score Executive Summary Tenant Score Information

Tenant: Law Firm 4 NAICS: 541110 Primary Industry: Offices of lawyers Date: 05.25.17 Table of Contents Law Firm 4 132 Main Street TABLE OF CONTENTS TIL Score Executive Summary Tenant Score Information

Procedures Used to Calculate Property Taxes for Agricultural Land in Mississippi

No. 1350 Information Sheet June 2018 Procedures Used to Calculate Property Taxes for Agricultural Land in Mississippi Stan R. Spurlock, Ian A. Munn, and James E. Henderson INTRODUCTION Agricultural land

No. 1350 Information Sheet June 2018 Procedures Used to Calculate Property Taxes for Agricultural Land in Mississippi Stan R. Spurlock, Ian A. Munn, and James E. Henderson INTRODUCTION Agricultural land

2016 Level I Tutorials. Income Approach to Value

2016 Level I Tutorials Income Approach to Value 1 The income approach is based on the principal that the value of an investment property reflects the quality and quantity of the income it is expected to

2016 Level I Tutorials Income Approach to Value 1 The income approach is based on the principal that the value of an investment property reflects the quality and quantity of the income it is expected to

March 23, 2006 Anderson ECON 136A 11am Class FINAL EXAM v. 1 Name

March 23, 2006 Anderson ECON 136A 11am Class FINAL EXAM v. 1 Name YOU MUST WRITE YOUR NAME ON THIS EXAM AND TURN IT IN WITH YOUR SCANTRON AND BLUE-BOOK! Complete questions #1-25 on your scantron AND WRITE

March 23, 2006 Anderson ECON 136A 11am Class FINAL EXAM v. 1 Name YOU MUST WRITE YOUR NAME ON THIS EXAM AND TURN IT IN WITH YOUR SCANTRON AND BLUE-BOOK! Complete questions #1-25 on your scantron AND WRITE

The construction loan collapses a series of costs (cash outflows) incurred during the construction process into a single value

incurred during the construction process into a single value") he construction loan collapses a series of costs (cash outflows) incurred during the construction process into a single value as of a single (future) point in time (the projected completion date of the

he construction loan collapses a series of costs (cash outflows) incurred during the construction process into a single value as of a single (future) point in time (the projected completion date of the

CHAPTER 18 Lease Financing and Business Valuation

Copyright 2008 by the Foundation of the American College of Healthcare Executives 6/13/07 Version 18-1 CHAPTER 18 Lease Financing and Business Valuation Lease financing Leasing basics Analysis by the lessee

Copyright 2008 by the Foundation of the American College of Healthcare Executives 6/13/07 Version 18-1 CHAPTER 18 Lease Financing and Business Valuation Lease financing Leasing basics Analysis by the lessee

WYOMING DEPARTMENT OF REVENUE CHAPTER 7 PROPERTY TAX VALUATION METHODOLOGY AND ASSESSMENT (DEPARTMENT ASSESSMENTS)

") CHAPTER 7 PROPERTY TAX VALUATION METHODOLOGY AND ASSESSMENT (DEPARTMENT ASSESSMENTS) Section 1. Authority. These Rules are promulgated under the authority of W.S. 39-11-102(b). Section 2. Purpose of Rules.

CHAPTER 7 PROPERTY TAX VALUATION METHODOLOGY AND ASSESSMENT (DEPARTMENT ASSESSMENTS) Section 1. Authority. These Rules are promulgated under the authority of W.S. 39-11-102(b). Section 2. Purpose of Rules.

2) All long-term leases should be capitalized in the accounts by the lessee.

All long-term leases should be capitalized in the accounts by the lessee.") Chapter 18 Leases 1) The principal attribute of finance leases is that the risks and rewards of asset ownership are deemed to remain with the lessor. LO: 18-02 List the criteria for classification of a

Chapter 18 Leases 1) The principal attribute of finance leases is that the risks and rewards of asset ownership are deemed to remain with the lessor. LO: 18-02 List the criteria for classification of a

The Cost of Property, Plant, Equipment

1 The Cost of Property, Plant, Equipment The cost of property, plant, and equipment includes the purchase price of the asset and all expenditures necessary to prepare the asset for its intended use. Land.

1 The Cost of Property, Plant, Equipment The cost of property, plant, and equipment includes the purchase price of the asset and all expenditures necessary to prepare the asset for its intended use. Land.

Lease-Versus-Buy. By Steven R. Price, CCIM

Lease-Versus-Buy Cost Analysis By Steven R. Price, CCIM Steven R. Price, CCIM, Benson Price Commercial, Colorado Springs, Colorado, has a national tenant representation and consulting practice. He was

Lease-Versus-Buy Cost Analysis By Steven R. Price, CCIM Steven R. Price, CCIM, Benson Price Commercial, Colorado Springs, Colorado, has a national tenant representation and consulting practice. He was

Auditing PP&E, Including Leases

Auditing PP&E, Including Leases Learning Objectives Discuss typical audit risks and special considerations. Tailor an audit plan to assessed audit risk. Explain key controls related to PP&E. Describe lease

Auditing PP&E, Including Leases Learning Objectives Discuss typical audit risks and special considerations. Tailor an audit plan to assessed audit risk. Explain key controls related to PP&E. Describe lease

Chapter 37. The Appraiser's Cost Approach INTRODUCTION

Chapter 37 The Appraiser's Cost Approach INTRODUCTION The cost approach for estimating current market value starts with the recognition that a parcel of real estate contains two components - the land and

Chapter 37 The Appraiser's Cost Approach INTRODUCTION The cost approach for estimating current market value starts with the recognition that a parcel of real estate contains two components - the land and

Table of Contents SECTION 1. Overview... ix. Course Schedule... xiii. Introduction. Part 1. Introduction to the Income Capitalization Approach

Table of Contents Overview... ix Course Schedule... xiii SECTION 1 Introduction Part 1. Introduction to the Income Capitalization Approach Preview Part 1... 1 Market Value... 3 Anticipation and Other Relevant

Table of Contents Overview... ix Course Schedule... xiii SECTION 1 Introduction Part 1. Introduction to the Income Capitalization Approach Preview Part 1... 1 Market Value... 3 Anticipation and Other Relevant

Basics of Commercial Real Estate Transactions Day Two

Basics of Commercial Real Estate Transactions Day Two John Rockwell, Partner Energy October 12, 2016 PG&E refers to the Pacific Gas and Electric Company, a subsidiary of PG&E Corporation. 2010 Pacific

Basics of Commercial Real Estate Transactions Day Two John Rockwell, Partner Energy October 12, 2016 PG&E refers to the Pacific Gas and Electric Company, a subsidiary of PG&E Corporation. 2010 Pacific

Broker. Sales Comparison, Cost Depreciation and Income Approaches. Chapter 7. Copyright Gold Coast Schools 1

Broker Chapter 7 Sales Comparison, Cost Depreciation and Income Approaches 1 Learning Objectives Describe the assumptions underlying the sales comparison approach Calculate the various adjustments necessary

Broker Chapter 7 Sales Comparison, Cost Depreciation and Income Approaches 1 Learning Objectives Describe the assumptions underlying the sales comparison approach Calculate the various adjustments necessary

In-Depth Capitalization Rate Review

In-Depth Capitalization Rate Review Leonard J. Patcella, Jr., CMI, MAI President Equity Appraisal Co., Inc. Springhouse, PA jack.equityappraisal@comcast.net David A. Schneider, Esq. Partner Archer & Greiner,

In-Depth Capitalization Rate Review Leonard J. Patcella, Jr., CMI, MAI President Equity Appraisal Co., Inc. Springhouse, PA jack.equityappraisal@comcast.net David A. Schneider, Esq. Partner Archer & Greiner,

Sales Associate Course

Sales Associate Course Chapter Sixteen Appraisal 1 2 Appraiser Specific amount Impartial (non biased) Defendable Estimate (Opinion) of value Fee based on time and difficulty Must follow Uniform Standards

Sales Associate Course Chapter Sixteen Appraisal 1 2 Appraiser Specific amount Impartial (non biased) Defendable Estimate (Opinion) of value Fee based on time and difficulty Must follow Uniform Standards

Cornerstone 2 Basic Valuation of Machinery and Equipment

INSTITUTE FOR PROFESSIONALS IN TAXATION PERSONAL PROPERTY TAX SCHOOL Cornerstone 2 Basic Valuation of Machinery and Equipment Learning Objectives At the end of this section, the learner will be able to:

INSTITUTE FOR PROFESSIONALS IN TAXATION PERSONAL PROPERTY TAX SCHOOL Cornerstone 2 Basic Valuation of Machinery and Equipment Learning Objectives At the end of this section, the learner will be able to:

Initial sales ratio to determine the current overall level of value. Number of sales vacant and improved, by neighborhood.

Introduction The International Association of Assessing Officers (IAAO) defines the market approach: In its broadest use, it might denote any valuation procedure intended to produce an estimate of market

Introduction The International Association of Assessing Officers (IAAO) defines the market approach: In its broadest use, it might denote any valuation procedure intended to produce an estimate of market

Four (4) Factors in Investment Definition: Investment

Factors in Investment Definition: Investment") Introductions Your name Where you work Your job responsibilities How long you have been in the industry What you hope to get from this class Chapter 1: Investments Agenda 2 Investments Adding Value to

Introductions Your name Where you work Your job responsibilities How long you have been in the industry What you hope to get from this class Chapter 1: Investments Agenda 2 Investments Adding Value to

UNCORRECTED SAMPLE PAGES

339 Chapter 13 Accounting for non-current assets 1 Where are we headed? After completing this chapter, you should be able to: identify the characteristics of a depreciable noncurrent asset define depreciation,

339 Chapter 13 Accounting for non-current assets 1 Where are we headed? After completing this chapter, you should be able to: identify the characteristics of a depreciable noncurrent asset define depreciation,

Credit Risk. Thinkstock. 42 May 2013 The RMA Journal Copyright 2013 by RMA

CR Credit Risk Thinkstock 42 May 2013 The RMA Journal Copyright 2013 by RMA Pitfalls in Conventional Earnings-Based DSCR Measures and a Recommended Alternative BY DAVID ANDRUKONIS, CRC FOR LENDERS, a significant

CR Credit Risk Thinkstock 42 May 2013 The RMA Journal Copyright 2013 by RMA Pitfalls in Conventional Earnings-Based DSCR Measures and a Recommended Alternative BY DAVID ANDRUKONIS, CRC FOR LENDERS, a significant

DETERMINING AGENCY VALUE PART 2