Fleming s Restaurant Ground Lease College Parkway Livonia, Michigan 48152

|

|

|

- Cecil Ford

- 5 years ago

- Views:

Transcription

1 Capital Markets Private Capital Group Fleming s Restaurant Ground Lease College Parkway Livonia, Michigan :: offering memorandum PCG Detroit Capital Markets Driving Price and Adding Value through Experience and Market Knowledge

2 Table of contents Executive Summary Investment Highlights The Offering Investment Summary Financial Overview Property Description Site Plan Area Maps Aerial Maps Area Overview Location Overview Demographic Profile Market Overview Rent Comparables Rent Comparable Analysis Rent Comparables Sale Comparables Sale Comparable Analysis Sales Comparables Financials - Fleming s Summary of Financial Assumptions Lease Abstract Tenant Overview Year One Cash Flow College Park - Flemings

3 Fleming s - College Park Executive Summary 01 Executive Summary Investment Highlights The Offering Investment Summary Financial Overview Property Description Site Plan Area Maps Aerial Maps

4 EXECUTIVE SUMMARY The Offering CBRE, Inc. has been retained by current ownership as the exclusive marketing advisor for the disposition of The Fleming s Restaurant Ground Lease consisting of 7,898 square feet located at College Park in Livonia, Michigan. The Summary Investment Highlights Currently 100% Occupied, Just Under Five Years Remain on the Current Lease Term Ground Leased to Fleming s Restaurant. The is lease Guaranteed by Outback Steakhouse with a Credit Rating of B- According to S & P Excellent Store Sales Excellent Demographics, One Mile Average Household Income of Over $100,000 Great Visibility and Frontage Along I-275 and College Parkway Close Access to Haggerty Road, Six Mile and Seven Mile Roads and I-275 Located Less Than Two Miles from Laurel Park Place Mall with over 609,000 Square Feet Anchored by Parisian and Von Maur Numerous Tenant Amenities Including Hotels, Banking, Many Retail Options and Some Within Walking Distance The Fleming s Restaurant was constructed in 2006 and consists of 7,898 square feet of office space. Fleming s signed an initial ground lease commencing in February of 2006 and runs through November, 2016 with 4.8 years remaining on their current term, from our projected closing date of February 1, Fleming s is on a ground lease and is responsible for reimbursing the landlord for common area expenses plus an administrative fee of 15 percent on top of CAM. The ground lease is guaranteed by Outback Steakhouse, Inc which carries a B- investment rating by Standard & Poor s. Fleming s is a fine steakouse and this location is one of two in the entire State of Michigan. The property is strategically located within the acre master-planned College Park Condominium Association Development, surrounded by numerous amenities including restaurants, abundant retail shopping, Schoolcraft College (enrollment of over 13,000 students) and various hotels. The I-275 freeway is just east of the property with an interchange just south of the property at the Six Mile Road exit and north at the Seven Mile Road Exit, which provides easy access throughout Metro Detroit. In addition to the Fleming s Restaurant Building, the adjacent single tenant buildings; TCF National Bank Building (S&P rated BBB) a 60,000 square foot office building leased through 11/2021 (9.8 years remaining), Trinity Senior Living Communities (S&P rated AA) a 39,673 square foot office building leased through 12/2020 (8.9 years remaining), and the Market Strategies office building consisting of 59,742 square feet leased through 7/2023 (11.5 years remaining). Please contact Bill O Connor for Executive Summary 3

4.")

5 FINANCIAL OVERVIEW Asking Sales Price $984,500 Down Payment Price per Square Foot All Cash $ CAP Rate 8.00% Financing Offered free and clear of existing financing Building information Fleming s - College Park Property College Parkway Livonia, MI Building Square Feet (RBA) 7,898 Square Feet Property Type Single Tenant Restaurant Ground Lease Year Built 2006 Parcel Size (Acres) 4.56 Acres Current Occupancy 100% Executive Summary 4

7,898 Square Feet Parcel Size 4.")

6 Property details GENERAL Property INFORMATION Property Address Fleming s - College Park College Parkway Livonia, Michigan County Wayne County Year Constructed 2006 Parcel Number Building Size (Rentable Building Area) 7,898 Square Feet Parcel Size 4.56 Acres Zoning C-2, General Business Number of Stories One Access One via College Parkway, visibility from I-275 BUILDING DETAILS Exterior Walls Brick Roof Rubber Membrane Structue Structural Steel Columns Foundation Poured Concrete Parking Surface Asphalt Paved Fire Protection To Code HVAC Roof Mounted Units Utilities All to Site Plumbing To Code Property Description 5

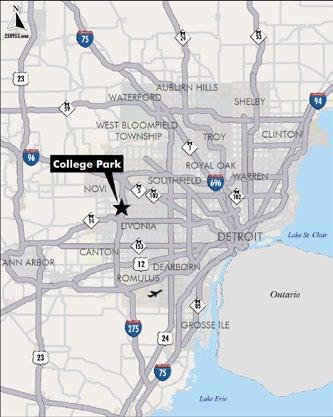

7 Area Maps Property Description 6

8 COLLEGE PARK Development Property Description 7

9 Close up aerial view Property Description 8

10 AERIAL VIEW Property Description 9

11 Fleming s - College Park Area Overview 02 Area Overview Location Overview Demographic Profile Market Overview

12 AREA overview City of Livonia Livonia, Michigan, is a safe, well-planned community of 36 square miles located in northwest Wayne County. City boundaries are Inkster Road on the east, Eight Mile Road on the north, Eckles Road and Haggerty Road on the west and Joy Road on the south. Livonia enjoys a strategic location second-to-none in the region, with easy eastwest access via the Jeffries Expressway (I-96) and northsouth along the I-275 expressway. Our main roads fan out in every direction providing convenient drive times throughout the metropolitan area. Location Overview The subject property is located along the south side of College Parkway with frontage and visibility along I-275. College Parkway is on the east side of Haggerty Road, just north of Six Mile Road. The subject property is located with in the College Park Condominium Association Development which consists of four office buildings and five retail properties including single tenant free-standing restaurants (Mitchell s Seafood, Bravo and Fleming s) as well as the College Park Marketplace shopping center consisting of 14,082 square feet and anchored by Caribou and Potbelly. The College Park development is across from the Northville Center anchored by Kroger, Bed, Bath & Beyond, Barnes & Noble and Staples. The property is located within the Southern I-275 submarket which consists of 789 office buildings totaling 10.7 million square feet of office space. The current occupancy for the submarket is 84 percent with rents ranging from $7.39 to $35.40 per square foot gross. The average rental rate for the submarket is $17.46 per square foot gross. With a population of just under 100,000 in the 2010 Census, Livonia is listed as the third-largest city in Wayne County and the ninth largest city in Michigan. Livonia was recognized by the FBI as the Second Safest City in Michigan (populations over 75,000). Over the years, Livonia has earned other accolades. It has been named as the Second Best Kid Friendly Place in the Nation by Population Connection; the Second Least Economic Stressful by the City American City Business Journals; and one of the top 50 Green Cities in the U.S. by Popular Science in There are some 4,300 businesses in Livonia. Major local employers include Ford Motor Company, United Parcel Services (UPS), Roush Enterprises, NYX Inc., Phillips Service Industries, Inc., McLaren Performance Technologies, and St. Mary Mercy Hospital. Livonia s industry is largely concentrated in a 6-square-mile corridor combining major railroad and highway access to all sections of the metropolitan region. Wayne County The property is located in Wayne County, which is the 13th most-populous county in the United States. The county seat is Detroit, the largest city in Michigan. Wayne County is located in southeastern Michigan, encompassing approximately 623 square miles. It is made up of 34 cities, including the city of Detroit, nine townships and 41 public school districts and its population consists of approximately two million. Companies Doing General Electric General Motors Severstal North Business in Wayne A123 Systems Fisher Coachworks America County: Ford Motor Company Great Lakes Recycling Area Overview 11

13 demographic profile 1 mile radius 3 mile radius 5 mile radius 2011 Estimated Population 6,796 65, , Projected Population 6,665 62, , Census Population 6,938 71, , Census Population 5,248 67, ,412 Growth % -8.33% -6.46% Growth % -4.46% -3.53% 2011 Estimated Median Age Estimated Average Age Estimated Households 2,592 25,526 75, Projected Households 2,537 24,428 72, Census Households 2,672 27,900 80, Census Households 1,874 24,698 71,674 Growth % -8.51% -6.62% Growth % -4.30% -3.39% 2011 Est. Average Household Size Est. Median Household Income $88,565 $77,064 $69, Prj. Median Household Income $89,054 $77,279 $69, Cen. Median Household Income $82,543 $73,883 $65, Cen. Median Household Income $55,176 $56,103 $48, Est. Average Household Income $102,246 $94,821 $88, Estimated Per Capita Income $39,468 $37,184 $36, Estimated Housing Units 2,721 26,750 79, Estimated Occupied Units 2,592 25,526 75, Estimated Vacant Units 130 1,224 4, Est. Owner Occupied Units 2,210 20,206 53, Est. Renter Occupied Units 381 5,320 21, Est. Median Housing Value $255,917 $214,788 $195, Est. Average Housing Value $272,405 $237,748 $224,346 Area Overview 12

14 demographic profile 1 mile radius 3 mile radius 5 mile radius 2011 Estimated Households 2,592 25,526 75,144 - Income Less than $15, (7.1%) 1,215 (4.8%) 4,547 (6.1%) - Income $15,000 to $24, (4.6%) 1,410 (5.5%) 5,421 (7.2%) - Income $25,000 to $34, (4.6%) 1,819 (7.1%) 6,284 (8.4%) - Income $35,000 to $49, (9.0%) 2,992 (11.7%) 9,631 (12.8%) - Income $50,000 to $74, (16.9%) 4,944 (19.4%) 14,650 (19.5%) - Income $75,000 to $99, (14.2%) 4,269 (16.7%) 11,988 (16.0%) - Income $100,000 to $149, (25.5%) 5,321 (20.8%) 13,407 (17.8%) - Income $150,000 to $199, (11.5%) 1,904 (7.5%) 4,487 (6.0%) - Income $200,000 to $499, (6.3%) 1,491 (5.8%) 4,142 (5.5%) - Income $500,000 and over 12 (.5%) 161 (.6%) 586 (.8%) 2011 Est. Average Household Income $102,246 $94,821 $88, Prj. Average Household Income $102,498 $94,860 $89, Cen. Avg. Household Income $95,791 $89,717 $83, Cen. Avg. Household Income $63,707 $64,071 $58, Estimated Households by Household Size 2,592 25,526 75,144-1 Person Household 638 (24.6%) 6,412 (25.1%) 22,253 (29.6%) - 2 Person Household 948 (36.6%) 8,916 (34.9%) 25,288 (33.7%) - 3 Person Household 399 (15.4%) 3,954 (15.5%) 11,315 (15.1%) - 4 Person Household 390 (15.0%) 4,010 (15.7%) 10,583 (14.1%) - 5 Person Household 157 (6.1%) 1,630 (6.4%) 4,168 (5.5%) - 6 Person Household 46 (1.8%) 472 (1.8%) 1,203 (1.6%) - 7 or More Person Household 13 (.5%) 132 (.5%) 334 (.4%) 2011 Est. Average Household Size Estimated Households by 2,592 25,526 75,144 Number of Vehicles - Households with No Vehicles 131 (5.1%) 843 (3.3%) 3,494 (4.6%) - Households with 1 Vehicle 764 (29.5%) 7,868 (30.8%) 25,580 (34.0%) - Households with 2 Vehicles 1,149 (44.3%) 11,407 (44.7%) 32,445 (43.2%) - Households with 3 Vehicles 397 (15.3%) 3,839 (15.0%) 9,990 (13.3%) - Households with 4 Vehicles 116 (4.5%) 1,200 (4.7%) 2,794 (3.7%) - Households with 5+ Vehicles 35 (1.4%) 369 (1.4%) 840 (1.1%) 2011 Est. Average Number of Vehicles Area Overview 13

15 demographic profile 2011 Estimated Population by Race and Origin 1 mile radius 3 mile radius 5 mile radius 6,796 65, ,342 - White Population 6,279 (92.4%) 60,004 (91.7%) 159,963 (86.8%) - Black Population 89 (1.3%) 1,216 (1.9%) 6,944 (3.8%) - Asian Population 305 (4.5%) 3,213 (4.9%) 13,574 (7.4%) - Pacific Islander Population 3 (.0%) 5 (.0%) 65 (.0%) - American Indian and Alaska Native 8 (.1%) 94 (.1%) 365 (.2%) - Other Race Population 34 (.5%) 259 (.4%) 1,001 (.5%) - Two or More Races Population 78 (1.1%) 653 (1.0%) 2,430 (1.3%) - Hispanic Population 117 (1.7%) 1,249 (1.9%) 4,103 (2.2%) - White Non-Hispanic Population 6,277 (92.4%) 59,627 (91.1%) 158,988 (86.2%) 2011 Estimated Population by Age 6,796 65, ,342 - Aged 0 to 4 Years 269 (4.0%) 2,981 (4.6%) 8,991 (4.9%) - Aged 5 to 9 Years 290 (4.3%) 3,206 (4.9%) 9,884 (5.4%) - Aged 10 to 14 Years 315 (4.6%) 3,373 (5.2%) 10,365 (5.6%) - Aged 15 to 17 Years 286 (4.2%) 2,958 (4.5%) 7,695 (4.2%) - Aged 18 to 20 Years 206 (3.0%) 2,248 (3.4%) 5,799 (3.1%) - Aged 21 to 24 Years 320 (4.7%) 3,263 (5.0%) 8,620 (4.7%) - Aged 25 to 34 Years 683 (10.1%) 7,098 (10.8%) 21,204 (11.5%) - Aged 35 to 44 Years 569 (8.4%) 6,984 (10.7%) 23,714 (12.9%) - Aged 45 to 54 Years 1,240 (18.2%) 11,863 (18.1%) 31,965 (17.3%) - Aged 55 to 64 Years 1,176 (17.3%) 10,419 (15.9%) 26,459 (14.4%) - Aged 65 to 74 Years 685 (10.1%) 5,884 (9.0%) 14,998 (8.1%) - Aged 75 to 84 Years 522 (7.7%) 3,587 (5.5%) 9,764 (5.3%) - Aged 85 Years and Older 235 (3.5%) 1,580 (2.4%) 4,884 (2.6%) 2011 Estimated Median Age Estimated Average Age Estimated Population Over 25 by Educational Attainment 5,110 47, ,989 - Less than 9th Grade 148 (2.9%) 863 (1.8%) 2,821 (2.1%) - High School - No Diploma 229 (4.5%) 1,512 (3.2%) 5,384 (4.0%) - High School Diploma 1,024 (20.0%) 9,128 (19.3%) 27,220 (20.5%) - Some College 1,070 (20.9%) 9,912 (20.9%) 27,912 (21.0%) - Associate Degree 311 (6.1%) 3,718 (7.8%) 10,176 (7.7%) - Bachelor's Degree 1,397 (27.3%) 13,218 (27.9%) 35,688 (26.8%) - Master's Degree 682 (13.3%) 7,197 (15.2%) 18,791 (14.1%) - Professional Degree 179 (3.5%) 1,375 (2.9%) 3,497 (2.6%) - Doctoral Degree 70 (1.4%) 493 (1.0%) 1,500 (1.1%) Area Overview 14

16 demographic profile 2011 Estimated Owner Occupied Units by Housing Value 1 mile radius 3 mile radius 5 mile radius 2,210 20,206 53,481 - Valued Less than $20, (.1%) 193 (.4%) - Valued $20,000-$39,999 3 (.1%) 44 (.2%) 303 (.6%) - Valued $40,000-$59, (.5%) 103 (.5%) 575 (1.1%) - Valued $60,000-$79, (1.1%) 257 (1.3%) 963 (1.8%) - Valued $80,000-$99, (1.7%) 594 (2.9%) 1,919 (3.6%) - Valued $100,000-$149, (9.5%) 2,988 (14.8%) 9,721 (18.2%) - Valued $150,000-$199, (12.1%) 4,752 (23.5%) 14,268 (26.7%) - Valued $200,000-$299, (44.5%) 7,606 (37.6%) 16,395 (30.7%) - Valued $300,000-$399, (20.5%) 2,399 (11.9%) 5,079 (9.5%) - Valued $400,000-$499, (8.1%) 828 (4.1%) 2,083 (3.9%) - Valued $500,000-$749, (1.8%) 458 (2.3%) 1,453 (2.7%) - Valued $750,000-$999,999 4 (.2%) 83 (.4%) 304 (.6%) - Valued More than $1,000, (.4%) 225 (.4%) 2011 Est. Median Housing Value $255,917 $214,788 $195, Est. Average Housing Value $272,405 $237,748 $224, Estimated Housing Units by Housing Type 2,721 26,750 79,207-1 Unit Detached 1,618 (59.5%) 17,889 (66.9%) 49,129 (62.0%) - 1 Unit Attached 605 (22.2%) 3,063 (11.5%) 7,282 (9.2%) - 2 Units 38 (1.4%) 247 (.9%) 679 (.9%) Units 296 (10.9%) 4,656 (17.4%) 17,306 (21.8%) Units 18 (.7%) 355 (1.3%) 1,651 (2.1%) Units 140 (5.1%) 517 (1.9%) 2,794 (3.5%) - Mobile Home 6 (.2%) 22 (.1%) 354 (.4%) - Boat, RV, Van or Other 1 (.0%) 2 (.0%) 11 (.0%) 2011 Estimated Housing Units by Year Structure Built 2,721 26,750 79,207 - Structure Built 2000 or Later 256 (9.4%) 1,136 (4.2%) 4,179 (5.3%) - Structure Built 1990 to (29.2%) 3,466 (13.0%) 9,447 (11.9%) - Structure Built 1980 to ,055 (38.8%) 6,504 (24.3%) 14,919 (18.8%) - Structure Built 1970 to (12.5%) 6,477 (24.2%) 18,642 (23.5%) - Structure Built 1960 to (4.3%) 5,813 (21.7%) 14,832 (18.7%) - Structure Built 1950 to (4.2%) 1,895 (7.1%) 10,426 (13.2%) - Structure Built 1940 to (1.0%) 633 (2.4%) 2,873 (3.6%) - Structure Built Before (.7%) 827 (3.1%) 3,888 (4.9%) 2011 Est. Median Year Structure Built Area Overview 15

17 demographic profile 1 mile radius 3 mile radius 5 mile radius 2011 Estimated Population by Sex 6,796 65, ,342 - Male 3,223 (47.4%) 31,628 (48.3%) 89,213 (48.4%) - Female 3,573 (52.6%) 33,817 (51.7%) 95,129 (51.6%) 2011 Estimated Pop. over 15 by Marital Status 5,922 55, ,102 - Males Never Married 846 (14.3%) 8,108 (14.5%) 23,423 (15.1%) - Males Married 1,686 (28.5%) 16,171 (28.9%) 43,368 (28.0%) - Males Widowed 72 (1.2%) 609 (1.1%) 1,827 (1.2%) - Males Divorced 172 (2.9%) 1,847 (3.3%) 5,701 (3.7%) - Females Never Married 725 (12.2%) 7,717 (13.8%) 21,427 (13.8%) - Females Married 1,751 (29.6%) 16,083 (28.8%) 42,539 (27.4%) - Females Widowed 387 (6.5%) 2,723 (4.9%) 8,502 (5.5%) - Females Divorced 282 (4.8%) 2,629 (4.7%) 8,317 (5.4%) 2011 Estimated Population in Group Quarters 355 1,348 4,536 - Institutional Group Quarters 266 (74.9%) 876 (65.0%) 3,388 (74.7%) - Non-Institutional Group Quarters 89 (25.1%) 472 (35.0%) 1,149 (25.3%) 2011 Estimated Occupied Housing Units by Year Occ. Moved In 2,592 25,526 75,144 - Moved In 2000 or Later 1,103 (42.6%) 10,376 (40.6%) 37,752 (50.2%) - Moved In (31.3%) 6,343 (24.8%) 16,984 (22.6%) - Moved In (20.6%) 4,177 (16.4%) 9,605 (12.8%) - Moved In (4.2%) 3,194 (12.5%) 6,933 (9.2%) - Moved In 1969 or Earlier 32 (1.2%) 1,436 (5.6%) 3,871 (5.2%) Area Overview 16

18 demographic profile 2011 Estimated Employed Population by Occupation 1 mile radius 3 mile radius 5 mile radius 3,382 35,274 98,354 - Management 582 (17.2%) 5,290 (15.0%) 13,947 (14.2%) - Business and Financial Operations 258 (7.6%) 2,501 (7.1%) 6,990 (7.1%) - Professional and Related 708 (20.9%) 7,892 (22.4%) 21,912 (22.3%) - Sales 475 (14.0%) 4,923 (14.0%) 12,950 (13.2%) - Office Support 381 (11.3%) 4,168 (11.8%) 12,475 (12.7%) - Service 275 (8.1%) 3,912 (11.1%) 11,092 (11.3%) - Health Care Support 369 (10.9%) 3,098 (8.8%) 7,920 (8.1%) - Farming, Fishing, and Forestry 2 (.1%) 16 (.0%) 85 (.1%) - Construction, Extraction, and 144 (4.3%) 1,384 (3.9%) 4,220 (4.3%) Maintenance - Production, Transportation, and Material Moving 2011 Estimated Employed Population Over 16 by Primary Transportation to Work - Car, Truck, Van or Motorcycle to Work 187 (5.5%) 2,091 (5.9%) 6,764 (6.9%) 3,274 34,695 96,921 3,031 (92.6%) 31,752 (91.5%) 86,931 (89.7%) - Carpooled 108 (3.3%) 1,283 (3.7%) 4,587 (4.7%) - Public Transportation to Work 6 (.2%) 125 (.4%) 308 (.3%) - Other Transportation to Work 54 (1.6%) 542 (1.6%) 1,792 (1.8%) - Work at Home 76 (2.3%) 993 (2.9%) 3,303 (3.4%) 2011 Estimated Employed Population Over 16 by Travel Time to Work 3,274 34,695 96,921 - Travel Time Less than 15 Min 1,003 (30.6%) 9,323 (26.9%) 26,411 (27.3%) - Travel Time Min 923 (28.2%) 11,585 (33.4%) 33,526 (34.6%) - Travel Time Min 1,027 (31.4%) 9,533 (27.5%) 24,440 (25.2%) - Travel Time Min 226 (6.9%) 2,457 (7.1%) 7,149 (7.4%) - Travel Time 60+ Min 41 (1.3%) 1,089 (3.1%) 2,977 (3.1%) Est. Average Travel Time Estimated Population Over 16 5,823 54, ,443 Years Old by Employment Status - Civilian Males 1,627 (27.9%) 17,475 (31.8%) 49,574 (32.5%) - Civilian Females 1,463 (25.1%) 15,178 (27.7%) 41,735 (27.4%) - Armed Forces Male 5 (.1%) 30 (.1%) 56 (.0%) - Armed Forces Female 0 3 (.0%) 16 (.0%) - Unemployed Males 81 (1.4%) 999 (1.8%) 3,276 (2.1%) - Unemployed Females 98 (1.7%) 974 (1.8%) 2,755 (1.8%) - Not in the Labor Force Male 1,016 (17.4%) 7,723 (14.1%) 20,118 (13.2%) - Not in the Labor Force Female 1,532 (26.3%) 12,489 (22.8%) 34,914 (22.9%) Area Overview 17

19 Detroit Market Report CBRE Detroit Office Third Quarter 2011 Quick Stats Vacancy 28.1% Lease Rates $17.55 Construction 55,000 Net Absorption 139,489 Change from last Current Yr. Qtr. *The arrows are trend indicators over the specified time period and do not represent a positive or negative value. (e.g., absorption could be negative, but still represent a positive trend over a specified period.) Hot Topics Quicken Loans CEO Dan Gilbert purchased both the First National Building and Dime Building in Detroit s CBD General Motors U.S. light vehicle sales increased by 18% in the month of August, which can be attributed to a GMC sales increase of 41% Chrysler Group outperformed Toyota Motor Sales U.S.A in the month of August after posting a sales increase of 31%. Metro Detroit s top automotive manufacturers Lear, Visteon, and TRW all reported increased profits from the second quarter of 2011 The Michigan economy continued to make gradual improvements during the third quarter of 2011, which can be much attributed to the recent performance of the automotive industry. U.S. light vehicle sales are up 10% on the year through September and experts are predicting this increase in demand for smaller, more fuel efficient automobiles, will accelerate in the upcoming months. In particular, Chrysler Group saw their saless jump 27% in the month of September, which followed a 31% increase in August. General Motors has also enjoyed the recent increased demand as their sales experienced a 20% gain in the month of September. As the Michigan economy improves, so too is the Detroit Metropolitan office market. Positive absorption has now been recorded for the sixth consecutive quarter, with the market posting a net absorption of 139,489 SF in the third quarter, increasing the 2011 year total to 415,815 SF. Following a slow second quarter, the Sub burban office market experienced an uptick in activity during the third quarter, posting a positive net absorption of 234,808 SF. The trend of positive absorption is expected to maintain in the final quarter of 2011, as the low average rental rate of $17.55 per square foot will continue to make Detroit a buyers market for tenants. Vacancy vs. Lease Rate Q Q Q Q Q 2009 While the Detroit Metropolitan office market as a whole is continuing to progress into the year, high vacancy rates remain a concern for landlords. However, after increasing slightly to 28.4% in the second quarter, the vacancy rate fell to 28.1% for the third quarter. The resurging office market the vacancy rate fell further down from the year end 2010 mark of 29.3% and is expected to decrease further as more tenants look to take advantage of the current market. Activity in the Detroit Metropolitan area continued to progress as there were a number of significant deals completed during the third quarter. Among the most notable were the purchases of The Dime Building and First National Building in Detroit s CBD by Quicken Loans CEO Dan Gilbert. The buildings sold in August for a reported $15 million and $8.1 million, respectively. Notable lease activity in the third quarter included Airfoil Public Relations signing a new lease for 14,500 square feet at 1000 Town Center with CBRE representing the landlord. 4Q Q Q 2010 Average Asking Lease Rate $/SF/YR Vacancy Rate 3Q Q Q Q 2011 $ % 3Q 2011 Area Overview 18

20 Detroit Market Report Market Statistics Vacancy 3Q Net Submarket Market Size Rate % Absorption Ann Arbor 4,915, % 11,832 Auburn Hills 1,595, % 26,053 Birmingham/Bloomfield 4,133, % 23,241 Dearborn 4,023, % 5,461 Farmington Hills/W Bloomfield 5,493, % 39,646 I-275 Corridor 5,152, % 5,580 Macomb 1,385, % 7,475 Other 3,021, % 17,059 Rochester 677, % 36,184 Southfield 15,553, % 13,273 Troy 12,902, % 49, Net Asking Availability Absorption Lease Rate Rate % 41,678 $ % 46,774 $ % 96,911 $ % -89,331 $ % 86,680 $ % 2,342 $ % 161 $ % 55,932 $ % 26,243 $ % 44,794 $ % 168,016 $ % Suburban Total 58,854, % 234, ,200 $ % Detroit 15,612, % -95, ,385 $ % Metro Detroit Total 74,467, % 139, ,815 $ % MarketView Detroit Office Market Size Vacancy 2Q Net 2011 Net Asking Availability Rate % Absorption Absorption Lease Rate Rate % Class A 22,482, % 123, ,080 $ % Class B 30,755, % 78,072 92,349 $ % Class C 5,616, % 33, ,325 $ % Suburban Total 58,854, % 234, ,200 $ % Class A 6,353, % -35,311 22,897 $ % Class B 7,299, % -61, ,030 $ % Class C 1,959, % 1,267 26,748 $ % Detroit Total 15,612, % -95, ,385 $ % Class A 28,836, % 88, ,977 $ % Class B 38,055, % 16,797-50,235 $ % Class C 7,575, % 34, ,073 $ % Metro Total 74,467, % 139, ,815 $ % Unemployment Q Q Q Q Q Q Q Q Q Q Q Q Q Q Q Q 2011 Metro Detroit 12.9% Michigan 11.0% National 9.1% Following a tough summer for the U.S. economy, Michigan s unemployment rate increased from the second quarter mark of 10.3 percent to 11 percent in the third quarter. However, despite the moderate uptick the unemployment rate is still down in all of Michigan s 17 major labor markets from the third quarter Metropolitan Detroit also experienced an increase in the unemployment rate during the third quarter, escalating to 12.9% from the 11.1% mark set in the second quarter. While Metro Detroit s unemployment rate is still above the national rate of 9.0%, further expansions in the automotive industry will continue to create jobs and improve the overall state of the economy. The national unemployment rate of 9.1% was essentially unchanged from the previous quarter s mark of 9.0%. Total nonfarm employment has continued to increase throughout the second quarter, which included a gain of 85,000in July. Page , CBRE, Inc. Third Quarter 2011 Area Overview 19

21 Detroit Market Report Vacancy Vacancy 28.1% 30% 29% 28% 27% 26% 25% 24% 23% 22% 21% 20% 2Q Q Q Q Q Q Q Q Q Q 2011 The Detroit Metropolitan office market saw its vacancy rate decrease in the third quarter as activity continues to pick up. Following a slight uptick to 28.4% during the second quarter, Metro Detroit s office vacancy rate fell to 28.1% in the third quarter. Overall vacancy in the Detroit CBD and Suburban office markets also decreased from the previous quarter, improving to 27.54% and 28.27% respectively. The submarket with the largest decline in vacancy from second quarter was the Rochester submarket with a current vacancy rate of 22.4% this quarter. The Auburn Hills submarket experienced the lowest vacancy in the second quarter at 13.0%, while the Dearborn submarket had the highest vacancy rate at 36.0%. MarketView Detroit Office Average Asking Lease Rates Detroit Suburban $18.62 $17.26 $19.00 $18.50 $18.00 $17.50 $17.00 $ Q Q Q Q Q Q Q Q Q Q 2011 The average asking rental rate for office space in the Detroit Metropolitan area decreased from $17.59 to $17.55 per square foot on a full service basis. Landlords continue to offer low rental rates which, in return, has created an attractive market place for potential tenants. Average asking lease rates for the Detroit CBD office market fell to $18.62 per square foot in the second quarter after reporting a second quarter rate of $18.73 per square foot. The average asking lease rates for the suburban office market also declined slightly from the second quarter to $17.26 per square foot in the third quarter. The Detroit Metropolitan office market s average quoted gross rental rate for Class A office space is $20.24 per square foot, down from $20.31 per square foot in the first quarter. Class B & C average asking lease rates in Metro Detroit were $16.80 and $13.88 per square foot respectively. Vacancy 28.1% Availability 29.5% Net Absorption 139,489 Vacancy/Availability/Net Absorption 32% 30% 28% 26% 24% 22% 20% 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q Net Absorption (Thousands SF) The Detroit Metropolitan Office market reported positive absorption for the sixth consecutive quarter, experiencing a net absorption of 139,489 square feet. The Troy submarket saw leasing activity continue in the third quarter reporting a positive absorption of 49,004 square feet. The Suburban office market returned to positive absorption after reporting a positive absorption of 234,808 square feet in the second quarter. The total availability rate for the overall Detroit Metropolitan area increased slightly with a reported 29.5% rate in the third quarter. In the suburban market, availability increased to 29.3%, compared to a rate of 29.0% in the second quarter. In the Detroit CBD total availability increased to 30.2% after posting a 28.8% availability rate in the second quarter. Page , CBRE, Inc. Third Quarter 2011 Area Overview 20

22 Detroit Market Report MarketView Detroit Office Selected Lease Transactions Size (Sq. Ft.) Tenant Address 19,986 Auto Club Group** 150 W Jefferson Ave 19,117 Aerotek** 901 Tower Dr 14,500 Airfoil Public Relations* 1000 Town Center 13,675 CEVA Logistics, Inc.* Civic Center Dr * New ** Renewal ***Expansion Submarket Map City Detroit Troy Southfield Southfield Average Asking Lease Rate Rate determined by multiplying the asking net lease rate for each building by its available space, summing the products, then dividing by the sum of the available space with net leases for all buildings in the summary. Net Leases Includes all lease types whereby the tenant pays an agreed rent plus most, or all, of the operating expenses and taxes for the property, including utilities, insurance and/or maintenance expenses. Market Coverage Includes all competitive multi-tenant office buildings 20,000 square feet and greater in size. Net Absorption The change in occupied square feet from one period to the next. Net Rentable Area The gross building square footage minus the elevator core, flues, pipe shafts, vertical ducts, balconies, and stairwell areas. Occupied Square Feet Building area not considered vacant. Under Construction Buildings which have begun construction as evidenced by site excavation or foundation work. Available Square Feet Available Building Area which is either physically vacant or occupied. Availability Rate Available Square Feet divided by the Net Rentable Area. Vacant Square Feet Existing Building Area which is physically vacant or immediately available. Vacancy Rate Vacant Building Feet divided by the Net Rentable Area. Normalization Due to a reclassification of the market, the base, number and square footage of buildings of previous quarters have been adjusted to match the current base. Availability and Vacancy figures for those buildings have been adjusted in previous quarters. For more information regarding the MarketView, please contact: John A. Latessa Jr., Managing Director john.latessa@cbre.com Trevor Jeske, Research Analyst trevor.jeske@cbre.com Copyright 2011 CBRE Statistics contained herein may represent a different data set than that used to generate National Vacancy and Availability Index statistics published by CBRE Corporate Communications or CBRE s research and econometric forecasting unit, CBRE Econometric Advisors. Information herein has been obtained from sources believed reliable. While we do not doubt its accuracy, we have not verified it and make no guarantee, warranty or representation about it. It is your responsibility to independently confirm its accuracy and completeness. Any projections, opinions, assumptions or estimates used are for example only and do not represent the current or future performance of the market. This information is designed exclusively for use by CBRE clients, and cannot be reproduced without prior written permission of CBRE. CBRE, Inc Town Center, Suite 500 Southfield, MI T F Area Overview 21

23 Fleming s - College Park Rent Comparables 03 Rent Comparables Rent Comparable Analysis Rent Comparables

24 rent comparables analysis Average Rental Rates $45.00 $41.63 $40.00 $35.52 $35.00 $33.23 $30.00 $25.00 $22.61 $30.00 $24.97 Comparable Average Average $27.47 $26.82 per SF $20.00 $19.92 $15.66 $17.23 Subject Average Rate $18.45 per SF $15.00 $10.00 $5.00 $ With a current rental rate for the subject tenant, Flemings of $18.45 per square foot, the subject property is operating at a rental rate that is lower than the market average of restaurant comparables $26.82 per square foot. Rent Comparables 23

25 rent comparables Building Name Address Building Size (SF) Year Built Current Occupancy Lease Status Average Rental Rate Expense Recovery Type Comments Fleming's Haggerty Road Livonia, MI 7, % $18.45 NNN Fleming's is on their initial 10 year lease expiring 11/2016 with 4.83 years remaining. The lease is guaranteed by Outback Steakhouse with an S & P Credit rating of B- 1 TGI Friday's Haggerty Road Livonia, MI 7, % Actual Signed Lease $22.61 NNN TGI Friday's building offers a long term 10 year corporate backed lease with a 10% increase every 5 years, with an additional 4, 5 year options. This is a corporate Backed Lease: T.G.I. Friday's, Inc. 2 Benihana Ground Lease Hubbard Drive Dearborn, MI 7, % Actual Signed Lease, 12/ /2035 $19.92 NNN Ground Lease This particular restaurant is on a 32 year ground lease (with 26.5 years remaining) with a rental increase of at least 10 percent every five years. 3 Maggiano's 2089 West Big Beaver Troy, MI 14, % Actual Signed Lease 5/2004-4/2014 $15.66 Absolute NNN Maggiano's is on an absolute NNN lease expiring 4/30/2014. Maggiano's is to pay percentage rent in years 1-5 of 5% over $8,500,000 and Years 6-10 over $8,700,000; Also breakpoint increases in options. However, their reported store sales from have not gone over their breakpoint. 4 #REF! Ruby Tuesday Ground Lease Southfield Road Allen Park, MI 6, % Actual Signed Lease, 8/2005-7/2020 $17.23 NNN Ground Lease Ruby Tuesday's is on a 15 year lease that commenced on August 1, 2005 and has a 10% rent increase in year 11. The tenant is responsible for real estate taxes, insurance, all operating expenses including the replacement of the paving as well as all building improvements. In addition, the tenant has up to six 5-year options to extend the lease provided the tenant gives written notice 180 days prior to the expiration of the lease. 5 Black Finn Pub & Restaurant 500 South Main Street Royal Oak, MI 7, / % Actual Signed Lease 6/2008-5/218 $30.00 Black Finn is on a 10 year lease through 5/31/2018 with a rental escalation on 6/1/2013 to $34.50 per square foot. The NN + 12% tenant also has two, five year renewal Admin Cam options with 180 days notification period. The tenant also has to pay percentage rent of 5% over $4,414,800 years 1-5 and 5% over $5,077,020 years Rent Comparables 24

26 rent comparables Building Name Address Building Size (SF) Year Built Current Occupancy Lease Status Average Rental Rate Expense Recovery Type Comments Fleming's Haggerty Road Livonia, MI 7, % $18.45 NNN Fleming's is on their initial 10 year lease expiring 11/2016 with 4.83 years remaining. The lease is guaranteed by Outback Steakhouse with an S & P Credit rating of B- 6 Mongolian BBQ 410 South Main Street Royal Oak, MI 6, % Actual Signed Lease 9/2005-8/2015 $33.23 NN+10% Admin on CAM & INS Mongolian BBQ is on a 10 year lease through 8/31/2015 with no remaining rental escalations. The tenant also has two, five year renewal options with 180 days notification period. 7 Joe's Crab Shack 320 Lohr Road Ann Arbor, MI 7, % Actual Signed Lease 3/2007-3/2027 $24.97 Absolute NNN The tenant/guarantor is Joe's Crab Shack Holding, LLC. The property was built in 1998 with 10% escalations every five years. The lease commenced 3/15/2007 through 3/31/2027 (17 years remaining). The lease is absolute NNN with zero landlord responsibilities. 8 Logan's Roadhouse Ford Road Canton, MI 8, % Actual Signed Lease $41.63 Absolute NNN The property is on an absolute net lease to Logan's Roadhouse. 9 Johnny Carino's 500 Loop Road Commerce Township, MI 6, % Actual Signed Lease $35.52 Absolute NNN The property was a build-to-suit for Carino s in A 20-year absolute net lease commenced May 28, 2004 on the primary lease term followed by three, fiveyear options at a rental rate of 10 percent above the preceding five year period. The tenant is responsible for all expenses associated with the property, including roof and structure. The subject property is located on an outparcel to Costco. 10 TGI Friday's 720 Town Center Drive Dearborn, MI 9, % Actual Signed Lease, 1/1986-1/2016 $27.47 NN T.G.I. Friday's was originally on a 20 year lease that they recently renewed through January 31, 2016, with 7.25 years remaining on their option period. The initial lease was NN in nature (tenant responsible for CAM, taxes and insurance), with the landlord responsible for the roof and structure; however, per the lease, the landlord is only to be responsible for capital items within the initial lease term. All Comparable Averages 100% $26.82 Rent Comparables 25

27 Fleming s - College Park Sale Comparables 04 Sale Comparables Sale Comparable Analysis Sales Comparables

28 sale comparable analysis Average Price per Square Foot $700 $610 $600 $568 $523 $500 $400 $391 Restaurant Average Price per SF $435 $335 $300 $229 $200 $144 $100 SUBJECT Average Price per SF $124 $ With an average price per square foot of $435 for comparable single tenant restaurant sales, the subject property, priced at $124 per square foot is priced more competitively than the market average due to its newer construction, great location, and high store sales. Sale Comparables 27

29 sale comparable analysis Average Cap Rate 9.0% 8.0% 7.51% 8.80% 7.40% 8.00% 7.61% SUBJECT Cap Rate 8.00% 7.0% 6.50% 6.66% Comparable Average Cap Rate 7.23% 6.0% 5.0% 4.0% 3.0% 2.0% 1.0% 0.0% With an average market cap rate of 7.23 percent for like assets, the subject property, priced at a cap rate of 8.00 percent, is priced more competitively than the market average. Sale Comparables 28

30 Sale comparables Building Name Address Year Built Building Size (SF) Sale Date Sales Price Price/SF Occupancy at Sale Cap Rate Comments Fleming's Ground Lease Haggerty Road Livonia, MI ,898 $984,500 $ % 8.00% Fleming's is on their initial 10 year lease expiring 11/2016 with 4.83 years remaining. The lease is guaranteed by Outback Steakhouse with an S & P Credit rating of B- 1 Ruby Tuesday Southfield Road Allen Park, MI ,385 7/27/2007 $1,465,000 $ % 7.51% Ruby Tuesday's was on a 15 year ground lease through 7/31/2020 with 14 years remaining on the lease at the time of the sale. 2 Not Available Ruth Chris Steakhouse Sarasota, FL ,725 9/1/2010 $3,018,625 $ % 8.80% Ruth Chris is on a 20 year lease that commenced on Sept. 17, 2008 (18 years remain). There are also two five-year options for renewal. The rental rate increase annually by 1.75% throughout the term.. 3 Chili's 128 Sparks Crossing Forest City, NC ,838 On Market $2,750,000 $ % 7.40% The initial 20 year lease expires 6/30/2027 (16 years remaining) with annual rental increases of 1.5 percent and two, 10-year renewal options. The lease is guaranteed by Pepper Dining, Inc. is the largest Chili s franchisee, operating 95 Chili s Grill and Bar restaurants located throughout the Northeastern and Mid- Atlantic regions of the United States. 4 Chili's 1957 South Muskogee Avenue Tahlequah, OK ,876 On Market $846,152 $ % 6.50% The lease guarantor is Brinker International, Inc. with the lease expiring 7/31/2016 (5 years remain) on this NNN ground lease. 5 Applebee's Venice, FL 1984 / ,060 5/1/2011 $3,085,000 $ % 6.66% Applebee's has 10 years remaining on their current term. 6 Chili's 4000 North Vinewood Lane Plymouth, MN ,167 12/22/2010 $2,065,000 $ % 8.00% The property is still leased to Chili's until (17 years remain) with 1.5% annual increases. 7 Chili's 2636 Taylor Road Chesapeake, VA ,564 11/19/2010 $2,910,000 $ % 7.61% This property was 100% occupied at the time of sale by Chili's. They are currently on a 20- year absolute NNN lease that expires in 6/30/2027 (17 years remain), with two 10-year options. The lease commenced on 6/27/2007. All Comparable Averages $ % 7.23% Sale Comparables 29

31 STNL - University Marketplace Financials - Fleming s 05 Financials - Fleming s Summary of Financial Assumptions Lease Abstract Tenant Overview Year One Cash Flow

32 Financial overview FINANCIAL OVERVIEW Sales Price $984,500 RENTAL ESCALATIONS Annual Rent Rent per SF Down Payment All Cash 12/ /2011 $132,500 $16.78 CAP Rate 8.00% Price Per Square Foot $ Offered Free & Clear of Financing Existing Financing Building information Fleming s Ground Lease Building Haggerty Road Livonia, MI Building Size (SF) 39,673 SF Property Type Year Built 2006 Type of Ownership Single Tenant Retail Fee Simple Current Occupancy 100% PROPOSED FINANCING TERMS All Cash GROUND LEASE TERMS Commencement Date 12/12/2006 Expiration Date 11/30/2016 Lease Term Term Remaining Lease Type 10 years 4.83 years / 58 Months NNN Ground Lease + 15% Admin on top of CAM 12/ /2016 $145,750 $18.45 Option One $160,325 $20.29 Option Two $176,350 $22.33 Option Three $193,995 $24.56 Option Four $213,395 $27.01 The tenant has four, five year renewal options with 360 days notice EXPENSE ESTIMATES Estimated per the 2011 SEV of $1,309,830 (same as the taxable value) and the 2011 Real Estate Taxes non-homestead millage rate of for a tax expense of $68,187 or $1.72 per square foot Estimated per the YTD Common Area 2011 Income and Expense Expense Estimates Statement Ground Lease Rent Expense Management Fees Vacancy Factor Capital Reserves (Included in Operating Expenses) The property is on a ground lease through 12/31/ % of EGR Not applied due to the single tenant nature of the asset $0.20 per Square Foot Financials-Fleming's 31

7,898 Square Feet 4.")

33 Lease Abstract GROUND LEASE ABSTRACT Tenant Name Lease Terms Premises Years Remaining on Current Term Rental Escalations Lease Type Operating Expenses: Common Area Maintenance (CAM) and Property Insurance Real Estate Taxes Fleming s Guaranteed by Outback Steakhouse, Inc. 12/12/ /30/2016 (Ground Lease) 7,898 Square Feet 4.83 Years / 58 Months None remaining in initial lease term NNN Ground Lease (Tenant to Reimburse for CAM plus an admin fee of 15% and property insurance) Tenant shall pay to landlord as additional rent all operating expenses Tenant shall pay to the appropriate taxing authorities. Tenant shall also furnish landlord with a copy of the tax bills and assessment bills. Percentage Rent Tenant shall pay percent rent equal to 2.0% over store sales of $4,700,000 Financial Statements Option to renew Underlying Ground Rent Upon landlord s request, tenant shall promptly furnish landlord financial statements. The tenant shall have four, five-year renewal options with rental increases and a notification period of 360 days. The property is controlled by a leasehold interest, with an affiliated entity of Schoolcraft College being the landlord. This term is 75 years which commenced on December 1, 2003 expiring on December 31, This expense is not reimbursed by the tenant and is included as a non-reimbursable expense on the year one calculation page. The ground lease has the following annual rental increases: Years 1 through 17: 1.00% Year 18: 10.00% Years 19 through End of the term: 0.50% Per the ground lease documents, the qualifications for purchasing entity of the subject property must have a net worth of the greater of $2,500,000 or $500,000 per acre. Financials-Fleming's 32

34 Tenant Overview TENANT INFORMATION Tenant Name Tenant Ownership Stock Symbol Credit Rating Number of Flemings Locations World Headquarters Revenues Website Fleming s Prime Steakhouse & Wine Bar Public OSI B- According to S&P N. West Shore Blvd., 5th Floor Tampa, Florida Total Six Month Revenue: $1,957,440,000 Operating Income: $103,868,000 Net Income: $58,201,000 Since the first Fleming s Prime Steakhouse & Wine Bar opened in 1998, they ve raised the standard of excellence for steakhouses to a whole new level, winning awards all over the country for outstanding food, wine and service. Flemings is part of the OSI Restaurant family. Flemings Profile Stylish, contemporary dining is the hallmark of Fleming s. As the name implies, the menu features the finest in prime beef, augmented by a tempting variety of chops, seafood, chicken, generous salads, inventive side orders and indulgent desserts. The celebrated wine list, known as the Fleming s 100, boasts some of the finest wines in the world, all available by the glass. OSI Restaurant Partners, LLC, headquartered in Tampa, Florida, was founded in 1988 by a group of people who believe in hospitality, sharing, quality, being courageous and having fun! Company Profile Today, their portfolio of brands consists of Outback Steakhouse units throughout the U.S., as well as Carrabba s Italian Grill, Bonefish Grill, Fleming s Prime Steakhouse & Wine Bar and Roy s Hawaiian Fusion Cuisine. They are now one of the largest casual dining restaurant companies in the world. They operate in 49 states and our Outback Steakhouse restaurants are also open in 24 countries around the world. Financials-Fleming's 33

35 Year one Cash Flow Fleming's Ground Lease Year One Cash Flow Estimates Proposed Financing Price $984,500 Down Payment All Cash Rentable Square Feet 7,898 Price per Square Foot $ Cap Rate 8.00% Income 2/2012-1/2013 Per SF Base Rent Fleming's 4.83 Years Remain (12/ /2016) 100.0% 7,898 SF $145,750 $18.45 Total Base Rent $145,750 $18.45 Scheduled Base Rental Revenue $145,750 $18.45 Expense Reimbursement Revenue Common Area Maintenance $23,760 $3.01 Real Estate Taxes $55,270 $7.00 Property Insurance $3,619 $0.46 Total Expense Reimbursement Revenue $82,649 $10.46 Gross Potential Income $228,399 $28.92 Vacancy/Collection Allowance 0.0% $0 $0.00 Effective Gross Income $228,399 $28.92 Operating Expense Estimates Common Area Expenses $20,660 $2.62 Real Estate Taxes $55,268 $7.00 Property Insurance $3,618 $0.46 Total Operating Expenses $79,546 $10.07 Non-Reimbursable Expenses Ground Rent $56,187 $7.11 Admin Expenses $4,358 $0.55 Total Non-Reimbursable Expense $60,545 $7.67 Management Fee 3.5% $7,994 $1.01 Replacement Reserve $0.20 $1,580 $0.20 Total Expenses $149,665 $18.95 Net Operating Income $78,734 $9.97 Financials-Fleming's 34

36 ::OFFERING MEMORANDUM Capital Markets Private Capital Group Provided by : :: Bill O Connor Senior Vice President bill.oconnor@cbre.com PCG Detroit Capital Markets Driving Price and Adding Value through Experience and Market Knowledge 2011 CBRE, Inc.. The information above has been obtained from sources believed reliable. While we do not doubt its accuracy, we have not verified it and make no guarantee, warranty or representation about it. It is your responsibility to independently confirm its accuracy and completeness. Any projections, opinions, assumptions or estimates used are for example only a and do not represent the current or future performance of the property. The value of this transaction to you depends on tax and other factors which should be evaluated by your tax, financial and legal advisors. You and your advisors should conduct a careful, independent investigation of the property to determine to your satisfaction the suitability of the property for your needs. CBRE, Inc. Printed in USA, 12/07, 2500/CP, HOU OM

RETAIL INVESTMENT VAN NESS AVENUE GARDENA, CA 90249

PROPERTY SUMMARY: Offering Price: $1,300,000 Address: 13901-13915 Van Ness Ave Gardena, CA 90249 APN: 4059-017-037 Building Size: 6,841 SF PRICING INMATION: Price Per SF: $190 Land Size: 16,500 SF (.38

PROPERTY SUMMARY: Offering Price: $1,300,000 Address: 13901-13915 Van Ness Ave Gardena, CA 90249 APN: 4059-017-037 Building Size: 6,841 SF PRICING INMATION: Price Per SF: $190 Land Size: 16,500 SF (.38

NNN LEASE/DOLLAR GENERAL

PROPERTY FOR SALE ACTUAL STORE NNN LEASE/ 30445 Northwestern Highway, Suite 275 Farmington Hills, MI 48334 248.254.3410 fortisnetlease.com BRYAN BENDER MANAGING DIRECTOR D: 248.419.3810 BBENDER@FORTISNETLEASE.COM

PROPERTY FOR SALE ACTUAL STORE NNN LEASE/ 30445 Northwestern Highway, Suite 275 Farmington Hills, MI 48334 248.254.3410 fortisnetlease.com BRYAN BENDER MANAGING DIRECTOR D: 248.419.3810 BBENDER@FORTISNETLEASE.COM

Suburban Boston Office MarketView

Suburban Boston Office MarketView CBRE Global Research and Consulting U.S. UNEMPLOYMENT 6.7% MA UNEMPLOYMENT 7.1% OCCUPIED SF 92.9M AVAILABILITY 20.3% SUBLEASE SF 2.6M UNDER CONSTRUCTION 1.6M *Arrows indicate

Suburban Boston Office MarketView CBRE Global Research and Consulting U.S. UNEMPLOYMENT 6.7% MA UNEMPLOYMENT 7.1% OCCUPIED SF 92.9M AVAILABILITY 20.3% SUBLEASE SF 2.6M UNDER CONSTRUCTION 1.6M *Arrows indicate

Another solid quarter for the industrial market as its reputation grows

MARKETVIEW Boston Industrial, Q1 2017 Another solid quarter for the industrial market as its reputation grows Vacancy 7.7% Availability 10.7% Occupied Sq. Ft. 148.5 MSF Under Construction 300K SF * Arrows

MARKETVIEW Boston Industrial, Q1 2017 Another solid quarter for the industrial market as its reputation grows Vacancy 7.7% Availability 10.7% Occupied Sq. Ft. 148.5 MSF Under Construction 300K SF * Arrows

Greater Boston Industrial Finishes 2015 with a Bang

MARKETVIEW Boston Suburban Industrial, Q4 2015 Greater Boston Industrial Finishes 2015 with a Bang Vacancy 9.8% Availability 13.4% Occupied Sq. Ft. 128.7 MSF Sublease 0.9 MSF Figure 1: Industrial Vacancy

MARKETVIEW Boston Suburban Industrial, Q4 2015 Greater Boston Industrial Finishes 2015 with a Bang Vacancy 9.8% Availability 13.4% Occupied Sq. Ft. 128.7 MSF Sublease 0.9 MSF Figure 1: Industrial Vacancy

Taco Bell - STNL Investment 1319 Dunn Avenue Jacksonville, FL 32218

Capital Markets Private Capital Group Taco Bell - STNL Investment nue Jacksonville, FL 32218 :: offering memorandum PCG Detroit Capital Markets Driving Price and Adding Value through Experience and Market

Capital Markets Private Capital Group Taco Bell - STNL Investment nue Jacksonville, FL 32218 :: offering memorandum PCG Detroit Capital Markets Driving Price and Adding Value through Experience and Market

Healthcare, Life Sciences and Technology Sectors Drive Q Leasing Activity

MARKETVIEW Boston Suburban Office, Q4 2015 Healthcare, Life Sciences and Technology Sectors Drive Q4 2015 Leasing Activity Vacancy 17.3% Availability 19.9% Absorption 87,036 SF Sublease 2.5 MSF Under Construction

MARKETVIEW Boston Suburban Office, Q4 2015 Healthcare, Life Sciences and Technology Sectors Drive Q4 2015 Leasing Activity Vacancy 17.3% Availability 19.9% Absorption 87,036 SF Sublease 2.5 MSF Under Construction

$26.00/SF/YR, NNN. I-5 116,966 ADT (15) Barbur Blvd (Hwy 99W) 15,600 ADT (16) Capitol Hwy 18,173 ADT (15)

Barbur Blvd (Hwy 99W) 15,600 ADT (16) Capitol Hwy 18,173 ADT (15)") FOR LEASE Capitol Corner PORTLAND, OREGON Location: Available Space: Rental Rate: Comments: Traffic CountS: At the corner of I-5 & SW Barbur Blvd intersecting at Capitol Hwy 1,300 SF (former Salon) 1,755

FOR LEASE Capitol Corner PORTLAND, OREGON Location: Available Space: Rental Rate: Comments: Traffic CountS: At the corner of I-5 & SW Barbur Blvd intersecting at Capitol Hwy 1,300 SF (former Salon) 1,755

NEW DOLLAR GENERAL ABS NNN LEASE RARE VA LOCATION 6088 KENTUCK RD., RINGGOLD, VA NOT ACTUAL STORE BENJAMIN SCHULTZ BRYAN BENDER

ABS NNN LEASE RARE VA LOCATION NOT ACTUAL STORE NEW DOLLAR GENERAL 30445 Northwestern Highway, Suite 275 Farmington Hills, MI 48334 248.254.3410 fortisnetlease.com BRYAN BENDER MANAGING DIRECTOR D: 248.419.3810

ABS NNN LEASE RARE VA LOCATION NOT ACTUAL STORE NEW DOLLAR GENERAL 30445 Northwestern Highway, Suite 275 Farmington Hills, MI 48334 248.254.3410 fortisnetlease.com BRYAN BENDER MANAGING DIRECTOR D: 248.419.3810

Almeda West Shopping Center Kleckley Houston, TX 77075

9940-9944 Kleckley CONFIDENTIALITY AND DISCLAIMER The information contained in the following Marketing Brochure is proprietary and strictly confidential. It is intended to be reviewed only by the party

9940-9944 Kleckley CONFIDENTIALITY AND DISCLAIMER The information contained in the following Marketing Brochure is proprietary and strictly confidential. It is intended to be reviewed only by the party

Suburban Boston Industrial MarketView

Suburban Boston Industrial MarketView CBRE Global Research and Consulting U.S. UNEMPLOYMENT 7.6% MA UNEMPLOYMENT 7.0% OCCUPIED SF 122.5M AVAILABILITY 19.7% SUBLEASE SF 2.6M UNDER CONSTRUCTION 170K *Arrows

Suburban Boston Industrial MarketView CBRE Global Research and Consulting U.S. UNEMPLOYMENT 7.6% MA UNEMPLOYMENT 7.0% OCCUPIED SF 122.5M AVAILABILITY 19.7% SUBLEASE SF 2.6M UNDER CONSTRUCTION 170K *Arrows

DOLLAR GENERAL LOW RENT/FT INCREASES IN PRIMARY TERM 1787 LA-121, HINESTON, LA REPRESENTATIVE STORE KYLE CARSON ANDY BENDER ROBERT BENDER

LOW RENT/FT INCREASES IN PRIMARY TERM REPRESENTATIVE STORE 30445 Northwestern Highway, Suite 275 Farmington Hills, MI 48334 248.254.3410 fortisnetlease.com KYLE CARSON SENIOR ADVISOR D: 248.419.3271 KCARSON@FORTISNETLEASE.COM

LOW RENT/FT INCREASES IN PRIMARY TERM REPRESENTATIVE STORE 30445 Northwestern Highway, Suite 275 Farmington Hills, MI 48334 248.254.3410 fortisnetlease.com KYLE CARSON SENIOR ADVISOR D: 248.419.3271 KCARSON@FORTISNETLEASE.COM

Boston starts the year slowly, but has plenty in store

Boston Downtown Office, Q1 2017 Boston starts the year slowly, but has plenty in store Vacancy 8.6% Availability 13.9% Quarterly Absorption (67,890) SF Sublease 1.3% Under Construction 1.8 MSF Figure 1:

Boston Downtown Office, Q1 2017 Boston starts the year slowly, but has plenty in store Vacancy 8.6% Availability 13.9% Quarterly Absorption (67,890) SF Sublease 1.3% Under Construction 1.8 MSF Figure 1:

ABSOLUTE NNN DOLLAR GENERAL

MORGANTOWN HOME TO WVU ~30,000 STUDENTS NOT ACTUAL STORE ABSOLUTE NNN 30445 Northwestern Highway, Suite 275 Farmington Hills, MI 48334 248.254.3410 fortisnetlease.com BRYAN BENDER MANAGING DIRECTOR D:

MORGANTOWN HOME TO WVU ~30,000 STUDENTS NOT ACTUAL STORE ABSOLUTE NNN 30445 Northwestern Highway, Suite 275 Farmington Hills, MI 48334 248.254.3410 fortisnetlease.com BRYAN BENDER MANAGING DIRECTOR D:

FOR LEASE IN MEDFORD, OREGON CARDINAL AVE. Cardinal Ave & Crater Lake Hwy, Medford, Oregon

CRATER LAKE HWY FORMER RETAIL PADS FOR LEASE IN MEDFORD, OREGON ANCHORS OPENING SUMMER 2018! CARDINAL AVE available 10,000 SF available 10,000 SF available 8,490 SF LEAR WAY available 7,000 SF Location

CRATER LAKE HWY FORMER RETAIL PADS FOR LEASE IN MEDFORD, OREGON ANCHORS OPENING SUMMER 2018! CARDINAL AVE available 10,000 SF available 10,000 SF available 8,490 SF LEAR WAY available 7,000 SF Location

Click Image For Online Property Map

O F F E R I N G M E M O R A N D U M Click Image For Online Property Map DISCLOSURE : All materials and information received or derived from Fortis Net Lease (hereinafter collectively referred to as FNL

O F F E R I N G M E M O R A N D U M Click Image For Online Property Map DISCLOSURE : All materials and information received or derived from Fortis Net Lease (hereinafter collectively referred to as FNL

CHICAGO CBD OFFICE INVESTMENT PROPERTIES GROUP

CHICAGO CBD OFFICE INVESTMENT PROPERTIES GROUP SECOND QUARTER NEWSLETTER 216 HOT TOPICS Capital markets remain a focus with 14 assets either under contract or sold totaling $2.6 billion, which includes

CHICAGO CBD OFFICE INVESTMENT PROPERTIES GROUP SECOND QUARTER NEWSLETTER 216 HOT TOPICS Capital markets remain a focus with 14 assets either under contract or sold totaling $2.6 billion, which includes

Patrick Hammond. Dollar General Nettleton (Okolona), MS DISCLOSURE :

, MS DISCLOSURE :") O F F E R I N G M E M O R A N D U M DISCLOSURE : All materials and information received or derived from Fortis Net Lease (hereinafter collectively referred to as FNL ), its directors, officers, agents,

O F F E R I N G M E M O R A N D U M DISCLOSURE : All materials and information received or derived from Fortis Net Lease (hereinafter collectively referred to as FNL ), its directors, officers, agents,

TIMBERLAND TOWN CENTER

TIMBERLAND TOWN CENTER IN PORTLAND, OREGON LOCATION AVAILABLE SPACE ECONOMICS COMMENTS TRAFFIC COUNT DEMOGRAPHICS NW Barnes Rd & NW 118th in Portland, Oregon Retail 1,299 SF & 2,360 SF (can combine to

TIMBERLAND TOWN CENTER IN PORTLAND, OREGON LOCATION AVAILABLE SPACE ECONOMICS COMMENTS TRAFFIC COUNT DEMOGRAPHICS NW Barnes Rd & NW 118th in Portland, Oregon Retail 1,299 SF & 2,360 SF (can combine to

Cambridge Office/Lab MarketView

Cambridge Office/Lab MarketView CBRE Global Research and Consulting U.S. UNEMPLOYMENT 6.7% MA UNEMPLOYMENT 6.3% OCCUPIED SQ. FT. 19.4M OFFICE AVAIL. 10.0% LAB AVAIL. 18.4% UNDER CONSTRUCTION 1.8MSF *Arrows

Cambridge Office/Lab MarketView CBRE Global Research and Consulting U.S. UNEMPLOYMENT 6.7% MA UNEMPLOYMENT 6.3% OCCUPIED SQ. FT. 19.4M OFFICE AVAIL. 10.0% LAB AVAIL. 18.4% UNDER CONSTRUCTION 1.8MSF *Arrows

At the corner of B Avenue and 3rd Street in downtown Lake Oswego, Oregon. Up to approximately 8500 SF with an all season 704 SF deck

FOR LEASE LAKE OSWEGO, OREGON 10 BRANCH DEVELOPMENT» PRIME RETAIL, MODERN URBAN OFFICE & WORLD-CLASS EVENT CENTER «CRA Location Available Space Rental Rate Comments DEMOGRAPHICS At the corner of B Avenue

FOR LEASE LAKE OSWEGO, OREGON 10 BRANCH DEVELOPMENT» PRIME RETAIL, MODERN URBAN OFFICE & WORLD-CLASS EVENT CENTER «CRA Location Available Space Rental Rate Comments DEMOGRAPHICS At the corner of B Avenue

CHECKERS DRIVE-IN RESTAURANT 3232 Clarksville Pike, Nashville, Tennessee 37218

REPRESENTATIVE PHOTO CURRENTLY UNDER CONSTRUCTION CHECKERS DRIVE-IN RESTAURANT 3232 Clarksville Pike, Nashville, Tennessee 37218 OFFERING MEMORANDUM EXCLUS IVELY LISTED BY: OF MARCUS & MILLICHAP www.caprates.com

REPRESENTATIVE PHOTO CURRENTLY UNDER CONSTRUCTION CHECKERS DRIVE-IN RESTAURANT 3232 Clarksville Pike, Nashville, Tennessee 37218 OFFERING MEMORANDUM EXCLUS IVELY LISTED BY: OF MARCUS & MILLICHAP www.caprates.com

KARMAR REALT Y GROUP, INC. C O M M E R C I A L & I N V E S T M E N T R E A L E S T A T E S E R V I C E S S A L E

KARMAR REALT Y GROUP, INC. C O M M E R C I A L & I N V E S T M E N T R E A L E S T A T E S E R V I C E S S A L E 99 ALDAN AVENUE, CONCORDVILLE, PA 19331 DESCRIPTION: 30,000 +/- SQ. FT. OF BUILDING FULLY

KARMAR REALT Y GROUP, INC. C O M M E R C I A L & I N V E S T M E N T R E A L E S T A T E S E R V I C E S S A L E 99 ALDAN AVENUE, CONCORDVILLE, PA 19331 DESCRIPTION: 30,000 +/- SQ. FT. OF BUILDING FULLY

Petco & Borders $7,172, % CAP $609,655 NOI. Petco & Borders. Canton Township, MI Ford Rd Canton Township, MI 48187

43473 Ford Rd 48187 $7,172,400 8.50% CAP $609,655 NOI Borders is open with no plans to close this location Prime retail area across from Lowe's, JC Penney, Office Max, and Target Canton is one of the safest,

43473 Ford Rd 48187 $7,172,400 8.50% CAP $609,655 NOI Borders is open with no plans to close this location Prime retail area across from Lowe's, JC Penney, Office Max, and Target Canton is one of the safest,

DOLLAR GENERAL BRAND NEW DOLLAR GENERAL FOR SALE 544 KIGHT RD, KITE, GA ACTUAL STORE BENJAMIN SCHULTZ BRYAN BENDER

BRAND NEW FOR SALE ACTUAL STORE 30445 Northwestern Highway, Suite 275 Farmington Hills, MI 48334 248.254.3410 fortisnetlease.com BRYAN BENDER MANAGING DIRECTOR D: 248.419.3810 BBENDER@FORTISNETLEASE.COM

BRAND NEW FOR SALE ACTUAL STORE 30445 Northwestern Highway, Suite 275 Farmington Hills, MI 48334 248.254.3410 fortisnetlease.com BRYAN BENDER MANAGING DIRECTOR D: 248.419.3810 BBENDER@FORTISNETLEASE.COM

FOR LEASE IN CANBY, OREGON. Hwy 99E & S Ivy St in Canby, OR

FOR LEASE IN CANBY, OREGON HI-WAY MARKETPLACE Location Available Space Rental Rate Comments Hwy 99E & S Ivy St in Canby, OR 2,300 SF Call for details New, high profile retail available by O Reilly Auto

FOR LEASE IN CANBY, OREGON HI-WAY MARKETPLACE Location Available Space Rental Rate Comments Hwy 99E & S Ivy St in Canby, OR 2,300 SF Call for details New, high profile retail available by O Reilly Auto

DOLLAR GENERAL MARKET - RARE OFFERING

ABS. NNN LEASE RELOCATION STORE ACTUAL STORE DOLLAR GENERAL MARKET - RARE OFFERING 30445 Northwestern Highway, Suite 275 Farmington Hills, MI 48334 248.254.3410 fortisnetlease.com BRYAN BENDER MANAGING

ABS. NNN LEASE RELOCATION STORE ACTUAL STORE DOLLAR GENERAL MARKET - RARE OFFERING 30445 Northwestern Highway, Suite 275 Farmington Hills, MI 48334 248.254.3410 fortisnetlease.com BRYAN BENDER MANAGING

I-45 and Parker Road 6500 North Freeway - Houston, Texas 77056

Large Pylon Sign Excellent Exposure to I-45 Freeway 6,554 SQ FT. SPACE AVAILABLE I-45 and Parker Road 6500 North Freeway - Houston, Texas 77056 NOW Lx 6,554 SQ FT and 1,000 SQ FT LEASE SPACE BPI Realty

Large Pylon Sign Excellent Exposure to I-45 Freeway 6,554 SQ FT. SPACE AVAILABLE I-45 and Parker Road 6500 North Freeway - Houston, Texas 77056 NOW Lx 6,554 SQ FT and 1,000 SQ FT LEASE SPACE BPI Realty

Cambridge Office & Lab market at tightest levels since early 2000 s.

MARKETVIEW Cambridge Office/Lab, Q2 2015 Cambridge Office & Lab market at tightest levels since early 2000 s. Office Availability 8.4% Lab Availability 9.6% Occupied Sq. Ft. 22.1 MSF Under Construction

MARKETVIEW Cambridge Office/Lab, Q2 2015 Cambridge Office & Lab market at tightest levels since early 2000 s. Office Availability 8.4% Lab Availability 9.6% Occupied Sq. Ft. 22.1 MSF Under Construction

Speculative construction and record breaking investment sales lead the way in Q2 2015

MARKETVIEW Boston Downtown Office, Q2 2015 Speculative construction and record breaking investment sales lead the way in Q2 2015 Vacancy 7.5% Availability 13.9% Absorption 424,525 SF Sublease 0.75% Under

MARKETVIEW Boston Downtown Office, Q2 2015 Speculative construction and record breaking investment sales lead the way in Q2 2015 Vacancy 7.5% Availability 13.9% Absorption 424,525 SF Sublease 0.75% Under

Staples ONTARIO, OR OFFERING MEMORANDUM

OFFERING MEMORANDUM CONFIDENTIALITY AND DISCLAIMER The information contained in the following Marketing Brochure is proprietary and strictly confidential. It is intended to be reviewed only by the party

OFFERING MEMORANDUM CONFIDENTIALITY AND DISCLAIMER The information contained in the following Marketing Brochure is proprietary and strictly confidential. It is intended to be reviewed only by the party

DOLLAR GENERAL BRAND NEW DOLLAR GENERAL 4709 W TRAPNELL, PLANT CITY, FL NOT ACTUAL STORE BENJAMIN SCHULTZ BRYAN BENDER

BRAND NEW DOLLAR GENERAL NOT ACTUAL STORE DOLLAR GENERAL 30445 Northwestern Highway, Suite 275 Farmington Hills, MI 48334 248.254.3410 fortisnetlease.com BRYAN BENDER MANAGING DIRECTOR D: 248.419.3810

BRAND NEW DOLLAR GENERAL NOT ACTUAL STORE DOLLAR GENERAL 30445 Northwestern Highway, Suite 275 Farmington Hills, MI 48334 248.254.3410 fortisnetlease.com BRYAN BENDER MANAGING DIRECTOR D: 248.419.3810

SINGLE TENANT INVESTMENT OPPORTUNITY NORTH CAROLINA CONNELLY SPRINGS ACTUAL SITE

SINGLE TENANT INVESTMENT OPPORTUNITY CONNELLY SPRINGS NORTH CAROLINA EXCLUSIVELY MARKETED BY JIM SCHUCHERT FIRST VICE PRESIDENT SRS NATIONAL NET LEASE GROUP 610 Newport Center Drive, Suite 1500 Newport

SINGLE TENANT INVESTMENT OPPORTUNITY CONNELLY SPRINGS NORTH CAROLINA EXCLUSIVELY MARKETED BY JIM SCHUCHERT FIRST VICE PRESIDENT SRS NATIONAL NET LEASE GROUP 610 Newport Center Drive, Suite 1500 Newport

JUDSON AND STAHL PAD SITE

JUDSON AND STAHL PAD SITE NWQ JUDSON & STAHL ROAD SAN ANTONIO, TX THOMAS TYNG 1604 ROLLING OAKS MALL PD C 44 7,1 T EC BJ SU 1604 Selma D MADISON HIGH SCHOOL 54 8,4 CP THE FORUM PD 1C,93 14 LIVE OAK CROSSING

JUDSON AND STAHL PAD SITE NWQ JUDSON & STAHL ROAD SAN ANTONIO, TX THOMAS TYNG 1604 ROLLING OAKS MALL PD C 44 7,1 T EC BJ SU 1604 Selma D MADISON HIGH SCHOOL 54 8,4 CP THE FORUM PD 1C,93 14 LIVE OAK CROSSING

Ground Lease NNN IREA. Actual Photo Richfield Parkway, Richfield, MN 55432

tcfbank Ground Lease NNN 6501 Richfield Parkway, Richfield, MN 55432 IREA tcfbank Actual Photo IREA INVESTMENT REAL ESTATE ASSOCIATES OFFICE 16501 Ventura Blvd. Suite 448 Encino, CA 91436 Phone: 818.386.6888

tcfbank Ground Lease NNN 6501 Richfield Parkway, Richfield, MN 55432 IREA tcfbank Actual Photo IREA INVESTMENT REAL ESTATE ASSOCIATES OFFICE 16501 Ventura Blvd. Suite 448 Encino, CA 91436 Phone: 818.386.6888

Click Image For Online Property Map

O F F E R I N G M E M O R A N D U M Click Image For Online Property Map DISCLOSURE : All materials and information received or derived from Fortis Net Lease (hereinafter collectively referred to as FNL

O F F E R I N G M E M O R A N D U M Click Image For Online Property Map DISCLOSURE : All materials and information received or derived from Fortis Net Lease (hereinafter collectively referred to as FNL

CORPORATE WOODS OFFICE BUILDING FOR SALE

CORPORATE WOODS OFFICE BUILDING FOR SALE 66210 JOHN SWEENEY, CCIM Senior Broker Associate john@reececommercial.com Ph: 913.945.3718 RC JENSEN, CCIM Senior Associate rc@reececommercial.com Ph: 913.945.3726

CORPORATE WOODS OFFICE BUILDING FOR SALE 66210 JOHN SWEENEY, CCIM Senior Broker Associate john@reececommercial.com Ph: 913.945.3718 RC JENSEN, CCIM Senior Associate rc@reececommercial.com Ph: 913.945.3726

DOLLAR GENERAL RELOCATION PLUS DOLLAR GENERAL 670 EAST ARCADIA AVE, DAWSON SPRINGS, KY ACTUAL STORE BENJAMIN SCHULTZ BRYAN BENDER

RELOCATION PLUS ACTUAL STORE 30445 Northwestern Highway, Suite 275 Farmington Hills, MI 48334 248.254.3410 fortisnetlease.com BRYAN BENDER BENJAMIN SCHULTZ MANAGING DIRECTOR D: 248.419.3810 BBENDER@FORTISNETLEASE.COM

RELOCATION PLUS ACTUAL STORE 30445 Northwestern Highway, Suite 275 Farmington Hills, MI 48334 248.254.3410 fortisnetlease.com BRYAN BENDER BENJAMIN SCHULTZ MANAGING DIRECTOR D: 248.419.3810 BBENDER@FORTISNETLEASE.COM

BANDERA & HAUSMAN PAD SITES

S NEC BANDERA & HAUSMAN ROADS SAN ANTONIO, TX 78023 SUB JEC T 17,5 87 C STEPHEN SCHNEIDER / CAROLYN MONROE 34, 100 C 36,7 5 8 CP D 35,92 0C KUENTZ ELEMENTARY 17,5 91 C TABLE OF CONTENTS SECTION I EXECUTIVE

S NEC BANDERA & HAUSMAN ROADS SAN ANTONIO, TX 78023 SUB JEC T 17,5 87 C STEPHEN SCHNEIDER / CAROLYN MONROE 34, 100 C 36,7 5 8 CP D 35,92 0C KUENTZ ELEMENTARY 17,5 91 C TABLE OF CONTENTS SECTION I EXECUTIVE

1636 NORTH VENTURA AVENUE

1636 NORTH VENTURA AVENUE VENTURA, CA 93001 OFFERING MEMORANDUM N O N - E N D O R S E M E N T A N D D I S C L A I M E R N O T I C E Non-Endorsements Marcus & Millichap is not affiliated with, sponsored

1636 NORTH VENTURA AVENUE VENTURA, CA 93001 OFFERING MEMORANDUM N O N - E N D O R S E M E N T A N D D I S C L A I M E R N O T I C E Non-Endorsements Marcus & Millichap is not affiliated with, sponsored

Beltway 8 & Hwy 90. SEC Beltway 8 and Hwy 90 (Crosby Freeway) Houston, Texas 77049

Houston, Texas 77049") Beltway 8 & Hwy 90 SEC Beltway 8 and Hwy 90 (Crosby Freeway) Houston, Texas 77049 BPI Realty Services Inc 3800 SW Freeway Suite 304 Houston, TX 77027 Phone: (281) 530-0900 Fax: (281) 530-0690 Beltway 8

Beltway 8 & Hwy 90 SEC Beltway 8 and Hwy 90 (Crosby Freeway) Houston, Texas 77049 BPI Realty Services Inc 3800 SW Freeway Suite 304 Houston, TX 77027 Phone: (281) 530-0900 Fax: (281) 530-0690 Beltway 8

NEW DOLLAR GENERAL FORTIS NET LEASE INVESTMENT REAL ESTATE SERVICES. 15 Year Absolute NNN lease Rare 3% Rent Increase in Year 11

NEW DOLLAR GENERAL 15 Year Absolute NNN lease Rare 3% Rent Increase in Year 11 203 J Ave, Eureka, SD 57437 Similar Store Design Shown - Not Actual Store FORTIS NET LEASE INVESTMENT REAL ESTATE SERVICES

NEW DOLLAR GENERAL 15 Year Absolute NNN lease Rare 3% Rent Increase in Year 11 203 J Ave, Eureka, SD 57437 Similar Store Design Shown - Not Actual Store FORTIS NET LEASE INVESTMENT REAL ESTATE SERVICES

4507 Spencer Hwy For Lease/Sale

4507 Spencer Hwy For Lease/Sale Location: 4507 Spencer Highway Pasadena, Texas 77515 Freestanding retail building in Pasadena, Texas on busy Spencer Highway. Ample parking and easy access. Area uses include

4507 Spencer Hwy For Lease/Sale Location: 4507 Spencer Highway Pasadena, Texas 77515 Freestanding retail building in Pasadena, Texas on busy Spencer Highway. Ample parking and easy access. Area uses include

Family Dollar. Turbeville, South Carolina RYAN D O CONNELL. CONTACT:

Family Dollar Turbeville, South Carolina CONTACT: RYAN D O CONNELL P. 602.595.4000 F. 602.467.3218 Ryan@rdoinvestments.com Office 602.595.4000 Fax 602.467.3218 3219 East Camelback Road, Phoenix, AZ 85018

Family Dollar Turbeville, South Carolina CONTACT: RYAN D O CONNELL P. 602.595.4000 F. 602.467.3218 Ryan@rdoinvestments.com Office 602.595.4000 Fax 602.467.3218 3219 East Camelback Road, Phoenix, AZ 85018

Pizza Hut - NPC International

Pizza Hut - NPC International OFFERING MEMORANDUM SITE PHOTO CONFIDENTIALITY AND DISCLAIMER The information contained in the following Marketing Brochure is proprietary and strictly confidential. It is

Pizza Hut - NPC International OFFERING MEMORANDUM SITE PHOTO CONFIDENTIALITY AND DISCLAIMER The information contained in the following Marketing Brochure is proprietary and strictly confidential. It is

DOLLAR GENERAL NEW ABSOLUTE NNN DOLLAR GENERAL 106 EAST LAPEER ST, PECK, MI BENJAMIN SCHULTZ BRYAN BENDER

NEW ABSOLUTE NNN 30445 Northwestern Highway, Suite 275 Farmington Hills, MI 48334 248.254.3410 fortisnetlease.com BRYAN BENDER MANAGING DIRECTOR D: 248.419.3810 BBENDER@FORTISNETLEASE.COM BENJAMIN SCHULTZ

NEW ABSOLUTE NNN 30445 Northwestern Highway, Suite 275 Farmington Hills, MI 48334 248.254.3410 fortisnetlease.com BRYAN BENDER MANAGING DIRECTOR D: 248.419.3810 BBENDER@FORTISNETLEASE.COM BENJAMIN SCHULTZ

POPEYES GROUND LEASE 3510 WEST BASELINE ROAD PHOENIX, ARIZONA Single Tenant Absolute Triple Net Investment Offering

Investment Properties CBRE Net Lease Single Tenant Absolute Triple Net Investment Offering POPEYES GROUND LEASE 3510 WEST BASELINE ROAD PHOENIX, ARIZONA 85339 www.cbre.com LAVEEN COMMONS SHOPPING CENTER

Investment Properties CBRE Net Lease Single Tenant Absolute Triple Net Investment Offering POPEYES GROUND LEASE 3510 WEST BASELINE ROAD PHOENIX, ARIZONA 85339 www.cbre.com LAVEEN COMMONS SHOPPING CENTER

MARKET SUMMARY MICHIGAN, METRO DETROIT AREA FOURTH QUARTER 2016 P LAN T E M OR AN CRES A. pmcresa.com

FOURTH QUARTER 2016 MICHIGAN, METRO DETROIT AREA MARKET SUMMARY P LAN T E M OR AN CRES A 26300 NORTHWESTERN HIGHWAY SOUTHFIELD, MI 48076 248.223.3500 pmcresa.com Connect with us for more information: Subscribe

FOURTH QUARTER 2016 MICHIGAN, METRO DETROIT AREA MARKET SUMMARY P LAN T E M OR AN CRES A 26300 NORTHWESTERN HIGHWAY SOUTHFIELD, MI 48076 248.223.3500 pmcresa.com Connect with us for more information: Subscribe

NORTHVILLE OUTSTANDING BUILD-TO-SUIT OPPORTUNITY TECHNOLOGY PARK FOR CORPORATE USER - OFFICE/TECH/R&D CONTACT US FOR SALE OR LEASE

FOR SALE OR LEASE NORTHVILLE TECHNOLOGY PARK OUTSTANDING BUILD-TO-SUIT OPPORTUNITY FOR CORPORATE USER - OFFICE/TECH/R&D 5 MILE AND BECK ROAD NORTHVILLE TOWNSHIP, MICHIGAN SOLD ZF TECHNOLOGIES REDICO is

FOR SALE OR LEASE NORTHVILLE TECHNOLOGY PARK OUTSTANDING BUILD-TO-SUIT OPPORTUNITY FOR CORPORATE USER - OFFICE/TECH/R&D 5 MILE AND BECK ROAD NORTHVILLE TOWNSHIP, MICHIGAN SOLD ZF TECHNOLOGIES REDICO is

US BANK. Table of Contents

Table of Contents US BANK Financial Overview Financial Overview....4 Tenant Overview....5 Lease Abstract.6 Investment Overview Investment Overview.. 8 Drone Photos..9 Site Aerials......10-11 Market Aerials....12-14

Table of Contents US BANK Financial Overview Financial Overview....4 Tenant Overview....5 Lease Abstract.6 Investment Overview Investment Overview.. 8 Drone Photos..9 Site Aerials......10-11 Market Aerials....12-14

Woodbridge Shopping Center Highway 6 & Voss Road

Woodbridge Shopping Center Highway 6 & Voss Road Highlights - Shadow Space to Kroger Store - Located at the Hard Corner of a Lighted Intersection on Hwy 6 - Pads Ideal for Fast Food, Bank, or Restaurant

Woodbridge Shopping Center Highway 6 & Voss Road Highlights - Shadow Space to Kroger Store - Located at the Hard Corner of a Lighted Intersection on Hwy 6 - Pads Ideal for Fast Food, Bank, or Restaurant

Boston Office MarketView

Boston Office MarketView CBRE Global Research and Consulting U.S. UNEMPLOYMENT 6.7% MA UNEMPLOYMENT 6.3% OCCUPIED SQ. FT. 70.0M AVAILABILITY 15.9% SUBLEASE SQ. FT. 1.1% UNDER CONSTRUCTION 1.8M FIRMS CHOOSE

Boston Office MarketView CBRE Global Research and Consulting U.S. UNEMPLOYMENT 6.7% MA UNEMPLOYMENT 6.3% OCCUPIED SQ. FT. 70.0M AVAILABILITY 15.9% SUBLEASE SQ. FT. 1.1% UNDER CONSTRUCTION 1.8M FIRMS CHOOSE

NEW DOLLAR GENERAL PLUS

NEW DOLLAR GENERAL PLUS 15 Year Absolute NNN lease Larger PLUS Store Design 5093 NC-88, Warrensville, NC 28693 Similar Store Design Shown - Not Actual Store FORTIS NET LEASE INVESTMENT REAL ESTATE SERVICES

NEW DOLLAR GENERAL PLUS 15 Year Absolute NNN lease Larger PLUS Store Design 5093 NC-88, Warrensville, NC 28693 Similar Store Design Shown - Not Actual Store FORTIS NET LEASE INVESTMENT REAL ESTATE SERVICES

Burger King - Cabazon Dinosaur Park

Burger King - Cabazon Dinosaur Park OFFERING MEMORANDUM CONFIDENTIALITY AND DISCLAIMER The information contained in the following Marketing Brochure is proprietary and strictly confidential. It is intended

Burger King - Cabazon Dinosaur Park OFFERING MEMORANDUM CONFIDENTIALITY AND DISCLAIMER The information contained in the following Marketing Brochure is proprietary and strictly confidential. It is intended

1636 NORTH VENTURA AVENUE

1636 NORTH VENTURA AVENUE VENTURA, CA 93001 OFFERING MEMORANDUM N O N - E N D O R S E M E N T A N D D I S C L A I M E R N O T I C E Non-Endorsements Marcus & Millichap is not affiliated with, sponsored

1636 NORTH VENTURA AVENUE VENTURA, CA 93001 OFFERING MEMORANDUM N O N - E N D O R S E M E N T A N D D I S C L A I M E R N O T I C E Non-Endorsements Marcus & Millichap is not affiliated with, sponsored

Shaw's - Peterborough, NH

, gendroncommercial@gmail.com 450 Baxter Blvd. Portland, ME 04103 207-939-8500 (p) 866-246-0114 (f) www.gendroncommercial.com Table of Contents Real Estate Investment Details Biography Property Description

, gendroncommercial@gmail.com 450 Baxter Blvd. Portland, ME 04103 207-939-8500 (p) 866-246-0114 (f) www.gendroncommercial.com Table of Contents Real Estate Investment Details Biography Property Description

MARKET INDICATORS Q Q TOTAL 2,909,848 IN DEALS

Research & Forecast Report DETROIT & ANN ARBOR OFFICE Q1 2017 OFFICE ENDS ON A STRONG NOTE Peter McGrath Metro Detroit s office market reported a strong first quarter, carrying over the previous quarter

Research & Forecast Report DETROIT & ANN ARBOR OFFICE Q1 2017 OFFICE ENDS ON A STRONG NOTE Peter McGrath Metro Detroit s office market reported a strong first quarter, carrying over the previous quarter

NN DOLLAR GENERAL PROVEN SALES! IN LEASE EXTENSION US HWY 72, ATHENS, AL REPRESENTATIVE PHOTO KYLE CARSON ANDY BENDER DAVID MORENO

PROVEN SALES! IN LEASE EXTENSION REPRESENTATIVE PHOTO NN DOLLAR GENERAL 30445 Northwestern Highway, Suite 275 Farmington Hills, MI 48334 248.254.3410 fortisnetlease.com KYLE CARSON SENIOR ADVISOR D: 248.419.3271

PROVEN SALES! IN LEASE EXTENSION REPRESENTATIVE PHOTO NN DOLLAR GENERAL 30445 Northwestern Highway, Suite 275 Farmington Hills, MI 48334 248.254.3410 fortisnetlease.com KYLE CARSON SENIOR ADVISOR D: 248.419.3271

NET LEASE INVESTMENT OFFERING MCDONALD S (GL) 1880 E Market Street Harrisonburg, VA 22801

1880 E Market Street Harrisonburg, VA 22801") MCDONALD S (GL) 1880 E Market Street Harrisonburg, VA 22801 TABLE OF CONTENTS TABLE OF CONTENTS I. Executive Profile Executive Summary Investment Highlights Property Overview II. Location Overview Photographs

MCDONALD S (GL) 1880 E Market Street Harrisonburg, VA 22801 TABLE OF CONTENTS TABLE OF CONTENTS I. Executive Profile Executive Summary Investment Highlights Property Overview II. Location Overview Photographs

Golden Corral. Golden Corral. Opelika, AL. Opelika, AL Birmingham Hwy

$2,313,835 9.5% CAP $219,814 NOI Brand new absolute triple net (NNN) 15 year lease; (2) 5 year options Large 10% escalations every 5 years, including options Rent was calculated as 8.75% of trailing twelve

$2,313,835 9.5% CAP $219,814 NOI Brand new absolute triple net (NNN) 15 year lease; (2) 5 year options Large 10% escalations every 5 years, including options Rent was calculated as 8.75% of trailing twelve

Sacramento Office MarketView Q3 2014

Sacramento Office MarketView Q3 2014 CBRE Global Research and Consulting UNEMPLOYMENT RATE 7.0% VACANCY RATE 19.4% NET ABSORPTION 123,907 sq. ft. AVG ASKING LEASE RATE $1.69 per sq. ft. FSG COMPLETED CONSTRUCTION

Sacramento Office MarketView Q3 2014 CBRE Global Research and Consulting UNEMPLOYMENT RATE 7.0% VACANCY RATE 19.4% NET ABSORPTION 123,907 sq. ft. AVG ASKING LEASE RATE $1.69 per sq. ft. FSG COMPLETED CONSTRUCTION

717 EAST 1ST STREET LONG BEACH, CA 90802

LONG BEACH, CA 90802 MULTI-FAMILY INVESTMENTS LONG BEACH, CA 90802 Sale Price: $1,249,000 Sale Price/SF: $319.93 Sale Price/Unit: $312,250 Rentable SF: 3,904 SF Lot Size SF: 7,511 SF Units: 4 Floors: 2

LONG BEACH, CA 90802 MULTI-FAMILY INVESTMENTS LONG BEACH, CA 90802 Sale Price: $1,249,000 Sale Price/SF: $319.93 Sale Price/Unit: $312,250 Rentable SF: 3,904 SF Lot Size SF: 7,511 SF Units: 4 Floors: 2

FOR SALE Absolute Net Retail Investment

PROPERTY HIGHLIGHTS: Dense population with over 175,000 residents within a 3-mile radius Brand new 5-year lease Strategically located along Highway 99 with immediate highway access Surrounded by strong

PROPERTY HIGHLIGHTS: Dense population with over 175,000 residents within a 3-mile radius Brand new 5-year lease Strategically located along Highway 99 with immediate highway access Surrounded by strong

FORTISNETLEASE A Sperry Van Ness Franchise

SUBJECT PROPERTY DISCLOSURE All materials and information received or derived from Sperry Van Ness Fortis Net Lease (hereinafter collectively Sperry Van Ness ), its directors, of icers, agents, advisors,

SUBJECT PROPERTY DISCLOSURE All materials and information received or derived from Sperry Van Ness Fortis Net Lease (hereinafter collectively Sperry Van Ness ), its directors, of icers, agents, advisors,

NEW DOLLAR GENERAL. 15 Year Absolute NNN lease M-63, Coloma, MI Not Actual Store

NEW DOLLAR GENERAL 15 Year Absolute NNN lease Not Actual Store Bryan Bender Managing Director bbender@fortisnetlease.com 248.419.3810 TABLE OF CONTENTS Investment Offering Property & Lease Dollar General

NEW DOLLAR GENERAL 15 Year Absolute NNN lease Not Actual Store Bryan Bender Managing Director bbender@fortisnetlease.com 248.419.3810 TABLE OF CONTENTS Investment Offering Property & Lease Dollar General

7 - ELEVEN ROMULUS, MICHIGAN. offering memorandum. Investment. Overview Financial. Overview. Financial. Overview. Lease. Lease.

3 9 3 9 0 E C O R S E R D R O M U L U S, M I C H I G A N 4 8 1 7 4 7 - ELEVEN ROMULUS, MICHIGAN offering memorandum INVESTMENT OVERVIEW Marcus & Millichap is pleased to present this recently extended 7-Eleven

3 9 3 9 0 E C O R S E R D R O M U L U S, M I C H I G A N 4 8 1 7 4 7 - ELEVEN ROMULUS, MICHIGAN offering memorandum INVESTMENT OVERVIEW Marcus & Millichap is pleased to present this recently extended 7-Eleven

THIS IS AN EXAMPLE REPORT

Ann Arbor Retail Space 2,000-4,000 SF, High Traffic Prepared on THIS IS AN EXAMPLE REPORT John, It was good speaking with you today. I've identified several spaces that appear to meet your needs. Look

Ann Arbor Retail Space 2,000-4,000 SF, High Traffic Prepared on THIS IS AN EXAMPLE REPORT John, It was good speaking with you today. I've identified several spaces that appear to meet your needs. Look

100% OCCUPIED - 2 TENANT INDUSTRIAL INVESTMENT. Sun MCLEOD BUSINESS CENTER E. Post Road, Las Vegas, Nevada Commercial Real Estate, Inc.

0% OCCUPIED - TENANT INDUSTRIAL INVESTMENT Sun Commercial Real Estate, Inc. MCLEOD BUSINESS CENTER 70 E. Post Road, Las Vegas, Nevada 890 Contact Team Lisa Hauger Senior Vice President 70-968-7333 LisaH@suncommercialre.com