9/18/2018. Federal Tax Issues. Agenda. CE Holder Approval Provisions. Handouts and Rally App. The Latest and Greatest

|

|

|

- Wesley Terry

- 5 years ago

- Views:

Transcription

1 9/18/2018 Agenda Federal Tax Issues The Latest and Greatest Rob Levin, Jessica Jay, Steve Small October 12/13, 2018 CE Holder Approval Provisions (10 Minutes) Public Recreation Test in Deductible CE (5 Minutes) Habitat Test in Deductible CE (5 Minutes) Valuation (5 Minutes) Quid Pro Quo Cases (10 Minutes) Tax Credit Limit Proposed Regulation (5 Minutes) Amendment Law Update (5 Minutes) Syndication Update (10 Minutes) Lessee as Donor (5 Minutes) CE Termination Proceeds Provision (15 Minutes) Q&A (15 Minutes) #Rally #RALLY2018 LAND TRUST ALLIANCE Handouts and Rally App CE Holder Approval Provisions Handouts > Termination Proceeds Examples > PowerPoint Slides Rally App > Alliance Letter to Karin Gross on Termination Proceeds > Case decisions/opinions Hoffman Properties, II, L.P. v. Commissioner, No > Three unpublished Tax Court orders finding that default approval provisions in conservation/preservation easements violate perpetuity requirement. > Historic preservation façade easement on building in Cleveland. > Disputed provision: If AAHP fails to expressly reject Hoffman's proposal within 45 days of receiving such, the easement provides Hoffman with automatic approval to "undertake the proposed activity in accordance with the plan or request submitted". 3 #RALLY2018 LAND TRUST ALLIANCE 4 #RALLY2018 LAND TRUST ALLIANCE 1

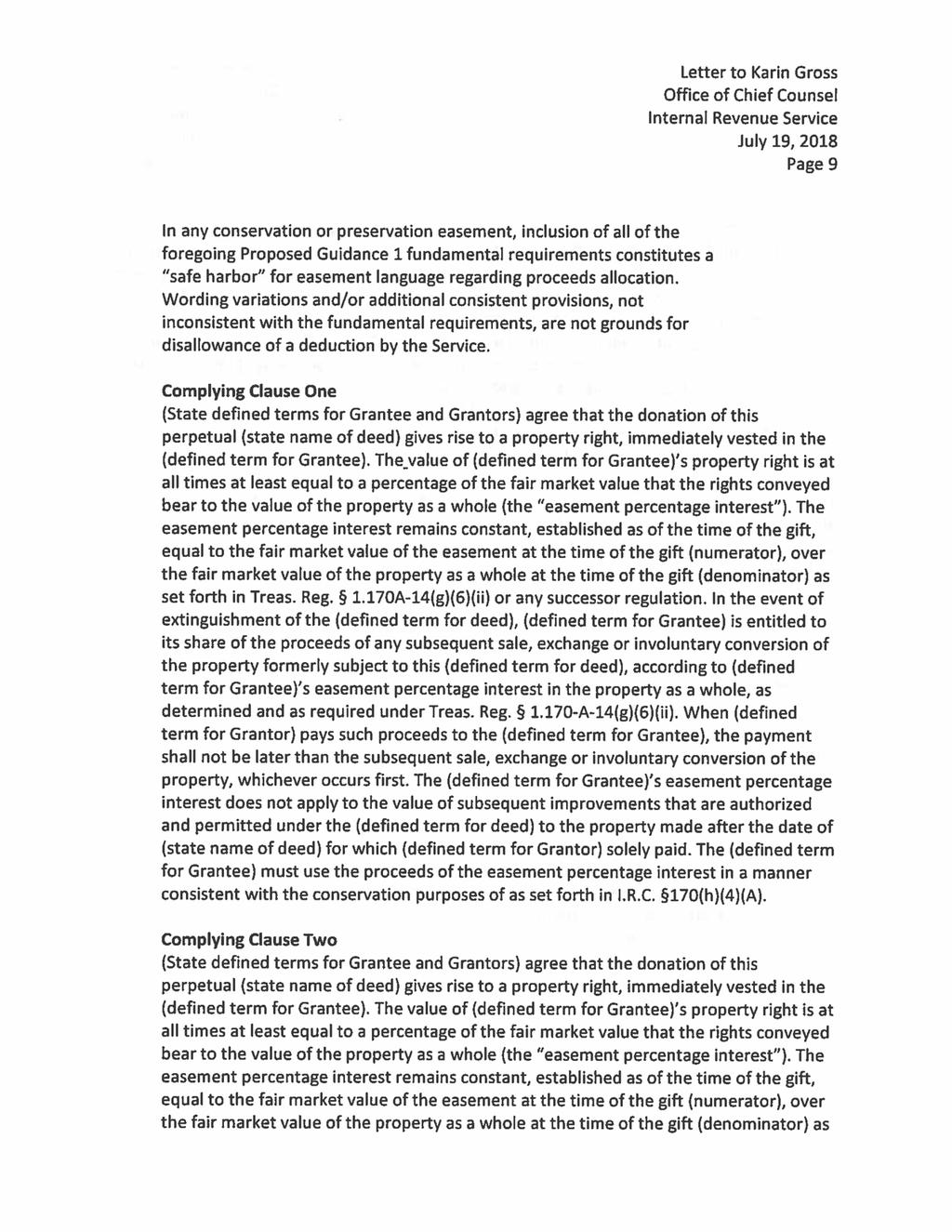

2 9/18/2018 CE Holder Approval Provisions Hoffman Properties, II, L.P. v. Commissioner, No o Decision default approval provision violated prohibition and preservation requirement of 170(h)(4)(B)(i). o Decision 1 same provision also violated exclusively for conservation purposes requirement of 170(h)(5) o Decision 2 Denied motion to reconsider decision. CE Holder Approval Provisions Hoffman Properties, II, L.P. v. Commissioner, No > Tax Court: Default approval provision was categorical. Landowner had no affirmative duty to self-evaluate its request against the regulatory standards. Even blatantly inconsistent request could sneak through if Holder wasn t paying attention. 5 #RALLY2018 LAND TRUST ALLIANCE 6 #RALLY2018 LAND TRUST ALLIANCE CE Holder Approval Provisions Alternate Approval Provision 1 > In the event that HOLDER fails to respond to GRANTOR s request within sixty (60) days, GRANTOR may proceed with the requested activity only if the following conditions are met: (a) HOLDER provided acknowledgment of receipt of the original request; (b) GRANTOR provides a separate written notice of its intent to proceed with the requested activity; (c) GRANTOR does not proceed with the requested activity until five (5) business days after providing such separate written notice of its intent to proceed; (d) GRANTOR does not receive any objection from HOLDER of GRANTOR s separate written notice of its intent to proceed; and (e) the activity in question is not contrary to any express or implied restriction in the Conservation Easement. CE Holder Approval Provisions Alternate Approval Provision 2 > Holder s failure to respond within the sixty (60) day period shall be deemed a constructive denial, and Owner may seek relief from the courts and recover reasonable fees and costs if a court rules the constructive denial unjustified. 7 #RALLY2018 LAND TRUST ALLIANCE 8 #RALLY2018 LAND TRUST ALLIANCE 2

3 9/18/2018 Public Recreational Access in Deductible CE I.R.C. 170(h)(4)(A)(i) > preservation of land areas for outdoor recreation by, or the education of, the general public Treas. Reg A-14(d)(2)(ii) > substantial and regular use of the general public Public Recreational Access in Deductible CE PBBM Rose Hill v. Commissioner, --- F.3d --- (5 th Cir. 2018) > CE on golf course in gated community. Tax Court ruled that CE didn t meet any of conservation purposes tests (open space, habitat, or public recreation). Taxpayer appealed on public recreation issue. > 27-hole golf course at time of CE donation. But after donation HOA purchased property and converted 9 holes into park for use of subdivision lot owners. Public allowed to pay to play golf, but not allowed to access park. 9 #RALLY2018 LAND TRUST ALLIANCE 10 #RALLY2018 LAND TRUST ALLIANCE Public Recreational Access in Deductible CE Public Recreational Access in Deductible CE PBBM Rose Hill v. Commissioner, --- F.3d --- (5 th Cir. 2018) > Issue 1 Should the degree of public access be evaluated only according to the four corners of the CE, or also take into account subsequent actions by landowner? > 5 th Circuit held that in general, courts should look only to the CE itself. Triangulated from other subsections of CE regs that referred to the terms of the easement or at the time of the gift. Exception where donor knew or should have known that public access would not be at the level provided for in the CE. 11 #RALLY2018 LAND TRUST ALLIANCE 12 #RALLY2018 LAND TRUST ALLIANCE 3

4 9/18/2018 Public Recreational Access in Deductible CE PBBM Rose Hill v. Commissioner, --- F.3d --- (5 th Cir. 2018) > Issue 2 - Contradictory provisions in CE about public access. Some said no public access, others said substantial and regular public access. Which prevailed? o 5 th Circuit said provisions allowing public access were more specific than the provisions precluding public access. o But how specific were they? Public Recreational Access in Deductible CE PBBM Rose Hill v. Commissioner, --- F.3d --- (5 th Cir. 2018) > Did the 5 th Circuit get the public access issues right? > What is the Holder s obligation to enforce the public access terms of the CE? 5 th Circuit doesn t really address that question. > If two-thirds of a large protected property is open for public recreational access but one-third is placed off limits, should that disqualify a deduction? > Should a pay-to-play golf course be considered accessible for public recreation? ($35 to play 18 holes) 13 #RALLY2018 LAND TRUST ALLIANCE 14 #RALLY2018 LAND TRUST ALLIANCE Habitat Test in Deductible CE Habitat Test in Deductible CE Champions Retreat Golf Founders, LLC v. Commissioner, 2018 T.C. 146 (U.S.T.C. Sept. 10, 2018) > Another golf course habitat case. See Atkinson, PBBM-Rose Hill, and Kiva Dunes (sort of) > Another NALT case (sixth so far) > All kinds of red flags o o o Syndicated deal Put together by accountant to rescue failing golf club High appraisal ($10M) 15 #RALLY2018 LAND TRUST ALLIANCE 16 #RALLY2018 LAND TRUST ALLIANCE 4

5 9/18/2018 Habitat Test in Deductible CE Champions Retreat Golf Founders, LLC v. Commissioner > Good news: Rare, threatened, or endangered species not limited to federal Endangered Species Act > But: not a sufficient presence of such species to meet habitat test > Extensive analysis of bird species. Conclusion: No highly threatened birds, only more common ones. > Southern fox squirrel in decline but not threatened > One arguably threatened plant species, but only found in small portion of Protected Property (17%), and pesticides used on golf course could harm it. Habitat Test in Deductible CE Champions Retreat Golf Founders, LLC v. Commissioner > Contributes to ecological viability or nearby park or preserve o o o Sumter National Forest was across river from Protected Property No go because PP was not a natural area Pesticides Golf course vegetation management Same holding as in Atkinson 17 #RALLY2018 LAND TRUST ALLIANCE 18 #RALLY2018 LAND TRUST ALLIANCE Habitat Test in Deductible CE How much do these golf course habitat cases threaten good CE projects? > Not at all? Marginally? Seriously? > Tips going forward: o Don t mail it in on habitat. (Especially if open space, recreation, historic preservation are also questionable.) o Apply a meaningful pesticides standard, if at all possible. o If deduction is important and habitat is best case, consider tailoring CE s to avoid marginal or un-natural habitats. o Don t worry too much (yet) these are all golf course cases. Remember Butler CE Valuation PBBM Rose Hill v. Commissioner, --- F.3d --- (5 th Cir. 2018) > Taxpayer s appraiser found Before value of $15,680,000 o Attorney s letter opining on right to develop commercially was key to Taxpayer appraisal s Extraordinary Assumption > IRS found Before value of $2,400,000 > Tax Court sided with IRS. > Fifth Circuit affirmed. 19 #RALLY2018 LAND TRUST ALLIANCE 20 #RALLY2018 LAND TRUST ALLIANCE 5

6 9/18/2018 CE Valuation Key Issues: Highest and Best Use When is additional development reasonable and probable? > As of right vs. requiring public review and approval (e.g., rezoning) > How to factor in the strength of neighborhood opposition? > How to weigh the validity of a privately granted use restriction? The tells in PBBM > Taxpayer sold the property for $2.3 million to the property owners association. > Attorney who wrote letter was not called to testify Quid Pro Quo in Charitable Donation/CEs Quid Pro Quo Cases o Wendell Falls o Triumph Mixed Use 21 #RALLY2018 LAND TRUST ALLIANCE 22 #RALLY2018 LAND TRUST ALLIANCE Quid Pro Quo Conservation Easement Wendell Falls Development, LLC v. Commissioner, T.C. Memo (U.S.T.C. April 4, 2018), (NC), (Motion for reconsideration pending) > LLC owns 1,280 acres; plans mixed-use community, 125-acre park to County, CE to land trust > Town approves PUD on 1,280 acres with 125 acres designated as park, states no preferential zoning in return > LLC agrees to sell 125 acres to County at appraised value with condition that LLC convey CE > LLC conveys CE on 125 acres to land trust, sells land to County > LLC claims charitable deduction of $4,818,000 based on appraisal of CE > IRS disallows on valuation and lack of donative intent, with penalties Quid Pro Quo Conservation Easement > Tax Court denies deduction on summary judgment: o Agrees with IRS that LLC conveyed CE with expectation of receiving substantial benefit of increased value to residential lots located near conserved land o Finds CE had zero value because highest and best use of 125 acres was as a park o o Finds enhanced value to LLC s abutting property outweighed any value of the easement Declines to assess any penalties applying reasonable cause and good faith exception in I.R.C. 6664(c)(1) 23 #RALLY2018 LAND TRUST ALLIANCE 24 #RALLY2018 LAND TRUST ALLIANCE 6

7 9/18/2018 Quid Pro Quo Conservation Easement Court s reasoning blended several different federal tax concepts > Substantial benefits analysis really donative intent and quid pro quo principles > Substantial benefits analysis cursory, with facts much less damning to LLC than other cases (Pollard v. Commissioner or Costello v. Commissioner) > Muddled enhancement issue, relevant only to valuation and not to deductibility analysis > Accepted without detailed analysis that enhancement effect exceeded value of CE Quid Pro Quo Charitable Donation Land Triumph Mixed Use Investments III, LLC v. Commissioner, T.C. Memo (U.S.T.C. May 15, 2018), (UT), appeal period open > LLC owns 2,800 acres of land, seeks to develop planned community for which 10% of land must remain undeveloped open space > City approves plans allowing 3,500 residential units; amends to allow additional 3,500 units with 1,000 acres of open space to be given to City > Final agreement of 747 acres open space to City and reduction by 2000 units > State transfer is voluntary charitable donation made without consideration, City s approval of plans was in no way contingent upon transfer of property. > LLC claims $11,040,000 charitable contribution deduction for land transfer > The IRS challenges the deduction in its entirety 25 #RALLY2018 LAND TRUST ALLIANCE 26 #RALLY2018 LAND TRUST ALLIANCE Quid Pro Quo Charitable Donation Land Proposed Fed. Regulation for State Tax Credits Tax Court denies deduction in entirety: > Finds LLC transferred 747 acres and development credits as quid pro quo exchange for current approval of concept plan and future approval of area plan > Finds despite provisions of agreement characterizing transfers as voluntary donations, external features of transaction evidenced by back and forth negotiations between City and LLC demonstrated a clear quid pro quo arrangement > Denied in its entirety because LLC failed to place any value on consideration of approvals following Pollard v. Commissioner and Seventeen Seventy Sherman St., LLC v. Commissioner *Takeaway--taxpayer cannot paper over quid pro quo arrangement with a purported donation agreement; proof is in the pudding Outgrowth of 2017 tax law $10,000-a-year cap on deductions for state and local taxes (SALT) > Response to NY and NJ work around tax credits > Requires federal deduction reduction by amount of state tax credit, unless tax credit is 15% or less of contribution > Effective August 27, 2018 with 45 day comment period > Relies on quid pro quo > Negative impact on conservation tax credits (CO, VA) > Potential coordinated response: o o o Beyond scope of original law Tax credits are not quid pro quo Grandfather/exclude conservation tax credits 27 #RALLY2018 LAND TRUST ALLIANCE 28 #RALLY2018 LAND TRUST ALLIANCE 7

8 9/18/2018 Amendment Law Update No Movement in Legal Cases > Three federal tax cases where IRS challenges amendment clauses as non-perpetual Sells, et al., v. Commissioner (Alliance amicus granted), Kumar, et al., v. Commissioner, (Alliance amicus granted), Pine Mountain Preserve, LLLP v. Commissioner, (Alliance amicus denied) No Movement in Regulation > IRS Notice Request for Comments to Priority Guidance Plan for 170(h) charitable contributions of conservation easements (Alliance Position Paper and Transmittal Letter) Amendment Law Update Yes Movement on Drafting Guidance: Alliance checklist of 8 elements: 1. Perpetual CE; intent to protect conservation purposes perpetually 2. Acknowledge natural conditions, landscape, consistent uses, economic and cultural conditions and technologies change over time 3. Full disclosure nothing requires Grantor/Grantee to modify CE 4. Grantee sole discretion for all determinations 5. Incorporate all Amendment Principles 6. Conform to all Grantee policies in effect at time of amendment 7. Approval dictated by state law, and U.S. Tax Code if donated 8. Discretionary approval, waiver and consent can be encompassed 29 #RALLY2018 LAND TRUST ALLIANCE 30 #RALLY2018 LAND TRUST ALLIANCE Syndication To stop syndicated conservation easement deduction transactions, we need legislative relief, a fix to the current tax code rules. > 1.IRS auditors are outgunned and outnumbered, best efforts are a drop in the bucket. > 2.Litigation process takes so long, not much of a deterrence to current investors. > 3.Investors are either (a) happily buying a package that seems too good to be true, but the investors are reassured by promoters, consultants, law firms, etc; Or (b) investors know they are buying into a tax shelter but are keenly aware of points 1 and 2 above. Syndication IRS Notice (December 2017) > Requires reporting a transaction as a Listed Transaction (which requires filing a separate form with the IRS identifying what you are doing) if a transaction meets the following requirements: o Oral or written promotional material; o Investors; o Promised federal tax deduction that is at least 250% of the investor s investment; and o A contribution and resulting deduction 31 #RALLY2018 LAND TRUST ALLIANCE 32 #RALLY2018 LAND TRUST ALLIANCE 8

and Senate (S.")

9 9/18/2018 Syndication IRS Large Business and International Division > September 2018 announcement new campaign targeting syndicated conservation easement transactions. Syndication Charitable Conservation Easement Program Integrity Act > House (H.R. 4459) and Senate (S. 2436) > Legislative language is complicated, relies on crossreferencing sections of the tax code partnership taxation provisions. > Summary: If you make an investment in a transaction, and the deduction you receive is greater than 250% of your investment, the deduction will be limited to 250% of your investment. There are exceptions to the rule, including for easement donations by family partnerships, but the rule is very carefully drafted to target syndicated conservation easement deduction tax shelters. 33 #RALLY2018 LAND TRUST ALLIANCE 34 #RALLY2018 LAND TRUST ALLIANCE Lessee as Donor Harbor Lofts: Vamp Building in Lynn, MA Lessee as Donor Harbor Lofts Associates v. Commissioner, 151 T.C. No. 3 (U.S.T.C. August 27, 2018) > Held: Harbor Lofts, as a long-term lessee of the two buildings, does not hold a fee interest in the property subject to the facade easement and cannot contribute a conservation easement under I.R.C. sec. 170(h). > Held, further, a lessee is not entitled to a charitable contribution deduction under I.R.C. sec. 170(h) for joining the fee owner of real property in granting a conservation easement. 35 #RALLY2018 LAND TRUST ALLIANCE 36 #RALLY2018 LAND TRUST ALLIANCE 9

10 9/18/2018 CE Termination Proceeds Provision Issue: In recent years, IRS began challenging CE deductions because the termination proceeds provision tweaked the Regulation language by allowing credit to the landowner for the value of improvements allowed under the CE. Land Trust Alliance letter to IRS. CE Termination Proceeds Provision PBBM Rose Hill v. Commissioner, --- F.3d - -- (5 th Cir. 2018) > CE provided that any amount attributable to improvements constructed on the Conservation Area, as well as actual bona fide expenses of the sale, should be subtracted from the total proceeds before determining the respective proportionate shares due to the Grantee and the Grantor. > Deduction denied. 37 #RALLY2018 LAND TRUST ALLIANCE 38 #RALLY2018 LAND TRUST ALLIANCE CE Termination Proceeds Provision PBBM Rose Hill v. Commissioner, --- F.3d --- (5 th Cir. 2018) > CE s termination proceeds provision included adjustment for any amount attributable to improvements constructed on the Conservation Area, as well as actual bona fide expenses of the sale. > Deduction denied. > The regulation does not indicate that any amount, including that attributable to improvements, may be subtracted out. CE Termination Proceeds Provision What do we do with current CE projects? > Keep improvements language out of termination provision and hope this never comes up > Continue using improvements language and be prepared to fight IRS on issue > Structure CE so improvements are excluded from deductible CE (i.e., not subject to any CE or placed in separate non-deductible CE) > See handout Proceeds Provision Examples 39 #RALLY2018 LAND TRUST ALLIANCE 40 #RALLY2018 LAND TRUST ALLIANCE 10

11 9/18/2018 CE Termination Proceeds Provision CE Termination Proceeds Provision Case By Case Approach > In many easements, there are no reserved rights to build value-enhancing improvements don t worry be happy. > Appreciate rarity of extreme situation where CE is completely or mostly terminated. 41 #RALLY2018 LAND TRUST ALLIANCE 42 #RALLY2018 LAND TRUST ALLIANCE 11

12 Conservation Easement Termination Proceeds Provision Steve Small s Fun Examples Example 1 Aunt Sally has a 100-acre farm. The farm is valued at $1 million. The farm includes Sally s residence, and a barn and other outbuildings. Aunt Sally conveys a conservation easement on the farm to the local land trust. The easement allows continuing agricultural activity, but no other residential, commercial, or industrial improvements. Assume the easement document includes the simple version of the proceeds rule. The value of the property after the easement is $400,000. According to the regulations and the proceeds rule, Aunt Sally is treated as having made a gift to the land trust of 60% of the value of the farm. The land trust is now treated as owning a 60% interest in the value of the farm, but, actually, only if and when the extinguishment and proceeds rule is triggered at some point in the future. If the easement is never extinguished, the 60% interest remains nothing but a concept. Time goes by, some event occurs that makes it impractical to keep the easement in place. The then-current landowner and the land trust go to court and the court agrees that under all the circumstances the easement can be extinguished, and it is. The property is sold for $2 million. According to the proceeds rule, what is the land trust s share of the $2 million? What is the landowner s share of the $2 million? Aaaah for the simple days of yesteryear. Bonus question: Is the land trust s share of the $2 million unrelated business income? 1

13 Example 2 Assume generally the same facts as in Example 1, except under the provisions of the easement Sally reserves the right to divide and convey from the property two five-acre lots, with the right to build one residence and appropriate outbuildings on each lot. The value of the farm (before the easement) is still $1,000,000. The easement reduces the value of the farm to $600,000. Under the proceeds rule, the land trust now has a proportionate interest of 40%. Time goes by, Sally sells one of the house lots to a new owner, who pays for the construction of a new principal residence and other allowed outbuildings. More time goes by, Sally sells the farm, including the remaining five-acre lot, to a new owner. The new owner needs cash, and sells the five-acre lot to another person, who pays for the construction of a new principal residence and other allowed outbuildings. More time goes by, the easement becomes impractical, the three then-current landowners and the land trust go to court and the court agrees that the easement can be extinguished, and it is. The property is sold for $3 million. According to the proceeds rule, how much does the land trust get? How is the balance of the money distributed? If the land trust gets $1.2 million, that leaves $1.8 million to divide among the three current landowners. The owner of the first house lot has an appraisal that values the house and lot at $550,000. The owner of the second house and lot has an appraisal that values that house and lot at $650,000. Assume you are the landowners, not the land trust. Does that work for you? 2

14 Example 3 Assume all of the same people and dollar facts as in Example 2, except the deed of easement follows the simple proceeds rule, BUT modified in this manner: After subtracting from the total proceeds any amount attributable to the value of improvements constructed by Grantor, Grantee shall be entitled to its proportionate share (as hereinabove defined) of the proceeds. Assume the value attributable to the improvements on the two house lots is $550,000 and $650,000 respectively. Recap: the property sold for $3,000,000. Subtracting the $1,200,000 attributable to improvements leaves $1,800,000. The land trust s share is $720,000 (40% of $1,800,000). The three landowners are now free to argue about how to divide up the balance of the proceeds. In Example 2, without the carve-out for improvements, the land trust receives $1,200,000. With the carve-out, the land trust receives $720,000. Is this fair? Discuss. Example 4 Assume all of the same facts as in Example 3, with this difference: there is a final determination by the IRS, or by a court of competent jurisdiction, that the easement did not qualify for a deduction in the first place because of the netting out of the value of improvements (or, actually, for any other reason). Of course the easement was still recorded and therefore enforceable in perpetuity. What is the result? Is this fair? If there was no deduction, should the land trust be entitled to any of the proceeds? Discuss. 3

15 Example 5 Assume all of the same facts as in Example 4 (easement; netting out of improvements, same numbers; deduction denied), except the easement document includes the following language at an appropriate place in the proceeds rule: Pursuant to Treas. Reg. Section 1.170A-14(g)(6)(ii) (first sentence), requiring the determination of the value of the Easement on the effective date of this grant, Grantor and Grantee hereby agree to amend such values, if necessary, to reflect any final determination of such value by the Internal Revenue Service or court of competent jurisdiction in any appeal of the final determination by the Internal Revenue Service. (emphasis added) Example 6 What about if the proceeds clause also (or instead) included this provision: After subtracting from the total proceeds any actual bona fide expenses of the sale, Grantee shall be entitled to its proportionate share (as hereinabove defined) of the proceeds. 4

16 Federal Tax Issues The Latest and Greatest Rob Levin, Jessica Jay, Steve Small October 12/13, 2018 #Rally2018

17 Agenda CE Holder Approval Provisions (10 Minutes) Public Recreation Test in Deductible CE (5 Minutes) Habitat Test in Deductible CE (5 Minutes) Valuation (5 Minutes) Quid Pro Quo Cases (10 Minutes) Tax Credit Limit Proposed Regulation (5 Minutes) Amendment Law Update (5 Minutes) Syndication Update (10 Minutes) Lessee as Donor (5 Minutes) CE Termination Proceeds Provision (15 Minutes) Q&A (15 Minutes) 2 #RALLY2018 LAND TRUST ALLIANCE

18 Handouts and Rally App Handouts > Termination Proceeds Examples > PowerPoint Slides Rally App > Alliance Letter to Karin Gross on Termination Proceeds > Case decisions/opinions 3 #RALLY2018 LAND TRUST ALLIANCE

19 CE Holder Approval Provisions Hoffman Properties, II, L.P. v. Commissioner, No > Three unpublished Tax Court orders finding that default approval provisions in conservation/preservation easements violate perpetuity requirement. > Historic preservation façade easement on building in Cleveland. > Disputed provision: If AAHP fails to expressly reject Hoffman's proposal within 45 days of receiving such, the easement provides Hoffman with automatic approval to "undertake the proposed activity in accordance with the plan or request submitted". 4 #RALLY2018 LAND TRUST ALLIANCE

20 CE Holder Approval Provisions Hoffman Properties, II, L.P. v. Commissioner, No o o Decision default approval provision violated prohibition and preservation requirement of 170(h)(4)(B)(i) Decision 1 same provision also violated exclusively for conservation purposes requirement of 170(h)(5) o Decision 2 Denied motion to reconsider decision. 5 #RALLY2018 LAND TRUST ALLIANCE

21 CE Holder Approval Provisions Hoffman Properties, II, L.P. v. Commissioner, No > Tax Court: Default approval provision was categorical. Landowner had no affirmative duty to self-evaluate its request against the regulatory standards. Even blatantly inconsistent request could sneak through if Holder wasn t paying attention. 6 #RALLY2018 LAND TRUST ALLIANCE

22 CE Holder Approval Provisions Alternate Approval Provision 1 > In the event that HOLDER fails to respond to GRANTOR s request within sixty (60) days, GRANTOR may proceed with the requested activity only if the following conditions are met: (a) HOLDER provided acknowledgment of receipt of the original request; (b) GRANTOR provides a separate written notice of its intent to proceed with the requested activity; (c) GRANTOR does not proceed with the requested activity until five (5) business days after providing such separate written notice of its intent to proceed; (d) GRANTOR does not receive any objection from HOLDER of GRANTOR s separate written notice of its intent to proceed; and (e) the activity in question is not contrary to any express or implied restriction in the Conservation Easement. 7 #RALLY2018 LAND TRUST ALLIANCE

23 CE Holder Approval Provisions Alternate Approval Provision 2 > Holder s failure to respond within the sixty (60) day period shall be deemed a constructive denial, and Owner may seek relief from the courts and recover reasonable fees and costs if a court rules the constructive denial unjustified. 8 #RALLY2018 LAND TRUST ALLIANCE

24 Public Recreational Access in Deductible CE I.R.C. 170(h)(4)(A)(i) > preservation of land areas for outdoor recreation by, or the education of, the general public Treas. Reg A-14(d)(2)(ii) > substantial and regular use of the general public 9 #RALLY2018 LAND TRUST ALLIANCE

25 Public Recreational Access in Deductible CE PBBM Rose Hill v. Commissioner, --- F.3d --- (5 th Cir. 2018) > CE on golf course in gated community. Tax Court ruled that CE didn t meet any of conservation purposes tests (open space, habitat, or public recreation). Taxpayer appealed on public recreation issue. > 27-hole golf course at time of CE donation. But after donation HOA purchased property and converted 9 holes into park for use of subdivision lot owners. Public allowed to pay to play golf, but not allowed to access park. 10 #RALLY2018 LAND TRUST ALLIANCE

26 Public Recreational Access in Deductible CE 11 #RALLY2018 LAND TRUST ALLIANCE

27 Public Recreational Access in Deductible CE PBBM Rose Hill v. Commissioner, --- F.3d --- (5 th Cir. 2018) > Issue 1 Should the degree of public access be evaluated only according to the four corners of the CE, or also take into account subsequent actions by landowner? > 5 th Circuit held that in general, courts should look only to the CE itself. Triangulated from other subsections of CE regs that referred to the terms of the easement or at the time of the gift. Exception where donor knew or should have known that public access would not be at the level provided for in the CE. 12 #RALLY2018 LAND TRUST ALLIANCE

28 Public Recreational Access in Deductible CE PBBM Rose Hill v. Commissioner, --- F.3d --- (5 th Cir. 2018) > Issue 2 - Contradictory provisions in CE about public access. Some said no public access, others said substantial and regular public access. Which prevailed? o o 5 th Circuit said provisions allowing public access were more specific than the provisions precluding public access. But how specific were they? 13 #RALLY2018 LAND TRUST ALLIANCE

29 Public Recreational Access in Deductible CE PBBM Rose Hill v. Commissioner, --- F.3d --- (5 th Cir. 2018) > Did the 5 th Circuit get the public access issues right? > What is the Holder s obligation to enforce the public access terms of the CE? 5 th Circuit doesn t really address that question. > If two-thirds of a large protected property is open for public recreational access but one-third is placed off limits, should that disqualify a deduction? > Should a pay-to-play golf course be considered accessible for public recreation? ($35 to play 18 holes) 14 #RALLY2018 LAND TRUST ALLIANCE

30 Habitat Test in Deductible CE Champions Retreat Golf Founders, LLC v. Commissioner, 2018 T.C. 146 (U.S.T.C. Sept. 10, 2018) > Another golf course habitat case. See Atkinson, PBBM-Rose Hill, and Kiva Dunes (sort of) > Another NALT case (sixth so far) > All kinds of red flags o o o Syndicated deal Put together by accountant to rescue failing golf club High appraisal ($10M) 15 #RALLY2018 LAND TRUST ALLIANCE

31 Habitat Test in Deductible CE 16 #RALLY2018 LAND TRUST ALLIANCE

32 Habitat Test in Deductible CE Champions Retreat Golf Founders, LLC v. Commissioner > Good news: Rare, threatened, or endangered species not limited to federal Endangered Species Act > But: not a sufficient presence of such species to meet habitat test > Extensive analysis of bird species. Conclusion: No highly threatened birds, only more common ones. > Southern fox squirrel in decline but not threatened > One arguably threatened plant species, but only found in small portion of Protected Property (17%), and pesticides used on golf course could harm it. 17 #RALLY2018 LAND TRUST ALLIANCE

33 Habitat Test in Deductible CE Champions Retreat Golf Founders, LLC v. Commissioner > Contributes to ecological viability or nearby park or preserve o o o Sumter National Forest was across river from Protected Property No go because PP was not a natural area Pesticides Golf course vegetation management Same holding as in Atkinson 18 #RALLY2018 LAND TRUST ALLIANCE

34 Habitat Test in Deductible CE How much do these golf course habitat cases threaten good CE projects? > Not at all? Marginally? Seriously? > Tips going forward: o o o o Don t mail it in on habitat. (Especially if open space, recreation, historic preservation are also questionable.) Apply a meaningful pesticides standard, if at all possible. If deduction is important and habitat is best case, consider tailoring CE s to avoid marginal or un-natural habitats. Don t worry too much (yet) these are all golf course cases. Remember Butler 19 #RALLY2018 LAND TRUST ALLIANCE

35 CE Valuation PBBM Rose Hill v. Commissioner, --- F.3d --- (5 th Cir. 2018) > Taxpayer s appraiser found Before value of $15,680,000 o Attorney s letter opining on right to develop commercially was key to Taxpayer appraisal s Extraordinary Assumption > IRS found Before value of $2,400,000 > Tax Court sided with IRS. > Fifth Circuit affirmed. 20 #RALLY2018 LAND TRUST ALLIANCE

36 CE Valuation Key Issues: Highest and Best Use When is additional development reasonable and probable? > As of right vs. requiring public review and approval (e.g., rezoning) > How to factor in the strength of neighborhood opposition? > How to weigh the validity of a privately granted use restriction? The tells in PBBM > Taxpayer sold the property for $2.3 million to the property owners association. > Attorney who wrote letter was not called to testify 21 #RALLY2018 LAND TRUST ALLIANCE

37 Quid Pro Quo in Charitable Donation/CEs Quid Pro Quo Cases o Wendell Falls o Triumph Mixed Use 22 #RALLY2018 LAND TRUST ALLIANCE

38 Quid Pro Quo Conservation Easement Wendell Falls Development, LLC v. Commissioner, T.C. Memo (U.S.T.C. April 4, 2018), (NC), (Motion for reconsideration pending) > LLC owns 1,280 acres; plans mixed-use community, 125-acre park to County, CE to land trust > Town approves PUD on 1,280 acres with 125 acres designated as park, states no preferential zoning in return > LLC agrees to sell 125 acres to County at appraised value with condition that LLC convey CE > LLC conveys CE on 125 acres to land trust, sells land to County > LLC claims charitable deduction of $4,818,000 based on appraisal of CE > IRS disallows on valuation and lack of donative intent, with penalties 23 #RALLY2018 LAND TRUST ALLIANCE

39 Quid Pro Quo Conservation Easement > Tax Court denies deduction on summary judgment: o Agrees with IRS that LLC conveyed CE with expectation of receiving substantial benefit of increased value to residential lots located near conserved land o Finds CE had zero value because highest and best use of 125 acres was as a park o Finds enhanced value to LLC s abutting property outweighed any value of the easement o Declines to assess any penalties applying reasonable cause and good faith exception in I.R.C. 6664(c)(1) 24 #RALLY2018 LAND TRUST ALLIANCE

40 Quid Pro Quo Conservation Easement Court s reasoning blended several different federal tax concepts > Substantial benefits analysis really donative intent and quid pro quo principles > Substantial benefits analysis cursory, with facts much less damning to LLC than other cases (Pollard v. Commissioner or Costello v. Commissioner) > Muddled enhancement issue, relevant only to valuation and not to deductibility analysis > Accepted without detailed analysis that enhancement effect exceeded value of CE 25 #RALLY2018 LAND TRUST ALLIANCE

41 Quid Pro Quo Charitable Donation Land Triumph Mixed Use Investments III, LLC v. Commissioner, T.C. Memo (U.S.T.C. May 15, 2018), (UT), appeal period open > LLC owns 2,800 acres of land, seeks to develop planned community for which 10% of land must remain undeveloped open space > City approves plans allowing 3,500 residential units; amends to allow additional 3,500 units with 1,000 acres of open space to be given to City > Final agreement of 747 acres open space to City and reduction by 2000 units > State transfer is voluntary charitable donation made without consideration, City s approval of plans was in no way contingent upon transfer of property. > LLC claims $11,040,000 charitable contribution deduction for land transfer > The IRS challenges the deduction in its entirety 26 #RALLY2018 LAND TRUST ALLIANCE

42 Quid Pro Quo Charitable Donation Land Tax Court denies deduction in entirety: > Finds LLC transferred 747 acres and development credits as quid pro quo exchange for current approval of concept plan and future approval of area plan > Finds despite provisions of agreement characterizing transfers as voluntary donations, external features of transaction evidenced by back and forth negotiations between City and LLC demonstrated a clear quid pro quo arrangement > Denied in its entirety because LLC failed to place any value on consideration of approvals following Pollard v. Commissioner and Seventeen Seventy Sherman St., LLC v. Commissioner *Takeaway--taxpayer cannot paper over quid pro quo arrangement with a purported donation agreement; proof is in the pudding 27 #RALLY2018 LAND TRUST ALLIANCE

43 Proposed Fed. Regulation for State Tax Credits Outgrowth of 2017 tax law $10,000-a-year cap on deductions for state and local taxes (SALT) > Response to NY and NJ work around tax credits > Requires federal deduction reduction by amount of state tax credit, unless tax credit is 15% or less of contribution > Effective August 27, 2018 with 45 day comment period > Relies on quid pro quo > Negative impact on conservation tax credits (CO, VA) > Potential coordinated response: o o o Beyond scope of original law Tax credits are not quid pro quo Grandfather/exclude conservation tax credits 28 #RALLY2018 LAND TRUST ALLIANCE

44 Amendment Law Update No Movement in Legal Cases > Three federal tax cases where IRS challenges amendment clauses as non-perpetual Sells, et al., v. Commissioner (Alliance amicus granted), Kumar, et al., v. Commissioner, (Alliance amicus granted), Pine Mountain Preserve, LLLP v. Commissioner, (Alliance amicus denied) No Movement in Regulation > IRS Notice Request for Comments to Priority Guidance Plan for 170(h) charitable contributions of conservation easements (Alliance Position Paper and Transmittal Letter) 29 #RALLY2018 LAND TRUST ALLIANCE

45 Amendment Law Update Yes Movement on Drafting Guidance: Alliance checklist of 8 elements: 1. Perpetual CE; intent to protect conservation purposes perpetually 2. Acknowledge natural conditions, landscape, consistent uses, economic and cultural conditions and technologies change over time 3. Full disclosure nothing requires Grantor/Grantee to modify CE 4. Grantee sole discretion for all determinations 5. Incorporate all Amendment Principles 6. Conform to all Grantee policies in effect at time of amendment 7. Approval dictated by state law, and U.S. Tax Code if donated 8. Discretionary approval, waiver and consent can be encompassed 30 #RALLY2018 LAND TRUST ALLIANCE

46 Syndication To stop syndicated conservation easement deduction transactions, we need legislative relief, a fix to the current tax code rules. > 1.IRS auditors are outgunned and outnumbered, best efforts are a drop in the bucket. > 2.Litigation process takes so long, not much of a deterrence to current investors. > 3.Investors are either (a) happily buying a package that seems too good to be true, but the investors are reassured by promoters, consultants, law firms, etc; Or (b) investors know they are buying into a tax shelter but are keenly aware of points 1 and 2 above. 31 #RALLY2018 LAND TRUST ALLIANCE

47 Syndication IRS Notice (December 2017) > Requires reporting a transaction as a Listed Transaction (which requires filing a separate form with the IRS identifying what you are doing) if a transaction meets the following requirements: o Oral or written promotional material; o Investors; o Promised federal tax deduction that is at least 250% of the investor s investment; and o A contribution and resulting deduction 32 #RALLY2018 LAND TRUST ALLIANCE

48 Syndication IRS Large Business and International Division > September 2018 announcement new campaign targeting syndicated conservation easement transactions. 33 #RALLY2018 LAND TRUST ALLIANCE

49 Syndication Charitable Conservation Easement Program Integrity Act > House (H.R. 4459) and Senate (S. 2436) > Legislative language is complicated, relies on crossreferencing sections of the tax code partnership taxation provisions. > Summary: If you make an investment in a transaction, and the deduction you receive is greater than 250% of your investment, the deduction will be limited to 250% of your investment. There are exceptions to the rule, including for easement donations by family partnerships, but the rule is very carefully drafted to target syndicated conservation easement deduction tax shelters. 34 #RALLY2018 LAND TRUST ALLIANCE

50 Lessee as Donor Harbor Lofts: Vamp Building in Lynn, MA 35 #RALLY2018 LAND TRUST ALLIANCE

51 Lessee as Donor Harbor Lofts Associates v. Commissioner, 151 T.C. No. 3 (U.S.T.C. August 27, 2018) > Held: Harbor Lofts, as a long-term lessee of the two buildings, does not hold a fee interest in the property subject to the facade easement and cannot contribute a conservation easement under I.R.C. sec. 170(h). > Held, further, a lessee is not entitled to a charitable contribution deduction under I.R.C. sec. 170(h) for joining the fee owner of real property in granting a conservation easement. 36 #RALLY2018 LAND TRUST ALLIANCE

52 CE Termination Proceeds Provision Issue: In recent years, IRS began challenging CE deductions because the termination proceeds provision tweaked the Regulation language by allowing credit to the landowner for the value of improvements allowed under the CE. Land Trust Alliance letter to IRS. 37 #RALLY2018 LAND TRUST ALLIANCE

53 CE Termination Proceeds Provision PBBM Rose Hill v. Commissioner, --- F.3d - -- (5 th Cir. 2018) > CE provided that any amount attributable to improvements constructed on the Conservation Area, as well as actual bona fide expenses of the sale, should be subtracted from the total proceeds before determining the respective proportionate shares due to the Grantee and the Grantor. > Deduction denied. 38 #RALLY2018 LAND TRUST ALLIANCE

54 CE Termination Proceeds Provision PBBM Rose Hill v. Commissioner, --- F.3d --- (5 th Cir. 2018) > CE s termination proceeds provision included adjustment for any amount attributable to improvements constructed on the Conservation Area, as well as actual bona fide expenses of the sale. > Deduction denied. > The regulation does not indicate that any amount, including that attributable to improvements, may be subtracted out. 39 #RALLY2018 LAND TRUST ALLIANCE

55 CE Termination Proceeds Provision What do we do with current CE projects? > Keep improvements language out of termination provision and hope this never comes up > Continue using improvements language and be prepared to fight IRS on issue > Structure CE so improvements are excluded from deductible CE (i.e., not subject to any CE or placed in separate non-deductible CE) > See handout Proceeds Provision Examples 40 #RALLY2018 LAND TRUST ALLIANCE

56 CE Termination Proceeds Provision 41 #RALLY2018 LAND TRUST ALLIANCE

57 CE Termination Proceeds Provision Case By Case Approach > In many easements, there are no reserved rights to build value-enhancing improvements don t worry be happy. > Appreciate rarity of extreme situation where CE is completely or mostly terminated. 42 #RALLY2018 LAND TRUST ALLIANCE

58 151 T.C. No. 3 UNITED STATES TAX COURT HARBOR LOFTS ASSOCIATES, CROWNINSHIELD CORPORATION, TAX MATTERS PARTNER, Petitioner v. COMMISSIONER OF INTERNAL REVENUE, Respondent Docket No Filed August 27, E, a nonprofit development corporation, is the fee simple owner of two buildings listed on the National Register of Historic Places. H, a partnership, is a long-term lessee of those buildings. In 2009, H and E joined together in transferring a facade easement to a qualified organization under I.R.C. sec. 170(h)(3). H claimed a charitable contribution deduction of $4,457,515 for In a notice of final partnership administrative adjustment issued with respect to H, R disallowed H s claimed charitable contribution deduction for the donation of the facade easement. R also determined that an accuracy-related penalty under I.R.C. sec. 6662(a) applies. H s tax matters partner filed a petition in this Court challenging R s determinations and filed a motion for partial summary judgment under Rule 121. R filed a cross-motion for partial summary judgment on the same issue.

59 -2- R argues that H, as the long-term lessee of the two buildings, is not entitled to a charitable contribution deduction under I.R.C. sec. 170(f)(3)(B)(iii) and (h) because H did not hold a fee interest in the buildings and cannot meet the perpetuity requirements of I.R.C. sec. 170(h)(2)(C) and (5)(A) and sec A-14, Income Tax Regs. H argues that fee ownership of real property is not expressly required by I.R.C. sec. 170(h) and that the contribution is similar to a facade easement granted by tenants in common. Alternatively, H argues that it is the equitable owner of the buildings for tax purposes and therefore is eligible for deductions relating to the buildings. Held: H, as a long-term lessee of the two buildings, does not hold a fee interest in the property subject to the facade easement and cannot contribute a conservation easement under I.R.C. sec. 170(h). Held, further, a lessee is not entitled to a charitable contribution deduction under I.R.C. sec. 170(h) for joining the fee owner of real property in granting a conservation easement. Held, further, H s motion for partial summary judgment will be denied. Held, further, R s motion for partial summary judgment will be granted. Jeffrey H. Paravano, Jay R. Nanavati, and Michelle M. Hervey, for petitioners. Deborah Aloof, Bartholomew Cirenza, Shari A. Salu, and Carina J. Campobasso, for respondent.

60 -3- BUCH, Judge: This case is a partnership-level action under section 6226 and is before the Court on the parties cross-motions for partial summary judgment. 1 The issue for decision is whether Harbor Lofts Associates (Harbor Lofts) is entitled to a charitable contribution deduction of $4,457,515 for the noncash contribution of a facade easement under section 170(f)(3)(B)(iii) and (h). We hold that they are not. Harbor Lofts gave up contractual rights it held under the terms of its lease. A contract right in a long-term lease is not a qualified real property interest, and the waiver of contract rights under such lease does not give rise to a charitable contribution deduction contemplated under section 170(f)(3)(B)(iii) and (h). FINDINGS OF FACT Harbor Lofts is a Massachusetts limited partnership and the long-term lessee of the Daly Drug Building and the Vamp Building in Lynn, Massachusetts. The buildings and land are owned by the Economic Development & Industrial Corporation of Lynn (Economic Development Corp.), a Massachusetts public corporation created under chapter 778 of the Massachusetts Legislative Acts of The Economic Development Corp. took ownership of the buildings in the 1 All section references are to the Internal Revenue Code (Code) in effect for the year in issue, and all Rule references are to the Tax Court Rules of Practice and Procedure, unless otherwise indicated.

61 -4- late 1970s under an option contract assigned to it by Lynn Revitalization Corp. Harbor Lofts and the Economic Development Corp. executed a lease for the buildings in 1979 for a term of 61 years. Under the terms of the lease Harbor Lofts took on many of the rights and obligations often associated with property ownership. It is required to pay all insurance and utility costs and can use the buildings for multi-family residential uses and such uses as may be incidental there to, and for no other purpose or purposes whatsoever without the prior written consent of the Economic Development Corp. Harbor Lofts has a right of first refusal to purchase the buildings and is entitled to a portion of the proceeds if the land is taken under eminent domain. The lease requires Harbor Lofts to keep and maintain the buildings at its own expense and allows it to construct on any part or all of the Leased Premises such improvements, alterations and additions * * * as the Lessee may from time to time desire, provided that such do not materially impair the structural integrity of the buildings. Its right to alter the buildings is not unfettered. Alterations over

62 -5- $100,000 must be approved by the Economic Development Corp. although approval may not unreasonably be withheld. 2 Soon after the lease was executed, the buildings went through a historic restoration and were converted into multifamily residential apartment buildings. Harbor Lofts leases the apartments under a combination of Federal housing assistance programs and Massachusetts interest subsidy programs. Since the work was completed in the early 1980s, both buildings have been listed on the National Register of Historic Places. On December 21, 2009, Harbor Lofts and the Economic Development Corp. entered into a preservation restriction agreement with Essex National Heritage Commission, Inc. (Heritage Commission), a Massachusetts nonprofit corporation. 3 The Heritage Commission is a qualified organization under section 170(h)(3) and is chartered to preserve and promote for the benefit of the public the historic, cultural, and natural resources of the North Shore in Essex County, Massachusetts * * * which purposes include the preservation of historically important properties. Harbor Lofts (the buildings lessee) joined together with the 2 The $100,000 limit is indexed for inflation. 3 The preservation restriction agreement was recorded in Essex County, Massachusetts, on December 29, 2009.

63 -6- Economic Development Corp. (the buildings fee simple owner) to grant a facade easement to the Heritage Commission to preserve the buildings exterior. Pursuant to the facade easement Harbor Lofts and the Economic Development Corp. are responsible for all repairs and must maintain the buildings facade in the condition and appearance existing on the Effective Date of this grant as documented in photographs and written descriptions. On December 29, 2009, the same day the facade easement was recorded, Harbor Lofts and the Economic Development Corp. amended the lease by extending its term until December 31, Along with extending the term of the lease Harbor Lofts and the Economic Development Corp. revised the rent payment schedule; in conjunction with these amendments, Harbor Lofts paid $4,500,000 to the Economic Development Corp. Harbor Lofts claimed on its 2009 Form 1065, U.S. Return of Partnership Income, a $4,457,515 charitable contribution deduction under section 170 for the donation of a facade easement. Harbor Lofts claimed that its contribution to Heritage Commission was a perpetual conservation restriction under section 170(h)(2)(C) and section 1.170A-14(b)(2), Income Tax Regs. On October 25, 2016, the Commissioner issued a notice of final partnership administrative adjustment (FPAA) for 2009 to Crowninshield Corp., the tax

64 -7- matters partner of Harbor Lofts. The Commissioner disallowed Harbor Lofts charitable contribution deduction under section 170 and determined an accuracyrelated penalty of 40% for a gross valuation misstatement under section 6662(b)(3), (e), and (h); or, in the alternative, a 20% penalty under section 6662(a). No specific grounds for the 20% penalty are asserted in the FPAA. At the time of the filing of the petition Harbor Lofts had its principal place of business in Massachusetts. Harbor Lofts filed a motion for partial summary judgment on May 25, In its accompanying memorandum Harbor Lofts argues that the facade easement was jointly entered into with the Economic Development Corp. and that it satisfied the requirements of section 170(h)(2)(C). Harbor Lofts position is that the joint facade easement is similar to an easement granted by tenants in common and requires both Harbor Lofts and the Economic Development Corp. to make a joint contribution of their respective interests. Harbor Lofts further contends that it was an essential party to the facade easement because as the lessee of the buildings it possessed the right to enjoy the Property free from hindrance or molestation by any person whatsoever and if it was not bound by the facade easement it would have no obligation to maintain or preserve the historic nature of the Building facades, and the Easement s conservation purpose could not be fulfilled. Among

65 -8- other arguments Harbor Lofts also states that it has the benefits and burdens of ownership of the property and it is the equitable owner of the Property and therefore the owner for tax purposes. The Commissioner filed a response objecting to Harbor Lofts motion and filed his own motion for partial summary judgment. The Commissioner s position is that Harbor Lofts was not the fee simple owner of the buildings at the time the facade easement was entered and is therefore not entitled to a deduction under section 170(f)(3)(B)(iii). The Commissioner does not dispute that the * * * [facade easement] itself is a restriction granted in perpetuity within the meaning of I.R.C. 170(h)(2)(C), because the fee owner of the building, EDIC [the Economic Development Corp.], along with * * * [Harbor Lofts], executed the easement. But the Commissioner disagrees that Harbor Lofts was required to join in granting the facade easement because Harbor Lofts only interest was a personal property interest as lessee of the buildings. He argues that if Harbor Lofts felt its rights under the lease agreement were restricted by the facade easement it could have sought consideration from the Economic Development Corp. The Commissioner disagrees with Harbor Lofts comparison of the facade easement to an easement granted by tenants in common and likewise disagrees with Harbor Lofts proposition that it is the equitable owner of the real property

66 -9- for tax purposes. The Commissioner distinguishes cases in which a lease has been treated as a sale for tax purposes, noting that the Courts have recast a lease as a sale transaction does not imply that taxpayers can do the same to convert a leasehold interest into a real property interest within the meaning of I.R.C. 170(h)(1)(A). Harbor Lofts filed a reply to the Commissioner s response, reiterating many of the same arguments it had made in its motion for partial summary judgment. Its principal argument is that section 170(h)(2)(C) does not explicitly require that a donor of a facade easement own the real property and that multiple parties, such as tenants in common, may join together in granting a facade easement. The Commissioner filed a sur-reply focusing largely on the perpetuity requirements under section 170(h)(2)(C) and (5) and disputing Harbor Lofts comparison to tenants in common. The Commissioner s position is that Harbor Lofts, as a time-limited lessee, does not have a perpetual interest to give and that a time-limited leasehold interest cannot be equated to the fee interest of a tenant-in-common. Finally the Commissioner states that the limited duration of the interest held by a lessee is a significant fact distinguishing the deductibility of a donation made by a tenant-in-common with other similarly situated tenants-in-

67 -10- common, each of whom has a perpetual fee interest, from the non-deductibility by a lessee of a donation made by a landlord. OPINION The issue before this Court is whether Harbor Lofts satisfied the requirements of section 170(f)(3)(B)(iii). In particular, did Harbor Lofts contribute a perpetual conservation restriction as defined under section 170(h)(2)(C) and section 1.170A-14(b)(2), Income Tax Regs., that is exclusively for conservation purposes under section 170(h)(1)(C) and (5)? I. Summary Judgment Either party may move for summary judgment regarding all or any part of the legal issues in controversy. See Rule 121(a). We may grant summary judgment only if there are no genuine disputes as to any material fact. See Rule 121(b); Naftel v. Commissioner, 85 T.C. 527, 529 (1985). The moving party bears the burden of proving that no genuine dispute exists as to any material fact and that it is entitled to judgment as a matter of law. See Sundstrand Corp. v. Commissioner, 98 T.C. 518, 520 (1992), aff d, 17 F.3d 965 (7th Cir. 1994). In deciding whether to grant summary judgment, the facts and the inferences drawn from them must be considered in the light most favorable to the nonmoving party. See FPL Grp., Inc. v. Commissioner, 115 T.C. 554, 559 (2000); Bond v.

68 -11- Commissioner, 100 T.C. 32, 36 (1993); Naftel v. Commissioner, 85 T.C. at 529. When a motion for summary judgment is made and properly supported, the nonmoving party may not rest on mere allegations or denials but must set forth specific facts showing that there is a genuine dispute for trial. See Celotex Corp. v. Catrett, 477 U.S. 317, 324 (1986); Sundstrand Corp. v. Commissioner, 98 T.C. at 520; see also Rule 121(d). Both the Commissioner and Harbor Lofts filed motions for partial summary judgment. In considering each motion we construe all factual materials and draw all inferences in favor of the opposing party. II. Charitable Contribution Deduction A deduction is allowed for any charitable contribution for which payment is made within the taxable year if the contribution is verified under regulations prescribed by the Secretary. Sec. 170(a)(1). Harbor Lofts sought a charitable contribution deduction for 2009 for a noncash contribution of a facade easement under section 170(f)(3)(B)(iii) and (h)(2)(c). A. Charitable Contributions of Property A donor is generally not eligible for a charitable contribution deduction for a contribution of property consisting of less than the donor s entire interest in that property. Sec. 170(f)(3)(A). But there is an exception for a qualified conservation contribution. Sec. 170(f)(3)(B)(iii). A contribution of property is a

69 -12- qualified conservation contribution if (1) the property is a qualified real property interest, (2) the property is contributed to a qualified organization, and (3) the contribution is exclusively for conservation purposes. Sec. 170(h)(1); see also sec A-14(a), Income Tax Regs. The Commissioner concedes that all three requirements under section 170(h)(1) are satisfied by the Economic Development Corp. The only dispute is whether Harbor Lofts contributed a qualified real property interest exclusively for conservation purposes under section 170(h)(1)(A) and (C). The phrases qualified real property interest and exclusively for conservation purposes are defined by section 170(h)(2) and (5), respectively. But before we consider those definitions, we must first determine the nature of the property rights held by Harbor Lofts when the facade easement was executed. B. Massachusetts Property Law State law determines the nature of property rights contributed, whereas Federal law determines the appropriate tax treatment of those rights. See United States v. Nat l Bank of Commerce, 472 U.S. 713, 722 (1985); see also 61 York Acquisition, LLC v. Commissioner, T.C. Memo , at *8. Both parties motions assert that the Economic Development Corp. is the fee owner of the two buildings. We agree. The Economic Development Corp.

70 -13- became fee owner of the buildings having taken ownership under the option agreement in the late 1970s. But Harbor Lofts is not a fee owner. In Massachusetts a demise for a period definitely fixed or at least capable of definite ascertainment is a leasehold interest for a term of years. Farris v. Hershfield, 89 N.E.2d 636, 637 (Mass. 1950). Harbor Lofts lease agreement ends in 2056 and is therefore a leasehold interest for a term of years. Massachusetts has traditionally found a leasehold interest for a term of years to be personal property, more specifically a chattel real. Moulton v. Long, 137 N.E. 297, 298 (Mass. 1922). Harbor Lofts is not a fee owner, tenant in common, or joint tenant and has not been granted a life estate or remainder interest. Rather, Harbor Lofts leased property from the Economic Development Corp., and a commercial lease is a contract rather than a conveyance of property. 275 Washington St. Corp. v. Hudson River Int l, LLC, 987 N.E.2d 194, 203 (Mass. 2013). C. Qualified Real Property Interest Section 170(h)(2)(C) defines a qualified real property interest as a restriction (granted in perpetuity) on the use which may be made of the real property. This perpetual conservation restriction, as defined under section 1.170A-14(b)(2), Income Tax Regs., includes an easement or other interest in real

71 -14- property that under state law has attributes similar to an easement (e.g., a restrictive covenant or equitable servitude). Harbor Lofts argues that section 170(h) does not explicitly require fee ownership of real property. But Harbor Lofts, having a leasehold interest for a term of years, is incapable of granting a perpetual restriction on the use of the buildings. Harbor Lofts does not hold a fee interest and cannot grant, through the use of an easement or other State law instrument, a perpetual restriction on the buildings. Harbor Lofts does not hold perpetual property rights in the buildings, so it is not possible for it to contribute a perpetual restriction on the use of the buildings. Harbor Lofts is correct that the Code does not specifically require a donor to hold a fee interest, but only the owner of real property or holder of a fee interest is able to grant a perpetual conservation restriction. Harbor Lofts has given up something of value: the rights to make improvements, alterations, and additions to the buildings. But those rights, initially created under the contract by which Harbor Lofts leases the property, were ceded to the Economic Development Corp. Harbor Lofts gave up contractual rights under the lease agreement, which are personal property rights. And a charitable contribution of a personal property right is not a qualified real property interest under section 170(h)(2)(C).

72 -15- Harbor Lofts argues that by granting the facade easement jointly with the Economic Development Corp. that it has made a contribution under section 170(h) similar to one made by tenants in common. But Harbor Lofts at no point held a fee interest in the properties; it was not a tenant in common with the Economic Development Corp. The limited duration of a lease is far different from fee ownership as tenants in common. Harbor Lofts also argues that its interest under the lease has made them equitable owners of the property for tax purposes. But it supports its argument only with cases involving sale leaseback transactions and rulings applying economic substance and disguised-sale doctrines. These cases are not relevant here. Although Harbor Lofts took on many of the rights and obligations often associated with property ownership, its possession of these rights and obligations is of a finite duration ending on the lease s expiration. Section 170(h)(2)(C) specifically sets forth a perpetuity requirement for a facade easement. Even if we were to find that Harbor Lofts holds equitable ownership in the buildings, it is equitable ownership for only a finite period and cannot satisfy the perpetuity requirements of section 170(h)(2)(C). See, e.g., Wachter v. Commissioner, 142 T.C. 140, 149 n.3 (2014).

73 -16- D. Exclusively for Conservation Purposes and Protected in Perpetuity Section 170(h)(5) defines a contribution made exclusively for conservation purposes and states that a contribution shall not be treated as exclusively for conservation purposes unless the conservation purpose is protected in perpetuity. As a time-limited lessee Harbor Lofts is incapable of making a contribution protected in perpetuity. Harbor Lofts as lessee does not have the power to impose perpetual restrictions on property in which it does not have an absolute right. It cannot give what it does not have. At most Harbor Lofts can create a restriction that runs through the term of the lease, which is not perpetual. The Economic Development Corp. on the other hand, as fee owner of the buildings, is capable of creating an easement or other State law restriction that runs with the buildings and can therefore protect the conservation purpose in perpetuity. III. Conclusion The Commissioner is entitled to partial summary judgment disallowing Harbor Lofts 2009 charitable contribution deduction. Harbor Lofts, as the buildings long-term lessee, did not have a fee interest in the buildings and did not contribute a conservation restriction protected in perpetuity under section 170(h). Harbor Lofts gave up contractual rights under the lease agreement, which are personal property rights. Because Harbor Lofts failed to meet the requirements of

74 -17- section 170(h), the facade easement does not result in a charitable contribution deduction to Harbor Lofts under section 170(f)(3)(B)(iii). To reflect the foregoing, An appropriate order will be issued.

75 T.C. Memo UNITED STATES TAX COURT CHAMPIONS RETREAT GOLF FOUNDERS, LLC., RIVERWOOD LAND, LLC., TAX MATTERS PARTNER, Petitioner v. COMMISSIONER OF INTERNAL REVENUE, Respondent Docket No Filed September 10, Vivian D. Hoard, for petitioner. Teri L. Jackson and John P. Healy, for respondent. MEMORANDUM FINDINGS OF FACT AND OPINION PUGH, Judge: After concessions, the issue for decision is whether Champions Retreat Golf Founders, LLC (Champions Retreat), is entitled to a $10,427,435 charitable contribution deduction related to the donation of a qualified conservation contribution for the 2010 taxable year disallowed by

76 - 2 - [*2] respondent in a notice of final partnership administrative adjustment (FPAA) issued on November 19, FINDINGS OF FACT Some of the facts have been stipulated and are so found. Champions Retreat is a Georgia limited liability company with a principal place of business in Augusta, Georgia. Champions Retreat was formed on November 6, 2001, to develop and operate a golf club. As of the 2010 taxable year, Champions Retreat Golf Management, LLC, owned a % interest in Champions Retreat; Robert W. Pollard owned a % interest; Riverwood Land, LLC (Riverwood Land), owned a % interest; Kiokee Creek owned a 15% interest; William F. Paine owned a 7.718% interest; Meybohm Realty, Inc., owned a 4.114% interest; and Wayne K. Millar owned a.5172% interest. The remaining interest--approximately 16.6%--was held by 32 other partners, each of whom owned a.5172% interest. 1 Respondent conceded that Champions Retreat did not make a disguised sale to Kiokee Creek Preservation Partners, LLC (Kiokee Creek). Respondent also conceded that Champions Retreat s allocation of the charitable contribution deduction at issue had substantial economic effect. Finally, respondent conceded that Champions Retreat complied with sec. 704 in decreasing the capital accounts of the members receiving allocations of the charitable contribution deduction and in properly allocating interest income and ordinary business loss to its members. All section references are to the Internal Revenue Code in effect for the year in issue, and all Rule references are to the Tax Court Rules of Practice and Procedure, unless otherwise indicated. All monetary amounts are rounded to the nearest dollar.

77 - 3 - [*3] Riverwood Land is a limited liability company with a principal place of business in Augusta. As of the 2010 taxable year, Meybohm Realty and Mr. Pollard each owned a 40% interest and M-Golf, Inc., which is solely owned by Mr. Millar, owned the remaining 20%. I. Development of the Golf Club The easement at issue was placed on part of a 2,215-acre tract of land owned by Canal Industries before 2000 along the Savannah River in Evans, Georgia, approximately 13 miles from Augusta. Canal Industries hired Mr. Millar to develop a golf course on the property because of his relationship with golf legend Gary Player. On August 28, 2000, Pollard Land, Mr. Pollard s timberland investment firm, purchased the property from Canal Industries at the behest of Mr. Millar and E.G. Meybohm, who owns Meybohm Realty. In 2001 Riverwood Land began to develop a portion of the property and marketed it as Riverwood Plantation. On April 5, 2002, Pollard Land conveyed a acre tract to Champions Retreat to build a golf club, which became Champions Retreat Golf Club (golf club). Champions Retreat raised an initial $13.2 million for construction of the golf club by selling 66 residential lots in a development called Founders Village. A lifetime membership at the golf club and an ownership share in Champions

78 - 4 - [*4] Retreat was included in the purchase of a lot in Founders Village. In addition to the $13.2 million, Champions Retreat borrowed heavily in order to complete construction of the golf club. The golf club was completed in June The golf club is in a section of Riverwood Plantation called the Reserve. The Reserve is private and can be accessed only through a security gate, which is manned 24 hours a day. Along with the golf club and Founders Village, the Reserve includes Bishops Court, the Cottages at Riverwood Plantation (Cottages), and the Bungalows at Champions Retreat (Bungalows). Bishops Court is a residential development separate from the golf club. The Cottages and the Bungalows provide guest accommodations. The Cottages adjoin the golf course. The golf club accounts for acres of the acre tract that Champions Retreat acquired in Photos and videos in the record show it to be a visually beautiful, manicured property. It features a 27-hole course (made up of three 9-hole courses), a pro shop, a restaurant, a locker room, a cart storage facility, a driving range and practice area, and a paved parking lot. Mr. Player, Arnold Palmer, and Jack Nicklaus each designed one of the nine-hole courses. Mr. Player designed the Creek course; Mr. Palmer designed the Island course; and Mr. Nicklaus designed the Bluff course.

79 - 5 - [*5] The Creek course is the westernmost of the three courses, and it almost completely surrounds the Founders Village development. Due east of the Creek course is the driving range. The Bluff course is to the north-northeast of the driving range. The Island course is due east of the driving range. The Little River--an offshoot of the Savannah River that goes around Germain Island--runs through the Island course. Six of the nine holes on the Island course are on Germain Island. The banks of this part of the Savannah River are anywhere from 3 to 10 feet high. Sumter National Forest, which is approximately 120,000 acres, lies across the Savannah River, 700 feet from the golf club. II. Donation of the Easement Champions Retreat was not profitable. After our decision in Kiva Dunes Conservation, LLC v. Commissioner, T.C. Memo , Douglass Cates, the accountant for Champions Retreat, proposed the donation of a conservation easement on the property including the golf club. The proposal was meant, among other things, to attract additional investment in Champions Retreat so that it could pay down its debt and remaining construction costs.

80 - 6 - [*6] Lee Echols, a conservation biologist with the North American Land Trust (NALT), 2 performed an initial survey of the property on November 30 and December 1, The initial survey consisted of a tour of the property to document and photograph any significant natural features or significant species or natural communities on the property for the purpose of determining a conservation purpose. Mr. Echols determined in 2009 that the property met the requirements for a conservation easement. Kiokee Creek, a Georgia partnership, was formed on September 24, 2010, as a vehicle for investing in Champions Retreat. Its 15 original members, most of whom were Mr. Cates clients, contributed a total of $2,705,000 for their interests. In November 2010 Kiokee Creek contributed $2,700,000 to Champions Retreat in exchange for a 15% interest. Mr. Echols returned to Champions Retreat on November 12, 2010, to perform another site visit. Mr. Echols again determined that the property was suitable for a conservation easement and, on December 16, 2010, Champions Retreat conveyed an easement to NALT that covered acres (easement area). The easement was recorded on December 29, 2010, in the deeds records of 2 NALT is registered as a charitable organization in Pennsylvania and has tax-exempt status under sec. 501(c)(3).

81 - 7 - [*7] Columbia County, Georgia. NALT acknowledged Champions Retreat s donation of the easement on February 7, Mr. Echols returned to the golf club again on May 12, 2011, so that NALT could have a record of the significant natural features of the property throughout the year. This followup visit, although after the conveyance of the easement, was included in NALT s baseline documentation that Champions Retreat submitted to the Internal Revenue Service (IRS). No representative of Champions Retreat signed the owner acknowledgment line in the documentation. Champions Retreat claimed a $10,427,435 charitable contribution deduction on its Form 1065, U.S. Return of Partnership Income, for the 2010 taxable year for its donation of the easement to NALT. Champions Retreat allocated approximately 98.8% of the deduction to Kiokee Creek, the remaining 1.2% of the deduction to Riverwood Land, and none to the other 37 members. III. Terms of the Easement The easement document identifies three conservation purposes: Preservation of the [easement] area as a relatively natural habitat of fish, wildlife, or plants or similar ecosystem; and Preservation of the [easement] area as open space which provides scenic enjoyment to the general public and yields a significant public benefit; and

82 - 8 - [*8] Preservation of the [easement] area as open space which, if preserved, will advance a clearly delineated Federal, State, or local governmental conservation policy and will yield a significant public benefit * * *. The easement document imposes several restrictions on Champions Retreat. It restricts the ways that Champions Retreat can use the easement area, including the types of structures that Champions Retreat can build on the easement area. It requires Champions Retreat to use the best environmental practices then prevailing in the golfing industry in maintaining the golf club, to keep records relating to maintenance of the golf club, and to submit an annual maintenance report to NALT. In addition, Champions Retreat cannot remove surface or ground water, live or dead trees, or any other raw materials from the easement area. It cannot put up signs or outdoor advertising or construct any new roads on the easement area. It must protect the bodies of water on or near the easement area; creeks and ponds cannot be manipulated, no chemical discharge can be allowed to flow into a creek or pond, no vegetation within 100 feet of a creek or pond can be cleared, and Champions Retreat must take care not to cause soil erosion and sedimentation. The easement document prohibits the division of the easement area into lots and requires Champions Retreat to notify NALT in writing before it exercises a reserved right in a way that may impair the conservation purposes underlying the donation.

83 - 9 - [*9] The easement document allows several exceptions to those restrictions. Champions Retreat can build additional structures of up to an aggregate 10,000 square feet on the easement area and can remove trees and vegetation to do so, and it can shift around greens, fairways, and other features of the golf courses. It can pave and widen an existing road by 10 feet. Champions Retreat has the right to [m]aintain in good and manicured condition the * * * fairways, greens, tee boxes, sand traps, waste bunkers, areas in the rough, and other Golf Course play areas including any lakes, ponds, and other water courses which are an integral part of the Golf Course. This includes the right to use chemicals. It also has the right to remove any tree--whether standing or fallen--that is within 30 feet of a playable area. Champions Retreat must give NALT written notice before it exercises these or any other rights reserved to it in the easement document, and NALT must give its written approval for the exercise of the right. IV. Natural Features of the Easement Area The acre easement area includes 25 of the 27 holes in their entirety, most of the 2 remaining holes, and the driving range. It does not include the parking lot, the pro shop, the restaurant, the locker room, the cart storage facility, the Cottages, the Bungalows, or Founders Village.

84 [*10] A. Plants, Animals, and Aquatic Life on the Easement Area The easement area is in the Lower Piedmont region, which runs from Virginia to Georgia. The Lower Piedmont region tends to be characterized by three types of habitat: (1) Piedmont oak-pine-hickory forest, which is characterized by large canopy trees; (2) Piedmont pine-oak woodlands and forest, which has a more open canopy but a greater presence of subcanopy trees; and (3) Piedmont floodplains and bottomlands, which are wetland forests that occur along rivers and creeks. While efforts were made to preserve the natural beauty of the easement area--especially certain trees--trees were cut down and vegetation was removed during the construction of the golf club. Indeed, the open pine woodlands and savannas in the easement area exhibit very little plant species diversity. However, swaths of wetland, bottomland and riparian forest, and open pond habitat survived the development and remain undisturbed. The two largest undisturbed swaths are the 31 acres to the west of the Little River and the 26 acres on Germain Island. Together these account for a little over 16% of the easement area. Species observed in the easement area are monitored by conservation organizations. NatureServe is a large, umbrella conservation group that relies on reports from biologists around the world to classify natural communities and to

85 [*11] track species of conservation concern. NatureServe s ranking system for the threat level to a species also is used by each State s Natural Heritage Program, which tracks species of conservation concern on a State level. Although not all States fund this program, scientists continue to contribute observations. The NatureServe rankings are G1 through G5; the G stands for global, G1 is the highest threat level, and G5 is the lowest. The State rankings are the same except that S stands for State. Several bird-specific conservation organizations also track bird species of concern. Partners in Flight (PIF) has five threat levels, from Possibly Extinct, at the highest level, to Planning and Responsibility, at the lowest. 3 The Atlantic Coast Joint Venture (ACJV) ranks the threat to birds from Highest Priority to Moderate Priority. 4 The North American Bird Conservation Initiative (NABCI) puts birds facing the most serious threats on the Red Watch list and birds facing less serious threats on the Yellow Watch List. The U.S. Fish and Wildlife Service 3 For PIF the threat levels are, from highest to lowest, (1) Possibly Extinct, (2) Critical Recovery, (3) Immediate Management, (4) Management Attention, and (5) Planning and Responsibility. 4 For ACJV the threat levels are, from highest to lowest, (1) Highest Priority, (2) High Priority, and (3) Moderate Priority.