Cambridge sub region SHMA 2013

|

|

|

- Bernadette Henderson

- 5 years ago

- Views:

Transcription

1 Private renting Interest and relevance This chapter looks at the private rented sector and the cost of private rents for our housing subregion. It is relevant to the SHMA because it helps understand an important part of the overall housing market. Data used in this chapter feed into Chapter 10, Incomes and affordability. Issues affecting benefit claimants in the private sector, and the potential effects of these changes are summarised briefly in section Headline messages The 2011 Census shows over 53,000 households (16%) in the private rented sector across our housing sub region. The average rent in March 2012 was 709 per calendar month across the sub region (Table 3). In February 2013 there were almost 12,000 private sector benefit claimants (Table 5). Changes over time Both nationally and locally there was considerable growth in both the number and proportion of households living in the private rented sector between 2001 and A range of changes are affecting benefits for both private and social tenants, changes to social housing allocations and an emphasis on encouraging more large scale investment in the private rented sector. These factors are likely to change and possibly expand the sector further. Geographical variation In 2011 around a quarter of households in Cambridge and Forest Heath lived in private rented accommodation. In other areas of the sub region, the proportion was between 12% and 16%. The number of households in the private rented sector has increased in all areas since Most of the private rented accommodation is found Cambridge and the market towns. Compared to England as a whole and the East of England, the sub region is a relatively expensive area for rents, with Cambridge is the most expensive area in the sub region and Fenland the cheapest. Forest Heath is the third most expensive area to rent and the second cheapest to buy suggesting the USA Air Force presence in the district significantly inflates rents. Fenland has the largest estimated proportion of private rented households in receipt of benefit (nearly half). Cambridge has a very low proportion of benefit claimants living in private rented accommodation. Future monitoring points We will continue to monitor the impact of welfare reforms and other recent legislation on issues such as access to the private rented sector for lower income households. There are several different rental markets recognised nationally. Further work is required to look at these markets locally. There are currently no large scale build to let homes planned in the sub region, but some are being built elsewhere. We will continue to monitor this trend. 1

2 SHMA contents 1 Introduction and background 2 Defining our housing market area 3 Economic and demographic context 4 Housing stock 5 Property prices 6 Private renting 6.1 Introduction Facts and figures Local context Average rent per calendar month Local Housing Allowance Recent and future changes affecting the private rented sector Analysis Background information Links and references Definition of terms Data issues VOA rent data, published Sept Local Housing Allowance Rates Social renting 8 Intermediate housing 9 Homelessness 10 Current incomes and affordability 11 Plans and land availability 12 Forecasts for homes of all tenures 13 Affordable housing need 14 Sizes, types and tenures 15 Specific housing needs Please visit current version to read other SHMA 2013 chapters 2

3 Section 6.1 Introduction 6 Private renting 6.1 Introduction The private rented sector is an important part of the overall housing market in the sub region. Factors such as affordability of purchase and the national policy environment mean private renting is likely to continue growing in the coming years. A more detailed focus on these changes and an improved understanding of different markets within the sub regional private rented sector is required. Understanding the rental market is one of the key outputs of our SHMA. Rents provide an indication of the costs of consuming housing in a market area and long term changes may indicate an imbalance in demand for and supply of housing (2013 draft Assessment Guidance). This chapter includes o o o Updated findings about households in the private rental market based on 2011 Census results. Analysis of the number of households in the sector and how many are claiming housing benefit. Average and entry level rents per calendar month (PCM) and trends to support the affordability and affordable need calculations. Rental costs are used in the calculation of affordability in Chapter 10 Incomes and affordability, and through this in the calculation of affordable need. The relevant tables used are highlighted in pale yellow. Data about rental costs are taken from Hometrack and the Valuation Office Agency (VOA). The 2013 Estate and Letting Agents Survey which informs this chapter are available at Housing stock condition is dealt with in Chapter 4 Dwelling Profile. 3

Section 6.")

and")

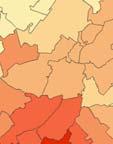

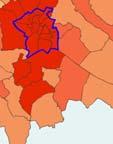

4 6.2 Facts and figures Local context Cambridge sub region SHMA 2013 Chapter 6 Private rentingg (updates using 2010/11 and 2011/12 data) Section 6.2 Facts and figures The private rented sector has grown substantially in the past decade. Table T 1 shows the change in the number of households renting privately between 2001 and Table 1 Cambridge East Cambridgeshire Fenland Huntingdonshire South Cambridgeshire Forest Heath St Edmundsbury Cambridge sub region Households in the private rented sector, 2001 to 2011 Private rented 2001 Private rentedd 2011 Source: Censuss 2001 (Table UV63) and Census 2011 (QS405EW) number 8,777 2,684 3,001 5,804 4,247 3,681 3,805 31,9999 % 21% 9% % 9% % 9% % 8% % 16% 9% % 11% Number 12,258 4,576 6,341 9,770 7,174 6,195 6,798 53,112 % 26% 13% 16% 14% 12% 24% 15% 16% Change 3,481 1,892 3,340 3,966 2,927 2,514 2,993 21,113 Difference 40% 70% 111% 68% 69% 68% 79% 66% Between 2001 and 2011 the number of households in the private rented sector in the sub region increased from 31,999 to 53,112. In Fenland the number of households in the private rented sector has more m than doubled. Cambridge (which has the highest number and proportionn of private tenants) has the t smallestt percentagee increase in households renting privately but still the second largest numerical increase after Huntingdonshire. Map 1 % households in the private rented sector (private landlord / agency) Cambridge sub region 2011 Source: Censuss 2011 via Hometrack 4

5 Section 6.2 Facts and figures Map 1 shows the percentage of households renting privately being concentrated around Cambridge and the market towns in each district. Table 2 shows how the wider Census category breaks down: Table 2 The private rented sector, 2011 Landlord/ letting agent Employer Relative/ friend Other Total (=100%) Private rented sector as % of total housing market Cambridge 91% 2% 3% 3% 12,258 26% East Cambridgeshire 91% 2% 6% 1% 4,576 13% Fenland 91% 1% 7% 1% 6,341 16% Huntingdonshire 88% 3% 6% 2% 9,770 14% South Cambridgeshire 87% 5% 5% 3% 7,174 12% Forest Heath 89% 4% 4% 2% 6,195 24% St Edmundsbury 87% 5% 6% 3% 6,798 15% Cambridge subregion Census, % 3% 5% 3% 53,112 16% Table 2 shows the proportion of private tenants renting from different landlords. About 89% of private tenant households in the sub region rent from a private landlord, either directly or through a letting agent. Fenland has the largest percentage of households renting from a family member or friend. More detailed tenure cross tabulations from the Census showing each tenure by age and household structure will be made available later in Other sources currently available suggest nationally: There are several different markets in the private rented sector: students, recent migrants, families, Generation Rent (locked out of ownership), people awaiting access to social housing, young professionals, housing benefit market, slum rentals, tied housing, high income high rent, transitional renters, temporary accommodation and regulated tenants (Rugg & Rhodes, 2008). A more recent paper by the Building and Social Housing Foundation (BSHF) identifies six sub sectors: higher income working age households, lower income working age households, students, older people, economically inactive households claiming housing benefit and economically active households claiming benefit. Higher income working age households are currently the largest group (46% of the market) and older people are the smallest (5%) (Pearce, 2013). Younger households (16 34) are over represented in the private rented sector and older people (over 55) are under represented (BSHF). Tenure trend projections by the Joseph Rowntree Foundation suggest around 34% of year olds will be housed in the private rented sector in 2020 (Clapham et al, 2012). Households in the private rented sector move more frequently than households in other tenures (English Housing Survey 2013) supported by local new development surveys and letting agents surveys. More than 60% of private rented households consist of 1 or 2 adults and no children, although the proportion of households in the sector with children is increasing (Pearce, 2013). 5

6 Section 6.2 Facts and figures Most (59%) private tenants expect to own. The number who expect to do so within the next two years has decreased from 34% in 2006/7 to 22% in 2011/12 (English Housing Survey 2013). The English Housing Survey also shows nationally private rented stock tends to have higher levels of non decency; to be less warm and more damp than owner occupied homes and homes in the social rented sector. Please see Chapter 4 Dwelling profile for links to local stock condition surveys Average rent per calendar month Table 3 shows the average rent per calendar month by district in March Table 3 Average rent PCM by number of bedrooms, Cambridge sub region, March 2012 Room Studio 1 bed 2 beds 3 beds 4 beds All Cambridge ,024 1, East Cambridgeshire No data No data , Fenland 282 No data Huntingdonshire , South Cambridgeshire , Forest Heath , St Edmundsbury , Cambridge sub region , Source: Valuation Office Agency Table 3 is used in Chapter 10 Incomes and affordability. As with prices for purchase, Cambridge is the most expensive area and Fenland is the cheapest. Forest Heath is the second cheapest area for purchase, but the third most expensive overall for rent. Table 4 shows the lower quartile (entry level) rent PCM by number of bedrooms for each district. Table 4 Lower quartile rent PCM by number of bedrooms, March 2012 Room Studio 1 bed 2 beds 3 beds 4 beds All Cambridge , East Cambridgeshire Fenland Huntingdonshire South Cambridgeshire Forest Heath St Edmundsbury Source: Valuation Office Agency Table 4 shows that Cambridge is the most expensive area and Fenland is the cheapest. The lower quartile rents for studios, 1 bed, 2 beds and 3 beds Cambridge are all more expensive than the average rent in all other districts. 6

7 Chapter 6 Private rentingg (updates using 2010/11 and 2011/12 data) Section 6.2 Facts and figures Fig 1 shows the average rent per calendar month for all properties by district. d Fig 1 Average rent PCM (all properties), Jun 2011 to Mar 2013, Cambridge sub regionn Source: Valuation Office Agency A more detailed breakdown of average rents by district and size is shown in Section In most areas rents increased between June 2011 and June In thee sub region as a whole, rents declined slightly between June 2012 and Marchh 2013 when they returned to a similar level as June In Huntingdonshire rents in March 2013 were slightly lower on average than in Junee As around 17% of the properties included in the dataset are in Huntingdonshire, this also skews the sub region downwards especially for rooms and four bedroom homes. Cambridgee saw the largest increase in rents. 7

")

Source:")

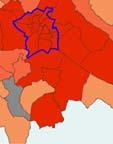

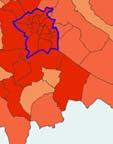

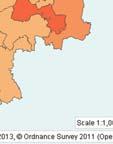

8 Chapter 6 Private rentingg (updates using 2010/11 and 2011/12 data) Section 6.2 Facts and figures Fig 2 shows a mix adjusted index of rents from June 2011 for the sub region districts, sub region, East of England and England. Fig 2 Mix adjusted rent index (based on Jun 2011 rents) Source: Valuation Office Agency Rents in the sub region as a whole have increased more sharply than across the whole country and across the region. Rents in Cambridge have increased especially fast. Rents in Fenland, East Cambridgeshire, Forest Heath and St Edmundsbury all increased by more than 5% between June 2011 and Marchh Hometrack provides data on private rent levels, but there is currently no n time series for this data and it is only collected for 1 to 3 bedroom homes. The median rent per week for 1, 2 and 3 bed properties is shown in Mapp 2, at ward level: 8

9 Chapter 6 Private rentingg (updates using 2010/11 and 2011/12 data) Section 6.2 Facts and figures Map 2 Median rent per week (1, 2 and 3 bedroom properties), May 2012 April 2013 Source: Hometrack, downloadedd June 2013 Grey shading denotes wards with insufficient data to be judged robust. 9

10 Section 6.2 Facts and figures The median rent across Cambridge is greater than 186 per week; or 806 per calendar month. The wards in South Cambridgeshire which are closest to Cambridge are also expensive. Forest Heath is the third most expensive districts, but the north east of the district (around Brandon and Thetford) is comparatively cheap and the more expensive parts of the district are around the USAAF bases (RAF Mildenhall and RAF Lakenheath). There is a split in Huntingdonshire with the more expensive wards in the South of the district along the A14 with wards in the north tending to be cheaper and closer in price to Fenland Local Housing Allowance Table 5 shows the proportion of households in the private rented sector in receipt of Local Housing Allowance (LHA) (see for definition). The broad rental market areas used to set the rent levels for this type of benefit are shown in Chapter 2 Defining our market area. Table 5 Private rented sector households and Local Housing Allowance Private tenants receiving LHA (Feb 2013) Private rented sector households (April 2011) Estimated percentage of LHA recipients Cambridge 1,278 12,258 10% East Cambridgeshire 1,112 4,576 24% Fenland 3,066 6,341 48% Huntingdonshire 2,340 9,770 24% South Cambridgeshire 1,176 7,174 16% Forest Heath 1,320 6,195 21% St Edmundsbury 1,675 6,798 25% Cambridge sub region 11,967 53,112 24% Source: DWP, Census, HSSA Table 5 shows that there are almost 12,000 households in the sub region as a whole, or about 24% of the estimated private rented sector households in receipt of Local Housing Allowance. Fenland has the highest estimated proportion of private tenants in receipt of benefits at 48%. Cambridge has the lowest at 10% Recent and future changes affecting the private rented sector A range of changes to the benefit system have been made since Some of these affecting Local Housing Allowance include Capping the maximum amount of LHA paid to households. The level of cap will mostly affect households in London, and even in higher rent areas like Cambridge this change will have minimal impacts. Overall benefit caps and Universal Credit will have more of an impact when they are introduced from October 2013 onwards. Calculating the LHA based on the 30 th percentile level private rent rather than the median. Between 2013 and 2016 benefits including housing benefit will be uprated at 1%, i.e. below inflation. Increasing the age bracket for the single accommodation rate from years old to years old, meaning single people in this age group are only entitled to the rate covering a room in a shared house rather than a self contained 1 bedroom home. This may lead to an increase in the number of Home in Multiple Occupation (see Chapter 4 Dwelling profile, Table 5 for further details on HMOs). 10

11 Section 6.2 Facts and figures The under occupation penalty for people in social rented housing. While this only affects social tenants, because of there being too few smaller properties in the social rented sector for people to downsize to, some households may move into the private rented sector. The 2011 Localism Act included a range of changes to housing. Mostly these affect social rented housing, but are likely to have an impact on the private rented sector. These include The introduction of affordable rents which are set at levels up to 80% of the market rent. This means there is a requirement for a greater awareness of market rent levels and a much closer relationship between private rent levels in an area, the viability of new housing where affordable rents are set, and the likely conversion of existing affordable rented homes over to the new affordable rent regime. The introduction of the option of using flexible and fixed term tenures of around 5 years for social tenants (or a minimum of 2 years in special circumstances). This may lead to an increase in demand for private rented properties in the long term for people leaving social rented accommodation at the end of the tenancy. Local authorities are able to discharge their homelessness duty by placing a homeless household in private rented accommodation, without the consent of the household. Although this is an added flexibility in finding accommodation for homeless households, in areas of high housing pressure and a shortage of available rented accommodation, this may not be practical as other types of renters may be more attractive to landlords. The 2012 Montague Review looked at barriers to institutional investment in the private rented sector. On the supply side, ARLA identifies most landlords as small scale investors who own fewer than 5 properties each. Only 1% own more than 10 properties. Different types of potential investors want different levels of involvement in the process of developing new homes for private rent. Novelty and a lack of experience was also seen as a problem there are some examples of build to rent schemes, but they are still quite rare. Yields were a key concern. Historical rent yields of around 3.5% are too low without a boost from capital appreciation through sale at some point. Changing to building just to rent would require higher rents and/or lower land, construction and management costs to make yields more attractive. Problems around the planning system not distinguishing between private rent and owner occupation were also seen as a barrier. The value of the market for owner occupied properties drives the price of sites for building to rent. Montague s recommendations included Making use of existing flexibilities in the planning system to plan for and enable the development of privately rented homes where they meet local needs. Release public land for development. Look at some of the schemes currently being developed to establish a body of best practice and benchmarking and to work with the HCA to establish a task force of officials and private sector specialists to overcome barriers of unfamiliarity around these schemes. Developing standards to make good quality private rent an attractive long term tenure. 11

12 Section 6.3 Analysis 6.3 Analysis Current Situation The average private market rent in the sub region as a whole in March 2012 was 709 per calendar month. Cambridge is the most expensive area and Fenland is the cheapest. Around 16% of households in the sub region lived in the private rented homes in The private rental market is mostly concentrated around Cambridge, the USAAF bases in Forest Heath and in the market towns. Households in the private rented sector are mostly young, move more frequently than households in other tenures and include fewer household members. In February 2013, an estimated 24% of households in the private rented sector in the sub region were in receipt of Local Housing Allowance. Changes over time Both nationally and locally, the proportion of households in the private rented sector increased between 2001 and 2011, as shown in Table 1. High costs of purchasing a home in the sub region and high levels of unmet demand for social rented accommodation are important factors driving this. The Rugg Review (2008) and Montague Review (2012) both recognise the sector as playing an increasingly important need in meeting demand. Between June 2011 and 2012, rents in the sub region increased by 2% which is consistent with the national trend. Between 2012 and 2013 overall average rents decreased slightly, but there is considerable variation by property size and district. Between June 2011 and March 2013 rents in the sub region increased more rapidly than they did both nationally and regionally. Recent guidance on assessing housing need suggests longer term mix adjusted rents changes may indicate an imbalance between supply and demand (CLG 2013). There is currently only 18 months of data available for this indicator at a local i.e. district level. We will continue to monitor this trend as more data is released. Ongoing changes to the benefit system and the way social housing is allocated are likely to increase demand on the private rented sector, especially at the lower cost end of the market. There are currently no substantial build to let schemes planned for development in the subregion (a quarter of the 1 billion funds allocated for Build to Rent so far were allocated to projects based in London. A further round of bidding for Build to Rent was announced in September 2013), but this may change if recommendations from the Montague Review are taken on nationally and we will continue to monitor this situation. Further work is also required to look at some of the schemes currently happening in other parts of the country. Proposed changes to Local Housing Allowance and Housing Benefit are likely to have a considerable impact on households affected (click here to see the LHA Changes Atlas ) The reduction of LHA from the figure based on the median rent within a Broad Rental Market Area to the 30 th percentile rent means pricing some claimant households out of some areas. For example, there are very few properties available for less than the BRMA 30 th percentile rent in Cambridge, meaning claimants either have a larger shortfall to cover living in the city, or need to look further afield than may be feasible for employment opportunities. 12

13 Section 6.3 Analysis Between 2013 and 2016 the LHA rates will be uprated at 1% per year. Nationally rents are rising at 2%/year further reducing the areas where the LHA rate covers average rent in full. Typically these more affordable areas are in some of the rural areas where there are fewer properties available. Increasing the age boundary for the shared accommodation rate is likely to increase the demand for rooms for rent. A quick glance of sites such as FlatmateWorld and EasyRoommate show very few people willing to let rooms to single people in receipt of benefits. However, some landlords may choose to convert difficult to let larger properties into rooms to let. Two changes to households claiming housing benefit in the social rented sector are also likely to have an impact. Firstly, increasing deductions for non dependent household members may create additional demand for private rented accommodation from these non dependents. Secondly, reducing payments based on the bedroom standard for working age households and limited availability of 1 bed homes in the social rented sector may mean some of these households looking for alternative accommodation in the private rented sector. An increase in the size of deposit required for both market and shared ownership means there is likely to be significant demand for private rented accommodation from low to middle income households (see Chapter 10). For many private landlords, these households are a more attractive tenant type than households with very low incomes who are dependent on benefits. Decreasing access to the private rented sector for lower income households is likely to increase rent levels and increase demand for affordable housing in the Cambridge sub region. Geographical variation Cambridge is the most expensive area for private rents and Fenland is the cheapest. Cambridge, South Cambridgeshire and the two Suffolk districts are all more expensive overall than the national average rent PCM from the English Housing Survey 2009/10. Forest Heath is the second cheapest place to buy, but the third most expensive for renting, largely due to the influence of the USAAF. The travel to work area for Mildenhall covers parts of East Cambridgeshire and St Edmundsbury, suggesting some influence on these areas too. This is an attractive market because of housing allowances for USAAF personnel and there is at least one letting agent in the district dealing exclusively with this group. Some properties are advertised as having space/ fittings for US appliances. Overall rents in Huntingdonshire decreased between 2012 and This is mostly due to a decrease in the rent for four bedroom properties. There are more households in the private rented sector in urban areas and proportionately fewer in more rural areas. What does all this data, combined, tell us? The number of households in the private rented sector increased significantly between 2001 and 2011, both locally and nationally. Factors such as changes to the benefit systems, allocations of affordable housing and continued unaffordability of purchase are likely to mean this trend continues. 13

14 Section 6.3 Analysis The percentage of privately renting households in receipt of housing benefit also varies between districts. It is low in Cambridge, which is expensive compared to the LHA rate for the area and high in Fenland, the cheapest area of the sub region. Changes to the benefit regime are likely to lead to smaller concentrations of areas affordable for households in receipt of LHA. It may also increase demand for affordable housing. Further work is required to better understand the different sub sets of the rental market in the sub region and look at the local potential for institutional investment in the private rented sector. 14

15 Section 6.4 Background information 6.4 Background information Links and references Correct at November 2013 ARLA surveys accessed at CIH (July 2010) Briefing Paper on the impact of changes to Housing Benefit and Local Housing Allowance in the Budget accessed at July 2010.htm CLG (2013) Assessment of housing and economic development needs accessed at of housing and economic development needs CLG (2013) English Housing Survey accessed at forcommunities and local government/series/english housing survey CLG (2011) Planning Policy Statement 3: Planning for Housing. Technical change to Annex B Affordable Housing Definition: Consultation accessed at Cambridgeshire County Council Research Group New Development Surveys are available at development surveys Cambridgeshire County Council Research Group LHA changes atlas accessed at maps/localhousingallowance Clapham D et al (2012) Housing Options and Solutions for Young People in 2020, Joseph Rowntree Foundation access at options solutions young people HCA Build to Rent web pages at rented sector Local Housing Allowance website accessed at direct.voa.gov.uk/search.aspx Pearce, J (2013) Who lives in the Private Rented Sector? Building and Social Housing Foundation accessed at information/publication.cfm?lang=00&thepubid=19f007b2 15C5 F4C C156D907F7 Montague, A (2012) Review of the barriers to institutional investment in private rented homes, CLG accessed at to institutional investment in private rented homes review ONS Results from 2001 and 2011 Census accessed at Rugg J and Rhodes D (2008) The Private Rented Sector: its contribution and potential, Centre for Housing Policy, University of York accessed at VOA Rents Data is published at Estate and Letting Agents Survey 2013 accessed at 15

16 6.4.2 Definition of terms Cambridge sub region SHMA 2013 Section 6.4 Background information Term used Abbreviation Meaning, source or link to relevant website Broad Rental Market Area Local Housing Allowance Mix adjusted rental index Private rent/ other Census category Private rented sector Per calendar month BRMA LHA N/A PCM Broad Rental Market Areas Areas used by the Valuation Office to set local housing allowance (LHA) levels. These boundaries are not contiguous with local authority boundaries. Some BRMAs are very large (e.g. Cambridge) and cover several different markets with different prices. direct.voa.gov.uk/search.aspx Method of calculating Housing benefit for households in the private rented sector. Previously calculated by continuous collection of data about rents within a Broad Rental Market Area. In June 2010, the coalition government announced plans to stop the data collection and uprate the amount. From 2012 to 2016 the rate will be uprated by 1%. Nationally, rents are increasing by between 2 and 3%. Adjusted rental data to allow for different types of properties rented in each period. The overall average rent can change depending on the balance of the stock let, for example an increase in the proportion of 4 bedroom properties let can make it appear as if the overall average rent has increased. The mix adjusted rent shows the true change in rents over time by assuming the balance of stock rented is consistent. The Census category is private rented/ other and includes households living rent free. Around 20% of the private rented sector are in this category, which will have included some benefit claimants whose housing benefit at the time was paid directly to their landlord. In Forest Heath it includes USAF personnel living in base accommodation. But some of these will also have described themselves as renting from employer. Some housing association tenants may also have been counted as living in the private rented sector because of confusion about what a housing association is. All households in the 2001 Census category Private rent/other Where rent is given as a weekly amount, multiply by 52/12 to calculate the per calendar month amount. 16

17 Section 6.4 Background information Data issues Main sources of data VOA, Hometrack and the 2011 Census. Recent changes to data VOA started to publish data in Sep Hometrack has recently started to display rent data on median rent levels, 30% percentile, 80% of median market rents, and upper quartile rents for 1, 2 and 3 bedroom homes. This is available to district level. Planned changes to data More detailed tenure cross tabulations from Census 2011 showing each tenure by age and household structure will be released late in

18 Section 6.4 Background information VOA rent data, published Sept 2011 Fig 3 Average private rent PCM by property size and district, Jun 2011 to Mar ,800 Cambridge 1,400 East Cambridgeshire 1,600 1,200 1,400 1,200 1,000 1, Jun-11 Sep-11 Dec-11 Mar-12 Jun-12 Sep-12 Dec-12 Mar-13 0 Jun-11 Sep-11 Dec-11 Mar-12 Jun-12 Sep-12 Dec-12 Mar Fenland 1,200 Huntingdonshire , Jun-11 Sep-11 Dec-11 Mar-12 Jun-12 Sep-12 Dec-12 Mar Jun-11 Sep-11 Dec-11 Mar-12 Jun-12 Sep-12 Dec-12 Mar-13 1,400 South Cambridgeshire 1,400 Forest Heath 1,200 1,200 1,000 1, Jun-11 Sep-11 Dec-11 Mar-12 Jun-12 Sep-12 Dec-12 Mar Jun-11 Sep-11 Dec-11 Mar-12 Jun-12 Sep-12 Dec-12 Mar-13 1,400 St Edmundsbury 1,400 Sub-Region 1,200 1,200 1,000 1, Jun-11 Sep-11 Dec-11 Mar-12 Jun-12 Sep-12 Dec-12 Mar-13 0 Jun-11 Sep-11 Dec-11 Mar-12 Jun-12 Sep-12 Dec-12 Mar-13 Source: Valuation Office Agency 18

19 6.4.5 Local Housing Allowance Rates Cambridge sub region SHMA 2013 Section 6.4 Background information The following tables show the LHA rates for the 5 main Broad Rental Market Areas covering the subregion, as at Mar 2012 Table 6 LHAs per week, by BRMA BRMA 1 bed 2 bed 3 bed Bury St Edmunds Cambridge Huntingdon King's Lynn Peterborough Source: direct.voa.gov.uk/search.aspx (downloaded May 2013) Table 7 LHAs per calendar month by BRMA BRMA 1 bed 2 bed 3 bed Bury St Edmunds Cambridge Huntingdon King's Lynn Peterborough Source: direct.voa.gov.uk/search.aspx (downloaded May 2013) For more detail on BRMAs boundaries please see 19

Current affordability and income

Current affordability and income 21.1 Introduction...1 21.2 The relationship between intermediate and private rented markets...2 21.3 Renting privately...3 Table 1: Lower quartile rent, required household

Current affordability and income 21.1 Introduction...1 21.2 The relationship between intermediate and private rented markets...2 21.3 Renting privately...3 Table 1: Lower quartile rent, required household

Sales of intermediate housing

Sales of intermediate housing - 2009 Summary of issues...1 20.1 Introduction... 2 20.2 Intermediate Housing who has been housed... 2 Table 1: Shared ownership and OMHomeBuy sales, 2007/08...3 Fig 1: Total

Sales of intermediate housing - 2009 Summary of issues...1 20.1 Introduction... 2 20.2 Intermediate Housing who has been housed... 2 Table 1: Shared ownership and OMHomeBuy sales, 2007/08...3 Fig 1: Total

The buy-to-let market

The buy-to-let market 16.1 Introduction...1 Fig 1: Buy-to-let & first time buyer mortgages, UK 2000-2006...1 16.2 Buy-to-let investors...2 Table 1: Number of buy-to-let sales, Cambridge sub-region (estimates),

The buy-to-let market 16.1 Introduction...1 Fig 1: Buy-to-let & first time buyer mortgages, UK 2000-2006...1 16.2 Buy-to-let investors...2 Table 1: Number of buy-to-let sales, Cambridge sub-region (estimates),

State of the Housing Market in Bristol 2013

State of the Housing Market in Bristol 2013 Housing Stock Bristol has 190,000 homes, and plans to increase this by around 13,000 by 2026. Currently 15% of stock is owned by the city council, 6% by housing

State of the Housing Market in Bristol 2013 Housing Stock Bristol has 190,000 homes, and plans to increase this by around 13,000 by 2026. Currently 15% of stock is owned by the city council, 6% by housing

Housing market bulletin

Edition 37 Published: June 2018 Data: April 2018 Our housing market Welcome to our latest housing market bulletin, helping you keep track of local, regional and national housing market signals at April

Edition 37 Published: June 2018 Data: April 2018 Our housing market Welcome to our latest housing market bulletin, helping you keep track of local, regional and national housing market signals at April

BOURNEMOUTH/ POOLE HOUSING MARKET AREA

BOURNEMOUTH/ POOLE HOUSING MARKET AREA 2011 Strategic Housing Market Assessment Update Summary report for: Borough of Poole Council January 2012 in association with Cont ents Contents 1. Background...1

BOURNEMOUTH/ POOLE HOUSING MARKET AREA 2011 Strategic Housing Market Assessment Update Summary report for: Borough of Poole Council January 2012 in association with Cont ents Contents 1. Background...1

Rent setting Policy. Contents. Summary:

Rent setting Policy Summary: This policy sets out Genesis Housing Association s approach to rent setting and rent increases and decreases for all properties. The policy sets out how we will calculate and

Rent setting Policy Summary: This policy sets out Genesis Housing Association s approach to rent setting and rent increases and decreases for all properties. The policy sets out how we will calculate and

X. Xx. Evaluating requirements for market and affordable housing

X. Xx Evaluating requirements for market and affordable housing Evaluating requirements for market and affordable housing Professor Steve Wilcox Centre for Housing Policy University of York Professor Glen

X. Xx Evaluating requirements for market and affordable housing Evaluating requirements for market and affordable housing Professor Steve Wilcox Centre for Housing Policy University of York Professor Glen

POLICY BRIEFING. ! Housing and Poverty - the role of landlords JRF research report

Housing and Poverty - the role of landlords JRF research report Sheila Camp, LGIU Associate 27 October 2015 Summary The Joseph Rowntree Foundation (JRF) published a report in June 2015 "Housing and Poverty",

Housing and Poverty - the role of landlords JRF research report Sheila Camp, LGIU Associate 27 October 2015 Summary The Joseph Rowntree Foundation (JRF) published a report in June 2015 "Housing and Poverty",

Earls Barton. Rural Housing Survey. Authors: A Miles & S Butterworth Date: October 2012

Earls Barton Rural Housing Survey Authors: A Miles & S Butterworth Date: October 2012 Swanspool House, Doddington Road, Wellingborough, Northamptonshire, NN8 1BP Tel: 01933 229777 DX 12865 www.wellingborough.gov.uk

Earls Barton Rural Housing Survey Authors: A Miles & S Butterworth Date: October 2012 Swanspool House, Doddington Road, Wellingborough, Northamptonshire, NN8 1BP Tel: 01933 229777 DX 12865 www.wellingborough.gov.uk

Managing the impact of housing reforms in your area: Working towards the tenancy strategy

Managing the impact of housing reforms in your area: Working towards the tenancy strategy June 2011 Gill Leng With contributions from: Abigail Davies Lesley Healey Sue Beecroft Niki Hollingworth Cambridgeshire

Managing the impact of housing reforms in your area: Working towards the tenancy strategy June 2011 Gill Leng With contributions from: Abigail Davies Lesley Healey Sue Beecroft Niki Hollingworth Cambridgeshire

Housing Need in South Worcestershire. Malvern Hills District Council, Wychavon District Council and Worcester City Council. Final Report.

Housing Need in South Worcestershire Malvern Hills District Council, Wychavon District Council and Worcester City Council Final Report Main Contact: Michael Bullock Email: michael.bullock@arc4.co.uk Telephone:

Housing Need in South Worcestershire Malvern Hills District Council, Wychavon District Council and Worcester City Council Final Report Main Contact: Michael Bullock Email: michael.bullock@arc4.co.uk Telephone:

Data Note 1/2018 Private sector rents in UK cities: analysis of Zoopla rental listings data

Data Note 1/2018 Private sector rents in UK cities: analysis of Zoopla rental listings data Mark Livingston, Nick Bailey and Christina Boididou UBDC April 2018 Introduction The private rental sector (PRS)

Data Note 1/2018 Private sector rents in UK cities: analysis of Zoopla rental listings data Mark Livingston, Nick Bailey and Christina Boididou UBDC April 2018 Introduction The private rental sector (PRS)

The introduction of the LHA cap to the social rented sector: impact on young people in Scotland

The introduction of the LHA cap to the social rented sector: impact on young people in Scotland Brought to you by the Chartered Institute of Housing Executive Summary About the research This research was

The introduction of the LHA cap to the social rented sector: impact on young people in Scotland Brought to you by the Chartered Institute of Housing Executive Summary About the research This research was

Housing Needs Survey Report. Arlesey

Housing Needs Survey Report Arlesey August 2015 Completed by Bedfordshire Rural Communities Charity This report is the joint property of Central Bedfordshire Council and Arlesey Parish Council. For further

Housing Needs Survey Report Arlesey August 2015 Completed by Bedfordshire Rural Communities Charity This report is the joint property of Central Bedfordshire Council and Arlesey Parish Council. For further

HOUSING AFFORDABILITY

HOUSING AFFORDABILITY (RENTAL) 2016 A study for the Perth metropolitan area Research and analysis conducted by: In association with industry experts: And supported by: Contents 1. Introduction...3 2. Executive

HOUSING AFFORDABILITY (RENTAL) 2016 A study for the Perth metropolitan area Research and analysis conducted by: In association with industry experts: And supported by: Contents 1. Introduction...3 2. Executive

Scottish Parliament Social Security Committee Social Security Support for Housing Written Submission from ARLA Propertymark March 2019

Scottish Parliament Social Security Committee Social Security Support for Housing Written Submission from ARLA Propertymark March 2019 Background 1. ARLA Propertymark is the UK s foremost professional

Scottish Parliament Social Security Committee Social Security Support for Housing Written Submission from ARLA Propertymark March 2019 Background 1. ARLA Propertymark is the UK s foremost professional

Frequently Asked Questions: The Social Housing Rent Settlement from 2015

Updated 15 November 2013 Frequently Asked Questions: The Social Housing Rent Settlement from 2015 1. Introduction Following the 2013 Spending Round announcement on the social housing rent settlement from

Updated 15 November 2013 Frequently Asked Questions: The Social Housing Rent Settlement from 2015 1. Introduction Following the 2013 Spending Round announcement on the social housing rent settlement from

APPENDIX A DRAFT. Under-occupation Policy

APPENDIX A DRAFT Under-occupation Policy Published: August 2013 1 1 EXECUTIVE SUMMARY 1.1 The introduction of the Welfare Reform Act 2012 has led to cuts in the amount of housing benefit people receive

APPENDIX A DRAFT Under-occupation Policy Published: August 2013 1 1 EXECUTIVE SUMMARY 1.1 The introduction of the Welfare Reform Act 2012 has led to cuts in the amount of housing benefit people receive

Rent and Service Charge Policy

Rent and Service Charge Policy Approval date: February 2018 Review date: February 2020 Page 1 of 8 Contents Contents... 2 Statement of intent... 3 Scope... 3 Social rents for existing tenants... 3 Non-collection

Rent and Service Charge Policy Approval date: February 2018 Review date: February 2020 Page 1 of 8 Contents Contents... 2 Statement of intent... 3 Scope... 3 Social rents for existing tenants... 3 Non-collection

Member briefing: The Social Housing Rent Settlement from 2015/16

28 May 2014 Member briefing: The Social Housing Rent Settlement from 2015/16 1. Introduction On Friday 23 May Government issued the final policy for Rents for Social Housing from 2015/16, following a consultation

28 May 2014 Member briefing: The Social Housing Rent Settlement from 2015/16 1. Introduction On Friday 23 May Government issued the final policy for Rents for Social Housing from 2015/16, following a consultation

Thames Gateway South Essex

Thames Gateway South Essex Housing Market Trends Quarterly Report April 2015 House Prices, Affordability & Market Indicators www.tgessex.co.uk Housing Market Trends Quarterly Report April 2015 Introduction

Thames Gateway South Essex Housing Market Trends Quarterly Report April 2015 House Prices, Affordability & Market Indicators www.tgessex.co.uk Housing Market Trends Quarterly Report April 2015 Introduction

West Surrey Strategic Housing Market Assessment

West Surrey Strategic Housing Market Assessment Guildford Summary Report October 2015 Prepared by GL Hearn Limited 280 High Holborn London WC1V 7EE T +44 (0)20 7851 4900 glhearn.com Contents Section Page

West Surrey Strategic Housing Market Assessment Guildford Summary Report October 2015 Prepared by GL Hearn Limited 280 High Holborn London WC1V 7EE T +44 (0)20 7851 4900 glhearn.com Contents Section Page

ARLA Survey of Residential Investment Landlords

Prepared for The Association of Residential Letting Agents & the ARLA Group of Buy to Let Mortgage Lenders ARLA Survey of Residential Investment Landlords March 2010 Prepared by O M Carey Jones 5 Henshaw

Prepared for The Association of Residential Letting Agents & the ARLA Group of Buy to Let Mortgage Lenders ARLA Survey of Residential Investment Landlords March 2010 Prepared by O M Carey Jones 5 Henshaw

Shaping Housing and Community Agendas

CIH Response to: DCLG Rents for Social Housing from 2015-16 consultation December 2013 Submitted by email to: rentpolicy@communities.gsi.gov.uk This consultation response is one of a series published by

CIH Response to: DCLG Rents for Social Housing from 2015-16 consultation December 2013 Submitted by email to: rentpolicy@communities.gsi.gov.uk This consultation response is one of a series published by

Rent Setting Policy

Rent Setting Policy 2016-2017 Contents 1. Scope 2. Policy statement 3. Monitoring and evaluation 4. Conditions and exceptions to policy 5. Policy equality and diversity statement 6. Resident/Tenant involvement

Rent Setting Policy 2016-2017 Contents 1. Scope 2. Policy statement 3. Monitoring and evaluation 4. Conditions and exceptions to policy 5. Policy equality and diversity statement 6. Resident/Tenant involvement

Housing Benefit and Council Tax Benefit Circular. All HB and CTB managers and staff. Officers preparing subsidy claims and estimates

Housing Benefit and Council Tax Benefit Circular Department for Work and Pensions 1 st Floor, Caxton House, Tothill Street, London SW1H 9NA HB/CTB S1/2011 SUBSIDY CIRCUR WHO SHOULD READ All HB and CTB

Housing Benefit and Council Tax Benefit Circular Department for Work and Pensions 1 st Floor, Caxton House, Tothill Street, London SW1H 9NA HB/CTB S1/2011 SUBSIDY CIRCUR WHO SHOULD READ All HB and CTB

ROTHERHAM METROPOLITAN BOROUGH COUNCIL S STRATEGIC TENANCY POLICY,

ROTHERHAM METROPOLITAN BOROUGH COUNCIL S STRATEGIC TENANCY POLICY, 2013-2018 1 1 INTRODUCTION Page 3 2 BACKGROUND Page 3 3 STRATEGIC CONTEXT Page 4 3.1 National 3.2 Local 4 HOUSING IN ROTHERHAM Page 5

ROTHERHAM METROPOLITAN BOROUGH COUNCIL S STRATEGIC TENANCY POLICY, 2013-2018 1 1 INTRODUCTION Page 3 2 BACKGROUND Page 3 3 STRATEGIC CONTEXT Page 4 3.1 National 3.2 Local 4 HOUSING IN ROTHERHAM Page 5

Research into the availability of property within the local housing allowance in Nottingham City

Research into the availability of property within the local housing allowance in Nottingham City December 2018 Hannah Clemson Policy and Communications Officer 1 Following last year s report into the private-rented

Research into the availability of property within the local housing allowance in Nottingham City December 2018 Hannah Clemson Policy and Communications Officer 1 Following last year s report into the private-rented

Spring Budget Submission to HM Treasury From the Association of Residential Letting Agents (ARLA) January 2017

January 2017") Spring Budget Submission to HM Treasury From the Association of Residential Letting Agents (ARLA) January 2017 Background 1. ARLA is the UK s foremost professional and regulatory body for letting agents;

Spring Budget Submission to HM Treasury From the Association of Residential Letting Agents (ARLA) January 2017 Background 1. ARLA is the UK s foremost professional and regulatory body for letting agents;

Housing & Neighborhoods Trends

Housing & Neighborhoods Trends Where do we stand in 2017 At A Glance: Indicator Trend Comparison to State Financial Housing Burden Tax Burden To Note: In 2017, there were a number of Housing & Neighborhood

Housing & Neighborhoods Trends Where do we stand in 2017 At A Glance: Indicator Trend Comparison to State Financial Housing Burden Tax Burden To Note: In 2017, there were a number of Housing & Neighborhood

High Level Summary of Statistics Housing and Regeneration

High Level Summary of Statistics Housing and Regeneration Housing market... 2 Tenure... 2 New housing supply... 3 House prices... 5 Quality... 7 Dampness, condensation and the Scottish Housing Quality

High Level Summary of Statistics Housing and Regeneration Housing market... 2 Tenure... 2 New housing supply... 3 House prices... 5 Quality... 7 Dampness, condensation and the Scottish Housing Quality

Tenancy Policy Introduction Legal Framework Purpose Principles Policy Statement Tenancy Statement...

1 Tenancy Policy January 2014 Table of Contents Tenancy Policy... 1 Introduction... 2 Legal Framework... 2 Purpose... 3 Principles... 3 Policy Statement... 4 Tenancy Statement... 4 Tenancy Types... 5 Assured

1 Tenancy Policy January 2014 Table of Contents Tenancy Policy... 1 Introduction... 2 Legal Framework... 2 Purpose... 3 Principles... 3 Policy Statement... 4 Tenancy Statement... 4 Tenancy Types... 5 Assured

Figures include all tenancy deposit protection schemes in England and Wales and are accurate as of September 2013.

1. Introduction The tenancy deposit protection legislation was introduced in April 2007 in England and Wales as a result of the 2004 Housing Act (as amended). This digest contains key statistics on deposit

1. Introduction The tenancy deposit protection legislation was introduced in April 2007 in England and Wales as a result of the 2004 Housing Act (as amended). This digest contains key statistics on deposit

The private rented housing sector: The UK and ideas from other countries

The private rented housing sector: The UK and ideas from other countries Social Market Foundation Seminar Thursday 23 rd March 2017 Professor Michael Oxley Director, Cambridge Centre for Housing Planning

The private rented housing sector: The UK and ideas from other countries Social Market Foundation Seminar Thursday 23 rd March 2017 Professor Michael Oxley Director, Cambridge Centre for Housing Planning

Queens Drive regeneration: Swindon Council's unaffordable housing strategy

Queens Drive regeneration: Swindon Council's unaffordable housing strategy Swindon's housing crisis has been described as a crisis of affordability. Much of the town's housing in unaffordable for a large

Queens Drive regeneration: Swindon Council's unaffordable housing strategy Swindon's housing crisis has been described as a crisis of affordability. Much of the town's housing in unaffordable for a large

December 2017 Website. Lettings Policy (General Needs Housing)

") December 2017 Website Lettings Policy (General Needs Housing) 1. Introduction CHS GROUP (CHS) is a charitable Housing Association which has a duty to ensure its homes are allocated to people in housing

December 2017 Website Lettings Policy (General Needs Housing) 1. Introduction CHS GROUP (CHS) is a charitable Housing Association which has a duty to ensure its homes are allocated to people in housing

Impact of welfare reforms on housing associations: Early effects and responses by landlords and tenants

Impact of welfare reforms on housing associations: Early effects and responses by landlords and tenants For the National Housing Federation February 2014 Legal notice 2014 Ipsos MORI all rights reserved.

Impact of welfare reforms on housing associations: Early effects and responses by landlords and tenants For the National Housing Federation February 2014 Legal notice 2014 Ipsos MORI all rights reserved.

Welsh White Paper Consultation Better Lives and Communities

Welsh White Paper Consultation Better Lives and Communities Introduction The Country Land & Business Association (CLA) is a member of the European Landowners Organisation and represents over 34,000 members

Welsh White Paper Consultation Better Lives and Communities Introduction The Country Land & Business Association (CLA) is a member of the European Landowners Organisation and represents over 34,000 members

An innovative approach to addressing the housing crisis CIH Eastern Region Conference & Exhibition Master Class

An innovative approach to addressing the housing crisis CIH Eastern Region Conference & Exhibition Master Class 10 November 2015 Why do we need a new Affordable Housing option? Why do we need a new Affordable

An innovative approach to addressing the housing crisis CIH Eastern Region Conference & Exhibition Master Class 10 November 2015 Why do we need a new Affordable Housing option? Why do we need a new Affordable

Radian RATE Programme STAR Survey Results April 2017 to December 2017 All Residents Report February 2018

Radian RATE Programme STAR Survey Results April 2017 to December 2017 All Residents Report February 2018 Executive summary This report summarises the results of the continuous STAR survey of Radian s residents,

Radian RATE Programme STAR Survey Results April 2017 to December 2017 All Residents Report February 2018 Executive summary This report summarises the results of the continuous STAR survey of Radian s residents,

Member consultation: Rent freedom

November 2016 Member consultation: Rent freedom The future of housing association rents Summary of key points: Housing associations are ambitious socially driven organisations currently exploring new ways

November 2016 Member consultation: Rent freedom The future of housing association rents Summary of key points: Housing associations are ambitious socially driven organisations currently exploring new ways

London Tenants Federation Genuinely affordable housing or just more of the affordable housing con?

London Tenants Federation Genuinely affordable housing or just more of the affordable housing con? Briefing about new and rebranded affordable housing types and delivery targets. Produced July 2017 1 Genuinely

London Tenants Federation Genuinely affordable housing or just more of the affordable housing con? Briefing about new and rebranded affordable housing types and delivery targets. Produced July 2017 1 Genuinely

Caddington and Slip End Housing Needs Survey Report

Caddington and Slip End Housing Needs Survey Report August 2013 Completed on behalf of Caddington and Slip End Parish Councils by BRCC (Bedfordshire Rural Communities Charity) This report is the joint

Caddington and Slip End Housing Needs Survey Report August 2013 Completed on behalf of Caddington and Slip End Parish Councils by BRCC (Bedfordshire Rural Communities Charity) This report is the joint

Strategic Housing Role of Local Authorities in the Big Society

Strategic Housing Role of Local Authorities in the Big Society Local authority role - what I will cover Localism Bill Supported Housing Pieces of the Jigsaw LIP s New Homes Bonus LEP s Affordable Rents

Strategic Housing Role of Local Authorities in the Big Society Local authority role - what I will cover Localism Bill Supported Housing Pieces of the Jigsaw LIP s New Homes Bonus LEP s Affordable Rents

Document under Separate Cover Refer to LPS State of Housing

Document under Separate Cover Refer to LPS5-17 216 State of Housing Contents Housing in Halton 1 Overview The Housing Continuum Halton s Housing Model 3 216 Income & Housing Costs 216 Indicator of Housing

Document under Separate Cover Refer to LPS5-17 216 State of Housing Contents Housing in Halton 1 Overview The Housing Continuum Halton s Housing Model 3 216 Income & Housing Costs 216 Indicator of Housing

A matter of choice? RSL rents and home ownership: a comparison of costs

sector study 2 A matter of choice? RSL rents and home ownership: a comparison of costs Key findings and implications Registered social landlords (RSLs) across the country should monitor their rents in

sector study 2 A matter of choice? RSL rents and home ownership: a comparison of costs Key findings and implications Registered social landlords (RSLs) across the country should monitor their rents in

Housing Options in Birmingham. February 2019

Housing Options in Birmingham February 2019 For further help and support visit our website: www.birmingham.gov.uk/housing_options If you are using this document on paper, then use your search engine to

Housing Options in Birmingham February 2019 For further help and support visit our website: www.birmingham.gov.uk/housing_options If you are using this document on paper, then use your search engine to

New Plymouth District Council 1 of 23

New Plymouth District Council 1 of 23 Contents Executive Summary... 4 Introduction... 4 Purpose of this Quarterly Report... 4 First Quarterly Report... 5 New Plymouth District... 5 New Plymouth District

New Plymouth District Council 1 of 23 Contents Executive Summary... 4 Introduction... 4 Purpose of this Quarterly Report... 4 First Quarterly Report... 5 New Plymouth District... 5 New Plymouth District

Highlights at March 2016

Edi on 29 Published: May 2016 Data: March 2016 Our housing market, March 2016 Welcome to the spring edi on of our housing market bulle n, helping you keep track of local, regional and na onal housing market

Edi on 29 Published: May 2016 Data: March 2016 Our housing market, March 2016 Welcome to the spring edi on of our housing market bulle n, helping you keep track of local, regional and na onal housing market

Getting Started With Your Local Housing Market Assessment. A Step by Step Guide

Getting Started With Your Local Housing Market Assessment A Step by Step Guide November 2014 2 Getting Started With Your Local Housing Market Assessment Contents Background and Introduction 4 Stage 1a:

Getting Started With Your Local Housing Market Assessment A Step by Step Guide November 2014 2 Getting Started With Your Local Housing Market Assessment Contents Background and Introduction 4 Stage 1a:

Business, Energy and Industrial Strategy Committee Energy Efficiency Inquiry Written Submission from ARLA Propertymark January 2019

Business, Energy and Industrial Strategy Committee Energy Efficiency Inquiry Written Submission from ARLA Propertymark January 2019 Background 1. ARLA Propertymark is the UK s foremost professional and

Business, Energy and Industrial Strategy Committee Energy Efficiency Inquiry Written Submission from ARLA Propertymark January 2019 Background 1. ARLA Propertymark is the UK s foremost professional and

An innovative approach to addressing the housing crisis. A new model for affordable housing

An innovative approach to addressing the housing crisis A new model for affordable housing April 2015 Why do we need a new affordable housing model? Housing sector background Nationally and locally, demand

An innovative approach to addressing the housing crisis A new model for affordable housing April 2015 Why do we need a new affordable housing model? Housing sector background Nationally and locally, demand

Myth Busting: The Truth About Multifamily Renters

Myth Busting: The Truth About Multifamily Renters Multifamily Economics and Market Research With more and more Millennials entering the workforce and forming households, as well as foreclosed homeowners

Myth Busting: The Truth About Multifamily Renters Multifamily Economics and Market Research With more and more Millennials entering the workforce and forming households, as well as foreclosed homeowners

Contents 3/24/2011. New delivery context. HCA role and remit. Delivering for local communities. HCA in North East, Yorkshire and the Humber

New look HCA funding new affordable housing NHF Building Neighbourhoods David Curtis 25 March 2011 Contents New delivery context HCA role and remit Delivering for local communities HCA in North East, Yorkshire

New look HCA funding new affordable housing NHF Building Neighbourhoods David Curtis 25 March 2011 Contents New delivery context HCA role and remit Delivering for local communities HCA in North East, Yorkshire

Brighton & Hove, Eastbourne, Hastings, Lewes, Rother, Wealden. Private sector housing stock condition surveys

Brighton & Hove, Eastbourne, Hastings, Lewes, Rother, Wealden Private sector housing stock condition surveys Sub regional overview report FINAL REPORT Working in partnership with Contents 1 Introduction...

Brighton & Hove, Eastbourne, Hastings, Lewes, Rother, Wealden Private sector housing stock condition surveys Sub regional overview report FINAL REPORT Working in partnership with Contents 1 Introduction...

Note on housing supply policies in draft London Plan Dec 2017 note by Duncan Bowie who agrees to it being published by Just Space

Note on housing supply policies in draft London Plan Dec 2017 note by Duncan Bowie who agrees to it being published by Just Space 1 Housing density and sustainable residential quality. The draft has amended

Note on housing supply policies in draft London Plan Dec 2017 note by Duncan Bowie who agrees to it being published by Just Space 1 Housing density and sustainable residential quality. The draft has amended

HM Treasury consultation: Investment in the UK private rented sector: CIH Consultation Response

HM Treasury Investment in the UK private rented sector: CIH consultation response This consultation response is one of a series published by CIH. Further consultation responses to key housing developments

HM Treasury Investment in the UK private rented sector: CIH consultation response This consultation response is one of a series published by CIH. Further consultation responses to key housing developments

Radian RATE Programme STAR Survey Results April 2017 to March 2018 All Residents Report April 2018

Radian RATE Programme STAR Survey Results April 2017 to March 2018 All Residents Report April 2018 Executive summary This report summarises the results of the continuous STAR survey of Radian s residents,

Radian RATE Programme STAR Survey Results April 2017 to March 2018 All Residents Report April 2018 Executive summary This report summarises the results of the continuous STAR survey of Radian s residents,

The cost of increasing social and affordable housing supply in New South Wales

The cost of increasing social and affordable housing supply in New South Wales Prepared for Shelter NSW Date December 2014 Prepared by Emilio Ferrer 0412 2512 701 eferrer@sphere.com.au 1 Contents 1 Background

The cost of increasing social and affordable housing supply in New South Wales Prepared for Shelter NSW Date December 2014 Prepared by Emilio Ferrer 0412 2512 701 eferrer@sphere.com.au 1 Contents 1 Background

Exploring Shared Ownership Markets outside London and the South East

Exploring Shared Ownership Markets outside London and the South East Executive Summary (January 2019) Shared ownership homes are found in all English regions but are geographically concentrated in London

Exploring Shared Ownership Markets outside London and the South East Executive Summary (January 2019) Shared ownership homes are found in all English regions but are geographically concentrated in London

Private Rented Sector Priorities For London

National Landlords Association Private Rented Sector Priorities For London Richard Lambert Chief Executive Officer The Private Rented Sector Looking to the Future CIH London 28 June 2012 The National Landlords

National Landlords Association Private Rented Sector Priorities For London Richard Lambert Chief Executive Officer The Private Rented Sector Looking to the Future CIH London 28 June 2012 The National Landlords

4/2018 Labour s Green Paper: Housing For The Many

4/2018 Labour s Green Paper: Housing For The Many 25/4/18 Key Points The Labour Party has published a Green Paper on social housing: Housing for the Many; it is a consultation document to which responses

4/2018 Labour s Green Paper: Housing For The Many 25/4/18 Key Points The Labour Party has published a Green Paper on social housing: Housing for the Many; it is a consultation document to which responses

TEE FABIKUN. Document Ref: REP.LP Matter 3 Housing

TEE FABIKUN Document Ref: REP.LP.145-01 Matter 3 Housing 1. Bearing in mind the recent Inspector s report following the Further Alterations to the London Plan (FALP) examination (see paragraphs 31-35 of

TEE FABIKUN Document Ref: REP.LP.145-01 Matter 3 Housing 1. Bearing in mind the recent Inspector s report following the Further Alterations to the London Plan (FALP) examination (see paragraphs 31-35 of

Strategic Housing Market Assessment South Essex. Executive Summary. May 2016

Strategic Housing Market Assessment South Essex Executive Summary May 2016 Executive Summary 1. Turley in partnership with specialist demographic consultancy Edge Analytics were commissioned by the Thames

Strategic Housing Market Assessment South Essex Executive Summary May 2016 Executive Summary 1. Turley in partnership with specialist demographic consultancy Edge Analytics were commissioned by the Thames

Affordable Homes Service Plan 2016/17 and 2017/18

Report To: Housing Portfolio Holder 15 March 2017 Lead Officer: Director of Housing Purpose Affordable Homes Service Plan 2016/17 and 2017/18 1. To provide the Housing Portfolio Holder with an update on

Report To: Housing Portfolio Holder 15 March 2017 Lead Officer: Director of Housing Purpose Affordable Homes Service Plan 2016/17 and 2017/18 1. To provide the Housing Portfolio Holder with an update on

The impact of the bedroom tax on stock management by social landlords March 2014

The impact of the bedroom tax on stock management by social landlords March 2014 www.cihscotland.org If you have any questions about this survey please contact david.bookbinder@cih.org Tel: 0131 225 4544

The impact of the bedroom tax on stock management by social landlords March 2014 www.cihscotland.org If you have any questions about this survey please contact david.bookbinder@cih.org Tel: 0131 225 4544

The role of policy in influencing differences between countries in the size of the private rented housing sector Professor Michael Oxley 26/2/14

The role of policy in influencing differences between countries in the size of the private rented housing sector Professor Michael Oxley 26/2/14. 1 Introduction Comparative studies of rented housing

The role of policy in influencing differences between countries in the size of the private rented housing sector Professor Michael Oxley 26/2/14. 1 Introduction Comparative studies of rented housing

Policy Briefing Banish the Bedroom Tax Monster Campaign- Action Plan for Scotland

Policy Briefing Banish the Bedroom Tax Monster Campaign- Action Plan for Scotland From the Shelter Scotland policy library August 2013. All rights reserved. This document is only for your personal, non-commercial

Policy Briefing Banish the Bedroom Tax Monster Campaign- Action Plan for Scotland From the Shelter Scotland policy library August 2013. All rights reserved. This document is only for your personal, non-commercial

No place to live. A UNISON survey report into the impact of housing costs on London s public service workers

No place to live A UNISON survey report into the impact of housing costs on London s public service workers 1 FOREWORD Public services are critical to the London economy. Good transport and housing, quality

No place to live A UNISON survey report into the impact of housing costs on London s public service workers 1 FOREWORD Public services are critical to the London economy. Good transport and housing, quality

Thames Gateway South Essex

Thames Gateway South Essex Housing Market Trends Quarterly Report April 2010 House Prices, Affordability & Market Indicators Housing Market Trends Quarterly Report April 2010 Introduction This report monitors

Thames Gateway South Essex Housing Market Trends Quarterly Report April 2010 House Prices, Affordability & Market Indicators Housing Market Trends Quarterly Report April 2010 Introduction This report monitors

How many homes did housing associations build in 2016/17?

May 2017 How many homes did housing associations build in 2016/17? Summary of key points: Housing associations started 47,709 homes in 2016/17, a 13% increase to last year Housing associations completed

May 2017 How many homes did housing associations build in 2016/17? Summary of key points: Housing associations started 47,709 homes in 2016/17, a 13% increase to last year Housing associations completed

Response. Reinvigorating the right to buy. Contact: Adam Barnett. Investment Policy and Strategy. Tel:

Response Contact: Adam Barnett Team: Investment Policy and Strategy Tel: 020 7067 1114 Email: Adam.Barnett@housing.org.uk Date: February 2012 Ref: RE.IN.2012.RE.01 Registered office address National Housing

Response Contact: Adam Barnett Team: Investment Policy and Strategy Tel: 020 7067 1114 Email: Adam.Barnett@housing.org.uk Date: February 2012 Ref: RE.IN.2012.RE.01 Registered office address National Housing

ARLA Members Survey of the Private Rented Sector

Prepared for The Association of Residential Letting Agents ARLA Members Survey of the Private Rented Sector Second Quarter 2014 Prepared by: O M Carey Jones 5 Henshaw Lane Yeadon Leeds LS19 7RW June, 2014

Prepared for The Association of Residential Letting Agents ARLA Members Survey of the Private Rented Sector Second Quarter 2014 Prepared by: O M Carey Jones 5 Henshaw Lane Yeadon Leeds LS19 7RW June, 2014

HomeLet Rental Index

HomeLet Rental Index HomeLet is the UK s largest supplier of tenant referencing to the lettings industry. The HomeLet Rental Index shows agreed rental prices, from over 3,000 letting agents each month,

HomeLet Rental Index HomeLet is the UK s largest supplier of tenant referencing to the lettings industry. The HomeLet Rental Index shows agreed rental prices, from over 3,000 letting agents each month,

Attachment 3. Guelph s Housing Statistical Profile

Attachment 3 Guelph s Housing Statistical Profile Table of Contents 1. Population...1 1.1 Current Population (26)...1 1.2 Comparative Growth, Guelph and Ontario (21-26)...1 1.3 Total Household Growth (21

Attachment 3 Guelph s Housing Statistical Profile Table of Contents 1. Population...1 1.1 Current Population (26)...1 1.2 Comparative Growth, Guelph and Ontario (21-26)...1 1.3 Total Household Growth (21

Monthly Indicators + 7.3% + 6.6% + 8.3% Single-Family Market Overview Condo Market Overview New Listings Pending Sales.

Monthly Indicators 2018 The three most prominent national market trends for residential real estate are the ongoing lack of abundant inventory, the steadily upward movement of home prices and year-over-year

Monthly Indicators 2018 The three most prominent national market trends for residential real estate are the ongoing lack of abundant inventory, the steadily upward movement of home prices and year-over-year

3.1.b Helping local authorities to meet their strategic housing goals. 3.1.d Providing clear information for customers about options / choices

Tenancy Policy 1 Introduction 1.1 This policy sets out a framework under which Notting Hill Housing Trust will let and manage homes following the introduction of the affordable rent product 2 Background

Tenancy Policy 1 Introduction 1.1 This policy sets out a framework under which Notting Hill Housing Trust will let and manage homes following the introduction of the affordable rent product 2 Background

Briefing Book. State of the Housing Market Update San Francisco Mayor s Office of Housing and Community Development

Briefing Book State of the Housing Market Update 2014 San Francisco Mayor s Office of Housing and Community Development August 2014 Table of Contents Project Background 2 Household Income Background and

Briefing Book State of the Housing Market Update 2014 San Francisco Mayor s Office of Housing and Community Development August 2014 Table of Contents Project Background 2 Household Income Background and

Adroddiad Asesiad Marchnad Tai Lleol Gwynedd Local Housing Market Report. Gwynedd Local Housing Market Report

Adroddiad Asesiad Marchnad Tai Lleol Gwynedd Local Housing Market Report Gwynedd Local Housing Market Report Uned Strategol Tai, Gwasanaethau Tai Strategic Housing Unit, Housing Services 2013 Index Content

Adroddiad Asesiad Marchnad Tai Lleol Gwynedd Local Housing Market Report Gwynedd Local Housing Market Report Uned Strategol Tai, Gwasanaethau Tai Strategic Housing Unit, Housing Services 2013 Index Content

Rents for Social Housing from

19 December 2013 Response: Rents for Social Housing from 2015-16 Consultation Summary of key points: The consultation, published by The Department for Communities and Local Government, invites views on

19 December 2013 Response: Rents for Social Housing from 2015-16 Consultation Summary of key points: The consultation, published by The Department for Communities and Local Government, invites views on

Terms of Reference for Town of Caledon Housing Study

1.0 Introduction Terms of Reference for Town of Caledon Housing Study The Town of Caledon is soliciting proposals for a comprehensive Housing Study. Results of this Housing Study will serve as a guiding

1.0 Introduction Terms of Reference for Town of Caledon Housing Study The Town of Caledon is soliciting proposals for a comprehensive Housing Study. Results of this Housing Study will serve as a guiding

Private rented sector housing

Private rented sector housing Purpose of report For discussion. Summary The private rented sector is an important part of the local housing market. This paper introduces some of the challenges for councils

Private rented sector housing Purpose of report For discussion. Summary The private rented sector is an important part of the local housing market. This paper introduces some of the challenges for councils

Rental Housing Strategy Study # 1

Rental Housing Strategy Study # 1 Submitted to: City of Vancouver by: Will Dunning Inc November 2009 Table of Contents Table of Contents... 1 Part 1 Summary and Conclusions... 2 Introduction... 2 Housing

Rental Housing Strategy Study # 1 Submitted to: City of Vancouver by: Will Dunning Inc November 2009 Table of Contents Table of Contents... 1 Part 1 Summary and Conclusions... 2 Introduction... 2 Housing

Appendix 3: Needs Assessment

Appendix 3: Needs Assessment Overview This section compiles the available information on the need for community-led housing in Oxford, focusing on the needs of local people. It is based on a range of published

Appendix 3: Needs Assessment Overview This section compiles the available information on the need for community-led housing in Oxford, focusing on the needs of local people. It is based on a range of published

Oxfordshire Strategic Housing Market Assessment

Oxfordshire Strategic Housing Market Assessment Summary Key Findings on Housing Need March 2014 Prepared by GL Hearn Limited 20 Soho Square London W1D 3QW T +44 (0)20 7851 4900 F +44 (0)20 7851 4910 glhearn.com

Oxfordshire Strategic Housing Market Assessment Summary Key Findings on Housing Need March 2014 Prepared by GL Hearn Limited 20 Soho Square London W1D 3QW T +44 (0)20 7851 4900 F +44 (0)20 7851 4910 glhearn.com

Residential Commentary Sydney Apartment Market

Residential Commentary Sydney Apartment Market April 2017 Executive Summary Sydney Apartment Market: Key Indicators 14,200 units are currently under construction in Inner Sydney with completion expected

Residential Commentary Sydney Apartment Market April 2017 Executive Summary Sydney Apartment Market: Key Indicators 14,200 units are currently under construction in Inner Sydney with completion expected

Christchurch Housing Accord Monitoring Report. For quarter ending June 2015

Christchurch Housing Accord Monitoring Report For quarter ending June 2015 Executive Summary This report provides an overview of the Christchurch housing market and an update on priority Accord actions.

Christchurch Housing Accord Monitoring Report For quarter ending June 2015 Executive Summary This report provides an overview of the Christchurch housing market and an update on priority Accord actions.

Cabinet Meeting 4 December 2013

Cabinet Meeting 4 December 2013 Agenda Item No: 8 Report title Decision designation Cabinet member with lead responsibility Key decision In forward plan Wards affected Accountable director Originating

Cabinet Meeting 4 December 2013 Agenda Item No: 8 Report title Decision designation Cabinet member with lead responsibility Key decision In forward plan Wards affected Accountable director Originating

Rent Setting. Date: March 2015 Version: 1. Document Reference: Document Owner: Bill Henderson. See also: Date last reviewed: March 2015

Rent Setting Date: March 2015 Version: 1 Document Reference: Document Owner: Bill Henderson See also: Date last reviewed: March 2015 Date due for next review: January 2018 1. Purpose of the procedure To

Rent Setting Date: March 2015 Version: 1 Document Reference: Document Owner: Bill Henderson See also: Date last reviewed: March 2015 Date due for next review: January 2018 1. Purpose of the procedure To

East Riding Of Yorkshire Council

East Riding Of Yorkshire Council Affordable Housing Viability Assessment Analysis of increasing S106/CIL Contributions & the potential impact of Affordable Rent Tenures St Pauls House 23 Park Square South

East Riding Of Yorkshire Council Affordable Housing Viability Assessment Analysis of increasing S106/CIL Contributions & the potential impact of Affordable Rent Tenures St Pauls House 23 Park Square South

State of the Johannesburg Inner City Rental Market

State of the Johannesburg Inner City Rental Market Presentation to TUHF- 5th July 2017 5 July 2017 State of the Johannesburg Inner City Rental Market National Association of Social Housing Organisations

State of the Johannesburg Inner City Rental Market Presentation to TUHF- 5th July 2017 5 July 2017 State of the Johannesburg Inner City Rental Market National Association of Social Housing Organisations

BUSINESS PLAN Part 1

BUSINESS PLAN 2016-17 Part 1 Contents Executive Summary... 1 Objectives... 2 Company Formation... 3 Governance and Management Structure... 4 Decision Making... 6 Operational Management... 7 Market Overview...

BUSINESS PLAN 2016-17 Part 1 Contents Executive Summary... 1 Objectives... 2 Company Formation... 3 Governance and Management Structure... 4 Decision Making... 6 Operational Management... 7 Market Overview...

21 March Development Update

21 March 214 Development Update Contact: Charlie Blagbrough Job Title: Policy Assistant, Investment Team Email: charlie.blagbrough@housing.org.uk Direct: 2 767 176 Reference: 1 Summary Development Update

21 March 214 Development Update Contact: Charlie Blagbrough Job Title: Policy Assistant, Investment Team Email: charlie.blagbrough@housing.org.uk Direct: 2 767 176 Reference: 1 Summary Development Update

Funding future homes: Executive summary and discussion

Funding future homes: Executive summary and discussion Funding future homes Executive summary and discussion questions When it comes to building new homes housing associations are navigating one of the

Funding future homes: Executive summary and discussion Funding future homes Executive summary and discussion questions When it comes to building new homes housing associations are navigating one of the

THE VALUE PROPOSITION OF A STRONG INDUSTRY ASSOCIATION SCOTT ANDISON

THE VALUE PROPOSITION OF A STRONG INDUSTRY ASSOCIATION SCOTT ANDISON JANUARY 15, 2016 THE LINE UP THE FRPO BRAND INDUSTRY PROFILE THE NEED FOR INDUSTRY ADVOCACY SELECT POLICY PRIORITIES QUESTIONS 2 Professional

THE VALUE PROPOSITION OF A STRONG INDUSTRY ASSOCIATION SCOTT ANDISON JANUARY 15, 2016 THE LINE UP THE FRPO BRAND INDUSTRY PROFILE THE NEED FOR INDUSTRY ADVOCACY SELECT POLICY PRIORITIES QUESTIONS 2 Professional