Top 10 Real Estate Issues in Not-for-Profit Organizations

|

|

|

- Sharleen Ray

- 5 years ago

- Views:

Transcription

1 Top 10 Real Estate Issues in Not-for-Profit Organizations OCTOBER 3, 2017 MARIE BRILMYER, CPA, MACC DONNA JENKINS, CPA ADAM SCHULTZ, CPA

2 Introduction Welcome Overview of the Webinar Introduction to Panelists - Adam Schultz, CPA - Marie Brilmyer, CPA, MACC - Donna Jenkins, CPA

3 Top 10 Real Estate Issues 1. Choosing the Right Location 2. Lease vs. Buy 3. Leasing of Cell Tower Space 4. Valuation of In-Kind Rent 5. Accounting for Internally-Constructed Property 6. Disposal of Long-Lived Assets 7. Impairment 8. Rental Income Subject to UBIT 9. Donated Real Estate and the Gift Acceptance Policy

4 1. Choosing the Right Location

5 1. Choosing the Right Location Location is important - Many NFP s have a community-based and locally operated quality to them - May play in to the final decision of a donor and beneficiary to say yes - Proximity to resources, labor, and beneficiaries can enhance (or challenge) an NFP s ability to succeed

6 1. Choosing the Right Location Consider all the financial and non-financial consequences - Access to beneficiaries and markets for products and services - Access to employees, donors, and volunteers - Access to materials and vendors - Competition from other organizations in the area Consider the prestige (or lack thereof) of the surroundings - Is it accessible for the beneficiaries? Are there target beneficiaries in the area? - Will volunteers want to come there? - Will donors want to continue affiliation with the organization?

7 1. Choosing the Right Location Examples - A not-for-profit organization seeking to attract, train, and deploy volunteers found it difficult to do so in a location without public parking in a crime-riddled area - An organization seeking to meet with and ask doctors to submit medical research articles found it best to have a location near a highway with nice business-like conference rooms - A not-for-profit providing alcohol and drug addiction counseling services found it best to have several locations in and around the communities they wanted to serve

8 2. Lease vs. Buy

9 2. Lease vs. Buy Each option has benefits and drawbacks Decision depends on organization s situation - Is the organization stable or growing? - Are funding sources consistent? - Are programs changing / expanding? - Need for customized space or specific location? - How does current space fit with above questions? - Can the organization afford to buy? (consider down payment, renovations, and unexpected repairs)

10 2. Lease vs. Buy Lease Pros Flexibility (lease what you need) Typically less expensive (short term) No large cash payments No property management Lease Cons Increasing rental rates Less control over operating expenses Re-negotiations at end of lease Uncertainty at end of lease Buy Pros Appreciating asset (build net assets) Greater control over operating expenses Savings (long-term) Less uncertainty Potential revenue from other tenants Buy Cons Up-front capital (or fundraising efforts) Less flexibility Operating responsibilities Long-term debt considerations

11 2. Lease vs. Buy Current lease accounting - Operating leases payments are expensed (no asset or liability recorded) - Capital leases Asset and liability recorded, asset is depreciated and lease payments reduce liability New lease accounting (effective in 2019) - Operating lease Asset and liability recorded, depreciation of asset and interest expense shown straight-line as lease expense on the statement of operations - Finance lease Similar to capital lease

12 2. Lease vs. Buy Free cash or other liquid funds Fundraising (capital campaign) Foundation / government grants Long-term debt / bond issuance

13 3. Leasing of Cell Tower Space

14 3. Leasing of Cell Tower Space The Wireless Tower Construction industry has seen steady growth with expected continued growth - 3.2% annually from ; 5.9% annually expected from Tower companies will lease/buy land from property owners and in turn lease out the constructed tower to wireless carriers (AT&T, Verizon, Sprint, etc.) With a growing industry and increasing reliance on wireless technology, there will be more opportunity to lease out small parcels of land or space

15 3. Leasing of Cell Tower Space Common leasing provisions: - Typically lease land ranging from 2,500 10,000 sq. ft. with the right to construct tower - Densely populated areas leasing rooftop space - Two common term structures: year initial term with multiple renewal periods - 40 year easement with buy-out provision for ownership

16 3. Leasing of Cell Tower Space Common leasing provisions: - Rental payments monthly or annually - Annual or term rental escalations - Lessor potential to negotiate for tower revenue share contingent rental consideration - Ex. $500/mo + 25% of rental revenue from tower - Asset Retirement Obligation for the lessee - Must remove equipment upon termination of lease

17 3. Leasing of Cell Tower Space Typically structured as operating leases - Accounting is simpler - Lease payments are operational expenses, thus fully deductible for the lessee Rental income will need to be straight-lined in accordance with GAAP - Majority of leases include annual escalations UBIT will need to be considered when entering into an arrangement ASU will need to be considered

18 4. Valuation of In-Kind Rent

19 4. Valuation of In-Kind Rent In-Kind Rent Defined - The ability to operate and/or usage rights to a facility at no formal cost to the NFP or at a below market rate - A contribution in the form of use of property - Under ASC the use of property in-kind is classified as a form of contributed assets, rather than a form of contributed services Initial Valuation - Based on fair market rental value in the current marketplace - Determine market price of a similar property using observable inputs such as rental square footage market price, available lease agreement, management estimate based on similar properties in area, etc.

20 4. Valuation of In-Kind Rent Recognition - The FV of the contributed use of the facility would be recognized as both revenue/support and corresponding expense in the period the in-kind rental facility is used - Determination needs to be made if the in-kind rent is for a single period vs. extended period of time Treatment Options - Single Period Recorded as in-kind revenue/expense in the period benefit is received - Extended Period Defaults to unconditional promises to give treatment, receivable and revenue recorded for discounted FV of entire rental term

21 4. Valuation of In-Kind Rent EXAMPLE: XYZ Foundation receives the free use of 10,000 square feet of premier office space provided by a local corporation. The local corporation has informed XYZ Foundation that it intends to continue providing the space as long as it is available, and although it expects it would be able to give the Foundation 30 days advance notice, it may discontinue providing the space at any time. The local corporation normally rents similar space for $14 - $16 annually per square foot, the going market rate for office space in the area. XYZ Foundation decides to accept this gift the free use of office space to conduct its programming activities. SOLUTION: Since the in-kind term is not a true unconditional promise over a specified time period (right to cancel with notice), XYZ Foundation would record a period revenue/expense for the FV of the in-kind rent between $140,000 - $160,000 in the period it receives such in-kind benefit.

22 4. Valuation of In-Kind Rent EXAMPLE: Given the same fact pattern, the local corporation has explicitly and unconditionally promises the use of the office space for 5 years, with no intentions of cancelling or amended the rental period until after the original 5 year term is completed. SOLUTION: Recognition would default to promise to give treatment, recognizing the FV of the entire rental term with a receivable and corresponding restricted revenue in current period. - The asset and related restricted revenue should be discounted based on NFP s incremental borrowing rate over the 5 year term - The asset is typically referred to as donated facility use asset - Expense recognition would occur over each period ratably until the asset is relieved at end of 5 year term

23 4. Valuation of In-Kind Rent Discounted Rent or $1 Lease - NFP would recognize in-kind rent/expense for the difference between amount paid and market rental price - Similar treatment as previous slides if period of time or extended period of time Lack of Observable Inputs - May require consultation of real estate or market expert to determine value

24 5. Accounting for Internally-Constructed Property

25 5. Accounting for Internally-Constructed Property Things to Consider - Identifying the Direct and Indirect costs of the project. - Cost accumulation continues during construction and is applied towards a CIP account (Construction-in- Progress). Direct Costs - Costs that can be easily and conveniently traced to a particular cost objective. - Include items such as direct materials (i.e. electrical wiring for a building), salaries for employees directly working on a project (i.e. labor hours), as well as employer paid taxes associated with the direct wages.

26 5. Accounting for Internally-Constructed Property Indirect Costs - Many different ways to allocate costs to a selfconstructed asset (i.e. allocated based off of labor hours of employees directly involved in construction). - Should be distinguished from G & A costs, as they are considered period costs (expensed in the period they are incurred). - It is advisable to have an internal policy on allocations of indirect costs.

27 5. Accounting for Internally-Constructed Property Recognition of In-Kind Labor - Donated services and labor are required to be recognized as contributions revenue (and assets and expenses) when certain criteria is met: - The labor or services must create or enhance the internally constructed asset of the entity. - The donated service must require specialized skills, are provided by individuals possessing those skills, and would typically need to have been purchased if not provided by donation. - Examples include architectural services.

28 5. Accounting for Internally-Constructed Property Statement of Financial Position - Should stay on the balance sheet as CIP until completion. - No depreciation is applied until completion. - Interest expense is generally capitalized if borrowing money to pay for costs relating to constructing an asset.

29 6. Disposal of Long-Lived Assets

30 6. Disposal of Long-Lived Assets NFP strategy many times involves disposing of long-lived assets to generate cash - Sale of real estate As demand for services and the market conditions change, NFP s react and move locations NFP may change its strategy and this may result in - Discontinued operations - Sale of the NFP to another entity, which would include long-lived assets such as real estate, computers, software, and vehicles

31 6. Disposal of Long-Lived Assets Assets to be Sold - A long-lived asset to be sold should be classified as held for sale in the period in which all of the criteria are met: - Management commits to a plan to sell - The asset is available for immediate sale in its present condition - The entity has initiated an active program to locate a buyer - The sale of assets is probable generally within one year of the asset being held for sale - The asset is being actively marketed for sale at a price that is reasonable relative to its current fair value - Actions required to complete the plan indicate that it is unlikely that significant changes to the plan will be made or that the plan will be withdrawn

32 6. Disposal of Long-Lived Assets Measured at the lower of carrying amount or fair value less cost to sell Should NOT be depreciated or amortized An impairment loss should be recorded for any initial or subsequent write-down to fair value less cost to sell A gain should be recorded for any subsequent increase in fair value less cost to sell, but not to exceed the cumulative loss previously recognized for a write-down to fair value less cost to sell

33 6. Disposal of Long-Lived Assets Present the asset separately on the statement of financial position Property and Equipment - net Building and improvements Furniture and fixtures Vehicles Less: Accumulated depreciation Construction in progress Asset held for sale XXXX XXXX XXXX XXXX XXXX XXXX XXXX Total property and equipment, net XXXX

34 6. Disposal of Long-Lived Assets Changes to a Plan of Sale - An entity may decide not to sell a long-lived asset and in that case, the asset should be reclassified as held and used - Such asset should be measured at the lower of its carrying amount prior to being held for sale, adjusted for deprecation or the fair value at the date of the decision not to sell

35 6. Disposal of Long-Lived Assets Assets to be Abandoned - If an entity commits to a plan to abandon an asset before the end of its useful life, the asset s depreciation estimates should be revised to reflected the shortened life

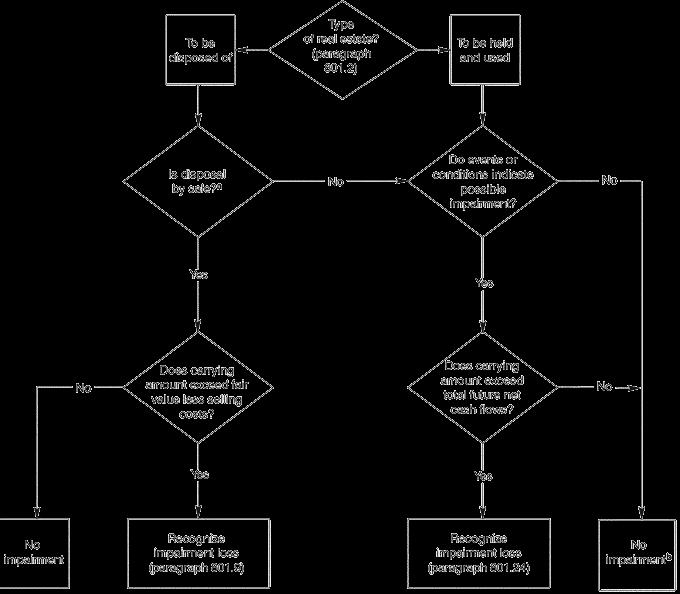

36 7. Impairment

37 7. Impairment

38 7. Impairment Does the carrying amount exceed fair value less selling costs? - If no, no impairment exists - If yes, recognize impairment loss Recognizing impairment loss - Recognize impairment for the excess and reduce the carrying amount accordingly - After this, carrying amount of property should be adjusted up or down for any subsequent changes in fair value

39 7. Impairment Signs of possible impairment - Significant decrease in the property s market value - Significant amount of physical damage - Significant adverse physical change in the property - Continuing losses for a property used to produce revenue Assessing for impairment - Does the carrying value exceed net future cash flows? - If yes, no impairment exists - If no, recognize impairment loss based on fair value of asset

40 7. Impairment Property to be disposed of DR Impairment Loss on Real Estate XXXX CR Allowance for Impairment XXXX Property to be held and used DR Impairment Loss on Real Estate XXXX CR Property to be Impaired XXXX - This will become the property s new cost basis

41 8. Rental Income Subject to UBIT

42 8. Rental Income Subject to UBIT Rental income from real property is generally excluded from UBIT except in the following situations Property is debt-financed and held to produce income OR Property with acquisition indebtedness during the year or 12 months before disposal - What is acquisition indebtedness? - A debt agreement is entered into when acquiring or improving the property - A debt agreement is entered into before or after acquiring or improving the property and the debt was reasonably foreseeable

43 8. Rental Income Subject to UBIT What is acquisition indebtedness? - The Organization buys mortgaged property, but does not assume the mortgage; tax planning tip available here! - Prepay a proportionate share of debt and secure releases of liability from creditor and co-owners - Acquire an undivided interest - Entire property remains encumbered - The Organization receives property by bequest - Not considered acquisition indebtedness for first 10 years - The Organization receives the property by gift - Same as Bequest if mortgage on property 5 years prior to gift - Donor held property > 5 years prior to gift - Exceptions do not apply if the Organization assumes or agrees to pay the debt (even if partial) secured by the mortgage

44 8. Rental Income Subject to UBIT Exceptions include: The Organization uses > 85% of the property for its exempt purpose The Convenience Exception, Volunteer Exception, or Donated Merchandise Exception applies - Convenience: Carried on by a governmental college or university for the convenience of its members, students, patients, officers or employees. (parking garage) - Volunteer: Substantially all the work is performed for the Organization without compensation. (parking lot) - Donated Merchandise: Consists of selling merchandise, substantially all or which the Organization received as gifts or contributions. (thrift store) Property is leased to a related organization for certain uses

45 8. Rental Income Subject to UBIT Leases that include both real and personal property Personal property is any property that is depreciable under the IRS Code, including tangible property as defined (note that cell towers are personal property) - Determined by the percentage of rents attributed to personal property compared to the total rent received - If > 10%, then all rents from the lease are excluded - If 10% to 50%, then only rents attributed to the real property are excluded - If < 50%, then all rents from the lease are subject to UBIT

46 8. Rental Income Subject to UBIT Rental income from a Controlled Corporation - Include in the parent s calculation of UBIT to the extent it would have been taxable otherwise Lease payments that include compensation for services rendered to the Lessee - Subject to UBIT if the services are not customarily rendered - Customarily rendered = furnishing heat, electric and trash removal - Not customarily rendered = hotel rooms, parking lots, warehouses and storage garages Rent that is calculated as a percentage of net income - Considered to have a profits interest or joint venture with the lessee

47 8. Rental Income Subject to UBIT Calculating Unrelated Debt-Financed Income - Compute using this formula: Average acquisition indebtedness X gross income from property Average adjusted basis - Expenses that are directly connected with the property are deductible - Planning tips: - An NOL can be carried back two years or forward twenty years. Filing a 990-T even if there is no other income to report can help the Organization preserve the loss and claim it in a future year. - Usually the gain from sale of debt-financed property is included in UBIT - If debt is paid off more than 12 months before the sale of property, then the gain is not taxable (although the transaction may still be taxable for other reasons such as depreciation recapture)

48 9. Donated Real Estate and the 990

49 9. Donated Real Estate and the 990 Use caution when accepting gifts of real estate - Understand the potential liability Detailed appraisal of the property by a professional is necessary - Appraisal is required for donations greater than $5,000 Donation should be recorded at fair market value (FMV) as of the date of the contribution Organization must return a written acknowledgement to the donor for any gift of $250 or more

50 10. Gift Acceptance Policy

51 10. Gift Acceptance Policy Organizations should implement a formal gift acceptance policy that specifies the following: - Type of assets accepted or not accepted - Mission statement does the gift make sense? - Zoning restrictions can the land be used for the desired purpose? - Comprehensive Environmental Response, Compensation and Liability Act (CERCLA) liability for clean up of environmentally damaged sites (Superfund). May hold all those in the chain of title responsible, regardless of material participation by the owner. The third party defense includes protection for innocent landowners, provided they had no reason to know of the existence of hazardous substances and made all "appropriate inquiry into the previous owner and uses of the property consistent with good commercial or customary practice." 42 U.S.C. sec. 9601(35). Before accepting any gift of real estate, it s a good idea to make sure an environmental evaluation has been done!

52 10. Gift Acceptance Policy What types of restrictions by donor are allowable - Will restricted land use impede the organization s use of the property? - Does the organization have the wherewithal and the desire to hold the land in perpetuity? Selling donated property - If the organization plans to sell the donation, is there a specific time of year that it can be sold? (may not want to accept a gift outside of this time frame) - What are the holding costs (taxes, insurance, maintenance) if the asset cannot be quickly sold? - If selling a donated asset, make sure the donor is aware that the property is being sold as this can sometimes cause tax consequences. (Also file Form 8282 if needed)

53 Questions? Information presented is not meant to constitute legal, accounting or other professional advice. Any action taken based on information in this presentation should be taken only after a detailed review of the specific facts and circumstances. Information is current as of the date presented.

54 Contact Information Marie Brilmyer - mbrilmyer@cohencpa.com Donna Jenkins - djenkins@cohencpa.com Adam Schultz - aschultz@cohencpa.com

2) All long-term leases should be capitalized in the accounts by the lessee.

All long-term leases should be capitalized in the accounts by the lessee.") Chapter 18 Leases 1) The principal attribute of finance leases is that the risks and rewards of asset ownership are deemed to remain with the lessor. LO: 18-02 List the criteria for classification of a

Chapter 18 Leases 1) The principal attribute of finance leases is that the risks and rewards of asset ownership are deemed to remain with the lessor. LO: 18-02 List the criteria for classification of a

HABITAT FOR HUMANITY KANSAS CITY, INC. FINANCIAL STATEMENTS

HABITAT FOR HUMANITY KANSAS CITY, INC. FINANCIAL STATEMENTS Year Ended December 31, 2015 Mayer Hoffman McCann P.C. An Independent CPA Firm 700 West 47th Street, Suite 1100 Kansas City, MO 64112 Main: 816.945.5600

HABITAT FOR HUMANITY KANSAS CITY, INC. FINANCIAL STATEMENTS Year Ended December 31, 2015 Mayer Hoffman McCann P.C. An Independent CPA Firm 700 West 47th Street, Suite 1100 Kansas City, MO 64112 Main: 816.945.5600

ROCKFORD AREA HABITAT FOR HUMANITY, INC. FINANCIAL STATEMENTS and INDEPENDENT AUDITOR S REPORT. For the years ended June 30, 2014 and 2013

FINANCIAL STATEMENTS and INDEPENDENT AUDITOR S REPORT For the years ended June 30, 2014 and 2013 TABLE OF CONTENTS Independent Auditor s Report 1 Statements of Financial Position 2 Statements of Activities

FINANCIAL STATEMENTS and INDEPENDENT AUDITOR S REPORT For the years ended June 30, 2014 and 2013 TABLE OF CONTENTS Independent Auditor s Report 1 Statements of Financial Position 2 Statements of Activities

Auditing PP&E, Including Leases

Auditing PP&E, Including Leases Learning Objectives Discuss typical audit risks and special considerations. Tailor an audit plan to assessed audit risk. Explain key controls related to PP&E. Describe lease

Auditing PP&E, Including Leases Learning Objectives Discuss typical audit risks and special considerations. Tailor an audit plan to assessed audit risk. Explain key controls related to PP&E. Describe lease

HABITAT FOR HUMANITY OF KANSAS CITY, INC. FINANCIAL STATEMENTS

FINANCIAL STATEMENTS Year Ended June 30, 2017 700 West 47th Street, Suite 1100 Kansas City, MO 64112 Main: 816.945.5600 Fax: 816.897.1280 www.mhmcpa.com INDEPENDENT AUDITORS' REPORT To the Board of Directors

FINANCIAL STATEMENTS Year Ended June 30, 2017 700 West 47th Street, Suite 1100 Kansas City, MO 64112 Main: 816.945.5600 Fax: 816.897.1280 www.mhmcpa.com INDEPENDENT AUDITORS' REPORT To the Board of Directors

Healthcare Accounting Update. February 14, 2018 Presented by: Greg Heitkamp, Audit/Accounting Senior Manager

Healthcare Accounting Update February 14, 2018 Presented by: Greg Heitkamp, Audit/Accounting Senior Manager Agenda ASU 2014-09 & ASU 2015-14 Revenue from Contracts with Customers Effective date: 12/31/18

Healthcare Accounting Update February 14, 2018 Presented by: Greg Heitkamp, Audit/Accounting Senior Manager Agenda ASU 2014-09 & ASU 2015-14 Revenue from Contracts with Customers Effective date: 12/31/18

roots The Substance of the Standard Contents Changes to the Accounting for Goodwill for Private Companies

The Substance of the Standard MAYER HOFFMAN MCCANN P.C. AN INDEPENDENT CPA FIRM TM A publication of the Professional Standards Group February 2014 Changes to the Accounting for Goodwill for Private Companies

The Substance of the Standard MAYER HOFFMAN MCCANN P.C. AN INDEPENDENT CPA FIRM TM A publication of the Professional Standards Group February 2014 Changes to the Accounting for Goodwill for Private Companies

HABITAT FOR HUMANITY OF BROWARD, INC.

FINANCIAL STATEMENTS CONTENTS Independent Auditors Report... 1-3 Financial Statements Statement of Financial Position...4 Statement of Activities and Changes in Net Assets...5 Statement of Cash Flows...6

FINANCIAL STATEMENTS CONTENTS Independent Auditors Report... 1-3 Financial Statements Statement of Financial Position...4 Statement of Activities and Changes in Net Assets...5 Statement of Cash Flows...6

2018 Accounting & Auditing Update P R E S E N T E D B Y : D A N I E L L E Z I M M E R M A N & A N D R E A S A R T I N

2018 Accounting & Auditing Update P R E S E N T E D B Y : D A N I E L L E Z I M M E R M A N & A N D R E A S A R T I N AGENDA Leases FASB & GASB Revenue Recognition FASB 2 FASB ASU 2016-02, Leases (Topic

2018 Accounting & Auditing Update P R E S E N T E D B Y : D A N I E L L E Z I M M E R M A N & A N D R E A S A R T I N AGENDA Leases FASB & GASB Revenue Recognition FASB 2 FASB ASU 2016-02, Leases (Topic

Leases. (a) the lease transfers ownership of the asset to the lessee by the end of the lease term.

the lease transfers ownership of the asset to the lessee by the end of the lease term.") Leases 1.1. Classification of leases A lease is classified as a finance lease if it transfers substantially all the risks and rewards incidental to ownership. A lease is classified as an operating lease

Leases 1.1. Classification of leases A lease is classified as a finance lease if it transfers substantially all the risks and rewards incidental to ownership. A lease is classified as an operating lease

Sri Lanka Accounting Standard LKAS 40. Investment Property

Sri Lanka Accounting Standard LKAS 40 Investment Property LKAS 40 CONTENTS SRI LANKA ACCOUNTING STANDARD LKAS 40 INVESTMENT PROPERTY paragraphs OBJECTIVE 1 SCOPE 2 DEFINITIONS 5 CLASSIFICATION OF PROPERTY

Sri Lanka Accounting Standard LKAS 40 Investment Property LKAS 40 CONTENTS SRI LANKA ACCOUNTING STANDARD LKAS 40 INVESTMENT PROPERTY paragraphs OBJECTIVE 1 SCOPE 2 DEFINITIONS 5 CLASSIFICATION OF PROPERTY

Perry Farm Development Co.

(a not-for-profit corporation) Consolidated Financial Report December 31, 2010 Contents Report Letter 1 Consolidated Financial Statements Balance Sheet 2 Statement of Operations 3 Statement of Changes

(a not-for-profit corporation) Consolidated Financial Report December 31, 2010 Contents Report Letter 1 Consolidated Financial Statements Balance Sheet 2 Statement of Operations 3 Statement of Changes

Financial Statements January 29, 2017 and January 31, 2016 PetSmart Charities of Canada

Financial Statements January 29, 2017 and January 31, 2016 PetSmart Charities of Canada Table of Contents Independent Auditor s Report... 1 Financial Statements... Error! Bookmark not defined. Statement

Financial Statements January 29, 2017 and January 31, 2016 PetSmart Charities of Canada Table of Contents Independent Auditor s Report... 1 Financial Statements... Error! Bookmark not defined. Statement

Miles CPA Review: FAR Updates

Miles CPA Review: FAR - 2019 Updates Summary of updates: - FAR-4.4: s [ASC 842] effective fiscal years beginning after Dec 15, 2018 (for issuers) and effective fiscal years beginning after Dec 15, 2019

Miles CPA Review: FAR - 2019 Updates Summary of updates: - FAR-4.4: s [ASC 842] effective fiscal years beginning after Dec 15, 2018 (for issuers) and effective fiscal years beginning after Dec 15, 2019

Financial Statements January 28, 2018 PetSmart Charities of Canada

Financial Statements January 28, 2018 Table of Contents Independent Auditor s Report... 1 Financial Statements Statement of Financial Position... 2 Statement of Operations and Changes in Fund Balances...

Financial Statements January 28, 2018 Table of Contents Independent Auditor s Report... 1 Financial Statements Statement of Financial Position... 2 Statement of Operations and Changes in Fund Balances...

IAS 38 Intangible Assets

21/12/2010, Tuesday From To Details Faculty 2:15 PM 5:30 PM IAS 38 : Intangible Assets IAS 40 : Investment Property IFRS 5 : Non Current Assets Held for Sale and Discontinued Operations CA. Chintan Patel,

21/12/2010, Tuesday From To Details Faculty 2:15 PM 5:30 PM IAS 38 : Intangible Assets IAS 40 : Investment Property IFRS 5 : Non Current Assets Held for Sale and Discontinued Operations CA. Chintan Patel,

Accounting and Auditing Update. Paul Lundy

Accounting and Auditing Update Paul Lundy Leases: Not Just for the Footnotes Anymore Significant Financial Statement Impact New lease standard generally requires all leases to be capitalized and recognized

Accounting and Auditing Update Paul Lundy Leases: Not Just for the Footnotes Anymore Significant Financial Statement Impact New lease standard generally requires all leases to be capitalized and recognized

IASB Staff Paper March 2011

IASB Staff Paper March 2011 Effect of board redeliberations on Exposure Draft Leases About this staff paper This staff paper indicates how the proposals in the Exposure Draft Leases would change as a result

IASB Staff Paper March 2011 Effect of board redeliberations on Exposure Draft Leases About this staff paper This staff paper indicates how the proposals in the Exposure Draft Leases would change as a result

Click to edit Master title style REVENUE RECOGNITION Understanding the New Revenue Recognition Standard ASC 606

Click to edit Master title style REVENUE RECOGNITION Understanding the New Revenue Recognition Standard ASC 606 9/7/2017 0 Agenda Overview of ASC 606 Review of the five-step process Accounting for contract

Click to edit Master title style REVENUE RECOGNITION Understanding the New Revenue Recognition Standard ASC 606 9/7/2017 0 Agenda Overview of ASC 606 Review of the five-step process Accounting for contract

REAL ESTATE PERSPECTIVE ON NEW LEASE ACCOUNTING STANDARDS

VALUATION & ADVISORY REAL ESTATE PERSPECTIVE ON NEW LEASE ACCOUNTING STANDARDS BY JOHN CORBETT, MAI, ASA, FRICS AND MARC R. SHAPIRO, MAI, MRICS INTRODUCTION The Financial Accounting Standards Board (FASB)

VALUATION & ADVISORY REAL ESTATE PERSPECTIVE ON NEW LEASE ACCOUNTING STANDARDS BY JOHN CORBETT, MAI, ASA, FRICS AND MARC R. SHAPIRO, MAI, MRICS INTRODUCTION The Financial Accounting Standards Board (FASB)

Accounting for Leases

Office: Business Services Procedure Contact: Director of Business Services Related Policy or Policies: Noted within procedure statement Revision History Revision Number: Change: Date: 001 Update content

Office: Business Services Procedure Contact: Director of Business Services Related Policy or Policies: Noted within procedure statement Revision History Revision Number: Change: Date: 001 Update content

Accounting for Leases in Public Sector (IPSAS 13 Leases)

") TRAINING WORKSHOP ON APPLICATION OF IPSASs Accounting for Leases in Public Sector (IPSAS 13 Leases) By Yona Killagane NSSF COMMERCIAL COMPLEX MOROGORO 7thApril 2017 Objectives and Scope Objective: Prescribes

TRAINING WORKSHOP ON APPLICATION OF IPSASs Accounting for Leases in Public Sector (IPSAS 13 Leases) By Yona Killagane NSSF COMMERCIAL COMPLEX MOROGORO 7thApril 2017 Objectives and Scope Objective: Prescribes

HABITAT FOR HUMANITY OF THE MIDDLE KEYS, INC. Financial Statements. December 31, (With Independent Auditors Report Thereon)

") Financial Statements (With Independent Auditors Report Thereon) TABLE OF CONTENTS PAGE Independent Auditors Report 1-2 Financial Statements for the year ended Statement of Financial Position 3 Statement

Financial Statements (With Independent Auditors Report Thereon) TABLE OF CONTENTS PAGE Independent Auditors Report 1-2 Financial Statements for the year ended Statement of Financial Position 3 Statement

The Financial Accounting Standards Board

V A L U A T I O N How the New Leases Standard May Impact Business Valuations By Judith H. O Dell, CPA, CVA The Financial Accounting Standards Board issued the 485 page Leases Standard (Topic 842) in February,

V A L U A T I O N How the New Leases Standard May Impact Business Valuations By Judith H. O Dell, CPA, CVA The Financial Accounting Standards Board issued the 485 page Leases Standard (Topic 842) in February,

Meet Definition of. Be investment property. & Follow FV Model. Earn Rentals

Meet Definition of Requirements It s Property Held to Use in Production Process Or Admin Purpose Earn Capital Appreciation Earn Rentals & Follow Model Instead of And Available on Property By Property Basis

Meet Definition of Requirements It s Property Held to Use in Production Process Or Admin Purpose Earn Capital Appreciation Earn Rentals & Follow Model Instead of And Available on Property By Property Basis

EN Official Journal of the European Union L 320/373

29.11.2008 EN Official Journal of the European Union L 320/373 INTERNATIONAL FINANCIAL REPORTING STANDARD 3 Business combinations OBJECTIVE 1 The objective of this IFRS is to specify the financial reporting

29.11.2008 EN Official Journal of the European Union L 320/373 INTERNATIONAL FINANCIAL REPORTING STANDARD 3 Business combinations OBJECTIVE 1 The objective of this IFRS is to specify the financial reporting

Lessor Example Performance Obligation Approach

Lessor Example Performance Obligation Approach **Disclaimer The exposure draft received nearly 700 letters of comment through the comment period ended December 15, 2010. There is some expectation that

Lessor Example Performance Obligation Approach **Disclaimer The exposure draft received nearly 700 letters of comment through the comment period ended December 15, 2010. There is some expectation that

Leases: Overview of the new guidance

Leases: Overview of the new guidance Prepared by: Richard Stuart, Partner, National Professional Standards Group, RSM US LLP richard.stuart@rsmus.com, +1 203 905 5027 March 2, 2016 Introduction On February

Leases: Overview of the new guidance Prepared by: Richard Stuart, Partner, National Professional Standards Group, RSM US LLP richard.stuart@rsmus.com, +1 203 905 5027 March 2, 2016 Introduction On February

HABITAT FOR HUMANITY OF BROWARD, INC.

FINANCIAL STATEMENTS CONTENTS Independent Auditors Report... 1-3 Financial Statements Statement of Financial Position...4 Statement of Activities and Changes in Net Assets...5 Statement of Cash Flows...6

FINANCIAL STATEMENTS CONTENTS Independent Auditors Report... 1-3 Financial Statements Statement of Financial Position...4 Statement of Activities and Changes in Net Assets...5 Statement of Cash Flows...6

Mountain Equipment Co-operative

Mountain Equipment Co-operative Consolidated Financial Statements, and December 28, 2009 April 11, 2012 Independent Auditor s Report To the Members of Mountain Equipment Co-operative We have audited the

Mountain Equipment Co-operative Consolidated Financial Statements, and December 28, 2009 April 11, 2012 Independent Auditor s Report To the Members of Mountain Equipment Co-operative We have audited the

Deeper Dive Leases. Overview

Deeper Dive Leases Presented by: Shaun Johnson, CPA Dingus, Zarecor & Associates PLLC Overview Effective dates Big picture Objective, impact, and implementation Applicability and definition Initial recognition

Deeper Dive Leases Presented by: Shaun Johnson, CPA Dingus, Zarecor & Associates PLLC Overview Effective dates Big picture Objective, impact, and implementation Applicability and definition Initial recognition

EN Official Journal of the European Union L 320/323

29.11.2008 EN Official Journal of the European Union L 320/323 INTERNATIONAL ACCOUNTING STANDARD 40 Investment property OBJECTIVE 1 The objective of this standard is to prescribe the accounting treatment

29.11.2008 EN Official Journal of the European Union L 320/323 INTERNATIONAL ACCOUNTING STANDARD 40 Investment property OBJECTIVE 1 The objective of this standard is to prescribe the accounting treatment

Technical Line FASB final guidance

No. 2016-09 14 April 2016 Technical Line FASB final guidance How the FASB s new leases standard will affect health care entities In this issue: Overview... 1 Key considerations... 3 Scope and scope exceptions...

No. 2016-09 14 April 2016 Technical Line FASB final guidance How the FASB s new leases standard will affect health care entities In this issue: Overview... 1 Key considerations... 3 Scope and scope exceptions...

HABITAT FOR HUMANITY OF GREATER NEW HAVEN, INC. AND SUBSIDIARY Consolidated Financial Statements December 31, 2009

HABITAT FOR HUMANITY OF GREATER NEW HAVEN, INC. AND SUBSIDIARY Consolidated Financial Statements December 31, 2009 HABITAT FOR HUMANITY OF GREATER NEW HAVEN, INC. AND SUBSIDIARY CONSOLIDATED FINANCIAL

HABITAT FOR HUMANITY OF GREATER NEW HAVEN, INC. AND SUBSIDIARY Consolidated Financial Statements December 31, 2009 HABITAT FOR HUMANITY OF GREATER NEW HAVEN, INC. AND SUBSIDIARY CONSOLIDATED FINANCIAL

These notes will be appropriate both for both students who have chosen financial reporting as a depth area as well as those who have not.

When it comes to the Financial Reporting competency, the challenge that many students face is the tremendous amount of technical knowledge included in this competency, especially in light of the fact that

When it comes to the Financial Reporting competency, the challenge that many students face is the tremendous amount of technical knowledge included in this competency, especially in light of the fact that

IFRS Training. IAS 38 Intangible Assets. Professional Advisory Services

IFRS Training IAS 38 Intangible Assets Table of Contents Section 1 Overview 2 Introduction to Intangible Assets 3 Recognition and Initial Measurement 4 Internally Generated Intangible Assets 5 Measurement

IFRS Training IAS 38 Intangible Assets Table of Contents Section 1 Overview 2 Introduction to Intangible Assets 3 Recognition and Initial Measurement 4 Internally Generated Intangible Assets 5 Measurement

Chapter 15 Leases 15-1

Chapter 15 Leases 1. Why Leasing sometimes makes more sense 2. The accounting issues in recording a lease transaction 3. The types of contractual provisions in lease 4. The lease classification: capital

Chapter 15 Leases 1. Why Leasing sometimes makes more sense 2. The accounting issues in recording a lease transaction 3. The types of contractual provisions in lease 4. The lease classification: capital

ACCOUNTING FOR CAPITAL ASSETS. Presented by: Joel Knopp, CPA Shareholder

ACCOUNTING FOR CAPITAL ASSETS Presented by: Joel Knopp, CPA Shareholder Agenda Definition Reporting Capital Assets Questions from Implementation Guides Modified Approach Interest Capitalization Intangibles

ACCOUNTING FOR CAPITAL ASSETS Presented by: Joel Knopp, CPA Shareholder Agenda Definition Reporting Capital Assets Questions from Implementation Guides Modified Approach Interest Capitalization Intangibles

CPE regulations require online participants to take part in online questions

KPMG s CFO Financial Forum Webcast FASB/IASB Revised Lease Accounting Exposure Drafts A Detailed Look Part III: Lessor Accounting June 25, 2013 Administrative CPE regulations require online participants

KPMG s CFO Financial Forum Webcast FASB/IASB Revised Lease Accounting Exposure Drafts A Detailed Look Part III: Lessor Accounting June 25, 2013 Administrative CPE regulations require online participants

International Accounting Standard 17 Leases. Objective. Scope. Definitions IAS 17

International Accounting Standard 17 Leases Objective 1 The objective of this Standard is to prescribe, for lessees and lessors, the appropriate accounting policies and disclosure to apply in relation

International Accounting Standard 17 Leases Objective 1 The objective of this Standard is to prescribe, for lessees and lessors, the appropriate accounting policies and disclosure to apply in relation

Accounting and Auditing. Norman Mosrie, CPA, FMFMA, CHFP James Sutherland, CPA

Accounting and Auditing Norman Mosrie, CPA, FMFMA, CHFP James Sutherland, CPA Leases (ASU 2016-02; Topic 842) A lease contract conveys the right to use an asset (the underlying asset) for a period of time

Accounting and Auditing Norman Mosrie, CPA, FMFMA, CHFP James Sutherland, CPA Leases (ASU 2016-02; Topic 842) A lease contract conveys the right to use an asset (the underlying asset) for a period of time

Applying IFRS for the real estate industry

www.pwc.co.uk Applying IFRS for the real estate industry 12 December 2018 Contents Introduction to applying IFRS for the real estate industry 1 1. Real estate value chain 2 1.1. Overview of the investment

www.pwc.co.uk Applying IFRS for the real estate industry 12 December 2018 Contents Introduction to applying IFRS for the real estate industry 1 1. Real estate value chain 2 1.1. Overview of the investment

Intangible Assets IAS 38, IAS 36, IFRS 3

Intangible Assets IAS 38, IAS 36, IFRS 3 Agenda 1. Introduction 2. Recognition 3. Measurement 4. Impairment of intangible assets (IAS 36) Basic concept Cash-Generating Units 5. Disclosures 2 1 Introduction

Intangible Assets IAS 38, IAS 36, IFRS 3 Agenda 1. Introduction 2. Recognition 3. Measurement 4. Impairment of intangible assets (IAS 36) Basic concept Cash-Generating Units 5. Disclosures 2 1 Introduction

GEORGIA ADVANCED TECHNOLOGY VENTURES, INC. AND SUBSIDIARIES CONSOLIDATED FINANCIAL STATEMENTS YEARS ENDED JUNE 30, 2017 AND 2016

GEORGIA ADVANCED TECHNOLOGY VENTURES, INC. CONSOLIDATED FINANCIAL STATEMENTS YEARS ENDED with INDEPENDENT AUDITORS REPORT TABLE OF CONTENTS PAGE INDEPENDENT AUDITORS REPORT 3-4 CONSOLIDATED STATEMENT OF

GEORGIA ADVANCED TECHNOLOGY VENTURES, INC. CONSOLIDATED FINANCIAL STATEMENTS YEARS ENDED with INDEPENDENT AUDITORS REPORT TABLE OF CONTENTS PAGE INDEPENDENT AUDITORS REPORT 3-4 CONSOLIDATED STATEMENT OF

Sri Lanka Accounting Standard-LKAS 40. Investment Property

Sri Lanka Accounting Standard-LKAS 40 Investment Property CONTENTS SRI LANKA ACCOUNTING STANDARD-LKAS 40 INVESTMENT PROPERTY paragraphs OBJECTIVE 1 SCOPE 2-4 DEFINITIONS 5-15 RECOGNITION 16-19 MEASUREMENT

Sri Lanka Accounting Standard-LKAS 40 Investment Property CONTENTS SRI LANKA ACCOUNTING STANDARD-LKAS 40 INVESTMENT PROPERTY paragraphs OBJECTIVE 1 SCOPE 2-4 DEFINITIONS 5-15 RECOGNITION 16-19 MEASUREMENT

LKAS 17 Sri Lanka Accounting Standard LKAS 17

Sri Lanka Accounting Standard LKAS 17 Leases CONTENTS SRI LANKA ACCOUNTING STANDARD LKAS 17 LEASES paragraphs OBJECTIVE 1 SCOPE 2 DEFINITIONS 4 CLASSIFICATION OF LEASES 7 LEASES IN THE FINANCIAL STATEMENTS

Sri Lanka Accounting Standard LKAS 17 Leases CONTENTS SRI LANKA ACCOUNTING STANDARD LKAS 17 LEASES paragraphs OBJECTIVE 1 SCOPE 2 DEFINITIONS 4 CLASSIFICATION OF LEASES 7 LEASES IN THE FINANCIAL STATEMENTS

SSAP 14 STATEMENT OF STANDARD ACCOUNTING PRACTICE 14 LEASES

SSAP 14 STATEMENT OF STANDARD ACCOUNTING PRACTICE 14 LEASES (Issued October 1987; revised February 2000) The standards, which have been set in bold italic type, should be read in the context of the background

SSAP 14 STATEMENT OF STANDARD ACCOUNTING PRACTICE 14 LEASES (Issued October 1987; revised February 2000) The standards, which have been set in bold italic type, should be read in the context of the background

Test Code F1 Branch (MULTIPLE) (Date : )

(Date : )") FINAL CA May 2018 ACCOUNTING STANDARDS (PART 1) Test Code F1 Branch (MULTIPLE) (Date : 03.12.2017) (50 Marks) compulsory. Note: All questions are Question 1 (5 marks) As per para 10 of AS 2 Valuation of

FINAL CA May 2018 ACCOUNTING STANDARDS (PART 1) Test Code F1 Branch (MULTIPLE) (Date : 03.12.2017) (50 Marks) compulsory. Note: All questions are Question 1 (5 marks) As per para 10 of AS 2 Valuation of

Implementing the New Lease Guidance

Implementing the New Lease Guidance October 22, 2018 2018 Crowe LLP 2018 Crowe LLP Agenda Background Scope Effective dates & transition requirements Lessee accounting model Lessor accounting model Specialized

Implementing the New Lease Guidance October 22, 2018 2018 Crowe LLP 2018 Crowe LLP Agenda Background Scope Effective dates & transition requirements Lessee accounting model Lessor accounting model Specialized

Lease Accounting: Gather your data now and understand tax implications. Tuesday, December 5, 2017

Lease Accounting: Gather your data now and understand tax implications Tuesday, December 5, 2017 Presenters Chris Stephenson Principal, Business Consulting & Technology chris.stephenson@us.gt.com Rebekah

Lease Accounting: Gather your data now and understand tax implications Tuesday, December 5, 2017 Presenters Chris Stephenson Principal, Business Consulting & Technology chris.stephenson@us.gt.com Rebekah

Technical Line FASB final guidance

No. 2016-11 14 April 2016 Technical Line FASB final guidance How the FASB s new leases standard will affect real estate entities In this issue: Overview... 1 Key considerations... 2 Scope and scope exceptions...

No. 2016-11 14 April 2016 Technical Line FASB final guidance How the FASB s new leases standard will affect real estate entities In this issue: Overview... 1 Key considerations... 2 Scope and scope exceptions...

Real Estate Syndication Income 19,451 NOTE

Real Estate Syndication Income 19,451 Section 10,500 Statement of Position 92-1 Accounting for Real Estate Syndication Income February 6, 1992 NOTE Statements of Position of the Accounting Standards Division

Real Estate Syndication Income 19,451 Section 10,500 Statement of Position 92-1 Accounting for Real Estate Syndication Income February 6, 1992 NOTE Statements of Position of the Accounting Standards Division

Before Class starts.(make sure your name is on all submissions)

") Before Class starts.(make sure your name is on all submissions) Fourth Homework due 10/27(MW) or 10/28(TR) before class. No exceptions. Help session 10/26 1:00-3:30pm in GBS130 Fifth Homework due 11/3(MW)

Before Class starts.(make sure your name is on all submissions) Fourth Homework due 10/27(MW) or 10/28(TR) before class. No exceptions. Help session 10/26 1:00-3:30pm in GBS130 Fifth Homework due 11/3(MW)

ASSURANCE AND ACCOUNTING ASPE - IFRS: A Comparison Investment Property

ASSURANCE AND ACCOUNTING ASPE - IFRS: A Comparison Investment Property In this publication we will examine the key differences between Accounting Standards for Private Enterprises (ASPE) and International

ASSURANCE AND ACCOUNTING ASPE - IFRS: A Comparison Investment Property In this publication we will examine the key differences between Accounting Standards for Private Enterprises (ASPE) and International

Chapter 9: Long-Lived Assets and Cost Allocation

1 Chapter 9: Long-Lived Assets and Cost Allocation 2 Capitalize vs Expense Revenue Expenditures Merely maintain a given level of services Should be Expensed Debit Expense Capital Expenditures Provide future

1 Chapter 9: Long-Lived Assets and Cost Allocation 2 Capitalize vs Expense Revenue Expenditures Merely maintain a given level of services Should be Expensed Debit Expense Capital Expenditures Provide future

The Real Estate Donation Process and the Professionals Involved

Donating Real Estate Monday February 9, 2015 Crescendo Charitable gifts of real estate can be a great way for a client to avoid capital gains taxes, generate an income tax deduction and achieve personal

Donating Real Estate Monday February 9, 2015 Crescendo Charitable gifts of real estate can be a great way for a client to avoid capital gains taxes, generate an income tax deduction and achieve personal

IFRS 3 Business Combinations

IFRS 3 Business Combinations 0 Objectives Define a business combination under IFRS 3 (Revised 2008) Describe the steps in applying the acquisition method Explain the recognition and measurement principles

IFRS 3 Business Combinations 0 Objectives Define a business combination under IFRS 3 (Revised 2008) Describe the steps in applying the acquisition method Explain the recognition and measurement principles

Sunrise Stratford, LP

Sunrise Stratford, LP Financial Statements as of and for the Years Ended December 31, 2017 and 2016, Other Financial Information, and Independent Auditors Reports TABLE OF CONTENTS INDEPENDENT AUDITORS

Sunrise Stratford, LP Financial Statements as of and for the Years Ended December 31, 2017 and 2016, Other Financial Information, and Independent Auditors Reports TABLE OF CONTENTS INDEPENDENT AUDITORS

Lease & Finance Accountants Conference. September The Westin Charlotte Charlotte, NC

Lease & Finance Accountants Conference September 11-13 The Westin Charlotte Charlotte, NC H A N D O U T S EQUIPMENT LEASING AND FINANCE ASSOCIATION Transitioning to the ASC 842 Guidance Lessee Requirements

Lease & Finance Accountants Conference September 11-13 The Westin Charlotte Charlotte, NC H A N D O U T S EQUIPMENT LEASING AND FINANCE ASSOCIATION Transitioning to the ASC 842 Guidance Lessee Requirements

Section 12 Accounting for Leases Accounting by the Lessor and Lessee

Section 12 Accounting for Leases Accounting by the Lessor and Lessee 15-1 A lease is an agreement in which the lessor conveys the right to use property, plant, or equipment, usually for a stated period

Section 12 Accounting for Leases Accounting by the Lessor and Lessee 15-1 A lease is an agreement in which the lessor conveys the right to use property, plant, or equipment, usually for a stated period

7/30/2018. Health Care. A CHC-Focused Plan for the New Lease Accounting Standard

Health Care A CHC-Focused Plan for the New Lease Accounting Standard July 31, 2018 1 TO RECEIVE CPE CREDIT Individuals Participate in entire webinar Answer polls when they are provided Groups Group leader

Health Care A CHC-Focused Plan for the New Lease Accounting Standard July 31, 2018 1 TO RECEIVE CPE CREDIT Individuals Participate in entire webinar Answer polls when they are provided Groups Group leader

CONSOLIDATED FINANCIAL STATEMENTS

CONSOLIDATED FINANCIAL STATEMENTS Dundee Real Estate Investment Trust Consolidated Balance Sheets (unaudited) June 30, December 31, (in thousands of dollars) Note 2004 2003 Assets Rental properties 3,4

CONSOLIDATED FINANCIAL STATEMENTS Dundee Real Estate Investment Trust Consolidated Balance Sheets (unaudited) June 30, December 31, (in thousands of dollars) Note 2004 2003 Assets Rental properties 3,4

Center for Plain English Accounting AICPA s National A&A Resource Center available exclusively to PCPS members

Report April 19, 2017 Center for Plain English Accounting AICPA s National A&A Resource Center available exclusively to PCPS members Sale-Leaseback Transactions Involving Real Estate Navigating the Twists

Report April 19, 2017 Center for Plain English Accounting AICPA s National A&A Resource Center available exclusively to PCPS members Sale-Leaseback Transactions Involving Real Estate Navigating the Twists

Lease accounting scope & impacts

Leasing Lease accounting scope & impacts Scope What s in? All industries, all entities Arrangements that meet the definition of a lease Embedded leases within other arrangements What s out? Leases of:

Leasing Lease accounting scope & impacts Scope What s in? All industries, all entities Arrangements that meet the definition of a lease Embedded leases within other arrangements What s out? Leases of:

Accounting and Auditing Update. Staci L. Brogan, CPA, Shareholder Patricia R. Giudici, CPA, Senior Manager Schneider Downs & Co. Inc.

Accounting and Auditing Update Staci L. Brogan, CPA, Shareholder Patricia R. Giudici, CPA, Senior Manager Schneider Downs & Co. Inc. Agenda Overview of the standard setting agenda Revenue recognition Lease

Accounting and Auditing Update Staci L. Brogan, CPA, Shareholder Patricia R. Giudici, CPA, Senior Manager Schneider Downs & Co. Inc. Agenda Overview of the standard setting agenda Revenue recognition Lease

Accounting for Intangible Assets

Accounting for Intangible Assets 1 Examples: Goodwill- internally generated and acquired Trade mark and brand names- internally generated and acquired Patents Copyright Franchise Licenses Customer loyalty

Accounting for Intangible Assets 1 Examples: Goodwill- internally generated and acquired Trade mark and brand names- internally generated and acquired Patents Copyright Franchise Licenses Customer loyalty

International Financial Reporting Standards (IFRS)

") FACT SHEET February 2011 IAS 17 Leases (This fact sheet is based on the standard as at 1 January 2011.) Important note: This fact sheet is based on the requirements of the International Financial Reporting

FACT SHEET February 2011 IAS 17 Leases (This fact sheet is based on the standard as at 1 January 2011.) Important note: This fact sheet is based on the requirements of the International Financial Reporting

NC STATE UNIVERSITY PARTNERSHIP CORPORATION AND AFFILIATES CONSOLIDATED FINANCIAL REPORT. JUNE 30, 2016 and 2015

NC STATE UNIVERSITY PARTNERSHIP CORPORATION AND AFFILIATES CONSOLIDATED FINANCIAL REPORT JUNE 30, 2016 and 2015 NC State University Partnership Corporation and Affiliates Consolidated Financial Statements

NC STATE UNIVERSITY PARTNERSHIP CORPORATION AND AFFILIATES CONSOLIDATED FINANCIAL REPORT JUNE 30, 2016 and 2015 NC State University Partnership Corporation and Affiliates Consolidated Financial Statements

Sri Lanka Accounting Standard-LKAS 17. Leases

Sri Lanka Accounting Standard-LKAS 17 Leases -516- Sri Lanka Accounting Standard-LKAS 17 Leases Sri Lanka Accounting Standard LKAS 17 Leases is set out in paragraphs 1 69. All the paragraphs have equal

Sri Lanka Accounting Standard-LKAS 17 Leases -516- Sri Lanka Accounting Standard-LKAS 17 Leases Sri Lanka Accounting Standard LKAS 17 Leases is set out in paragraphs 1 69. All the paragraphs have equal

GAAP UPDATE DEANA BOWDEN, CPA, MSA WHITE NELSON DIEHL EVANS LLP

GAAP UPDATE DEANA BOWDEN, CPA, MSA WHITE NELSON DIEHL EVANS LLP TOPICS 2016-02 Topic 842 Leases 2016-14 Topic 958 Not for Profits 2016-18 Topic 230 Cash Flows LEASES Current US Generally Accepted Accounting

GAAP UPDATE DEANA BOWDEN, CPA, MSA WHITE NELSON DIEHL EVANS LLP TOPICS 2016-02 Topic 842 Leases 2016-14 Topic 958 Not for Profits 2016-18 Topic 230 Cash Flows LEASES Current US Generally Accepted Accounting

Lease & Finance Accountants Conference. September The Westin Charlotte Charlotte, NC

Lease & Finance Accountants Conference September 11-13 The Westin Charlotte Charlotte, NC H A N D O U T S Basic Principles of Lessors under ASC 842 Mamta Shori, Wells Fargo Equipment Finance Joe Sebik,

Lease & Finance Accountants Conference September 11-13 The Westin Charlotte Charlotte, NC H A N D O U T S Basic Principles of Lessors under ASC 842 Mamta Shori, Wells Fargo Equipment Finance Joe Sebik,

Materiële Vaste Activa. 27 September 2005 Pearl Couvreur

Materiële Vaste Activa 27 September 2005 Pearl Couvreur P w C Contents 1. Principle 2. Acquisition cost 3. Subsequent costs 4. Borrowing costs 5. Assets acquired in a business combination 6. Revaluation

Materiële Vaste Activa 27 September 2005 Pearl Couvreur P w C Contents 1. Principle 2. Acquisition cost 3. Subsequent costs 4. Borrowing costs 5. Assets acquired in a business combination 6. Revaluation

Impact of lease accounting changes to corporate real estate

Impact of lease accounting changes to corporate real estate Overview In February 2016, the Financial Accounting Standards Board (FASB) issued its long-awaited revision to lease accounting Accounting Standards

Impact of lease accounting changes to corporate real estate Overview In February 2016, the Financial Accounting Standards Board (FASB) issued its long-awaited revision to lease accounting Accounting Standards

Copyright 2009 The Learning House, Inc. Fixed and Intangible Assets Page 1 of 13

Copyright 2009 The Learning House, Inc. Fixed and Intangible Assets Page 1 of 13 Introduction This lesson focuses on the long-term assets used to operate a company. These assets can be grouped into fixed

Copyright 2009 The Learning House, Inc. Fixed and Intangible Assets Page 1 of 13 Introduction This lesson focuses on the long-term assets used to operate a company. These assets can be grouped into fixed

EITF ABSTRACTS. [Nullified by FIN 46 and FIN 46(R) for entities within the scope of FIN 46 or FIN 46(R)]

![EITF ABSTRACTS. [Nullified by FIN 46 and FIN 46(R) for entities within the scope of FIN 46 or FIN 46(R)]](/thumbs/83/87695858.jpg "EITF ABSTRACTS. [Nullified by FIN 46 and FIN 46(R) for entities within the scope of FIN 46 or FIN 46(R)]") EITF ABSTRACTS Issue No. 90-15 Title: Impact of Nonsubstantive Lessors, Residual Value Guarantees, and Other Provisions in Leasing Transactions [Nullified by FIN 46 and FIN 46(R) for entities within the

EITF ABSTRACTS Issue No. 90-15 Title: Impact of Nonsubstantive Lessors, Residual Value Guarantees, and Other Provisions in Leasing Transactions [Nullified by FIN 46 and FIN 46(R) for entities within the

IAS 16 Property, Plant and Equipment. Uphold public interest

IAS 16 Property, Plant and Equipment Uphold public interest Background IAS 16 became operational in 1983 Major amendments have been made several times including 1998, 2003, 2008, 2012, 2013, 2014 The objective

IAS 16 Property, Plant and Equipment Uphold public interest Background IAS 16 became operational in 1983 Major amendments have been made several times including 1998, 2003, 2008, 2012, 2013, 2014 The objective

The New Lease Accounting Standard. Hunter Mink, CPA, CCIFP Brian Rosenberg, CPA, MBA

The New Lease Accounting Standard Hunter Mink, CPA, CCIFP Brian Rosenberg, CPA, MBA 1 Agenda Introduction Lease Identification and Classification Lessee Accounting Other Considerations Disclosures Impact

The New Lease Accounting Standard Hunter Mink, CPA, CCIFP Brian Rosenberg, CPA, MBA 1 Agenda Introduction Lease Identification and Classification Lessee Accounting Other Considerations Disclosures Impact

GASB 87: Leases. Hosted By: Ben Lindekugel, Executive Director Association of Washington Public Hospital Districts

GASB 87: Leases Hosted By: Ben Lindekugel, Executive Director Association of Washington Public Hospital Districts November 6, 2018 Presented By Tom Dingus, CPA, Partner Dingus, Zarecor & Associates PLLC

GASB 87: Leases Hosted By: Ben Lindekugel, Executive Director Association of Washington Public Hospital Districts November 6, 2018 Presented By Tom Dingus, CPA, Partner Dingus, Zarecor & Associates PLLC

Financial Statements January 31, 2016 and February 1, 2015 PetSmart Charities of Canada

Financial Statements January 31, 2016 and February 1, 2015 PetSmart Charities of Canada www.eidebailly.com Table of Contents Independent Auditor s Report... 1 Financial Statements... Error! Bookmark not

Financial Statements January 31, 2016 and February 1, 2015 PetSmart Charities of Canada www.eidebailly.com Table of Contents Independent Auditor s Report... 1 Financial Statements... Error! Bookmark not

CP:

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 10-1 10-2 PREVIEW OF CHAPTER 10 10-3

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 10-1 10-2 PREVIEW OF CHAPTER 10 10-3

NEW LEASE ACCOUNTING STANDARD

NEW LEASE ACCOUNTING STANDARD Accounting Standards Update (ASU) 2016-02, Leases & GASB 87, Leases LEASES Leases: Why a New Leases Standard? 1 IMPLEMENTATION TIMELINE January 2016 IASB issued IFRS 16, Leases

NEW LEASE ACCOUNTING STANDARD Accounting Standards Update (ASU) 2016-02, Leases & GASB 87, Leases LEASES Leases: Why a New Leases Standard? 1 IMPLEMENTATION TIMELINE January 2016 IASB issued IFRS 16, Leases

SOLUTIONS Learning Goal 19

S1 Learning Goal 19 Multiple Choice 1. b 2. a 3. c 4. b However, the double-declining-balance method calculates the depreciation expense on the full asset cost until the final year of use. 5. d Total appraised

S1 Learning Goal 19 Multiple Choice 1. b 2. a 3. c 4. b However, the double-declining-balance method calculates the depreciation expense on the full asset cost until the final year of use. 5. d Total appraised

EUROPEAN UNION ACCOUNTING RULE 7 PROPERTY, PLANT & EQUIPMENT

EUROPEAN UNION ACCOUNTING RULE 7 PROPERTY, PLANT & EQUIPMENT Page 2 of 10 I N D E X 1. Objective... 3 2. Scope... 3 3. Definitions... 3 4. Recognition... 4 4.1 General recognition principle... 4 4.2 Initial

EUROPEAN UNION ACCOUNTING RULE 7 PROPERTY, PLANT & EQUIPMENT Page 2 of 10 I N D E X 1. Objective... 3 2. Scope... 3 3. Definitions... 3 4. Recognition... 4 4.1 General recognition principle... 4 4.2 Initial

Impairment or disposal of longlived

Financial reporting developments A comprehensive guide Impairment or disposal of longlived assets Revised December 2017 To our clients and other friends ASC 360-10, Impairment and Disposal of Long-Lived

Financial reporting developments A comprehensive guide Impairment or disposal of longlived assets Revised December 2017 To our clients and other friends ASC 360-10, Impairment and Disposal of Long-Lived

IFRS 15 and IFRS 16 Webinar

CPA Ireland Skillnet CPA Ireland Skillnet, is a training network that is funded by Skillnets, a state funded, enterprise led support body dedicated to the promotion and facilitation of training and up-skilling

CPA Ireland Skillnet CPA Ireland Skillnet, is a training network that is funded by Skillnets, a state funded, enterprise led support body dedicated to the promotion and facilitation of training and up-skilling

CC HOLDINGS GS V LLC INDEX TO FINANCIAL STATEMENTS. Consolidated Financial Statements Years Ended December 31, 2011, 2010 and 2009

INDEX TO FINANCIAL STATEMENTS Consolidated Financial Statements Years Ended December 31, 2011, 2010 and 2009 Report of PricewaterhouseCoopers LLP, Independent Auditors...................................

INDEX TO FINANCIAL STATEMENTS Consolidated Financial Statements Years Ended December 31, 2011, 2010 and 2009 Report of PricewaterhouseCoopers LLP, Independent Auditors...................................

New leases standard ASC 842 Lessee - operating leases. Itai Gotlieb, Partner, Professional Practice July 2017

ASC 842 Lessee - operating leases Itai Gotlieb, Partner, Professional Practice July 2017 Overview Under Accounting Standards Codification (ASC) 842, Leases, lessees recognize assets and liabilities for

ASC 842 Lessee - operating leases Itai Gotlieb, Partner, Professional Practice July 2017 Overview Under Accounting Standards Codification (ASC) 842, Leases, lessees recognize assets and liabilities for

In December 2003 the Board issued a revised IAS 40 as part of its initial agenda of technical projects.

IAS 40 Investment Property In April 2001 the International Accounting Standards Board (the Board) adopted IAS 40 Investment Property, which had originally been issued by the International Accounting Standards

IAS 40 Investment Property In April 2001 the International Accounting Standards Board (the Board) adopted IAS 40 Investment Property, which had originally been issued by the International Accounting Standards

This version includes amendments resulting from IFRSs issued up to 31 December 2009.

International Accounting Standard 40 Investment Property This version includes amendments resulting from IFRSs issued up to 31 December 2009. IAS 40 Investment Property was issued by the International

International Accounting Standard 40 Investment Property This version includes amendments resulting from IFRSs issued up to 31 December 2009. IAS 40 Investment Property was issued by the International

Real estate project costs

Financial reporting developments A comprehensive guide Real estate project costs Revised June 2017 To our clients and other friends The guidance for real estate project costs is contained within ASC 970,

Financial reporting developments A comprehensive guide Real estate project costs Revised June 2017 To our clients and other friends The guidance for real estate project costs is contained within ASC 970,

Chapter 08 - Long-Term Assets. Chapter Outline

Section 1 Plant Assets I. Cost Determination Plant assets are tangible assets used in a company's operations that have a useful life of more than one accounting period. Consistent with cost principle,

Section 1 Plant Assets I. Cost Determination Plant assets are tangible assets used in a company's operations that have a useful life of more than one accounting period. Consistent with cost principle,

Applying IFRS for the real estate industry

www.pwc.co.uk Applying IFRS for the real estate industry November 2017 Contents Introduction to applying IFRS for the real estate industry 1 1. Real estate value chain 2 1.1. Overview of the investment

www.pwc.co.uk Applying IFRS for the real estate industry November 2017 Contents Introduction to applying IFRS for the real estate industry 1 1. Real estate value chain 2 1.1. Overview of the investment

Before Class starts.(make sure your name is on all submissions)

") Before Class starts.(make sure your name is on all submissions) March 27 exam conflicts must be resolved before Spring break. Fourth Homework due Thursday 3/6 before class. Fifth Homework due 3/20 before

Before Class starts.(make sure your name is on all submissions) March 27 exam conflicts must be resolved before Spring break. Fourth Homework due Thursday 3/6 before class. Fifth Homework due 3/20 before

University of Missouri System Accounting Policies and Procedures

University of Missouri System Accounting Policies and Procedures Policy Number: APM-20.05.10 Policy Name: Capital Assets Buildings and Improvements General Policy and Procedure Overview: This policy provides

University of Missouri System Accounting Policies and Procedures Policy Number: APM-20.05.10 Policy Name: Capital Assets Buildings and Improvements General Policy and Procedure Overview: This policy provides

HABITAT FOR HUMANITY OF SAN FERNANDO / SANTA CLARITA VALLEYS, INC. FINANCIAL STATEMENTS FOR THE YEAR ENDED DECEMBER 31, 2015

ENG: 1375T01/2015/II/2110 4/27/2016 9:20 AM Draft #1.4 Final Sent April 27, 2016 HABITAT FOR HUMANITY OF SAN FERNANDO / SANTA CLARITA VALLEYS, INC. FINANCIAL STATEMENTS FOR THE YEAR ENDED FINANCIAL STATEMENTS

ENG: 1375T01/2015/II/2110 4/27/2016 9:20 AM Draft #1.4 Final Sent April 27, 2016 HABITAT FOR HUMANITY OF SAN FERNANDO / SANTA CLARITA VALLEYS, INC. FINANCIAL STATEMENTS FOR THE YEAR ENDED FINANCIAL STATEMENTS

CENTRAL GOVERNMENT ACCOUNTING STANDARDS

CENTRAL GOVERNMENT ACCOUNTING STANDARDS NOVEMBER 2016 STANDARD 4 Requirements STANDARD 5 INTANGIBLE ASSETS INTRODUCTION... 75 I. CENTRAL GOVERNMENT S SPECIALISED ASSETS... 75 I.1. The collection of sovereign

CENTRAL GOVERNMENT ACCOUNTING STANDARDS NOVEMBER 2016 STANDARD 4 Requirements STANDARD 5 INTANGIBLE ASSETS INTRODUCTION... 75 I. CENTRAL GOVERNMENT S SPECIALISED ASSETS... 75 I.1. The collection of sovereign

4/4/2018. GASB's New Leases Standard

GASB's New Leases Standard April 4, 2018 1 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing this webinar in a group Complete group attendance form

GASB's New Leases Standard April 4, 2018 1 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing this webinar in a group Complete group attendance form

TAX ISSUES FOR REAL ESTATE LEASING BY TAX-EXEMPT ORGANIZATIONS Part One: Residential and Commercial Leases

TAX ISSUES FOR REAL ESTATE LEASING BY TAX-EXEMPT ORGANIZATIONS Part One: Residential and Commercial Leases Written by: Michael J. Huft mhuft@schiffhardin.com 312.258.5627 Nina M. Knierim nknierim@schiffhardin.com

TAX ISSUES FOR REAL ESTATE LEASING BY TAX-EXEMPT ORGANIZATIONS Part One: Residential and Commercial Leases Written by: Michael J. Huft mhuft@schiffhardin.com 312.258.5627 Nina M. Knierim nknierim@schiffhardin.com

White Paper Estate Freeze Technique: Installment Sales

White Paper Estate Freeze Technique: Installment Sales www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA,

White Paper Estate Freeze Technique: Installment Sales www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA,

Teresa Gordon s Recommended Alternative to Accounting for Leases

Teresa Gordon s Recommended Alternative to Accounting for Leases Key features: Leases with title transfer and bargain purchase options would not be excluded from the scope. Leases with title transfer or

Teresa Gordon s Recommended Alternative to Accounting for Leases Key features: Leases with title transfer and bargain purchase options would not be excluded from the scope. Leases with title transfer or